2014 CONSUMER HEALTH SENTIMENTS REPORT - Nielsen

16

2014 CONSUMER HEALTH SENTIMENTS REPORT A CLOSER LOOK AT THE UNINSURED CONSUMER

Transcript of 2014 CONSUMER HEALTH SENTIMENTS REPORT - Nielsen

12014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

2014 CONSUMER HEALTH SENTIMENTS REPORTA CLOSER LOOK AT THE UNINSURED CONSUMER

2 2014 CONSUMER HEALTH SENTIMENTS REPORT

2014 CONSUMER HEALTH SENTIMENTS REPORTA CLOSER LOOK AT THE UNINSURED CONSUMER

Despite continued political debate, it seems that the Affordable Care

Act (ACA), signed into law by President Obama in 2010, is here to stay.

While the law means different things to the different entities involved

in the health care industry, one thing is certain—things will never be

the same. Many primary care physicians, taxed with too many patients

due to decreasing numbers of generalist physicians, have been forced

to consolidate into larger health systems. Health insurers, no longer

allowed to underwrite the individual market and ordered by law to spend

$0.80 for every dollar earned, specifically on health services, also are

feeling the impact on business-as-usual. Then there are those who are

feeling the greatest influence from the ACA—the consumers.

Designed to help aid those unable to provide health insurance coverage

for themselves and/or their families, the ACA appears to be working

with an estimated 9 to 10 million newly insured consumers entering

the system in 2014, according to several recent studies. Yet, this is just

the beginning. The trend is expected to continue into 2015 enrollment

with Centers for Medicare/Medicaid Services (CMS) estimates of

6.2% projected growth from 2015 to 20221. These numbers can be

extremely attractive to health insurers who see opportunity to bulk up

their membership. However, it may not be ideal to cast a broad net to

capture the uninsured seeking coverage for the first time (or first time in

several years)—it must be a refined process that stems from building a

foundational understanding of this consumer.

1Centers for Medicare & Medicaid Services. “National Health Expenditure Projections 2012-2022.” Accessed 8/5/14: http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/downloads/proj2012.pdf

32014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

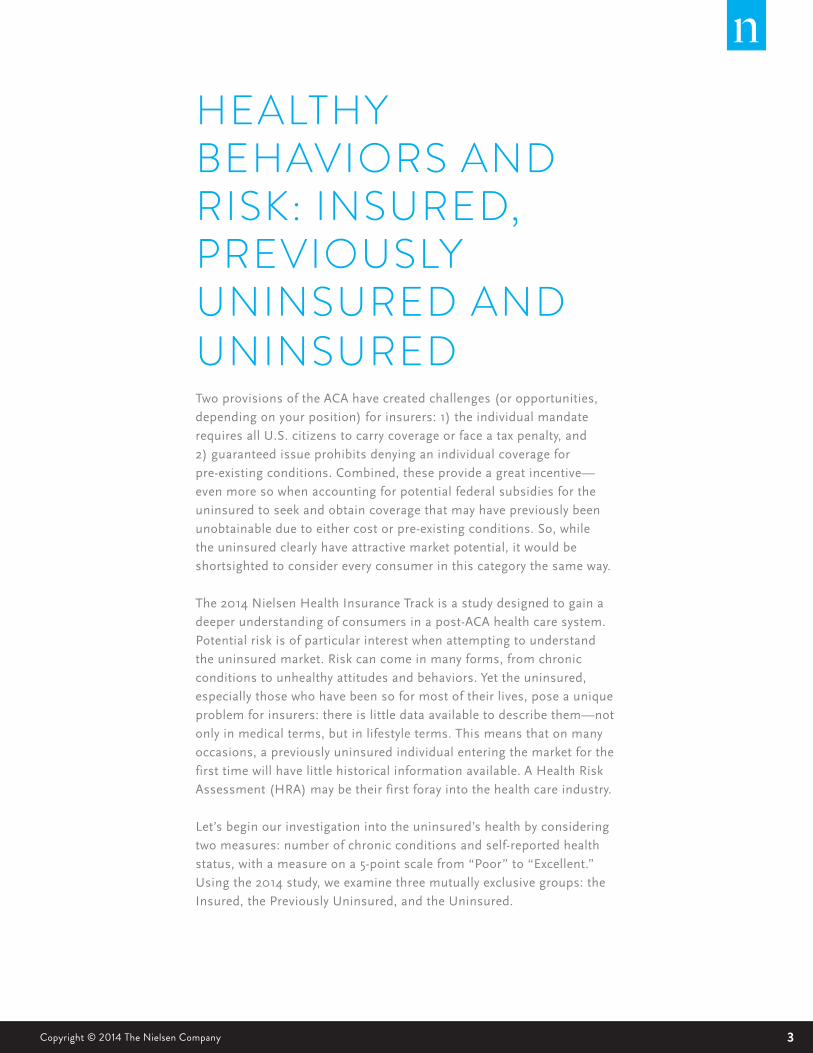

HEALTHY BEHAVIORS AND RISK: INSURED, PREVIOUSLY UNINSURED AND UNINSURED Two provisions of the ACA have created challenges (or opportunities,

depending on your position) for insurers: 1) the individual mandate

requires all U.S. citizens to carry coverage or face a tax penalty, and

2) guaranteed issue prohibits denying an individual coverage for

pre-existing conditions. Combined, these provide a great incentive—

even more so when accounting for potential federal subsidies for the

uninsured to seek and obtain coverage that may have previously been

unobtainable due to either cost or pre-existing conditions. So, while

the uninsured clearly have attractive market potential, it would be

shortsighted to consider every consumer in this category the same way.

The 2014 Nielsen Health Insurance Track is a study designed to gain a

deeper understanding of consumers in a post-ACA health care system.

Potential risk is of particular interest when attempting to understand

the uninsured market. Risk can come in many forms, from chronic

conditions to unhealthy attitudes and behaviors. Yet the uninsured,

especially those who have been so for most of their lives, pose a unique

problem for insurers: there is little data available to describe them—not

only in medical terms, but in lifestyle terms. This means that on many

occasions, a previously uninsured individual entering the market for the

first time will have little historical information available. A Health Risk

Assessment (HRA) may be their first foray into the health care industry.

Let’s begin our investigation into the uninsured’s health by considering

two measures: number of chronic conditions and self-reported health

status, with a measure on a 5-point scale from “Poor” to “Excellent.”

Using the 2014 study, we examine three mutually exclusive groups: the

Insured, the Previously Uninsured, and the Uninsured.

4 2014 CONSUMER HEALTH SENTIMENTS REPORT

From an initial review, it appears (as we would hope) that there is a

negative relationship between the mean number of chronic conditions

one reports and health status. However, when considering the

Uninsured, it seems that they tend to report slightly fewer conditions

across health status than their Insured counterparts. Although the

difference is typically marginal, the pattern occurs across all levels of the

health status measure. This may indicate that the Uninsured are actually

healthier than the insured in terms of having few potentially debilitating/

costly diseases, or that the Uninsured are not necessarily healthier and

are undiagnosed without having an outlet to medical care.

INTERACTION AMONG HEALTH STATUS, INSURANCE STATUS AND CHRONIC CONDITIONS

UNINSURED

POOR GOODFAIR VERY GOOD EXCELLENT

# O

F C

HR

ON

IC C

ON

DIT

ION

S

(MEA

N)*

SELF-REPORTED HEALTH STATUS

INSURANCE STATUS

INSURED PREVIOUSLY UNINSURED

6

4

2

0

*Outliers >17 chronic conditions indicated, removed

Source: Nielsen Health Insurance Track 2014

52014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

UNINSURED

POOR GOODFAIR VERY GOOD EXCELLENT

# O

F PH

YSIC

AL

AC

TIV

ITIE

S PE

R W

EEK

(M

EAN

)*

INSURANCE STATUS

INSURED PREVIOUSLY UNINSURED

3

2

1

0

* Outliers >6 weekly activities indicated, removed

Source: Nielsen Health Insurance Track 2014

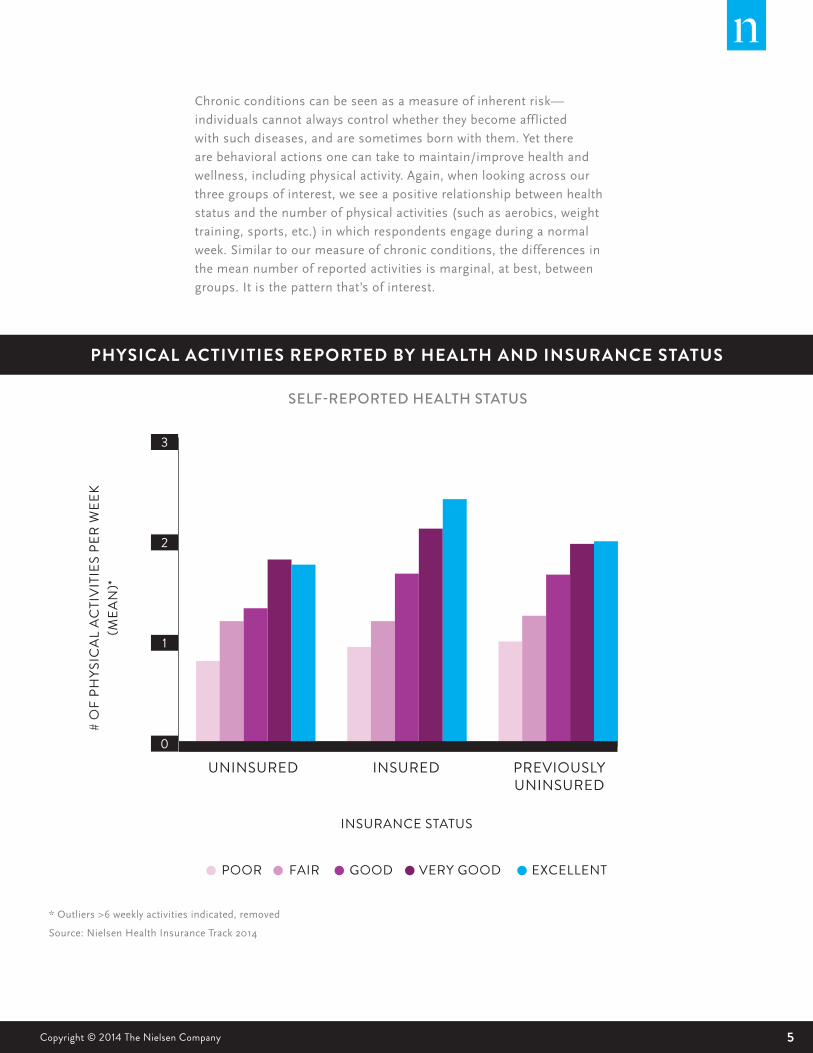

Chronic conditions can be seen as a measure of inherent risk—

individuals cannot always control whether they become afflicted

with such diseases, and are sometimes born with them. Yet there

are behavioral actions one can take to maintain/improve health and

wellness, including physical activity. Again, when looking across our

three groups of interest, we see a positive relationship between health

status and the number of physical activities (such as aerobics, weight

training, sports, etc.) in which respondents engage during a normal

week. Similar to our measure of chronic conditions, the differences in

the mean number of reported activities is marginal, at best, between

groups. It is the pattern that’s of interest.

PHYSICAL ACTIVITIES REPORTED BY HEALTH AND INSURANCE STATUS

SELF-REPORTED HEALTH STATUS

6 2014 CONSUMER HEALTH SENTIMENTS REPORT

PREVALENCE OF TOBACCO USE BY INSURANCE STATUS

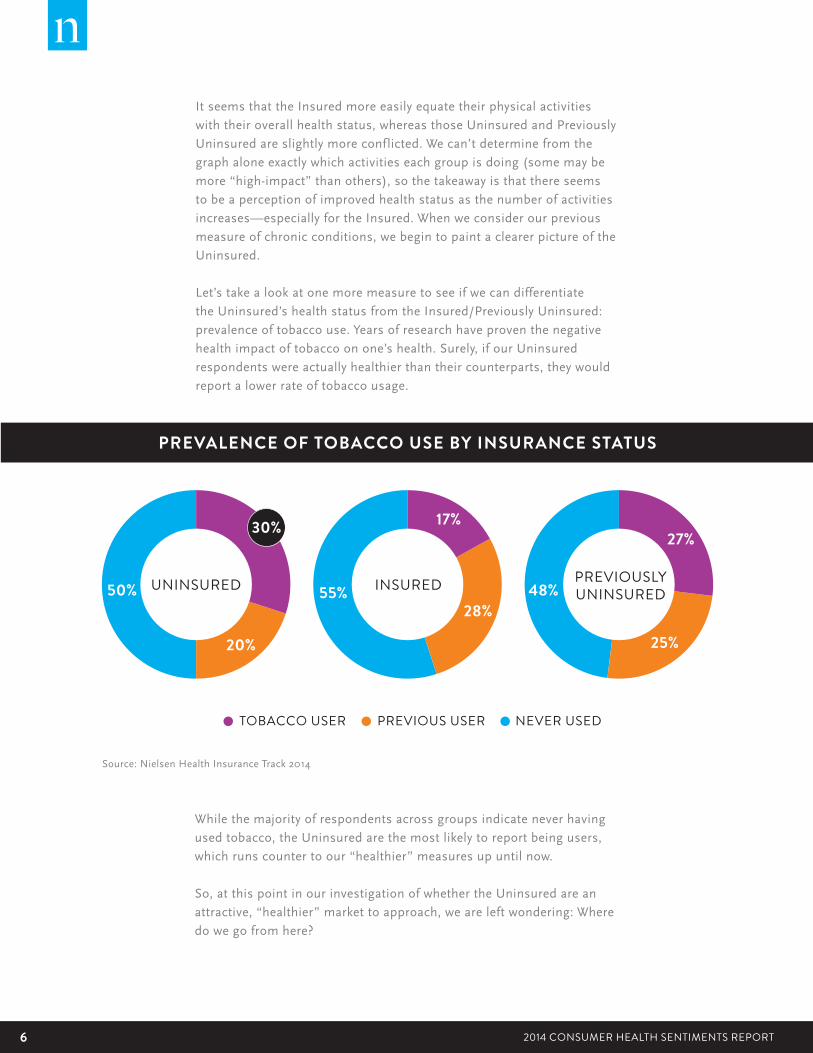

It seems that the Insured more easily equate their physical activities

with their overall health status, whereas those Uninsured and Previously

Uninsured are slightly more conflicted. We can’t determine from the

graph alone exactly which activities each group is doing (some may be

more “high-impact” than others), so the takeaway is that there seems

to be a perception of improved health status as the number of activities

increases—especially for the Insured. When we consider our previous

measure of chronic conditions, we begin to paint a clearer picture of the

Uninsured.

Let’s take a look at one more measure to see if we can differentiate

the Uninsured’s health status from the Insured/Previously Uninsured:

prevalence of tobacco use. Years of research have proven the negative

health impact of tobacco on one’s health. Surely, if our Uninsured

respondents were actually healthier than their counterparts, they would

report a lower rate of tobacco usage.

Source: Nielsen Health Insurance Track 2014

TOBACCO USER NEVER USEDPREVIOUS USER

While the majority of respondents across groups indicate never having

used tobacco, the Uninsured are the most likely to report being users,

which runs counter to our “healthier” measures up until now.

So, at this point in our investigation of whether the Uninsured are an

attractive, “healthier” market to approach, we are left wondering: Where

do we go from here?

UNINSURED INSURED PREVIOUSLY UNINSURED50% 55% 48%

17%27%

20% 25%

28%

30%

72014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

PREVALENCE OF TOBACCO USE BY INSURANCE STATUS

D I G G I N G D E E P E R F O R A M O R E C O M P L E T E V I E WLet’s take a step back. Granted, our example above uses only three

data points (chronic conditions, healthy activities and tobacco use)

coming from a single research study. A savvy researcher’s appetite for

knowing more about the Uninsured would not be sated. Because no

single study will provide all the answers, many researchers will find the

need to combine sources for a better understanding of these groups.

The Nielsen Health Insurance Track can provide far more behavioral

insights—thousands more—and it links to Nielsen PRIZM segmentation

for a more extensive view of consumers.

Nielsen’s PRIZM® segmentation model classifies every U.S. household

into one of 66 segments based on household lifestyle behaviors, media

and purchasing preferences. From this, a wealth of information is

available as PRIZM is linked to thousands of Nielsen and third-party data

assets. This allows a much broader picture of the consumer outside of a

single survey’s data—everything from what they watch to what they buy.

You can think of the Nielsen Health Insurance Track as a starting point

to a much more robust collection of insightful information around any

specific group of interest to your business.

In this particular situation, we would like to know more about the

Uninsured. Let’s start by finding out which PRIZM segments include the

highest proportions of this group within the Nielsen Health Insurance

Track. Although PRIZM is composed of 66 segments, these segments

can be rolled up into cohesive groups based on their “Lifestage” (a

combination of measures based on age, affluence, and presence of

children within a household) and their “Social Group” (a combination

of affluence and urbanization—a proprietary Nielsen measure

accounting for population density surrounding a household).

8 2014 CONSUMER HEALTH SENTIMENTS REPORT

YOUNGER YEARS

SUBURBANURBAN

MIDLIFE SUCCESS

4.5%

ELITE SUBURBS

0.6%

URBAN UPTOWN

3.4%

YOUNG ACHIEVERS

11.2%

THE AFFLUENTIALS

2.6%

MIDTOWNMIX8.2%

STRIVING SINGLES

24.4%

MIDDLEBURBS5.4%

INNER SUBURBS

10.2%

URBAN CORES

11.4%

FAMILY LIFE

SECOND CITY

ACCUMULATED WEALTH

0.5%

SECOND CITY SOCIETY

1.4%

YOUNG ACCUMULATORS

3.7%

CITY CENTERS

5.6%

MAINSTREAM FAMILIES

12.7%

MICRO-CITY BLUES16.8%

SUSTAINING FAMILIES

16.1%

MATURE YEARS

TOWN AND COUNTRY

AFFLUENT EMPTY NESTS

1.1%

LANDED GENTRY

1.3%

CONSERVATIVE CLASSICS

1.6%

COUNTRY COMFORT

3.3%

CAUTIOUS COUPLES

6.7%

MIDDLE AMERICA

7.6%

SUSTAINING SENIORS

16.4%

RUSTIC LIVING

21.2%

$$$

$$$

$

$

UNINSURED PROPORTIONS BY PRIZM LIFESTAGE AND SOCIAL GROUP

Source: Nielsen PRIZM 2014

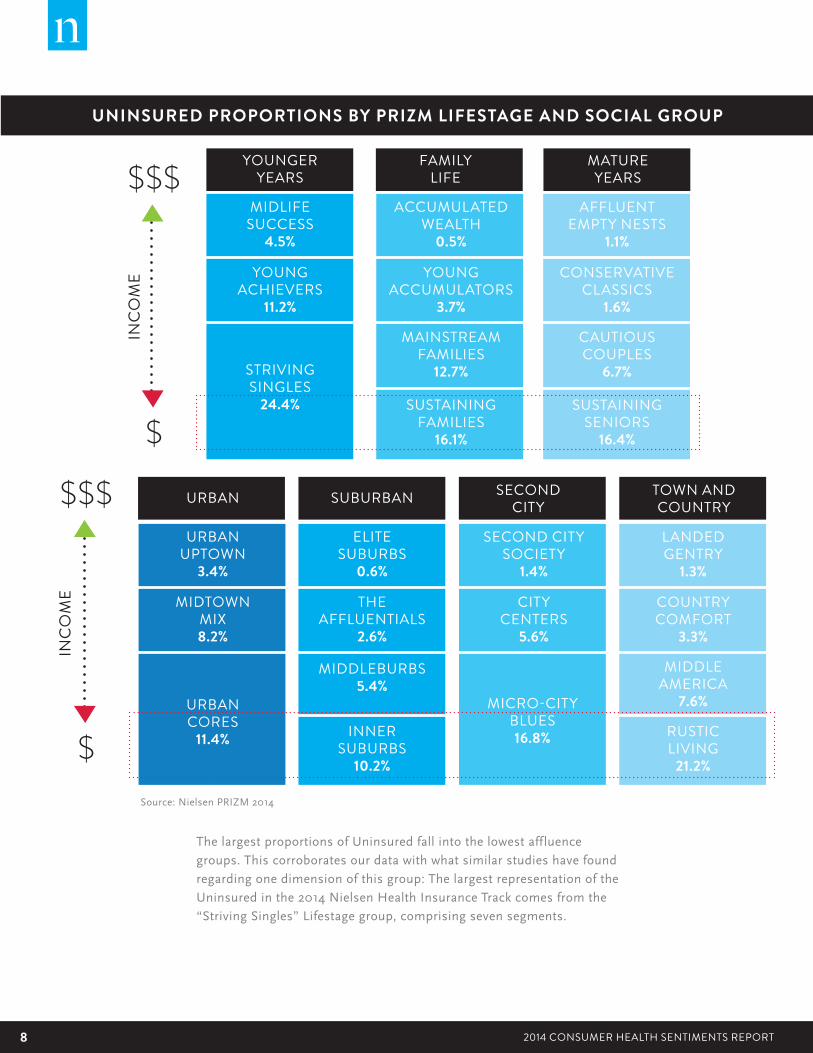

The largest proportions of Uninsured fall into the lowest affluence

groups. This corroborates our data with what similar studies have found

regarding one dimension of this group: The largest representation of the

Uninsured in the 2014 Nielsen Health Insurance Track comes from the

“Striving Singles” Lifestage group, comprising seven segments.

INC

OM

E

INC

OM

E

92014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

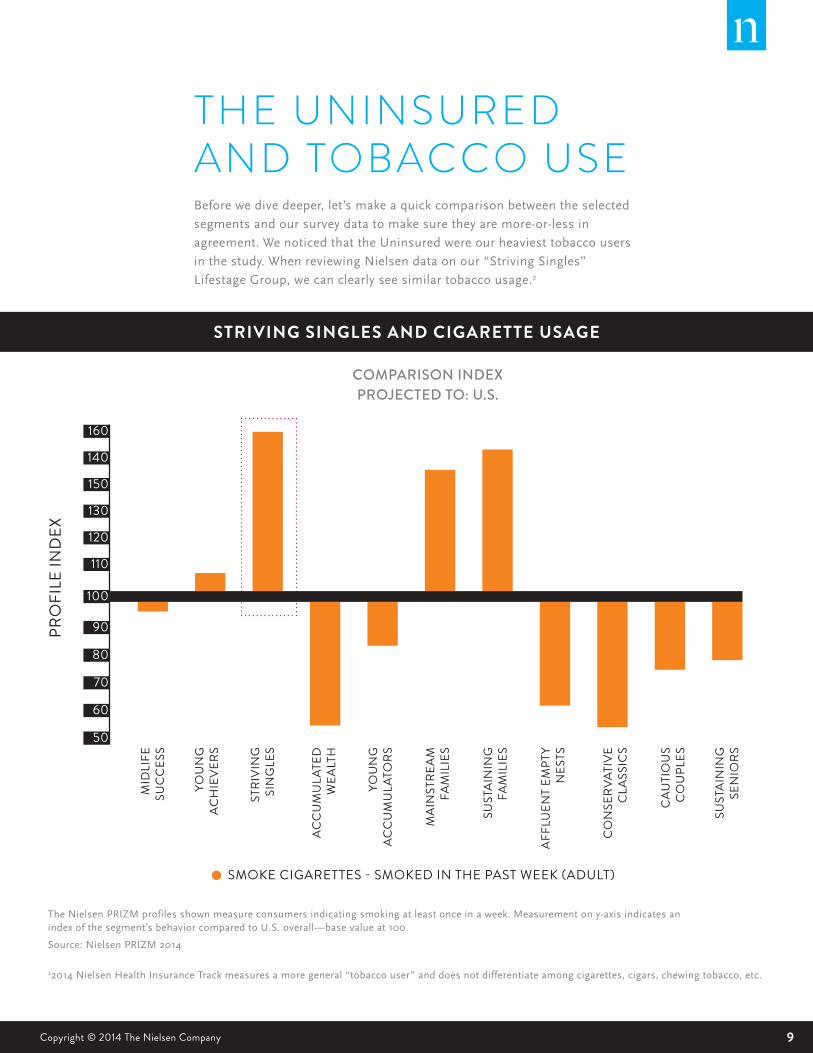

THE UNINSURED AND TOBACCO USEBefore we dive deeper, let’s make a quick comparison between the selected

segments and our survey data to make sure they are more-or-less in

agreement. We noticed that the Uninsured were our heaviest tobacco users

in the study. When reviewing Nielsen data on our “Striving Singles”

Lifestage Group, we can clearly see similar tobacco usage.2

STRIVING SINGLES AND CIGARETTE USAGE

MID

LIFE

SU

CC

ESS

YOU

NG

ACH

IEVE

RS

YOU

NG

ACC

UM

ULA

TORS

MAI

NST

REAM

FAM

ILIE

S

SUST

AIN

ING

FAM

ILIE

S

AFFL

UEN

T EM

PTY

NES

TS

CO

NSE

RVAT

IVE

CLA

SSIC

S

CAU

TIO

US

CO

UPL

ES

SUST

AIN

ING

SEN

IORS

STRI

VIN

GSI

NG

LES

ACC

UM

ULA

TED

WEA

LTH

PRO

FILE

IND

EX

SMOKE CIGARETTES - SMOKED IN THE PAST WEEK (ADULT)

The Nielsen PRIZM profiles shown measure consumers indicating smoking at least once in a week. Measurement on y-axis indicates an index of the segment’s behavior compared to U.S. overall—base value at 100.

Source: Nielsen PRIZM 2014

22014 Nielsen Health Insurance Track measures a more general “tobacco user” and does not differentiate among cigarettes, cigars, chewing tobacco, etc.

COMPARISON INDEX PROJECTED TO: U.S.

160

150

140

130

120

110

100

90

80

70

60

50

10 2014 CONSUMER HEALTH SENTIMENTS REPORT

MID

LIFE

SU

CC

ESS

YOU

NG

ACH

IEVE

RS

YOU

NG

ACC

UM

ULA

TORS

MAI

NST

REAM

FAM

ILIE

S

SUST

AIN

ING

FAM

ILIE

S

AFFL

UEN

T EM

PTY

NES

TS

CO

NSE

RVAT

IVE

CLA

SSIC

S

CAU

TIO

US

CO

UPL

ES

SUST

AIN

ING

SEN

IORS

STRI

VIN

GSI

NG

LES

ACC

UM

ULA

TED

WEA

LTH

STRIVING SINGLES, CIGARETTE USE AND SMOKING CESSATION

The Nielsen PRIZM profiles shown measure consumers indicating smoking at least once in a week. Measurement on y-axis indicates an index of the segment’s behavior compared to U.S. overall—base value at 100.

Source: Nielsen PRIZM 2014

PRO

FILE

IND

EX

SMOKE CIGARETTES - IN THE LAST WEEK (ADULT)USED SMOKING CESSATION AID - IN THE LAST YEAR (ADULT)

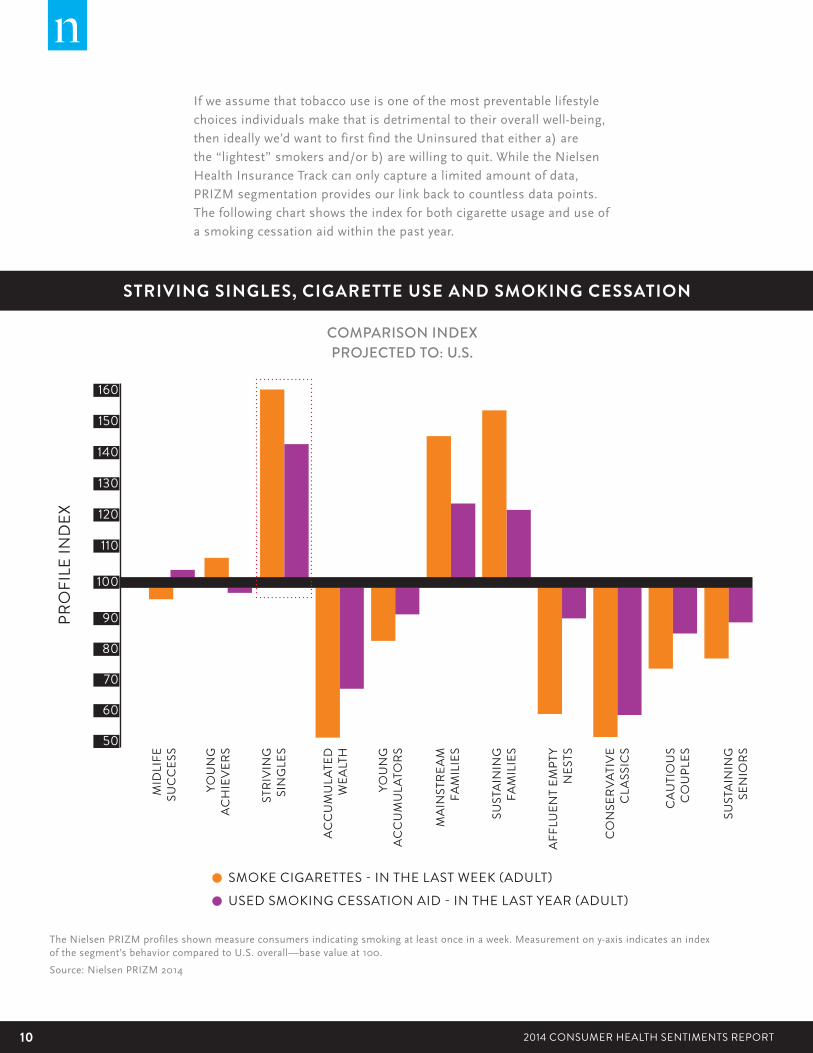

If we assume that tobacco use is one of the most preventable lifestyle

choices individuals make that is detrimental to their overall well-being,

then ideally we’d want to first find the Uninsured that either a) are

the “lightest” smokers and/or b) are willing to quit. While the Nielsen

Health Insurance Track can only capture a limited amount of data,

PRIZM segmentation provides our link back to countless data points.

The following chart shows the index for both cigarette usage and use of

a smoking cessation aid within the past year.

COMPARISON INDEXPROJECTED TO: U.S.

160

150

140

130

120

110

100

90

80

70

60

50

112014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

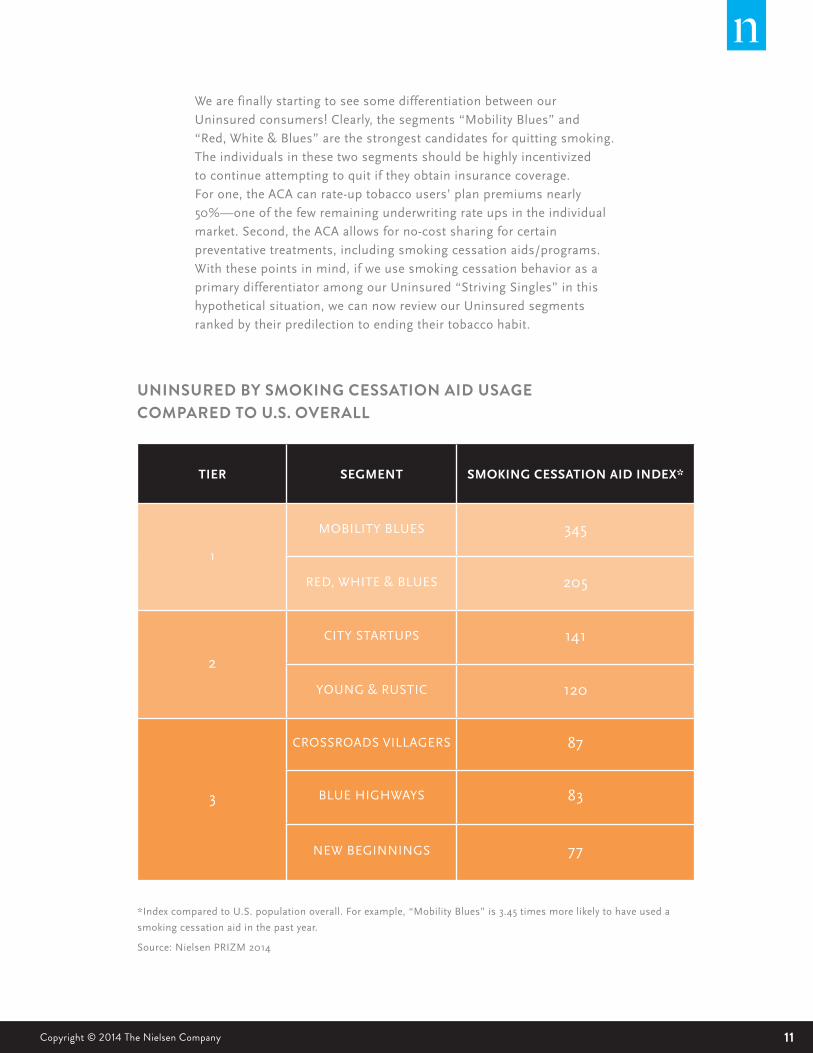

*Index compared to U.S. population overall. For example, “Mobility Blues” is 3.45 times more likely to have used a

smoking cessation aid in the past year.

Source: Nielsen PRIZM 2014

We are finally starting to see some differentiation between our

Uninsured consumers! Clearly, the segments “Mobility Blues” and

“Red, White & Blues” are the strongest candidates for quitting smoking.

The individuals in these two segments should be highly incentivized

to continue attempting to quit if they obtain insurance coverage.

For one, the ACA can rate-up tobacco users’ plan premiums nearly

50%—one of the few remaining underwriting rate ups in the individual

market. Second, the ACA allows for no-cost sharing for certain

preventative treatments, including smoking cessation aids/programs.

With these points in mind, if we use smoking cessation behavior as a

primary differentiator among our Uninsured “Striving Singles” in this

hypothetical situation, we can now review our Uninsured segments

ranked by their predilection to ending their tobacco habit.

TIER SEGMENT SMOKING CESSATION AID INDEX*

1

MOBILITY BLUES 345

RED, WHITE & BLUES 205

2

CITY STARTUPS 141

YOUNG & RUSTIC 120

3

CROSSROADS VILLAGERS 87

BLUE HIGHWAYS 83

NEW BEGINNINGS 77

UNINSURED BY SMOKING CESSATION AID USAGE COMPARED TO U.S. OVERALL

12 2014 CONSUMER HEALTH SENTIMENTS REPORT

U N D E R S TA N D I N G T H E B E H AV I O R S O F C O N S U M E R S E G M E N T SBy using the power of Nielsen’s PRIZM segmentation model, we can

expose numerous behaviors exhibited by our segment tiers of interest.

When we simply examine how these segments index on specific

behaviors relative to the U.S. population overall, a clearer picture forms.

Here is a set of example health and wellness behaviors by tier and index:

132014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

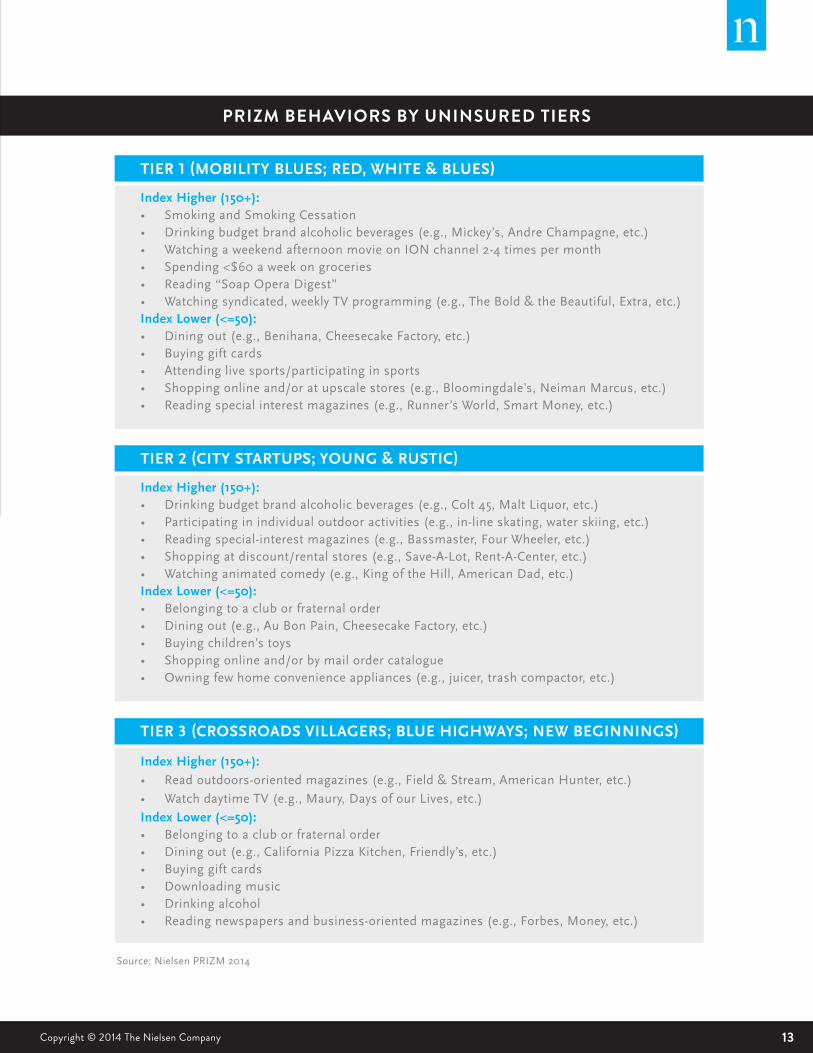

PRIZM BEHAVIORS BY UNINSURED TIERS

TIER 1 (MOBILITY BLUES; RED, WHITE & BLUES)

Index Higher (150+):• Smoking and Smoking Cessation• Drinking budget brand alcoholic beverages (e.g., Mickey’s, Andre Champagne, etc.)• Watching a weekend afternoon movie on ION channel 2-4 times per month• Spending <$60 a week on groceries• Reading “Soap Opera Digest”• Watching syndicated, weekly TV programming (e.g., The Bold & the Beautiful, Extra, etc.)Index Lower (<=50):• Dining out (e.g., Benihana, Cheesecake Factory, etc.)• Buying gift cards• Attending live sports/participating in sports• Shopping online and/or at upscale stores (e.g., Bloomingdale’s, Neiman Marcus, etc.)• Reading special interest magazines (e.g., Runner’s World, Smart Money, etc.)

TIER 2 (CITY STARTUPS; YOUNG & RUSTIC)

Index Higher (150+):• Drinking budget brand alcoholic beverages (e.g., Colt 45, Malt Liquor, etc.)• Participating in individual outdoor activities (e.g., in-line skating, water skiing, etc.)• Reading special-interest magazines (e.g., Bassmaster, Four Wheeler, etc.)• Shopping at discount/rental stores (e.g., Save-A-Lot, Rent-A-Center, etc.)• Watching animated comedy (e.g., King of the Hill, American Dad, etc.)Index Lower (<=50):• Belonging to a club or fraternal order• Dining out (e.g., Au Bon Pain, Cheesecake Factory, etc.)• Buying children’s toys• Shopping online and/or by mail order catalogue• Owning few home convenience appliances (e.g., juicer, trash compactor, etc.)

TIER 3 (CROSSROADS VILLAGERS; BLUE HIGHWAYS; NEW BEGINNINGS)

Index Higher (150+):• Read outdoors-oriented magazines (e.g., Field & Stream, American Hunter, etc.)

• Watch daytime TV (e.g., Maury, Days of our Lives, etc.)

Index Lower (<=50):• Belonging to a club or fraternal order• Dining out (e.g., California Pizza Kitchen, Friendly’s, etc.)• Buying gift cards• Downloading music• Drinking alcohol• Reading newspapers and business-oriented magazines (e.g., Forbes, Money, etc.)

Source: Nielsen PRIZM 2014

14 2014 CONSUMER HEALTH SENTIMENTS REPORT

Both similarities and differences exist among our three tiers, and

while these behaviors are just examples, they illustrate the level of

detail available to describe PRIZM segments. Take for example Tier 1:

“Watching a weekend afternoon movie on ION channel 2-4 times per

month”—the minutiae captured by PRIZM can be quite profound. Not

only does PRIZM aid in our quest to understand the health status of

the Uninsured, but it also provides information that can be used for

marketing purposes—often new territory for health insurers traditionally

marketing to groups/employers.

S E G M E N TAT I O N B R I N G S F O C U S TO YO U R M A R K E T I N G E F F O R T SAlthough our example is simply illustrative and the particular needs

of a company will vary, PRIZM presents a unique way of looking at the

consumer from a 360-degree perspective. Starting from segmentation

(to understand the consumer), Nielsen further provides the ability to

find consumers geographically. For example, our “Mobility Blues” and

“Red, White & Blues” segments are heavily concentrated in southwest

Oregon and most of Colorado. Building on that foundation, we can

determine the optimal methods for engaging these consumers according

to client strategy and tactics.

The Uninsured will continue to be of interest within the health care

industry as more and more seek coverage. With Nielsen’s PRIZM

segmentation in your tool box, the opportunity to focus marketing efforts

on key segments becomes a reality.

METHODOLOGY

Nielsen Health Insurance Track is a survey conducted biennially,

collecting consumer-level data on behaviors related to health insurance

coverage, purchase process, and health behaviors/risk. Approximately

25,000 respondents, sampled to be nationally representative, participate.

For more information please contact your Nielsen representative.

152014 CONSUMER HEALTH SENTIMENTS REPORT Copyright © 2014 The Nielsen Company

ABOUT NIELSEN Nielsen N.V. (NYSE: NLSN) is a global information and measurement

company with leading market positions in marketing and consumer

information, television and other media measurement, online

intelligence and mobile measurement. Nielsen has a presence in

approximately 100 countries, with headquarters in New York, USA

and Diemen, the Netherlands.

For more information, visit www.nielsen.com.

Copyright © 2014 The Nielsen Company. All rights reserved. Nielsen and

the Nielsen logo are trademarks or registered trademarks of CZT/ACN

Trademarks, L.L.C. Other product and service names are trademarks or

registered trademarks of their respective companies. 14/8214

16 2014 CONSUMER HEALTH SENTIMENTS REPORT