2013 Results Presentation - Astra International | Beranda laporan keuangan/AI... · Strong results...

34

PT Astra International Tbk 2013 Results Presentation

Transcript of 2013 Results Presentation - Astra International | Beranda laporan keuangan/AI... · Strong results...

PT Astra International Tbk2013 Results Presentation

This report has been prepared by PT Astra International Tbk independently and is circulated for thepurpose of general information only. It is not intended for the specific person who may receive this report.The information in this report has been obtained from sources which we deem reliable. No warranty(expressed or implied) is made as to the accuracy or completeness of the information. All opinions andestimations included in this report constitute our judgment as of this date and are subject to changewithout prior notice.

We disclaim any responsibility or liability whatsoever arising which may be brought or suffered by anyperson as a result of acting in reliance upon the whole or any part of the contents of this report andneither PT Astra International Tbk and/or its affiliated companies and/or their respective employeesand/or agents accepts liability for any errors, omissions, negligent or otherwise, in this report and anyinaccuracy herein or omission here from which might otherwise arise.

Cautionary note on forward-looking statements: This report may contain statements regarding thebusiness of PT Astra International Tbk and its subsidiaries that are of a forward-looking nature and aretherefore based on management's assumptions about future developments. Forward-looking statementsinvolve certain risks and uncertainties because they relate to future events. Actual results may varymaterially from those targeted, expected or projected due to several factors. Potential risks anduncertainties includes such factors as general economic conditions, foreign exchange fluctuations, interestrate changes, commodity price fluctuations and regulatory developments. The reader and/or listener iscautioned to not unduly rely on these forward-looking statements. We do not undertake any duty topublish any update or revision of any forward-looking statements.

Disclaimer

2

Indonesia economic growth slowed moderately to 5.78% in2013 (2012: 6.23%), driven by slowdown in investment whileconsumption remained strong

Strong results from the Group’s financial services and miningcontracting businesses were offset by a decline in earnings fromthe Group’s heavy equipment and palm oil businesses.

While automotive demand remained favourable, increasedcompetition coupled with higher labour costs led to the earningscontribution from the car sector being little changed.

Overview

Highlights

3

Period ended 31st December

2013 2012 Change

Net Revenue (Rp bn) 193,880 188,053 3%

Net Income (Rp bn)* 19,417 19,421 0%

Net earnings per share (Rp) 480 480 0%

As at 31st

December 2013As at 31st

December 2012Change

Shareholders’ Funds (Rp bn)** 83,938 71,201 18%

Net asset value per share (Rp)** 2,073 1,759 18%

* Net income is profit attributable to owners of the parent. ** Shareholders' funds and Net asset value per share are based on equity attributable to owners of the parent.

• Indonesia economic growth slowed moderately to 5.78% in 2013 (2012: 6.23%),driven by slowdown in investment while consumption remained strong

• Strong results from the Group’s financial services and mining contractingbusinesses were offset by a decline in earnings from the Group’s heavyequipment and palm oil businesses.

• While automotive demand remained favourable, increased competition coupledwith higher labour costs led to the earnings contribution from the car sectorbeing little changed.

Business structure

4

Automotive

Automobile

•Toyota•Daihatsu• Isuzu•BMW•Peugeot•UD Trucks

Motorcycle

Honda

Component

Astra Otoparts

Others

Astraworld

Financial Services

•Astra Credit Companies

•Toyota Astra Finance

Motorcycle

Federal Intl. Finance

Heavy Equipment

Banking

•SAN Finance•Komatsu Astra

Finance

Bank Permata

Insurance

Asuransi Astra Buana

Heavy Equipment & Mining

Construction Machinery

•United Tractors•Traktor

Nusantara

Mining Contractor

PAMA PersadaNusantara

Coal Mining

•PMM• TTA• ABP• BEE• ABB / ABJ• DS / DN• PJU

Agribusiness

Palm Oil

Astra Agro Lestari

Infrastructure& Logistics

Toll Road

•MMS : 72km•MTN : 11km•MHI : 41km

Water Utility

Palyja

Fuel Logistic

Gresik Terminal

InformationTechnology

Document Solution

Astra Graphia

IT Solution

Astra GraphiaInformation Technology

Logistics

•SERA / TRAC•Mobil 88 (used)•SELOG•TFLI

Automobile

Sea Port

Eastkal

• Astra’s car market share declined from 54% to 53%, while Astra’s motorcycle market share increased from 58% to 61%.

• Komatsu’s market share was 41% and maintained it’s leading market position despite tight competition and weaker demand for heavy equipment due to lower commodity prices.

Market position at 31 December 2013

5

Toyota35%

Daihatsu15%

Isuzu3%

Mitsubishi13%

Suzuki13%

Nissan5%

Honda7%

Others9%

Car

Source : Gaikindo

Honda61%

Yamaha32%

Suzuki5%

Kawasaki2%

Motorcycle

Source : AISI

Komatsu 41%

Caterpillar 19%

Hitachi 21%

Kobelco17%

Others2%

Source: United Tractors – Internal Market Research

Heavy Equipment

Corporate actions

6

March ‘13

Jan ‘13• Astratel acquired 100% share of PT Pelabuhan Penajam Banua

Taka (Eastkal Seaport) in Balikpapan, East Kalimantan for Rp442 billion, to provide an integrated logistic hub for Astra group.

• Pama Persada completed final payment of USD 80m to increase its ownership to 75.40% in Asmin Bara Bronang/Jaan coal mines.

May ‘13 • AOP completed right issue of Rp 3.0 trillion, with AI participation of Rp 2.9 trillion.

April ‘13• AOP acquired 51% share of PT Pakoakuina (Pako), a wheel rim

manufacturer, for Rp 700 billion.

May ‘13 • AI placed 15.7% of AOP shares at a price of Rp 3,750 per share to increase the liquidity of the stock, generating Rp 2.8 trillion in gross proceeds.

Corporate actions

7

Aug ‘13 • AAL established a joint venture in Singapore (Astra – KLK Pte. Ltd), to market its palm oil products. AAL holds a 49% stake and Malaysian partner KL-Kepong Plantation Holdings owns 51%.

Sep ‘13 • Astra commercially launched the Low Cost Green Cars Astra-Toyota Agya and the Astra-Daihatsu Ayla.

Dec ‘13

Oct ‘13 • AI announced agreements to develop 2.4 hectares of land for an office tower and residential apartment complex in central Jakarta.

• Bank Permata completed a Rp 2.2 trillion senior and subordinated debt issuance.

Jan ‘14 • Bank Permata completed a Rp 1.5 trillion rights issue.

• JV Agreement signed with Aviva plc to form Astra Aviva Life.

Financial Performance

Consolidated income statement

9

In Billion Rupiah 2013 2012 Change

USD / IDR, average 10,563 9,419 12%

Revenue 193,880 188,053 3%

Gross Profit 35,311 36,200 (2%)

Operating Expenses (16,708) (16,330) 2%

Other Income 2,623 2,352 12%

Equity Income 6,297 5,676 11%

Income Tax Expense (5,226) (5,156) 1%

Non-controlling interest (2,880) (3,321) (13%)

Net Income 19,417 19,421 0%

“The Group produced satisfactory results in 2013, particularly as a number of ourbusinesses faced challenging conditions. The outlook for 2014 remains sound, although itis expected that there will continue to be heightened competition in the car market andweakness in coal prices, while concerns remain about increases in interest rates andrupiah volatility.”

- Prijono Sugiarto, President Director

Ownership %

Share of NI %

2013 2012

Auto Non-Auto Auto Non-Auto

4W AutomotiveSO – Toyota, Daihatsu, IsuzuToyota Astra MotorAstra Daihatsu MotorIsuzu Astra Motor Indonesia

100513245

31 30

2W AutomotiveAstra Honda MotorHonda SO

50100

15 14

ComponentAstra Otoparts 80 5 5

Financial ServicesAstra Sedaya FinanceFederal International FinanceToyota Astra Financial ServicesKomatsu Astra FinanceSAN FinanceAsuransi Astra BuanaPermata Bank

1001005050609645

17 5 15 4

Heavy Equipment & MiningUnited TractorsPamapersada Nusantara

6060

15 18

AgribusinessAstra Agro Lestari 80 7 10

Infrastructure, Logistics, ITSERAPalyjaMarga MandalasaktiAstra Graphia

100497977

5 4

10

2001 2011 2012 2013

Auto (Incl. autorelated Financial Services)

89% 61% 64% 68%

Non-Auto 11% 39% 36% 32%

Astra portfolio as at 31 December 2013

Net income contribution Auto vs. Non-Auto segments:

• Astra’s net asset value of Rp 2,073 per share at 31st December 2013 was 18% higher than at the end of 2012.

• Net debt at 31st December 2013, exclusive of the Group’s financial services subsidiaries, was Rp 3.7 trillion, mainly due to the sell down of 15.7% stake in Astra Otoparts and a reduction in working capital in the Group’s heavy equipment businesses.

Consolidated balance sheet

11

In Billion Rupiah 31-Dec-13 31-Dec-12 Change

Cash and Cash Equivalents 18,557 11,055 68%

Trade Receivables 19,843 16,443 21%

Inventories 14,433 15,285 (6%)

Financing Receivables 54,677 48,631 12%

Investments in Associates and Jointly Controlled Entities 23,870 19,801 21%

Fixed Assets 37,862 34,326 10%

Other Assets 44,752 36,733 22%

Total Assets 213,994 182,274 17%

Short-term Borrowings 12,854 7,202 78%

Trade Payables 17,275 12,685 36%

Long-term Debt 51,669 49,555 4%

Other Liabilities 26,008 23,018 13%

Total Liabilities 107,806 92,460 17%

Equity Attributable to The Owners of The Parent 83,938 71,201 18%

Non – controlling Interest 22,250 18,613 20%

Total Equity 106,188 89,814 18%

Net Debt (45,966) (45,702) 1%

Net Debt (Excl. Financial Services) (3,687) (8,918) (59%)

Consolidated cash flow

12

In Billion Rupiah 2013 2012 Change

Cash from operations 26,690 13,943 12,747

Tax Payments (6,382) (5,688) (694)

Interest received 942 675 267

Dividends Received 3,336 4,064 (728)

Cash flow from Operating Activities + Dividends Received 24,586 12,994 11,592

Net Capex (9,998) (10,576) 578

Net Investment (1,321) (2,534) 1,213

Other Investing (323) (391) 68

Cash flow for Investing Activities (11,642) (13,501) 1,859

Net proceed of Debt 2,080 9,163 (7,083)

Interest Payment (1,105) (990) (115)

Dividend Payment (10,017) (9,768) (249)

Other Financing 2,377 (332) 2,709

Cash flow from Financing Activities (6,665) (1,927) (4,738)

Increase/(Decrease) in Cash 6,279 (2,434) 8,713

Opening Cash Balance 10,815 13,071 (2,256)

Exchange Rate Adjustment 1,461 178 1,283

Closing Cash Balance 18,555* 10,815* 7,740

The Group’s cash balance at 31 December 2013 increased by Rp 7.7 trillion, mainly driven by stronger working capital inflows.

* Inclusive of bank overdraft

Business Updates

136 147 218 259 175 223318 281

426 483605 655

182 207266

275

144211

290205

338411

511575

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Astra OthersLehman Crisis

(↓20%)

Segment 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Sedan 8% 11% 8% 7% 6% 6% 6% 5% 4% 3% 3% 3%

4x2 & 4x4 55% 53% 56% 62% 63% 66% 64% 69% 67% 64% 67% 69%

Commercial 37% 36% 36% 31% 31% 28% 30% 26% 29% 33% 30% 28%

Historical domestic car sales

In thousand unitsFuel price increase

(↓40%)

The wholesale market for cars grew by 10% in 2013, benefitting from rising incomes and increased domestic capacity

14

318

1,116

894

764

486

608

434319

534484

354

Source: Gaikindo

1,230

Astra 605,19154.2%

Astra 654,55853.2%

Others 511,03945.8%

Others575,34346.8%

4x2 & 4x479.4%

4x2 & 4x480.4%

Commercial17.4%

Commercial 16.6%

Toyota36.4%

Toyota35.4%

Daihatsu14.6%

Daihatsu 15.1%

Isuzu 3.0%Isuzu 2.6%

Mitsubishi13.3%

Mitsubishi12.8%

Suzuki 11.3%

Suzuki 13.3% Honda 6.2%

Honda 7.4%Nissan 6.0%

Nissan 5.0% Others 9.2%

Others 8.4%

Sedan 3.1% Sedan 2.8%

4x2 & 4x4746,37366.9%

4x2 & 4x4845,54168.7%

Commercial335,135 30.0%

Commercial349,61628.4 %

Sedan 56.6% Sedan 43.1%

4x2 & 4x464.4%

4x2 & 4x462.3%

Commercial 31.4%

Commercial31.1%

M/S2012

AI Product Segment

Brand Segment AI Product M/S

M/S2013

AI Product Segment

Brand Segment AI Product M/S

Sedan 3.%

Source: Gaikindo

Automotive – car & wholesale market

15

2012 2013

Astra’s car sales rose by 8%, leading to a decline in market share from 54% to 53%

1,229,901

Sedan 3.0%

1,116,230

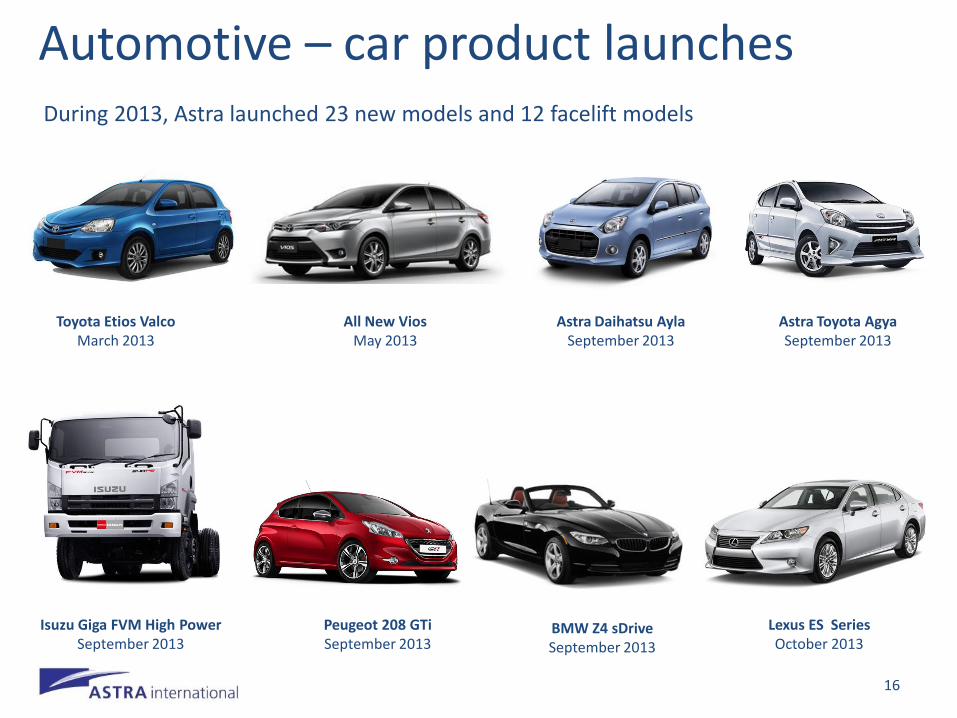

Automotive – car product launchesDuring 2013, Astra launched 23 new models and 12 facelift models

Astra Daihatsu AylaSeptember 2013

16

Astra Toyota AgyaSeptember 2013

Toyota Etios ValcoMarch 2013

Lexus ES SeriesOctober 2013

All New ViosMay 2013

Isuzu Giga FVM High PowerSeptember 2013

Peugeot 208 GTiSeptember 2013

BMW Z4 sDriveSeptember 2013

1,437 1,577 2,036 2,648 2,340 2,141 2,875 2,701

3,416 4,274 4,089 4,697

850 1,233

1,852

2,426 2,087 2,547

3,341 3,151

3,957 3,739

2,975 3,047

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Astra Others

In thousand units

Segment 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Cub 90% 90% 89% 88% 84% 73% 63% 52% 45% 38% 26% 19%

Scooter 0% 0% 2% 4% 8% 18% 26% 39% 46% 52% 60% 63%

Sport 10% 10% 9% 8% 8% 9% 11% 9% 9% 11% 14% 18%

Historical domestic motorcycle sales• The wholesale market for motorcycles grew by 10% in 2013 to 7.7 million• Shifting consumer demand from cub to automatic scooter type, and improved

contribution from sport type

17

2,287

4,6884,4275,074

3,888

2,810

7,373

5,8526,216

8,013

7,064Fuel price increase

(↓13%)

Lehman Crisis( ↓6%)

Min. DP requirement

Source: AISI

7,744

Honda, 4,088,888

57.9%

Honda, 4,696,999

60.7%

Yamaha,2,423,854

34.3%

Yamaha, 2,492,596

32.2%

Suzuki, 5.9%

Suzuki, 5.1%Others 1.9%

Others 2.0%

Cub1,058,281

25.9%

Cub874,75718.6%

Scooter2,859,989

69.9%

Scooter3,425,075

72.9%

Sport/Others4.2%

Sport/Others8.5%

Cub1,058,281

57.1%

Cub874,75758.5%

Scooter2,859,989

68%

Scooter3,425,075

70%

Sport/Others17.0 %

Sport/Others29.3%

Cub1,852,792

26.2%

Cub1,495,209

19.3%

Scooter4,208,219

59.6%

Scooter4,893,647

63.2%

Sport & Others 14.2%

Sport & Others 17.5%

Brand2012

Honda Segment Honda Product M/S

Segment Brand2013

Honda Segment Honda Product M/S

Segment

Automotive – motorcycle & wholesale market

Source: AISI

2012 2013

Astra Honda Motor’s sales increased by 15%, with it’s market share increasing from 58% to 61%

18

7,064,457 7,743,879

Automotive – motorcycle product launches

19

During 2013, Astra Honda Motor launched 2 new models and 9 revamped models

Honda CBR 150 ROctober 2013

Honda CB 150 RDecember 2013

Honda Verza January 2013

Honda Scoopy FIFebruary 2013

Honda Vario 125 CBS Idling Stop March 2013

Supra X 125 Helm-In FIJuly 2013

OEM68%

After Market

23%

Export9%

268401

785605

Equity Income Consolidated

51%51%

41%

39%8%

10%

Export After Market OEM

Automotive - components

20

Net Income (IDR billion)

Astra Otoparts, the Group’s 80%-owned automotive components business, reported net income of Rp 1 trillion, a decrease of 4%. The decline in earnings was largely due to higher raw material and labour costs that could not be passed on fully to customers.

1,0531,006

Revenue (IDR billion)

8,277

29%

(4%)

2012 2013 2012 2013

10,702

OEM56%

After Market

37%

Export7%

Amount Financed (Rp bio) 2013 2012 %

Auto

ACC (Incl.HE) 26,141 23,165 13

TAFS 9,368 8,255 13

Total 4W 35,510 31,420 13

FIF 21,419 18,877 13

Total Auto 56,929 50,297 13

HE

SANF 3,277 4,610 (29)

KAF 1,722 2,486 (31)

Total HE 4,999 7,096 (30)

Financial services

21

• 2013 consolidated net income increased by

26% to Rp 1.7 trillion

• Loan book grew by 26% to Rp 120 trillion

• LDR 89% & CAR 14%

• Gross-NPL ratio were down from 1.4% to

1.0%

Asuransi Astra Buana

• 2013 Gross Written Premium up by 23%year on year to Rp 3.8 trillion

• RBC : 157%, requirement 120%

Bank Permata

Net income from the Group’s financial services businesses grew by 15% to Rp 4.3 trillion, driven by loan book growth in the automotive focused finance companies and Bank Permata

Unit Financed 2013 2012 %

Auto

ACC (new & used cars) 192,364 164,605 17

TAFS 61,640 54,777 13

Total 4W 254,004 219,382 16

FIF (Incl.Electronics) 2,609,925 2,295,915 14

HE

SANF 2,655 3,715 (29)

KAF 341 377 (10)

Total HE 2,996 4,092 (27)

* Incl. Joint Financing

Historical heavy equipment market

825 916 1,619 2,406 2,250 3,454 4,345

3,111 5,404

8,467 6,202

4,203 868 1,331

2,3452,587 2,437

3,584

5,339

3,533

6,377

8,893

8,219

6,049

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Others Komatsu

1,693 2,247

3,9644,993 4,687

7,038

9,684

6,644

11,781

17,360

14,421

Market Share 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Komatsu 49% 41% 41% 48% 48% 49% 45% 47% 46% 49% 43% 41%

Caterpillar 26% 34% 29% 28% 23% 22% 23% 21% 16% 18% 19% 19%

Hitachi 16% 13% 16% 13% 16% 16% 17% 17% 19% 15% 21% 21%

Others 9% 11% 14% 11% 13% 13% 15% 15% 19% 18% 17% 19%

22

Weaker heavy equipment market in 2013 driven by a decline in mining sector demand due to a fall in commodity prices.

In Unit

Source: UT’s internal research

10,252

94.4 105.1

Coal Production (mn tonnes)

855.5 844.9

Overburden Removal (mn bcm)

2,779 1,629

2,848

2,554

5,627

4,183

PMM & Asmin TTA & DN (all in thousand tonnes)

22,15815,644

27,99431,554

5,8023,814

Construction Machinery Mining Contracting Mining

54%43%

5%

8%

25%

26%

16%

23%

Mining Forestry Agro Construction

United Tractors, 59.5%-owned, reported net income down 16% to Rp 4.8 trillion, due to lower heavy equipment sales, partly offset by strong results from Pama, its mining contracting business.

Mining Contracting

Coal Mines: Reserves and SalesKomatsu Unit Sales

4,203

Revenue (Rp bio)

2012 2013 2012 2013

Heavy equipment & mining

23

6,202Est. Combined Coal Reserves (Mio Tons)

TTA 30

PMM 3

ABP 9

ABB/ABJ 100

DS/DN 45

BEE 177

PJU 45

Total 409

55,954

2012 2013 2012 2013

51,012

14.1 16.1 17.3

19.4 21.0 22.1 24.3

26.9 28.3

2005 2006 2007 2008 2009 2010 2011 2012 2013

In million tonnes

Historical national palm oil production

24

Palm Oil Area 2005 2006 2007 2008 2009 2010 2011 2012 2013F

Mature (Million hectare)

3.69 4.11 4.54 4.95 5.37 5.74 6.08 6.50 6.90

Yields (T/Ha) 3.82 3.91 3.80 3.92 3.91 3.85 4.00 4.14 4.10

• Indonesia is the world largest palm oil producer

• Demand for CPO remains strong, largely driven by emerging markets

Source : Oil World

5.23 4.63

234 247

39 37

Immature

Mature

11,231

12,558 333

117

Export

Local

Area Maturity (‘K Ha) *

Revenue (Rp bio)

CPO Production & Sales (‘K tonnes)

284273

Astra Agro Lestari, 79.7%-owned, reported net income of Rp 1.8 trillion, a decline of 25%, due to declining nucleus FFB yield, higher labour costs and foreign exchange translation loss on US dollar borrowings, despite increased CPO sales by 11%.

* Incl. plasma plantation

CPO Yield (tonne/Ha)

Agribusiness

25

11,564

12,675

1,476 1,5391,424 1,577

Production Sales

2012 2013 2012 2013

2012 2013 2012 2013

159.8 158.5

31,339 30,956

Infrastructure, logistics and others

26

• Marga Mandalasakti, the Tangerang – Merak72.5km toll road operator, reported a 9% increase in traffic volumes to 41 million vehicles

• PAM Lyonnaise Jaya, which operates the western Jakarta water utility system, experienced lower sales volume by 1% to 159million cubic metres

• Serasi Autoraya’s revenue improved, despite lower number of vehicles under contract at its TRAC car rental business by 1% to 31,000

TRAC Rental Car (unit)

37,482 40,760

MMS Vehicle Traffic Volume (‘K unit) Palyja Water Sales Volume (Mn m3)

2012 2013

2012 20132012 2013

Appendices

Divisional Revenue

Divisional revenue and net income

28

In Billion Rupiah 2013 2012 % Chg

Automotive 108,039 99,639 8%

Financial Services 13,615 12,712 7%

Heavy Equipment 50,920 55,800 (9%)

Agribusiness 12,675 11,564 10%

Infrastructure, Logistics & Others 6,585 6,489 1%

Information Technology 2,046 1,849 11%

Total 193,880 188,053 3%

Divisional Net Income

In Billion Rupiah 2013 2012 % Chg

Automotive 9,829 9,472 4%

Financial Services 4,273 3,714 15%

Heavy Equipment 2,971 3,500 (15%)

Agribusiness 1,435 1,920 (25%)

Infrastructure, Logistics & Others 748 683 10%

Information Technology 161 132 22%

Total 19,417 19,421 0%

Car products launched in 2013

29

Models Launched Launching Time Engine Capacity Prices (IDR mn)

Car

Lexus LS 460 L Jan-13 4,600cc 2,300

Lexus LS 600 HL Jan-13 5,000cc 2,900

BMW X1 sDrive18i Business Jan-13 2,000cc 499*

BMW X1 sDrive18i xLine Jan-13 2,000cc 559*

BMW X1 sDrive20d Sport Jan-13 2,000cc 649*

Isuzu NQR 71 Feb-13 125ps 287.5

BMW M 135i Feb-13 3,000cc 888*

Toyota Etios Valco Mar-13 1,200cc 139.5-169.5

Toyota New Avanza Airbag May-13 1,300cc-1,500cc 155.5-193

Toyota All New Vios May-13 1,500cc 242.5-272.5

Daihatsu New Xenia Airbag May-13 1,000cc-1,300cc 133.1-185.8

Peugeot New RCZ May-13 1,600cc 689.1*

Isuzu Giga FVZ Jun-13 7,800cc 788.5

BMW 320d Jun-13 2,000cc 659*

BMW M6 Gran Coupe Jul-13 4,400cc 2,598*

Lexus IS Series Jul-13 2,500cc 850-950

*Off the road

Car products launched in 2013

30

Models Launched Launching Time Engine Capacity Prices (IDR mn)

Car Toyota New Innova Aug-13 2,000cc-2,500cc 197.3-316.5Toyota New Rush Aug-13 1,500cc 205.5-232.7

Daihatsu New Terios Aug-13 1,500cc 169.5-220.3Toyota New Fortuner Sep-13 2,500cc-2,700cc 396-506.5

BMW 435i Coupe M Sport Sep-13 3,000cc 998*BMW Z4 sDrive20i Sep-13 2,000cc 929*

BMW Z4 sDrive35i Sep-13 3,000cc 1,409*Peugeot 208 Gti Sep-13 1,600cc 565.2*Astra Toyota Agya Sep-13 1,000cc 99.9-120.75

Astra Daihatsu Ayla Sep-13 1,000cc 76.5-107Isuzu D-Max Sep-13 2,500cc 266

Isuzu D-Max Sep-13 3,000cc 399Isuzu Giga FVM High Power Sep-13 285ps n/a

Isuzu Giga FTR Tractor Head Sep-13 210ps 487Isuzu GIGA FVZ MX 34 P Mixer Sep-13 285ps 802Isuzu GIGA FVZ 34T Long wheel base Sep-13 285ps n/a

Isuzu Elf NKR 55 Long Wheel Base Sep-13 101ps 221Isuzu Elf NKR 71 Econo Sep-13 125ps 274

Lexus ES Series Oct-13 2,500cc 810-915*Off the road

Motorcycle products launched in 2013

31

Models Launched Launching Time Engine Capacity Prices (IDR mn)*

Motorcycle

Honda Verza Jan-13 150cc 16.1 – 16.9

Honda Revo Series Jan-13 110cc 13

Honda Vario Feb-13 110cc 14.6

Honda Scoopy FI Feb-13 110cc 13.9

Honda Spacy FI Mar-13 110cc 13.2

Honda Vario 125 CBS Idling Stop Mar-13 125cc 16.4

Honda Supra X 125 R Apr-13 125cc 14.9-15.9

Honda Supra X 125 Helm-In FI Jul-13 125cc 16.5

Honda Scoopy FI Sep-13 110cc 14.3

Honda CBR 150R Oct-13 150cc 41.8-42.5

Honda CB 150 R Dec-13 150cc 23.5

32

2013 2012Major Brands

Wholesale Astra Wholesale Astra

Car

Sedan 34,744 55.6% 34,722 56.6%Toyota - Vios/Limo, Camry, Altis ; Honda - City,Civic, Accord; Mercedes - E Series, C Series

4X2 & 4X4 845,541 62.2% 746,373 64.3%

Toyota - Avanza, Innova, Rush, AgyaDaihatsu - Xenia, Terios, Ayla; Nissan - Grand Livina,March, Evalia; Suzuki - Ertiga, APV, Splash; Honda -Jazz, CR-V, Freed; Mitsubishi – Pajero Sport, Mirage, Outlander Sport

Pick Up/ Trucks/ Bus 334,501 30.9% 316,476 30.9%Mitsubishi – Canter, L-300, Strada; Daihatsu – Gran Max; Suzuki – Carry, APV; Isuzu – Elf, Panther, Giga; Toyota – Dyna ,Hi-Lux, Hi-Ace

Double Cabin 15,115 37.1% 18,659 38.6%Toyota – Hilux; Mitsubishi – Strada; Ford – Ranger; Isuzu – D-Max

Total 1,229,901 1,116,230

Mo

torc

ycle

Cub 1,495,209 58.5% 1,852,792 57.1%Honda - Supra X 125, Revo Series, Blade; Yamaha -Jupiter MX, Vega RR, Jupiter Z; Suzuki – SmashTitan, Shooter, Shogun Axello 125

Scooter 4,893,647 70.0% 4,208,219 68.0%Honda - BeAT, Vario, Scoopy; Yamaha - Mio, Xeon, X-Ride; Suzuki – Nex, Hayate, Let’s

Sport & Others 1,355,023 29.3% 1,003,446 17.0%Yamaha - V-ixion, Byson, Scorpio Z; Honda - CB 150 R, Verza, New Mega Pro; Suzuki - Satria F 150, Thunder 125

Total 7,743,879 60.7% 7,064,457 57.9%

Source: Gaikindo & AISI

National market data (summary)

For further information please contact:

Investor Relations of PT Astra International Tbk - Attn:

Iwan Hadiantoro / Tira Ardianti / Inneke Soendoro / Christian

P: (+62 21) 652 2555

F: (+62 21) 6530 4953

E: [email protected] / [email protected] /

[email protected] / [email protected]

33