Career Planning Process Michael Tavares, MS Counselor Sacramento City College.

Upload

shannon-barkerCategory

view

213download

0

©2013, College for Financial Planning, all rights reserved.

Module 3Employer-Sponsored Plans

Chartered Retirement Planning CounselorSM Professional Designation Program

Learning Objectives

3–1: Describe basic characteristics of qualified retirement plans and the main types of qualified plans.

3–2: Describe basic characteristics of profit sharing and money purchase plans.

3–3: Describe basic characteristics of 401(k) plans.

3–4: Describe basic characteristics of Keogh plans.

3–5: Explain basic characteristics of defined benefit plans.

3–6: Describe basic characteristics of retirement plans that are designed for small employers.

3–7: Describe basic provisions of retirement plans that are designed for nonprofit entities.

3-2

Questions to Get Us Warmed Up

3-3

Learning Objectives

3–1: Describe basic characteristics of qualified retirement plans and the main types of qualified plans.

3–2: Describe basic characteristics of profit sharing and money purchase plans.

3–3: Describe basic characteristics of 401(k) plans.

3–4: Describe basic characteristics of Keogh plans.

3–5: Explain basic characteristics of defined benefit plans.

3–6: Describe basic characteristics of retirement plans that are designed for small employers.

3–7: Describe basic provisions of retirement plans that are designed for nonprofit entities.

3-4

Factors Affecting Qualified Plan Contributions & Benefits (plan level issues)

Contributions to Plan During Employment Years

• (deduction limits)

3-5

Diversification & Investment Requirements

IRC Section 401(a)(28)

ERISA Section 204(j) requires most defined contribution plans maintained by publicly traded corporations to permit

participants to direct that the following percentages of employer securities held in their accounts be reinvested in suitable alternative investments:• 100% of amounts attributable to 401(k) elective deferrals

• For participants with at least 3 years of service: 33% of amounts attributable to employer contributions for the first year; 66% of amounts attributable to employer contributions for the second year; and 100% of amounts attributable to employer contributions for the third year

3-6

Diversification & Investment Requirements

IRC Section 401(a)(28)

ESOPs maintained by either publicly traded or privately owned companies that are funded with employer

contributions only (“stand-alone” ESOPs) must permit a participant age

55 or older with at least 10 years of participation to diversify the following percentages of employer securities held in his

account into other assets over six consecutive plan years:• 25% of account balance over the first five plan years,

and

• 50% of his account balance in the sixth and last plan year.

• Stand-alone ESOPs are not subject to ERISA 204(j)

3-7

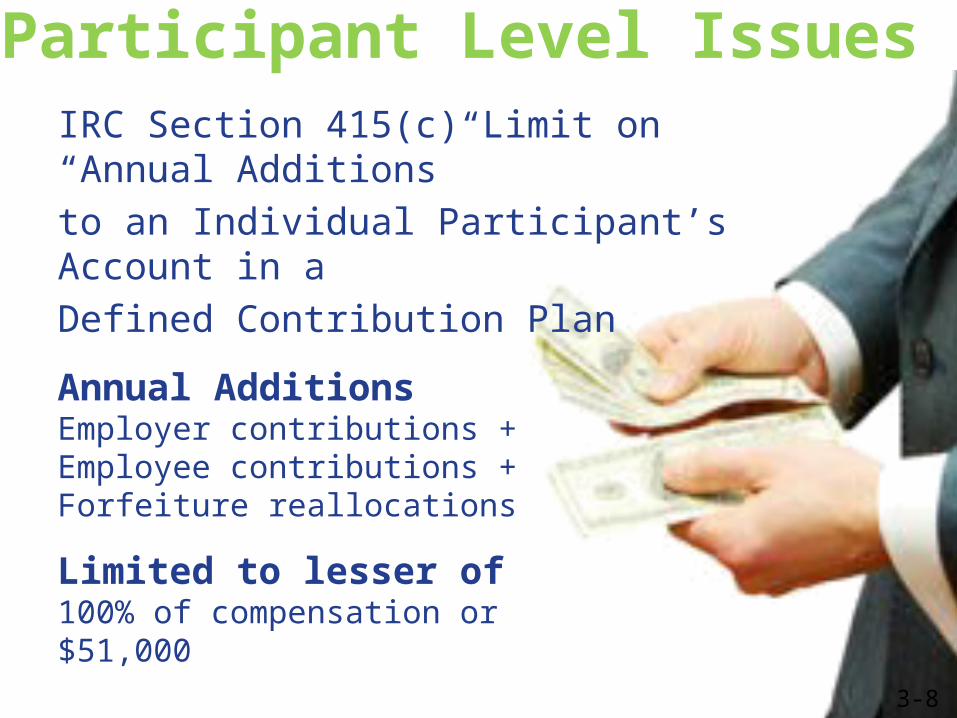

Participant Level IssuesIRC Section 415(c) Limit on “Annual Additions”to an Individual Participant’s Account in aDefined Contribution Plan

Annual AdditionsEmployer contributions + Employee contributions +Forfeiture reallocations

Limited to lesser of100% of compensation or $51,000

3-8

Selected Characteristics of SEPs & Defined Contribution Plans

Basic Characteristics

SimplifiedEmployeePension

Plan(SEP)*

ProfitSharin

gPlan

Stock BonusPlan orESOP

Money Purchase

Plan

Target Benefit

Plan

Employer Contribution:Maximum Deduction

25% of covered payroll

Mandatory?No; fully

discretionary

No, but must besubstantial and

recurring

Yes; % of compensation or

flat sum, as stated in plan

Yes; per plan

formula

Employee Contribution 401(k) / CODA provisions may

be permitted

401(k)/CODA not permitted, but after

tax contributionsallowed

After tax contributio

nsallowed

Forfeitures N/A ReallocatedReallocated or reduce employer

contribution

Annual Additions Limit

The lesser of 100% of individual’s compensation or $51,000

Nondiscrimination Coverage and participation tests*Although not considered a qualified plan because it consists of participants’ IRAs, a SEP is subject to many defined contribution plan requirements.

3-9

Learning Objectives

3–1: Describe basic characteristics of qualified retirement plans and the main types of qualified plans.

3–2: Describe basic characteristics of profit sharing and money purchase plans.

3–3: Describe basic characteristics of 401(k) plans.

3–4: Describe basic characteristics of Keogh plans.

3–5: Explain basic characteristics of defined benefit plans.

3–6: Describe basic characteristics of retirement plans that are designed for small employers.

3–7: Describe basic provisions of retirement plans that are designed for nonprofit entities.

3-10

Employer

Participant

Profit Sharing Plans

Basic Provisions

• 25% employer deduction limit.

• Employer contributions usually are discretionary, but must be “substantial and recurring.”

• Forfeitures usually are reallocated to remaining participants’ accounts.

3-11

Participant

Employer

Basic Provisions• Same provisions as profit sharing plans,

except contribution is in employer stock

Stock Bonus Plans

3-12

Participant

Employer

Leveraged Stock Ownership Plan

Basic Provisions

• Primary purpose of ESOP is to invest in qualifying employer securities

• Contributions of up to 25% of payroll may be used to buy securities for plan

• Diversification requirements for ESOPs: participants age 55 or over with at least 10 years of service must be offered election to transfer up to 25% of account to alternative investments—election period covers six years, with 50% transfer available in year 6

3-13

Employer

Participant

Basic Provisions

• Employer contributions of up to 25% of covered payroll

• Forfeitures may be reallocated to remaining participants’ accounts or applied to reduce employer contributions

• Subject to minimum funding standard

• Money purchase plans are no longer useful with 25% profit sharing plans available

Money Purchase Plan

3-14

Target Benefit PlansProvisions Shared with Defined Contribution Plans• Maximum annual additions

to a participant’s account are limited to the lesser of 100% of compensation or $51,000

• Retirement benefit is determined by account balance

• Employee assumes investment risk

• No annual actuarial determination

• Forfeitures may be reallocated or used to reduce employer contribution

Provisions Shared with Defined Benefit Plans• Plan generally benefits

older employees

• Actuary determines initial contribution level and formula for allocating contributions

• Mandatory annual contributions

3-15

Participant

Employer

Target Benefit Plans

Basic Provisions

• Employer contributions of up to 25% of covered payroll

• Allocation of employer contributions based on age-weighted formula

• Forfeitures may be reallocated to remaining participants’ accounts or applied to reduce employer contributions

• Subject to minimum funding standard

3-16

Learning Objectives

3–1: Describe basic characteristics of qualified retirement plans and the main types of qualified plans.

3–2: Describe basic characteristics of profit sharing and money purchase plans.

3–3: Describe basic characteristics of 401(k) plans.

3–4: Describe basic characteristics of Keogh plans.

3–5: Explain basic characteristics of defined benefit plans.

3–6: Describe basic characteristics of retirement plans that are designed for small employers.

3–7: Describe basic provisions of retirement plans that are designed for nonprofit entities.

3-17

401(k) Provisions

• Section 401(k) plan must be combined with a qualified defined contribution plan (profit sharing, stock bonus, pre-ERISA money purchase), a SARSEP (if SARSEP is established prior to 1997), or a SIMPLE

• 25% limit on total of employer contribution excluding salary reduction or CODA contribution

• Employee is always 100% vested in own contributions

• Nondiscrimination requirements: ADP and ACP tests

3-18

401(k) Plans Employee & Employer Eligibility

• Employee eligibility requirements – one year of service (generally 1,000 hours) and age 21

• Employer eligibility to establish 401(k) planso Sole proprietorso Partnershipso C and S corporationso Tax-exempt organizationso Indian tribal governments

• Under current law, state and local governments are prohibited from establishing 401(k) plans

3-19

401(k) Plans Pre-tax Participant Contributions

• Are called “elective deferrals” or “salary reduction contributions” (tax-deferred but are subject to payroll taxes; i.e., FICA and FUTA).

• 2013 limit = $ 17,500, or $23,000 if age 50 or over

• Affirmative election—salary reduction agreement

• Negative elections—employees are automatically enrolled unless they elect out

• Catch-up contributions ($5,500 for 2013)

3-20

401(k) Usage & Investment Responsibility

• Studies indicate 401(k) plans are:o underutilized by employees o but the vast majority of employees contribute

something to their 401(k) plans o most plan participants lack the knowledge to

make good investment choices• 401(k) plan fiduciary duties include establishing

a funding policy suitable for the participants

• 401(k) plans do not have to permit participant-directed investments—but many plans allow this

• A plan fiduciary is potentially liable for losses if a substandard directed investment option is selected

3-21

401(k) Provisions

3-22

Participant

Employer

Basic Characteristics of Plans with 401(k)/ Salary Reduction Provisions

3-23

Characteristic SARSEP

Profit Sharing or Stock Bonus Plan with 401(k)

EmployeeContribution

$17,500 in 2013 (indexed) maximum elective deferral plus $5,500 age 50 catch-up if eligible

Employee Matching Contribution Available?

No Yes

Forfeitures N/A; no forfeitures Reallocated (employer contributions)

In-ServiceWithdrawals

Distributions at any time, subject to 10% penalty if premature

Under hardship conditions, employee’s elective contributions can be withdrawn (subject to 10% penalty if premature)

Tax Treatment ofDistribution

Ordinary income tax ondistribution amount

Forward averaging may be available

Nondiscrimination Tests

Coverage and special ADP test

Coverage, ADP, and ACP tests

Loan Provisions Not allowed Per plan provisions; five-yearrepayment

Keogh Plans

Basic Provisions

• May be established by sole proprietor or partnership

• Takes the form of a qualified plan (defined contribution or defined benefit), but certain provisions for owner/employee are unique to Keoghs:o owner/employee’s contribution is calculated on earned

incomeo plan loans to common law employee-participants and

owner/employee-participants (such as sole proprietors or partners) are permitted

o lump-sum distribution treatment is not available to owner/employee for separation from service before age 59½—available only for death, disability, or attainment of age 59½

• IRC definition of employee: An individual who has “earned income”

3-24

Learning Objectives

3–1: Describe basic characteristics of qualified retirement plans and the main types of qualified plans.

3–2: Describe basic characteristics of profit sharing and money purchase plans.

3–3: Describe basic characteristics of 401(k) plans.

3–4: Describe basic characteristics of Keogh plans.

3–5: Explain basic characteristics of defined benefit plans.

3–6: Describe basic characteristics of retirement plans that are designed for small employers.

3–7: Describe basic provisions of retirement plans that are designed for nonprofit entities.

3-25

Participant

Employer

Defined Benefit Plans

Basic Provisions

• Employer funds plan to provide annual retirement benefit equal to a specific dollar amount of up to the lesser of $205,000 (in 2013, indexed) or 100% of compensation

• No limit on contribution amount—whatever is required to fund plan benefits that do not exceed statutory limits ($205,000 in 2013, indexed) or 100% of compensation

• Actuary determines required contribution each year

• Plan can be integrated with Social Security

3-26

Factors Affecting Annual Retirement Benefits in a Defined Benefit Plan

Participant Level Issues

• Retirement Ageo Normal retirement: at age 65 or the Social Security

retirement age, the maximum benefit is the lesser of $205,000 in 2013 (indexed) or 100% of average compensation

o Retirement after age 65: normal maximum retirement benefit limit is adjusted upward

o Retirement before age 62: normal maximum retirement benefit limit is adjusted downward

• Years of Plan Participationo 10% reduction in maximum dollar

limitation ($205,000 in 2013, indexed) on normal retirement benefit for each year of plan participation less than 10

o 10% reduction in maximum percentage limitation (100%) for each year of service less than 10

3-27

Factors Affecting Annual Retirement Benefits in a Defined Benefit Plan

Definition of Earnings• Career-average pay

Average earnings over plan participation period lower benefit

• Final-average payAverage earnings over final 3 or 5 years, or average highest 3 or 5 of last 10 years higher benefit, reflecting more recent impact of inflation on employee’s salary

3-28

Factors Affecting Annual Retirement Benefits in a Defined Benefit Plan

Benefit Formulas

• Flat benefit: service is not considered

o benefit is flat amount or % of earningso service reduction may be used: reduced

benefit for <X years of service (X = owner/key employee’s number of years of service at retirement)

• Fixed benefit: plan provides a retirement that is a stated amount not related to a participant’s compensation or years of service

• Unit benefit: plan provides credit for years of service

o benefit is a dollar amount per year of service or a % of earnings per year of service

o participant accrues additional benefit each year

o service limitation may be used; considers years of service up to specified maximum (resolves problem of older owner with 20 years of service at age 65 vs. younger employee with 30–40 years of service at age 65)

3-29

Learning Objectives

3–1: Describe basic characteristics of qualified retirement plans and the main types of qualified plans.

3–2: Describe basic characteristics of profit sharing and money purchase plans.

3–3: Describe basic characteristics of 401(k) plans.

3–4: Describe basic characteristics of Keogh plans.

3–5: Explain basic characteristics of defined benefit plans.

3–6: Describe basic characteristics of retirement plans that are designed for small employers.

3–7: Describe basic provisions of retirement plans that are designed for nonprofit entities.

3-30

Participant

Employer

Simplified Employee Pensions (SEPs)

3-31

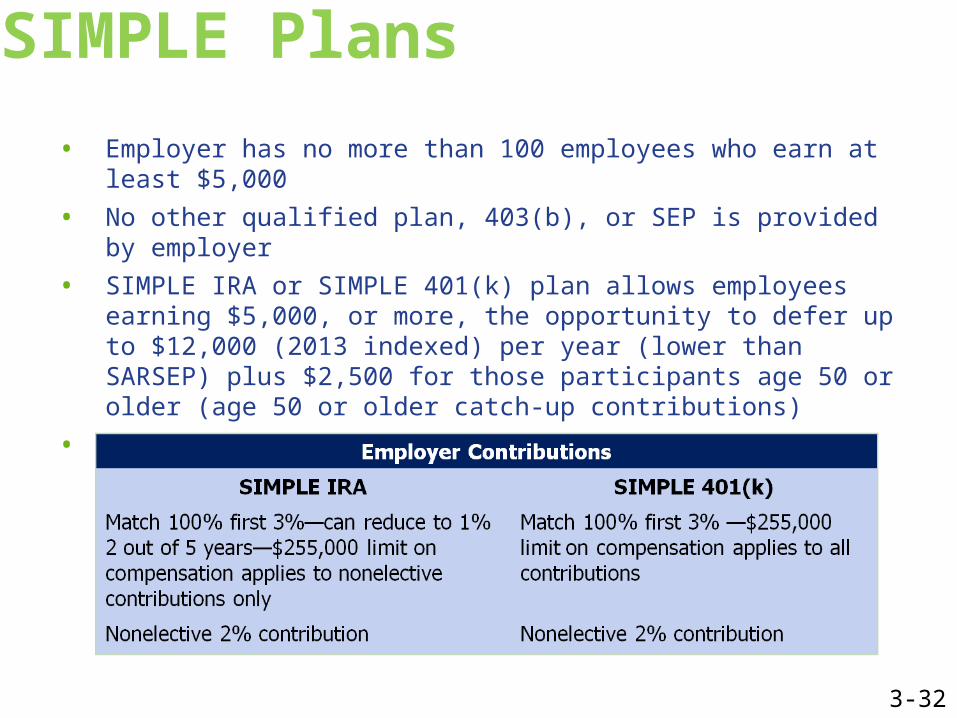

SIMPLE Plans

• Employer has no more than 100 employees who earn at least $5,000

• No other qualified plan, 403(b), or SEP is provided by employer

• SIMPLE IRA or SIMPLE 401(k) plan allows employees earning $5,000, or more, the opportunity to defer up to $12,000 (2013 indexed) per year (lower than SARSEP) plus $2,500 for those participants age 50 or older (age 50 or older catch-up contributions)

• Employer contributions less flexible than under SARSEPs

3-32

Simple IRA Plans

• All contributions are immediately 100% vested

• Top-heavy rules and 415 limit do not apply

• Distributions from SIMPLE IRAs are generally treated under IRA ruleso Rollovers permitted from one SIMPLE IRA

to another or (after two-year participation o period) to an individual IRA, qualified plan, o TSA, SEP, or governmental 457 plan that

accounts for rollovers separately.o Early withdrawals are permitted o During initial two years of participation:

25% early withdrawal penalty taxo After two years of participation: 10% early withdrawal

penalty tax• Loans are not permitted from SIMPLE IRA

3-33

SIMPLE 401(k) Plan (a qualified plan)

• All contributions immediately 100% vested

• Nondiscrimination tests (ADP/ACP) do not apply

• Top-heavy rules do not apply

• Distributions from SIMPLE 401(k) generally treated under qualified plan ruleso Rollovers permitted from a SIMPLE 401(k) to

an individual IRA, qualified plan, TSA, SEP, or governmental 457 plan that accounts for rollovers separately.

o In-service hardship withdrawals are permitted—generally subject to 10% penalty tax

• Loans are permitted

3-34

Defined Contribution Plan Limits

3-35

Type of Plan

Limits on Employer Contribution

Limits on EmployeeDeferrals/Catch-ups

Allocation of Employer’sContributions

AdministrativeCosts/Burden

Target Benefit

25% deduction limit—subject to minimum funding standard

Not available Age weighted Actuary first year

MoneyPurchase

25% deduction limit—subject to minimum funding standard

Not available Fixed contributions,can be integratedwith Social Security

Relatively low

Profit Sharing

25% deduction limit

Profit sharing 401(k)—$17,500 (indexed) plus catch-up if eligible. (Catch-up contributions not allowed in regular pr/sh plans.)

Plan formula may usesalary or service; canbe age weighted orinclude integrationwith Social Security

Relatively low —employercontributions must be “substantial and recurring,” but employer has flexibility with annualcontributions

Defined Contribution, SEP & SIMPLE Plan Limits

3-36

Type of Plan

Limits on Employer Contribution

Limits on EmployeeDeferrals/Catch-ups

Allocation of Employer’sContributions

AdministrativeCosts/Burden

Simplified EmployeePensions (SEPs)

25% deduction limit

Not allowed. Prior to January 1, 1997, could include 401(k)-type provisions (SARSEP), but can no longer establish a SARSEP

Allocation formula used—can include integration with Social Security

Low—employer has full discretion re: future contributions within the 25% limitation

Savings IncentiveMatch Plan forEmployees(SIMPLE) IRA

3% dollar-for-dollar or 1% in 2 out of 5 years matching or 2% nonelective

$12,000 (indexed) plus $2,500 age 50 catch-up if eligible

Percentage of compensation

Low—no ADP or ACP testing; employer may reduce matching contribution to 1% in 2 out of 5 years

SIMPLE 401(k)

3% dollar-for-dollar matching or 2% nonelective

$12,000 (indexed) plus $2,500 age 50 catch-up if eligible

Percentage of compensation

Low—no ADP or ACPtesting

Points to Consider for Selection of Most Appropriate Plan

3-37

Employer Characteristics and ObjectivesAppropriate Plan

• Seeks maximum tax shelter• Owner usually 45 or older and oldest or one of the oldest employees,

only one or two older• Reward long-term employees, and favor older employees• Willing and able to make annual financial commitment in excess

of 25% of compensation• Willing to accept investment risk• Means to allow owner to meet his/her retirement

Defined Benefit Plan

• Business has stable cash flow and owner willing to make annual financial commitment, but either unwilling or unable to commit more than 25% of compensation• Shift investment risk to employees• Easier to communicate plan to employees, and reduce administrative costs• Younger employees benefit from years of contributions and compounding

Money Purchase or Target BenefitPlan to provideage-weightedPlan

• Business cash flow fluctuates• Shift investment risk to employees• Desire plan that will motivate employees• Younger employees benefit from years of contributions and compounding

Profit Sharing,SEP,or Tandem Plan

• No other qualified plan or 403(b)• No more than 100 employees earning $5,000 or more• Owner willing to make minimal contribution—2% or 3% of compensation• Desire to provide tax-deferred savings for employees• Desire very low administrative cost

SIMPLE IRAorSIMPLE 401(k)

Learning Objectives

4–1: Explain the characteristics of the eight legal forms of business.

4–2: Describe basic characteristics of qualified retirement plans and the main types of qualified plans.

4–3: Describe basic characteristics of profit sharing and money purchase plans.

4–4: Describe basic characteristics of 401(k) plans.

4–5: Describe basic characteristics of Keogh plans.

4–6: Explain basic characteristics of defined benefit plans.

4–7: Describe basic characteristics of retirement plans that are designed for small employers.

4–8: Describe basic provisions of retirement plans that are designed for nonprofit entities.

3-38

TSA Provisions

• Eligibility: must be employee of public school or 501(c)(3) (tax-exempt) organization

• Limit: the lesser of $17,500 (2013) plus long service catch-up if eligible, or the Section 415(c) limit plus age 50 catch-up if eligible.

• Taxation: contributions and earnings are tax deferred until distribution—ordinary tax rates apply

• Distributions: loans and

• distributions per qualified plan rules

• Investments: limited to annuities, mutual funds

3-39

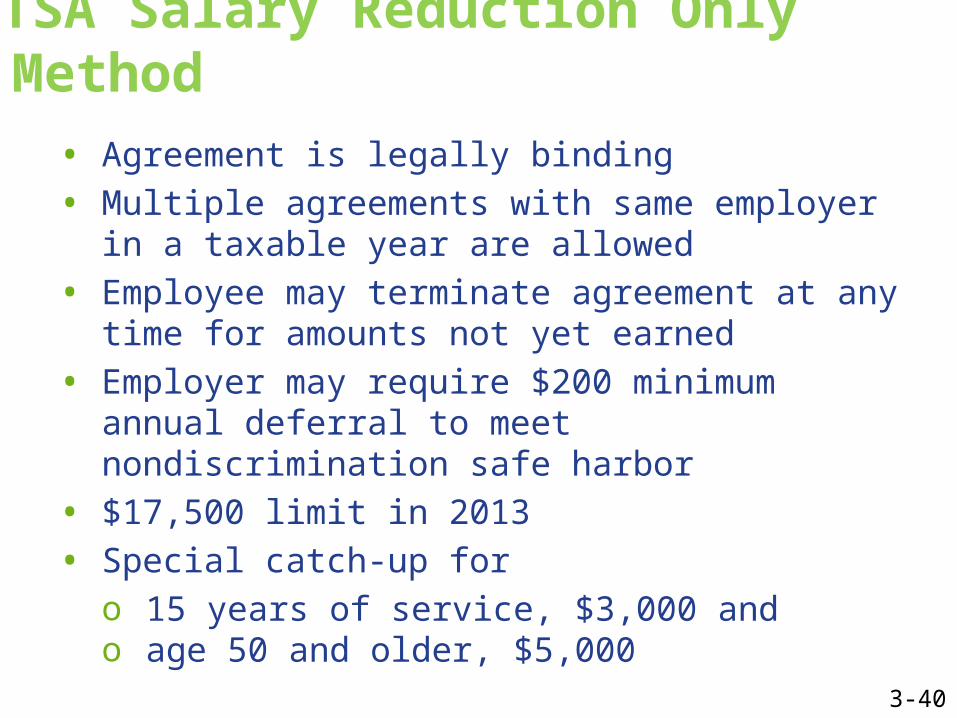

TSA Salary Reduction Only Method• Agreement is legally binding• Multiple agreements with same employer in

a taxable year are allowed• Employee may terminate agreement at any

time for amounts not yet earned• Employer may require $200 minimum

annual deferral to meet nondiscrimination safe harbor

• $17,500 limit in 2013 • Special catch-up for

o 15 years of service, $3,000 ando age 50 and older, $5,000

3-40

Calculating Maximum TSA Salary Deferral

The lesser of the following two limits:1. the annual deferral limit:

$17,500 in 2013 plus the long service catch-up2. Section 415(c) limit:

lesser of 100% of compensation or $51,000 in 2013 plus age 50 catch-up if eligible

Compensation means total compensation,including salary reduction for TSA and redirectionamounts for cafeteria plans (Section 415(c) definition of “compensation” includes electivedeferrals and salary redirections)

3-41

Section 457 Plan Provisions• Eligibility: state/local governments, nonprofit

organizations, not churches or other religious organizations

• Contributions: salary reduction agreement must be executed before the first day of the month in which services were performed

• Limit: lesser of $17,500 (2013 indexed) plus the age 50 catch-up or the final three year catch-up or 100% of includible compensation (includible compensation is annual compensation paid to employee including deferral).

The age 50 catch-up cannot be used in conjunction with the final three year catch-up.

3-42

Section 457 Plan Provisions• Catch-Up Elections

(must choose 1) or 2) from below, not both):1. long service: available in

three years preceding normal retirement age—up to $17,500 total deferral per year, or

2. age 50: additional $5,500 for those age 50 and older not in the final three years prior to retirement

• Taxation: contributions and earnings are tax deferred until distributed—ordinary tax rates apply

3-43

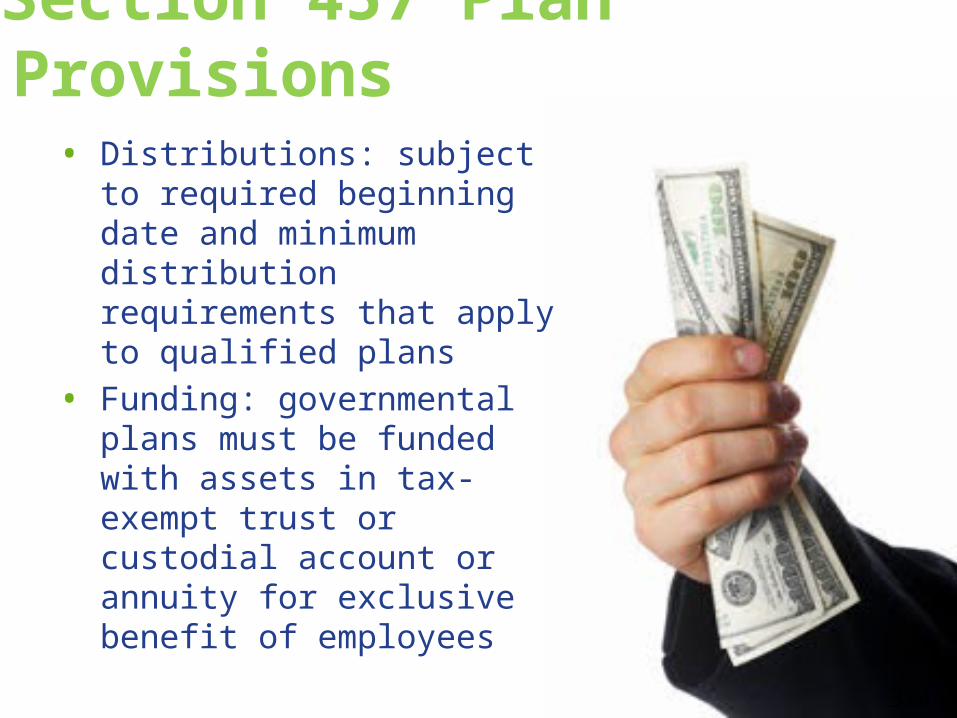

Section 457 Plan Provisions• Distributions: subject to

required beginning date and minimum distribution requirements that apply to qualified plans

• Funding: governmental plans must be funded with assets in tax-exempt trust or custodial account or annuity for exclusive benefit of employees

3-44

Question 1

Which of the following statements is correct regarding 403(b) plans and Section 457 plans?

a. Investment options in a 403(b) plan include annuities and stocks.

b. Section 457 plans can be rolled over into an IRA account.

c. Section 457 plans do not have required minimum distributions (RMDs).

d. 403(b) plans may be subject to ACP, but not ADP testing.

4-45

Question 2

Which one of the following is not a provision of the special limits that are available to certain employees in a TSA plan?

a. It is available to employees of health, education, and religious organizations (HER organizations).

b. It may use both catch-up provisions if qualified.

c. It may typically defer at least $200 to their TSA during the first year of service.

d. With 10 or more years of service, a participant may increase each year’s deferral limit by $3,000 (up to $15,000 of cumulative increases).

e. If prior salary reductions exceed $5,000 times years of service, no increase to the deferral amount is available to employees with more than 15 years of service.

4-46

Question 3

Which of the following accurately describe provisions under the hardship withdrawals from a profit sharing 401(k) plan?

I. A withdrawal may be made from employee elective deferrals and associated earnings.

II. A participant must establish an “immediate and heavy financial need.”

III. A withdrawal is exempt from the 10% early withdrawal penalty.

IV. A participant must exhaust other available resources.

a. I and II onlyb. II and III onlyc. II and IV onlyd. I, III, and IV onlye. II, III, and IV only

4-47

Question 4

Target benefit plans are subject to which one of the following limitations on employer contributions?

a. 10% of covered payrollb. 15% of covered payrollc. 25% of covered payrolld. 100% of covered payroll

4-48

Question 5

Which of the following could be expected to reduce the annual cost of a defined benefit plan?

I. a high turnover assumptionII. use of salary scalesIII.a high interest rate assumptionIV.a high benefit cost assumptionV. a low turnover assumption

a. I and II onlyb. I and III onlyc. II and IV onlyd. I, II, and III onlye. II, IV, and V only

4-49

©2013, College for Financial Planning, all rights reserved.

Module 3End of Slides

Chartered Retirement Planning CounselorSM Professional Designation Program