2013 Annotated Tax Forms Book 1: Common Forms … Annotated Tax Forms Book 1: Common Forms and...

47

2013 Annotated Tax Forms Book 1: Common Forms and Schedules Prepared for SSS By NAIS by: Mike Szydlowski, Director of Financial Aid Woodberry Forest School (VA) Mark J. Mitchell, Vice President SSS By NAIS March, 2014

Transcript of 2013 Annotated Tax Forms Book 1: Common Forms … Annotated Tax Forms Book 1: Common Forms and...

2013AnnotatedTaxForms

Book1:CommonFormsandSchedules

Prepared for SSS By NAIS by:

Mike Szydlowski, Director of Financial Aid

Woodberry Forest School (VA)

Mark J. Mitchell, Vice President

SSS By NAIS

March, 2014

Book1ContentsWhat’sNew Highlightsofkeyprovisionsandchangesforthe2013taxyear

QuickReferenceChart Lineitemcross‐referenceofkeyPFSand1040entries

W‐2 WageandTaxStatement

1099‐DIV DividendsandDistributions

1099‐G CertainGovernmentPayments

1099‐INT InterestIncome

1099‐MISC MiscellaneousIncome

1099‐R DistributionsfromPensions,Annuities,IRA’s,etc.

1098‐E StudentLoanInterestStatement

1098‐T TuitionStatement

Form1040 U.S.IndividualIncomeTaxReturn

Form1040A U.S.IndividualIncomeTaxReturn

ScheduleA ItemizedDeductions

ScheduleB InterestandOrdinaryDividends

ScheduleC ProfitorLossfromBusiness(SoleProprietorship)

ScheduleC‐EZ NetProfitfromBusiness

ScheduleD CapitalGainsandLosses

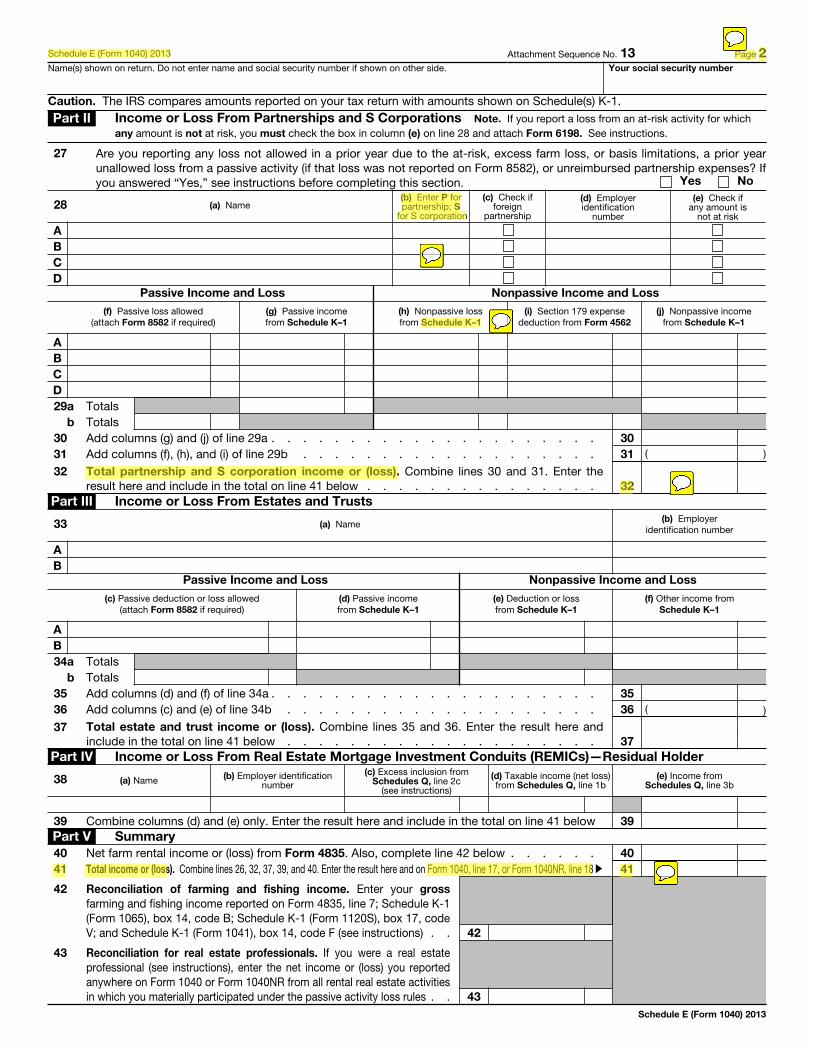

ScheduleE SupplementalIncomeandLoss

ScheduleF ProfitorLossFromFarming

ScheduleSE Self‐EmploymentTax

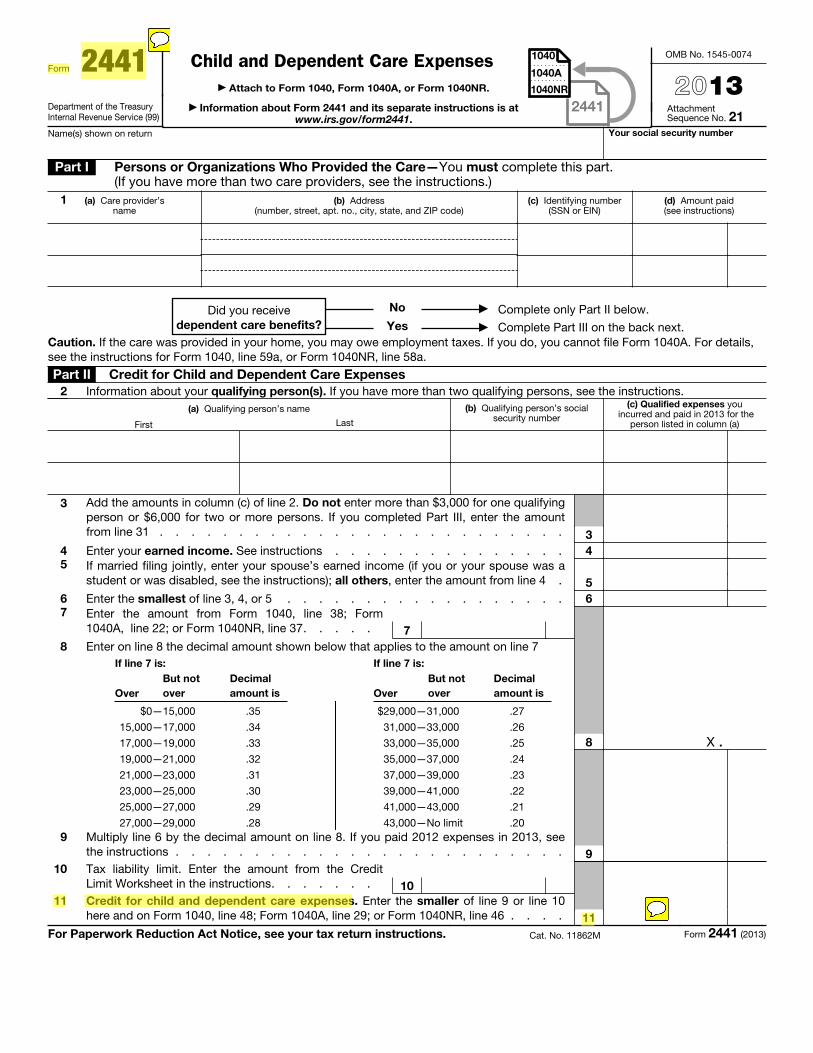

Form2441 ChildandDependentCareExpenses

Form2555 ForeignEarnedIncome

Form4506‐T RequestforTranscriptofTaxReturn

Form4562 DepreciationandAmortization

Form8606 NondeductibleIRA’s

Form8829 ExpensesforBusinessUseofYourHome

Form8949 SalesandOtherDispositionsofCapitalAssets

2013 SSS By NAIS Annotated Tax Packet

How To Use The Annotated Tax Forms Packet The 2013 Annotated Tax Forms Packet is designed for use as an on-screen document for review. The

annotations are provided as ‘mouse-over’ text attached to symbols pointing to specific line items,

phrases, or headings on each tax document.

There are three types of annotations you will find:

1. PFS and RFC References – Many of the annotations highlight those items on tax forms that have

corresponding line references to the Parents’ Financial Statement (PFS) and/or the Report of

Family Contribution (RFC). These are helpful in verifying that parents entered the information

correctly and if not, what to use to revise the entries. These items are also captured in the SSS

document collection process and presented within the software for your review.

2. Helpful Pointers – There are some forms that include notations that offer commentary on

specific line items on a tax form that do not have a corresponding PFS or RFC line but may

provide insight or additional information useful in review and in increasing your knowledge of

tax-related information that may have relevance in better understanding a family’s financial

profile.

3. General Guidance – A few of the annotations offer general commentary about the document

overall or a section of the document. This helps the reader understand things like the purpose

of the form and how much scrutiny or attention to pay to it.

Look for text and/or line numbers highlighted in yellow. If you see a highlight, there’s usually a “thought

balloon” symbol providing the annotated text for your review. In a few instances, the highlighting is

self-explanatory and is done simply to draw your attention to some information without the need for

annotation.

To read the annotation, simply “hover” your cursor/pointer over the balloon symbol that appears next

to the highlighted text. A pop-up box should appear beneath your pointer with the annotation. You do

not need to click on the symbol to see the annotation. If you do, the text will appear in a larger box that

can be minimized after you read it.

All annotated documents are provided as PDF files, so be sure to have the Adobe Acrobat Reader

installed. Since they are PDF’s, you can use features of the Acrobat Reader to make it easier for you to

navigate around the document, such as adding bookmarks to pages that you refer to often or using

thumbnail views to jump between pages that you’re looking to get to more quickly than by scrolling.

Also, you can save the PDF to your computer by clicking “File/Save As...” to save it locally instead of

returning to the site each time you need to view it.

2013 SSS By NAIS Annotated Tax Packet

What’s New? Highlights of Key Changes in the 2013 Tax Code

New Taxes for High-Income Earners

1) The top tax bracket for 2013 is 39.6%, up from 35% in 2012.

2) There is a new 3.8% Net Investment Income Tax (NIIT).

3) The top long-term capital gain tax rate for 2013 is 20% and, if applicable, the NIIT could add

another 3.8% making possible a 23.8% rate, up from 15% in 2012.

4) There is a new 0.9% additional Medicare tax. According to the IRS website, individuals are

liable for this tax when wages, compensation or self-employment income (together with spouse

if filing jointly) exceed the thresholds below:

Filing Status Threshold Amount

Married Filing Jointly $250,000

Married Filing Separate $125,000

Single $200,000

Head of Household $200,000

Qualifying Widow(er) with Dependent Child $200,000

Separately, none of these new taxes may be significant but taken together and when you couple

these new taxes with the fact that high income earners may also lose a percentage of their

personal exemption amount(s) and their itemized deductions (which increases marginal tax

rates), some former full-pay families may feel the need to apply for aid. For example, it is

possible for a family earning $400,000 and another $100,000 in capital gains with four children

and large itemized deductions to see an increase in their income tax of $30,000 or more. Of

course, as taxes increase, the calculated parent contribution will increase (all other things being

equal). For some, this could mean increased aid eligibility.

Other Key Changes

1) Medical Expenses Deduction. Line #3 on Schedule A now allows a deduction for only

those medical expenses in excess of 10% of Adjusted Gross Income, up from 7.5%.

2) FICA Tax Rates. The 6.2% Social Security portion of the FICA tax rate now applies to the

first $113,700 of income up from $110,100.

3) Business Use of Home Deduction. For 2013, there is a simplified home office deduction

option available: $5.00 per square foot up to 300 square feet ($1,500 maximum deduction

allowed) can be deducted on line #30 of Schedule C without having to complete Form

8829. According to IRS rules, none of the home office deduction when determined by using this

simplified method is considered depreciation. Taxpayers can select to use the “regular” option

of completing the Form 8829, so it’s possible you may still see some of those filed. If the

taxpayer uses the simplified option, do not expect to see or require a Form 8829.

Note: These references are based on the 2013 federal 1040 and schedules and 2014-15 Parents’ Financial Statement. RFC line references are based on the Comp*Assist Online RFC as of February, 2014. Line references are subject to change.

Produced by SSS By NAIS, March, 2014

Quick Reference Chart 2014-15 Parents’ Financial Statement and 2013 Tax Documents

Item

2014-15 PFS Item/RFC Line #

2013

1040 Line/Schedule/Form

Additional child tax credit* PFS 6E/RFC 17 1040 Line 65 Adoption credit* Crosscheck RFC 17 1040 Line 53 Alimony paid PFS 24 / RFC 22 1040 Line 31a Alimony received PFS 7D / RFC 4 1040 Line 11 Alternative Minimum Tax (AMT) PFS 6E / RFC 17 1040 Line 45 Business profit/loss PFS 7I / RFC 5 1040 Line 12 / Schedule C Child care expenses PFS 21 1040 Line 48 / Form 2441 Line 11

Capital gains/losses PFS 7E / RFC 6 1040 Lines 13, 14 / Sch D/Form 8949 Child tax credit* PFS 6E or 8C / RFC 11 or 17 1040 Line 51 Children in home PFS 3B, 19, 21 1040 Line 6c Earned income credit PFS 8C / RFC 11 1040 Line 64a / Schedule EIC Education credit* PFS 6E OR 8C / RFC 17 1040 Line 49 & 66 / Form 8863 Elderly, disabled credit* PFS 6E / RFC 17 1040 Line 53/Schedule R Energy credit* PFS 6E / RFC 17 1040 Line 52, 53, and/or 71 Exemptions claimed PFS 6C 1040 Line 6d Farm profit/loss PFS 7I / RFC 5 1040 Line 18 / Schedule F Federal income taxes due PFS 6E / RFC 17 1040 Line 55 Foreign income PFS 7E or 8C / RFC 6 or 11 1040 Line 21 / Form 2555 Interest, dividends--taxable PFS 7C / RFC 3 1040 Line 8a, 9 / Schedule B Interest--nontaxable PFS 8C / RFC 11 1040 Line 8b Itemized deductions PFS 6D 1040 Line 40 / Schedule A Line 29 Medical, dental expenses PFS 22, 23 / RFC 21 Schedule A, Line 1 Partnership profit / loss PFS 7E or 7I / RFC 5 or 6 1040 Line 17 / Schedule E Line 32

Form 1065 and K-1 Pension income PFS 7E / RFC 6 1040 Line 15, 16a, b / 1099 R box 1, 2a Rental income PFS 7E or 7I / RFC 6 1040 Line 17 / Schedule E Line 26 Salary and wages PFS 7A, 7B / RFC 1, 2 1040 Line 7 / Form W-2 Box 1 S-Corporation profit / loss PFS 7E / RFC 6 1040 Line 17/ Schedule E line 32

Form 1120S and K-1 Self-employment taxes paid PFS 7P / RFC 7, 16 1040 Line 56 / Schedule SE Social security benefits PFS 8B / RFC 10 1040 Line 20a, 20b Tax filing status PFS 6B 1040 Lines 1 – 5 Trust income PFS 7E / RFC 6 1040 Line 17 / Schedule E Line 37 Unemployment compensation PFS 7E / RFC 6 1040 Line 19 Untaxed IRA/Keogh contributions PFS 7F, 7G / RFC 7 1040 Line 28, 32

*Represents a tax credit not reported on the PFS. However, the presence of these credits may not be included in the SSS generated tax allowance; cross-check with RFC #17 and revise using tax owed from 1040, if available.

22222 a Employee’s social security number OMB No. 1545-0008

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation 2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9 10 Dependent care benefits

11 Nonqualified plans 12a C o d e

12bC o d e

12cC o d e

12dC o d e

13 Statutory employee

Retirement plan

Third-party sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20 Locality name

Form W-2 Wage and Tax Statement 2013 Department of the Treasury—Internal Revenue Service

Copy 1—For State, City, or Local Tax Department

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Net wages after pre-tax contributions

mitchell

Sticky Note

For most applicants, Box 3 and Box 5 will be equal. But Box 3 only reflects how much salary/wages are subject to Social Security tax, up to $113,700 . Box 5 could be more than that.

mitchell

Sticky Note

Should not be reported in PFS 6E. Withheld tax is not necessarily the same as total tax.

mitchell

Sticky Note

Add Box 4 + Box 6 for total FICA tax. Double-check against SSS calculated FICA.

mitchell

Sticky Note

A check or "x" here can confirm voluntary pre-tax contributions to retirement plans.

mitchell

Sticky Note

This box may also be used to itemize pre-tax contributions

mitchell

Sticky Note

Generally, codes A-G reflect different type(s) of pre-tax contributions to retirement plans. These contributions should be included as nontaxable income. Box 12 entry code DD represents the cost of employer-sponsored health coverage. The amount is not taxable and is not a pre-tax contribution. Do NOT add back as untaxed income.

mitchell

Sticky Note

An amount listed in Box 12a through 12d with code letters D through G represent pre-tax retirement contributions. This amount should NOT be reported in PFS 7F, 7G, or RFC 7. It should be reported in PFS 8C.

mitchell

Highlight

mitchell

Sticky Note

The W-2 gives total wage income in Box 5, pre-tax contributions in Boxes 12 and 14, and income tax withheld in Box 2.

Form 1099-DIV

2013 Dividends and Distributions

Copy 1

For State Tax Department

Department of the Treasury - Internal Revenue Service

OMB No. 1545-0110 VOID CORRECTED

PAYER’S name, street address, city or town, province or state, country, ZIP or foreign postal code, and telephone no.

PAYER’S federal identification number RECIPIENT’S identification number

RECIPIENT’S name

Street address (including apt. no.)

City or town, province or state, country, and ZIP or foreign postal code

Account number (see instructions)

1a Total ordinary dividends

$ 1b Qualified dividends

$ 2a Total capital gain distr.

$ 2b Unrecap. Sec. 1250 gain

$ 2c Section 1202 gain

$

2d Collectibles (28%) gain

$ 3 Nondividend distributions

$ 4 Federal income tax withheld

$ 5 Investment expenses

$ 6 Foreign tax paid

$

7 Foreign country or U.S. possession

8 Cash liquidation distributions

$ 9 Noncash liquidation distributions

$ 10 Exempt-interest dividends

$

11 Specified private activity bond interest dividends

$ 12 State 13 State identification no. 14 State tax withheld

$ $

Form 1099-DIV www.irs.gov/form1099div

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Form 1040, line 9a/9b Form 1040A, line 9a/9b PFS 7C RFC line 3

mitchell

Sticky Note

This amount is a subset of the amount in box 1a...it does not represent an additional amount of dividend or distribution income.

mitchell

Sticky Note

This form doesn't usually accompany a filed tax return. It details dividends paid as either qualified (0 or 15% tax rate) or nonqualified (taxed as ordinary income). Most dividends qualify for low tax rates.

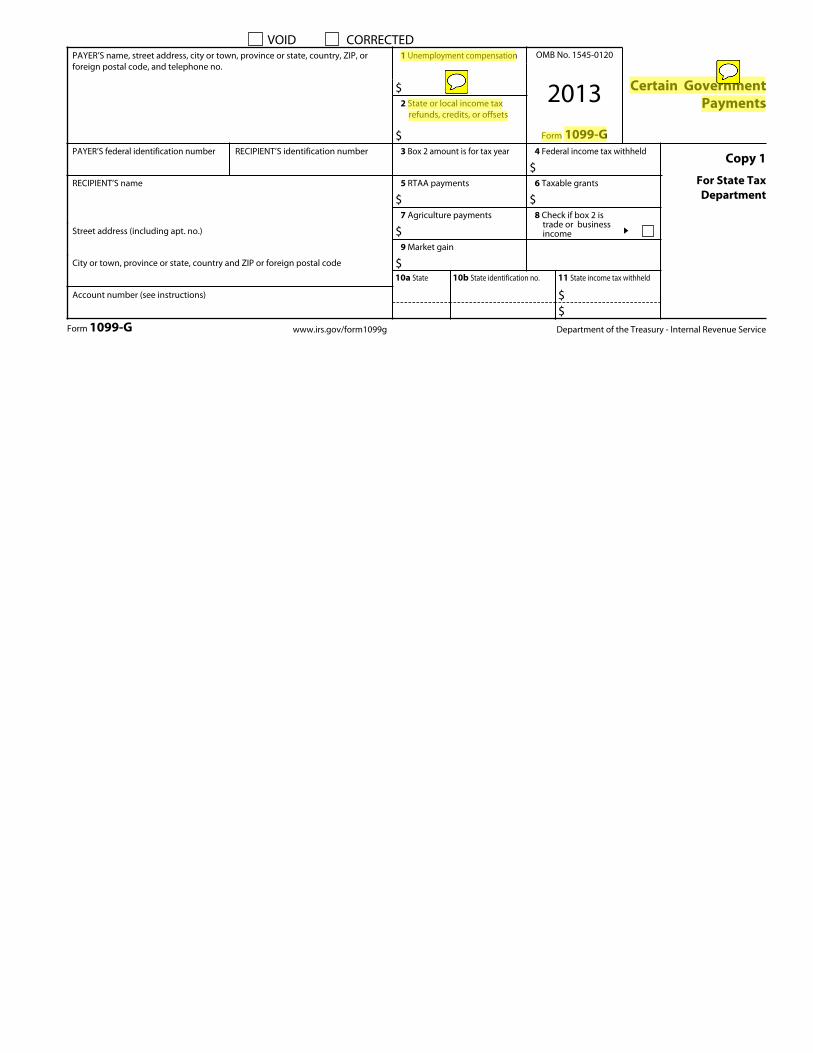

Form 1099-G

2013 Certain Government Payments

Copy 1

For State Tax Department

Department of the Treasury - Internal Revenue Service

OMB No. 1545-0120VOID CORRECTED

PAYER’S name, street address, city or town, province or state, country, ZIP, or foreign postal code, and telephone no.

PAYER’S federal identification number RECIPIENT’S identification number

RECIPIENT’S name

Street address (including apt. no.)

City or town, province or state, country and ZIP or foreign postal code

Account number (see instructions)

1 Unemployment compensation

$2 State or local income tax

refunds, credits, or offsets

$3 Box 2 amount is for tax year 4 Federal income tax withheld

$5 RTAA payments

$6 Taxable grants

$7 Agriculture payments

$8 Check if box 2 is

trade or business income ▶

9 Market gain

$11 State income tax withheld

$10b State identification no.10a State

$Form 1099-G www.irs.gov/form1099g

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

1040 line 19 1040A line 13 RFC line 6 PFS 7E

mitchell

Sticky Note

Generally used to report unemployment compensation, fully taxable in 2013.

Form 1099-INT

2013 Interest Income

Copy 1

For State Tax Department

Department of the Treasury - Internal Revenue Service

OMB No. 1545-0112

VOID CORRECTEDPAYER’S name, street address, city or town, province or state, country, ZIP or foreign postal code, and telephone no.

PAYER’S federal identification number RECIPIENT’S identification number

RECIPIENT’S name

Street address (including apt. no.)

City or town, province or state, country, and ZIP or foreign postal code

Account number (see instructions)

Payer's RTN (optional)

1 Interest income

$2 Early withdrawal penalty

$3 Interest on U.S. Savings Bonds and Treas. obligations

$4 Federal income tax withheld

$

5 Investment expenses

$6 Foreign tax paid

$

7 Foreign country or U.S. possession

8 Tax-exempt interest

$

9 Specified private activity bond interest

$10 Tax-exempt bond CUSIP no. 11 State 12 State identification no. 13 State tax withheld

$$

Form 1099-INT www.irs.gov/form1099int

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Form 1040 line 8a Form 1040A line 8a RFC line 3 PFS 7C

mitchell

Sticky Note

Issued by banks, brokerage firms, and money market funds. Interest rates are typically below 1%, so it may require $10,000 in the bank to generate $100 of interest income.

Form 1099-MISC

2013 Miscellaneous Income

Copy 1For State Tax Department

Department of the Treasury - Internal Revenue Service

OMB No. 1545-0115VOID CORRECTED

PAYER’S name, street address, city or town, province or state, country, ZIP or foreign postal code, and telephone no.

PAYER’S federal identification number RECIPIENT’S identification number

RECIPIENT’S name

Street address (including apt. no.)

City or town, province or state, country, and ZIP or foreign postal code

Account number (see instructions)

15a Section 409A deferrals

$

15b Section 409A income

$

1 Rents

$2 Royalties

$3 Other income

$4 Federal income tax withheld

$5 Fishing boat proceeds

$

6 Medical and health care payments

$7 Nonemployee compensation

$

8 Substitute payments in lieu of dividends or interest

$9 Payer made direct sales of

$5,000 or more of consumer products to a buyer (recipient) for resale ▶

10 Crop insurance proceeds

$11 Foreign tax paid

$12 Foreign country or U.S. possession

13 Excess golden parachute payments

$

14 Gross proceeds paid to an attorney

$16 State tax withheld

$$

17 State/Payer’s state no. 18 State income

$$

Form 1099-MISC www.irs.gov/form1099misc

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

1040 line 12 or 17 PFS 7I RFC line 5

mitchell

Sticky Note

Generally no income tax or FICA has been withheld. Doesn't necessarily mean they don't owe taxes if this is zero.

mitchell

Sticky Note

Many self-employed people (e.g., doctors, lawyers, real estate brokers) receive income reported on this form. Generally, no income tax or FICA tax has been withheld. You will generally not receive this form with the 1040, but the amounts will be included on Schedule C and/or Schedule E.

Form 1099-R

2013

Distributions From Pensions, Annuities, Retirement or

Profit-Sharing Plans, IRAs, Insurance

Contracts, etc.

Copy 1 For

State, City, or Local

Tax Department

Department of the Treasury - Internal Revenue Service

OMB No. 1545-0119VOID CORRECTED

PAYER’S name, street address, city or town, province or state, country, and ZIP or foreign postal code

PAYER’S federal identification number

RECIPIENT’S identification number

RECIPIENT’S name

Street address (including apt. no.)

City or town, province or state, country, and ZIP or foreign postal code

10 Amount allocable to IRR within 5 years

$

11 1st year of desig. Roth contrib.

Account number (see instructions)

1 Gross distribution

$2a Taxable amount

$2b Taxable amount

not determinedTotal distribution

3 Capital gain (included in box 2a)

$

4 Federal income tax withheld

$5 Employee contributions

/Designated Roth contributions or insurance premiums

$

6 Net unrealized appreciation in employer’s securities

$7 Distribution code(s)

IRA/ SEP/ SIMPLE

8 Other

$ %9a Your percentage of total

distribution %

9b Total employee contributions

$12 State tax withheld

$$

13 State/Payer’s state no. 14 State distribution

$$

15 Local tax withheld

$$

16 Name of locality 17 Local distribution

$$

Form 1099-R www.irs.gov/form1099r

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Form 1040 line 15a or 16a Form 1040A line 11a or 12a

mitchell

Sticky Note

Form 1040 line 15b or 16b Form 1040A line 11b or 12b If "0," then that usually indicates a tax-free rollover from one plan to another often due to a job change. This means the applicant did not actually receive any money.

mitchell

Sticky Note

Distributions prior to age 59.5 are subject to 10% additional tax, which shows on 1040 line 58. This usually indicates the the applicant may have had financial hardship requiring withdrawal.

mitchell

Sticky Note

Generally this form will be included with the tax filing because income taxes are withheld on pension distributions

mitchell

Highlight

mitchell

Sticky Note

Refer to the codes on the next page to help determine if the taxpayer took possession of the distribution.

1—Early distribution, no known exception (in most cases, under age 59½).2—Early distribution, exception applies (under age 59½).3—Disability.4—Death.5—Prohibited transaction.6—Section 1035 exchange (a tax-free exchange of life insurance, annuity,

qualified long-term care insurance, or endowment contracts).7—Normal distribution.8—Excess contributions plus earnings/excess deferrals (and/or earnings)

taxable in 2013.9—Cost of current life insurance protection.A—May be eligible for 10-year tax option (see Form 4972).B—Designated Roth account distribution.

Note. If Code B is in box 7 and an amount is reported in box 10, see the instructions for Form 5329.D—Annuity payments from nonqualified annuities that may be subject to tax under section 1411.

Box 7. The following codes identify the distribution you received. For more information on these distributions, see the instructions for your tax return. Also, certain distributions may be subject to an additional 10% tax. See the instructions for Form 5329.

E—Distributions under Employee Plans Compliance Resolution System (EPCRS).

F—Charitable gift annuity.

If the IRA/SEP/SIMPLE box is checked, you have received a traditional IRA, SEP, or SIMPLE distribution.

W—Charges or payments for purchasing qualified long-term care insurance contracts under combined arrangements.

Note. This distribution is not eligible for rollover.U—Dividend distribution from ESOP under sec. 404(k).T—Roth IRA distribution, exception applies.

S—Early distribution from a SIMPLE IRA in first 2 years, no known exception (under age 59½).

R—Recharacterized IRA contribution made for 2012 and recharacterized in 2013.

Q—Qualified distribution from a Roth IRA.

P—Excess contributions plus earnings/excess deferrals (and/or earnings) taxable in 2012.

N—Recharacterized IRA contribution made for 2013 and recharacterized in 2013.

L—Loans treated as distributions.

J—Early distribution from a Roth IRA, no known exception (in most cases, under age 59½).

H—Direct rollover of a designated Roth account distribution to a Roth IRA.

G—Direct rollover of a distribution (other than a designated Roth account distribution) to a qualified plan, a section 403(b) plan, a governmental section 457(b) plan, or an IRA.

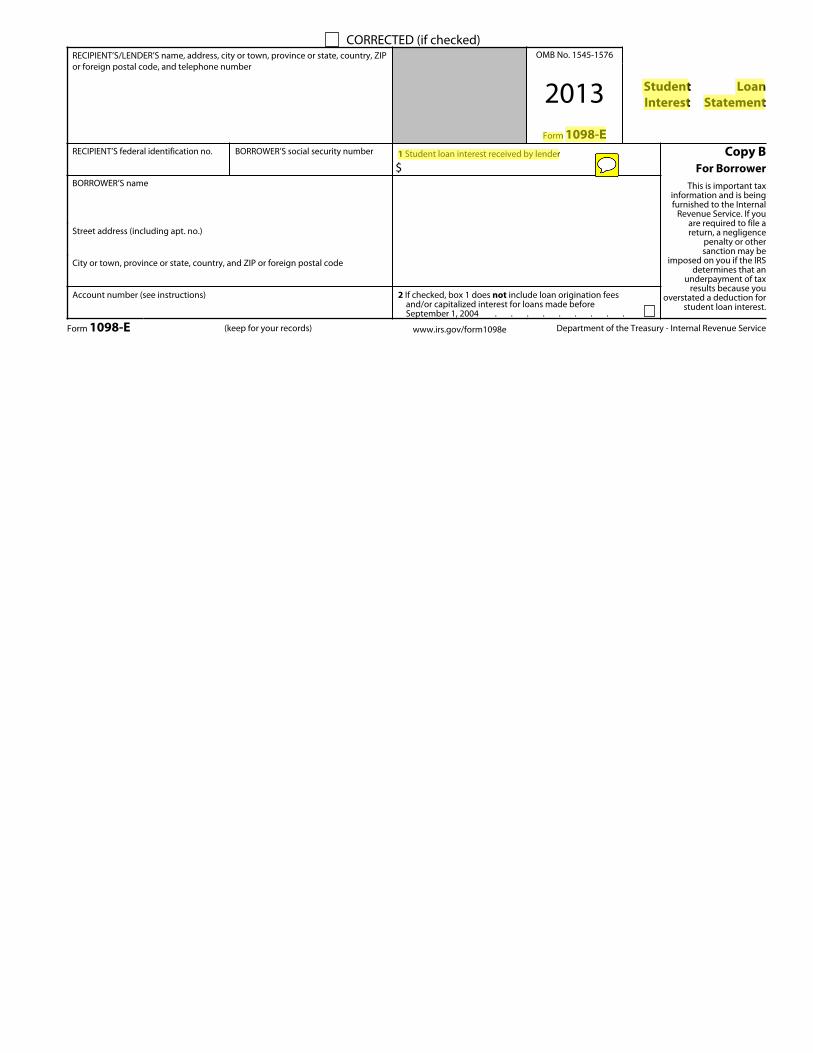

Form 1098-E

2013 Student Loan Interest Statement

Copy BFor Borrower

Department of the Treasury - Internal Revenue Service

This is important tax information and is being furnished to the Internal

Revenue Service. If you are required to file a return, a negligence

penalty or other sanction may be

imposed on you if the IRS determines that an

underpayment of tax results because you

overstated a deduction for student loan interest.

OMB No. 1545-1576CORRECTED (if checked)

RECIPIENT’S/LENDER’S name, address, city or town, province or state, country, ZIP or foreign postal code, and telephone number

RECIPIENT’S federal identification no. BORROWER’S social security number

BORROWER’S name

Street address (including apt. no.)

City or town, province or state, country, and ZIP or foreign postal code

Account number (see instructions)

1 Student loan interest received by lender

$

2 If checked, box 1 does not include loan origination fees and/or capitalized interest for loans made before September 1, 2004 . . . . . . . . .

Form 1098-E (keep for your records) www.irs.gov/form1098e

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Interest paid by borrower. Appears on 1040 line 33, 1040A line 18. An above the line deduction that affects taxable income and tax paid. Should be included in PFS 7H, RFC line 7.

Form 1098-T

2013 Tuition Statement

Copy BFor Student

Department of the Treasury - Internal Revenue Service

This is important tax information and is

being furnished to the Internal Revenue

Service.

OMB No. 1545-1574CORRECTED

FILER’S name, street address, city or town, province or state, country, ZIP or foreign postal code, and telephone number

FILER’S federal identification no. STUDENT'S social security number

STUDENT'S name

Street address (including apt. no.)

City or town, province or state, country, and ZIP or foreign postal code

Service Provider/Acct. No. (see instr.)

1 Payments received for qualified tuition and related expenses

$2 Amounts billed for

qualified tuition and related expenses

$3 If this box is checked, your educational institution has

changed its reporting method for 2013

4 Adjustments made for a prior year

$

5 Scholarships or grants

$6 Adjustments to

scholarships or grants for a prior year

$

7 Checked if the amount in box 1 or 2 includes amounts for an academic period beginning January - March 2014 ▶

8 Check if at least half-

time student

9 Checked if a graduate

student . . . .

10 Ins. contract reimb./refund

$Form 1098-T (keep for your records) www.irs.gov/form1098t

mitchell

Highlight

mitchell

Sticky Note

Amounts entered in Box 1 or 2 minus any amount in Box 5 will give an idea of actual tuition paid

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Does the PFS indicate sibling(s) in college?

mitchell

Sticky Note

American Opportunity Credit up to $2,500. Lifetime Learning Credit up to $2,000. Can be useful for documenting payments to college, university, etc., especially if PFS indicates a sibling enrolled in college.

mitchell

Sticky Note

1040 line 49 and line 66 1040A line 31 and line 40 PFS 6E, RFC 17

Form 1040 Department of the Treasury—Internal Revenue Service

OMB No. 1545-0074

(99)

IRS Use Only—Do not write or staple in this space. U.S. Individual Income Tax Return 2013For the year Jan. 1–Dec. 31, 2013, or other tax year beginning , 2013, ending , 20 See separate instructions.Your first name and initial Last name Your social security number

If a joint return, spouse’s first name and initial Last name Spouse’s social security number

▲ Make sure the SSN(s) above and on line 6c are correct.

Home address (number and street). If you have a P.O. box, see instructions. Apt. no.

City, town or post office, state, and ZIP code. If you have a foreign address, also complete spaces below (see instructions).

Foreign country name Foreign province/state/county Foreign postal code

Presidential Election Campaign

Check here if you, or your spouse if filing jointly, want $3 to go to this fund. Checking a box below will not change your tax or refund. You Spouse

Filing Status

Check only one box.

1 Single

2 Married filing jointly (even if only one had income)

3 Married filing separately. Enter spouse’s SSN above and full name here. ▶

4 Head of household (with qualifying person). (See instructions.) If

the qualifying person is a child but not your dependent, enter this

child’s name here. ▶

5 Qualifying widow(er) with dependent child

Exemptions 6a Yourself. If someone can claim you as a dependent, do not check box 6a . . . . .

b Spouse . . . . . . . . . . . . . . . . . . . . . . . .}

c Dependents: (1) First name Last name

(2) Dependent’s social security number

(3) Dependent’s relationship to you

(4) ✓ if child under age 17 qualifying for child tax credit

(see instructions)

If more than four dependents, see instructions and check here ▶

d Total number of exemptions claimed . . . . . . . . . . . . . . . . .

Boxes checked on 6a and 6bNo. of children on 6c who: • lived with you • did not live with you due to divorce or separation (see instructions)

Dependents on 6c not entered above

Add numbers on lines above ▶

Income

Attach Form(s) W-2 here. Also attach Forms W-2G and 1099-R if tax was withheld.

If you did not get a W-2, see instructions.

7 Wages, salaries, tips, etc. Attach Form(s) W-2 . . . . . . . . . . . . 7

8a Taxable interest. Attach Schedule B if required . . . . . . . . . . . . 8a

b Tax-exempt interest. Do not include on line 8a . . . 8b

9 a Ordinary dividends. Attach Schedule B if required . . . . . . . . . . . 9a

b Qualified dividends . . . . . . . . . . . 9b

10 Taxable refunds, credits, or offsets of state and local income taxes . . . . . . 10

11 Alimony received . . . . . . . . . . . . . . . . . . . . . 11

12 Business income or (loss). Attach Schedule C or C-EZ . . . . . . . . . . 12

13 Capital gain or (loss). Attach Schedule D if required. If not required, check here ▶ 13

14 Other gains or (losses). Attach Form 4797 . . . . . . . . . . . . . . 14

15 a IRA distributions . 15a b Taxable amount . . . 15b

16 a Pensions and annuities 16a b Taxable amount . . . 16b

17 Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E 17

18 Farm income or (loss). Attach Schedule F . . . . . . . . . . . . . . 18

19 Unemployment compensation . . . . . . . . . . . . . . . . . 19

20 a Social security benefits 20a b Taxable amount . . . 20b

21 Other income. List type and amount 21 22 Combine the amounts in the far right column for lines 7 through 21. This is your total income ▶ 22

Adjusted Gross Income

23 Educator expenses . . . . . . . . . . 23

24 Certain business expenses of reservists, performing artists, and fee-basis government officials. Attach Form 2106 or 2106-EZ 24

25 Health savings account deduction. Attach Form 8889 . 25

26 Moving expenses. Attach Form 3903 . . . . . . 26

27 Deductible part of self-employment tax. Attach Schedule SE . 27

28 Self-employed SEP, SIMPLE, and qualified plans . . 28

29 Self-employed health insurance deduction . . . . 29

30 Penalty on early withdrawal of savings . . . . . . 30

31 a Alimony paid b Recipient’s SSN ▶ 31a

32 IRA deduction . . . . . . . . . . . . . 32

33 Student loan interest deduction . . . . . . . . 33

34 Tuition and fees. Attach Form 8917 . . . . . . . 34

35 Domestic production activities deduction. Attach Form 8903 35

36 Add lines 23 through 35 . . . . . . . . . . . . . . . . . . . 36 37 Subtract line 36 from line 22. This is your adjusted gross income . . . . . ▶ 37

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11320B Form 1040 (2013)

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Probably the most important form to review. Lines 7-21 represent taxable income; lines 23-35 represent IRS allowable adjustments to taxable income or "above the line" deductions. Remember the purpose of the form is to determine taxable income.

mitchell

Highlight

mitchell

Sticky Note

Double-check against PFS 6B

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Be sure to collect the tax form from the person who is claiming your student aid applicant as a dependent. In non/co-custodial arrangements, the student cannot be claimed by both parents.

mitchell

Sticky Note

Double check against PFS 6C

mitchell

Sticky Note

PFS 7A + 7B RFC line 1+ 2

mitchell

Highlight

mitchell

Sticky Note

Line 7 combines the salary/wages of both parents, if married. Must collect the W2's to see individual parent earnings from work.

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

This sum, minus lines 28 and 32, should be reported on PFS 7H

mitchell

Sticky Note

Detail on Form 8917 reflects tuition paid, grants/scholarships received for higher education.

mitchell

Sticky Note

NOT from W2, Box 12 PFS 7F RFC line 7

mitchell

Sticky Note

If paid to the student's other parent, be sure he/she reports it as income. No need to account for it as "Unusual Expenses," if reported here.

mitchell

Sticky Note

Not on W2 Box 12 PFS 7G RFC Line 7

mitchell

Highlight

mitchell

Sticky Note

For self-employed, sole proprietors. Compare against SSS-calculated FICA tax and SE tax on 1040.

mitchell

Sticky Note

Allowable adjustments to taxable income. Should be reported on the PFS "Other Adjustments to Income" section.

mitchell

Sticky Note

Not on PFS, not on RFC SSS "Total Income" is not equivalent to IRS "Total Income." One main difference is that the SSS "Total Income" includes nontaxable income, which IRS forms don't track to the same degree.

mitchell

Sticky Note

NOT children's benefits Difference between 20a and 20b is nontaxable income, and should be included in PFS 8B.

mitchell

Sticky Note

PFS 8B RFC 10

mitchell

Sticky Note

PFS 7E RFC line 6

mitchell

Sticky Note

Will often result in losses. Review detail on Sch F to determine if any write-offs are not allowable for financial aid review.

mitchell

Sticky Note

PFS 7E RFC line 6 Should NOT be included as business profit.

mitchell

Sticky Note

Line 17 amount should be included in PFS 7E, RFC line 6. This should NOT be included as business profit on the PFS.

mitchell

Highlight

mitchell

Sticky Note

Entries represent withdrawals from retirement accounts; consider if there were hardship or discretionary factors at play if early withdrawals are made. Refer to Form 1099R Box 7 to determine if amounts were received by the taxpayer or rolled into another plan.

mitchell

Sticky Note

Can be potentially time-intensive to review! Be sure you have the Sch E for needed details.

mitchell

Sticky Note

Lines 15b+ 16b should be included on: PFS 7E RFC line 6 Refer to Form 1099R Box 7 to determine if amounts were received by the taxpayer or rolled into another plan.

mitchell

Sticky Note

Sale of equipment by a business

mitchell

Sticky Note

PFS 7E RFC 6

mitchell

Sticky Note

Review Sch D for details on amounts of assets that were exchanged or sold.

mitchell

Highlight

mitchell

Sticky Note

May require professional judgment on write-offs not allowable for financial aid review, such as depreciation or business use of home.

mitchell

Sticky Note

PFS 7I RFC 5

mitchell

Sticky Note

May be from more than one payor, if the parent was divorced more than once.

mitchell

Sticky Note

PFS 7D RFC line 4

mitchell

Sticky Note

From 1099-G PFS 7E RFC line 6

mitchell

Sticky Note

Does not represent additional dividend income. Reflects portion of the amount in 9a that is "qualified." No action or additional review is necessary.

mitchell

Sticky Note

8a+9a should be reported as one number on PFS 7C, RFC line 3

mitchell

Sticky Note

Nontaxable income that should be reported in PFS 8C

mitchell

Sticky Note

As reported on 1099 DIV

mitchell

Sticky Note

As reported on 1099 INT

mitchell

Highlight

Form 1040 (2013) Page 2

Tax and Credits

38 Amount from line 37 (adjusted gross income) . . . . . . . . . . . . . . 38

39a Check if:

{ You were born before January 2, 1949, Blind.

Spouse was born before January 2, 1949, Blind.} Total boxes

checked ▶ 39a

b If your spouse itemizes on a separate return or you were a dual-status alien, check here ▶ 39b Standard Deduction for— • People who check any box on line 39a or 39b or who can be claimed as a dependent, see instructions. • All others: Single or Married filing separately, $6,100 Married filing jointly or Qualifying widow(er), $12,200 Head of household, $8,950

40 Itemized deductions (from Schedule A) or your standard deduction (see left margin) . . 40

41 Subtract line 40 from line 38 . . . . . . . . . . . . . . . . . . . 41

42 Exemptions. If line 38 is $150,000 or less, multiply $3,900 by the number on line 6d. Otherwise, see instructions 42

43 Taxable income. Subtract line 42 from line 41. If line 42 is more than line 41, enter -0- . . 43

44 Tax (see instructions). Check if any from: a Form(s) 8814 b Form 4972 c 44

45 Alternative minimum tax (see instructions). Attach Form 6251 . . . . . . . . . 45

46 Add lines 44 and 45 . . . . . . . . . . . . . . . . . . . . . ▶ 46

47 Foreign tax credit. Attach Form 1116 if required . . . . 47

48 Credit for child and dependent care expenses. Attach Form 2441 48

49 Education credits from Form 8863, line 19 . . . . . 49

50 Retirement savings contributions credit. Attach Form 8880 50

51 Child tax credit. Attach Schedule 8812, if required . . . 51

52 Residential energy credits. Attach Form 5695 . . . . 52

53 Other credits from Form: a 3800 b 8801 c 53

54 Add lines 47 through 53. These are your total credits . . . . . . . . . . . . 5455 Subtract line 54 from line 46. If line 54 is more than line 46, enter -0- . . . . . . ▶ 55

Other Taxes

56 Self-employment tax. Attach Schedule SE . . . . . . . . . . . . . . . 56

57 Unreported social security and Medicare tax from Form: a 4137 b 8919 . . 57

58 Additional tax on IRAs, other qualified retirement plans, etc. Attach Form 5329 if required . . 58

59a 59a

b 59bHousehold employment taxes from Schedule H . . . . . . . . . . . . . .

First-time homebuyer credit repayment. Attach Form 5405 if required . . . . . . . .

60 Taxes from: a Form 8959 b Form 8960 c Instructions; enter code(s) 60

61 Add lines 55 through 60. This is your total tax . . . . . . . . . . . . . ▶ 61

Payments 62 Federal income tax withheld from Forms W-2 and 1099 . . 62

63 2013 estimated tax payments and amount applied from 2012 return 63If you have a qualifying child, attach Schedule EIC.

64a Earned income credit (EIC) . . . . . . . . . . 64a

b Nontaxable combat pay election 64b

65 Additional child tax credit. Attach Schedule 8812 . . . . . 65

66 American opportunity credit from Form 8863, line 8 . . . . 66

67 Reserved . . . . . . . . . . . . . . . . 67

68 Amount paid with request for extension to file . . . . . 68

69 Excess social security and tier 1 RRTA tax withheld . . . . 69

70 Credit for federal tax on fuels. Attach Form 4136 . . . . 70

71 Credits from Form: a 2439 b Reserved c 8885 d 7172 Add lines 62, 63, 64a, and 65 through 71. These are your total payments . . . . . ▶ 72

Refund

Direct deposit? See instructions.

73 If line 72 is more than line 61, subtract line 61 from line 72. This is the amount you overpaid 73

74a Amount of line 73 you want refunded to you. If Form 8888 is attached, check here . ▶ 74a ▶

▶

b Routing number ▶ c Type: Checking Savings

d Account number

75 Amount of line 73 you want applied to your 2014 estimated tax ▶ 75Amount You Owe

76 Amount you owe. Subtract line 72 from line 61. For details on how to pay, see instructions ▶ 76

77 Estimated tax penalty (see instructions) . . . . . . . 77

Third Party Designee

Do you want to allow another person to discuss this return with the IRS (see instructions)? Yes. Complete below. No

Designee’s name ▶

Phone no. ▶

Personal identification number (PIN) ▶

Sign Here Joint return? See instructions. Keep a copy for your records.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Your signature Date Your occupation Daytime phone number

Spouse’s signature. If a joint return, both must sign.

▲

Date Spouse’s occupation If the IRS sent you an Identity Protection PIN, enter it here (see inst.)

Paid Preparer Use Only

Print/Type preparer’s name Preparer’s signature Date Check if self-employed

PTIN

Firm’s name ▶

Firm’s address ▶

Firm's EIN ▶

Phone no.

Form 1040 (2013)

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

PFS 6D

mitchell

Sticky Note

Tentative income tax before credits below are accounted for. Do not use this figure. SSS does not use this number to verify federal income tax allowance.

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

These credits will lower federal income tax due. Will impact PFS 6E and RFC line 17. May require overriding SSS-calculated tax allowance, since SSS doesn't assume that any possible credits may be claimed.

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Similar to FICA for self-employed; amount listed on 1040 line 27 and SSS FICA calculation on business profit should equal the amount reported here.

mitchell

Sticky Note

RFC lines 17+18 PFS 6E + 7P SSS federal tax allowance should reflect line 61 MINUS line 56. You may have to override the calculated allowance.

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

These three additional refundable credits should either be reported as untaxed income or subtracted from tax due.

mitchell

Highlight

mitchell

Sticky Note

Tax refunds are not income. Represent money withheld that is coming back to you, except the amount of the refund driven by the refundable tax credits in lines 64a-66 above.

Form

1040A 2013U.S. Individual Income Tax ReturnDepartment of the Treasury—Internal Revenue Service

IRS Use Only—Do not write or staple in this space. (99)

OMB No. 1545-0074Your first name and initial Last name

Your social security number

If a joint return, spouse’s first name and initial Last name Spouse’s social security number

▲ Make sure the SSN(s) above and on line 6c are correct.

Home address (number and street). If you have a P.O. box, see instructions. Apt. no.

City, town or post office, state, and ZIP code. If you have a foreign address, also complete spaces below (see instructions).

Foreign country name Foreign province/state/county Foreign postal code

Presidential Election CampaignCheck here if you, or your spouse if filing jointly, want $3 to go to this fund. Checking a box below will not change your tax or refund. You Spouse

Filing status Check only one box.

1 Single2 Married filing jointly (even if only one had income)3 Married filing separately. Enter spouse’s SSN above and

full name here. ▶

4 Head of household (with qualifying person). (See instructions.) If the qualifying person is a child but not your dependent, enter this child’s name here. ▶

5 Qualifying widow(er) with dependent child (see instructions)

Exemptions 6a Yourself. If someone can claim you as a dependent, do not check box 6a.

b Spouse}

c Dependents:

(1) First name Last name

(2) Dependent’s social security number

(3) Dependent’s relationship to you

(4) ✓ if child under age 17 qualifying for child tax credit (see

instructions)If more than six dependents, see instructions.

d Total number of exemptions claimed.

Boxes checked on 6a and 6bNo. of children on 6c who: • lived with you

• did not live with you due to divorce or separation (see instructions)

Dependents on 6c not entered above

Add numbers on lines above ▶

Income Attach Form(s) W-2 here. Also attach Form(s) 1099-R if tax was withheld. If you did not get a W-2, see instructions.

7 Wages, salaries, tips, etc. Attach Form(s) W-2. 7

8a Taxable interest. Attach Schedule B if required. 8ab Tax-exempt interest. Do not include on line 8a. 8b

9a Ordinary dividends. Attach Schedule B if required. 9ab Qualified dividends (see instructions). 9b

10 Capital gain distributions (see instructions). 1011 a IRA

distributions. 11a11b Taxable amount

(see instructions). 11b12 a Pensions and

annuities. 12a12b Taxable amount

(see instructions). 12b

13 Unemployment compensation and Alaska Permanent Fund dividends. 1314 a Social security

benefits. 14a14b Taxable amount

(see instructions). 14b

15 Add lines 7 through 14b (far right column). This is your total income. ▶ 15Adjusted gross income

16 Educator expenses (see instructions). 1617 IRA deduction (see instructions). 1718 Student loan interest deduction (see instructions). 18

19 Tuition and fees. Attach Form 8917. 1920 Add lines 16 through 19. These are your total adjustments. 20

21 Subtract line 20 from line 15. This is your adjusted gross income. ▶ 21For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11327A Form 1040A (2013)

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Generally, this "simpler" form is for those applicants who do not itemize deductions and have taxable income less than $100,000. Remember the purpose of this form is to determine taxable income.

mitchell

Highlight

mitchell

Sticky Note

PFS 6B

mitchell

Highlight

mitchell

Sticky Note

Be sure to collect the tax form from the person who is claiming the student applicant as a dependent deduction. Keep in mind that in the case of non- or co-custodial parents, only one of the parents can claim each child.

mitchell

Highlight

mitchell

Sticky Note

PFS 6C

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

PFS 7A + 7B RFC lines 1 + 2

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

The total of 8a + 9a should be reported on PFS 7C RFC line 3

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Should be included as non-taxable income in PFS 8C

mitchell

Sticky Note

Does not represent additional income. Reflects a portion of the amount reported in 9a. No action needed on any amounts here.

mitchell

Sticky Note

1099-R reports IRA and pension distributions and tax withheld, if any, from them.

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

May be a hardship issue if distribution is taxed due to early withdrawal. May be a rollover if distribution is untaxed. Refer to Form 1099R Box 7 to determine if amounts were received by the taxpayer or rolled into another plan.

mitchell

Sticky Note

Amounts in these lines 11b and 12b should be reported on PFS 7E, RFC line 6 Refer to Form 1099R Box 7 to determine if amounts were received by the taxpayer or rolled into another plan.

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Does not reflect any benefits paid to children. Difference between 14a and 14b is nontaxable amount, which should be reported in PFS 8B.

mitchell

Sticky Note

PFS 7E RFC line 6

mitchell

Sticky Note

PFS 8B RFC line 10

mitchell

Sticky Note

NOT the same as RFC line 8, which is okay. SSS "total income" is not the same as IRS "total income." One major difference is that SSS includes nontaxable income when calculating Total Income.

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

This deduction is not the same as the pre-tax contributions reported on the W2. Should be reported on the PFS 7F, RFC line 7. Avoid double counting retirement contributions.

mitchell

Sticky Note

NOT the same as RFC line 8.

Form 1040A (2013) Page 2Tax, credits, and payments

22 Enter the amount from line 21 (adjusted gross income). 2223 a Check

if: { You were born before January 2, 1949, BlindSpouse was born before January 2, 1949, Blind }Total boxes

checked ▶ 23ab If you are married filing separately and your spouse itemizes

deductions, check here ▶ 23bStandard Deduction for— • People who check any box on line 23a or 23b or who can be claimed as a dependent, see instructions. • All others: Single or Married filing separately, $6,100 Married filing jointly or Qualifying widow(er), $12,200 Head of household, $8,950

24 Enter your standard deduction. 2425 Subtract line 24 from line 22. If line 24 is more than line 22, enter -0-. 2526 Exemptions. Multiply $3,900 by the number on line 6d. 2627 Subtract line 26 from line 25. If line 26 is more than line 25, enter -0-.

This is your taxable income. ▶ 2728 Tax, including any alternative minimum tax (see instructions). 2829 Credit for child and dependent care expenses. Attach

Form 2441. 2930 Credit for the elderly or the disabled. Attach

Schedule R. 3031 Education credits from Form 8863, line 19. 3132 Retirement savings contributions credit. Attach

Form 8880. 3233 Child tax credit. Attach Schedule 8812, if required. 3334 Add lines 29 through 33. These are your total credits. 3435 Subtract line 34 from line 28. If line 34 is more than line 28, enter -0-. This is

your total tax. 3536 Federal income tax withheld from Forms W-2 and

1099. 3637 2013 estimated tax payments and amount applied

from 2012 return. 37If you have a qualifying child, attach Schedule EIC.

38a Earned income credit (EIC). 38ab Nontaxable combat pay

election. 38b39 Additional child tax credit. Attach Schedule 8812. 3940 American opportunity credit from Form 8863, line 8. 4041 Add lines 36, 37, 38a, 39, and 40. These are your total payments. ▶ 41

Refund Direct deposit? See instructions and fill in 43b, 43c, and 43d or Form 8888.

42 If line 41 is more than line 35, subtract line 35 from line 41. This is the amount you overpaid. 42

43a Amount of line 42 you want refunded to you. If Form 8888 is attached, check here ▶ 43a

▶ b Routing number

▶ c Type: Checking Savings

▶ d Account number

44 Amount of line 42 you want applied to your 2014 estimated tax. 44

Amount you owe

45 Amount you owe. Subtract line 41 from line 35. For details on how to pay, see instructions. ▶ 45

46 Estimated tax penalty (see instructions). 46

Third party designee

Do you want to allow another person to discuss this return with the IRS (see instructions)? Yes. Complete the following. No

Designee’s name ▶

Phone no. ▶

Personal identification number (PIN) ▶

Sign here Joint return? See instructions. Keep a copy for your records.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and accurately list all amounts and sources of income I received during the tax year. Declaration of preparer (other than the taxpayer) is based on all information of which the preparer has any knowledge.▲ Your signature Date Your occupation Daytime phone number

Spouse’s signature. If a joint return, both must sign. Date Spouse’s occupation If the IRS sent you an Identity Protection PIN, enter it here (see inst.)

Paid preparer use only

Print/type preparer's name Preparer’s signature DateCheck ▶ if self-employed

PTIN

Firm's name ▶

Firm's address ▶

Firm's EIN ▶

Phone no.

Form 1040A (2013)

mitchell

Highlight

mitchell

Sticky Note

1040A filers cannot itemize; must use the standard deduction.

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

Tentative tax before credits

mitchell

Highlight

mitchell

Sticky Note

These credits are not factored into the SSS-calculated federal tax allowance. These credits will reduce income tax due. May require an override to the SSS-derived federal income tax on RFC line 17 and the parent-reported value on PFS 6E.

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

From W2 box 2. Does not represent tax paid.

mitchell

Sticky Note

Capture items 38a, 39, and 40 as either untaxed income or subtract from income tax due. These are refundable tax credits.

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

NOT income! Do not add in anywhere.

SCHEDULE A (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Itemized Deductions▶ Information about Schedule A and its separate instructions is at www.irs.gov/schedulea.

▶ Attach to Form 1040.

OMB No. 1545-0074

2013Attachment Sequence No. 07

Name(s) shown on Form 1040 Your social security number

Medical and Dental Expenses

Caution. Do not include expenses reimbursed or paid by others. 1 Medical and dental expenses (see instructions) . . . . . 1 2 Enter amount from Form 1040, line 38 2 3 Multiply line 2 by 10% (.10). But if either you or your spouse was

born before January 2, 1949, multiply line 2 by 7.5% (.075) instead 3 4 Subtract line 3 from line 1. If line 3 is more than line 1, enter -0- . . . . . . . . 4

Taxes You Paid

5 State and local (check only one box):a Income taxes, orb General sales taxes } . . . . . . . . . . . 5

6 Real estate taxes (see instructions) . . . . . . . . . 6 7 Personal property taxes . . . . . . . . . . . . . 7 8 Other taxes. List type and amount ▶

8 9 Add lines 5 through 8 . . . . . . . . . . . . . . . . . . . . . . 9

Interest You Paid

Note. Your mortgage interest deduction may be limited (see instructions).

10 Home mortgage interest and points reported to you on Form 1098 10 11

Home mortgage interest not reported to you on Form 1098. If paid to the person from whom you bought the home, see instructions and show that person’s name, identifying no., and address ▶

11 12

Points not reported to you on Form 1098. See instructions for special rules . . . . . . . . . . . . . . . . . 12

13 Mortgage insurance premiums (see instructions) . . . . . 13 14 Investment interest. Attach Form 4952 if required. (See instructions.) 14 15 Add lines 10 through 14 . . . . . . . . . . . . . . . . . . . . . 15

Gifts to CharityIf you made a gift and got a benefit for it, see instructions.

16

Gifts by cash or check. If you made any gift of $250 or more, see instructions . . . . . . . . . . . . . . . . 16

17

Other than by cash or check. If any gift of $250 or more, see instructions. You must attach Form 8283 if over $500 . . . 17

18 Carryover from prior year . . . . . . . . . . . . 1819 Add lines 16 through 18 . . . . . . . . . . . . . . . . . . . . . 19

Casualty and Theft Losses 20 Casualty or theft loss(es). Attach Form 4684. (See instructions.) . . . . . . . . 20 Job Expenses and Certain Miscellaneous Deductions

21

Unreimbursed employee expenses—job travel, union dues, job education, etc. Attach Form 2106 or 2106-EZ if required. (See instructions.) ▶ 21

22 Tax preparation fees . . . . . . . . . . . . . 22 23

Other expenses—investment, safe deposit box, etc. List type and amount ▶

23 24 Add lines 21 through 23 . . . . . . . . . . . . 24 25 Enter amount from Form 1040, line 38 25 26 Multiply line 25 by 2% (.02) . . . . . . . . . . . 26 27 Subtract line 26 from line 24. If line 26 is more than line 24, enter -0- . . . . . . 27

Other Miscellaneous Deductions

28 Other—from list in instructions. List type and amount ▶

28 Total Itemized Deductions

29

Is Form 1040, line 38, over $150,000?

29 No. Your deduction is not limited. Add the amounts in the far right column for lines 4 through 28. Also, enter this amount on Form 1040, line 40. } . .Yes. Your deduction may be limited. See the Itemized Deductions Worksheet in the instructions to figure the amount to enter.

30

If you elect to itemize deductions even though they are less than your standard deduction, check here . . . . . . . . . . . . . . . . . . . ▶

For Paperwork Reduction Act Notice, see Form 1040 instructions. Cat. No. 17145C Schedule A (Form 1040) 2013

mitchell

Highlight

mitchell

Sticky Note

If 1040 line 40 is greater than $11,600 this Schedule must be filed

mitchell

Highlight

mitchell

Highlight

mitchell

Highlight

mitchell

Sticky Note

PFS 22 + 23. It is possible that the PFS-reported values for medical and dental expenses do not match what's listed here, depending on what the family is reporting or claiming.

mitchell

Sticky Note

Not the same as the medical allowance used by SSS on RFC line 21. Review parent explanations of expenses. While they may be allowable for tax purposes, they may not be allowable for your review.

mitchell

Highlight

mitchell

Sticky Note

Generally, those who pay mortgage interest will itemize their deductions. Can be helpful to help 'guesstimate' value of outstanding mortgage or verify ownership of a home.

mitchell

Sticky Note

Form 1040 line 40 PFS 6D

mitchell

Highlight

SCHEDULE B (Form 1040A or 1040)

Department of the Treasury Internal Revenue Service (99)

Interest and Ordinary Dividends▶ Attach to Form 1040A or 1040.

▶ Information about Schedule B (Form 1040A or 1040) and its instructions is at www.irs.gov/scheduleb.

OMB No. 1545-0074

2013Attachment Sequence No. 08

Name(s) shown on return Your social security number

Part I

Interest

(See instructions on back and the instructions for Form 1040A, or Form 1040, line 8a.) Note. If you received a Form 1099-INT, Form 1099-OID, or substitute statement from a brokerage firm, list the firm’s name as the payer and enter the total interest shown on that form.

1

List name of payer. If any interest is from a seller-financed mortgage and the buyer used the property as a personal residence, see instructions on back and list this interest first. Also, show that buyer’s social security number and address ▶

1

Amount

2 Add the amounts on line 1 . . . . . . . . . . . . . . . . . . 2 3

Excludable interest on series EE and I U.S. savings bonds issued after 1989. Attach Form 8815 . . . . . . . . . . . . . . . . . . . . . 3

4

Subtract line 3 from line 2. Enter the result here and on Form 1040A, or Form 1040, line 8a . . . . . . . . . . . . . . . . . . . . . . ▶ 4

Note. If line 4 is over $1,500, you must complete Part III. Amount

Part II

Ordinary Dividends (See instructions on back and the instructions for Form 1040A, or Form 1040, line 9a.)

Note. If you received a Form 1099-DIV or substitute statement from a brokerage firm, list the firm’s name as the payer and enter the ordinary dividends shown on that form.

5 List name of payer ▶

5

6

Add the amounts on line 5. Enter the total here and on Form 1040A, or Form 1040, line 9a . . . . . . . . . . . . . . . . . . . . . . ▶ 6

Note. If line 6 is over $1,500, you must complete Part III.

Part III Foreign Accounts and Trusts (See instructions on back.)

You must complete this part if you (a) had over $1,500 of taxable interest or ordinary dividends; (b) had a foreign account; or (c) received a distribution from, or were a grantor of, or a transferor to, a foreign trust. Yes No

7a At any time during 2013, did you have a financial interest in or signature authority over a financial account (such as a bank account, securities account, or brokerage account) located in a foreign country? See instructions . . . . . . . . . . . . . . . . . . . . . . . .If “Yes,” are you required to file FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR), formerly TD F 90-22.1, to report that financial interest or signature authority? See FinCEN Form 114 and its instructions for filing requirements and exceptions to those requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . .

b If you are required to file FinCEN Form 114, enter the name of the foreign country where the financial account is located ▶

8 During 2013, did you receive a distribution from, or were you the grantor of, or transferor to, a foreign trust? If “Yes,” you may have to file Form 3520. See instructions on back . . . . . .

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 17146N Schedule B (Form 1040A or 1040) 2013

mitchell

Highlight

mitchell

Sticky Note

If interest income is greater than $1500, then each payor must be listed separately and the amounts of interest paid by each.

mitchell

Highlight

mitchell

Sticky Note

If dividend income is greater than $1500, then each payor must be listed separately along with the amounts paid by each.

mitchell

Highlight

mitchell

Sticky Note

Indicates presence of assets held in a foreign account that may not otherwise appear on the PFS. A "yes" answer here could be a trigger to follow up with the family for more information on these accounts.

Schedule B (Form 1040A or 1040) 2013 Page 2

General InstructionsSection references are to the Internal Revenue Code unless otherwise noted.

Future DevelopmentsFor the latest information about developments related to Schedule B (Form 1040A or 1040) and its instructions, such as legislation enacted after they were published, go to www.irs.gov/scheduleb.

Purpose of FormUse Schedule B if any of the following applies.

• You had over $1,500 of taxable interest or ordinary dividends.

• You received interest from a seller-financed mortgage and the buyer used the property as a personal residence.

• You have accrued interest from a bond.

• You are reporting original issue discount (OID) in an amount less than the amount shown on Form 1099-OID.

• You are reducing your interest income on a bond by the amount of amortizable bond premium.

• You are claiming the exclusion of interest from series EE or I U.S. savings bonds issued after 1989.

• You received interest or ordinary dividends as a nominee.

• You had a financial interest in, or signature authority over, a financial account in a foreign country or you received a distribution from, or were a grantor of, or transferor to, a foreign trust. Part III of the schedule has questions about foreign accounts and trusts.

Specific Instructions

TIPYou can list more than one payer on each entry space for lines 1 and 5, but be sure to clearly show the amount paid next to the payer's name. Add the separate amounts paid by the payers

listed on an entry space and enter the total in the “Amount” column. If you still need more space, attach separate statements that are the same size as the printed schedule. Use the same format as lines 1 and 5, but show your totals on Schedule B. Be sure to put your name and social security number (SSN) on the statements and attach them at the end of your return.

Part I. InterestLine 1. Report on line 1 all of your taxable interest. Taxable interest should be shown on your Forms 1099-INT, Forms 1099-OID, or substitute statements. Include interest from series EE, H, HH, and I U.S. savings bonds. List each payer’s name and show the amount. Do not report on this line any tax-exempt interest from box 8 or box 9 of Form 1099-INT. Instead, report the amount from box 8 on line 8b of Form 1040A or 1040. If an amount is shown in box 9 of Form 1099-INT, you generally must report it on line 12 of Form 6251. See the Instructions for Form 6251 for more details.

Seller-financed mortgages. If you sold your home or other property and the buyer used the property as a personal residence, list first any interest the buyer paid you on a mortgage or other form of seller financing. Be sure to show the buyer’s name, address, and SSN. You must also let the buyer know your SSN. If you do not show the buyer’s name, address, and SSN, or let the buyer know your SSN, you may have to pay a $50 penalty.

Nominees. If you received a Form 1099-INT that includes interest you received as a nominee (that is, in your name, but the interest actually belongs to someone else), report the total on line 1. Do this even if you later distributed some or all of this income to others. Under your last entry on line 1, put a subtotal of all interest listed on line 1. Below this subtotal, enter "Nominee Distribution" and show the total interest you received as a nominee. Subtract this amount from the subtotal and enter the result on line 2.

TIPIf you received interest as a nominee, you must give the actual owner a Form 1099-INT unless the owner is your spouse. You must also file a Form 1096 and a Form 1099-INT with the IRS. For

more details, see the General Instructions for Certain Information Returns and the Instructions for Forms 1099-INT and 1099-OID.

Accrued interest. When you buy bonds between interest payment dates and pay accrued interest to the seller, this interest is taxable to the seller. If you received a Form 1099 for interest as a purchaser of a bond with accrued interest, follow the rules earlier under Nominees to see how to report the accrued interest. But identify the amount to be subtracted as “Accrued Interest.”

Original issue discount (OID). If you are reporting OID in an amount less than the amount shown on Form 1099-OID, follow the rules earlier under Nominees to see how to report the OID. But identify the amount to be subtracted as “OID Adjustment.”

Amortizable bond premium. If you are reducing your interest income on a bond by the amount of amortizable bond premium, follow the rules earlier under Nominees to see how to report the interest. But identify the amount to be subtracted as “ABP Adjustment.”

Line 3. If, during 2013, you cashed series EE or I U.S. savings bonds issued after 1989 and you paid qualified higher education expenses for yourself, your spouse, or your dependents, you may be able to exclude part or all of the interest on those bonds. See Form 8815 for details.

Part II. Ordinary Dividends

TIPYou may have to file Form 5471 if, in 2013, you were an officer or director of a foreign corporation. You may also have to file Form 5471 if, in 2013, you owned 10% or more of the total

(a) value of a foreign corporation’s stock, or (b) combined voting power of all classes of a foreign corporation’s stock with voting rights. For details, see Form 5471 and its instructions.

Line 5. Report on line 5 all of your ordinary dividends. This amount should be shown in box 1a of your Forms 1099-DIV or substitute statements. List each payer’s name and show the amount.

Nominees. If you received a Form 1099-DIV that includes ordinary dividends you received as a nominee (that is, in your name, but the ordinary dividends actually belong to someone else), report the total on line 5. Do this even if you later distributed some or all of this income to others. Under your last entry on line 5, put a subtotal of all ordinary dividends listed on line 5. Below this subtotal, enter “Nominee Distribution” and show the total ordinary dividends you received as a nominee. Subtract this amount from the subtotal and enter the result on line 6.

TIPIf you received dividends as a nominee, you must give the actual owner a Form 1099-DIV unless the owner is your spouse. You must also file a Form 1096 and a Form 1099-DIV with the IRS. For more

details, see the General Instructions for Certain Information Returns and the Instructions for Form 1099-DIV.

Part III. Foreign Accounts and Trusts

TIPRegardless of whether you are required to file FinCEN Form 114 (FBAR), you may be required to file Form 8938, Statement of Specified Foreign Financial Assets, with your income tax

return. Failure to file Form 8938 may result in penalties and extension of the statute of limitations. See www.irs.gov/form8938 for more information.

Line 7a–Question 1. Check the “Yes” box if at any time during 2013 you had a financial interest in or signature authority over a financial account located in a foreign country. See the definitions that follow. Check the “Yes” box even if you are not required to file FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR).

Financial account. A financial account includes, but is not limited to, a securities, brokerage, savings, demand, checking, deposit, time deposit, or other account maintained with a financial institution (or other person performing the services of a financial institution). A financial account also includes a commodity futures or options account, an insurance policy with a cash value (such as a whole life insurance policy), an annuity policy with a cash value, and shares in a mutual fund or similar pooled fund (that is, a fund that is available to the general public with a regular net asset value determination and regular redemptions).

Financial account located in a foreign country. A financial account is located in a foreign country if the account is physically located outside of the United States. For example, an account maintained with a branch of a United States bank that is physically located outside of the United States is a foreign financial account. An account maintained with a branch of a foreign bank that is physically located in the United States is not a foreign financial account.

Signature authority. Signature authority is the authority of an individual (alone or in conjunction with another individual) to control the disposition of assets held in a foreign financial account by direct communication (whether in writing or otherwise) to the bank or other financial institution that maintains the financial account. See the FinCEN Form 114 instructions for exceptions. Do not consider the exceptions relating to signature authority in answering Question 1 on line 7a.

Other definitions. For definitions of “financial interest,” “United States,” and other relevant terms, see the instructions for FinCEN Form 114.

Line 7a–Question 2. See FinCEN Form 114 and its instructions to determine whether you must file the form. Check the “Yes” box if you are required to file the form; check the “No” box if you are not required to file the form.

If you checked the “Yes” box to Question 2 on line 7a, FinCEN Form 114 must be electronically filed with the Financial Crimes Enforcement Network (FinCEN) at the following website: http://bsaefiling.fincen.treas.gov/main.html. Do not attach FinCEN Form 114 to your tax return. To be considered timely, FinCEN Form 114 must be received by June 30, 2014.

▲!CAUTION

If you are required to file FinCEN Form 114 but do not properly do so, you may have to pay a civil penalty up to $10,000. A person who willfully fails to report an account or provide account

identifying information may be subject to a civil penalty equal to the greater of $100,000 or 50 percent of the balance in the account at the time of the violation. Willful violations may also be subject to criminal penalties.

Line 7b. If you are required to file FinCEN Form 114, enter the name of the foreign country or countries in the space provided on line 7b. Attach a separate statement if you need more space.

Line 8. If you received a distribution from a foreign trust, you must provide additional information. For this purpose, a loan of cash or marketable securities generally is considered to be a distribution. See Form 3520 for details.

If you were the grantor of, or transferor to, a foreign trust that existed during 2013, you may have to file Form 3520.

Do not attach Form 3520 to Form 1040. Instead, file it at the address shown in its instructions.

If you were treated as the owner of a foreign trust under the grantor trust rules, you are also responsible for ensuring that the foreign trust files Form 3520-A. Form 3520-A is due on March 17, 2014, for a calendar year trust. See the instructions for Form 3520-A for more details.

SCHEDULE C (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Profit or Loss From Business (Sole Proprietorship)

▶ For information on Schedule C and its instructions, go to www.irs.gov/schedulec. ▶ Attach to Form 1040, 1040NR, or 1041; partnerships generally must file Form 1065.

OMB No. 1545-0074

2013Attachment Sequence No. 09

Name of proprietor Social security number (SSN)

A Principal business or profession, including product or service (see instructions) B Enter code from instructions

▶

C Business name. If no separate business name, leave blank. D Employer ID number (EIN), (see instr.)

E Business address (including suite or room no.) ▶

City, town or post office, state, and ZIP code

F Accounting method: (1) Cash (2) Accrual (3) Other (specify) ▶

G Did you “materially participate” in the operation of this business during 2013? If “No,” see instructions for limit on losses . Yes No

H If you started or acquired this business during 2013, check here . . . . . . . . . . . . . . . . . ▶

I Did you make any payments in 2013 that would require you to file Form(s) 1099? (see instructions) . . . . . . . . Yes No

J If "Yes," did you or will you file required Forms 1099? . . . . . . . . . . . . . . . . . . . . . Yes No

Part I Income 1 Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on

Form W-2 and the “Statutory employee” box on that form was checked . . . . . . . . . ▶ 1

2 Returns and allowances . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 Subtract line 2 from line 1 . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Cost of goods sold (from line 42) . . . . . . . . . . . . . . . . . . . . . . 4

5 Gross profit. Subtract line 4 from line 3 . . . . . . . . . . . . . . . . . . . . 5