©2012 Pearson Education, Auditing 14/e, Arens/Elder/Beasley 5 - 5 Completing the Tests in the...

41

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e, Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 5 - 5 Completing the Tests in the Completing the Tests in the Acquisition and Payment Acquisition and Payment Cycle: Verification of Cycle: Verification of Selected Accounts Selected Accounts Chapter 19 Chapter 19

-

Upload

jonas-cole -

Category

Documents

-

view

222 -

download

1

Transcript of ©2012 Pearson Education, Auditing 14/e, Arens/Elder/Beasley 5 - 5 Completing the Tests in the...

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 5 - 5

Completing the Tests in the Completing the Tests in the Acquisition and Payment Cycle: Acquisition and Payment Cycle:

Verification of Selected AccountsVerification of Selected Accounts

Chapter 19Chapter 19

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 22

Learning Objective 1Learning Objective 1

Recognize the many accounts in the Recognize the many accounts in the acquisition and payment cycle.acquisition and payment cycle.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 33

Accounts Associated with the Accounts Associated with the Acquisition and Payment Acquisition and Payment

CycleCycleAssets:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 44

Learning Objective 2Learning Objective 2

Design and perform audit tests of Design and perform audit tests of property, plant, and equipment and property, plant, and equipment and related accounts.related accounts.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 55

Classifications of Property, Classifications of Property, Plant and EquipmentPlant and Equipment

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 66

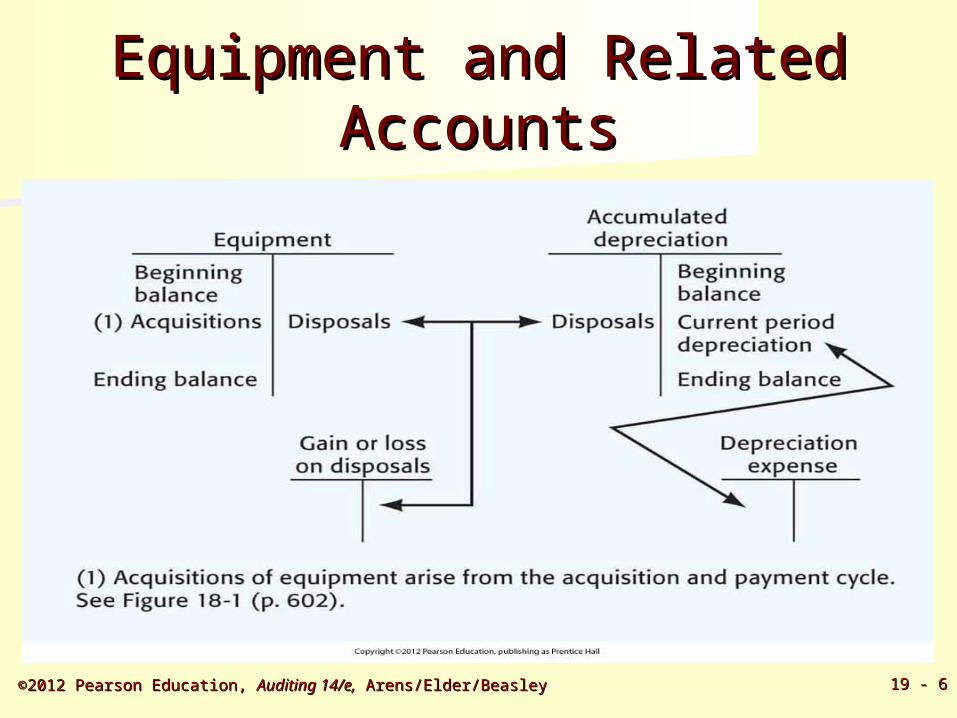

Equipment and Related Equipment and Related AccountsAccounts

Manufacturing Equipment

AccumulatedDepreciated

Beginningbalance

Beginningbalance

DepreciationExpense

Gain or Losson Disposals

Current perioddepreciationEnding balance

DisposalsDisposals

Acquisitions

Endingbalance

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 77

Auditing Manufacturing Auditing Manufacturing Equipment and Related Equipment and Related

AccountsAccounts

Perform analytical proceduresPerform analytical procedures

Current year acquisitions Current year disposals Ending balance in the asset account Depreciation expense Ending balance in accumulated depreciation

Current year acquisitions Current year disposals Ending balance in the asset account Depreciation expense Ending balance in accumulated depreciation

Plus verify:Plus verify:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 88

Analytical Procedures for Analytical Procedures for Manufacturing EquipmentManufacturing Equipment

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 99

Verify Current Year Verify Current Year AcquisitionsAcquisitions

Current year additions have a long-term effect on the financial statements.

Seven of the eight balance-relatedaudit objectives are used as a frame of reference.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1010

Balance-related Audit Balance-related Audit ObjectivesObjectives

Detail tie-in:

Current acquisitions agreewith the master file.

1. Foot the acquisition schedule.2. Trace the individual acquisitions to the master file.3. Trace the total to the general ledger.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1111

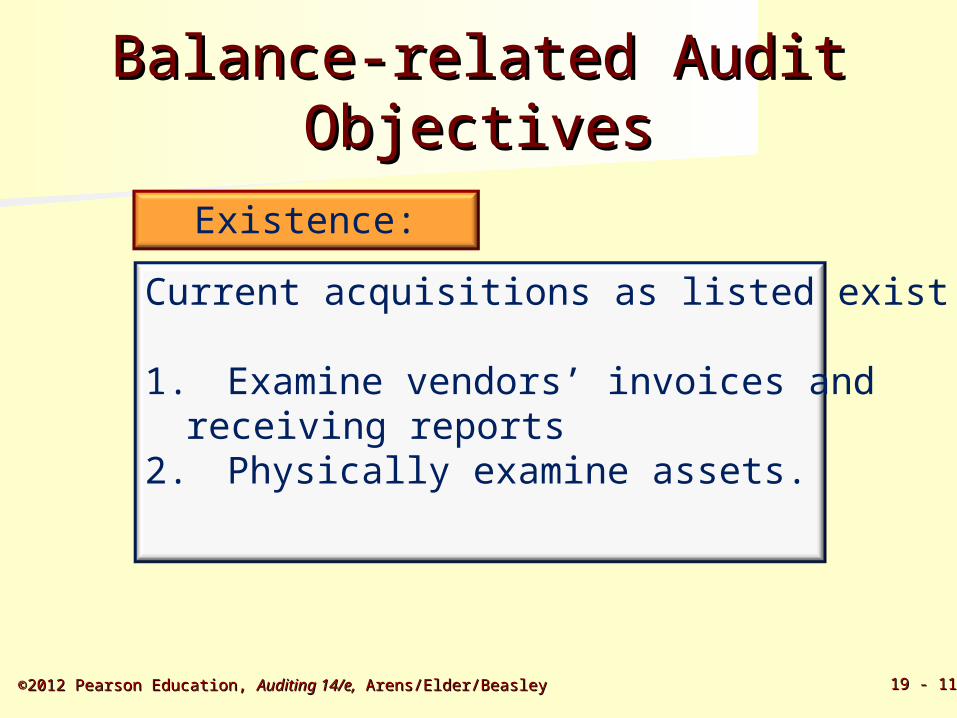

Balance-related Audit Balance-related Audit ObjectivesObjectives

Existence:

Current acquisitions as listed exist.

1.Examine vendors’ invoices andreceiving reports

2.Physically examine assets.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1212

Balance-related Audit Balance-related Audit ObjectivesObjectives

Completeness:

Existing acquisitions are recorded.

1.Examine vendors’ invoices of closelyrelated accounts to uncover items thatshould be manufacturing equipment.

2.Review lease and rental agreements.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1313

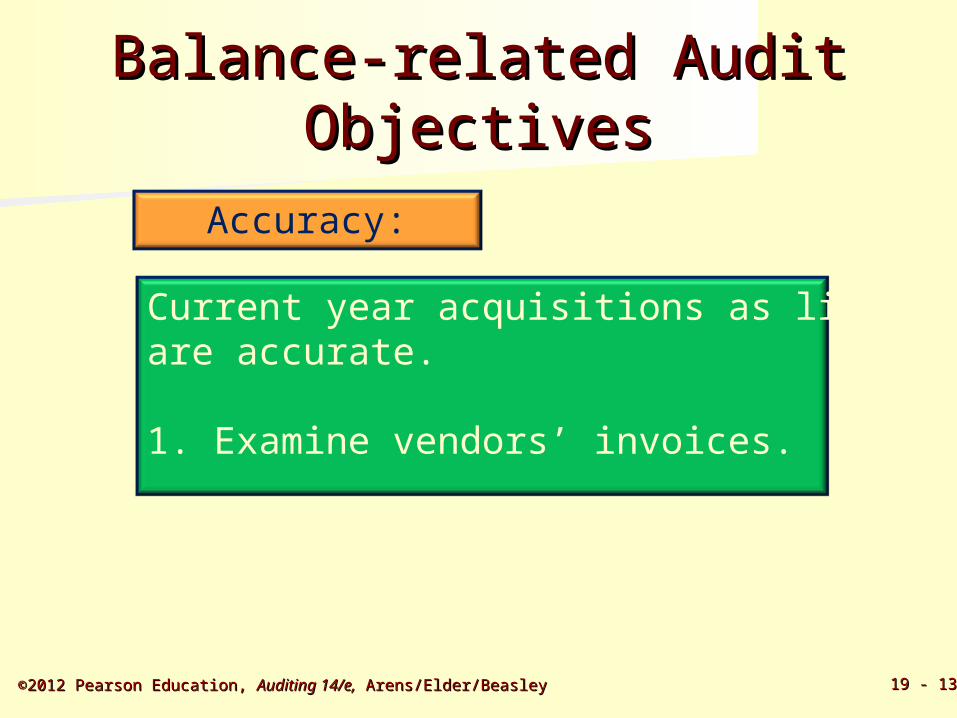

Balance-related Audit Balance-related Audit ObjectivesObjectives

Current year acquisitions as listedare accurate.

1. Examine vendors’ invoices.

Accuracy:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1414

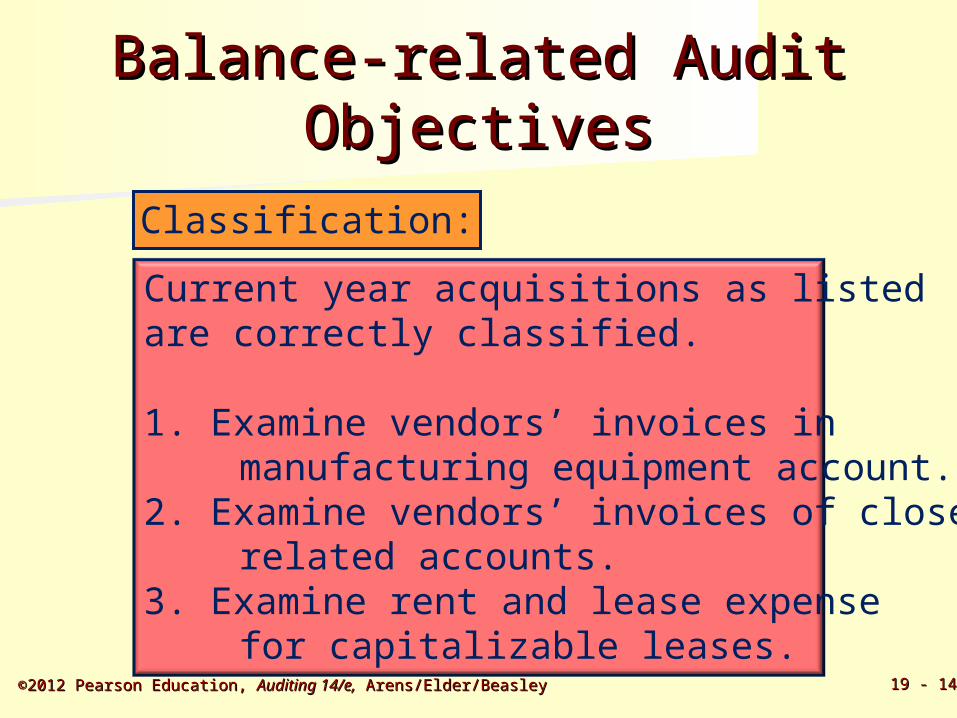

Balance-related Audit Balance-related Audit ObjectivesObjectives

Classification:

Current year acquisitions as listedare correctly classified.

1. Examine vendors’ invoices inmanufacturing equipment account.

2. Examine vendors’ invoices of closelyrelated accounts.

3. Examine rent and lease expensefor capitalizable leases.

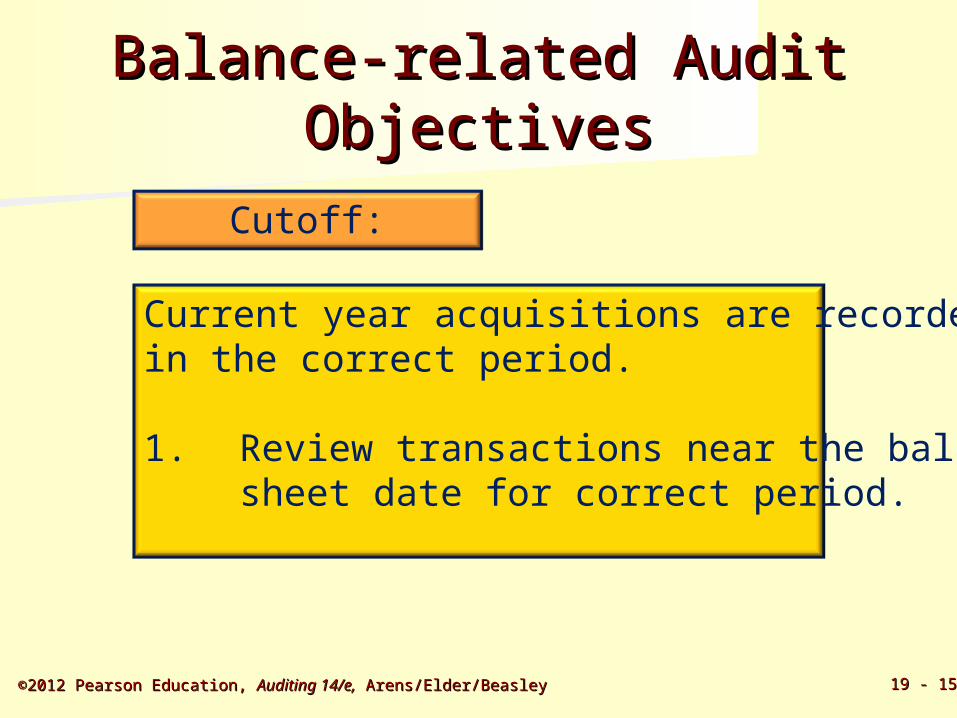

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1515

Current year acquisitions are recordedin the correct period.

1. Review transactions near the balancesheet date for correct period.

Balance-related Audit Balance-related Audit ObjectivesObjectives

Cutoff:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1616

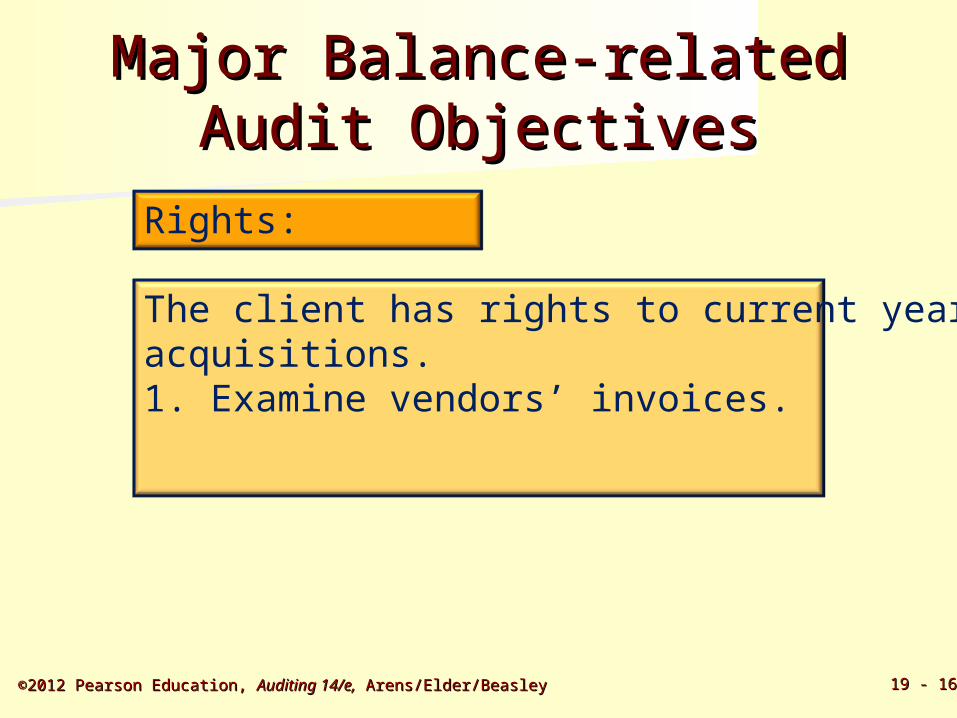

The client has rights to current yearacquisitions.1. Examine vendors’ invoices.

Major Balance-relatedMajor Balance-relatedAudit ObjectivesAudit Objectives

Rights:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1717

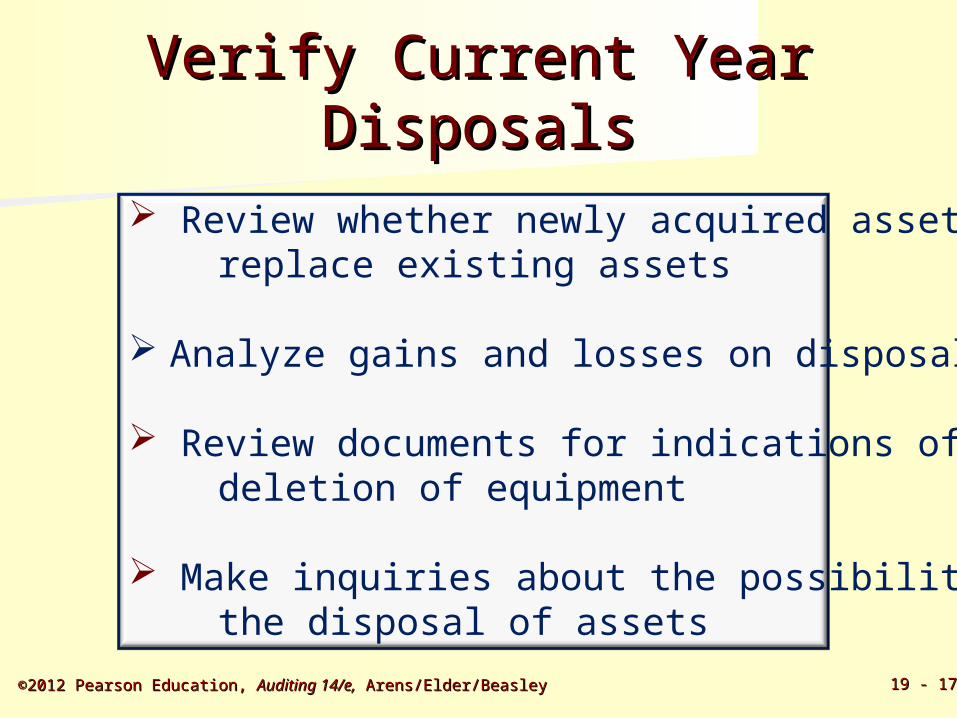

Verify Current Year Verify Current Year DisposalsDisposals

Review whether newly acquired assets replace existing assets

Analyze gains and losses on disposal

Review documents for indications of deletion of equipment

Make inquiries about the possibility of the disposal of assets

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1818

Verify Ending BalanceVerify Ending Balanceof Asset Accountsof Asset Accounts

All recorded equipment physically exists on the balance sheet date

All equipment owned is recorded

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 1919

Verify Depreciation ExpenseVerify Depreciation Expense

The most important objective is accuracy.

Consistent depreciation policy

Correct calculations

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2020

Verify Ending Balance in Verify Ending Balance in Accumulated DepreciationAccumulated Depreciation

Accumulated depreciation as statedin the property master file agreeswith the general ledger.

Accumulated depreciation in themaster file is accurate.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2121

Learning Objective 3Learning Objective 3

Design and perform audit tests of Design and perform audit tests of prepaid expenses.prepaid expenses.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2222

Audit of Prepaid ExpensesAudit of Prepaid Expenses

Prepaid rent Organization costs Prepaid taxes Patents Prepaid insurance Trademarks Deferred charges Copyrights

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2323

Prepaid Insurance and Prepaid Insurance and Related AccountsRelated Accounts

Prepaid Insurance

Beginning balance

Acquisitions

Ending balance

Current period insurance expense

Insurance Expense

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2424

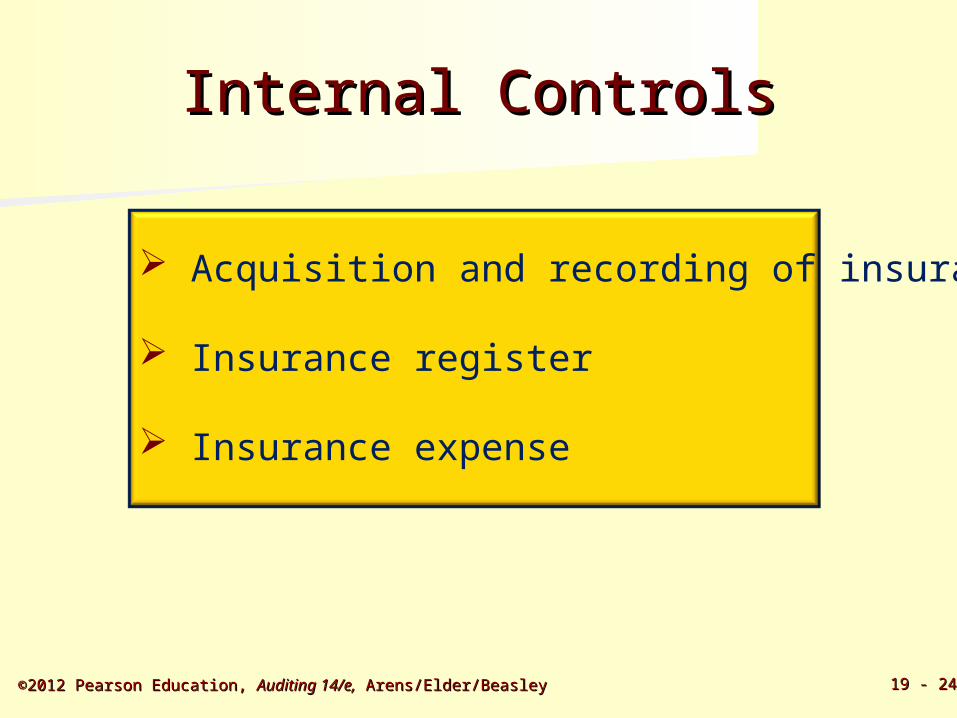

Internal ControlsInternal Controls

Acquisition and recording of insurance

Insurance register

Insurance expense

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2525

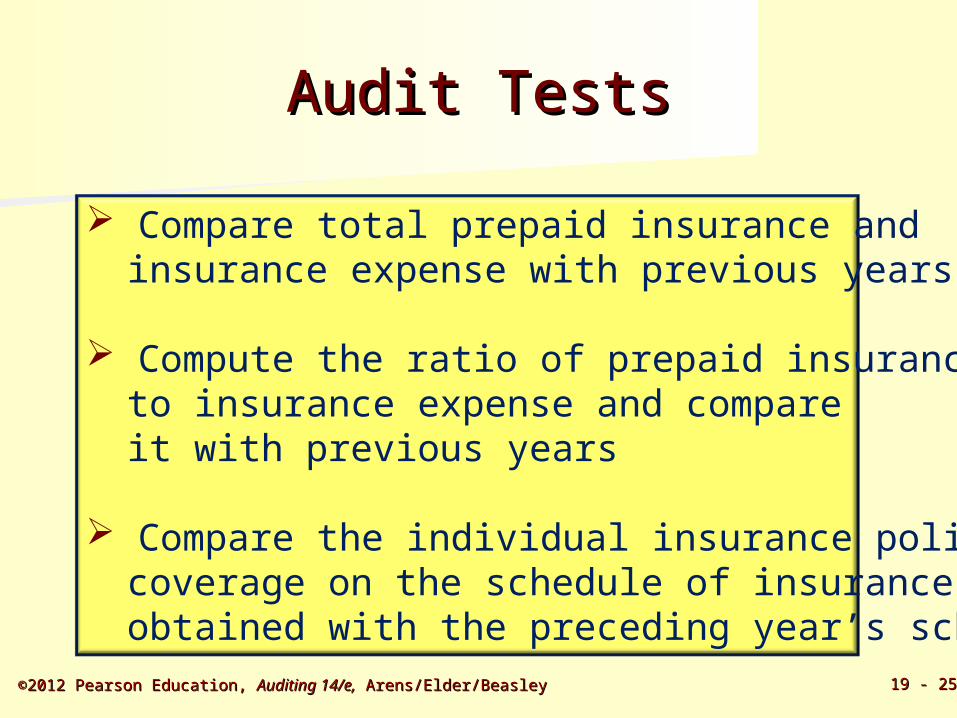

Audit TestsAudit Tests

Compare total prepaid insurance andinsurance expense with previous years

Compute the ratio of prepaid insuranceto insurance expense and compareit with previous years

Compare the individual insurance policycoverage on the schedule of insuranceobtained with the preceding year’s schedule

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2626

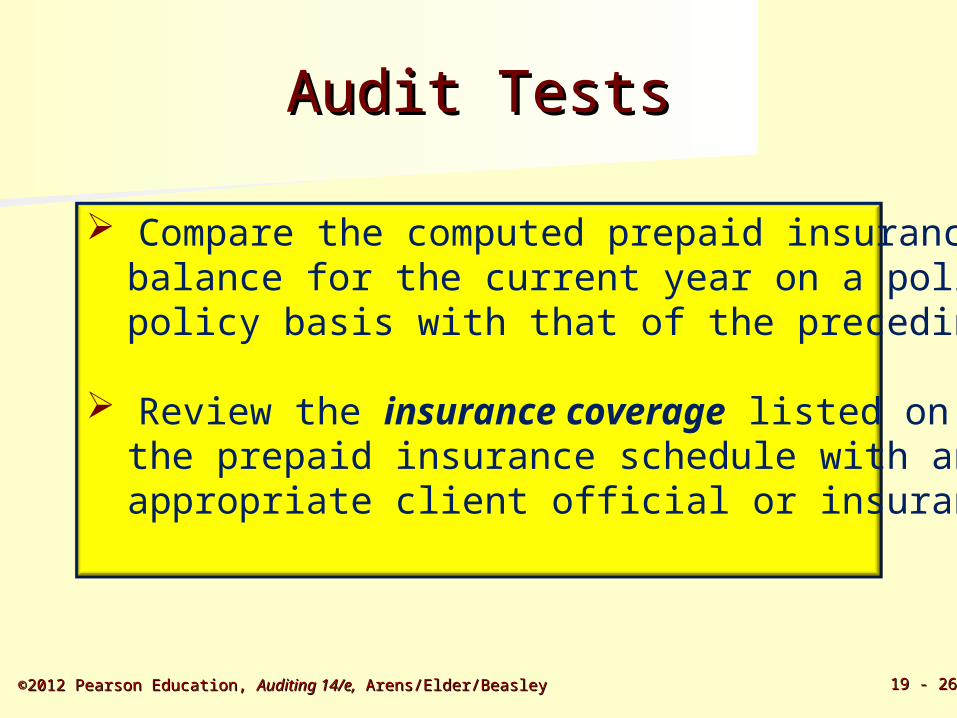

Audit TestsAudit Tests

Compare the computed prepaid insurancebalance for the current year on a policy-by-policy basis with that of the preceding year.

Review the insurance coverage listed onthe prepaid insurance schedule with anappropriate client official or insurance broker.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2727

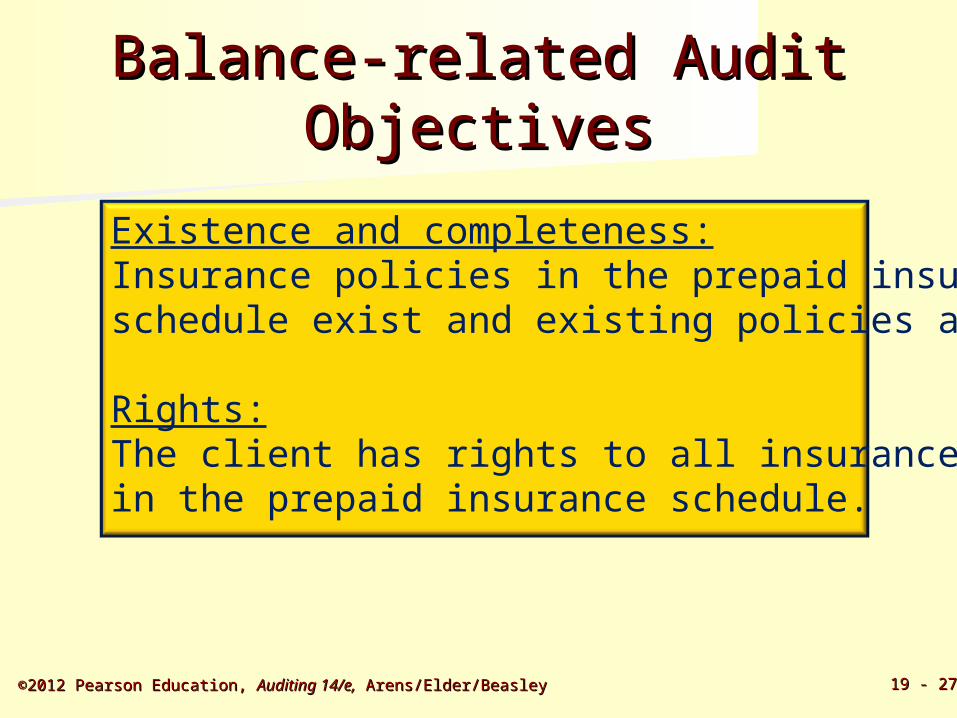

Balance-related Audit Balance-related Audit ObjectivesObjectives

Existence and completeness:Insurance policies in the prepaid insuranceschedule exist and existing policies are listed.

Rights:The client has rights to all insurance policiesin the prepaid insurance schedule.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2828

Balance-related Audit Balance-related Audit ObjectivesObjectives

Accuracy and detail tie-in:Prepaid amounts are accurate and the totalis correctly added and agrees with thegeneral ledger.Classification:Insurance expense is properly classified.Cutoff:Insurance transactions are recorded in theproper period.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 2929

Learning Objective 4Learning Objective 4

Design and perform audit tests of Design and perform audit tests of accrued liabilities.accrued liabilities.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3030

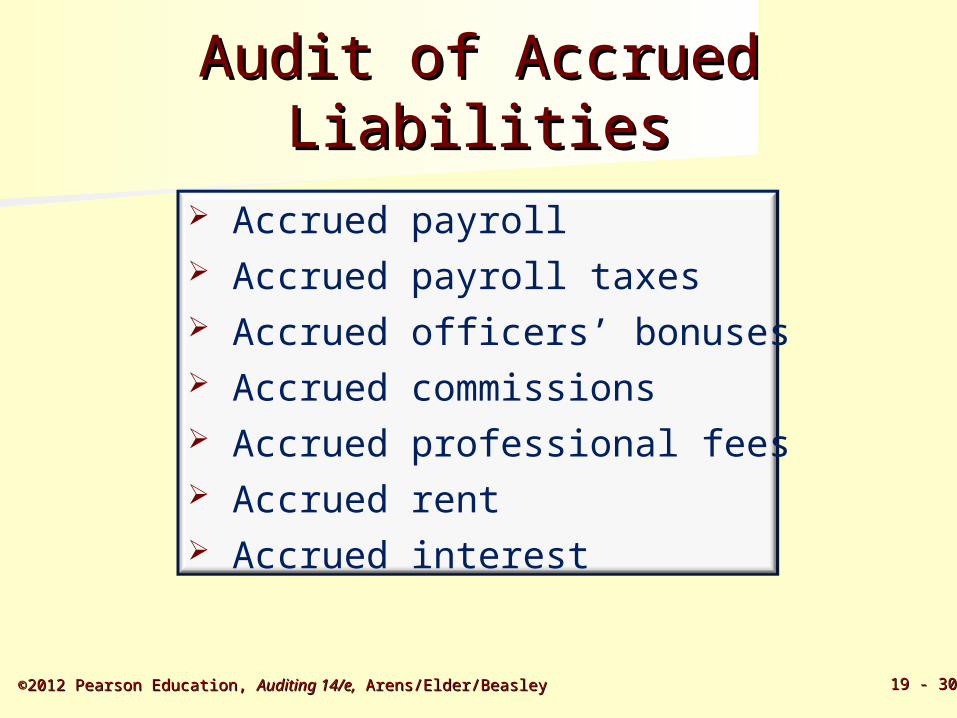

Audit of Accrued LiabilitiesAudit of Accrued Liabilities

Accrued payroll Accrued payroll taxes Accrued officers’ bonuses Accrued commissions Accrued professional fees Accrued rent Accrued interest

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3131

Accrued Property TaxesAccrued Property Taxesand Related Accountsand Related Accounts

Accrued Property TaxesBeginning balance

Current period property tax expense

Ending balance

Property Tax ExpensePayments(property taxes)

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3232

Learning Objective 5Learning Objective 5

Design and perform audit tests of Design and perform audit tests of income and expense accounts.income and expense accounts.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3333

Approach to Auditing Approach to Auditing IncomeIncome

and Expense Accountsand Expense Accounts Analytical procedures

Tests of controls and substantivetests of transactions

Tests of details of account balances

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3434

Analytical Procedures for Analytical Procedures for Income and Expense Income and Expense

AccountsAccounts

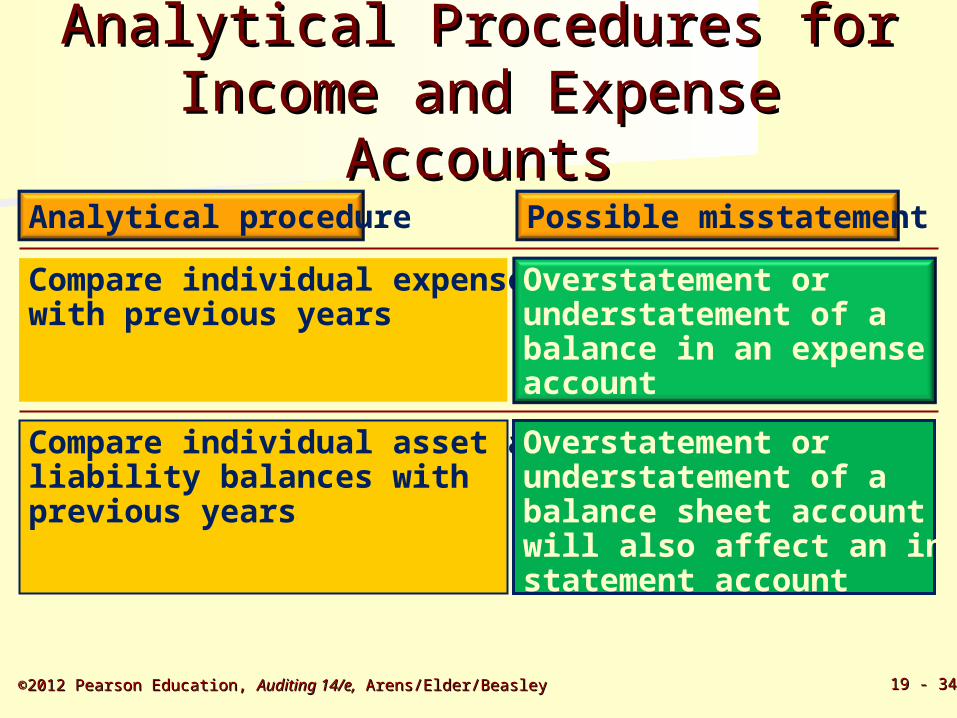

Compare individual asset andliability balances with previous years

Overstatement orunderstatement of abalance sheet account thatwill also affect an incomestatement account

Analytical procedure

Compare individual expenseswith previous years

Overstatement orunderstatement of abalance in an expenseaccount

Possible misstatement

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3535

Analytical Procedures for Analytical Procedures for Income and Expense Income and Expense

AccountsAccountsAnalytical procedure

Compare individual expenseswith budgets

Misstatement of expensesand related balancesheet accounts

Possible misstatement

Compare gross marginpercentage with previousyears

Misstatement of cost ofgoods sold and inventory

Compare inventory turnoverratio with previous years

Misstatement of cost ofgoods sold and inventory

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3636

Analytical Procedures for Analytical Procedures for Income and Expense Income and Expense

AccountsAccountsAnalytical procedure

Compare prepaid insuranceexpense with previous years

Misstatement of insurance expense and prepaid insurance

Possible misstatement

Compare commission expense divided by sales with previous years

Misstatement ofcommission expense andaccrued commissions

Compare individualmanufacturing expensesdivided by total mfg.expenses with previous years

Misstatement of individual manufacturing expenses and related balance sheet accounts

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3737

Tests of Controls and Tests of Controls and SubstantiveSubstantive

Test of TransactionsTest of TransactionsBoth tests of controls and substantivetests of transactions have the effect ofsimultaneously verifying balance sheet and income statement accounts.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3838

Analysis of Legal Expense Analysis of Legal Expense

Expense account analysis: Repairs and maintenance

Rent and lease

Legal expense

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 3939

Analysis of Legal Expense Analysis of Legal Expense

Expense account analysis:

Repairs and maintenance

Rent and lease

Legal expense

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 19 - 19 - 4040

Tests of Details of Account Tests of Details of Account Balances – AllocationBalances – Allocation

Several expense accounts result from the allocationof accounting data rather than discrete transactions.

These include depreciation, depletion, and theamortization of copyrights and catalog cost.

The allocation of manufacturing overhead betweeninventory and cost of goods sold is an example ofa different type of allocation that affects expenses.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 5 - 5

End of Chapter 19End of Chapter 19