2012 IRS Form 990 Whats New - Whats Important

59

2012 Form 990: What’s New, What’s Important February 26, 2013 Deborah G. Kosnett, CPA

-

Upload

tate-tryon-cpas -

Category

Documents

-

view

272 -

download

0

Transcript of 2012 IRS Form 990 Whats New - Whats Important

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 1/59

2012 Form 990: What’s

New, What’s ImportantFebruary 26, 2013

Deborah G. Kosnett, CPA

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 2/59

©Copyright Tate & Tryon 20131

IRS Highlights:

2012 EO Annual Report/2013 Workplan

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 3/59

©Copyright Tate & Tryon 2013

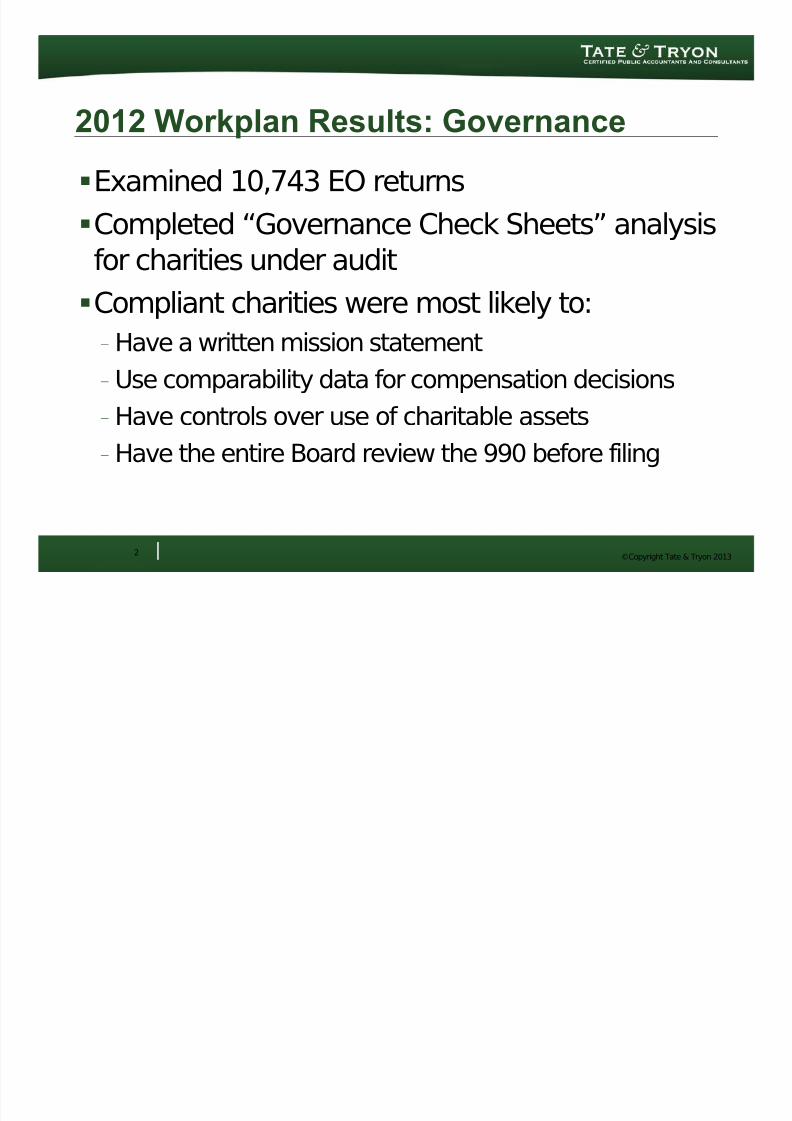

2012 Workplan Results: Governance

Examined 10,743 EO returns

Completed “Governance Check Sheets” analysisfor charities under audit

Compliant charities were most likely to:

- Have a written mission statement

- Use comparability data for compensation decisions

-

Have controls over use of charitable assets- Have the entire Board review the 990 before filing

2

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 4/59

©Copyright Tate & Tryon 2013

2012 Workplan Results: Auto Revocation

More than 450,000 organizations have lost

exempt statusAbout 30,000 have applied for reinstatement

IRS offered transitional relief for small orgs-

reduced fees, etc. through Dec. 31IRS launched “Select Check” web site in 2012:info on revocation, filings, eligibility to receive

deductible contributionsIRS also routinely sends out “compliance check”

notices to intermittent non-filers

3

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 5/59

©Copyright Tate & Tryon 2013

2012 Workplan Results: Outreach

Initiated ‘virtual workshops’ - “What You

Need to Know About Automatic Revocationof Exemption”

Made extensive use of introductoryworkshops, webinars, e-newsletters

2013: In-person outreach for larger groups;

technology and ‘virtual content’ for smallerorgs

4

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 6/59

©Copyright Tate & Tryon 2013

2012 Workplan Results: Exam Process Info

Launched web pages that provide centralized

information on the EO exam process:- Why an org might be selected for review

-

Different types of exams (field, correspondence, etc.)- What to expect during an exam

- Taxpayer rights

- Info on Fast Track Settlement

www.irs.gov/Charities-&-Non-Profits/Exempt-Organizations-Audit-Process

5

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 7/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: Form 990 Compliance

“The IRS uses the Form 990responses to select returns for

examination, so a complete and

accurate return is in your best

interest.”

-- IRS FY 2013 Workplan

6

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 8/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: Form 990 Compliance

“As we examine organizations selected through thisdata-driven approach, we find that the Form 990

responses of some organizations do not alwaysaccurately reflect their activities. If those

organizations had been more careful in completingtheir returns, they might not have been identified by

our indicators or selected for examination.”-- IRS FY 2013 Workplan

7

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 9/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: Form 990 Compliance

Compensation transparency – IRS will examine 200 orgs

- Focus on high gross receipts / very low total compensationUnlawful political campaign intervention – IRS will

evaluate 300 cases for possible examination

-

IRS will also evaluate whether Forms 1120-POL should havebeen filed

Unrelated business income – IRS plans to examine orgs

with high gross UBI / no taxable income

Charitable spending initiative – IRS sources/uses of

charitable funds exams will focus on medium/large orgs

- Focus on high fundraising income/low fundraising expense

8

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 10/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: Governance

§501(c)(3) and (4) orgs will be examined for

governance practices- Based on 2012 findings

- IRS checksheet will look for additional relevant factors

or practices285 orgs that in 2009 reported a “significantdiversion of assets” – IRS will look at their before/

after governance practices

9

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 11/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: §512(b)(13) Study

The Pension Protection Act of 2006 made some

changes to this code section – transactions withcontrolled entities

PPA 2006 mandated Treasury to report on

administration of the changes and makerecommendations

IRS EO Division is starting to analyze data

gathered from 2,000 checksheets

No info on when this might be complete

10

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 12/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: Employment Tax Compliance

IRS is in its 3rd year of an employment tax

compliance research project (NationalResearch Program (NRP))

EO has examined employment tax formsfiled by exempt orgs in 2008 – 2010

For 2013, EO will finish its analysis and

provide data to the IRS NRP for furtherwork

11

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 13/59

©Copyright Tate & Tryon 2013

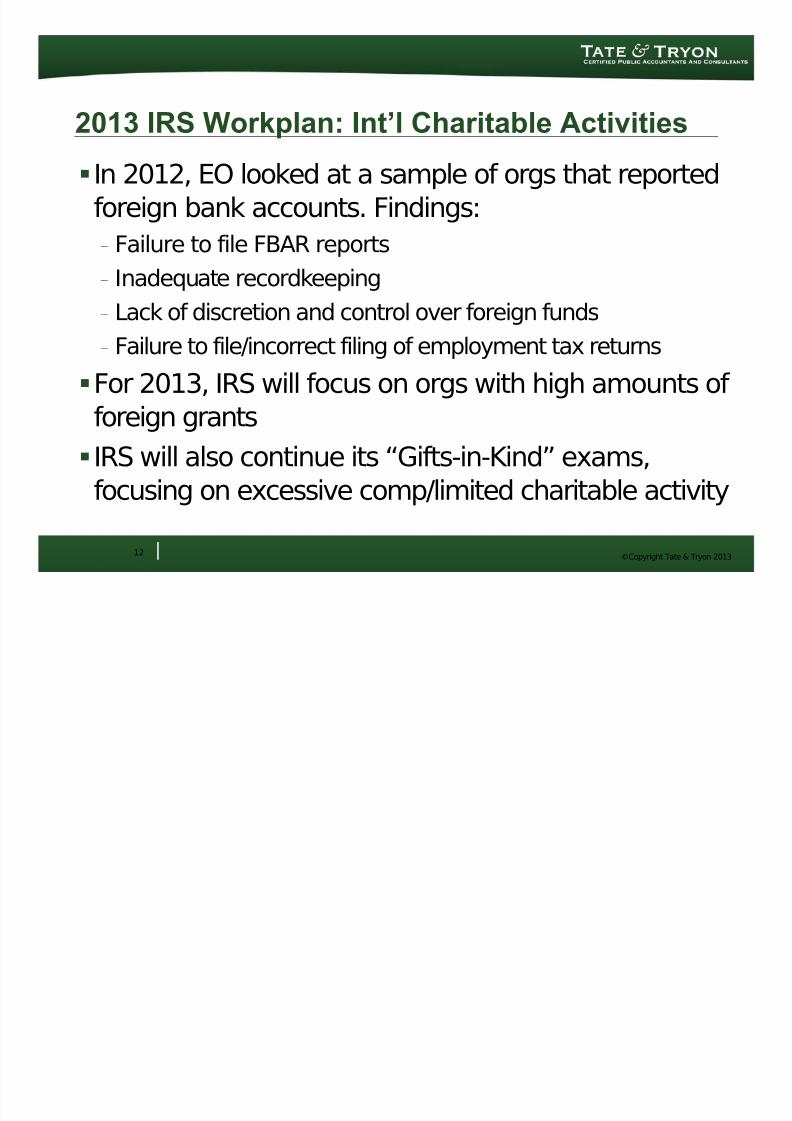

2013 IRS Workplan: Int’l Charitable Activities

In 2012, EO looked at a sample of orgs that reported

foreign bank accounts. Findings:- Failure to file FBAR reports

- Inadequate recordkeeping

-

Lack of discretion and control over foreign funds- Failure to file/incorrect filing of employment tax returns

For 2013, IRS will focus on orgs with high amounts of

foreign grants IRS will also continue its “Gifts-in-Kind” exams,

focusing on excessive comp/limited charitable activity

12

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 14/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: Group Rulings

IRS is currently sending out a Group Rulings

Questionnaire to > 2,000 randomly selected“central” organizations

- 2011 Advisory Committee to TE/GE report questioned

utility of group exemptions- Large numbers of subordinates have been auto-revoked

Questionnaire seeks to examine central org/

subordinate relationships and reportingNew web page on group rulings:www.irs.gov/Charities-&-Non-Profits/Group-Exemption-Rulings-and-

Group-Returns

13

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 15/59

©Copyright Tate & Tryon 2013

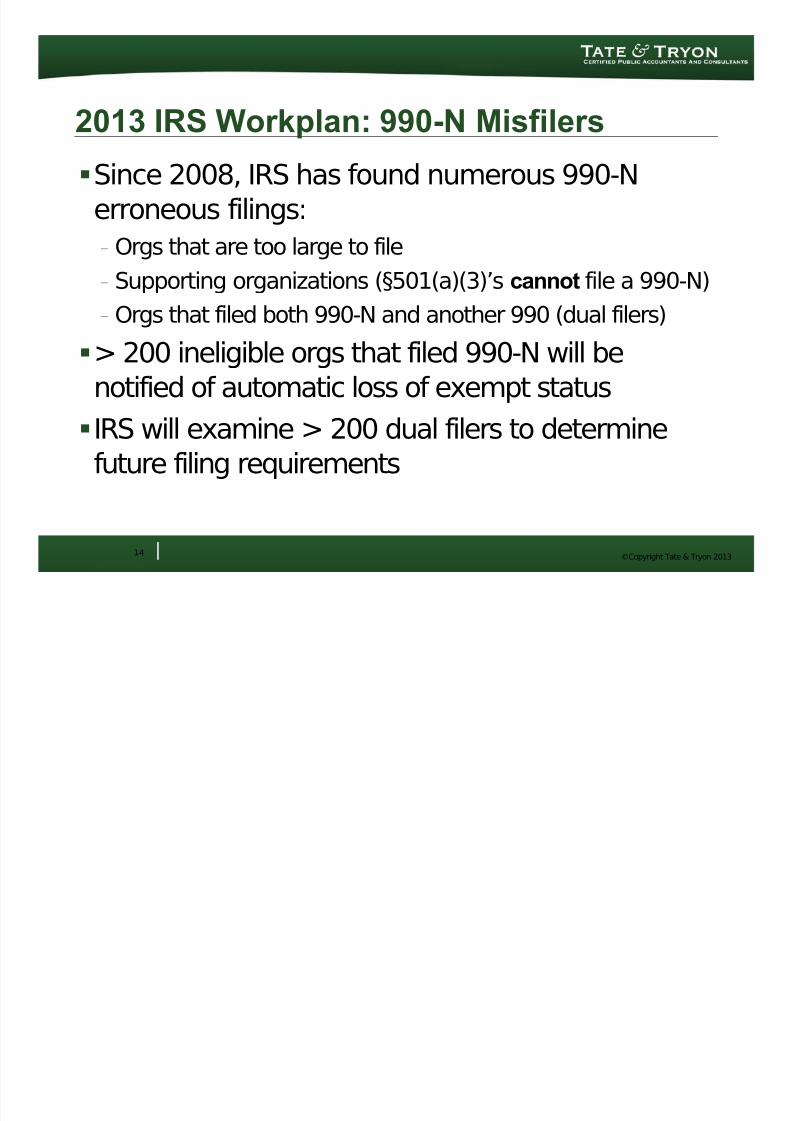

2013 IRS Workplan: 990-N Misfilers

Since 2008, IRS has found numerous 990-N

erroneous filings:- Orgs that are too large to file

- Supporting organizations (§501(a)(3)’s cannot file a 990-N)

-

Orgs that filed both 990-N and another 990 (dual filers)> 200 ineligible orgs that filed 990-N will benotified of automatic loss of exempt status

IRS will examine > 200 dual filers to determinefuture filing requirements

14

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 16/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: “Self Declared” Exempt Orgs

§501(c)(4)/(5)/(6) orgs can declare themselves

exempt without asking for determinationIRS will send out a questionnaire to 2010/2011“self-declarers” to determine correctness of

classification and complianceIRS is no longer granting automatic retroactiveexemption to Form 1024 filers! (Rev. Proc. 2013-9)

- IRS is adopting the 27-month rule that now applies toForm 1023 filers

15

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 17/59

©Copyright Tate & Tryon 2013

2013 IRS Workplan: Miscellaneous

“Plain language” writing courses will be extended

to tax law specialists in Rulings and AgreementsAuto-revocation – IRS will update AutomaticRevocation List monthly

IRS will be developing new communications andmaterials designed to meet the tax needs of smallexempt organizations

IRS will debut an interactive, educational online

version of Form 1023

16

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 18/59

©Copyright Tate & Tryon 201317

Form 990 2012: Form and

Instruction Update

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 19/59

©Copyright Tate & Tryon 2013

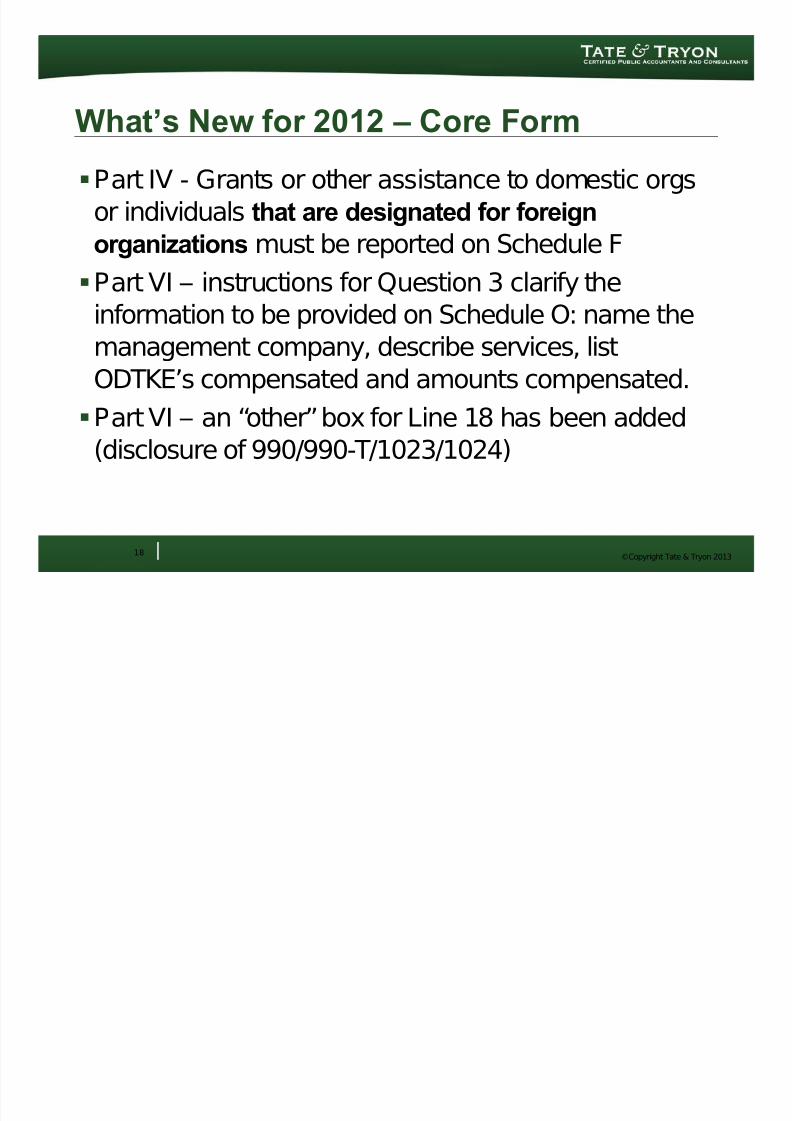

What’s New for 2012 – Core Form

Part IV - Grants or other assistance to domestic orgs

or individuals that are designated for foreignorganizations must be reported on Schedule F

Part VI – instructions for Question 3 clarify the

information to be provided on Schedule O: name themanagement company, describe services, list

ODTKE’s compensated and amounts compensated.

Part VI – an “other” box for Line 18 has been added(disclosure of 990/990-T/1023/1024)

18

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 20/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – Core Form

Part VII – you now mustinclude averagehours/week for related orgs

Section A providesinstructions for reporting

self-insured medical planbenefits (page 31)

Section B, independent

contractors – insuranceproviders should not bereported (nor public utilities,either)

19

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 21/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – Core Form

Part VIII – You are no longer required to report

revenue from J V’s and partnerships on a K-1 basisPart VIII – a §501(c)(3) organization must treat all S

corporation income as UBI; gain on disposition of S

corporation stock is also UBI (§512(e))Part VIII – if you get any Forms 1099-K: report on

appropriate line based on nature of the payments

(i.e

., contribution, income from sale of inventory)- Keep 1099-K copies with your records

20

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 22/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – Core Form

Part IX – Line 3, grants

and assistance must now

include grants to U.S. orgs

or individuals that are

designated for foreign

orgs or individuals

Part IX – new Line 11g: if

“other” fees > 10% of total

expenses, then detail onSchedule O

21

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 23/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – Core Form

Part IX – You are no

longer required toreport assets from J V’sand partnerships on a

K-1 basis

Part IX – Line 6:receivables reported

here trigger Schedule Ldisclosure

22

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 24/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – Core Form

Part XI – new lines

(because Schedule Dreconciliation is gone)

Part XII – simplereformatting of compiled/

reviewed/ auditedstatements question

23

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 25/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – Glossary

“Disqualified person” definition clarifies that if a 5-

year disqualification period ends within the org’stax year, it may treat the person as disqualified for

the entire year

“Grants and other assistance” no longer includes“program-related investments” (Schedule F)

“Professional fundraising services” now includes

“preparation of applications for grants or otherassistance.”

24

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 26/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – Miscellaneous

If an organization accepts a contribution in the

name of one its programs, the donoracknowledgement should indicate the

organization’s name – not the program’s name

IRS reminds filers not to include social securitynumbers on 990 or 990-EZ

Form 990-EZ, Part IV – officer/director address no

longer required

25

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 27/59

©Copyright Tate & Tryon 2013

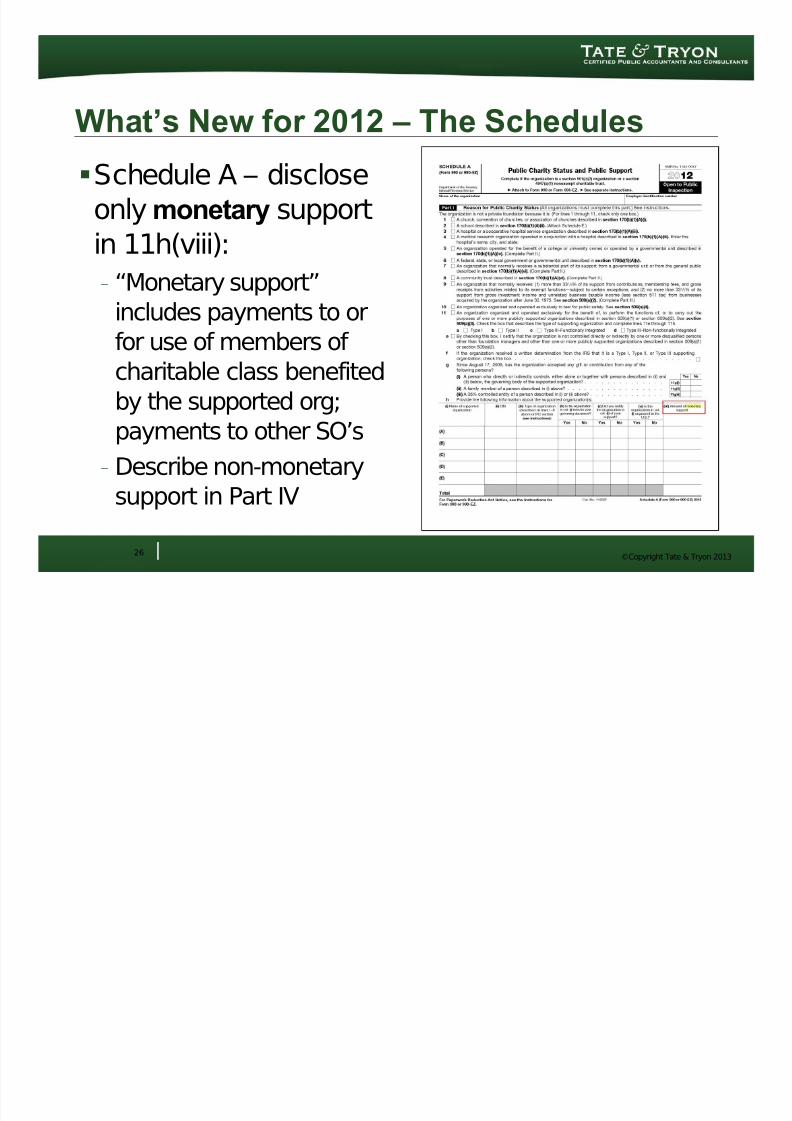

What’s New for 2012 – The Schedules

Schedule A – disclose

only monetary supportin 11h(viii):

- “Monetary support”includes payments to orfor use of members of charitable class benefitedby the supported org;

payments to other SO’s- Describe non-monetarysupport in Part IV

26

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 28/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – The Schedules Schedule B – accrual method organizations reporting

pledges of non-cash property must check the “non-cash” box

and fill out Part II, even if property not received by year-end Schedule C – special focus coming up

Schedule D – Part IX, Reconciliation, has been eliminated

Schedule D – donor-advised funds reportable in Part I are notlimited to funds or accounts that meet the GAAP “funds”definition

Schedule D – The FIN 48 footnote needs to be reported

regardless standards used to determine (FIN 48, ASC 740,

IFRS, or other)

Schedule F – special focus coming up

27

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 29/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – The Schedules

Schedule G – for Part II, Line 2, all contributions

related to a fundraising event should be reported, not just charitable contributions

Schedule H – hospital-related schedule, N/A

Schedule I – removed a checkbox, nothing otherwiseSchedule J – new example of how to report value of

benefits from a nonqualified benefit plan

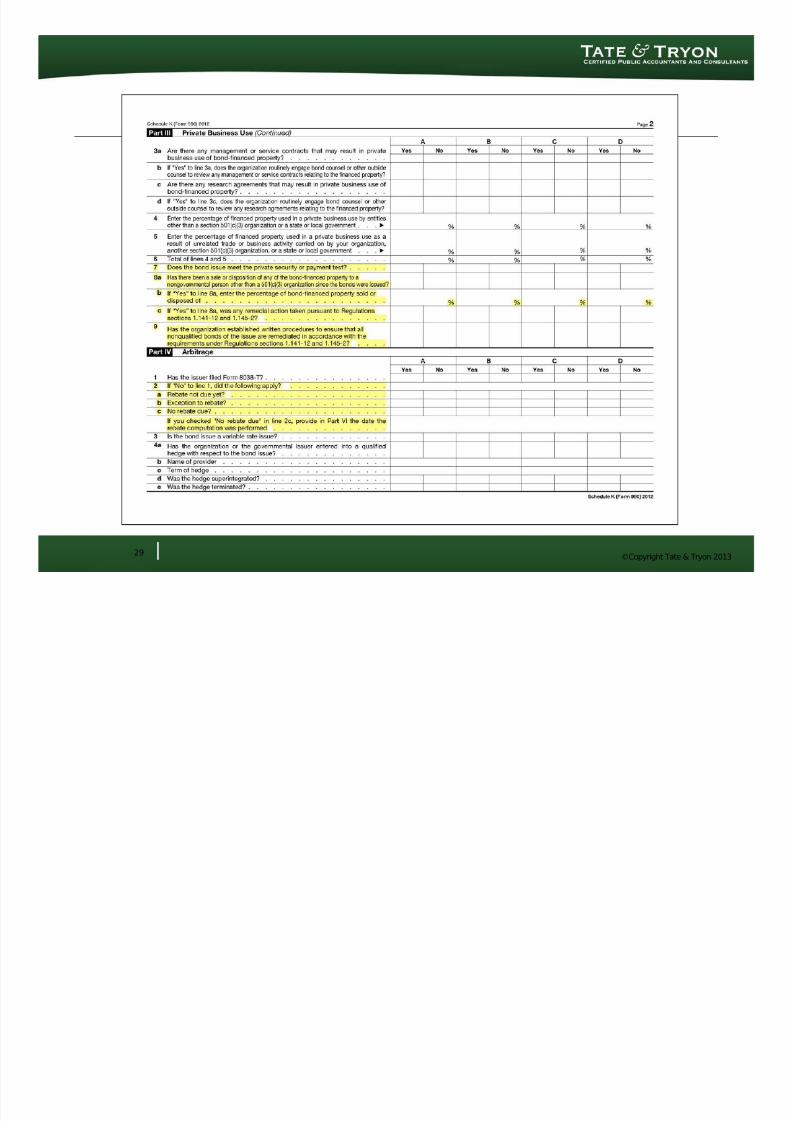

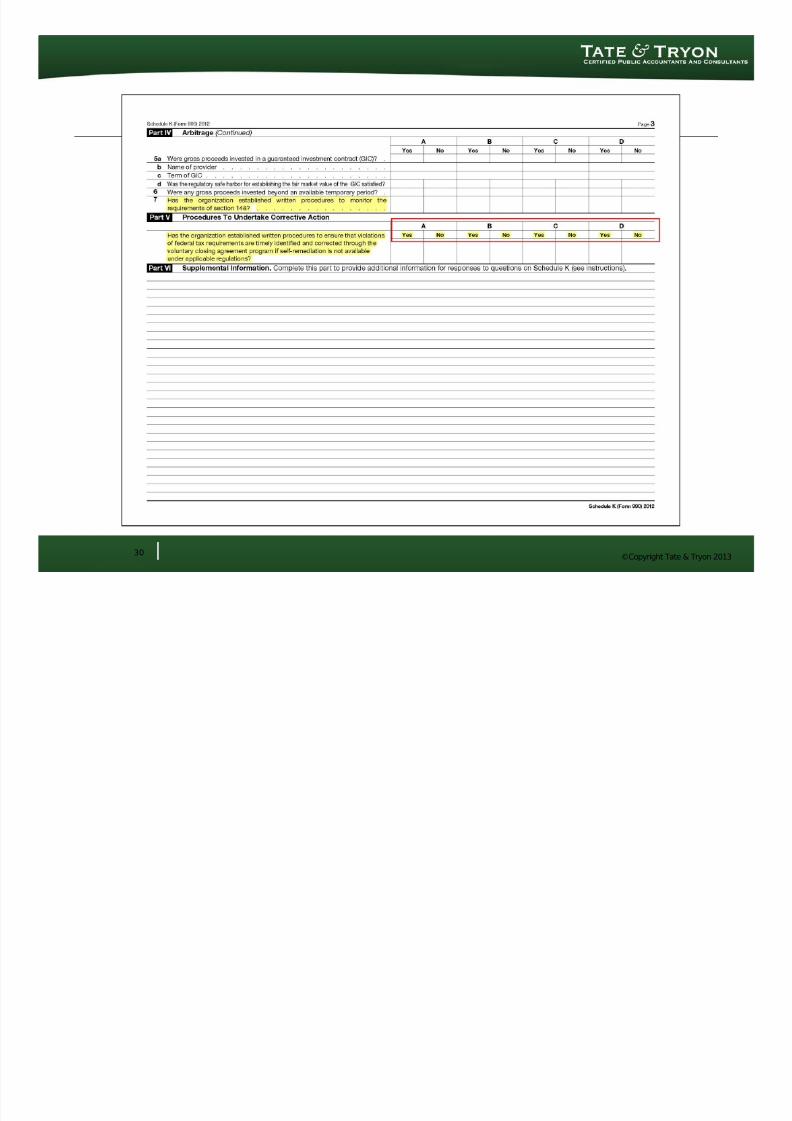

Schedule K – significant new questions regarding salesand dispositions of bond-financed property, rebates,

etc.

28

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 30/59

©Copyright Tate & Tryon 201329

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 31/59

©Copyright Tate & Tryon 201330

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 32/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – The Schedules

Schedule L – special focus coming up

Schedule M – definition of a “qualified organization”for purposes of a qualified conservation contribution

Schedule N – revision of “significant disposition of net

assets” to exclude grants or other assistance made inthe ordinary course of exempt activities

Schedule N – organizations winding up but not yet

terminated should not fill out Part I, but may need tocomplete Part II

31

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 33/59

©Copyright Tate & Tryon 2013

What’s New for 2012 – The Schedules

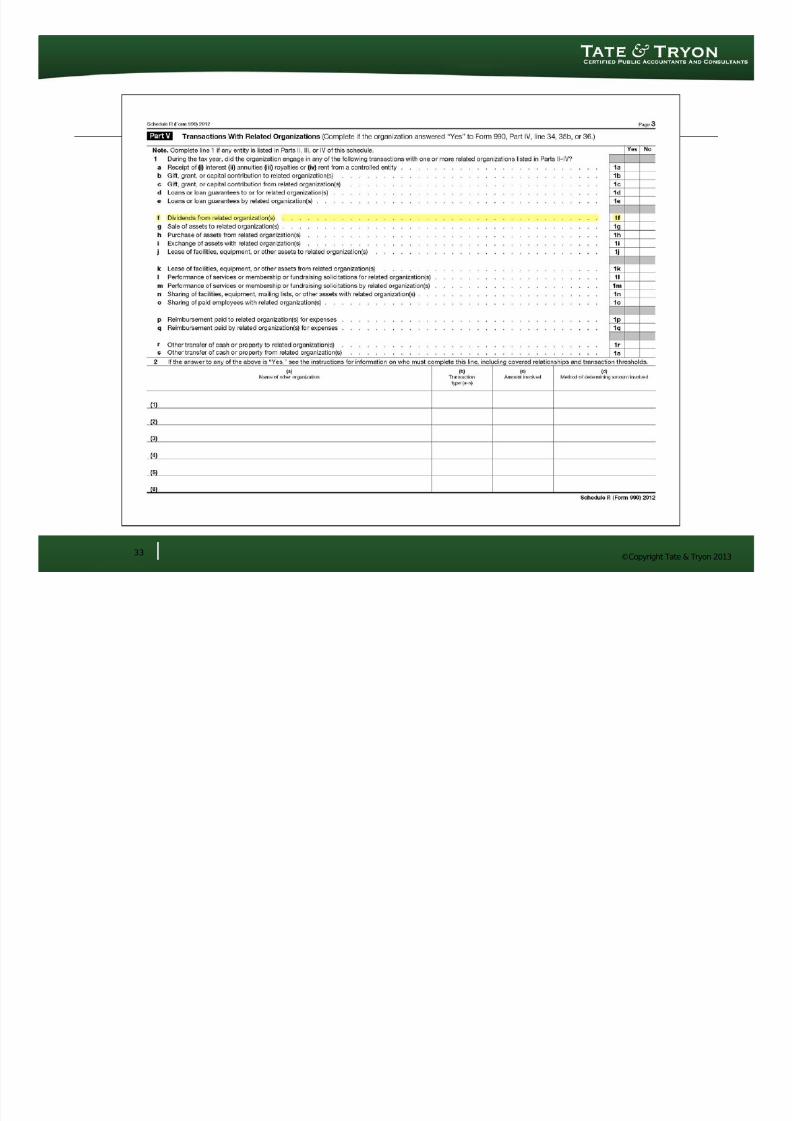

Schedule R – new section in instructions

regarding what VEBAs need to reportSchedule R – 3 more examples of “indirectcontrol” for schedule reporting purposes

Schedule R – Part IV now has a “§512(b)(13)controlled entity” column

Schedule R – Part V has a new item: “Dividends

from related organizations”

32

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 34/59

©Copyright Tate & Tryon 201333

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 35/59

©Copyright Tate & Tryon 201334

Form 990 2012:

Focus on Schedule C

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 36/59

©Copyright Tate & Tryon 2013

Schedule C – What Are the Trigger Questions?

35

Identicalto 2012

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 37/59

©Copyright Tate & Tryon 2013

Schedule C – Political Activity Reporting

36

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 38/59

©Copyright Tate & Tryon 2013

Part I-A – for (Almost) Everyone

Report both direct and indirect political campaignactivities

- Line 1: requires a Part IV narrative description – even if only activity is through a connected PAC

- Line 2: Correctly-handled PAC contributions are NOTreported here; everything else isLine 3: Report volunteer hours for the organization’s own

political activities – not those of connected PAC

37

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 39/59

©Copyright Tate & Tryon 2013

Part I-B – Sec. 501(c)(3) ONLY

The term “political expenditure” means any amount paid or incurred by a

section 501(c)(3) organization in any participation in, or intervention in

(including the publication or distribution of statements), any political

campaign on behalf of (or in opposition to) any candidate for publicoffice. – §4955(d)(1)

Part I-B asks about excise taxes imposed by§4955 inconnection with political expenditures …

So, Part I-B is never filled out … unless a§501(c)(3) hasdone something it shouldn’t have!

38

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 40/59

©Copyright Tate & Tryon 2013

Part I-C – Everyone BUT Section 501(c)(3)

39

Report both political

contributions shunted to

your PAC and your own

political expenditures, if any

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 41/59

©Copyright Tate & Tryon 2013

Part II-A – Lobbying under Section 501(h)

40

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 42/59

©Copyright Tate & Tryon 2013

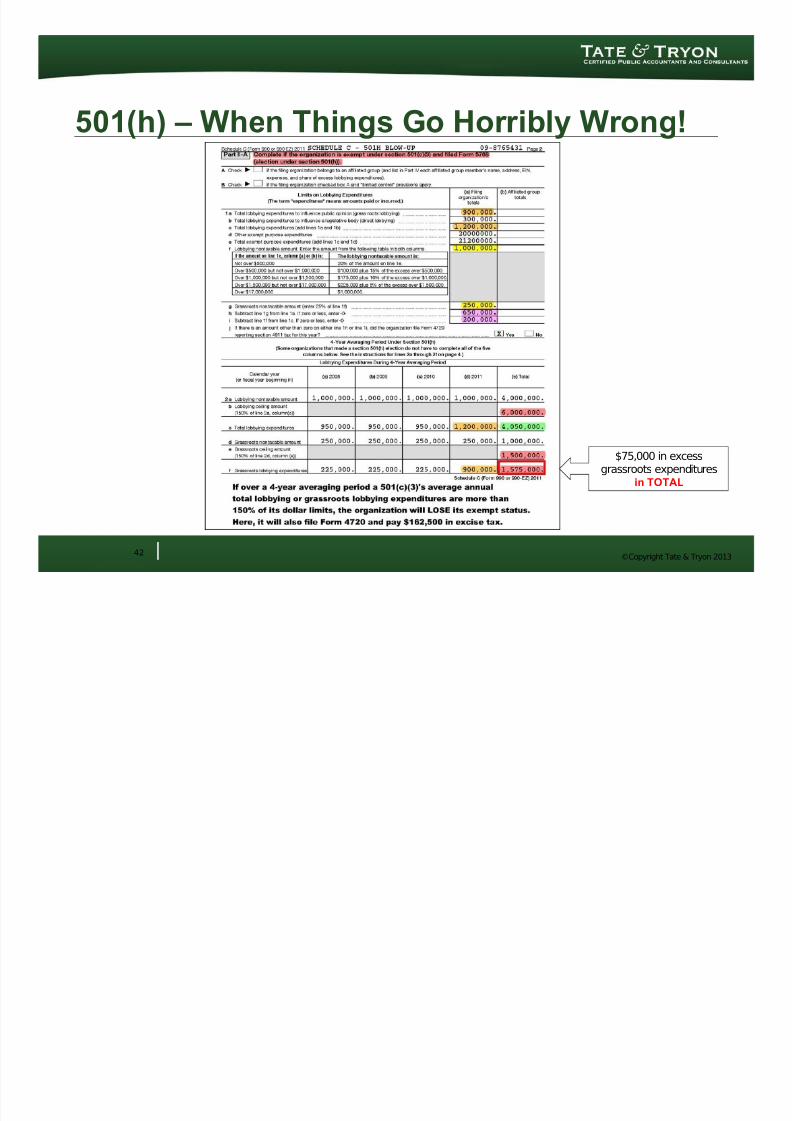

501(h) – When Things Go Somewhat Wrong

41

$1,100,000 excesslobbying expenditures in

2011 ONLY

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 43/59

©Copyright Tate & Tryon 2013

501(h) – When Things Go Horribly Wrong!

42

$75,000 in excessgrassroots expenditures

in TOTAL

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 44/59

©Copyright Tate & Tryon 2013

What Happens When a §501(c)(3) Fails 501(h)?

It does NOT get §501(c)(4) status (even though it might

otherwise qualify)

It becomes a taxable organization (usually a corporation)

GCM 39813: tax treatment of –

- Gross receipts of trade/business activities - taxable

- Income from investment and other formerly “excluded” activities -taxable

- “Good faith” contributions – generally nontaxable under §102

- Donors may be subject to gift tax

43

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 45/59

©Copyright Tate & Tryon 2013

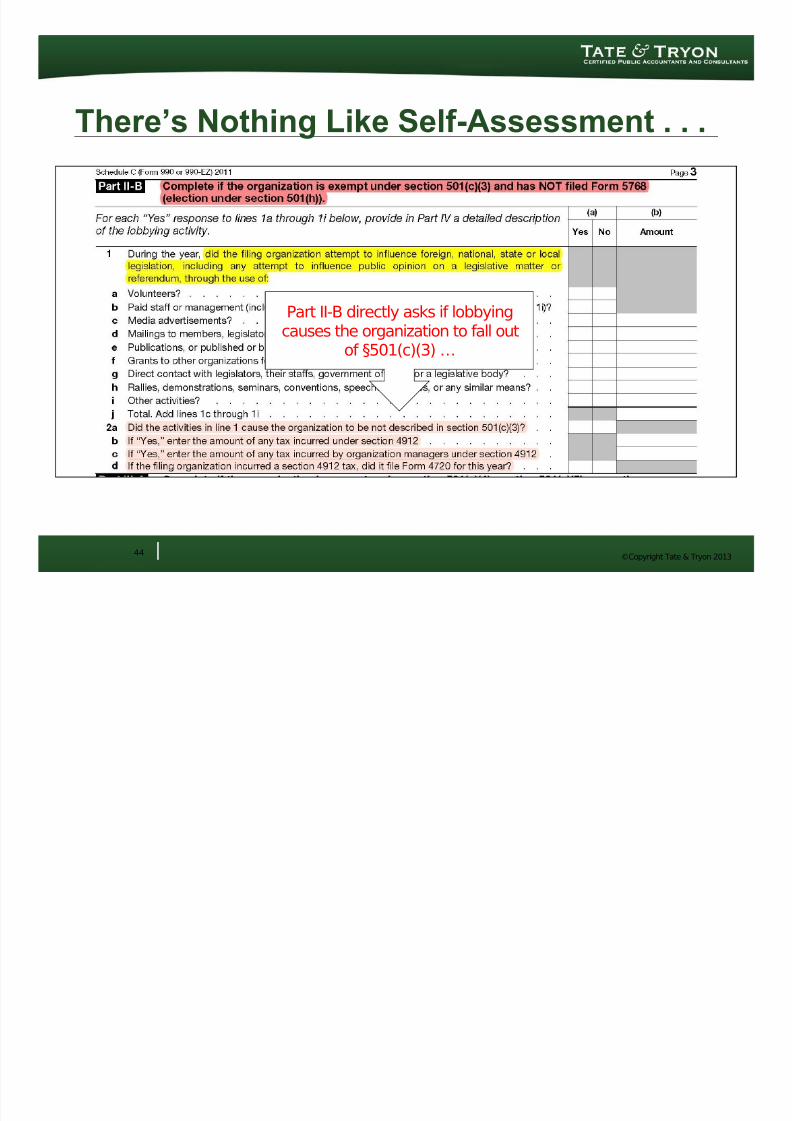

There’s Nothing Like Self-Assessment . . .

44

Part II-B directly asks if lobbying

causes the organization to fall outof §501(c)(3) …

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 46/59

©Copyright Tate & Tryon 2013

Part III – Section 501(c)(4), (5), (6) Lobbying

45

"Dues payments, contributions or gifts to XYZ Associationare not tax deductible as charitable contributions for federalincome tax purposes. However, they may be deductible as

ordinary and necessary business expenses subject torestrictions imposed as a result of XYZ's lobbying activities

as defined by the Budget Reconciliation Act of 1993. XYZestimates that the nondeductible portion of your 20XX dues

-- the portion that is allocable to lobbying -- is ___%.“

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 47/59

©Copyright Tate & Tryon 201346

Form 990 2012:

Focus on Schedule F

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 48/59

©Copyright Tate & Tryon 2013

Focus on Schedule F2012 updates:

- Expenditures and investments in a single region are

to be reported on separate lines

- Foreign program-related investments go in Part I,

but not Parts II and III

- Grants and other assistance to US organizations or

individuals destined for foreign organizations are

reportable in Parts II and III

“ . . . To or for the use of foreign organizations, foreign

governments, foreign individuals, and U.S. individuals or

entities for foreign activity . . .”

47

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 49/59

©Copyright Tate & Tryon 2013

Make Sure You Are Capturing All Expenses

“Expenditures include salaries, wages, and other

employment-related costs paid to or for the benefit of employees located in the region; travel expenses to, from,and within the region; rent and other costs relating to offices

located in the region; grants to or for recipients located in

the region; bank fees and other financial accountmaintenance fees and costs; and payments to agents

located in the region. Report expenditures based on the

method used to account for them on the organization'sfinancial statements, and describe this method in Part V.”

48

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 50/59

©Copyright Tate & Tryon 2013

A Few Details . . .Foreign investments held through a domestic entity are notreportable (“domicile” is not foreign)

You may round off both investments and expenses to thenearest $1,000

For 2012, you may skip allocating indirect expenditures to

foreign activities if you don’t already separately track themFor “grants and other assistance” do not include salariesor payments to independent contractors, or payments toaffiliates that are not separate legal entities

Even if you have no expenditures for an activity, you mustreport the activity in Part I if you derived more than$10,000 in revenue from its operations

49

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 51/59

©Copyright Tate & Tryon 2013

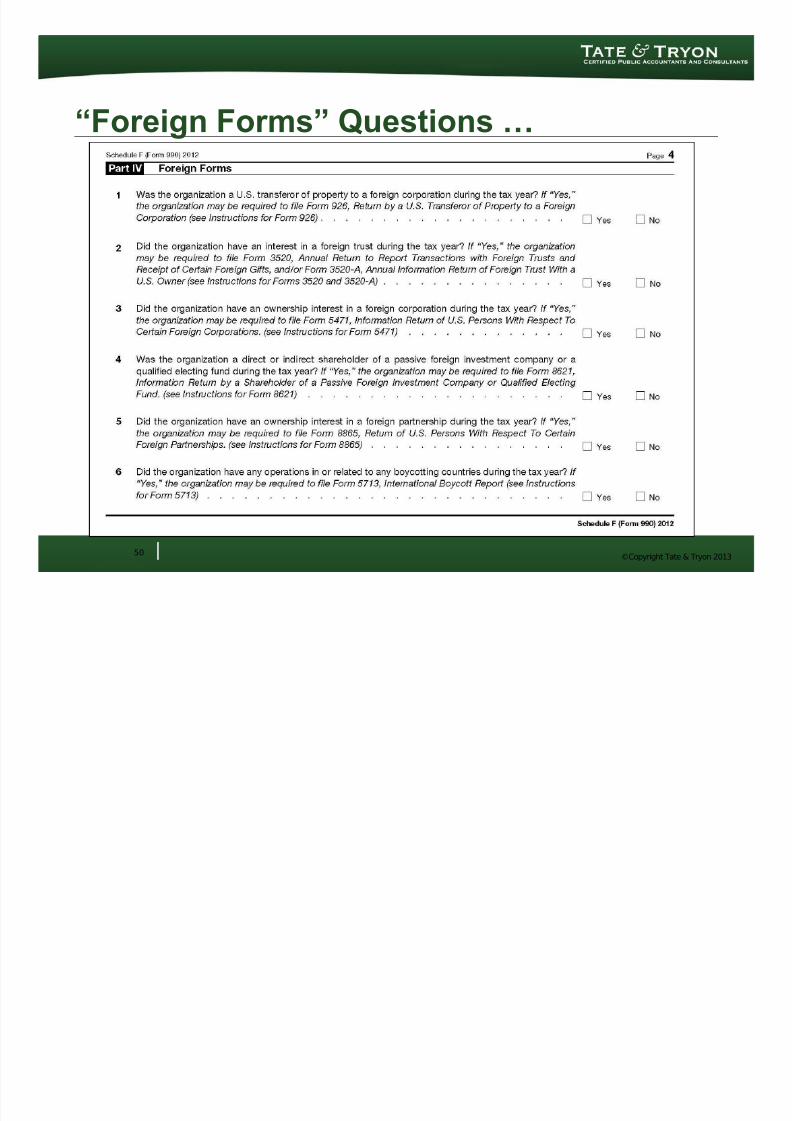

“Foreign Forms” Questions …

50

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 52/59

©Copyright Tate & Tryon 2013

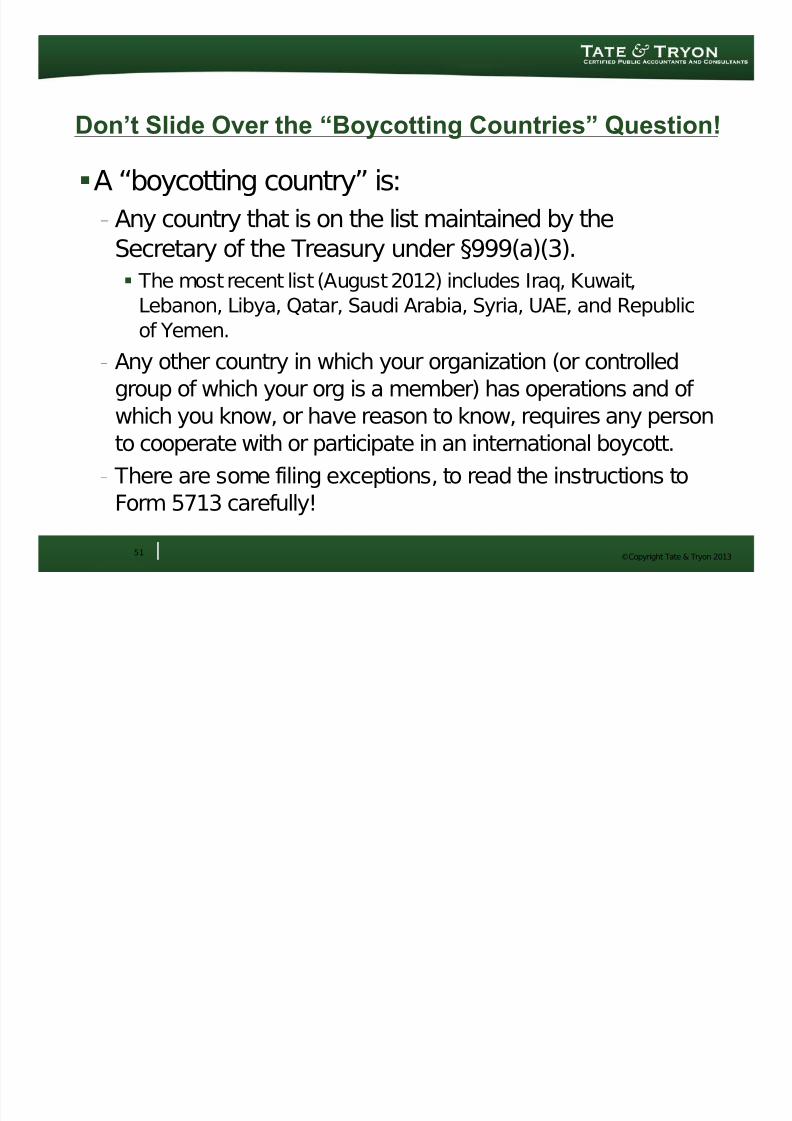

Don’t Slide Over the “Boycotting Countries” Question!

A “boycotting country” is:

- Any country that is on the list maintained by theSecretary of the Treasury under §999(a)(3).

The most recent list (August 2012) includes Iraq, Kuwait,

Lebanon, Libya, Qatar, Saudi Arabia, Syria, UAE, and Republic

of Yemen.- Any other country in which your organization (or controlled

group of which your org is a member) has operations and of which you know, or have reason to know, requires any person

to cooperate with or participate in an international boycott.- There are some filing exceptions, to read the instructions to

Form 5713 carefully!

51

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 53/59

©Copyright Tate & Tryon 201352

Form 990 2012:

Focus on Schedule L

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 54/59

©Copyright Tate & Tryon 2013

Focus on Schedule LNew columns in Parts I, II, III

Part I asks for amount of tax

“incurred by” … formerly“imposed on”

Part II emphasis placed on

amounts reported in Part X(balance sheet), lines 5, 6, 22

Part IV clarification that bankdeposits/ withdrawals are notreportable if made in ordinarycourse of business

53

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 55/59

©Copyright Tate & Tryon 2013

“Interested Person” Includes for Part IV:

An entity (other than a section501(c)(3) organization, a section

501(c) organization of the samesubsection as the filing

organization, or a governmental

unit or instrumentality) more than

35% owned or controlled, directly orindirectly, individually or collectively,

by one or more current or formerofficers, directors, trustees, or key

employees listed on Form 990, PartVII, Section A, or their family

members.

54

Note that disclosure is

required only if there arereportable transactions.

But between related

exempt orgs, there usually

are! See pages 3 and 4 of

Schedule L instructions.

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 56/59

©Copyright Tate & Tryon 2013

How To Determine “More than 35%” Control

“For purposes of this Part IV, a nonprofit organization is'more than 35%' controlled when more than 35% of its

directors or trustees either (a) consist of interested personsof the filing organization, or (b) serve as directors or trusteessubject to powers held by one or more interested persons of

the filing organization to elect or appoint, or remove andreplace, such directors or trustees or the members that elect

or appoint them.”

55

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 57/59

©Copyright Tate & Tryon 2013

Yes

No

Yes

Not Reportable

Not Reportable

Sch L threshold business transactions?

> 35% control?

Is other org a 501(c)(3) or same 501(c) type?

Not ReportableYes

Reportable On Sch L Pt IV

I s T h

a t O r g R e p o r t a b l e

o n S c h e d u l e L ? No

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 58/59

©Copyright Tate & Tryon 2013

Schedule L “Related” Orgs – Effect on 990, Part VI

3. Neither the member, nor any familymember of the member, was involved in atransaction with the organization (whetherdirectly or indirectly through affiliation withanother organization) that is required to bereported on Schedule L (Form 990 or 990-

EZ) for the organization's tax year.

4. Neither the member, nor any family memberof the member, was involved in atransaction with a taxable or tax-exemptrelated organization (whether directly or

indirectly through affiliation with anotherorganization) of a type and amount thatwould be reportable on Schedule L (Form990 or 990-EZ) if required to be filed by therelated organization.

57

“Independent” voting members mustpass these two criteria (and 2 more):

7/29/2019 2012 IRS Form 990 Whats New - Whats Important

http://slidepdf.com/reader/full/2012-irs-form-990-whats-new-whats-important 59/59

©Copyright Tate & Tryon 2013

Questions??

58