2012-09-20 Market Power Shifting to Subsea Equipment Players - D. Gacicia

54

People. Ideas. Success. Guggenheim Securities, LLC Oil Services & Equipment September 20, 2012 Darren Gacicia (212) 293-3054 [email protected] Robert Miller - Associate (972) 638-5504 [email protected] Market Power Shifting to Subsea Equipment Players Upgrading FTI to Buy From Neutral GUGGENHEIM SECURITIES, LLC See pages 53 - 54 for analyst certification and important disclosures.

-

Upload

darren-gacicia -

Category

Documents

-

view

405 -

download

0

Transcript of 2012-09-20 Market Power Shifting to Subsea Equipment Players - D. Gacicia

People. Ideas. Success.

Guggenheim Securities, LLC Oil Services & Equipment

September 20, 2012

Darren Gacicia

(212) 293-3054

Robert Miller - Associate

(972) 638-5504

Market Power Shifting to Subsea Equipment Players Upgrading FTI to Buy From Neutral

GUGGENHEIM SECURITIES, LLC See pages 53 - 54 for analyst certification and important disclosures.

Investment Thesis

Market Power Shifting Toward Subsea Equipment Players. The credit crisis and recession, coupled with the Macondo incident, slowed offshore activity and

demand of equipment from 2008-2010. Market power shifted to offshore operators, as oilfield equipment players competed to win awards amid more limited

subsea tree demand. The inflection of offshore activity in 2011 marked a migration in market power back to the oilfield equipment players. In this report, we track

the shift in market power with a “deep dive” into the subsea tree business, through an in-depth analysis of subsea tree demand, manufacturing capacity, orders,

and backlog across the industry. Our analysis distills to our conclusion that visibility for demand from offshore fleet growth, rising utilization, and emergent signs of

capacity constraints likely translate into revenue growth (asset turns), improved mix/pricing (higher margins), and returns for oilfield equipment players. Given

operating leverage across equipment businesses, we believe the stage is set for upward revisions to consensus estimates and valuation multiples for subsea

players, and oilfield equipment players more broadly.

High Visibility for Subsea Tree Demand. Our revised subsea tree forecast calls for nearly three times the number of deliveries in 2017 from 2011, a ~19%

CAGR annually. We calibrated our forecast for subsea trees against the Guggenheim/PFC offshore rig supply/demand model and field-by-field data from Infield

(pgs. 10-18). Our new forecast falls below our previous estimates and below popular industry outlooks, as we tailored our assumptions to better represent

relationships with prior tree deliveries, especially related to well water depths. Albeit tempered from our original estimates, strong growth in our new forecast is

anchored by existing orders that support near-term estimates and high visibility into offshore fleet growth (pgs. 12-13). Likewise, our analysis of demand by region

and company, relative to existing orders, planned projects, and potential projects, implies strong new order flow if operators look to schedule deliveries in front of

projects in the coming years (pgs. 15-18).

Capacity Utilization Increasing. Rising demand for subsea trees likely lifts production capacity utilization from below 50% to above 70% and beyond during the

next five years. Within this report, our estimation of manufacturing capacity by major manufacturer and region suggests the subsea tree market is tightening (pgs.

20-22). The key constraints on capacity remain engineers and the supply chain (emphasis on forging), both less adjustable in the near term due to longer training

cycles and capacity/logistical solutions requiring time. As industry backlogs sit above two times current annual production capacity and new order lead times

appear poised to expand, we see potential for pricing power on the horizon (pgs. 24-25, 28).

Asset Turns and Operating Margins Set to Drive ROE Equation. Improved capacity utilization, pricing power, and expanding new order lead times look set to

drive revenue growth, asset turns, and operating margins (pg. 26). A steady rise in average revenue per tree across industry backlogs, either from improved mix or

pricing, supports our view of improving incremental economics, especially as lower margin backlog rolls off (pg. 23). The absorption of production capacity and

lengthening of lead times may also give equipment providers sway to push for greater subsea tree design standardization, likely a further boost to turns of existing

capacity and a benefit to bottom line economics (pgs. 21, 24-25). In our view, subsea tree estimates remain low as we emerge from the recession-driven lull in

tree orders and deliveries (pg. 12). Amid low expectations, we see room for upward revisions to consensus estimates and re-rating of multiples higher as investors

discount greater earnings growth.

Upgrading FTI to Buy from Neutral, Raising Price Target to $64, Increasing 2013 estimates. We are upgrading FMC Technologies to Buy from Neutral and

raising our price target to $64 from $46. Likewise, we are raising our 2013 EPS estimate to $2.70 from $2.65. As the largest subsea tree provider, FTI has the

greatest leverage to improving subsea market economics. Over the next 12 months, we believe the positive trajectory of its subsea business will overshadow risks

to its Surface business, implicit from volatility in North American activity. If our bullish thesis plays out, we anticipate upward consensus estimate revisions and

multiple expansion to propel FTI shares higher (pgs. 3, 34-36).

Positive Read-Throughs for CAM, AKSO, & GE (not covered). As most industry players will likely benefit from improved subsea economics, our analysis of the

subsea market supports our estimates and outlooks for our other Buy-rated oilfield equipment companies: Cameron (pgs. 41-42) and Aker Solutions (pgs. 43-44).

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 2

FTI – Upgrading to Buy – Seeking Leverage to Improving Subsea Economics

We are upgrading FTI to Buy from Neutral. We see improving subsea economics

overshadowing North American-related risks to the Surface business. Although risks for

near-term quarters from lower margin subsea backlog remains, we believe the upside from

asset turns from completion of near-term deliveries and incrementally better economics

baked into backlog should outweigh near-term risks that Subsea margins may fall below

2H12 guidance of 12.5-13.5% (pg. 35). Forecasted to expand from ~55% of operating

income, we think the outlook for the continued improvement in the trajectory of Subsea

margins since 4Q11 will remain the key driver for FTI shares. Given operating leverage in

FTI’s business model from outsourcing, we see potential upward revisions to consensus

earnings estimates with growth in the Subsea business. Additionally, we see valuation

multiple expansion for the shares as the combination of growth and a favorable return

structure hits stride. We would take advantage of the current consolidation within FTI shares

as an entry point.

Raising Our Price Target & 2013 Estimate. We are raising our price target to $64 from

$46. Given our more positive outlook, we are raising our 2013E EPS to $2.70 from $2.65.

Subsea Technologies Growth to Take Lead. After gaining 600bps of market share from

2009-2011, a competitive bidding environment and lower margin backlog has forced 2012

Subsea margin guidance down to 11-12%. Improved revenue/tree in backlog and visibility

into accelerating deliveries into 2013 (pg. 35), likely improves revenue, asset turns, and

margins through 2H12. As a result, we are more confident in 2H12 Subsea margin guidance

for an uptick to 12.5-13.5%. As industry manufacturing capacity tightens and lead times

expand, we see room for improved pricing and greater standardization of tree orders, which

may propel subsea economics ahead of our current estimates.

Surface Technologies Remains a Risk, but Reflected in Estimates. Our forecast for a

2H12 decline in North American activity risks 18-20% 2012 margin guidance for the Surface

business and leads our margin numbers lower for 2013, as backlog protection fades.

Exposure to North American surface wellheads, as well as pressure pumping equipment,

rentals, and consumables, lead us to revise our estimates below current guidance (pg. 36).

Although strength in international businesses may offset downside, negative revision risk

likely remains. In our view, upside in the Subsea business will offset this drag.

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12E

4Q

12E

1Q

13E

2Q

13E

3Q

13E

Segm

ent

Revenue (

$m

)

Subsea Technologies Surface Technologies Energy Infrastructure

15%

25%

35%

45%

55%

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12E

1Q

13E

3Q

13E

1Q

14E

3Q

14E

1Q

15E

3Q

15E

Retu

rn o

n E

quity(A

nnualz

ed Q

uart

ers

)

Source: Company Reports, Guggenheim Securities, LLC

Source: Company Reports, Guggenheim Securities, LLC

FTI Annualized Return on Equity

FTI Segment Revenue Breakdown

Source: FactSet, Guggenheim Securities, LLC

Company Category 2008 2009 2010 2011 2012E 2013E 1Q12 2Q12 3Q12E 4Q12E 1Q13E 2Q13E 3Q13E 4Q13E

FMC Technologies EPS 2.94 2.93 3.06 1.64 2.00 2.70 0.41 0.43 0.56 0.60 0.63 0.65 0.67 0.74

Previous EPS 2.00 2.65 0.56 0.60 0.63 0.64 0.66 0.72

Consensus EPS 2.09 2.61 0.57 0.64 0.56 0.61 0.67 0.73

Consensus EPS-High 2.16 2.90 0.60 0.71 0.63 0.66 0.73 0.87

Consensus EPS-Low 2.00 2.00 0.54 0.57 0.52 0.50 0.49 0.49

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 3

Guggenheim Subsea Tree Forecast Expected to Grow at 19% CAGR 2011-2017

269 258

386 338

296

237 262

464 496

539

613

736 753 757 807

853

-

100

200

300

400

500

600

700

800

900

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

2017E

2018E

2019E

2020E

Subse

a T

ree D

eliv

eries

Worldwide Subsea Tree Expected Deliveries Worldwide Subsea Tree Deliveries

Guggenheim Annual Worldwide Subsea Tree Deliveries History & Forecast

Source: Infield, PFC Energy - Guggenheim

Actual subsea tree deliveries into

the market

Subsea tree deliveries expected

to nearly triple from 2011 to 2017

The subsea tree market expected

to grow at 19% CAGR from

2011-2017

Our forecast sees 2012 surpass

previous high delivery year of

2007

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 4

Manufacturing Capacity Utilization Suggests Market Power for Equipment Names

138

173

182

230

298

306

331

336

351

363

384

410

498

515

534

548

558

628

713

718

718

64%

74%

67%

75%

82%

54%

70%

66%58%

44%

70%

63%

77%

66%

55%

43%

47%

74%

70%

75%

85%

-

100

200

300

400

500

600

700

800

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

Subse

a T

ree M

anufa

cturin

g C

apacity

Capaci

ty U

tiliz

ation

Subsea Tree Manufacturing Capacity Capacity Utilization

Guggenheim Estimated Subsea Tree Production Capacity

Source: Infield, Guggenheim Securities, LLC

The ramp in estimated

deliveries in 2012 and

beyond looks set to rapidly

increase utilization of

subsea tree manufacturing

capacity across the

industry, despite capacity

expansions for all of the

major equipment providers.

The subsea tree market is

headed back to utilization

levels that heralded high

margins, high assets turns,

and favorable return

structures during that last

cycle.

We see potential for rising utilization to push

toward more standardized tree designs in order to

minimize engineering bottlenecks seen with

specially designed trees.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 5

Visible Near-Term Demand Supports Estimates & Suggests Strong Order Flow

464 496

539

613

736 753 757 807

853

436 396

253

156 110

52 36 17 8

-

100

200

300

400

500

600

700

800

900

2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Subse

a T

ree

Deliv

eries

Guggenheim Subsea Tree Demand Forecast Ordered Wedge

Guggenheim Worldwide Subsea Tree Demand vs. Current Orderbook Existing orders and delivery dates support

our delivery forecast for 2012 and 2013.

In our view, the market does not see the

ramp in scheduled deliveries during this

year and next, which should both drive

capacity utilization and burn off lower

margin backlog awarded during the recent

downturn.

Unordered portions of demand should

translate into strong new order numbers

across companies over the next few

years.

Source: Infield, PFC Energy - Guggenheim

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 6

164 231

222

205

159

269

258

386

338

296

237

262

599 632 6

92

769

868

-

100

200

300

400

500

600

700

800

900

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

Subse

a T

ree D

eliv

eries

Guggenheim's Previous Forecast

164 231

222

205

159

269

258

386

338

296

237

262

464

496

539 6

13

736

164

231

222

205

159

269

258

386

338

296

237

262

436

396

253

156

110

-

100

200

300

400

500

600

700

800

900

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

Subse

a T

ree D

eliv

eries

Total Forecast Demand Delivered/Ordered

New Forecast More Conservative Than Previous Estimates

Guggenheim Annual Worldwide Subsea Tree

Deliveries History & Forecast

Source: Infield, PFC Energy - Guggenheim

Guggenheim Previous Forecast, Before Tighter

Calibration Against Historical Deliveries

Source: PFC Energy - Guggenheim

Our forecast becomes more conservative after back testing

historical well counts and tree deliveries. The key drivers of the

downward revisions stem from lowered expected subsea tree

demand from shallow water projects.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 7

164 231

222

205

159

269

258

386

338

296

237

262

464

496

539 6

13

736

164

231

222

205

159

269

258

386

338

296

237

262

436

396

253

156

110

-

100

200

300

400

500

600

700

800

900

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

Subse

a T

ree D

eliv

eries

Total Forecast Demand Delivered/Ordered438

462

452

432

318 3

74

311

551

661

664 7

23

798

0

100

200

300

400

500

600

700

800

900

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

Subse

a T

ree A

ward

s

FMC Industry Awards

Multi-Year Book-to-Build Ratio Above “1” ─ Positive Demand Indicator

Guggenheim Annual Worldwide Subsea Tree

Deliveries History & Forecast

Source: Infield, PFC Energy - Guggenheim

FMC Forecasted Industry Subsea Tree Awards as

Attributed to Quest Offshore

Source: FMC Company Presentation, Guggenheim Securities, LLC

Awards can run higher than

deliveries in any given year, as

future large orders may have

multi-year lead times.

Our forecast differs in both

approach and scale relative to

other benchmarks published in

company presentations.

Although a Quest number, FTI

guidance sees ~400-500 wet

trees ordered in 2012.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 8

Key Drivers & Assumptions

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 9

Guggenheim/PFC Offshore Rig Demand Model Supports & Constrains Subsea

Tree Demand Outlook

Source: RigLogix, PFC Energy-Guggenheim Source: RigLogix, PFC Energy-Guggenheim

20 22 26 32 36 38 44 55 63 69 94 92 88

92 97

83 82 84 80

88

103 105 101 100 99

-

50

100

150

200

250

300

350

400

2012E 2013E 2014E 2015E 2016E

Num

ber

of

Rig

s

7500+ WD 5000-7500 WD3000-5000 WD 1000-3000 WD400-1000 WD UDW SupplyUDW & DW Supply UDW&DW&MW Supply

99 99 98 101 109

331 331 330 333 339

-

50

100

150

200

250

300

350

400

450

500

2012E 2013E 2014E 2015E 2016E

Num

ber

of

Rig

s

300-400000-300Premium & High End JackupsStandard & Lower Spec Jackups

Global Supply / Demand of Floaters Global Supply / Demand of Jackups

We derive our subsea tree model from our offshore rig supply/demand

model. Within this context, we cross-reference input data from PFC

Energy with Infield data.

Potential demand could be much greater if not constrained by rig

undersupply. Accordingly, as further new floater constructions are

announced, our model would continue to suggest upward demand

revisions for subsea trees.

Historically, shallow water activity has not proved a large source of subsea

tree demand. Our forecast for high jackup utilization, especially for

premium rigs, may offer potential upside to subsea tree demand, as plays

become both more complex and remote from existing infrastructure.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 10

Assumptions Applied to Guggenheim/PFC Offshore Rig Supply/Demand Model

2005 2006 2007 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Percent of Wells Needing Tieback (by well type)

Exploration 5% 5% 5% 5% 5% 5% 5% 10% 10% 10% 10% 10% 10% 10% 10% 10%

Appraisal 5% 5% 5% 5% 5% 5% 5% 10% 10% 10% 10% 10% 10% 10% 10% 10%

Development 90% 90% 90% 90% 90% 90% 90% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Percent of Wells Needing a Wet Tree (by water depth)

0-300 WD 5% 5% 5% 5% 5% 5% 5% 7% 7% 7% 7% 7% 7% 7% 7% 7%

300-400 WD 5% 5% 5% 5% 5% 5% 5% 10% 10% 10% 10% 10% 10% 10% 10% 10%

400-1000 WD 10% 10% 10% 10% 10% 10% 10% 20% 25% 30% 35% 40% 45% 45% 45% 45%

1000-3000 WD 30% 30% 30% 30% 30% 30% 30% 40% 45% 50% 55% 60% 65% 65% 65% 65%

3000-5000 WD 60% 60% 60% 60% 60% 60% 60% 65% 75% 80% 85% 90% 95% 95% 95% 95%

5000-7500 WD 80% 80% 80% 80% 80% 80% 80% 90% 95% 100% 100% 100% 100% 100% 100% 100%

7500+ WD 80% 80% 80% 80% 80% 80% 85% 95% 100% 100% 100% 100% 100% 100% 100% 100%

Rig/Frictional Delays

% 0-400 WD Slippage 0% 0% 0% 0% 0% 0% 0% 0% 0%

% 1,000 WD Slippage 10% 13% 15% 15% 15% 15% 15% 15% 15%

Only a smaller number of E&A

wells have needed trees, but we

see more of these wells

transitioned to production in the

future.

We made assumptions to conform previous

subsea tree deliveries with prior well count

data, using “rules of thumb” for the probability

for tree demand among water depths.

As incremental plays become more remote,

moving away from established infrastructure,

we see the penetration of subsea tree demand

increasing, especially in the midwater.

Our forecast factors a certain amount of

demand slippage, as rig shortages push

demand further out.

Source: Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 11

Midwater Subsea Tree Demand Growth Foreshadows Path for Ultra/Deepwater

-

50

100

150

200

250

300

350

400

450

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Subse

a T

ree D

eliv

eries

Shallow Water Midwater Deepwater Ultra Deepwater

Subsea Tree Deliveries by Water Depth

Growth in subsea tree demand

from Midwater drilling grew

slowly with growth of the floater

fleet and transition of drilling

activity from exploration to

development.

The slow growth of subsea tree

demand for Ultra/Deepwater

projects has begun to expand

slowly, similar to what was seen

with the evolution of Midwater

demand.

Shallow water penetration has

also begun to expand, as fields

become both more complex and

more remote.

Source: Infield, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 12

Floater Fleet & Subsea Tree Market Grow in Tandem

Source: Infield, Guggenheim Securities, LLC

Total Subsea Tree Deliveries to Track Floater Deliveries

Exhibit 1: Guggenheim

100

150

200

250

300

350

400

-

100

200

300

400

500

600

700

800

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

2017E

GLobal F

loate

r Fle

et S

izeSubse

a T

ree D

eliv

eries

Total Deliveries Total Floaters

-

50

100

150

200

250

300

350

400

-

50

100

150

200

250

300

350

400

450

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

2017E

Glo

bal F

loate

r Fle

et S

izeSubse

a T

ree O

rders

Total Orders Total Floaters

We see the continued growth of

the floater fleet as directly

correlated with subsea tree

deliveries.

New Orders to Recover with Fleet Growth

The recession and Macondo incidents de-

railed the progression of subsea tree

orders and deliveries. We expect growth

to resume its correlation with floater fleet

growth and drilling activity.

Source: Infield, RigLogix, Guggenheim Securities, LLC Note: 2012 Subsea Orders are shown year-to-date

Source: Infield, RigLogix, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 13

Near-Term Demand More Firm, Rising Activity Supports Possible Demand

164

231

222

205

159 269

258 386

338

296

237

262

436

396

253

156

110

52

36

10 55

133

158

207

187

151

86

18

45

153

300 419

514

570

704

828

-

100

200

300

400

500

600

700

800

900

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

2016E

2017E

2018E

2019E

2020E

Subse

a T

ree D

eliv

eries

Delivered/Ordered Planned Project - Potential Orders Possible Project - Potential Orders

Worldwide Subsea Tree Demand Tiered by Ordered, Planned, and Possible

Source: Infield, PFC Energy - Guggenheim

Ordered and planned demand supports

estimates for 2012-2014.

Visibility on firm demand trails off later in

the forecast. In our view, an increase in

the number of announcement for EPC

and FEED studies for offshore projects

illustrate the initial steps to converting

“Possible” projects into “Planned” project.

The number of planned projects that jump

in deliveries in 2012 and 2013 remains

sustainable, even if “Possible” demand

proves at risk.

The risk lies in companies underbidding

projects, without giving weight to the wave

of “Possible” project demand.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 14

0

100

200

300

400

500

600

700Petr

obra

s

Tota

l

BP

Shell

Chevro

n

Sta

toil

Exx

onM

obil

Eni

Gazp

rom

Anadark

o

Woodsi

de

Conoco

Phill

ips

Hess

Tullo

w

Pre

mie

r

Noble

BG

Gro

up

Maers

k

Apach

e

Murp

hy

Talis

man

ON

GC

Nexe

n

Inpex

EnQ

uest

Centr

ica

Husk

y

KN

OC

ATP

CN

OO

C

PEM

EX

BH

P B

illiton

GD

F S

uez

Fairfield

Queiroz

Galv

ao

Mara

thon

Relia

nce

PTT

DN

O

Lundin

Subse

a T

rees

Deliv

eries

Ordered / Undelivered Planned Project - Potential Orders Possible Project - Potential Orders

Demand from Key Operators Represents Wave of New Orders

Top Offshore Operator Subsea Tree Orders and Demand

Sources: Infield, Guggenheim Securities, LLC

The largest offshore operators have

ordered few trees in relation to their total

potential demand. In particular, the largest

operators still must order 989 trees in

order to meet planned project demand.

CVX and PBR are known for greater

engineering content and longer lead

times for orders.

BP and Shell are known for more subsea

standardization.

Wall of ordered trees and a constrained

supply chain may lead to greater subsea

tree order standardization.

Petr

obra

s

Tota

l

BP

Shell

Chevro

n

Sta

toil

Exx

onM

obil

Eni

Gazp

rom

Anadark

o

Woodsi

de

Conoco

Phillips

Hess

Tullow

Pre

mie

r

Noble

BG

Gro

up

Maers

k

Apach

e

Murp

hy

Talism

an

ON

GC

Nexe

n

Inpex

EnQ

uest

Centr

ica

Husk

y

KN

OC

ATP

CN

OO

C

PEM

EX

BH

P B

illito

n

GD

F S

uez

Fair

field

Queir

oz

Galv

ao

Mara

thon

Reliance

PTT

DN

O

Lundin

To

tal T

op

40

Oth

er

To

tal

Ordered / Undelivered 389 91 34 83 50 51 31 45 3 11 11 18 12 9 4 12 8 12 17 18 6 3 5 22 10 14 21 10 17 17 0 15 1 1 0 10 0 0 3 4 1,068 105 1,173

Planned Project - Potential Orders 62 111 120 82 125 39 72 37 48 16 10 11 14 25 8 15 25 29 12 2 10 12 14 0 9 1 5 4 2 10 8 2 13 9 1 3 3 11 6 3 989 101 1,090

Possible Project - Potential Orders 241 289 286 242 222 220 167 115 128 111 107 80 78 63 70 54 40 24 32 41 42 41 34 26 22 22 11 22 16 5 24 14 17 17 26 11 21 12 11 12 3,016 420 3,436

Total 692 491 440 407 397 310 270 197 179 138 128 109 104 97 82 81 73 65 61 61 58 56 53 48 41 37 37 36 35 32 32 31 31 27 27 24 24 23 20 19 5,073 626 5,699

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 15

Market Share by Top 40 Subsea Tree Customers 2000-2011

Operator

Total

Orders

'00-'11 Cameron

Aker

Solutions

GEOG

VetcoGray FMC Dril-Quip Other

Petrobras 832 27% 21% 19% 29% - 3%

Statoil 590 2% 29% 16% 53% - -

Total 295 23% 24% 2% 52% - -

Shell 275 15% 1% 37% 39% 7% -

BP 253 59% - 5% 36% - -

ExxonMobil 222 38% - 26% 36% - -

Chevron 206 28% - 41% 31% 1% -

Eni 98 42% 9% 18% 30% 1% -

Talisman 91 16% 9% 43% 32% - -

Anadarko 76 - - 9% 91% - -

Apache 67 72% 3% 10% 12% 3% -

Nexen 58 7% - 90% 2% 2% -

Canadian Natural Resources 57 35% - 9% 56% - -

ConocoPhillips 56 20% - 16% 36% 29% -

BHP Billiton 55 75% 2% 24% - - -

Woodside 55 - 16% - 84% - -

BG Group EGPC Petronas 43 100% - - - - -

Hess 41 71% 7% 10% 12% - -

Centrica 39 - - 59% 8% 33% -

Marathon 40 28% 53% 20% - - -

Maersk 34 32% - 68% - - -

Suncor Energy/Petro-Canada 33 - - - 100% - -

KNOC 33 27% - 70% - 3% -

Murphy 33 15% 48% - 30% 6% -

BG Group 31 71% - 6% 23% - -

Husky 30 100% - - - - -

ATP 29 45% - - 3% 52% -

Petronas 29 - 7% 31% 62% - -

Walter 26 - - 4% - 96% -

ADNEC 26 50% - 31% 19% - -

Tullow 26 4% - 15% 77% 4% -

CNOOC 26 - - - 100% - -

Premier 23 - - 74% 26% - -

Noble 20 75% - 10% 5% 10% -

GDF Suez 19 16% - 16% 68% - -

PetroSA 19 - - 21% 79% - -

EnQuest 18 - 33% 22% 44% - -

PEMEX 17 - - - 100% - -

Fairfield 16 94% - 6% - - -

Reliance 16 - 100% - - - -

Market Share 2000-2011

Total

Orders

'00-'11

% of

Market

Total Top 40 3,953 93%

Other 275 7%

Total Tree Demand 2000-2011 4,228

The largest 40 operators represent nearly

all of subsea tree demand.

Sources: Infield, Guggenheim Securities, LLC

Green indicates #1 provider status

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 16

Unordered Trees Demographics Point to Expansion of Subsea Tree Market

0

100

200

300

400

500

600

700

UK

Angola

USA

Aust

ralia

Nig

eria

Bra

zil

Norw

ay

Russ

ia (

FSU

)

Indonesi

a

Congo (

Bra

zzavill

e)

India

Ghana

Canada

Mala

ysi

a

Egypt (M

editerr

anean)

Equato

rial G

uin

ea

Moza

mbiq

ue

Falk

land I

slands

Isra

el

Italy

Aze

rbaijan (

FSU

)

Mexi

co

Republic

of

South

Afr

ica

Tanza

nia

Lib

ya

Maurita

nia

Sie

rra L

eone

Chin

a (

PRC)

Irela

nd

Russ

ia (

FSU

) (S

akhalin

)

Ivory

Coast

Phili

ppin

es

Trinid

ad

Tunis

ia

Lib

eria

Myanm

ar

Bru

nei

Guyane (

Fre

nch

Guia

na)

Vie

tnam

Oth

er

Unord

ere

d S

ubse

a T

rees

Possible Planned

0

500

1,000

1,500

2,000

2,500

3,000

SW MW DW UDW

Unord

ere

d S

ubse

a T

rees

Planned Possible

We expect Ultra/deepwater demand to

grow comparable to Midwater subsea

tree demand over time.

Unordered Midwater Demand Remains Significant

Traditional & Non-Traditional Sources of Demand

Source: Infield, Guggenheim Securities, LLC

Sources: Infield, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 17

Guggenheim “Watch List” for Subsea Tree Awards

Historical Historical

Operator Field Country Trees Preference #1 Preference #2 FTI CAM GE AKSO DRQ

Gazprom Shtokmanovskoye Russia (FSU) 72 - - - - -

Maersk Chissonga (Block 16) Angola 39 GEOG VetcoGray Cameron - - - - -

Total Egina (OML 130 Ex OPL 246) Nigeria 39 FMC Aker Solutions - - - - -

BP Green Canyon 826 Mad Dog South USA 38 Cameron FMC - - - - -

Shell Bonga North (OML 118 Ex OPL 212) Nigeria 29 FMC GEOG VetcoGray - - - - -

Chevron Lucapa (Block 14) Angola 28 GEOG VetcoGray FMC - - - - -

Chevron Rosebank UK 28 GEOG VetcoGray FMC - - - - -

BP Shah Deniz (Phase 2) Azerbaijan (FSU) 26 Cameron FMC - - - - -

Fairfield Darwin (North West Hutton Phase 2) UK 21 Cameron GEOG VetcoGray - - - - -

ExxonMobil Scarborough (WA-1-R) Australia 16 Cameron FMC - - - - -

GDF Suez Petrel (NT/RL1 & WA-6-R) (Bonaparte LNG) Australia 16 FMC Cameron - - - - -

Woodside Calliance (Ex Brecknock Sth) (WA-31-R Browse) Australia 16 FMC Aker Solutions - - - - -

Petrobras Franco (Phase 2) (2-ANP-1-RJS) Brazil 16 FMC Cameron - - - - -

Gazprom Kamennomysskoye More (Obskaya Bay) Russia (FSU) 16 - - - - -

Shell Mississippi Canyon 391-392 & 348 Appomattox USA 16 FMC GEOG VetcoGray - - - - -

Tullow Tweneboa (TEN) (Deepwater Tano) Ghana 14 FMC GEOG VetcoGray - - - - -

Chevron Nsiko (OML 140 Ex OPL 249) Nigeria 14 GEOG VetcoGray FMC - - - - -

Chevron Negage (Block 14) Angola 13 GEOG VetcoGray FMC - - - - -

Total Gindungo (Kaombo 1) (Block 32) Angola 12 FMC Aker Solutions - - - - -

Total Canela (Kaombo 2) (Block 32) Angola 12 FMC Aker Solutions - - - - -

Total Louro (Kaombo 2) (Block 32) Angola 12 FMC Aker Solutions - - - - -

PTT Cash/Maple (AC/RL7) Australia 12 - - - - -

Petrobras Carioca (Phase 1) (BM-S-9) (Sugarloaf) Brazil 12 FMC Cameron - 2 - - -

Tullow Enyenra (TEN) (Ex Owo) (Deepwater Tano) Ghana 12 FMC GEOG VetcoGray - - - - -

Noble Leviathan (Med) Israel 12 Cameron GEOG VetcoGray - - - - -

Chevron Aparo (OML 132 & OPL 249) Nigeria 12 GEOG VetcoGray FMC - - - - -

ONGC Krishna-Godavari UD-1 (KG-DWN-98/2) (D5) India 11 - - - - -

ConocoPhillips South Belut Indonesia 11 FMC - - - - -

ExxonMobil Erha North Extension (OML 133) Nigeria 11 Cameron FMC - - - - -

BP Plutao (PSVM) (Block 31 North East) Angola 10 Cameron FMC - 11 - - -

ExxonMobil Mbulumbumba (Kizomba Block 15) Angola 10 Cameron FMC - - - - -

ExxonMobil Vicango (Kizomba Block 15) Angola 10 Cameron FMC - - - - -

BP Urano (Block 31 South East) Angola 10 Cameron FMC - - - - -

Petrobras Lula North (BM-S-11) Brazil 10 FMC Cameron - - - - -

Tullow Ntomme (TEN) (Deepwater Tano) Ghana 10 FMC GEOG VetcoGray - - - - -

PEMEX Kosni Mexico 10 FMC Cameron - - - - -

Hess Green Canyon 468 Pony (Knotty Head North) USA 10 Cameron FMC - - - - -

Total Gengibre (Kaombo 1) (Block 32) Angola 9 FMC Aker Solutions - - - - -

Total Mostarda (Kaombo 2) (Block 32) Angola 9 FMC Aker Solutions - - - - -

Shell Brunei Government Geronggong Brunei 9 - - - - -

E.ON Ruhrgas Huntington UK 9 GEOG VetcoGray Cameron 4 - - - -

BP Saturno (PSVM) (Block 31 North East) Angola 8 Cameron FMC - 13 - - -

BP Cesio (PCC) (Block 18) Angola 8 Cameron FMC - - - - -

BP Chumbo (PCC) (Block 18) Angola 8 Cameron FMC - - - - -

Noble Aphrodite (Cyprus Block 12) Cyprus 8 Cameron GEOG VetcoGray - - - - -

Kosmos Odum (West Cape Three Points) Ghana 8 - - - - -

Chevron Gendalo Indonesia 8 GEOG VetcoGray FMC - - - - -

PEMEX Lakach Mexico 8 FMC Cameron - - - - -

Anadarko Windjammer/Barquentine (Prosperidade) Mozambique 8 FMC GEOG VetcoGray - - - - -

Shell DeSoto Canyon 353 & 397 & MC 393 Vicksburg USA 8 FMC GEOG VetcoGray - - - - -

Current Field Installations

Methodology: Our

“Watch List” is

comprised of the

largest potential

orders for planned

projects that

currently remain

unordered. We

have determined

the preferred

subsea tree

providers for each

operator through

an assessment of

market shares for

orders since 2000.

Sources: Infield,

Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 18

Manufacturing Capacity

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 19

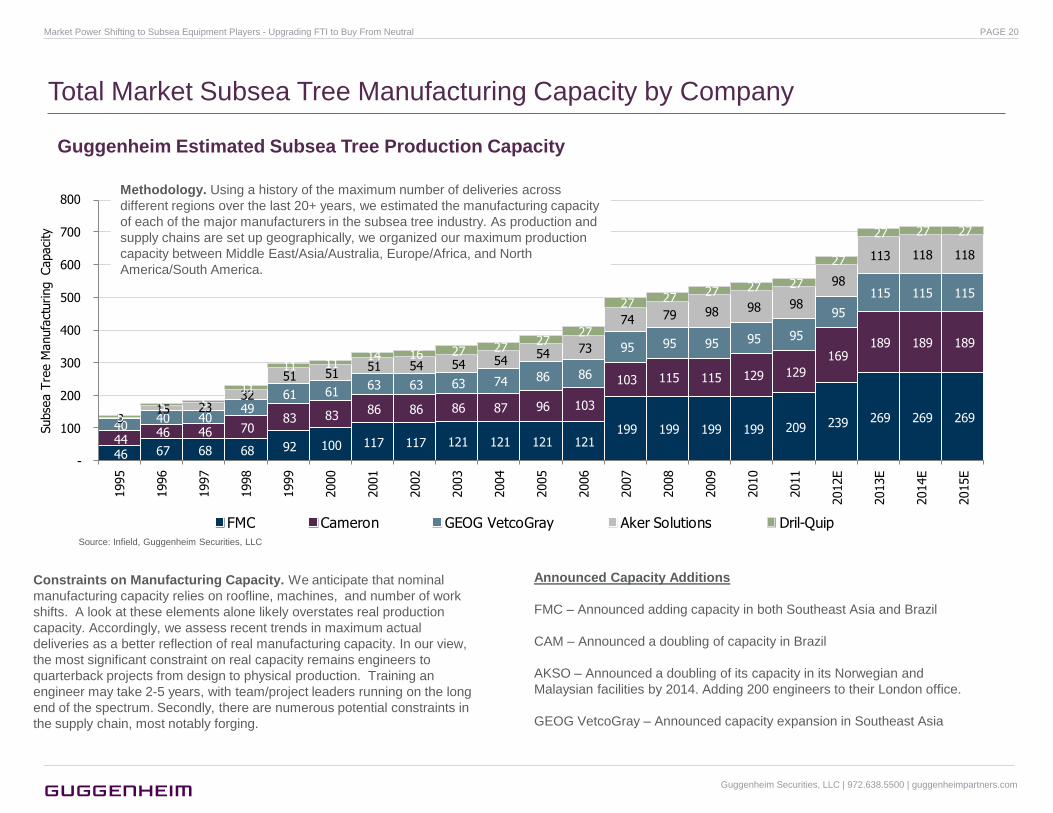

Total Market Subsea Tree Manufacturing Capacity by Company

Guggenheim Estimated Subsea Tree Production Capacity

46 67 68 68 92 100 117 117 121 121 121 121 199 199 199 199 209 239 269 269 269

44 46 46 70

83 83 86 86 86 87 96 103

103 115 115 129 129

169 189 189 189

40 40 40

49 61 61

63 63 63 74 86 86

95 95 95 95 95

95

115 115 115

3 15 23

32

51 51 51 54 54 54

54 73

74 79 98 98 98

98

113 118 118

5 5 5

11

11 11 14 16 27 27

27 27

27 27 27 27 27

27

27 27 27

-

100

200

300

400

500

600

700

800

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

Subse

a T

ree M

anufa

cturing Capaci

ty

FMC Cameron GEOG VetcoGray Aker Solutions Dril-Quip

Methodology. Using a history of the maximum number of deliveries across

different regions over the last 20+ years, we estimated the manufacturing capacity

of each of the major manufacturers in the subsea tree industry. As production and

supply chains are set up geographically, we organized our maximum production

capacity between Middle East/Asia/Australia, Europe/Africa, and North

America/South America.

Constraints on Manufacturing Capacity. We anticipate that nominal

manufacturing capacity relies on roofline, machines, and number of work

shifts. A look at these elements alone likely overstates real production

capacity. Accordingly, we assess recent trends in maximum actual

deliveries as a better reflection of real manufacturing capacity. In our view,

the most significant constraint on real capacity remains engineers to

quarterback projects from design to physical production. Training an

engineer may take 2-5 years, with team/project leaders running on the long

end of the spectrum. Secondly, there are numerous potential constraints in

the supply chain, most notably forging.

Announced Capacity Additions

FMC – Announced adding capacity in both Southeast Asia and Brazil

CAM – Announced a doubling of capacity in Brazil

AKSO – Announced a doubling of its capacity in its Norwegian and

Malaysian facilities by 2014. Adding 200 engineers to their London office.

GEOG VetcoGray – Announced capacity expansion in Southeast Asia

Source: Infield, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 20

Manufacturing Capacity Utilization Suggests Market Power for Equipment Names

138

173

182

230

298

306

331

336

351

363

384

410

498

515

534

548

558

628

713

718

718

64%

74%

67%

75%

82%

54%

70%

66%58%

44%

70%

63%

77%

66%

55%

43%

47%

74%

70%

75%

85%

-

100

200

300

400

500

600

700

800

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

Subse

a T

ree M

anufa

cturin

g C

apacity

Capaci

ty U

tiliz

ation

Subsea Tree Manufacturing Capacity Capacity Utilization

Guggenheim Estimated Subsea Tree Production Capacity

Source: Infield, Guggenheim Securities, LLC

The ramp in estimated

deliveries in 2012 and

beyond looks set to rapidly

increase utilization of

subsea tree manufacturing

capacity across the

industry, despite capacity

expansions for all of the

major equipment providers.

The subsea tree market is

headed back to utilization

levels that heralded high

margins, high assets turns,

and favorable return

structures during that last

cycle.

We see potential for rising utilization to push

toward more standardized tree designs in order to

minimize engineering bottlenecks seen with

specially designed trees.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 21

9 27

4

5

12

2

14

11

3

16

15

16

32

42

24

28

14 6

0 57

86

113 175

115

144

134

131

77 1

58

177 229

184

140

128

112

19 45

33 5

5

57

47

73

77

71

66

96

65

125

112

132

81

136

-

50

100

150

200

250

300

350

400

450

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Subse

a T

ree D

eliv

eries

ME/Asia/Australia Europe/Africa NA/LA

5 8 12 5 4 21 2 9 23 1847 53 59

22 38 3388

5858

176

92134135 93

211170119

236231

189167230

110137

139

9831

26

57

8246 81

99

98

67

102

122172171

167

167

205 93

128

0

50

100

150

200

250

300

350

400

450

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

New

Subse

a T

ree O

rders

ME/Asia/Australia Europe/Africa NA/LA

Deliveries & Manufacturing Capacity by Region

Subsea Tree Production Capacity by Region Subsea Tree Deliveries

Subsea Tree New Orders

More orders from Australia and Asia, as well as more visibility for

drilling activity in the region, has spurred an expansion of

capacity.

Recession and Macondo limited

the growth in activity.

Recession and

Macondo

reduced order

growth.

The visible expansion in activity in the Gulf of Mexico and Brazil

looks set to grow new tree orders from current depressed levels.

A fast ramp in activity in traditional markets, like the North Sea

and West Africa, looks set to increase orders from these basins.

Meanwhile, growth in activity from non-traditional African markets

will lead to growth in the overall market.

Sources: Infield, Guggenheim Securities, LLC

9

27

30

30

38

38

43

43

43

48

49

49

50

59

63

77

77

87

132

137

137

94

94

100

138

187

187

191

191

195

195

195

221

285

285

285

285

285

285

285

285

285

35

52

52 62 7

3

81

97

102

113

120

140

140 163

171

186

186

196

256 296

296

296

-

100

200

300

400

500

600

700

800

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012E

2013E

2014E

2015E

Subse

a T

ree M

anufa

cturing Capaci

ty

ME/Asia/Australia Europe/Africa NA/LA

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 22

“Calorie Count” Subsea Backlog Indicates Uptick in Industry Economics

6.46.4

7.2

7.3 7.3

7.9

8.1 8.1

8.2

8.1

6.0

6.5

7.0

7.5

8.0

8.5

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

$/S

ubse

a T

ree

Backlog - $/Subsea Tree

We expect a backlog conversion at not much longer than two

years. Accordingly, we expect the burn off of low Rev/Tree

backlog will yield to higher Rev/Tree backlog, likely leading to

improved Asset Turns and Margins across equipment players.

Note: Average of FTI, CAM, & ASKO backlog figures.

Source: Infield, Guggenheim Securities, LLC

Revenue/Subsea Tree Improving in Industry Backlog ($M)

More revenue per tree in backlog, either

translates to an improvement in mix (more

manifolds or control systems) or better

average pricing since the bottom of the

cycle.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 23

Marking Capacity Constraint and Pricing Power Through New Order Lead Time

300

500

700

900

1,100

1,300

1,500 1

Q0

1

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

Day

s fr

om

Ne

w O

rde

r to

De

live

ry

Trailing Twelve Month Average New Order Lead Time

Longer lead times from new orders to

delivery marked the tightening of

production capacity and foundation of

pricing power during the last cycle.

New order lead times appear to show

signs of finding a base and moving higher.

We continue to see the expansion of order

lead times as a positive indicator for the

direction of equipment player economics.

As lead times expand, operators

concerned about near-term delivery dates

will either move toward more standardized

tree designs or pay more for specialized

product that requires more engineering.

Industry Lead Times May Show Signs of Lengthening Again

Source: Infield, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 24

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1Q

1999

4Q

1999

3Q

2000

2Q

2001

1Q

2002

4Q

2002

3Q

2003

2Q

2004

1Q

2005

4Q

2005

3Q

2006

2Q

2007

1Q

2008

4Q

2008

3Q

2009

2Q

2010

1Q

2011

4Q

2011

LTM

Rolli

ng A

vera

ge

Days

to D

eliv

er

Cameron Aker Solutions

GEOG VetcoGray FMC

Dril-Quip

Positive Lead Times Trend: Field Complexity & Shift in the Company Pack

0

500

1,000

1,500

2,000

2,500

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

LTM

Rolli

ng A

vera

ge

Days

to D

eliv

er

SW MW DW

Move to greater field complexity within ultradeepwater, greater

drilling depths, or pre-salt structures will likely lead to greater

need for engineering content.

DRQ is an outlier that will only look to win

small, high margin tree awards.

Lead times across companies appear to

be in the same channel, possibly showing

signs of inflection.

Source: Infield, Guggenheim Securities, LLC

Source: Infield, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 25

0.8

0.9

1.0

1.1

1.2

1.3

1.4

100

150

200

250

300

350

1Q

06

2Q

06

3Q

06

4Q

06

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

Ass

et

Turn

s

Rolli

ng N

TM

Subse

a T

ree D

eliv

eries

Rolling NTM Subsea Tree Deliveries Asset Turns

Asset Turns and Deliveries in Aggregate

Note: Average of FTI and CAM

Source: Infield, Guggenheim Securities, LLC

Since companies book revenues on

percentage of completion, a wave of

scheduled deliveries over the next four

quarters implies higher revenues and

asset turns in the coming quarters.

Accordingly, we see potential for asset

turns to recover to heights seen during the

last cycle.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 26

Company Breakdown

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 27

Rising Backlog Coverage Has Bullish Implications

0.0

0.5

1.0

1.5

2.0

2.5

3.0

-

100

200

300

400

500

600

FMC Cameron GEOG VetcoGray Aker Solutions

Years o

f Back

log (B

ack

log/A

nnual C

apacity

)

Num

ber

of

Subse

a T

rees

in B

ack

log

-

100

200

300

400

500

600

1Q

05

2Q

05

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

4Q

06

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

Num

ber

of

Subse

a T

rees

in B

ack

log

Cameron Aker Solutions GEOG VetcoGray

FMC Dril-Quip

Total Subsea Trees in Backlog Subsea Trees in Backlog Over Time

CAM’s flat backlog likely

illustrates less aggressive

bidding.

FTI and GE appear to have

gained share amid more

competitive pricing.

Source: Infield, Guggenheim Securities, LLC Source: Infield, Guggenheim Securities, LLC

Except for Aker Solutions, each

company has over two years of

backlog relative to current annual

production capacity.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 28

Comparative New Orders

-

50

100

150

200

250

300

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

Subse

a T

ree N

ew

Ord

ers

Cameron Aker Solutions GEOG VetcoGray FMC Dril-Quip

-

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009 2010 2011

Subse

a T

ree N

ew

Ord

ers

Cameron Aker Solutions GEOG VetcoGray FMC Dril-Quip

FTI and GE appear to have

gained share amid more

competitive pricing.

Bigger mix for CAM in 2008,

likely helped CAM from 2009-

2011.

Both 4Q and 1Q continue to demonstrate seasonally strong

patterns, as operators set budgets and place orders ahead of

newly scheduled projects.

Source: Infield, Guggenheim Securities, LLC Source: Infield, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 29

Date Operator Value ($m) Field Region Country

Subsea

Trees Delivery Comments Scope of Supply

05-Jul-12 Statoil $200 Gullfaks South Field Europe Norway 7 To commence in 2Q13 7 subsea production trees, 7 wellhead systems, 2

integrated protection structures with manifolds, and

additional controls and equipment

29-Mar-12 Petrobras $1,500 Brazil Pre-Salt L Amer Brazil 130 To commence in 2014 4 year Pre-Salt agreement ~ 130 subsea trees, subsea

multiplex controls and related tools and equipment

29-Mar-12 "initial call-off" (from contract above)

$900 Brazil Pre-Salt L Amer Brazil 78

20-Mar-12 Statoil $70 H-Nord Europe Norway 1 Throughout 2013 1 subsea production tree, 1 manifold, 1 multiphase

meter, an integrated template structure, one umbilical,

two wellheads and additional controls and equipment

10-Jan-12 Anadarko Lucius N Amer GOM 5 To commence in 4Q12 5 subsea production trees and 2 manifolds

09-Jan-12 Woodside $150 Greater Western Flank Phase 1 APAC Australia 6 To commence in 2H12

and continue through

2013

6 subsea production trees, 6 wellheads, 2 manifolds,

subsea and topside controls and flow line connection

systems

12-Dec-11 BP Block 18 Africa Angola 4 To be delivered in 2013 4 subsea trees, control systems, wellheads, tubing

hangers, well jumpers and subsea distribution systems

07-Dec-11 LLOG $40 Who Dat N Amer GOM 7 To commence in 2012 7 subsea production trees and control systems

30-Nov-11 Chevron $325 Wheatstone APAC Australia 11 To commence in 2013 11 subsea production trees, 11 wellheads, 3 manifolds,

subsea and topside controls and well access systems

20-Sep-11 BG Norge $135 Knarr Europe Norway 3 To commence in 2Q13 3 subsea production trees, 3 water injection trees, 6

subsea control modules, 5 wellheads, 2 manifolds and

other related equipment and controls.

27-Jun-11 Shell Prelude APAC Australia 7 7 large bore subsea production trees, production

manifolds, riser bases, subsea control systems and other

related equipment

06-Jun-11 Statoil $50 Visund Europe Norway 2 Commenced in 2Q12

and to continue through

1Q13

2 subsea production trees, 1 manifold and associated

subsea and topside control systems

02-Mar-11 Petrobras $125 L Amer Brazil 32 To commence in 2013 Represents the remaining equipment under a 107-tree

frame agreement that was announced in 2/2010

15-Feb-11 COP $96 3-fields APAC Indonesia 12 Commenced in 2011 3-year frame agreement COP Indonesia to manufacture

and supply of subsea production equipment (immediate

$57m call-off revenue). 12 subsea production trees,

wellheads, control systems and associated offshore

tooling and services.

24-Jan-11 CNOOC $85 Liuhua 4-1 APAC China 8 Commenced in 4Q11 8 subsea trees and tie-back to the existing Liuhua 11-1

field

FTI Recently Announced Subsea Tree Awards (2011-2012)

Source: Company Reports, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 30

CAM Recently Announced Subsea Tree Awards (2011-2012)

Source: Company Reports, Guggenheim Securities, LLC

Date Operator Value ($m) Field Region Country

Subsea

Trees Delivery Comments Scope of Supply

04-Jun-12 CNOOC $100 PANYU 35-1/2 APAC China 6 To commence in 2013 6 subsea production trees, production controls, 1

manifold, associated subsea equipment, rental tooling

and service support

10-Oct-11 DET NORSKE $56 JETTE Europe Norway N/A Commenced in early

2012

Wellheads, trees, flow bases, electro-hydraulic

multiplexed controls, connections, pipeline end manifolds

and other associated subsea equipment

13-Jan-11 Petrobras $72 N/A L Amer Brazil 27 Commenced in 2011,

deliveries over following

4 years

27 subsea trees & related equipment remaining from

9/2009 138-tree frame agreement

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 31

AKSO Recently Announced Subsea Tree Awards (2011-2012)

Date Operator Value ($m) Field Region Country

Subsea

Trees Delivery Comments Scope of Supply

04-May-12 Total NOK 470 Dalia Africa Angola 7 2013-2014 7 production subsea trees, 7 wellhead systems and 7

well jumper systems, and may include some contract

options

02-May-12 Murphy Undisclosed Siakap North APAC Malaysia 13 1Q13 13 subsea trees, eight manifolds, well jumpers,

engineering for topside controls and lifecycle support

services

05-Jan-12 Marathon NOK 210 Boyla Europe Norway 4 1Q13 Engineering, procurement, construction and delivery of

4r subsea trees, 4r over-trawlable subsea structures

and control systems

29-Dec-11 Statoil NOK 400 Svalin Europe Norway 2 Final Deliveries in 3Q13 2 subsea trees, 1 four-slot integrated template structure

with process distribution manifold, subsea and topside

production control systems, wellhead systems and

remote connection systems

24-Nov-11 Statoil NOK 225 Vilje Europe Norway 1 Final Deliveries in 2Q13 1 subsea tree, satellite production flowbase and

protection structure, subsea production control system,

wellhead system, remote connection system and a 150

metre static umbilical. This contract is an extension to

the subsea production system Aker Solutions' delivered

to the Vilje field in 2006.

11-Nov-11 Lundin NOK 700 Brynhild Europe Norway 3 Final Deliveries in 2Q13 1 template-manifold structure, 1 riser base, 3 subsea

trees, 3 wellhead systems, control system, a tie-in

system, 38 kilometres of umbilicals, HP riser and rental

tooling. The contract contains several options for

additional equipment, including other field developments.

11-Aug-11 Murphy Undisclosed Kikeh APAC Malaysia Undisclosed 2013 Iincludes the delivery of deepwater oil production

equipment such as subsea trees, control modules

distribution system and manifolds that will be installed at

a water depth of 1350 meters. Aker Solutions was

responsible for the delivery of the original Kikeh scope

back in 2005. It was the first deepwater development in

Malaysia and the Asia Pacific region.

30-Mar-11 Statoil NOK 1000 Fossekall-Dompap Europe Norway 11 Final Deliveries in 2Q13 3 template-manifold structures, 11 subsea trees, a

control system and a tie-in system. The contract also

contains several options for other field developments on

the Norwegian continental shelf which Statoil may

exercise.

Source: Company Reports, Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 32

Announced Alliances and Frame Agreements (2011-2012)

Source: Company Reports, Guggenheim Securities, LLC

Date Operator Type Region Country Scope of Agreement

FMC Technologies29-Mar-12 Petrobras Contract L Amer Brazil 4-year agreement with Petrobras for the supply of pre-salt subsea equipment. The total award would result in approximately $1.5Bn in

revenue to FTI if all of the subsea equipment included in the agreement is ordered. The initial call-off has an approximate value of $900m

in revenue to FTI and includes 78 subsea trees. FTI's total scope of supply could include the delivery of up to 130 subsea trees, subsea

multiplex controls and related tools and equipment. The tree systems are for use offshore Brazil in water depths up to 8,200 feet. The

equipment will be engineered at FTI's South American Technology Center and manufactured at FTI's subsea facility, both of which are

located in Rio de Janeiro, Brazil. The subsea trees will achieve 70% Brazilian local content and deliveries are scheduled to commence in

2014.

01-Dec-11 Anadarko Global Alliance

Agreement

World-wide To provide subsea systems and life-of-field services for their worldwide subsea development projects. An alliance has been in place with

Anadarko and its legacy companies since 1992 to support their Gulf of Mexico exploration and production projects. The agreement will

allow FTI to broaden its support of Anadarko's expanding E&P activities worldwide, including recent discoveries offshore the East and

West coasts of Africa.

01-Mar-11 British

Petroleum

Global Frame

Agreement

World-wide 5-year global frame agreement with BP to provide subsea production systems and life-of-field services for their worldwide subsea

development projects.

15-Feb-11 ConocoPhillips

Indonesia

Country Frame

Agreement

APAC Indonesia 3-year frame agreement with ConocoPhillips Indonesia Inc. Ltd for the manufacture and supply of subsea production equipment. The

contract includes an immediate $57 million call-off and is expected to result in approximately $96 million in total revenue to FTI if all of the

subsea equipment included in the agreement is ordered. The equipment will support 3 of ConocoPhillips Indonesia's offshore fields, which

are located in approximately 300 feet (90 meters) of water offshore Indonesia in the Natuna Sea. FTI's scope of supply includes the

manufacture of up to 12 subsea production trees, wellheads, control systems and associated offshore tooling and services. The

equipment will be engineered and manufactured at FMC's facilities in Indonesia, Singapore and Malaysia, with deliveries scheduled to

commence in 2011.

21-Dec-10 Shell Enterprise

Framework

Agreement

N Amer &

L Amer

5-year Enterprise Framework Agreement (EFA) with Shell with an option to extend the agreement for an additional 5 years. This

agreement facilitates to international projects the same mutual benefits that Shell and FTI have enjoyed through a strategic GOM

relationship that has existed over the past 17 years. Under the agreement, Shell's business units in the Americas intend to utilize FTI for

all deepwater subsea equipment projects within the scope of the agreement, unless tendering is otherwise required. Specific scope of

supply includes subsea trees, mounted controls, processing equipment, manifolds, sled components, jumpers and various other hydraulic,

chemical, electrical and control systems. This agreement for deepwater subsea equipment is also available for use by other Shell global

business units as may be allowed by local commercial and legal requirements.

Broader FTI Alliance Agreement Partners Include: Shell, BP (split w/CAM), Woodside - 5/2008, BG - 4/2010, Anadarko, Noble (for GOM) - 12/2008, Cobalt - 2/2010, LLOG (for GOM) - 4/2008 and Statoil (split w/AKSO for Norway) - 9/2007

Cameron15-Mar-11 Petrobras MOU L Amer Brazil Future technology cooperation with Petrobras & includes a $30m investment in R&D facilities at two Brazilian locations

01-Mar-11 British

Petroleum

Non-Exclusive

Global Agreement

Worldwide Engineering, Procurement, Construction and Operational Support for Subsea Production Systems. The Global Agreement recognizes that

the alignment of standards, specifications and processes and the introduction of product standardization, will optimize the use of

resources, shorten execution cycles, optimize life cycle cost and deliver superior long term value. The Agreement is aimed at developing a

long-term, collaborative, performance-based relationship between BP and Cameron, maximizing the benefits to be gained of

standardization; recognizing that this is the route to enhance quality, reliability and production availability of subsea systems.

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 33

FTI – Upgrading to Buy – Seeking Leverage to Improving Subsea Economics

We are upgrading FTI to Buy from Neutral. We see improving subsea economics

overshadowing North American-related risks to the Surface business. Although risks for

near-term quarters from lower margin subsea backlog remains, we believe the upside from

asset turns from completion of near-term deliveries and incrementally better economics

baked into backlog should outweigh near-term risks that Subsea margins may fall below

2H12 guidance of 12.5-13.5% (pg. 35). Forecasted to expand from ~55% of operating

income, we think the outlook for the continued improvement in the trajectory of Subsea

margins since 4Q11 will remain the key driver for FTI shares. Given operating leverage in

FTI’s business model from outsourcing, we see potential upward revisions to consensus

earnings estimates with growth in the Subsea business. Additionally, we see valuation

multiple expansion for the shares as the combination of growth and a favorable return

structure hits stride. We would take advantage of the current consolidation within FTI shares

as an entry point.

Raising Our Price Target & 2013 Estimate. We are raising our price target to $64 from

$46. Given our more positive outlook, we are raising our 2013E EPS to $2.70 from $2.65.

Subsea Technologies Growth to Take Lead. After gaining 600bps of market share from

2009-2011, a competitive bidding environment and lower margin backlog has forced 2012

Subsea margin guidance down to 11-12%. Improved revenue/tree in backlog and visibility

into accelerating deliveries into 2013 (pg. 35), likely improves revenue, asset turns, and

margins through 2H12. As a result, we are more confident in 2H12 Subsea margin guidance

for an uptick to 12.5-13.5%. As industry manufacturing capacity tightens and lead times

expand, we see room for improved pricing and greater standardization of tree orders, which

may propel subsea economics ahead of our current estimates.

Surface Technologies Remains a Risk, but Reflected in Estimates. Our forecast for a

2H12 decline in North American activity risks 18-20% 2012 margin guidance for the Surface

business and leads our margin numbers lower for 2013, as backlog protection fades.

Exposure to North American surface wellheads, as well as pressure pumping equipment,

rentals, and consumables, lead us to revise our estimates below current guidance (pg. 36).

Although strength in international businesses may offset downside, negative revision risk

likely remains. In our view, upside in the Subsea business will offset this drag.

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12E

4Q

12E

1Q

13E

2Q

13E

3Q

13E

Segm

ent

Revenue (

$m

)

Subsea Technologies Surface Technologies Energy Infrastructure

15%

25%

35%

45%

55%

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12E

1Q

13E

3Q

13E

1Q

14E

3Q

14E

1Q

15E

3Q

15E

Retu

rn o

n E

quity(A

nnualz

ed Q

uart

ers

)

Source: Company Reports, Guggenheim Securities, LLC

Source: Company Reports, Guggenheim Securities, LLC

FTI Annualized Return on Equity

FTI Segment Revenue Breakdown

Source: FactSet, Guggenheim Securities, LLC

Company Category 2008 2009 2010 2011 2012E 2013E 1Q12 2Q12 3Q12E 4Q12E 1Q13E 2Q13E 3Q13E 4Q13E

FMC Technologies EPS 2.94 2.93 3.06 1.64 2.00 2.70 0.41 0.43 0.56 0.60 0.63 0.65 0.67 0.74

Previous EPS 2.00 2.65 0.56 0.60 0.63 0.64 0.66 0.72

Consensus EPS 2.09 2.61 0.57 0.64 0.56 0.61 0.67 0.73

Consensus EPS-High 2.16 2.90 0.60 0.71 0.63 0.66 0.73 0.87

Consensus EPS-Low 2.00 2.00 0.54 0.57 0.52 0.50 0.49 0.49

Guggenheim Securities, LLC | 972.638.5500 | guggenheimpartners.com

Market Power Shifting to Subsea Equipment Players - Upgrading FTI to Buy From Neutral PAGE 34

5.1

5.2

6.8

7.8

7.7

8.3

8.1

8.6

8.8

8.1

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12E

4Q

12E

1Q

13E

2Q

13E

3Q

13E

4Q

13E

4

5

6

7

8

9

10

Revenue (

$m

)

Backlo

g $

/Subse

a T

ree

Subsea Backlog Subsea Backlog ($/tree)

Key Drivers of FMC Technologies Economics Paint Bullish Picture

18.4

%

16.6

%

14.2

%

12.3

%

10.2

%

10.5

%

11.5

%

7.2

%

8.4

%

10.2

%

12.8

%

13.3

%

13.5

%

13.7

%

13.9

%

14.1

%

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1Q

10

2Q

10

3Q

10

4Q

10

1Q