2012 06 22 Presentationformacau Volatility-As-An-Asset-class

20

VOLATILITY AS AN ASSET CLASS JUNE 2012 Societe Generale Corporate & Investment Banking Global Markets Division | CROSS-ASSET SOLUTIONS GROUP Julien Lascar – Cross Asset Solutions

-

Upload

jaime-maihuire -

Category

Documents

-

view

19 -

download

0

Transcript of 2012 06 22 Presentationformacau Volatility-As-An-Asset-class

VOLATILITY AS AN ASSET CLASS

JUNE 2012

Societe Generale Corporate & Investment Banking

Global Markets Division | CROSS-ASSET SOLUTIONS GROUP

Julien Lascar – Cross Asset Solutions

2

CONTENTS

VOLATILITY:

● WHAT IS IT?

● WHICH VOLATILITY?

● WHAT TO DO WITH IT?

TAIL HEDGING

● HOW TO TRADE VOLATILITY

● VIX IS THE BEST EQUITY VOLATILITY INDEX

● ACCESS TO VIX

● CASE STUDY

ALTERNATIVE INVESTMENT

● VOLATILITY PREMIUM

● ACCESS TO VOLATILITY PREMIUM

● CASE STUDY

2

3

VOLATILITY

WHAT IS IT? WHICH ONE?

WHAT TO DO WITH IT?

VOLATILITY

WHAT IS IT?

● A MEASURE OF RISK

● Volatility most frequently refers to the standard

deviation of the continuously compounded returns of

a financial instrument with a specific time horizon. It

is often used to quantify the risk of the instrument

over the time period.

WHICH VOLATILITY?

● IMPLIED vs. REALIZED

● VOLATILITY IMPACTED BY TIME PERSPECTIVES

(MATURITY), LEVEL OF RISK (STRIKE/SMILE)

● EACH UNDERLYING HAS ITS OWN VOLATILITY

● MODELISED DIFFERENTLY

Bp/day for HJM model (Interest rate)

%/year for Black model (FX, Equity, Commo…)

WHAT TO DO WITH IT?

● CAPTURE OPPORTUNITIES

4

5

VOLATILITY

HEDGING: OPPORTUNITIES INVESTMENT: OPPORTUNITIES

5

WHAT TO DO WITH IT?

TAIL HEDGING ALTERNATIVE INVESTMENT

6

TAIL HEDGING

HOW TO TRADE VOLATILITY? VIX IS THE BEST EQUITY VOLATILITY INDEX

ACCESS TO VIX CASE STUDY

LISTED/OTC OPTIONS ON AN EQUITY INDEX

VARIANCE/VOLATILITY SWAPS

● Exchange of realized volatility at maturity with

a pre-determined fixed amount, The “Variance

Strike”.

● Spot Start, Forward Start.

VIX FUTURES

● The benchmark for stock market volatility,

measuring implied short-term volatility of S&P

500 Index options.

ETNs & ETFs

SYSTEMATIC FUNDS

TAIL HEDGING HOW TO TRADE VOLATILITY?

Liquidity

Roll Mgt

Bid-Offer Spd

Flexibility

Cost of Carry

Transparency

7

WHAT IS VIX ?

● The benchmark for stock market volatility,

measuring implied short-term volatility of S&P

500 Index options.

● Highly Transparent & Liquid – VIX futures

are exchanged traded on the CBOE.

● Tight Bid/Offer Spread – especially in

comparison to Vol and Variance swaps.

WHY VIX ?

● Negative Correlation with Equity Market

● When equity market are dropping, they all

move down

TAIL HEDGING VIX IS THE BEST PROXY

0%

50%

100%

150%

200%

250%

300%

350%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

SPX Index HSI Index VIX Index

8

ROLL VIX FUTURE CONTRACTS

● But, the market is in contango most of the time

TAIL HEDGING ACCESS TO VIX – BASIC WAY

Time

Future

Price

! COST

OF

CARRY

9

SGI VI BETA INDEX – Calculated by S&P

The SGI VI Beta Index provides long implied volatility exposure through VIX futures.

The Index invests in the VIX futures contracts through a utility function, which aims to provide the best roll in

order to benefit from:

● The smallest carry cost1 of the contango term structure (low volatility regime).

● The highest positive carry earning of the backwardation term structure (high volatile regime).

The Index contains a dynamic exposure that leverages expo to VIX Futures when VIX is going in backwardation

The higher the volatility, the higher the exposure to the short-term futures contract.

High Transparency & Liquidity

10

Negative carry in

contango

markets

1Primarily invests from 1st to 6th contract

1/5th of positions are daily rolled.

Positive carry in

backwardation

markets

TAIL HEDGING ACCESS TO VIX – SMART WAY

CASE STUDY 1 - DIVERSIFIED PORTFOLIO (KOREA)

The increased allocation of the SGI VI Beta Index to the diversified portfolio shows enhanced

performance.

11

THE FIGURES RELATING TO PAST PERFORMANCES AND SIMULATED PERFORMANCES REFER TO PAST

PERIODS AND ARE NOT A RELIABLE INDICATOR OF FUTURE RESULTS. THIS ALSO APPLIES TO

HISTORICAL MARKET DATA

Diversified Portfolio

KIS Govt Bonds 5Y+ (KISKGV5Y Index): 75%

Korean Equities (KOSPI2 Index): 20%

Commodities (DJUBS Index): 5%

Diversified Portfolio 95% x Diversified Portfolio

+ 5% SGI VI Beta

90% x Diversified Portfolio

+ 10% SGI VI Beta

Since 18 Jun 2007 (5 Year) 6.90% 8.80% 10.68%

Since 1 Sep 2008 (Financial Crisis) 9.23% 11.49% 13.72%

Since 14 Mar 2011 (Launch Date) 5.54% 7.39% 9.22%

Source: Bloomberg as of June 18th 2012

Annualised Return Comparison

0

100

200

300

400

500

600

700

90

100

110

120

130

140

150

160

170

180

Jun-2007 Jun-2008 Jun-2009 Jun-2010 Jun-2011 Jun-2012

Diversified Portfolio

90% Diversified Portfolio + 10% SGI VI Beta Index

95% Diversified Portfolio + 5% SGI VI Beta Index

SGI VI Beta Index

TAIL HEDGING

CASE STUDY 1 - DIVERSIFIED PORTFOLIO (HONG KONG)

The increased allocation of the SGI VI Beta Index to the diversified portfolio shows enhanced

performance.

12

THE FIGURES RELATING TO PAST PERFORMANCES AND SIMULATED PERFORMANCES REFER TO PAST

PERIODS AND ARE NOT A RELIABLE INDICATOR OF FUTURE RESULTS. THIS ALSO APPLIES TO

HISTORICAL MARKET DATA

Diversified Portfolio

iBoxx ABF Hong Kong TR Index (ABTRHK Index): 75%

Hong Kong Equities (HSI Index): 20%

Commodities (DJUBS Index): 5%

Diversified Portfolio 95% x Diversified Portfolio

+ 5% SGI VI Beta

90% x Diversified Portfolio

+ 10% SGI VI Beta

Since 18 Jun 2007 (5 Year) 4.18% 6.18% 8.16%

Since 1 Sep 2008 (Financial Crisis) 2.98% 5.42% 7.85%

Since 14 Mar 2011 (Launch Date) 0.53% 4.53% 2.53%

Source: Bloomberg as of June 18th 2012

Annualised Return Comparison

0

100

200

300

400

500

600

700

90

100

110

120

130

140

150

160

Jun-2007 Jun-2008 Jun-2009 Jun-2010 Jun-2011 Jun-2012

Diversified Portfolio

90% Diversified Portfolio + 10% SGI VI Beta Index

95% Diversified Portfolio + 5% SGI VI Beta Index

SGI VI Beta Index

TAIL HEDGING

13

ALTERNATIVE INVESTMENT

VOLATILITY PREMIUM ACCESS TO VOLATILITY PREMIUM

CASE STUDY

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

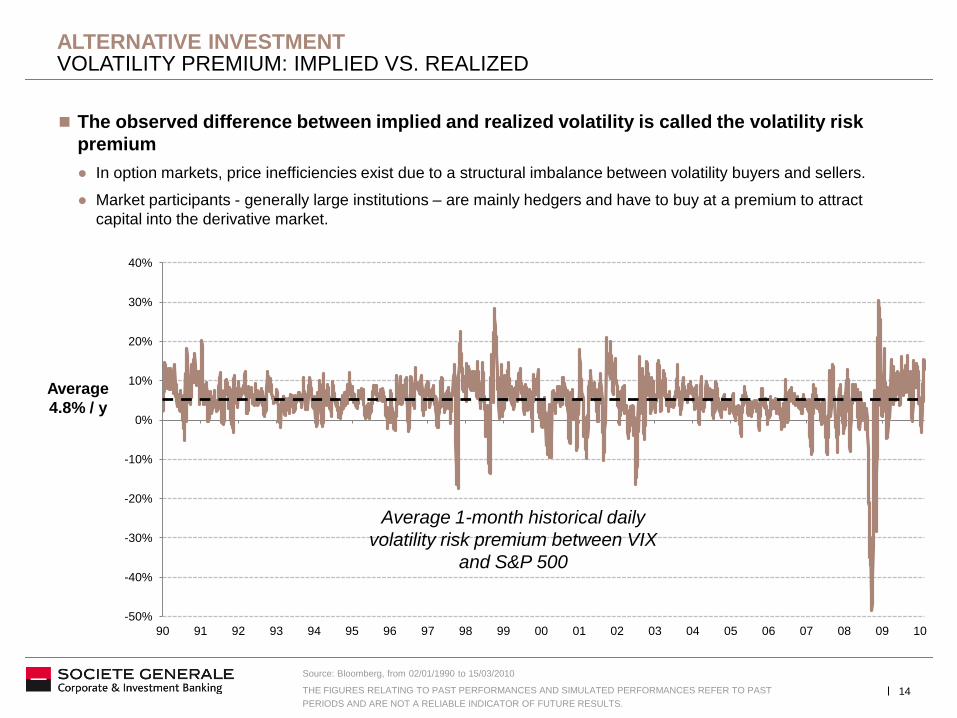

The observed difference between implied and realized volatility is called the volatility risk

premium

● In option markets, price inefficiencies exist due to a structural imbalance between volatility buyers and sellers.

● Market participants - generally large institutions – are mainly hedgers and have to buy at a premium to attract

capital into the derivative market.

Average

4.8% / y

Average 1-month historical daily

volatility risk premium between VIX

and S&P 500

Source: Bloomberg, from 02/01/1990 to 15/03/2010

THE FIGURES RELATING TO PAST PERFORMANCES AND SIMULATED PERFORMANCES REFER TO PAST

PERIODS AND ARE NOT A RELIABLE INDICATOR OF FUTURE RESULTS.

ALTERNATIVE INVESTMENT VOLATILITY PREMIUM: IMPLIED VS. REALIZED

14

BASIC WAY: SHORT VARIANCE SWAP

● VARIANCE SWAPS ARE FORWARD CONTRACTS ON THE REALIZED SAMPLE VARIANCE OF RETURNS

OF AN UNDERLYING ASSET.

● THEY PROVIDE A LINEAR PAYOFF THAT IS A FUNCTION OF THE SAMPLE VARIANCE OVER THE

CONTRACT LIFE.

ALTERNATIVE INVESTMENT CAPTURE THE VOLATILITY PREMIUM – BASIC WAY

Can be easily customised

Advantages

Higher bid-offers

Less liquid, as OTC

Disadvantages

LONG LEG:

IMPLIED VOLATILITY

SHORT LEG:

REALIZED VOLATILITY

15

SGI VOL PREMIUM DYNAMIC 2 INDEX

1. Trend Indicator

● “Trend indicator” to determine the position on the variance

swaps Long or Short?

● The Trend Indicator is a dynamic mechanism that looks at

different market parameters

short term realized volatility of S&P 500 Index

change in VIX

the observed volatility premium

2. Taking a Long/Short Position

● Positions taken each day in 1-month variance swaps, on a

fraction of the index value.

● The index is computed on a daily basis using mark-to-market

levels of the variance swaps.

16

The figures used in this example are given for purely indicative purposes, the objective is to describe the

mechanism of the product. It allows an understanding of how the product would have performed at different

market stages over previous years, but is no guarantee as to future returns and has no contractual value

Trend Indicator

Short position in 1M

Variance Swaps

(40% leverage)

Long position in

1M Variance Swaps

(10% leverage)

If positive

If negative

Short

Long

Trend Indicator

Short position allows to capture the spread between implied and realized volatility on the S&P 500 Index. Long position enables to quickly offset the risk of a short realized volatility exposure in volatile markets.

Seller of variance swap

Buyer of variance swap

Buyer pays the swap strike

ALTERNATIVE INVESTMENT CAPTURE THE VOLATILITY PREMIUM – SMART WAY (1)

3. Dynamic Exposure

● The dynamic exposure mechanism makes it possible to deleverage more quickly in case of a sudden rise of volatility

(40% leverage for a short position and 10% leverage for a long position).

● The Index tracks the performance of a variance swap’ portfolio¹.

17

The figures used in this example are given for purely indicative purposes, the objective is to describe the mechanism

of the product. It allows an understanding of how the product would have performed at different market stages over

previous years, but is no guarantee as to future returns and has no contractual value

1The portfolio is usually made up of around 21 short or long positions, corresponding to the number of business days during the month.

2 Computed one day before

3 Number of business days corresponding to 30 calendar days since the launch of the previous variance swap (Trend Indicator is the

one observed for the week, not necessarily on that day)

ALTERNATIVE INVESTMENT CAPTURE THE VOLATILITY PREMIUM – SMART WAY (2)

SGI VOL PREMIUM DYNAMIC 2 INDEX

18

THE FIGURES RELATING TO PAST PERFORMANCES AND SIMULATED PERFORMANCES REFER TO PAST PERIODS

AND ARE NOT A RELIABLE INDICATOR OF FUTURE RESULTS. THIS ALSO APPLIES TO HISTORICAL MARKET DATA

Source: Bloomberg as of June 18th 2012

50

100

150

200

250

300

350

Jan-1999 Jan-2003 Jan-2007 Jan-2011

SGI Vol Premium Dynamic 2 Index S&P500 Index

SGI Vol Premium Dynamic 2

1Y 0.04%

5Y 7.48%

Since Launch

(14 Mar, 2011) 4.02%

Volatility (5Y) 9.74%

Sharpe 0.77

Source: Bloomberg as of June 18th 2012

19

The SGI VI Beta Index (The “Index”) is the sole and exclusive property of Société Générale (“SG”). SG has contracted with Standard & Poor’s (“S&P”) to maintain and

calculate the Index. S&P shall have no liability for errors or omissions in calculating the Index. The VIX® is the property of the Chicago Board Options Exchange,

Incorporated. The VIX ® Index has been licensed for use by SG in connection with the Index.

The SGI Vol Premium Dynamic 2 (The “Index”) is the sole and exclusive property of Société Générale (“SG”). SG has contracted with Standard & Poor’s (“S&P”) to

maintain and calculate the Index. The S&P 500® Total Return index is the exclusive property of S&P and the CBOE Volatility Index® (the VIX®) is the property of the

Chicago Board Options Exchange, Incorporated. The S&P 500® Total Return index and the VIX® have been licensed for use by SG in connection with the Index. S&P

shall have no liability for any errors or omissions in calculating the Index.

Without prejudice to its legal or regulatory obligations, Société Générale may not be held responsible for any financial or other consequences that may arise from investing

in a product having as its underlying the index described herein (the “Index”), and investors are responsible, prior to making any investment in a product having the Index

as its underlying, for making their own appraisal and, if they deem it necessary, to seek and obtain professional advice on the risks and merits of the product.

No offer to contract / no possibility to invest directly in the Index: this document does not constitute an offer, a solicitation, an advice or a recommendation from Société

Générale to purchase or sell the Index, which cannot be invested in directly. The purpose of this document is simply to describe the principles and main financial

characteristics of the Index.

General selling restrictions: a product having the Index as underlying may be subject to restrictions with regard to certain persons or in certain countries under national

regulations applicable to such persons or in said countries. It is each investor’s responsibility to ascertain that it is authorised to conclude, or invest into, this product. By

undertaking such an investment, each investor is deemed to certify to Société Générale that it is duly authorised to do so.

Warning regarding the Index: the Index is the sole and exclusive property of Société Générale.

Société Générale does not guarantee the accuracy and/or the completeness of the composition, calculation, dissemination and adjustment of the Index, nor of the data

included therein.

Société Générale shall have no liability for any errors, omissions, interruptions or delays relating to the Index. Société Générale makes no warranty, whether express or

implied, relating to (i) the merchantability or fitness for a particular purpose of the Index, and (ii) the results of the use of the Index or any data included therein. Société

Générale shall have no liability for any losses, damages, costs or expenses (including loss of profits) arising, directly or indirectly, from the use of the Index or any data

included therein. The levels of the Index do not represent a valuation or a price for any product referencing such Index. The Index rules (the “Index Rules”) define the

calculation principles of the Index and the consequences on this Index of extraordinary events which may affect one or several of the underlying programmes on which it

is based. A summary of the Index Rules is available either online on the website

This index includes embedded leverage which amplifies the variation, upwards or downwards, in the value of the underlying instrument(s).

Commercial nature of the document: this document is of a commercial and not of a regulatory nature.

Information on market data presented in this document: the market information presented in this document is based on data at a given moment and may change from time

to time.

Confidentiality: this document is confidential and may be neither communicated to any third party (with the exception of external advisors on the condition that they

themselves respect this confidentiality undertaking) nor copied in whole or in part, without the prior written consent of Société Générale.

Conflict of interest management: The roles of the different teams involved within Société Générale in the design, maintenance and replication of some of the Indices have

been strictly defined. Where Société Générale holds the product and other positions exposing it to some of the Indices for its own account, the replication of these Indices

is made in the same manner by a single team within Société Générale, be it for the purpose of hedging the product held by external investors or for the purpose of the

positions held by Société Générale acting for its own account. Société Générale may take positions in the market of the financial instruments or of other assets involved in

the composition of some of the Indices, including as liquidity provider.

19

19 Société Générale Index

E-mail address: [email protected]

Webite: www.sgindex.com

Bloomberg Page: SGIX

IMPORTANT INFORMATION

20

The information contained herein, including any expression of opinion, and any information which accompanies this presentation or which is supplied

subsequently, has been obtained from or is based upon sources believed to be reliable but has not been independently verified and is not guaranteed as to

accuracy. This presentation and any information which accompanies this presentation does not constitute, and under no circumstances should be considered in

whole or in part as, an offer to buy or sell, a solicitation, a price (firm or otherwise), advice or a recommendation of any kind, to acquire or dispose of any

transactions and to the extent permitted by law

SG is not, and will not be, responsible for ascertaining whether all the risks and other significant factors associated with the transactions contemplated herein

have been identified or disclosed, nor for providing advice to you:- (1) as to whether you should enter into the transaction; or (2) on the documentation to be used

for the transaction; or (3) on the merits of purchasing or selling any investments mentioned herein. The information contained herein is indicative and you must

make your own assessment of the transaction and the risks and benefits associated with it and of all the matters referred to in the preceding sentence and, in this

connection, you should consult, to the extent necessary, your own legal, financial, tax, accounting and other professional advisors prior to entering into any

transactions. Neither SG nor any of its officers or employees makes any representation as to, or assumes any responsibility or liability for, the merits, suitability,

expected or projected success, profitability, performance or benefit of any such transaction. SG recommends that you enter into transactions only after having

considered, with the assistance of external advisors, without reliance upon SG, the specific risks of any transaction, including but not limited to, the financial,

investment, legal, tax and accounting implications so as to enable you to appraise and understand the financial and legal terms of such transaction and to enter

into such transaction in reliance on your own judgment and that of your advisers and not on any views expressed by SG.

This presentation was prepared exclusively for your benefit and your internal use. Neither the presentation nor any of its contents may be disclosed to,

reproduced or used or relied upon by, any other person or used for any other purpose without the prior written consent of SG.

Notice to Australian Investors: Société Générale (ABN 71 092 516 286) is regulated in Australia by APRA and ASIC and holds an AFSL no. 236651 issued under

the Corporations Act 2001 (Cth) ("Act"). The information contained in this document is only directed to recipients who are wholesale clients as defined under the

Act. SG Securities (HK) Limited is a Registered Foreign Company and Foreign Financial Services Provider in Australia (ARBN 126058688), and is exempt from

the requirement to hold an Australian financial services license under the Act in respect of financial services. SG Securities (HK) Limited is regulated by the

Securities & Futures Commission under Hong Kong laws, which differ from Australian laws. The information contained in this document is only directed to

recipients who are wholesale clients as defined under the Act.

Notice to Hong Kong Investors: This document is distributed in Hong Kong by SG Securities (HK) Limited and Société Générale Hong Kong Branch, which is

regulated by the Securities and Futures Commission and Hong Kong Monetary Authority respectively. This document is issued solely to "professional investors"

within the meaning of the Securities and Futures Ordinance (Cap. 571) of Hong Kong and any rules made under that Ordinance.

Notice to Japanese Investors: This document is distributed in Japan by Société Générale Securities (North Pacific) Ltd., Tokyo Branch, which is regulated by the

Financial Services Agency of Japan. This document is intended only for the Specified Investors as defined by the Financial Instruments and Exchange Law in

Japan and only for those people to whom it is sent directly by Société Générale Securities (North Pacific) Ltd., Tokyo Branch, and under no circumstances should

it be forwarded to any third party.

Notice to Singapore Investors: This document is provided in Singapore by or through Société Générale, Singapore Branch and is only provided to institutional

investors, as defined in Section 4A of the Securities and Futures Act, Cap. 289.

Notice to Investors in Asia-Pacific region: This document is to present you with all our capital markets activities across Asia- Pacific region and may only be

distributed to the professional institutional investors. The product mentioned in this document may not be eligible or available for sale in your country and may not

be suitable for all types of investors.

20

20 Société Générale Index

E-mail address: [email protected]

Webite: www.sgindex.com

Bloomberg Page: SGIX

IMPORTANT INFORMATION