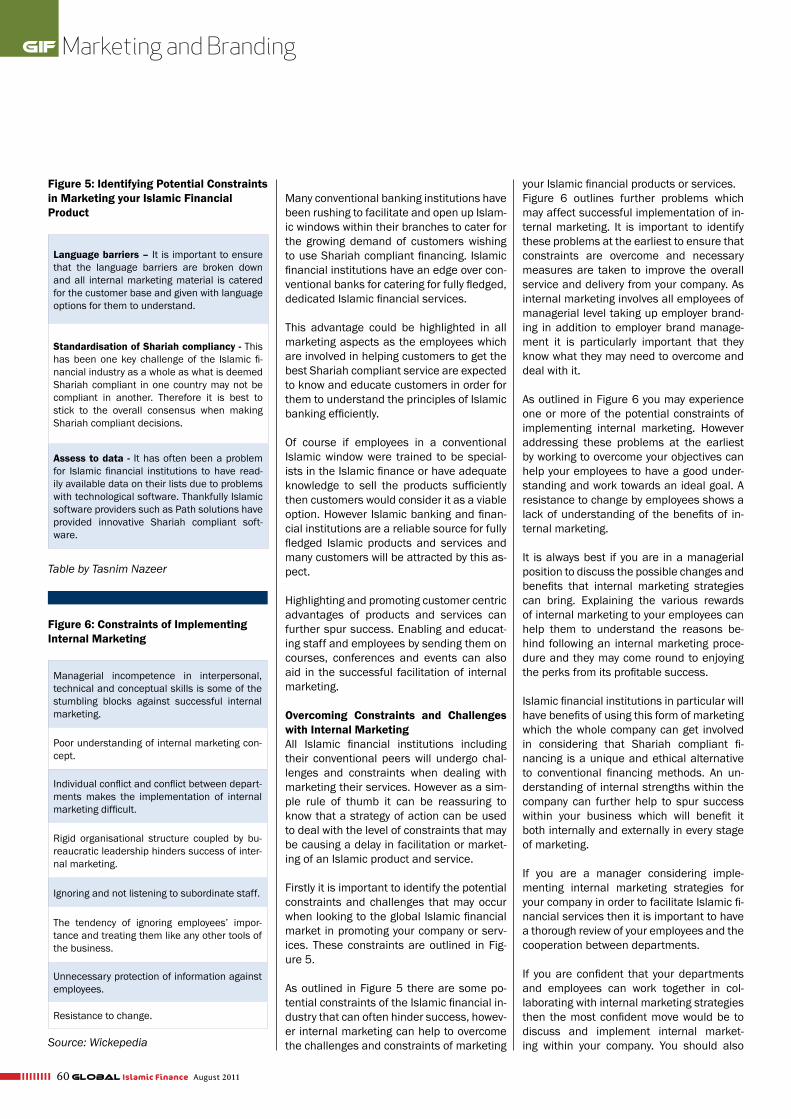

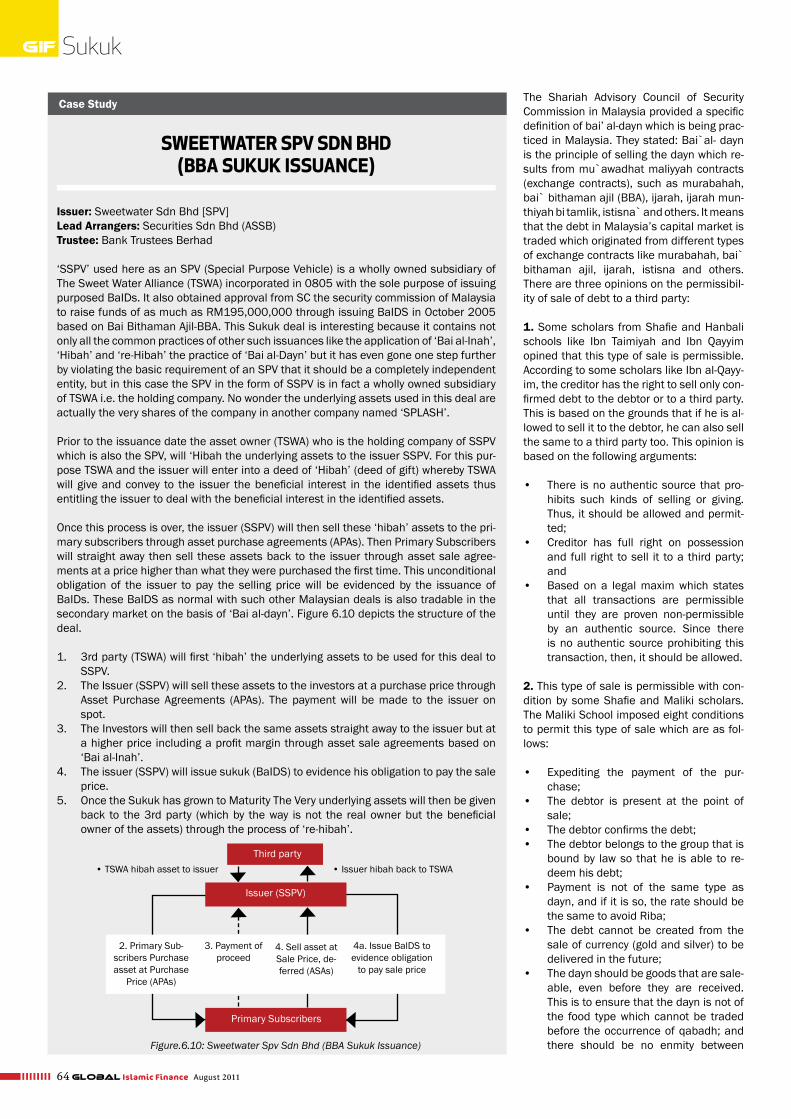

201108 Global Islamic Finance

88

Ethical Banking & Finance UK: £6.00 PUTTING CORPORATE STRATEGY IN PLACE ISLAMIC BANK HOW TO RUN AN ISLAMIC BANK Islamic Finance gains momentum in Europe P. 32 Islamic Project Financing Setting the Agenda for Innovative Opportunities P. 28 State of Qatar End of Islamic Banking Windows August 2011 GLOBAL Finance Islamic www.globalislamicfinancemagazine.com P. 42

Transcript of 201108 Global Islamic Finance

Ethica

l

Bankin

g & Fi

nanc

e

UK: £6.00

PUTTING CORPORATE STRATEGY IN PLACE

ISLAMIC BANKHOW TO RUN

AN ISLAMIC BANK

Islamic Finance gains momentum in Europe

P. 32

Islamic Project Financing Setting the Agenda for Innovative Opportunities

P. 28

State of QatarEnd of Islamic Banking Windows

August 2011

GLOBAL

FinanceIslamicwww.globalislamicfinancemagazine.com

P. 42

Addressing tomorrow’s business needs today

Global Risk Management Group provides Banks, Investment companies, Insurance Companies, Brokerage Houses, Leasing, investment banks and other major companies, across all industry sectors, with assistance and support on a broad range of risk management services and practical issues affecting an employee’s ability to perform their best at work.

www.grmg.co.uk

GRMG ads A3.indd 16-17 04/05/2011 12:52:40

Addressing tomorrow’s business needs today

Global Risk Management Group provides Banks, Investment companies, Insurance Companies, Brokerage Houses, Leasing, investment banks and other major companies, across all industry sectors, with assistance and support on a broad range of risk management services and practical issues affecting an employee’s ability to perform their best at work.

www.grmg.co.uk

GRMG ads A3.indd 16-17 04/05/2011 12:52:40

Contents;QWERTYUIIOPDFHJUIIOPDFHJJIslamic Banking

14

14 How to run an Islamic bankPart I: Putting corporate strategy in place, values, regulations The term ‘Islamic banking’ means the carrying out of banking operations in compliance with Shariah principles. Islamic banking and finance have been growing rapidly over the years. Its successes not only include countries with large Muslim populations but also those countries where the Muslim population is a minority. Banking practices with the concept of receipt and payment of interest are not in accordance with Shariah principles. In the past Muslim communities could not avoid conventional ways of banking but Islamic banking practices have been flourishing over the past years so that Islamic finance is now recognised throughout the financial world...

News

9 Islamic Finance News

Interview

25 Islamic Finance is one of the key functional areas for the Halal IndustryInterview with Mahmood Hasan, CEO of Rasul Group of CompaniesMahmood Hasan is the CEO of Rasul Group of Companies, Pakistan. With a Masters in Business Adminis-tration he established this entrepreneurial venture in 1983. His transformational leadership and visionary approach led to the establishment of the brand Bake Parlor. The Halal industry and Islamic finance share an economic and ideological interdependence and also have a high growth potential when looking at the retail and commercial forefront...

World Islamic Finance Review

28 State of Qatar: End of Islamic Banking WindowsAt the beginning of February, 2011, Qatar Central Bank (QCB) notified all conventional banks in Qatar that they were required to stop operating Islamic windows (IWs) by the 31st of December 2011.On the 10th of February 2011, QCB issued a public press release detailing the requirements and explain-ing the reasons for its decision to stop the operation of the IWs...

32 Part 1: Islamic Finance gains momentum in EuropeIslam all too often resonates negatively in Europe, with much non-Muslim public opinion uncomfortable with Islamic culture and values. Secular and Christian opinion is at best suspicious of Shariah, Islamic law, and indeed often antagonistic. The notion of wanting to apply Shariah principles to banking and finance is treated with scepticism if not outright hostility, especially as there is no concept of Christian or Jewish banking, even if there are some parallels between Shariah financial principles and the teaching of the Old Testament...

32

25

Islamic Finance

42 Part 1: Islamic Project Financing Setting the Agenda for Innova-tion Opportunities The global demand for Islamic project financing is growing at an unprecedented rate where many investors around the world are looking into major financial hubs to aid in funding lucrative projects. As the Islamic financial market adheres to the principles set out by Shariah law all investments and projects have to be constructed in a Shariah compliant manner and authorised by an Islamic financial governing or regulatory body of the country. There are many lucrative sectors which provide scope for profitable projects across the spectrum of Islamic finance. Traditionally projects in the infrastructure sector proved more rewarding as there were many opportunities especially in the Islamic financial hub of the United Arab Emirates...

48 Do Conventional and Islamic Finance Share Common Episte-mology?An overall socio-political-economic system gives rise to an economic system out of which grows a system of financing to facilitate production, trade and exchange. The idea of the contemporary conventional eco-nomic system is usually traced to Adam Smith’s conception of an economy as envisioned in his book, the Wealth of Nations. What has been ignored until recently, however, the fact that, from an epistemological point of view, Smith’s vision of the economy is embedded in his vision of a moral-ethical system that gives rise to the economy envisioned in the Wealth of Nations...

4 Global Islamic Finance August 2011

Marketing and Branding

55 Unleash the Power of Internal Marketing in your Islamic Finan-cial Institution There are various forms of marketing techniques and strategies that can help to spur the Islamic finance industry forward. However one such technique which cannot be understated is the effectiveness of using internal marketing strategies. So what exactly is the concept of internal marketing? Internal marketing is the application of processes and principles within the marketing framework of financial institutions. Internal marketing therefore involves a business or company using various different methods and dividing marketing roles within their departments transforming them into business units...

Market Review

54 Russia needs Changes to Law to Facilitate SukukAs the Islamic finance industry is growing at an unprecedented speed, Russia still remains to have changed laws in order to facilitate sukuk. Russian borrowers are pitching plans to sell the nation’s first Islamic bonds even as regulators lag behind in customising laws for the industry...

72 Oman to Add a Staggering $6 Billion Worth of Islamic Financial AssetsIt has been reported that Oman is to add a staggering $6 Billion worth of assets for the development over the next few years, according to estimates by Ernst & Young’s Islamic Financial Services Group...

74 Islamic Countries Urged To Adopt Economic Financial ReformsSaudi Arabia’s finance minister has reportedly urged Muslim countries to adopt suitable economic reform programs and adapt to the changing global financial economic changes to confront the challenges of fac-ing them and building solutions...

75 Islamic Finance Trade Sector Expands in Asia and Middle EastIslamic trade finance has grown progressively towards Shariah-compliant banking and could serve as one of the key growth drivers to aid the $1 trillion Islamic finance industry in its growing global expansion...

80 Gulf Banks Tackle Challenges to Boost Shariah InvestmentsGulf Banks are making significant efforts to boost Arabian Gulf banks saying that they are more ready to accept Asian Islamic debt as Shariah-compliant, allowing them to invest in a market that has issued twice as much sukuk as the Middle East this year...

76 Event Review

79 Events Calendar

82 Business Directory

84 Glossary

86 In the Next Issue

62

55

48

Sukuk

62 Analysis of Sale/Debt based Sukuk: The Malaysian Saga, part 2 The absence of bonds instruments in most al-murabaha project finance particularly in the ever liquid Middle-East countries may be explained by the controversy on the validity of using bai al-‘inah in the securitisation process and the application of bai al-dayn at a discount in bonds in secondary trading. The question now is; what are the underlying issues behind this controversy about the legitimacy of bai al-‘inah and bai al-dayn in Islamic law? What could explain its rejection in the Middle-East countries while gaining acceptance in Malaysia?...

Latest IssueGet the instant access toIslamic finance news & articles

Getting SocialJoin our fast growing Facebook Group

Awards of the DecadeFind out more about prestigious award ceremony

Article CollectionGet the articles from ourExclusive collection

GIFM Online

Scan the barcode with your mobile device to be directed to the specified website.

78 Book Review

6 Global Islamic Finance August 2011

Website:

www.globalislamicfinancemagazine.com

Published by:

Business Media Group Ltd.Marble Arch Tower, LondonW1H 7AA, United KingdomTel: +44 207 859 8201Fax: +44 207 183 4004

Editor-in-Chief

Farhad ReyazatPhD in Risk Management

International Editorial Board

Prof Dr Khawaja Amjad Saeed, Principal of The University of the Punjab, PakistanProf Habib Ahmad, Sharjah Chair in Islamic Law and Finance in the School of Government and International Affairs at University of Durham, United Kingdom Prof Rodney Wilson, Professor in the School of Government and International Affairs at Durham University, United KingdomProf Humayon Dar, Chief Executive Officer at BMB Islamic UK, United KingdomProf Muhammed Shahid Ebrahim, Professor of Islamic Banking and Finance at the Bangor Business School, United KingdomProf Andrew White, Director of International Islamic Law & Finance Centre, Associate Professor of Law, Singapore Management University, SingaporeProf Simon Archer, ICMA Centre, Henley Business School, University of Reading, United KingdomHailey College of Banking & Finance, University of the PunjabDr Majdi Ali Ghaith, King Saudi University Assistant Professor Business Administrator Department, Saudi ArabiaDr Abu Umar Faruq Ahmad, School of Law University of Western Sydney Australia, Australia Dr Julien Pelissier, Lecturer in Islamic economics’ law, FranceDr Alberto Brunoni, Founder and Director of AASAIF, Italy Dr Aznan Hassan, Shariah scholar Bursa Malaysia, Malaysia

Dr Zukifli Hassan, PhD Research Scholar at University of Durham, United KingdomDr Mohammed Obaidullah, Economist at the Islamic Research and Training Institute (IRTI) of the Islamic Development Bank, Saudi ArabiaDr Amal El-Kharouf, Head of Research and Consultancy Department at University of Jordan, JordanDr M.Kabir Hassan, Associate Professor and Associate Chair of the Department, University of New Orleans, USADr Abdelhafid Benamraoui,Westminster Business School, United KingdomDr M. Ishaq Bhatti , Faculty of Law and Management, La Trobe University, AustraliaMughees Shaukat, PHD researcher and Assistant Researcher in INCEIF & ISRA, MalaysiaWarren Edwards, CEO of Delphi Risk Management, United Kingdom John Sandwick, Islamic Wealth & Asset Management Independent Consultant, Switzerland Brian Kettel, Director at Islamic Banking and Finance Training, United Kingdom Salina Hj. Kassim, Department of Economics atInternational Islamic University Malaysia, Malaysia Kasim Randeree, Saïd Business School, University of Oxford, United Kingdom Abbas J. Ali, School of International Management Eberly college of Business,Indiana University of Pennsylvania, USA

Contributors

Professor Rodney WilsonDr Farhad ReyazatDr Osama AlsulaimanRichard WilliamsImran PashaMughees Shaukat

Siraj Al IslamAbbas MirakhorEdib SmoloWarren EdwardesDato’ Hafsah Hashim

Shah FahadMahmood HasanTasnim NazeerSara HasanAutumn Louise St. John

Editing and Proofreading

Colette Sensier Carina Lewis

Executive staff

Agnes GradzewiczDavid SmithGareth PlattSimon Hartshorne

Amy ThompsonNelly AhmedovaRitika BanerjeeAjay Surti

Beata JagorowPatricia Ke-Hsuan TsaiTajah BrownDioumel Ka

Somayeh Rastgar Kamran Khalid

Top Brand Ambassadors

Saleem Uddin Faisal, BahrainAmjad Suri, IndiaAmjad Suri, IndiaSyed Ilyas, IndiaMahamoud El Aref, EgyptShuhratbek Iskandarov, Germany

Basil Armoush, JordanBouhssine Ben Jadda, MoroccoAuwalu Ado, NigeriaAdeeb Zaki, Pakistan Asim Hameed, Pakistan Muhammad Farrukh Saleem, Pakistan

Said Bunu, QatarFarhaa Xha, Saudi ArabiaMirak Farook, Sri LankaKareem Hammour, UAEMuhammad Zeeshan, UAEMajd Ghanem, UAE

Ichrak Bennani, UAEMuhammad Athar Khan, UAEIchrak Bennani, UAEAnees Razzak, United KingdomDian Kartika Rahajeng, United Kingdom

Worldwide Advertising Enquiry – Business Media Group, Tel. 0044 2078598201UAE Representative - 7dimensions Media, Tel. 0097 165579579Saudi Arabia Representative – Marketing Advanced System, Tel. 00974 444528036Qatar Representative - Marketing Advanced System, Tel. 00974 444528036Malaysia Representative – Fusion Brand, Tel. 0006 037954 2075Iran Representative – Sabin Business and Economics Group, Tel. 0098 21 882073368United Kingdom & Luxury Sector - Major Media Ltd, Tel. 0044 208 467 8884

Global Islamic Finance Awards www.globalislamicfinanceawards.comGlobal Islamic Finance Conferences www.globalislamicfinanceconferences.comGlobal Islamic Finance Events www.globalislamicfinanceevents.comGlobal Islamic Finance Jobs www.globalislamicfinancejobs.comIslamic Finance Marketing Services www.businessmediagroup.co.uk

Representative Offices Our Brands

Illustrator– Rasha MahdiGlobal Newsstand Distribution - Native Publisher Services LtdFind out more about Global Islamic Finance Global Newsstand Sale at www.globalislamicfinancemagazine.com/global-saleAnnual Individual Subscriptions from £109.99 €129.99 $169.99Contact us on +44 2078598201 or email on [email protected]

Reprints are available for sale, please contact our sales office for individual quotation. Contact us on +44 2078598201 or email on [email protected] Sites: join our groups on Facebook & Linked InAdvertising and Sponsorship: Global Islamic Finance Magazine provides long-term brand and product placement op-portunities as well as initial responses. Continuous monitoring and updating of our database ensures that each copy of Global Islamic Finance Magazine is precision-targeted with no wastage. Our magazine is distributed around the world and helps to establish a tighter community that can interact and work together. Please contact us on +44 207 859 8201 or email to [email protected].

Copyright 2007 by Business Media Group Ltd. The views expressed in contents are the authors’ and not necessarily those of Business Media Group Ltd. No part of this publication may be reproduced or used in any form of advertising without prior permission in writing from Business Media Group Ltd. While every care has been taken in the publication on this magazine, Business Media Group Ltd will not be responsible for accuracy of the information or for any

consequence arising from it.

Trade Financeservices

www.otfonline.co.uk

A business can grow only as much as its horizon allows.

otf ads 1.indd 23 02/05/2011 11:41:20

8 Global Islamic Finance August 2011

gif

Islamic bank-ing is at the peak of its

success with many branches opening up worldwide. It is there-fore crucial that both business professionals and entrepreneurs understand the best ways to establish an Islamic financial insti-tution which adheres to the principles of the Shariah

„Islamic Banking is fast developing in the global financial world with many establishments being set up worldwide to cater for the demands of both Muslims and Non Muslims around the world. It is therefore imperative that the development of Islamic banks is well defined and the system of running a Shariah compliant bank is well under-stood by all industry professionals.

The last decade has seen an increasing demand for Shariah compliant banking with well estab-lished conventional banks opening up Islamic windows to cater for the rising demand. The UK alone has an estimated US$300 million of com-bined assets and overall the Islamic finance in-dustry is expected to rise to over US$1 trillion. This provides adequate scope for the develop-ment of Islamic banks and a real opportunity for companies and interested business professionals to learn more about running an Islamic banking institution.

If you are considering opening up an Islamic bank there are a number of issues which need to be addressed. It is first and foremost crucial that you have a good support team and reliable regulatory body who understand the concepts of Shariah finance to the core. With efficient Shariah super-visory backing your financial institution you can then implement the facilitation of Shariah compli-ant products and services which are currently in global demand around the world.

Islamic banking institutions cannot divert from the ethics of Shariah as all transactions should remain Shariah compliant and this should be the primary ethos when establishing and running your bank. Malaysia, the Middle East and the GCC have played a significant role in supporting the facilitation of the running of Islamic banks around the world. The Islamic Development Bank (IDB) in particular has contributed significantly to the implementation of Islamic banks and funding throughout the world and is a forerunner in estab-lishing Islamic banking institutions worldwide.

It is important to remember that developing strat-egies is key in achieving profitable asset growth for any potential development of an Islamic bank. Improving the position of risks is a crucial aspect that contributes significantly to the Islamic bank-ing strategy, although Islamic banks have man-aged well in overcoming negative asset of invest-

ment depositors. Islamic banks have more than 300 institutions spread over 51 countries, includ-ing the United States, as well as an additional 250 mutual funds that comply with Islamic principles. It is estimated that over US$822 billion worldwide Shariah-compliant assets are managed according to The Economist.

Although the implementation of Islamic banks may face some challenges such as liquidity and the lack of Islamic liquid instruments it still has potential for any avid investor wishing to tap into the lucrative current market. Islamic banking is continuing to grow which is why many internation-al banks such as HSBC, Deutsche Bank and many others have developed their own Islamic windows or services.

The main challenge that the heads of Islamic banks face is the core problem of regulatory con-formity to the Shariah. Therefore standardisation is key in Islamic finance to ensure that all trans-actions and services have set guidelines which can be applied to Islamic banking institutions worldwide. Islamic banking institutions need to address these challenges and work effectively alongside Islamic regulatory bodies to ensure Shariah compliancy at all times which will help to build up the prestige of Islamic banks around the world.

Promoting transparency and product breadth can further help Islamic banks to be successful in promoting Shariah-compliant funds. With almost 2 billion Muslims worldwide and a vast number of Non Muslims who prefer to use the ethical meth-ods of Shariah-compliant financing there is much scope for the development and success of Islamic banks worldwide.

Farhad ReyazatPhD in Risk Management Editor in Chief

Editorial Letter

To write the letter to the editor, send an email to [email protected].

2011 August Global Islamic Finance 9

Islamic finance newsIslamic finance news

gifNews

Bank Rakyat Indonesia’s Shariah Branch Debuts Scheme to Tap Gold in Islamic Fi-nance

It has been reported that BRI Shariah, a subsidiary of state-owned Bank Rakyat In-donesia, has launched a new product that allows its customer to buy gold in instal-ments, in a bid to draw broader segments of the population to Islamic banking.

The bank plans to provide Rp 400 billion ($46.4 million) in financing for customers to buy gold, president director Ventje Rahardjo said.

The first scheme of its kind in Indonesia, Precious Metal Ownership (KLM) is intended to appeal to the young, middle-class popu-lation because of its long-term investment appeal, with customers able to pay in instal-ments from six months to 15 years, Ventje said.

“Imagine that in 1998 gold was around Rp 78,000 per gram, and now it’s already over Rp 400,000 per gram,” he said. “How many have regretted not buying it at that time? With this facility, customers can buy gold at the current price and pay that in monthly in-stalments.”

The product utilises two Shariah contracts, qardh and ijara. Under qardh, the bank loans money to the customer to buy the gold, and the debtor is only required to repay the amount borrowed. The customer must keep the physical gold in the bank’s vault which, under ijara, is rented out by the bank.

Islamic finance must match the level of serv-ice and innovation of conventional banking, Ventje said, and that means taking unique approaches.

“I think the ‘hardcore’ Shariah market is fin-ished,” he said, “For Islamic banking to ex-pand, it has to see itself as part of overall banking, not as an alternative.”

Total Islamic lending in Indonesia reached Rp 75.7 trillion by the end of April, compared with Rp 1,843.5 trillion in conventional bank-ing, according to Bank Indonesia data.

At the end of May, BRI Syariah’s total financ-ing was almost Rp 6 trillion, about a third of which came from consumer financing. Ventje said the bank wants to reach Rp 9 trillion in financing by the end of 2011. The high target will erode the lender’s capital ad-equacy ratio to 15 percent by the end of this year, he said.

As of May, its capital adequacy ratio was at 20 percent. Although the bank has the full support from its parent company, it did not rule out selling sub-ordinate sukuk to bolster its capital.

Tenaga to Sell $1.7 Billion 20-Year Islamic Bond, CEO Says

Tenaga Nasional Bhd., Malaysia’s biggest power producer, plans to raise as much as 5 billion ringgit ($1.7 billion) from a 20-year ringgit-denominated Islamic bond of-fering.

Its chief executive officer said, “We plan to sell the bonds in August or September,” Che Khalib Mohamad Noh said. Proceeds from the offering, the company’s first debt sale since 2004, will be used to finance a coal-fired Manjung power plant in the northern state of Perak, Che Khalib said.

The utility is raising power generation capac-ity to meet rising demand on the Malaysian peninsula after shelving plans to buy elec-tricity generated by the Bakun hydroelectric dam on Borneo Island earlier this year. The 20-year paper will help alleviate a shortage of longer-dated securities that insurers need to match assets and liabilities.

“There will be demand for Tenaga’s sukuk as long-dated corporate Islamic paper is scarce,” said Michael Chang, who oversees $1 billion as head of fixed-income at MCIS Zurich Insurance Bhd. in Kuala Lumpur. “Ul-timately, demand will depend on the inter-est-rate outlook and pricing.”

The Islamic insurance, or takaful, industry grew at an annual pace of 16 percent over the last five years, double that of non-Islam-ic insurers, RAM Rating Bhd., the bigger of Malaysia’s two rating companies said last

week. Sarawak Energy Bhd., a Malaysian state-owned electricity company based on Borneo Island, sold 3 billion ringgit of 5-, 10- and 15 year Islamic bonds last month at the lower end of its yield guidance.

“It’s the right time to sell bonds in the do-mestic market as there’s a lot of liquidity,” Che Khalib said, adding that three invest-ment banks have been short-listed as un-derwriters. “The attractive price for the gov-ernment’s sukuk sold last week is a good benchmark.”

Sri Lanka Commercial Bank Launches Is-lamic Finance Unit

Sri Lanka’s Commercial Bank said it is starting alternative banking services com-pliant with Islamic Shariah principles with a three member committee of scholars to ensure that all products and services under the Islamic unit are Shariah compliant.

“As one of Sri Lanka’s largest private banks it is our obligation to ensure that the servic-es the unit provides are fully compliant with the tenets of the Shariah,” managing direc-tor Amitha Gooneratne said in a statement. M M A Mubarak, Fazil Farook and M M Mur-shid, from Sri Lanka’s All Ceylon Jamiyyathul Ulama will be on the Shariah board.

Commercial Bank will offer deposit products such as ‘Mudaraba’ savings accounts and ‘Mudaraba’ investment accounts’ and asset products such as ‘Murabaha,’ ‘Musharaka,’ ‘Diminishing Musharaka,’ and ‘Ijara’ leasing and import financing.

The bank said the products operate on the Islamic principle of both the bank and the customer sharing returns as well as risks. Mudaraba, which is a form of profit sharing investment, is a partnership where one part-ner provides full capital while the other man-ages the business.

Any profit made using the funds is divis-ible between the customer and the Bank at a predetermined ratio agreed to by both parties. Murabaha is the sale of goods by the Bank to customers at a cost plus profit where the selling price is decided at the time

Newsgif

10 Global Islamic Finance August 2011

of the sale. Murabaha can be used for local purchases or import of trading commodities and the customer is given a fixed tenor to settle the sales proceeds, the bank said.

Musharaka is a method of financing based on partnership, used for asset financing and export financing. Partners are entitled to a share in the profits that result from the project at a predetermined ratio which is mutually agreed upon at the time of enter-ing into the contract.

Diminishing Musharaka is a partnership in which one partner (the customer) will pur-chase the Bank’s share in a fixed asset over a predetermined period and become the owner of the asset.

The ownership of it will be passed to the client upon successful completion of the agreed terms. This can be used for property purchase, housing purposes and project fi-nance. Available for unregistered vehicles and equipment and machinery, Ijara is a contract where the lessor (Bank) who owns the asset transfers its usufruct to another person for an agreed period at an agreed rental.

The asset will be gifted to the customer when all lease rentals are met on time. Im-port financing involves providing letters of credit with financing on Islamic terms, this includes import Murabahas.

Bahrain’s Elaf Bank Licence Granted By Malaysia

Bahrain-based Elaf Bank, licensed by the Central Bank of Bahrain to operate as a wholesale Islamic bank with a paid-up cap-ital of $200 million, has been granted a li-cense by the Ministry of Finance Malaysia to open a branch office under the Malaysia International Islamic Finance initiative in Malaysia.

Elaf Bank was presented with the license during a formal ceremony held at Bank Ne-gara Malaysia in the presence of key officials and representatives from both sides.

Elaf Bank plans to start its branch office op-erations in Kuala Lumpur immediately now that it has fulfilled the formalities required for obtaining the license.

Jamil El Jaroudi, CEO of Elaf Bank, highlight-ed the importance of opening a branch of-fice in Malaysia, which falls in line with the bank’s long-term business strategy.

He said “Elaf Bank is developing its busi-ness through two hubs covering the GCC and MENA region and the South East Asia region, as a two-way business corridor. Be-

ing a wholesale Islamic bank headquartered in the capital of Islamic finance in the Middle East (Bahrain), the logical next step would be to open our first international branch of-fice in the capital of Islamic finance in South East Asia (Malaysia). This will help us oper-ate more efficiently and closely to meet the needs of our cross-regional clients, and be able to execute deals that will contribute to the sustainable growth of the Islamic fi-nance industry in both strategic markets,” he added.

“We firmly believe the bank is poised to not only widen its scope and reach through the opening of the branch office in Malaysia, but also to consolidate its excellent client rela-tions and business activities as a result of this step, which will no doubt generate ben-efits for both regions and create value for the Bank,” Jaroudi said.

Elaf Bank is a closed shareholding company incorporated in Bahrain. The bank encom-passes the full spectrum of wholesale Islam-ic banking with an additional differentiating dimension geared toward developing the

sukuk secondary market to act as a market maker. Elaf Bank currently provides a wide range of financial services to clients involv-ing investment banking including fund-rais-ing advisory, mergers and acquisitions and asset management and treasury and capital markets such as liquidity management, for-eign exchange, investment, structured prod-ucts and derivatives.

UAE Central Bank To Launch Islamic Cer-tificates of Deposit For Repo Facility

The UAE Central Bank is doing unprece-dently well and is about to launch a facility for repurchase for Islamic certificates of deposits in order to provide a new liquidity tool for the OPEC member’s banks.

It has been quite a challenge for the UAE with the lack of liquidity management tools in the Islamic finance industry, which has close to $1 trillion worth of assets globally. The Shariah compliant principle of the ban on interest rules out the possibility of most interbank tools therefore liquidity tools need to be further developed.

“The Shariah-compliant facility, which ac-cepts the Central Bank’s Islamic certificates of deposits as collateral, is introduced to provide a source of liquidity to banks,” the central bank said in its circular to banks, which was seen by Reuters.

The new facility is based on a murabaha concept; the circular also showed Murabaha is a sales contract, usually employed in com-modity transactions, that involves the pur-chase from an independent supplier which is then sold at an agreed price that includes the institution’s costs plus additional profit.

In November, the UAE central bank launched auctions of Islamic certificates of deposit, which saw volumes increasing steadily. Banks held 12 billion dirhams ($3.3 billion) worth of the certificates in April, some 10 percent of the overall volume, central bank’s data show.

“It is a repo with Islamic certificates of de-posits as collateral against cash and allows them to free up liquidity when needed,” said an executive at an Abu Dhabi-based bank.“There is a shortage of liquidity instruments and it is more pronounced on the Islamic side,” he said, asking not to be named. Is-lamic finance accounts for around 17 per-cent of banking assets in the UAE.

The UAE central bank’s monetary policy is limited by its dirham peg to the US dollar. It uses CDs auctions and repurchases facili-ties among other tools to regulate liquidity in the banking system. Late last month, the central bank said it planned to tighten regu-

Visit our website

We update news daily to deliver to you fresh information as it happens. Visit now»

Follow us on Twitter

Keep up to date with us here at the Entrepre-neurs’ Business Academy. Follow us»

Find us on Facebook

Are you on Facebook? Join us on Facebook to keep in contact with us via our page. Find us»

Link to us on LinkedIn

We’re on LinkedIn! Join in on our discussions on our LinkedIn Group page. Link up»

gif

Keep updated with latest news online

lations on how banks in the second largest Arab economy manage liquidity so they can better cope with future crises. UAE lenders remain hesitant to lend following Dubai’s $25 billion debt restructuring last year and weakness in the property sector, although deposits stand at their highest level in more than two years as the country enjoys safe-haven status amid unrest in the region.

Malaysian Islamic Banks See A Brighter Future

Islamic banks in Malaysia enjoy a bright fu-ture as they are able to compete and have the resilience to survive in the country’s open and competitive economy said Dr Awan Adek. Malaysia is an unprecedented Islamic financial hub with a significant scope to provide a benchmark to other Is-lamic financial hubs around the world.

Deputy Minister of Finance Datuk Dr Awang Adek Hussin said 21 Islamic banks are op-erating in Malaysia, with RM351 billion in combined total assets.

“There are 11 domestic Islamic banks; six foreign Islamic banks; and four international Islamic banks, reflecting bright prospects to plans to transform Malaysia into a premier international Islamic financial centre,” he said.

Siti Zailah sought explanation on the impli-cations to Islamic banks in the country fol-lowing impending restructuring of the banks. Awang Adek said the government had still no definite plans to carry out a restructuring ex-

ercise for banks, including for Islamic banks, except if the banks themselves conducted such an exercise. He alluded to the govern-ment’s merger of commercial banks under which 23 local banks were merged into nine. “Any merger exercise in future will hinge on the business decision by the banks’ board of directors and shareholders.

“Given the increasingly competitive econom-ic scenario today, banks will find ways and means that will favour them,” he said.

Awang Adek said completed merger exer-cises thus far had yielded good impact for banks as they have emerged stronger with higher working capital, have opened more branches and enjoyed higher national profile in the banking sector.

“The mergers have also enhanced banks’ financial standing; improved their internal

risk management; quality of their assets, efficient management; and are able to ven-ture into regional and global markets,” he added.

Bahrain Takaful Industry Prospering in 2011

The takaful industry in Bahrain is said to be prospering in 2011 as people are fa-vouring Shariah-compliant methods of Is-lamic insurance.

Takaful total contributions grew by 16.5 per-cent to reach BD13.4 million ($35.6m) in the first quarter of the year compared with BD11.5m for the same period last year,

according to the Central Bank of Bahrain (CBB). But traditional insurance still took the largest share of the market, down slightly at BD43.3m in the first quarter compared to BD44.1m last time. The insurance market in Bahrain consists of 27 domestic insur-ance companies and 11 branches of foreign insurance companies covering both direct insurance and reinsurance.

The recorded data for the insurance market during the first quarter of the year shows a slight increase of 1.8 percent in gross written premiums in the quarter up from BD55.7m last time to BD56.7m.

This growth was mainly due to the surge in the premiums of life insurance and the re-markable growth of the takaful. The com-bined capital of both conventional and taka-ful insurance companies grew by 4 percent to reach BD163.6m in the first quarter

compared to BD157.2m in the first quarter of 2010. The total assets of insurance com-panies increased by 6 percent to BD1.29 billion compared to BD1.22bn last time. Conventional insurance reported the high-est contribution in total assets at the rate of 79 percent.

Reinsurance companies that operate from Bahrain showed a rise in both reinsurance premiums and net profit during the first quarter, increasing reinsurance premiums by 5.6 percent to BD151m compared with BD143m. The net profit of reinsurance companies increased by 3.8 percent to reach BD8.1m compared to BD7m reached previously. “The key indicators show that

Newsgif

12 Global Islamic Finance August 2011

Islamic finance is one of the fastest grow-ing industries in the world. However, authentic education on the subject is not widely and easily available. We are delighted to work with Durham University and Hawkamah to fill this vacuum and create what will be the bench-mark in Islamic finance teaching. For the first time in the UAE, practitioners as well as stu-dents can benefit from a curriculum designed to teach both the academic and practical skills needed to succeed in Islamic finance

,,

,,Dr. Hussain Hamed Hassan, Managing Director, Dar Al Sharia

Institutional and corporate banking will always be more volatile than the retail side. However, the retail side has the most untapped potential in terms of offering investment products, Takaful and other forms of financing. Financial institutions that focus on the retail side will win over those focused on the institutional side

,,

,,

Tariq Al-Rifai,Director, Dow Jones Islamic Market Index

To prosper and grow, the Islamic financial industry needs to be served by firms that can deliver well-researched and designed tools that are Shariah-compliant and commer-cially viable; [it must] also comprehensively consider taxation, audit and accounting perspectives,,

Neil D Miller,Global head of Islamic finance, KPMG

,, Islamic finance is becoming much more prominent throughout the financial institu-tions of the world, rapidly growing from a niche industry to a mainstay of finance,,

John Willsdon, CIMA, the Chartered Institute of Management Accountants

,, We want to make that capacity available to regional Takaful, both in the GCC and Asia, in order to assist them in their reliance upon conventional facultative reinsurance for those risks that either exceed their own underwriting capacity or are for exposures that are not core to their underwriting capabilities. We hope that in time, all Takaful operators will realise that there is abundant Retakaful capacity available, and that they will seek to utilise only Retakaful when looking to mitigate their risk exposures and volatility of profits,,

Richard Bishop, CEO of GNL Insurance

,,

News gif

2011 August Global Islamic Finance 13

there has been minimal negative effect on the growth of insurance companies due to recent events in Bahrain, where indicators clearly show a rise in total insurance pre-miums, capital and assets of the insurance market in Bahrain, in addition to the remark-able growth of the takaful insurance industry keeping up with the growth of both the direct insurance market or the reinsurance market in previous years,” the CBB said.

Islamic Finance The ‘Greener’ Ethical Op-tion

Islamic Banking is the right platform to boost ‘green financing’ as it is based on the concept of promoting good practices and values,” said R Seetharaman, Chief Executive Officer of Doha Bank.

The Chief Executive delivered the inaugural address at a seminar on Islamic economics,

organised by the Indian Islamic Association – Qatar (IIAQ), under the title “Towards an Alternative Economy” at Omar Bin Al Khat-tab Preparatory School for Boys in Doha. Seetharaman said Islamic banking is not just a financial system but it is part of a to-tal value-based social system that seeks to enhance the general welfare of society as a whole.

“Sustainable environment development, developing water resources, facing global warming, ensuring women’s participation and promotion of small-scale enterprises are all part of green financing. This is clearly an area where Islamic Banking can play a pivotal role,” he said.

Seetharaman, however, noted that Islamic banking is currently in its infancy and faces several challenges. Young people should be encouraged to take up these challenges to ensure that this significant economic system carries through and plays a leading role in the current global financial stage. He added that Islamic banking is growing in popularity as Japan has just issued five Sukuk Ijara (Is-lamic leasing bonds) and many other coun-tries including Italy, Canada and Spain are showing great interest in such products and services of Islamic banking.

In the UK, there is a full-fledged Islamic bank, called the Islamic Bank of Britain, and there are 22 counters at conventional banks that offer Islamic banking services and prod-ucts. Seetharaman noted that infrastructure development projects in India can attract foreign investment if the country opens up its banking sector to Islamic banking. India’s

11th Planning Commission has earmarked $542bn for this sector, but hardly any mon-ey comes from the Gulf-based financiers as they are reluctant to deposit in an interest-based system.

P P Abdur Rasheed, former Head of Eco-nomics Dept at Government College, Malap-puram, India, and K Abdullah Hassan, Head of Research at Islamic University, Santa-puram, India, also delivered speeches on ‘Fundamentals of Islamic Economics’ and ‘Basic Principles of the Zakah System in Islam’. Nizar Kocheri, lawyer and noted hu-manitarian activist, delivered a felicitation speech and Abdul Wahid Nadvi, Acting Pres-ident of Indian Islamic Association, Qatar,

presided over the ceremony. V T Faisal, Gen-eral Secretary of IIAQ, welcomed the guests and Taj Aluva proposed a vote of thanks.

Albaraka Turkish Unit Secures $150m Funding

Albaraka Banking Group said its Turkish subsidiary has mandated several major banks to arrange a $150 million dual-cur-rency syndicated finance facility to expand its activities in the country.

Albaraka Türk said the banks involved in the arrangement of Murabaha financing facility are ABC Islamic Bank, Emirates NBD Bank, Noor Islamic Bank and Standard Chartered Bank (together the initial mandated lead ar-rangers and the book runners).

As a prominent participation bank in Tur-key, Albaraka Türk enjoys a market share of 19.14 per cent in the participation banking segment by asset size in Q1’ March 2011. The financing facility has a tenor of one year and carries a profit rate of 150 bppa over the relevant Libor/Euribor. The facility was launched into general syn-dication last month with banks from across the globe invited to participate in the facility. Financing under this facility will be used by Albaraka Türk to expand its financing activi-ties in Turkey. The facility has a tenor of one year and carries a profit rate of 150 bppa over the relevant LIBOR/EURIBOR.

The facility was launched into general syn-dication on the 29th June 2011, with banks from across the globe invited to participate. Albaraka Türk is amongst the first financial institutions and one of the pioneers in the field of interest-free banking in Turkey. It completed its establishment in 1984 and commenced operations in the beginning of 1985. Albaraka Türk is currently rated “BB” with negative outlook by S&P.

Albaraka Türk continues its operations in compliance with the Law of Banking num-bered 5411. Albaraka Türk was founded by Albaraka Banking Group (ABG), one of the prominent groups of the Middle East, Is-lamic Development Bank (IDB) and Alharthy Family, which served the Turkish economy for more than half a century.

As of the 31st May 2011, the foreign part-ners own 66.16 per cent, the domestic part-ners 11.33 per cent and 22.51 per cent are publicly held. Albaraka Türk has a market share of 19.14 per cent in the Turkish par-ticipation banking segment by asset size in Q1 2011.

Islamic finance is one of the fastest grow-ing industries in the world. However, authentic education on the subject is not widely and easily available. We are delighted to work with Durham University and Hawkamah to fill this vacuum and create what will be the bench-mark in Islamic finance teaching. For the first time in the UAE, practitioners as well as stu-dents can benefit from a curriculum designed to teach both the academic and practical skills needed to succeed in Islamic finance

,,

,,Dr. Hussain Hamed Hassan, Managing Director, Dar Al Sharia

Institutional and corporate banking will always be more volatile than the retail side. However, the retail side has the most untapped potential in terms of offering investment products, Takaful and other forms of financing. Financial institutions that focus on the retail side will win over those focused on the institutional side

,,

,,

Tariq Al-Rifai,Director, Dow Jones Islamic Market Index

To prosper and grow, the Islamic financial industry needs to be served by firms that can deliver well-researched and designed tools that are Shariah-compliant and commer-cially viable; [it must] also comprehensively consider taxation, audit and accounting perspectives,,

Neil D Miller,Global head of Islamic finance, KPMG

,, Islamic finance is becoming much more prominent throughout the financial institu-tions of the world, rapidly growing from a niche industry to a mainstay of finance,,

John Willsdon, CIMA, the Chartered Institute of Management Accountants

,, We want to make that capacity available to regional Takaful, both in the GCC and Asia, in order to assist them in their reliance upon conventional facultative reinsurance for those risks that either exceed their own underwriting capacity or are for exposures that are not core to their underwriting capabilities. We hope that in time, all Takaful operators will realise that there is abundant Retakaful capacity available, and that they will seek to utilise only Retakaful when looking to mitigate their risk exposures and volatility of profits,,

Richard Bishop, CEO of GNL Insurance

,,

gif

Islamic Banking gif

14 Global Islamic Finance August 2011

HOW TO RUN AN ISLAMIC BANKPUTTING CORPORATE STRATEGY IN PLACE, VALUES, REGULATIONS, PART I

Author: Imran Pasha, Head of Retail, Islamic Bank of Britain, United Kingdom Richard Williams, Finance Director, Bank of London and Middle East, United Kingdom Tajah Brown, Global Islamic Finance Magazine Editorial Team, United Kingdom

Abstract: When considering the aspects involved in running an Islamic bank it is vital to channel resources such as knowledge and relationships in the right direction in order to strike a balance be-tween innovation and control. Strategy is the art of creating value and providing frameworks, models and governing ideas. It could be compared to software, which needs to be updated as people expand their knowledge and gain experience. How to run an Islamic bank will explore the different strategies involved in the running of an Islamic bank such as risk positioning and financial fundamentals.

Islamic banking is a rapidly growing industry with the establishment of many new institutions em-bracing Shariah compliant banking. The UK has combined assets of US$300 million and overall the Islamic finance industry is worth an estimated one trillion US dollars globally. This article explores the key factors in running an Islamic bank, covering topics such as regulations and risk management. Im-ran Pasha and Richard Williams will give their views and advice on subjects such as the tailoring and overseeing of Islamic products and the attraction of non-Muslims to Islamic finance. The article also looks at the comparison of Islamic and conventional banks and the steps required when establishing an Islamic institution.

Keywords: Strategies, Shariah Principles, Basel III, Risk Management, Islamic Financial Products

2011 August Global Islamic Finance 15

Exploring the structure of Islamic bankingThe term ‘Islamic banking’ means the carry-ing out of banking operations in compliance with Shariah principles. Islamic banking and finance have been growing rapidly over the years. Its successes not only include coun-tries with large Muslim populations but also those countries where the Muslim popula-tion is a minority. Banking practices with the concept of receipt and payment of interest are not in accordance with Shariah princi-ples.

In the past Muslim communities could not avoid conventional ways of banking but Is-lamic banking practices have been flour-ishing over the past years so that Islamic finance is now recognised throughout the financial world. One of the first tasks that should be implemented when establishing an Islamic bank is the establishment of a reli-able body to provide Shariah supervision.

With the advice and approv-al of a Shariah supervisory body the bank can then start development of Shariah com-pliant products. The Shariah supervisory board enables the Islamic bank to conduct financial transactions which follow Shariah principles. The board should be a group of scholars who are expert in Islamic jurisprudence.

When focusing on the theo-retical aspect of Islamic fi-nance, the dominant issue is that of interest, which is prohibited in Islam and is not wanted or needed within Islamic banking operations. Islam teachings provide a strong foundation for organ-ising banking operations. This attitude towards interest in Islamic finance faced chal-

lenges when introduced to a world where interest plays an important role in most fi-nancial operations. The key principles of Islamic finance are the prohibition of riba, uncertainty and forbidden assets such as alcohol and the existence of underlying as-sets and finally, profit and risk sharing. The Shariah principles explain in detail the ethi-cal aspects of money and capital within Is-lamic finance and the relations between risk and profit as well as the social duty of the financial institutions.

The definition of ethics could be described as a set of moral values that distinguish right from wrong. There are various nega-tive effects of interest based finance such as instability, under-financing the economy,

which may lead to employ-ment losses, and not enough attention given to economic development. When consid-ering the ethical and moral principles within Islamic fi-nance and banking there is a responsibility to ensure that Shariah principles are met, such as full transparency and a focus on the Shariah board membership ensuring that the Shariah quality of finan-cial products is met.

Islamic banks cannot sepa-rate themselves from moral and ethical decisions. Their surroundings and staff, in-cluding experts, should abide by the moral and ethi-cal standards of the Islamic religion, which therefore determines the values and standards within Islamic fi-nance. Conventional banking uses the interest rate to con-duct financial actions. On the other hand Muslim scholars within Islamic banking have developed a different model of banking that does not use

Richard Williams, Finance Director, Bank of London and Middle East

Having qualified as a Chartered Accountant with KPMG in 1980, Richard’s early career in Invest-ment Banking was spent with

Chase Manhattan, Credit Agricole and Bankers Trust. He then spent 10 years at Robert Fleming & Co setting up their Global Equities Derivatives business which took

him to Tokyo and 3 years in Hong Kong with Jardine Fleming. Richard

joined BLME in January 2007 as Finance Director.

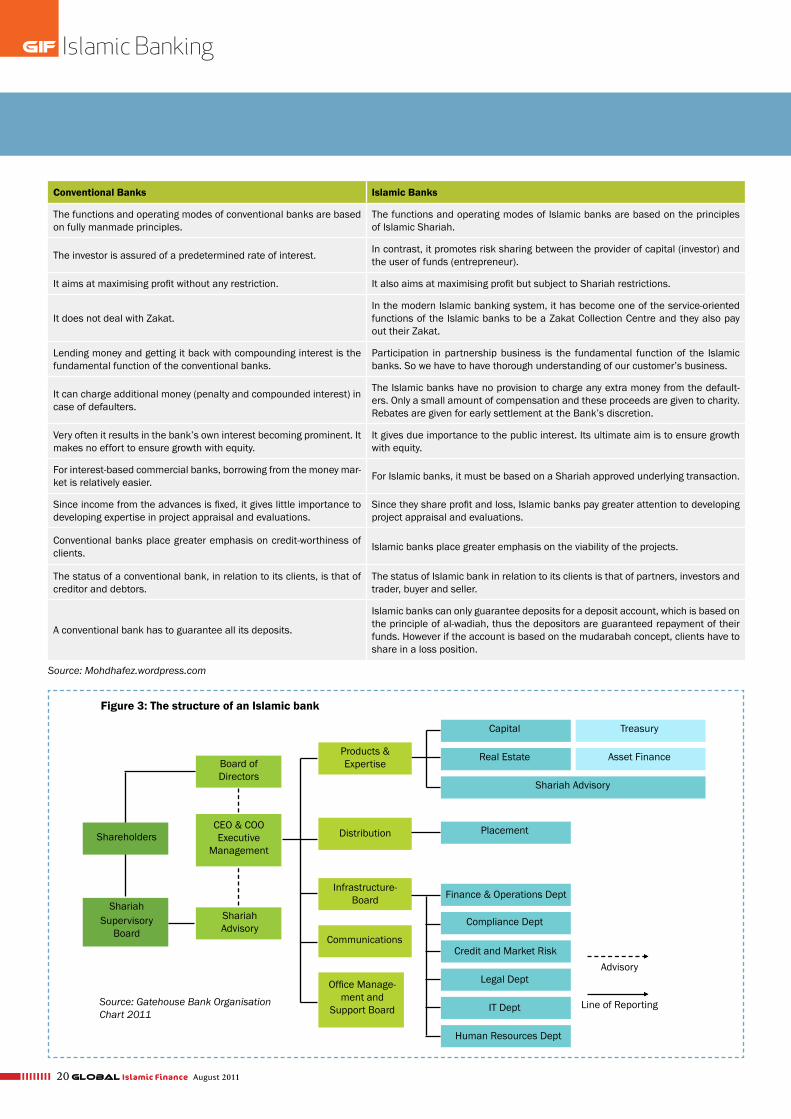

Characteristics Paradigm Version of Islamic Banking Conventional Banking

Nominal value guarantee of: Demand depositsInvestment deposits

YesNo

YesYes

Equity-based system where capital is at risk Yes No

Rate of return on deposits Uncertain, no guar-anteed

Certain and guaran-teed

Mechanism to regulate final returns on deposits

Depending on Banks performance/profits from investment

Irrespective of Banks performance/profits from investment

PLS principle is applied Yes No

Use of Islamic modes of financ-ing: PLZ and non-PLS modes Yes N/A

Use of discretion by banks with regard to collateral

Possible for reducing moral hazard in PLS modesYes in non-PLS modes

Yes always

Banks pooling of depositors funds to provide depositors with professional investment management

Yes No

Figure 1: Comparison of Islamic and conventional banking frameworks

Source: IMF working paper: Islamic Banking Issues in Prudential regulations and supervision

Islamic Banking gif

gif

16 Global Islamic Finance August 2011

interest. Islamic banks in comparison with conventional banks both have similar types of deposits. Conventional banks offer cur-rent accounts, savings accounts and fixed deposit account and Islamic banks have cur-rent and savings account. The Islamic banks also have investment accounts.

The big difference between conventional and Islamic banks is that the conventional banks pay a guaranteed interest rate on the sav-ings and fixed accounts while Islamic banks pay the depositor a profit depending on the deposit amount. Figures 1 and 2 show the comparison of conventional and Islamic banks and their banking frameworks.

The first standalone Shariah compliant retail bank in the UK authorised by the Financial Services Authority is the Islamic Bank of Britain (IBB) established in 2004. The IBB is also a member of the Financial Services Compensation Scheme. The bank aims to provide its customers with an individual and welcoming service.

Head of Retail, Imran Pasha, shares his ex-pert knowledge of how to run an Islamic bank. He is currently responsible for the bank’s distribution network, marketing func-tion and deposits. With over 10 years of experience in the financial services sector and various positions in the IBB such as Area Manager and Branch Manager, Imran Pasha talks us through the establishment of the IBB and the effect it had on the financial industry.

He says that the IBB has impacted the UK and Eu-ropean financial industry, “The bank has continued to maintain this position and still remains the only Islamic retail bank in the UK and Europe. It is con-sidered a pioneer of retail Islamic banking and cur-rently offers the largest range of Shariah-compliant retail financial products to the UK consumer.” Almost seven years on and IBB has grown at a steady rate and carved itself a niche in the UK retail banking sector.

The bank, based on its Shariah principles, is often viewed as an ethical and stable al-ternative to conventional banks. Certainly, its achievements are well recognised both in the UK and internationally. As a result it has earned a well deserved reputation as the UK leader in British Islamic banking. The strate-gies behind the success of Islamic banking.

There are a range of strategies to consider when running an Islamic bank, such as risk positioning and the financial fundamentals. The purpose of having a strategy is to help the banks improve and establish a strong place in a selection of markets rather than a place in a range of competitive markets. Is-lamic banks have ways to manage commer-cial risk, such as profit equalisation, invest-ment risk reserves, Mudarib fees and share holders. In addition, Islamic banks pay more attention to assets and liabilities compared to their conventional counterparts.

Islamic banks have problems in manag-ing liquidity and risk because of the limited amount of financial instruments on offer. Islamic products are not as commoditised and tend to need more altering and at-

tention, which can result in operation risk. The latest in-strument to complement the operating systems of Islamic transactions internationally is the wakalah structure. The exclusion of limitations within the Islamic finance industry should encourage the devel-opment and growth of the industry. The rapidly growing Islamic finance industry is al-ready worth an estimated one trillion US dollars globally.

Liquidity management struc-ture can be challenging for Islamic banks because of the lack of liquid instruments within Islamic finance. After attaining extra revenue the GCC Islamic banks kept a large amount of core liquid-ity in the form of short-term Murabaha and deposits from central banks. The result of these actions proved that it was the right choice for that particular area, which is known for numerous cycles and recurring shocks.

Imran Pasha, Head of Retail, Is-lamic Bank of Britain

Having over 10 year’s experience within the financial services sector, Imran held management positions with Merrill Lynch and HSBC. At IBB

Imran has held various positions progressing from Branch Manager

to Area Manager. He currently holds the position of Head of Retail. In

this role Imran holds responsibility for Bank’s the distribution net-

work, the marketing function and deposits.

The first steps to establishing an Islamic bank – Establishment of the IBB

Imran Pasha, Head of Retail at the Islamic Bank of Britain talks us through the steps:

Licensing. Establishing a bank is a long and painstaking task consisting of several elements. The first is regulatory and financial. IBB therefore came into existence in August 2004 when the UK government’s regulatory body, the Financial Services Authority (FSA), granted the bank its license. In September 2004 IBB became a UK publicly listed company on the Alternative Investment Market (AIM).

Retail financial services. Once the capital was raised by investors in the UK and the Middle East, the bank set about implementing the vision of offering Shariah complaint retail financial services. This included designing and setting up the infra-structure, processes and products as well as bringing together the team.

Branch network. This was followed by the setting up of a branch network. IBB now has a national branch network in key locations including London, the Midlands and North West.

Smart banking facilities. To complement this, and to enable Shariah compliant banking to be accessible to consumers across the UK, IBB also developed its Smart banking facilities. These allow customers to carry out their banking over the internet or telephone by liaising with one of the bank’s customer services representatives.

Marketing and awareness. Marketing and community relations have also played an important role in the bank’s activities. In order to establish a presence IBB has played a strong role in the British Muslim community, providing services to local mosques and charities. It has also undertaken extensive marketing, advertising and PR activities to ensure its target audience are aware of the bank and its prod-ucts and services.

Product development. Finally, the bank has undertaken extensive product devel-opment so that its customers can genuinely manage their finance according to the principles of their faith, i.e. without the use of interest. As a result of its ongoing work, the bank now offers the largest range of Shariah compliant retail financial products and services in the UK.

Islamic Banking

TOP ISLAMIC FINANCE INSTITUTION

RANKING?

WILL YOUR INSTITUTION BE IN

2011

Global Islamic Finance Awards of the Decade »Top 300 Islamic Finance Institutions across the Globe »

Top 50 Most Influential People in Islamic Finance »50 Best Companies to Work for in Islamic Finance Industry »

Global Islamic Finance Awards & Rankings Now Open For Submissions

These prestigious rankings provide a comprehensive outlook into the Global Islamic finan-cial industry and are the first of their kind. GIF is working hard to ensure that both individu-als and institutions are included in the list of high ranking categories. If you are interested in

taking part please register your interest at the earliest opportunity.

We are only able to include Institutions for which we have updated results in each category, so ensure that your Institution will provide us with updated data.

No financial payment is made as the cost of the research is funded by Global Islamic Finance magazine, with no third party financial sponsorship or support.

www.globalislamicfinancerankings.com

Deadline Extended Until 1st of September

gif

18 Global Islamic Finance August 2011

Warren Edwardes, CEO, Del-phi Risk Management, United Kingdom

Islamic products require more tailor-ing which could create operational risk. In what way can Islamic banks reduce the operational risk?

Shariah risk and reputational risk are prime sources of operational risk for Islamic banks.

The Holy Qur’an states: [3:130] ‘O you who have believed, do not consume usury, doubled and multiplied …’ [2:275] ‘Allah hath per-mitted trade and forbidden interest.’

Hadith I in al-Nawawi’s Forty Hadith, states that ‘actions are accord-ing to intent’ or ‘actions are what they are by virtue of intent’. Niyyah is intention: an inner act of the heart whereby one performs an outer act as the fulfilment of a particular duty, rather than merely a series of motions without religious value. The point of Shariah finance is to fulfil religious compliance and not just to appear to do so.

An issue for Islamic banks is the tendency to replicate conventional products with an Islamic veneer rather than create Islamic products based on Islamic principles of profit and loss sharing and genuine, rather than fabricated, trade transactions.

Cleverly engineered products, perhaps not fully explained to Shariah scholars, may initially be deemed Shariah compliant. However, when the undisclosed side trades affected by the SPVs become apparent, the products are uncovered as repackaged conventional products thus damaging the reputation of the Islamic bank.

Niyya, the intention which underlies all transactions, is the respon-sibility of the end-user investor or finance-seeker. It is important to have full transparency and disclosure about all of the transactions making up the structured product, so that stakeholders can evaluate the true intention behind it and see if it is compliant with their own Niyya, which may be genuine Shariah compliance or just the appear-ance of Shariah compliance. It is for the Muslim end-user to enter into contracts, directly or via financial institutions, with which he is happy to be judged on the day of judgement and not just on earth. For that transparency is key.

Products may be structured as a package of trades, which are indi-vidually Hallal, while the Niyya of the package as a whole is to repli-cate Riba, which is Haram. Each person involved must ask himself what his own Niyya is. If the transactions involve trades in certain markets, do the investors really understand these markets or are they entering into a synthetic Riba transaction that does not depend on the performance of these markets?

Transparency will help to mitigate operational risk represented by Shariah and reputational risk.

The risks within banking strategiesA selection of people in Islamic banking, such as regulators, share-holders, customers and company employees and management, determine its business strategy and performance All these people affect the financial strength of Islamic banks, but regulators in par-ticular have an affect on the bank’s strategy and ratings through their influence on the regulatory environment and overall support. The main aims of the bank regulator are to ensure that the deposi-tors are protected and to spread awareness of a strong banking sys-tem.

Shariah compliant products and investments are very important within Islamic Banking and may determine the bank’s reputation. If an investment did not follow Shariah principles it would have nega-tive consequences on the bank and create a risk of dissolution of the investment entity. It is vital that all investments are checked by the bank and by a Shariah authority or regulator. The product structure, contracts, asset securities and other aspects should be assessed before deciding whether the product or project is Shariah compli-ant.

After the approval of the Shariah board the product or project can be released on to the financial market. If the legitimacy is uncertain then the issue should be taken on by a Shariah auditor or supervisor, who can quickly deal with and solve any problems.

The purpose of most of Islamic banking strategies is to achieve prof-itable asset growth. Certain factors can affect the use of strategies, such as the progression of Islamic banking and finance, the position of the banks in their home markets, the resources available and me-dium and long term goals.

Improving risk position is another aspect that is part of Islamic bank-ing strategy, although Islamic banks are able to overcome negative shocks to the assets aspect of the investment depositors. Commer-cial risk is also something to be considered and, according to CPI Financial, Islamic banks have put in place buffers against loss in order to manage commercial risk. These are:

Profit equalisation (consistent earning across the cycle)• Investment risk reserves (attract negative shocks on asset • value)Mudarib fees (can decrease in order to avoid having a negative • affect on the depositing Rab al Maal)Shareholders (always supplying Qardh Hasan to profit-sharing • depositors)

The Finance Director at the Bank of London and the Middle East, Richard Williams gives his views on Islamic banks in the financial crisis. “When the credit crisis hit in 2008 many commentators and industry leaders appeared to believe that Islamic banks were ‘im-mune’ from the financial crisis. Now, however, we can see that some Islamic banks were exposed due to over-zealous expansion and ex-cessive risk concentrations, particularly in the property sector.” He continues “One of BLME’s priorities has been to offer a diversified range of products and services, ranging from asset management to trade finance and leasing.”

The legal and regulatory changes in Islamic finance and banking An important aspect of Islamic banking regulations is the ‘mainte-nance of a level playing field between banking institutions’, this re-

Islamic Banking

gif

2011 August Global Islamic Finance 19

sults in the regulators within Islamic finance applying the same prin-ciples of handling risks to all banks. Regulators apply the national supervisory principles to all banks, no matter what services they offer, Islamic or conventional. However the generic principles may not apply to every Islamic banking framework and the regulatory requirements should be tailored to cater to any relevant characteristics when run-ning an Islamic bank.

The Islamic financial industry is challenged by the development of consistent regulatory standards that apply to the specific features of Islamic banking. It is necessary for the regulatory standard to apply within the industry and to meet the requirements of the basic regula-tory standards worldwide. Capital adequacy is a very important part of assessing whether a bank will succeed or fail. It is an important as-pect when looking at a bank’s risk exposure and may reveal a bank’s risk relationships.

The Basel III system is the most recent of global regulatory standards which has developed from the previous Basel I and Basel II agree-ments. The Basel committee agree on the Basel II standards for banks’ capital adequacy and liquidity. The goal of the Basel III system is to strengthen bank capital requirements and encourage new poli-cies on bank leverage and liquidity.

Imran Pasha explores the legal and regulatory changes to ensure the aims of Islamic banks are met. He says that within the UK the govern-ment and the Financial Services Authority (FSA) have worked with and encouraged those aiming to establish Islamic financial institu-tions. The overall goal is to make the UK the capital Islamic financial hub in Europe. Imran Pasha says “To illustrate, the UK was the first member of the EU to authorise Islamic banks. The government also introduced changes so that Islamic mortgages would not be subject to double taxation. There have been at least five Financial Acts since 2003, where legislative changes have been introduced to put Islamic finance on a level playing field with conventional finance.” He adds that there have also been numerous changes made by the HMRC and the FSA covering the aspects of profits, taxation and regulation of Home Purchase Plans.

He refers to the CityUK Islamic Finance 2011 report and gives ex-amples of the UK within Islamic finance. “There are 22 banks in the UK offering Islamic products. This figure exceeds that of any other western country. There were five Sukuk listings at the London Stock Exchange (LSE) in 2010 and one in early 2011. This brings the aggre-gate total at the LSE to 31 listings worth US$19 billion. Islamic funds in the UK have combined assets of US$300 million.”

The Bank of London and the Middle East (BLME) is an independent wholesale Shariah compliant bank based in London and provides Is-lamic investment and products to businesses and individuals. The financial director, Richard Williams, discusses the changes in regula-tion and how it affects Islamic banks. Joining the BLME in 2007 the financial director spent his early career working in investment bank-ing.

He spent the next ten years at Robert Fleming & Co setting up the global equities derivatives business and travelled to Tokyo and Hong Kong. Richard also has experience with start up companies and in the areas of private equity with legal and general ventures. He shares his views saying “Basel III was introduced over the coming years with full accord, scheduled to be fully implemented by 2019.” Richard Wil-

Shah Fahad Yousufzai, Vice President, Products Develop-ment Department, Islamic bank of Thailand

How are values and regulations tai-lored to apply to Islamic finance and banking?

Any muamilat (financial transaction) without Akhlaq (ethics) is considered irregular and inappropriate.

Muamilat (financial transaction) and Akhlaq (ethics) work side by side within Islamic finance. Business transactions under the um-brella of Shariah must be according to the ethos of Islam. One can ask what the logic is behind not earning funds through interest. Is-lam prohibits it because it greatly restricts the physical activity and circulation of capital. As Islamic business transactions are based on real trade such as Murabaha sales, Musharakah venture capital and Istisna for construction purposes etc.

Islam is against the concentration of wealth in the hands of one individual and also encourages the distribution of wealth from rich to poor, as in the Zakath and Ushar system.

Islamic prohibits unlawful practices within Islamic finance and pro-hibits activities that could harm society, such as uncertainty and gambling.

The role of the Shariah supervisory board and Shariah audit and compliance team is crucial. One sees many examples of the Mu-rabaha role in developed Islamic banking market economies. All concerned authorities, for example Shariah compliance and audit teams and finance assigning executives, are responsible together with Shariah advisors for supervising financial practices. Each IFI needs a team of experts to eradicate non-Shariah compliant trans-actions and strictly monitor each and every transaction.

The main objective of Islamic banks is to carry out precise and ac-curate transactions according to Shariah principles. The executives of IFIs all over the world always associate profitability with their suc-cess, but profit is a secondary aspect of Islamic finance; the primary aspect is Shariah compliancy while practicing any mode of Islamic finance.

My suggestion to all central banks of countries practising Islamic banking is that a Shariah advisor should be an employee of the cen-tral bank and not of the commercial banks involved in practising Islamic banking. Islamic banks must add spiritual satisfaction to the job description, since it is an essential professional and social re-sponsibility. It would be helpful for true Islamic banking to function according to the real Islamic spirit.

Islamic Banking

gif

20 Global Islamic Finance August 2011

Conventional Banks Islamic Banks

The functions and operating modes of conventional banks are based on fully manmade principles.

The functions and operating modes of Islamic banks are based on the principles of Islamic Shariah.

The investor is assured of a predetermined rate of interest. In contrast, it promotes risk sharing between the provider of capital (investor) and the user of funds (entrepreneur).

It aims at maximising profit without any restriction. It also aims at maximising profit but subject to Shariah restrictions.

It does not deal with Zakat.In the modern Islamic banking system, it has become one of the service-oriented functions of the Islamic banks to be a Zakat Collection Centre and they also pay out their Zakat.

Lending money and getting it back with compounding interest is the fundamental function of the conventional banks.

Participation in partnership business is the fundamental function of the Islamic banks. So we have to have thorough understanding of our customer’s business.

It can charge additional money (penalty and compounded interest) in case of defaulters.

The Islamic banks have no provision to charge any extra money from the default-ers. Only a small amount of compensation and these proceeds are given to charity. Rebates are given for early settlement at the Bank’s discretion.

Very often it results in the bank’s own interest becoming prominent. It makes no effort to ensure growth with equity.

It gives due importance to the public interest. Its ultimate aim is to ensure growth with equity.

For interest-based commercial banks, borrowing from the money mar-ket is relatively easier. For Islamic banks, it must be based on a Shariah approved underlying transaction.

Since income from the advances is fixed, it gives little importance to developing expertise in project appraisal and evaluations.

Since they share profit and loss, Islamic banks pay greater attention to developing project appraisal and evaluations.

Conventional banks place greater emphasis on credit-worthiness of clients. Islamic banks place greater emphasis on the viability of the projects.

The status of a conventional bank, in relation to its clients, is that of creditor and debtors.

The status of Islamic bank in relation to its clients is that of partners, investors and trader, buyer and seller.

A conventional bank has to guarantee all its deposits.

Islamic banks can only guarantee deposits for a deposit account, which is based on the principle of al-wadiah, thus the depositors are guaranteed repayment of their funds. However if the account is based on the mudarabah concept, clients have to share in a loss position.

Figure 2: Comparison of conventional and Islamic banks

Shareholders

Source: Gatehouse Bank Organisation Chart 2011

Figure 3: The structure of an Islamic bank

Board of Directors

CEO & COO Executive

Management

Shariah Supervisory

Board

Distribution

Infrastructure-Board

Products & Expertise

Communications

Office Manage-ment and

Support Board

Capital

Real Estate

Shariah Advisory

Treasury

Asset Finance

Placement

Finance & Operations Dept

Compliance Dept

Credit and Market Risk

Legal Dept

IT Dept

Shariah Advisory

Human Resources Dept

Line of Reporting

Advisory

Islamic Banking

Source: Mohdhafez.wordpress.com

gif

2011 August Global Islamic Finance 21

Dr Osama Alsulaiman, Legal Consultant in Islamic finance, Saudi Arabia

How are values and regulations tailored to apply to Islamic finance and bank-ing?

It is of the utmost importance for the prop-er functioning of Islamic finance (IF) that there is an appropriate legal framework to accommodate its applications. Traditional

finance has enabled legislation, contract enforcement measures and effective settlement dispute mechanisms. In addition to that IF re-quires a framework which takes into consideration its own distinctive characteristics. This necessitates the establishment of a competent legal framework to achieve the following:

Enabling legislation for the creation and authorisation of financial 1. instruments, establishing Shariah governance, and addressing conflicts between common or civil law and Shariah principles. Ensuring that contracts can be enforced by assuring that the le-2. gal documentation of any transactions or instruments complies with both Shariah and local law. Forming an appropriate mechanism for dispute settlement.3.

These legal considerations are crucial not only for proper implemen-tation but also to maintain the growth of the industry. After examin-ing the second and third points above, it can be seen that in practice contracts should comply simultaneously with two sets of laws: Islamic law and secular law. Compliance in this situation can be looked at in the same way as compliance between the laws of two or more jurisdic-tions when structuring any cross-border transactions. However IF, as part of the corpus of Islamic law, does not pertain to any particular country, territory or sovereign legal system. This raises concerns about the extent to which the norms and principles of IF are recognised by western countries. For example, in some cases the UK courts have ignored the reference to Shariah as a governing law; for instance in the case of Shamil Bank of Bahrain EC v Beximco Pharmaceuticals Ltd and others.