2011 Northern California Commercial Real Estate Overvie Cassidy Turley Northern... · 2011 Northern...

56

An annual report on Commercial Real Estate in Alameda, Contra Costa, El Dorado, Marin, Monterey, Napa, Placer, Sacramento, San Francisco, San Mateo, Santa Clara, Santa Cruz, Solano, Sonoma, and Yolo Counties. 2011 Northern California Commercial Real Estate Overview

Transcript of 2011 Northern California Commercial Real Estate Overvie Cassidy Turley Northern... · 2011 Northern...

An annual report on Commercial Real Estate

in Alameda, Contra Costa, El Dorado, Marin,

Monterey, Napa, Placer, Sacramento,

San Francisco, San Mateo, Santa Clara,

Santa Cruz, Solano, Sonoma, and Yolo Counties.

2011 Northern CaliforniaCommercial Real Estate Overview

www.ctbt.com

We are Cassidy Turley.

CAPITAL MARKETS

CORPORATE SERVICES

PROJECT & DEVELOPMENT SERVICES

PROJECT LEASING

PROPERTY MANAGEMENT

TENANT REPRESENTATION

INT

RO

DU

CT

ION

INTRODUCTION

The 2011 Northern California Commercial Real Estate Overview

is an annual review of the major markets covered by each of

Cassidy Turley’s 15 regional offi ces.

This guide offers summaries and specifi c local submarket

information that are easily located and quickly understood.

This overview represents only a fraction of our research

capabilities. Each of Cassidy Turley’s regional offi ces provides

quarterly reports and custom building-by-building analysis as a

service to our customers.

Our Insight. Your Advantage.

2011 Northern CaliforniaCommercial Real Estate Overview

TA

BL

E O

F C

ON

TE

NT

S

TABLE OF CONTENTS

Introduction 6

Corporate Overview 8

Offi ce Overview 10

R&D Overview 12

Warehouse Overview 14

Shopping Center Overview 16

Multi-Family Overview 22

Investment Overview 24

San Francisco County Overview 26

Santa Clara County Overview 28

San Mateo County Overview 30

I-80/880 Corridor Overview 32

North I-680 Corridor Overview 34

Tri-Valley Overview 36

Sacramento Valley Overview 38

Marin County Overview 40

Sonoma County Overview 42

Napa County / Solano County Overviews 44

Santa Cruz County Overview 46

Monterey County Overview 48

Addendum - City by City Data 50

Credits & Terms 54

For a digital ebook version of this book, go to www.ctbt.com/Overview2011

6 CASSIDY TURLEY

CE

O L

ET

TE

R CEO LETTER

There is no doubt that 2010 was a rollercoaster year for commercial real estate in Northern California. We entered the year in the depths of the worst economic downturn since the Great Depression. Vacancy levels for all property types were up across the board. Rents had dropped substantially for nearly every commercial real estate property type. Commercial delinquencies and foreclosures were reaching record levels and the overall mood was one of gloom.

2010 began against this dour backdrop. Unemployment in California was well above the 12% mark and above the 10% mark in most Bay Area cities. Once again we heard the economists speaking of “jobless recoveries” and commercial real estate being the “last shoe to drop.” Commercial real estate always is a lagging indicator of the economy, so it makes sense that we are the last to feel the impacts of a downturn and the last to recover. And so many questioned whether our local markets would even hit bottom in 2010.

But after a weak start, the local commercial real estate market found footing in 2010. Led by a resurgent tech sector, offi ce product along the Highway 101 Corridor from Mountain View to Market Street began to post the largest occupancy growth numbers we have seen in years. Prime retail space was suddenly in high demand again as a wave of discounters, grocery store chains, off-price retailers and a new crop of quick service and fast casual restaurant concepts sought to take advantage of once-in-a-generation rental rates. Most of the region’s industrial markets showed signs of stabilization. Last, but not least, what had been a stagnant investment market in 2009, came back to life by year-end with trophy offi ce properties in San Francisco’s urban core leading the charge.

Perhaps most importantly, against all of the challenges of the past year, we closed 2010 with not just resurgent activity, but resurgent optimism. We still have a long way to go on the road to recovering from the “Great Recession.” Though plenty of challenges remain, the overriding sense is that the worst is now behind us.

WE ARE CASSIDY TURLEYJust as 2010 was a year in which the Bay Area commercial real estate markets showed remarkable resilience and growth during challenging times, the same holds true of our company. In 2010, BT Commer-cial joined forces with other leading private commercial real estate fi rms to form Cassidy Turley, immediately the largest privately held commercial real estate services fi rm in the nation. We are a national team of dedicated professionals with over 100 years of successful client relationships. We have over 3,000 professionals in 60 offi ces nationwide and completed transactions valued over $17 billion in 2010. We manage over 430 million square feet on behalf of private, institutional and corporate clients and support over 25,700 domestic corporate services locations. Cassidy Turley serves owners, investors and occupiers with a full spectrum of integrated commercial real estate services—including capital markets, corporate services, project leasing, property management, project and development services, and tenant representation. We were recently ranked in the Top 10 on the Lipsey Company’s Commercial Real Estate Top Brands Survey, and were ranked #1 by Real Estate Alert for Offi ce Sales in three of the top six U.S. markets.

As part of this continued effort to improve our capabilities, I am also very pleased to share that in 2010 Cassidy Turley BT Commercial and CPS CORFAC International reached an agreement to merge ownership. In doing so, we became the #1 commercial real estate brokerage fi rm in the Silicon Valley in terms of agent count according to the San Jose/Silicon Valley Business Journal. We also hold the #1 commercial brokerage fi rm ranking in both the San Francisco and Peninsula markets. Our market presence now includes over 400 professionals and staff in 15 offi ces locally and recorded over $3.1 billion in transactions in 2010.

Also in 2010, Cassidy Turley reached an agreement to form a partner-ship with London-based GVA Grimley, one of the U.K.’s leading fi rms and the controlling fi rm in GVA Worldwide in order to improve our delivery of services internationally. Indeed, 2010 was a year in which there are a lot of exciting changes happening within our fi rm.

Our fi rm also continues to grow within the United States. In 2010, three former Colliers affi liates, Houston in New Jersey, Moore in Louisville and Barry in Milwaukee as well as a former NAI affi liate, Fuller, in Denver also merged in to Cassidy Turley. And, in January, we expanded to the Dallas and Houston markets with our merger with Capstar Commercial Real Estate Services.

There will be more growth in 2011 and more changes that will continue to enhance the resources and services we provide to you. We are eager to continue working with you and to expand our relationship across our expanded business lines and geography. Though our name may have changed last year, we have not changed our commitment to our market leading research products. In fact, we will continue to improve in this effort, because we know that information is vital to your decision making process. Our research and knowledge are the core capability that allows Cassidy Turley BT Commercial to produce over 50 different quarterly market reports — the most of any commercial real estate services fi rm in Northern California. Our commitment to research is our commitment to you; our clients, so that you may have a better understanding of our markets’ past, present and projected future.

THE MARKETSo, what is driving this new sense of optimism in the Bay Area?

It is new technology, driven by social media, wireless, hand held devices and cloud computing. We lead in the percentage of our workforce that is in high tech with Silicon Valley double that of the next market which happens to be San Francisco and even as we evolve from legacy tech to the new tech, the percentage of our workforce dedicated to this sector will increase. Of the ten largest social networking sites, six are headquartered in the Bay Area, but more impressively, they account for 85% of the monthly unique visitors to the top 10 sites. Of the fi ve largest U.S. Search Engines, three are headquartered in the Bay Area and more impressively they account for 88% of all unique searches in the US. The fact is that the resurgence of the Bay Area economy has been driven by these fi rms and our region’s outsized role in the development of the next generation of technology.

So how did each of the product types perform in 2010?

OFFICEBay Area offi ce vacancy ended 2010 at 16.6%, down from 17.4% in 2009. We track 59 separate offi ce submarkets in the Bay Area. Of those 59 markets, 33 showed positive net absorption and 26 were negative for the year. The one consistent factor was that markets with strong tech clusters were the winners. On the whole, what we have seen is that the Highway 101 Corridor from Mountain View in Silicon Valley to Market Street in San Francisco is where the growth has been concentrated.

Asking rents for offi ce space stabilized over the course of the past twelve months. The current average asking rent in the Bay region is $2.44 per square foot (on a monthly full service basis). This number has not budged since the fi rst quarter of 2010. That being said, we are already seeing rental rate growth in the region’s strongest offi ce submarkets, while stabilization is taking place in most of the weaker trade areas.

All told, the market absorbed over 2.6 million square feet of space in 2010—nearly all of it in the fi nal half of the year. What is more telling is the fact that this represents a swing of over 9.1 million square feet compared to 2009 when the market hemorrhaged over 6.5 million square feet of occupancy.

To Our Valued Clients,

2011 NORTHERN CALIFORNIA COMMERCIAL REAL ESTATE OVERVIEW 7

CE

O L

ET

TE

R

Clearly, we are a boom and bust market. This should not come as a surprise considering that we are a tech market. But we think that it is interesting to note that in comparison to the dot bomb implosion of 2001, this economic downturn has actually been much milder locally. All told, the region lost a total of roughly 27 million square feet of occupancy during the “Great Recession.” In the tech wreck of 2001/2002, the market lost 65 million square feet. That net absorption has turned positive once more tells us that, so long as the ongoing fragile economic recovery is not derailed, that the San Francisco Bay region offi ce market is beginning to enter its next boom phase.

We are currently tracking active tenant space requirements of over 5.2 million square feet, 45% of which is in our traditional services industries. Some of these will end up as renewals or consolidations rather than growth. But even with that caveat, we believe that both the San Francisco and Silicon Valley offi ce markets will record occupancy growth in the range of two million square feet in 2011. The San Mateo County offi ce market could record one million square feet of occupancy growth in the coming year. The real challenge will be for East and North Bay markets which typically have not had as strong a tech presence. But, improving economic fundamentals should also see most of these trade areas stabilizing over the fi rst half of the year and posting modest improvement by late 2011.

R&D2010 was a year of stabilization for R&D space in the Bay Area. Today’s vacancy rate of 18.1% is the same as it was exactly one year ago. Two years ago this number stood at 15.5%. Though total occupancy growth was slightly negative—to the tune of roughly 66,000 square feet, the good news is that the market has fi nally found its fl oor. Average asking rents for R&D space in the Bay Area also stabilized in 2010. They declined slightly from $1.11 per square foot (on a monthly triple net basis) to $1.10 over the past year. They had peaked in 2007 at $1.36 per square foot.

We are tracking 7.8 million square feet of R&D and offi ce require-ments in the Silicon Valley and 101 Corridor markets alone. Leasing activity and touring were picking up as 2010 came to a close. These trends are escalating in 2011. If 2010 was a year of stabilization, 2011 will be a year of recovery. Net absorption will trend positive throughout the year, with momentum building heading into the fi nal half of 2011. Our worst case scenario is that the market absorbs 1.5 million square feet of space this year. Our likely case forecast is for two million square feet of occupancy growth. An unexpectedly robust economic turnaround could mean as much as 2.5 million square feet of expansion.

WAREHOUSEVacancy for warehouse space in the Bay Area also stabilized in 2010. Today’s vacancy rate of 9.4% is the same as it was exactly one year ago. Two years ago this number stood at 6.6%. Total occupancy growth was just over 5,000 square feet—or virtually zero.

There are two factors that hammered the previously rock solid warehouse market over the past few years. First, the global supply chain has become much more effi cient; and, second, warehousing has largely become a month to month business with third party logistics fi rms tying their lease commitments to the terms of their contracts with their clients. The good news is that as consumers begin to spend more—as they have been doing since last year’s stellar holiday shop-ping season—warehouse vacancies will begin to fall rapidly. 2011 will be a year of modest recovery. Net absorption will continue to trend positive throughout the year, with momentum building heading into the fi nal half of the year.

MANUFACTURINGVacancy for manufacturing space in the Bay Area climbed from 6.8% to 7.4% over the course of 2010. Manufacturing space has been negatively impacted by both off-shoring and technology. The global supply chain has become so effi cient and information-centric that when consumers stop buying, factories stop producing literally overnight. These trends have translated into the region losing over 3.7 million square feet of occupancy since 2008. The Bay Area manufacturing market lost 924,000 square feet of occupancy in 2010, but net absorption should turn minimally positive in 2011. Increased consumer spending will also spur manufacturing demand, though these trends likely won’t translate into occupancy growth until late in the year.

RETAILThe San Francisco Bay Area shopping center market closed 2010 with an overall vacancy rate of 6.8%. One year ago this number stood at 7.6%. The Bay Area continues to rank in the top fi ve U.S. markets in terms or retail activity. Throughout the past year, discounters, off-price apparel chains, new grocery players (discount, organic and ethnic-themed) scoured the market for deals on superior space that had been vacated in the last wave of bankruptcies. Meanwhile, restaurant chains continue to drive the market for smaller space. Retailers will continue to boost expansion plans throughout the Bay Area—a trend that will mean further declines in vacancy. Right now the big problem is that the region is running low on fi rst-tier space to accommodate the growth plans of top chains. Look for fi rst and second-tier shopping centers to continue to record occupancy growth in 2011 and for rental rate growth to be strong.

INVESTMENTThe Bay Area investment market showed improvement in both overall activity and valuation metrics in 2010. Total sale volume tallied $7.8 billion in 2010 for offi ce, industrial, retail and multi-family transac-tions. This was a dramatic, 122% improvement from a year ago when the total volume registered $3.5 billion. And activity will only increase further in 2011. Last year investors were focused on core urban offi ce and trophy shopping center assets. In many cases properties traded at cap rates in the 5% to 6% range. This year investors will increasingly look to other property types, secondary and tertiary markets and will increasingly be willing to explore partially stabilized properties in light of improving economic fundamentals.

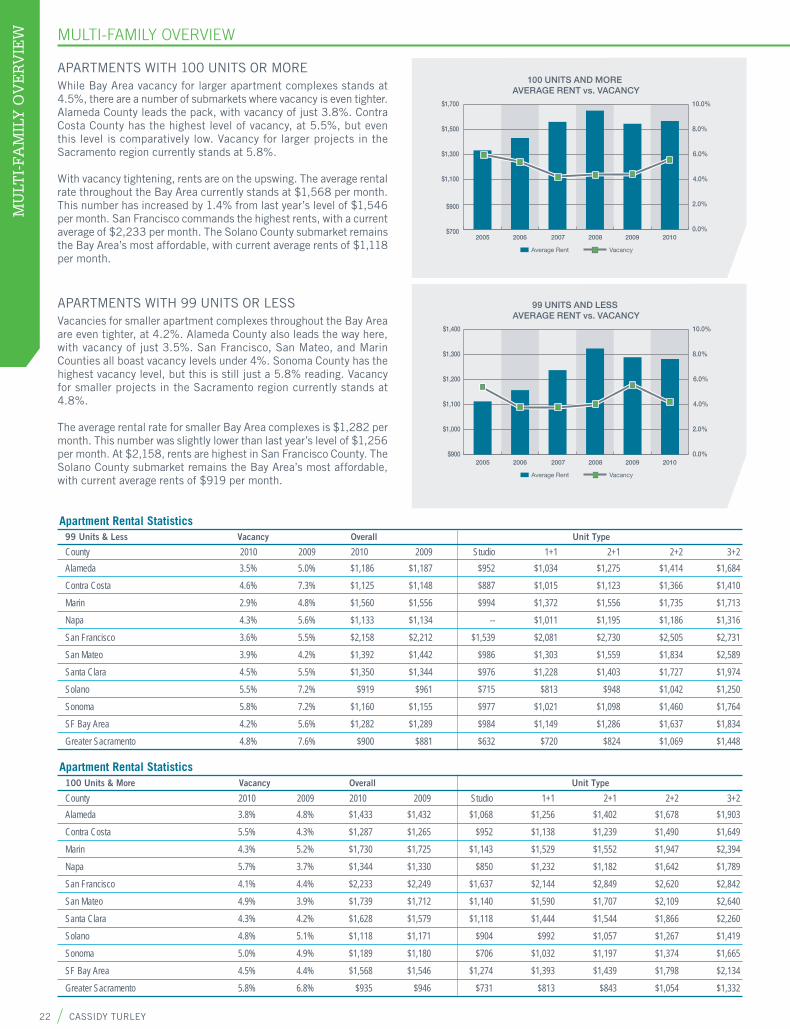

MULTI-FAMILYLastly, our multi-family sector remained tight throughout the downturn and currently has a market-wide vacancy rate of 4.6%. As the economy heats up and households begin to “unbundle” we should see very strong upward movement in multifamily rents.

There is a new sense of optimism in the marketplace. It is one that is tempered by rationality and grounded in reality, as opposed to stoked by irrational exuberance. There is no doubt that we are still in the midst of a very fragile recovery and that many challenges lay ahead. Even as our hearts and prayers go out to the victims of the recent terrible tragedy in Japan, we still do not know what the full impact of this catastrophe will be. Likewise, rising fuel prices could threaten one of the current engines driving recovery—the resurgent U.S. consumer. There will still be challenges in the months to come, but better times are fi nally here. The worst of the “Great Recession” is, at last, behind us.

Thank you,

Mike KammCEOCassidy Turley BT Commercial

8 CASSIDY TURLEY

CO

RP

OR

AT

E O

VE

RV

IEW CORPORATE OVERVIEW

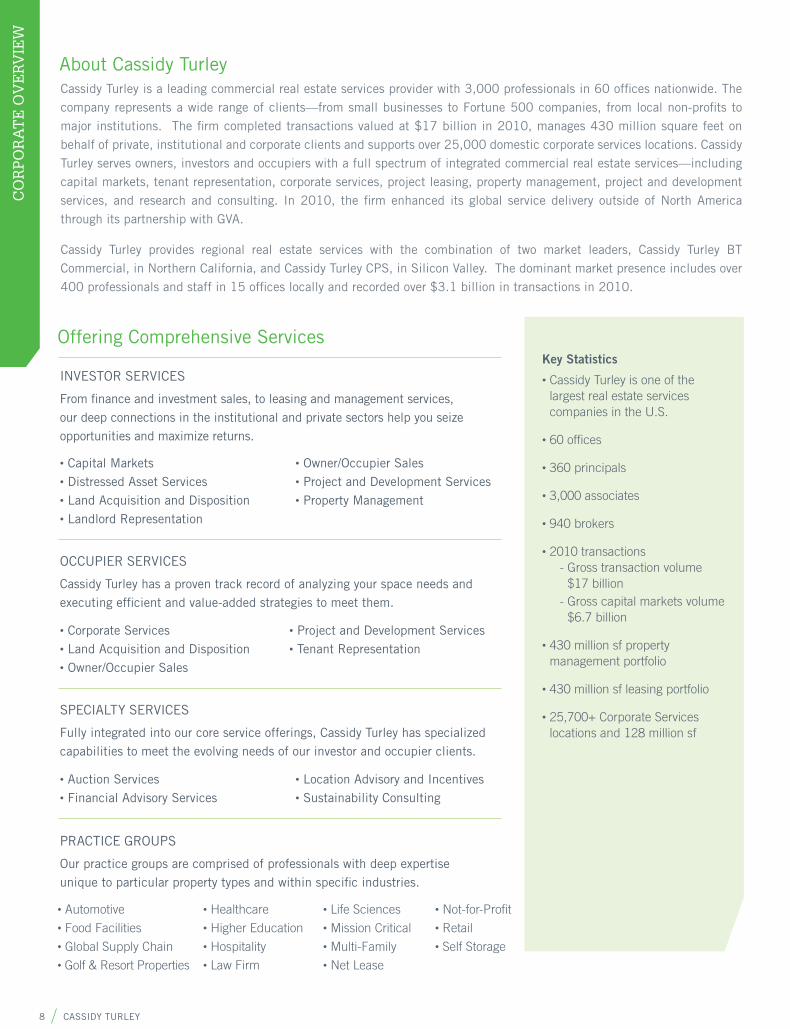

About Cassidy TurleyCassidy Turley is a leading commercial real estate services provider with 3,000 professionals in 60 offi ces nationwide. The company represents a wide range of clients—from small businesses to Fortune 500 companies, from local non-profi ts to major institutions. The fi rm completed transactions valued at $17 billion in 2010, manages 430 million square feet on behalf of private, institutional and corporate clients and supports over 25,000 domestic corporate services locations. Cassidy Turley serves owners, investors and occupiers with a full spectrum of integrated commercial real estate services—including capital markets, tenant representation, corporate services, project leasing, property management, project and development services, and research and consulting. In 2010, the fi rm enhanced its global service delivery outside of North America through its partnership with GVA.

Cassidy Turley provides regional real estate services with the combination of two market leaders, Cassidy Turley BT Commercial, in Northern California, and Cassidy Turley CPS, in Silicon Valley. The dominant market presence includes over 400 professionals and staff in 15 offi ces locally and recorded over $3.1 billion in transactions in 2010.

Offering Comprehensive Services

• Capital Markets• Distressed Asset Services • Land Acquisition and Disposition• Landlord Representation

• Owner/Occupier Sales• Project and Development Services• Property Management

PRACTICE GROUPS

Our practice groups are comprised of professionals with deep expertise unique to particular property types and within specifi c industries.

INVESTOR SERVICES

From fi nance and investment sales, to leasing and management services, our deep connections in the institutional and private sectors help you seize opportunities and maximize returns.

OCCUPIER SERVICES

Cassidy Turley has a proven track record of analyzing your space needs and executing effi cient and value-added strategies to meet them.

• Auction Services• Financial Advisory Services

• Location Advisory and Incentives• Sustainability Consulting

SPECIALTY SERVICES

Fully integrated into our core service offerings, Cassidy Turley has specialized capabilities to meet the evolving needs of our investor and occupier clients.

• Corporate Services• Land Acquisition and Disposition• Owner/Occupier Sales

• Project and Development Services• Tenant Representation

Key Statistics

• Cassidy Turley is one of the largest real estate services companies in the U.S.

• 60 offi ces

• 360 principals

• 3,000 associates

• 940 brokers

• 2010 transactions - Gross transaction volume

$17 billion - Gross capital markets volume

$6.7 billion

• 430 million sf property management portfolio

• 430 million sf leasing portfolio

• 25,700+ Corporate Services locations and 128 million sf

• Automotive• Food Facilities• Global Supply Chain• Golf & Resort Properties

• Healthcare• Higher Education• Hospitality• Law Firm

• Life Sciences• Mission Critical• Multi-Family• Net Lease

• Not-for-Profi t• Retail• Self Storage

2011 NORTHERN CALIFORNIA COMMERCIAL REAL ESTATE OVERVIEW 9

CO

RP

OR

AT

E O

VE

RV

IEW

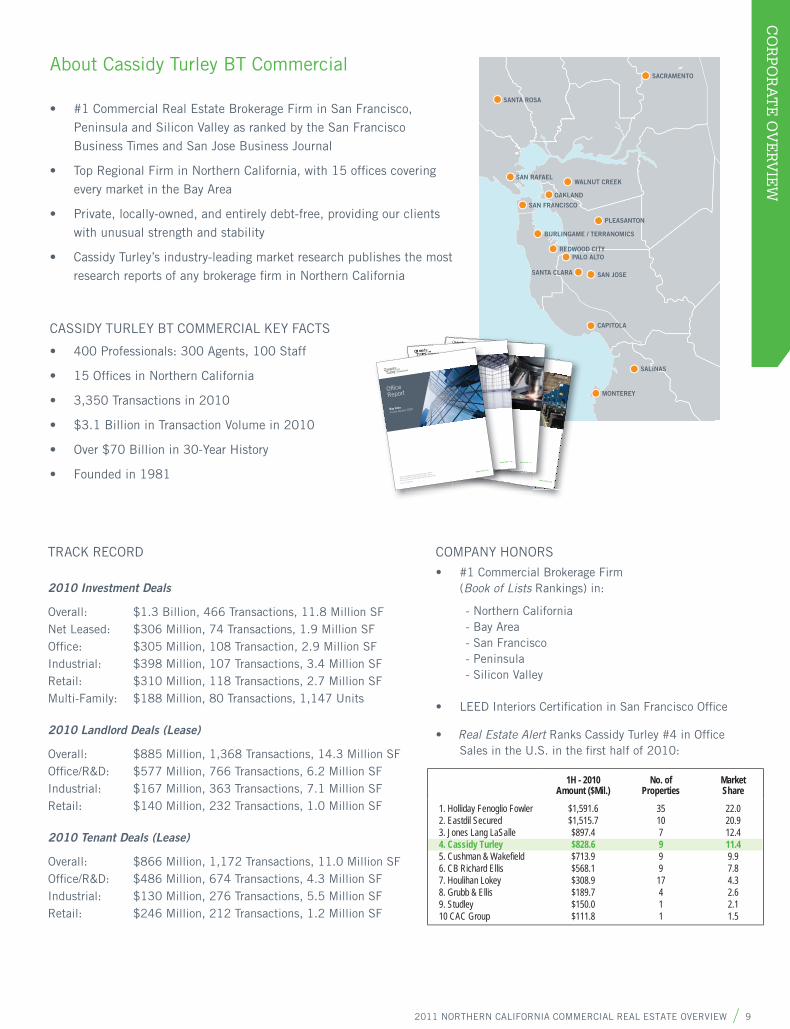

About Cassidy Turley BT Commercial

#1 Commercial Real Estate Brokerage Firm in San Francisco, • Peninsula and Silicon Valley as ranked by the San Francisco Business Times and San Jose Business Journal

Top Regional Firm in Northern California, with 15 offi ces covering • every market in the Bay Area

Private, locally-owned, and entirely debt-free, providing our clients • with unusual strength and stability

Cassidy Turley’s industry-leading market research publishes the most • research reports of any brokerage fi rm in Northern California

CASSIDY TURLEY BT COMMERCIAL KEY FACTS

400 Professionals: 300 Agents, 100 Staff •

15 Offi ces in Northern California•

3,350 Transactions in 2010 •

$3.1 Billion in Transaction Volume in 2010 •

Over $70 Billion in 30-Year History •

Founded in 1981•

SACRAMENTO

WALNUT CREEK

SANTA ROSA

SAN RAFAEL

SAN FRANCISCO

BURLINGAME / TERRANOMICS

PALO ALTO

SAN JOSE

CAPITOLA

SALINAS

MONTEREY

OAKLAND

REDWOOD CITY

PLEASANTON

SANTA CLARA

Offi ces in Burlingame, Capitola, Monterey, Napa, Oakland,

Palo Alto, Pleasanton, Redwood City, Sacramento, Salinas,

San Francisco, San Jose, San Rafael, Santa Rosa, Walnut Creek

Broker Lic #00825241

www.ctbt.com

City, State Year

ManufacturingReport

Bay AreaFourth Quarter 2009

www.ctbt.com

Offi ces in Burlingame, Capitola, Monterey, Napa, Oakland, Palo Alto, Pleasanton, Redwood City, Sacramento, Salinas, San Francisco, San Jose, San Rafael, Santa Rosa, Walnut CreekBroker Lic #00825241

www.ctbt.com

City, State YearBay AreaFourth Quarter 2009

wwwwwwww.ctbt.comOffi ces in Burlingame, Capitola, Monterey, Napa, Oakland,

Palo Alto, Pleasanton, Redwood City, Sacramento, Salinas,

San Francisco, San Jose, San Rafael, Santa Rosa, Walnut Creek

Broker Lic #00825241

www.ctbt.com

City, State Year

WarehouseReport

Bay AreaFourth Quarter 2009

,a Rosa, WalnWalnut Cut CreeCreekek

,

Offices in Burlingame, Capitola, Monterey, Napa, Oakland,

fiPalo Alto, Pleasanton, Redwood City, Sacramento, Salinas,

San Francisco, San Jose, San Rafael, Santa Rosa, Walnut Creek

Broker Lic #00825241

www.ctbt.co

WarehouseReport

Bay AreaFourth Quarter 2009

ta Rosa Wa,

Offi ces in Burlingame, Capitola, Monterey, Napa, Oakland,

Palo Alto, Pleasanton, Redwood City, Sacramento, Salinas,

San Francisco, San Jose, San Rafael, Santa Rosa, Walnut Creek

Broker Lic #00825241

www.ctbt.com

City, State Year

Offi ceReport

Bay Area

Fourth Quarter 2009

TRACK RECORD

2010 Investment Deals

Overall: $1.3 Billion, 466 Transactions, 11.8 Million SF Net Leased: $306 Million, 74 Transactions, 1.9 Million SF Offi ce: $305 Million, 108 Transaction, 2.9 Million SF Industrial: $398 Million, 107 Transactions, 3.4 Million SF Retail: $310 Million, 118 Transactions, 2.7 Million SF Multi-Family: $188 Million, 80 Transactions, 1,147 Units

2010 Landlord Deals (Lease)

Overall: $885 Million, 1,368 Transactions, 14.3 Million SF Offi ce/R&D: $577 Million, 766 Transactions, 6.2 Million SF Industrial: $167 Million, 363 Transactions, 7.1 Million SF Retail: $140 Million, 232 Transactions, 1.0 Million SF

2010 Tenant Deals (Lease)

Overall: $866 Million, 1,172 Transactions, 11.0 Million SF Offi ce/R&D: $486 Million, 674 Transactions, 4.3 Million SF Industrial: $130 Million, 276 Transactions, 5.5 Million SF Retail: $246 Million, 212 Transactions, 1.2 Million SF

COMPANY HONORS

#1 Commercial Brokerage Firm • (Book of Lists Rankings) in:

- Northern California - Bay Area - San Francisco - Peninsula - Silicon Valley

LEED Interiors Certifi cation in San Francisco Offi ce•

• Real Estate Alert Ranks Cassidy Turley #4 in Offi ceSales in the U.S. in the fi rst half of 2010:

1H - 2010Amount ($Mil.)

No. ofProperties

MarketShare

1. Holliday Fenoglio Fowler2. Eastdil Secured3. Jones Lang LaSalle4. Cassidy Turley5. Cushman & Wakefi eld6. CB Richard Ellis7. Houlihan Lokey8. Grubb & Ellis9. Studley10 CAC Group

$1,591.6$1,515.7$897.4$828.6$713.9$568.1$308.9$189.7$150.0$111.8

35107999

17411

22.020.912.411.49.97.84.32.62.11.5

10 CASSIDY TURLEY

OF

FIC

E O

VE

RV

IEW

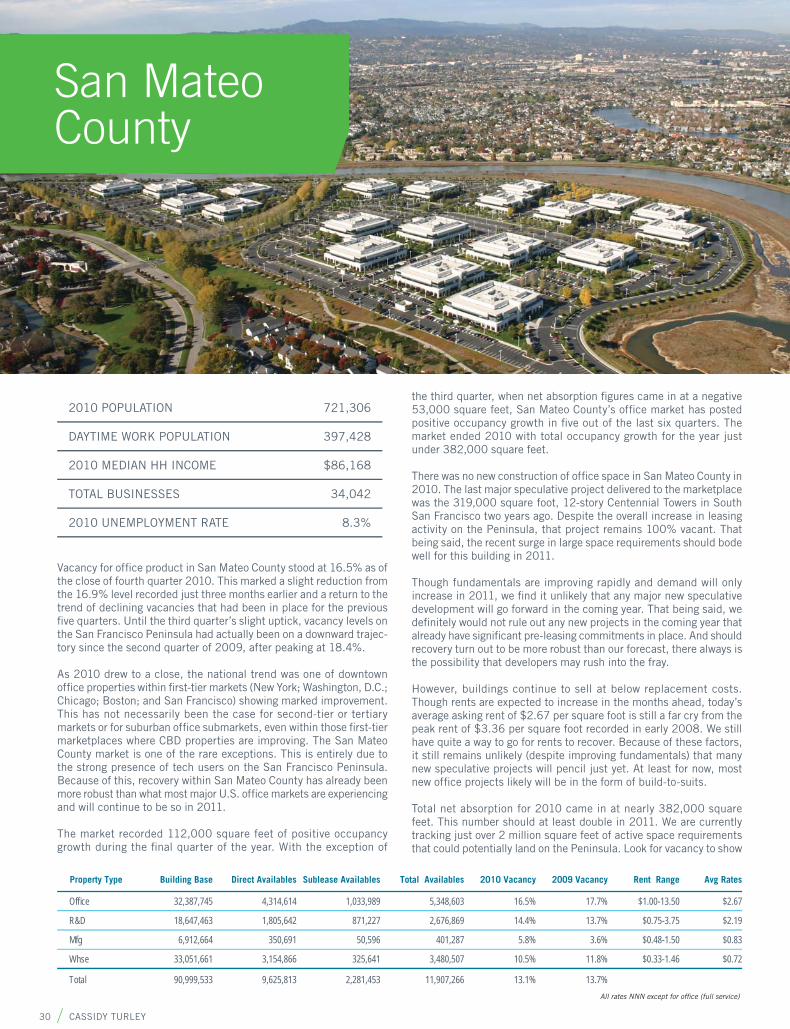

REVIEWOffi ce vacancy in San Mateo County stood at 16.5% as of the close of 2010. This marked a return to the trend of declining vacancies that had been in place for the previous fi ve quarters. Until the third quarter’s slight uptick, vacancy levels on the San Francisco Peninsula had actually been on a downward trajectory since the second quarter of 2009, after peaking at 18.4%.

The market ended 2010 with total occupancy growth for the year of just under 382,000 square feet. This was driven primarily by tech users. We track active tenant space requirements in the marketplace and are currently aware of just under 1.8 million square feet of poten-tial deals that could land in this market over the next 24 months. Tech companies, ranging from software development and Internet companies to biotech, account for nearly 1.3 million square feet of that total.

FORECASTVenture capital funding will increase heading into 2011, launching more start-ups and fueling more demand for commercial real estate. Tech companies will continue to dominate leasing activity on the Peninsula, but look for improved activity from other sectors of the economy by the second half of 2011. Meanwhile, fl ight-to-quality relocations will slow as rental rate growth picks up.

Look for improving fundamentals to gradually shift dynamics in favor of landlords by 2012. Rental rate growth will pick up steam in 2011, particularly by the end of the year. Total net absorption for 2010 came in at nearly 382,000 square feet. We are currently tracking just under 1.8 million square feet of active space requirements that could potentially land on the Peninsula. Based upon this and other factors, our worst-case forecast is that occupancy growth in 2011 will surpass 700,000 square feet. Most likely this number will come in between 700,000 square feet and 1 million square feet. However, an even more robust economy could see the market backfi lling slightly above that amount over the next 12 months. In our most-likely case forecast scenario, vacancy by year-end 2011 will have decreased from today’s rate of 16.5% to the low 14% range.

SAN MATEO

OFFICE VACANCY & RATE TREND

OFFICE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-1

0

1

2

3

4

5

0%

5%

10%

15%

20%

25%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

FU

LL S

ER

VIC

E R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

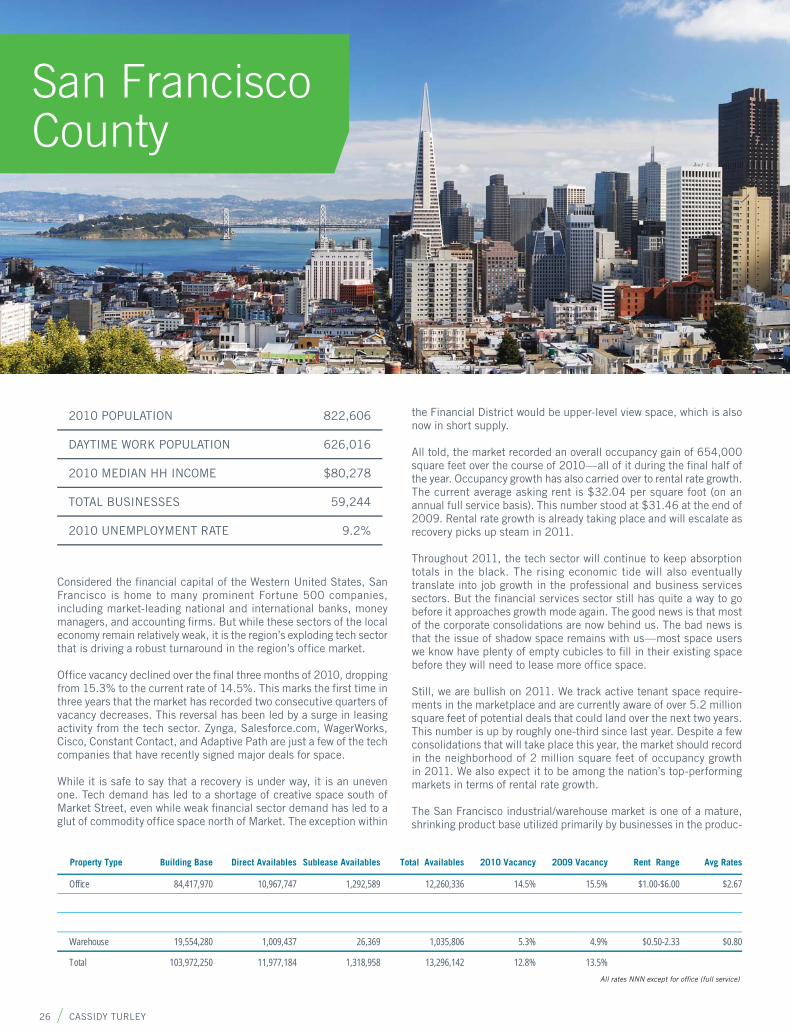

REVIEWAs 2010 came to a close, San Francisco’s offi ce market had recorded two consecutive quarters of strong occupancy growth and declining vacancy rates. Though tech users led this surge, we also began to see an increase in active space requirements from other sectors of the economy as the year came to an end. Though the fi nancial services sector still remained largely on the sidelines, it appeared that business and personal services users were beginning to return to the marketplace as well. The market closed the year with a vacancy rate of 14.5% and positive annual occupancy growth for the fi rst time since 2007.

The market clearly has entered recovery mode. With the overall Bay Area regional economy beginning to show some signs of life, we see the pace of recovery accelerating in 2011. The booming tech sector will continue to keep absorption totals in the black. The rising tide—lifted by tech—will also translate into job growth in the professional and business services sectors. That being said, the fi nancial services sector still has quite a way to go before it approaches growth mode again. But the good news is that the ongoing trend of consolidations that has been with us for the better part of two years will come to an end by midyear 2011.

FORECASTTotal net absorption for 2010 came in at roughly 654,000 square feet. We are currently tracking about 5.2 million square feet in active space requirements that could potentially land in San Francisco. Based upon this and other factors, our worst-case forecast is that occupancy growth in 2011 will surpass 1.5 million square feet. Most likely this number will come in at about 2 million square feet, and an even more robust economy could see San Francisco backfi lling as much as 2.5 million square feet of offi ce space over the next 12 months. In our most-likely case forecast scenario, vacancy will have decreased from today’s rate of 14.4% to 12.0% by year-end 2011. Throughout the coming year, San Francisco should rank as one of the top fi ve U.S. markets in terms of rental rate growth.

SAN FRANCISCO

OFFICE VACANCY & RATE TREND

OFFICE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-2

0

2

4

6

8

10

0%

5%

10%

15%

20%

25%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

Avg. Asking Rate

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

FU

LL S

ER

VIC

E R

AT

E

Vacancy

Gross Absorption Net Absorption New Construction

OFFICE OVERVIEW

2011 NORTHERN CALIFORNIA COMMERCIAL REAL ESTATE OVERVIEW 11

OF

FIC

E O

VE

RV

IEW

REVIEWThe Santa Clara County offi ce market entered 2010 with a vacancy rate of 18.8% and over 13.5 million square feet of available space. Vacancy levels actually peaked during the fi rst quarter of the year, topping out at 18.9%. This is where the market fi nally hit bottom after nearly three challenging years. Since that time, vacancy has been on a downward trend. As 2010 came to a close, the overall vacancy rate had dropped to 17.2%. Meanwhile, the market recorded occupancy growth of over 1.6 million square feet for the year—including a robust fourth quarter that alone saw over 680,000 square feet of positive net absorption. Rents are fi nally beginning to show signs of stabilization. The current average asking rent for offi ce space is $2.54 per square foot and has changed little over the last half of 2010. One year ago, this number stood at $2.66 per square foot. Two years ago, this number stood at $3.11.

FORECASTThe market fi nally hit bottom in 2010 and was clearly in recovery mode as the year came to an end. A surge in demand, driven by tech users, was already driving gains in occupancy. A gradually improving economy in 2011 should only intensify this trend. We track active user space requirements in the marketplace and are currently aware of as much as 7.8 million square feet of offi ce and R&D requirements that could land throughout Silicon Valley and the southern San Francisco Peninsula over the next 24 months. We expect deal activity to continue to build velocity heading deeper into 2011 and vacancy rates to fall. That being said, though we do expect robust occupancy growth for offi ce product in 2011, with current vacancy levels in the mid-teens and nearly 12.5 million square feet of existing vacancy to work through, it will take some time before the market achieves equilibrium. Still, look for rental rate growth to begin to occur in the region’s strongest submarkets and best-quality projects in 2011. Market conditions still favor tenants, but the pendulum is beginning to swing the other way. The window for opportunistic tenants to take advantage of today’s reduced rents may be a brief one.

SANTA CLARA

OFFICE VACANCY & RATE TREND

OFFICE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-2

0

2

4

6

8

10

12

0%

5%

10%

15%

20%

25%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

FU

LL S

ER

VIC

E R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

I-80/880 CORRIDOR

OFFICE VACANCY & RATE TREND

OFFICE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-1

0

1

2

3

4

0%

5%

10%

15%

20%

25%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

FU

LL S

ER

VIC

E R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

REVIEWThe vacancy rate for offi ce space in the East Bay market currently stands at 17.2%. This marks a slight increase from the 16.7% rate recorded during the third quarter of 2010. The market recorded just over 164,000 square feet of positive net absorption in 2010.

Over the past two years, leasing activity in the East Bay has been dominated by user consolidations, early renewals at reduced rates (“blend and extend” deals), and fl ight-to-quality relocations. Though renewals still account for the lion’s share of deal activity, the good news is that the market is fi nally seeing the return of actual growth deals. We track active tenant space requirements in the marketplace, and this number is up signifi cantly from where it stood just one year ago. We are currently aware of over 700,000 square feet of potential offi ce deals in the marketplace that could land over the next 24 months.

The current average asking rent for offi ce space in the region is $2.14 per square foot (on a monthly full service basis). Though there was some minimal movement in both directions over the course of 2010, rental rates have stabilized.

FORECASTWith medical and governmental users having historically driven growth in the East Bay, this market will see little direct growth from the Bay Area’s booming tech sector. But a rising tide lifts all boats, and increased job creation heading into 2011 will help boost demand above today’s levels in the coming year.

Total net absorption for 2010 came in at roughly 164,000 square feet. We are currently tracking about 700,000 million square feet in active space requirements that could potentially land in the East Bay. In 2011, this number will most likely come in at about 300,000 square feet; however, an even more robust economy could see the East Bay backfi lling as much as 400,000 square feet of offi ce space over the next 12 months. In our most-likely-case forecast scenario, vacancy by year-end 2011 will have decreased from today’s rate of 17.2% to 16.1%.

Leasing activity will continue on its upward trajectory in 2011, but the tech bounce that other Bay Area markets feel will be minimal in the East Bay. Rents have stabilized, but it will likely be late 2011 before the East Bay offi ce market sees rental rate growth, and this will be minimal, at best.

12 CASSIDY TURLEY

R&

D O

VE

RV

IEW

R&D OVERVIEW

REVIEWSan Francisco’s R&D market consists of just over 1.6 million square feet of inventory, nearly all of which is considered life science, or biotech, space. The overall vacancy rate for biotech space in San Francisco currently stands at 16.5%, up from the 12.7% mark that was recorded one year ago. Despite the spike in vacancy, the market actually recorded positive net absorption in 2010, with just over 29,000 square feet of occupancy growth.

Unfortunately, these numbers were offset by the delivery of a 105,000 square foot speculative building in Mission Bay, which is what drove up overall vacancy numbers. That being said, the relatively weak performance in 2010 merely refl ects the ongoing trend of mergers and acquisitions that has been negatively impacting the biotech market for most of the past three years. Thanks partially to the impact of the Great Recession, liquidity issues and the need to cut costs have played a role in the merger and consolidation of big pharmaceutical players. The need to fi ll product pipeline gaps also has played a role in larger companies picking up promising early- and mid-stage companies. We have yet to see signs that this trend is ending.

The current average asking rent for biotech space in San Francisco stands at $2.24 per square foot (on a monthly triple net basis). Though asking rents stabilized over the course of 2010 (they stood at $2.25 per square foot one year ago), they are still well below the peak of $2.70 per square foot recorded in 2007 at the peak of the last cycle.

FORECASTThe good news is that, as 2010 came to a close, venture capital funding was on the upswing. As of the close of the third quarter (the most recent data available), venture capital fl ows in the United States were up to $16.7 billion from $12.9 billion at the same time in 2009. Better yet, of that $16.7 billion, $6.3 billion was raised for Bay Area companies. Venture capital is what is fueling the reversal of the local offi ce and R&D markets. It also is what will be behind a new crop of start-ups that will eventually help to absorb currently vacant space. Likewise, an improving economy will help to alleviate cost pressures on big pharmaceutical players. The only problem is that relief to the biotech commercial real estate market is not likely to come until late in 2011. The good news for the San Francisco market is that it will likely outperform the region’s other biotech clusters in 2011, but that being said, we still expect growth to be tepid at best.

SAN FRANCISCO SAN MATEO

REVIEWVacancy for R&D product in San Mateo County crept up over the fi nal quarter of 2010, ending the year at 14.4%. This number dipped to 12.9% in the third quarter, but the market has failed to string together more than two consecutive quarters of vacancy declines ever since the impact of the recession began to be felt during the fi nal quarter of 2008. In fact, today’s vacancy levels are a return to where the market stood during the fi rst quarter of 2009. While vacancy has fl uctuated as much as two percentage points since that time, the market has essentially “bounced” along the bottom for two years now.

The market incurred occupancy losses in excess of 278,000 square feet during the fi nal quarter of 2010. While the Foster City/Redwood Shores, Belmont/San Carlos, and Menlo Park submarkets actually recorded fl at to slightly positive occupancy growth during the fourth quarter, both the South San Francisco/Burlingame/Brisbane and Redwood City submarkets recorded negative net absorption in six fi gures. The market ended the year with total annual negative net absorption to the tune of roughly 51,000 square feet. In 2009, the market recorded positive occupancy growth of over 616,000 square feet. Occupancy losses of over 278,000 square feet of space during the fourth quarter demonstrate that the market continues to face challenges.

FORECASTWhile today’s vacancy numbers may seem like a serious setback, there are some reasons for optimism. We track active space user requirements in the marketplace and are currently aware of as many as 7.9 million square feet in potential offi ce and R&D requirements that could land on the San Francisco Peninsula over the next 24 months. This number is up over 30% from one year ago. Touring activity is up, and this will translate into greater deal velocity and occupancy growth going forward.

The current average asking rent for R&D space in San Mateo County is $2.19 per square foot (on a monthly triple net basis). Though average asking rents remained stable over the second half of 2010, they have declined over the course of the past 12 months. One year ago, the average asking rent stood at $2.27 per square foot. Increased leasing activity in 2011 should see rents stabilizing over the fi rst half of the year. Modest rental rate growth for some of the region’s premier properties and strongest submarkets may occur as soon as late 2011.

R&D / LIFE SCIENCE VACANCY & RATE TREND

R&D / LIFE SCIENCE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-100

0

100

200

300

400

500

600

0%

5%

10%

15%

20%

25%

$0

$2

$4

$6

$8

$10

VA

CA

NC

YS

QU

AR

E F

EE

T IN

TH

OU

SA

ND

S

NN

N R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

R&D VACANCY & RATE TREND

R&D ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-1

0

1

2

3

4

0%

5%

10%

15%

20%

25%

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

NN

N R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

2011 NORTHERN CALIFORNIA COMMERCIAL REAL ESTATE OVERVIEW 13

R&

D O

VE

RV

IEW

REVIEWSanta Clara County houses more than 70% of the total R&D product in the Bay Area, with the heavy majority of all R&D activity continuing to reside in this region. The effects of the recession fi nally took their toll on the R&D market in 2009. As we entered 2010, the vacancy rate stood at 17.7% and over 23.4 million square feet of space was available. Market vacancy peaked during the fi rst quarter of 2010 at 18.0%. The good news is that this is where the market hit bottom. Though it was not in a straight line, the overriding trend of 2010 was one of gradual decreases in overall vacancy. As we closed 2010, the vacancy rate had fallen to 17.3%.

Though occupancy growth totals for the year remained in negative territory to the tune of 565,000 square feet, the market experienced a surge in activity over the fi nal quarter of the year. In the fourth quarter alone, occupancy growth topped 876,000 square feet. While this was not enough to overcome losses recorded earlier in the year, it came about as a direct result of surging tech sector requirements that are still in play and driving market activity. Against this backdrop, rents stabilized. The current average asking rent for R&D space in the Santa Clara County market is $1.04 per square foot (on a monthly triple net basis)—the same rate we recorded exactly one year ago.

FORECASTHeading into 2011, the booming tech sector will keep absorption totals in the black. The rising economic tide will also eventually translate into job growth in other sectors of the economy, though this might not translate into commercial real estate demand until late 2011 or early 2012. The good news is that the trend of consolidations that has been with us for the better part of two years is coming to an end. We are currently tracking about 7.8 million square feet in active offi ce and R&D space requirements that could potentially land throughout the greater Silicon Valley region over the next 24 months.

Look for leasing velocity to pick up steam as 2011 progresses. We expect occupancy growth to fi nally return to positive territory in 2011 and vacancy to continue the trend of decline that was in place in late 2010. But the market currently has over 22.8 million square feet of vacant space to work through. Though rental rates remained stable in 2010, we do not expect signifi cant growth in the coming year. Though we have a way to go before the market approaches equilibrium, the pendulum is slowly beginning to swing back in favor of landlords.

SANTA CLARA

R&D ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010-6

-3

0

3

6

9

12

15

18

R&D VACANCY & RATE TREND

2006 2007 2008 2009 20100%

5%

10%

15%

20%

25%

$0.00

$0.60

$1.20

$2.40

$3.00

$1.80

Vacancy Avg. Asking Rate

SQ

UA

RE

FE

ET

IN M

ILL

ION

S

Gross Absorption Net Absorption New Construction

NN

N R

AT

E

VA

CA

NC

YREVIEWVacancy for R&D product in the East Bay currently stands at 23.4%. One year ago, this number stood at 23.5%. The market made respect-able occupancy gains over the fi rst three quarters of 2010. By midyear, vacancy had reached as low as 21.9%. But the East Bay R&D market continues to face challenges from large blocks of vacancy left behind by single users. Because of this, most of the region’s vacancy is concentrated in just a few trade areas. Vacancy levels in Berkeley and Emeryville, for example, are well below 5.0%. The region’s three largest R&D submarkets—Fremont, Hayward, and Newark—account for roughly 6.8 million of the 7.1 million square feet of total R&D vacancy in the East Bay.

In terms of quarterly performance, the market recorded occupancy losses to the tune of 701,000 square feet during the fi nal three months of 2010. Prior to the fourth quarter’s dismal reading, net absorption had been in the black for four consecutive quarters. The East Bay R&D market closed 2010 with a total annual negative net absorption fi gure of nearly 402,000 square feet. This marks the second consecutive year of occupancy losses in this range. In 2009, the market logged 311,000 square feet of negative net absorption.

The current average asking rent for R&D space in the East Bay is $0.87 per square foot (on a monthly triple net basis). Rents remain under strong downward pressure. One year ago, the average asking rent stood at $0.93 per square foot. And though we saw the pace of rental rate declines slow over the course of the year, this trend may not yet be over.

FORECASTIf we are not at the bottom, we are near it. Improving fundamentals in 2011 should result in rent stabilization in most trade areas. Rental rate growth in the region’s three largest submarkets (Fremont, Hayward, and Newark) is not likely anytime soon.

The good news is that tenant space requirements and touring activity are both up. We also do not expect to see any large blocks of space being returned to the marketplace in the near future. But while we expect the market to return to positive territory in 2011, it will take a considerable amount of time to backfi ll current vacancies. It will likely be at least two to three years before the market approaches anything close to equilibrium.

I-80/880 CORRIDOR

R&D VACANCY & RATE TREND

R&D ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-1.5

0.0

1.5

3.0

4.5

6.0

0%

5%

10%

15%

20%

25%

$0.00

$0.60

$1.20

$1.80

$2.40

$3.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

NN

N R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

14 CASSIDY TURLEY

WA

RE

HO

USE

OV

ER

VIE

WWAREHOUSE OVERVIEW

REVIEWThe overall vacancy rate for industrial space in the San Mateo County market currently stands at 9.8%. This marks the second consecutive quarter in which vacancy has posted modest declines. One year ago, the vacancy rate stood at 10.6%. Though it has not been in a straight line, the overriding trend of 2010 was declining vacancy.

The market’s largest submarket, South San Francisco/San Bruno, recorded a slight uptick in vacancy during the fourth quarter, as vacancy increased from 10.8% to 11.0%. But despite a weak fourth quarter, this trade area has turned in the strongest performance of the year. Vacancy here one year ago stood at 13.4%; over the course of 2010, this trade area recorded over 319,000 square feet of occupancy growth.

The Burlingame/Millbrae submarket also continues to perform well. Vacancy has dropped from 11.7% to 6.8% over the past 12 months as the market has backfi lled over 140,000 square feet of previously vacant second-generation space. Going forward, this trend should intensify across all of San Mateo County’s trade areas as economic fundamentals improve. Meanwhile, with an overall vacancy rate of 9.8%, the market is fi nally fi nding equilibrium after a stormy 30 months.

FORECASTThe San Mateo industrial market will continue to outperform most of the Bay Area’s other industrial trade areas in 2011. Thanks to the surging tech industry, Bay Area employment growth will be strongest in San Francisco, Silicon Valley, and the Peninsula. Though San Mateo’s offi ce and retail markets will likely see a greater increase in terms of overall demand, this will play out as improving fundamentals for industrial space as well. Because vacancy here is already relatively tight, we should see modest rental rate growth in 2011. New construc-tion will continue to be a non-factor due to the lack of available land and prohibitive pricing (for industrial development) on what little dirt is on the market.

Look for the San Mateo County industrial market to continue to record occupancy growth in 2011, with fundamentals improving as the year progresses. While consolidations, renewals, and relocations have dominated leasing activity for much of the past 30 months, 2011 will see an increase in actual growth and expansion activity. Vacancy will continue to post modest declines. Rents for the strongest submarkets and premier product should post modest gains by late 2011.

REVIEWThe San Francisco County industrial market represents the smallest industrial market in the Bay Area, with only 19.5 million square feet of inventory. The market closed 2010 with an overall vacancy rate of 5.3%. Though this marks a slight improvement over the 5.4% mark recorded at the close of the third quarter, it still refl ects an increase over the 4.9% vacancy level posted one year ago. As recently as 2007, the industrial vacancy rate was as low as 2.1%.

While the recent decrease in vacancy will come as welcome news to landlords, the reality is that industrial product in San Francisco is just now beginning to stabilize. Though occupancy growth during the fourth quarter was positive to the tune of 11,000 square feet, this was not enough to make up for the losses incurred earlier in the year. The market closed 2010 with a total of 92,000 square feet of negative net absorption for the year. The last time that the market closed the year with positive net absorption was 2007, when a paltry 34,000 square feet of occupancy gain was recorded.

The current average asking rent for industrial space in San Francisco is $0.80 per square foot (on a monthly triple net basis). Despite the fact that market activity in 2010 was largely in negative territory, asking rents for industrial space in San Francisco have been slowly creeping up. Just one year ago, the average asking rent stood at $0.75 per square foot.

FORECASTBecause of the historically limited demand for industrial space within city limits, stabilization—not recovery—will likely be the story for 2011. Look for industrial leasing in San Francisco to show modest improvement over the course of the year. Following three consecutive years of occupancy losses, the market will record positive net absorption in 2011, but gains will likely be minimal. The City will continue to be perceived as more expensive for industrial uses than neighboring industrial markets to the south and across the Bay, where users can still fi nd plenty of modern buildings, yard space, and access to rail, shipping, and interstate freeways. Demand here will continue to be driven by production, distribution, and repair sector users who need to be located in San Francisco. That being said, we do see the likelihood of further rental rate growth in 2011 despite the fact that absorption will be tepid. This is because vacancy levels are already tight, and users that are active in this marketplace are motivated by locational issues.

SAN MATEOSAN FRANCISCO

WAREHOUSE VACANCY & RATE TREND

WAREHOUSE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-0.6

-0.3

0.0

0.3

0.6

0.9

1.2

0%

3%

6%

9%

12%

15%

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

NN

N R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

WAREHOUSE VACANCY & RATE TREND

WAREHOUSE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010

0%

3%

6%

9%

12%

15%

-2

-1

0

1

2

3

4

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

NN

N R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

2011 NORTHERN CALIFORNIA COMMERCIAL REAL ESTATE OVERVIEW 15

WA

RE

HO

USE

OV

ER

VIE

W

REVIEWThe Santa Clara County warehouse market closed 2010 with an overall vacancy rate of 9.3%. The good news is that this is below the midyear 2010 peak of 9.8%. The bad news is that it is still above the 8.7% level that we saw at the end of 2009. While vacancy remains well below the peak level of 14.0% that we saw at the height of the last market downturn, the fact remains that local warehouse vacancy has remained well above the 8.0% mark for going on three years now. Meanwhile, the Santa Clara warehouse market recorded over 228,000 square feet of occupancy losses over the course of 2010.

The news is not all bad. Though the market ended the year in the red, most of these occupancy losses were incurred over the fi rst half of 2010. And while deal activity in general has been dominated by renewals and consolidations over the past 12 months, we did see an increase in actual growth requirements over the fi nal six months of the year. Meanwhile, rents stabilized over the course of 2010. Today’s current average asking rent of $0.44 per square foot (on a monthly triple net basis) has remained fi rmly in place for going on two years now.

FORECASTWhile it is too soon to say that the market has turned the corner, we do believe that it is currently at—or very near—bottom. Tenant space requirements are up, and our brokers report increased touring activity. Leasing momentum picked up as 2010 came to a close, and this trend, so far, has rolled over into 2011. Improving Bay Area economic fundamentals are already driving recovery for offi ce and retail product, and this will translate into increased demand for warehouse space; unfortunately, the industrial sector will be the last to see this boost. Look for the fi rst half of 2011 to be about stabilization, with signs of modest recovery becoming evident by the fi nal half of the year. The pendulum will slowly begin to swing in favor of landlords. However, with over 2.9 million square feet of space currently available throughout the marketplace, it will take some time before any signifi cant rental rate growth will be possible.

SANTA CLARA

WAREHOUSE VACANCY & RATE TREND

WAREHOUSE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-1

0

1

2

3

4

0%

3%

6%

9%

12%

15%

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

NN

N R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

REVIEWThe overall vacancy rate for warehouse space in the East Bay currently stands at 10.1%. This marks the second consecutive quarter in which vacancy has held at this rate. It also marks the fourth consecutive quarter of either decreasing or fl at vacancy. The market essentially remained stable throughout 2010. One year ago the vacancy rate stood at 9.9%.

In terms of quarterly performance, the market recorded occupancy losses to the tune of 80,000 square feet during the fourth quarter. Net absorption was in the black during the second and third quarters of 2010, when the market absorbed a combined 490,000 square feet of space. All told, the East Bay warehouse market recorded occupancy losses of nearly 106,000 square feet in 2010. This marks the fourth consecutive year of negative net absorption for this product type. But the news is not all bad. Though negative net absorption means that the economy is contracting, 2010’s loss of 106,000 square feet of occupancy is downright paltry compared to where the market has been.

In 2007, the East Bay warehouse market lost over 945,000 square feet of occupancy. It hemorrhaged just over 1 million square feet in 2008. The market recorded nearly 1.9 million square feet of negative net absorption in 2009. The good news? The bleeding has stopped. While 2010 was a year of stabilization, 2011 will be a year of recovery.

The current average asking rent is $0.37 per square foot (on a monthly triple net basis). The Berkeley submarket leads all trade areas in terms of highest average asking rent, at $0.58 per square foot. The Newark submarket, with an average asking rent of $0.32 per square foot, is the region’s most affordable trade area. While today’s average asking rent of $0.37 per square foot remains virtually unchanged from the previous quarter, this number stood at $0.40 just one year ago. While rents have either stabilized or posted minimal gains in the Emeryville, Oakland, and Hayward submarkets, they continue to face downward pressure in nearly every other trade area.

FORECASTImproving fundamentals in 2011 will result in rent stabilization in most trade areas over the fi rst half of the year. More than likely, it will be 2012 before we see any signifi cant traction for rents.

I-80/880 CORRIDOR

WAREHOUSE VACANCY & RATE TREND

WAREHOUSE ABSORPTION & NEW CONSTRUCTION TREND

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010-3

0

3

6

9

12

0%

3%

6%

9%

12%

15%

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

VA

CA

NC

YS

QU

AR

E F

EE

T IN

MIL

LIO

NS

NN

N R

AT

E

Vacancy Avg. Asking Rate

Gross Absorption Net Absorption New Construction

16 CASSIDY TURLEY

SHO

PP

ING

CE

NT

ER

OV

ER

VIE

WSHOPPING CENTER OVERVIEW

The San Francisco Bay Area shopping center market closed 2010 with an overall vacancy rate of 6.8%. At the end of 2009, this number stood at 7.6%. The Bay Area continues to rank in the top fi ve U.S. markets in terms of retail activity. The current national average for shopping center vacancy is 10.9%.

This rebound has been led by a surge of activity from a select group of players. Grocery players remain particularly active; Safeway inked a number of deals in 2010 and is looking at as many as six or seven Bay Area openings in 2011. Fresh & Easy fi nally will be launching its Northern California presence beginning in March. The U.K.’s largest retailer has over 40 stores throughout Northern California—some of which have had leases in place for as long as three years—that it will be launching this year.

Grocery Outlet also has been active; the chain has at least 15 new West Coast stores lined up for 2011. In Northern California, this includes new locations in Davis, Fremont, and South San Francisco. Ethnic grocer Mi Pueblo has signed a few recent deals and continues to look for sites. Organic chains Henry’s Farmers Market, Sunfl ower Farmers Market, and Sprouts have also been active, opening new stores in 2010 and continuing to look for sites. Other players on the move include Big Lots!, Save-A-Lot, Stein Mart, 99 Ranch Market, and other players.

Target and Wal-Mart have both been active in the marketplace. Target recently inked deals at the Metreon in San Francisco and has other deals in the works locally. Wal-Mart is looking at adding as many as 12 Sacramento region stores and is also looking in the South Bay and East Bay. Both Target and Wal-Mart are experimenting with new formats. Target is exploring a new smaller urban design while also rolling out its P-Fresh grocery sections to as many as 300 stores this year.

Wal-Mart is looking at opening as many as 300 stores throughout the United States and Canada over the next 30 months, including125,000 square foot or greater Superstores; 80,000 square foot stand-alone grocery stores (the chain acquired a couple of former Mervyns stores for just this purpose); and 30,000 to 40,000 square foot neighbor-hood small-grocery formats. We’ve even heard of a couple of 10,000 square foot urban grocery deals done by Wal-Mart in other markets recently.

Walgreens and CVS both remain active, but we have also seen activity tick up from a wide array of users outside of the grocery, drug, and category killers. Ross Dress for Less, T. J. Maxx, and Marshalls have all inked numerous deals in the region and continue to scout for new sites. Also on the move is 24 Hour Fitness, with as many as four new Bay Area health clubs in its sights. Crunch Fitness is also in the market. Sleep Train has been particularly active, with as many as seven new Bay Area stores slated to open in the next year. The same goes for Mattress Discounters, Goodwill, Tuesday Morning, PETCO, Rochester Big & Tall, and DSW shoe stores.

Restaurant chains continue to drive the market for smaller space. Five Guys Burgers and Fries has been active both in opening units in 2010 and in looking for sites for 2011. Smashburger is reportedly looking to head to the Bay Area after having successfully launched in Sacramento in 2010. Chick-fi l-A is launching locally, with as many as four new restaurants slated to open in the fi rst half of 2011. In-N-Out is also actively looking for sites and opening new restaurants throughout Northern California. Gott’s Roadside, formerly Taylor’s Refresher, is also looking for additional Bay Area locations.

Meanwhile, Yogurtland inked 10 local deals in 2010 and will likely match that number in the coming year. Chipotle, Panda Express, Qdoba, Panera Bread, Sweet Tomatoes, and Rubio’s all remain active. Casual restaurant chains have also boosted their expansion plans. IHOP, Sizzler, Fresh Choice, BJ’s Brewhouse, Johnny Rockets, and Denny’s are just a few chains that either have recently opened new

units or are looking to open restaurants throughout the region over the coming year.

Vacancy within the Bay Area currently stands at 6.8%, indicating continued improvement over the past six months, but this is not to say that recovery for the retail market has been even. Activity throughout 2010 was driven by larger national credit tenants. Discounters, off-price apparel chains, and new grocery players (discount, organic, and ethnic-themed) scoured the market for deals on superior second-generation junior-anchor and big-box space that had been vacated in the last wave of bankruptcies. Roughly 120 million square feet of big-box space has been vacated since 2008. By the close of 2010, just under 40 million square feet of this space had been backfi lled. This trend played out strongly in the Bay Area, where nearly all of the vacant fi rst-tier big-box spaces have now been accounted for.

But if larger deals from box and junior-box users have helped to take large chunks of vacancy off the market, the market for leasing smaller in-line space continues to face some challenges. Activity here was also driven in 2010 by national players. Food concepts, both new and old, were particularly active. But the mom-and-pop sector remains missing in action and is unlikely to return to the marketplace in any large numbers until the housing market begins to recover (home equity loans are the initial line of funding for many of these start-ups). This has had a particularly dire impact on unanchored retail strip centers.

Unfortunately, because our survey tracks only shopping centers of 50,000 square feet or more, strip retail centers are not covered in our statistics. But we estimate strip retail vacancy levels throughout the Bay Area to be two to three times greater than those posted in the region’s larger, anchored shopping centers. The hardest-hit markets, in terms of strip retail vacancy, are those in the Bay Area’s outlying reaches. In many of the communities on the outermost pattern of growth, strip centers were built ahead of housing at the peak of the last real estate cycle.

There are some other factors to consider as well. Retail vacancy is a tricky number to track. Overall vacancy numbers certainly give an accurate big-picture view of the sector’s health, but they don’t tell the full story. Unlike offi ce space, which is largely a commodity property type that varies little beyond simple class distinctions from one market to the next, retail centers have a myriad of other variables that come into play.

Breaking down shopping centers by type—malls, power centers, neighborhood centers, strip, etc.—can help, but this has its limitations as well. This is because the largest single factor impacting vacancy for shopping centers remains location. “Location, location, location” is the old mantra, but the real key to strength in today’s marketplace is location, strong anchors, tenant mix, attractive design/architecture and fi nishes, top-quality property management, and superior leasing teams. That being said, to fully understand what is happening in the retail world, it might be most helpful to break the market into three tiers.

BAY AREA Shopping Center Gross Leasable Area

Neighborhood25%

Other12% Community

38%Strip4%

Power21%

BAY AREA SHOPPING CENTER OVERVIEW

2011 NORTHERN CALIFORNIA COMMERCIAL REAL ESTATE OVERVIEW 17

SHO

PP

ING

CE

NT

ER

OV

ER

VIE

W

First-tier properties are those within vibrant urban marketplaces or located at top suburban intersections or along trade corridors. They boast successful anchor tenants that help drive traffi c to their centers, and they have strong existing tenant mixes. Throughout the Bay Area, fi rst-tier centers are uniformly posting lower vacancy levels and are currently positioned for rental rate growth, if not already achieving it. With a diminished pool of tenants seeking space, these tier-one centers are seeing the most touring activity and the most deals.

Second-tier centers can be situated within vibrant urban marketplaces or even located at top suburban intersections or along trade corridors, but if so, they are lacking in terms of either strong anchor tenants or tenant mix. More often, however, in built-out markets they are in secondary locations—not “on the main drag” but around the corner. They tend to be near the action, but not in it. They also can be in primary locations in small trade areas, such as being the only supermarket-anchored shopping center in a small bedroom commu-nity. These centers are seeing some spillover of deals from the region’s fi rst-tier centers but have had to be much more competitive with their rents to land tenants. Vacancy for these centers remains elevated, though it is slowly improving. Rental rate growth, on the other hand, has largely not happened yet for most of these centers, though many (not all) will be in position to post modest growth later in 2011.

Third-tier centers would be defi ned as the weakest locations within the urban or suburban core, or weaker centers in smaller or rural markets. Unanchored strip retail, with a few exceptions, would largely fall into this category. This category also includes aging shopping centers challenged by obsolescence issues or in dire need of upgrades. With today’s diminished pool of tenants, few are even touring third-tier projects. The deals that are being inked at these centers are almost exclusively value driven—usually with mom-and-pop tenants. The lack of small retail start-ups in the marketplace is having a particularly profound impact on these shopping centers. They almost uniformly boast the highest vacancy levels. Rents are only now beginning to stabilize for this product type (with a few exceptions in both direc-tions), and for these landlords 2011 is less likely to be a year of recovery than one of stabilization.

COUNTY HIGHLIGHTSThe San Francisco Bay region shopping center market consists of 723 centers (we track only those above 50,000 square feet) that account for just over 100 million square feet of inventory. The Santa Clara County market is the largest trade area, with over 31.3 million square feet of inventory and a current vacancy rate of 6.7%, down from 7.1% just one year ago.

The Alameda County market is the second-largest trade area within the region and consists of 116 shopping centers comprising over 20.3 million square feet of inventory. Vacancy now stands at 7.5%, up marginally from the 7.0% mark recorded one year ago.

The Contra Costa County market consists of 115 shopping centers with a total inventory of over 16 million square feet. Vacancy currently stands at 6.5%—down considerably from 8.7% at the close of 2009.

The San Mateo County market boasts the region’s tightest vacancy, with just 3.5% of its major shopping center space available as of the close of 2010.

With the exception of Alameda County, every single market within the greater Bay Area posted declines in retail vacancy over the second half of 2010. None of the trade areas in the region have vacancy in excess of 12.0%, and there are only two trade areas where vacancy tops 10.0%. There are four markets within the region that have extremely low vacancy levels of 5.0% or less. While retail development has virtu-ally disappeared from the landscape in nearly every single major U.S. marketplace, we have a number of trade areas where the challenge of fi nding quality retail space is increasingly becoming an issue.

RENTAL RATE TRENDSThe current average asking rent for shopping center space throughout the Bay Area is $25.23 (on an annual triple net basis) per square foot. This marks a negligible decline over the $25.58 mark that we recorded one year ago. That being said, rents are still below where they stood two years ago, when this number was $31.05. The good news for landlords is that rents have largely bottomed and the region’s top centers are driving overall growth. But we have to emphasize that it is the region’s fi rst-tier centers that are behind this. Some second-tier centers are also raising rents, but this trend has been uneven for that asset class. Third-tier centers, meanwhile, continue to face leasing challenges and downward pressure on asking rates. Keep in mind that these numbers refl ect a wide range of shopping center types and classes and work best as an overall benchmark for the region. We are actually tracking rents ranging from $7.60 to as high as $100.00 per square foot.

LOOKING FORWARDThough the market will almost certainly see at least a couple of high-profi le retailer bankruptcies in the fi rst half of 2011, the overall news is good. The 2010 holiday sales season saw an increase in sales of 5.5% and the strongest numbers posted since 2006. Many publicly traded retailers have already boosted their expansion plans for the year. Though the market will likely see large blocks of space returned from players like Blockbuster and Borders, new growth in the pipeline will surpass this.

One other factor to consider is that, as retailers boost their expansion outlook, their targets are largely where the job growth is taking place. Washington, D.C.; New York; and the San Francisco Bay Area are expected to be the top three U.S. job markets in 2011. Retailers will continue to boost expansion plans throughout the Bay Area, a trend that will mean further declines in vacancy. In fact, we know of a number of retailers who are already concerned that the region is running low on fi rst-tier space.

Look for fi rst- and second-tier shopping centers to continue to record occupancy growth in 2011. Rental rate growth will spread slowly to second-tier shopping centers while escalating in fi rst-tier projects. Third-tier product, however, will continue to face challenges. The good news is that these properties have already seen the worst of the rental rate declines; 2011 will see some stabilization of rents for the region’s weakest properties as the entire marketplace continues to tighten.

Spring 2011ChainLinks Retail Advisors

U.S. National Retail Report

Matt KircherChainLinks President650.931.2220 [email protected]

Garrick H. BrownChainLinks Research Director916.329.1558 [email protected]

Brought to you by:

Chainlinks is proud to present the inaugural edition of our U.S. National Retail Report. This report covers vacancy, absorption, construction and rental rate trends for the shopping center markets in over 40 major U.S. metropolitan regions. We also track investment trends across the country for multiple product types. We track retailer demand from the local to national levels. We also track the big picture trends that impact the retail industry in general. Our goal is nothing less than to create the industry gold standard for retail commercial real estate research reporting and to that end, we will strive to give you the most in-depth level of analysis and forecasting available in the marketplace.

IN THIS ISSUEPower Rankings .......................................................................................................................................2

Transactional Trends ...............................................................................................................................2

Marketplace Trends .................................................................................................................................2

Retailer Trends .........................................................................................................................................4

Restaurant Trends ....................................................................................................................................5

Economic & Retail Indicators .................................................................................................................6

Flat Vacancy Rate Hides Uneven Recovery ............................................................................................8

Rental Rate Trends ..................................................................................................................................9

New Construction at Record Lows ........................................................................................................11

Demand on the Rise - Retailer Growth Requirements Up 40% in 2011 ...............................................11

More Challenges Ahead for Media Retailers .........................................................................................13

Grocery Store Consolidation .................................................................................................................13

M&A Madness ........................................................................................................................................15

Foreign Affairs ........................................................................................................................................17

Retail Investment Outlook - Trophies, Trash & ‘Tweeners .....................................................................18

Triple Net Leased Properties Remain Strong ........................................................................................18

2011: From Bifurcated Market to Trifurcated Market ............................................................................19

Looking Ahead .......................................................................................................................................21