2011-ESMA 116 Annex - Report on equivalence China

25

12 April 2011 | ESMA/2011/Annex 1 Report Supplementary Progress Report on the equivalence of Chinese Accounting Standards with International Financial Reporting Standards

Transcript of 2011-ESMA 116 Annex - Report on equivalence China

12 April 2011 | ESMA/2011/Annex 1

Report

Supplementary Progress Report on the equivalence of Chinese Accounting Standards

with International Financial Reporting Standards

ESMA • 11-13 avenue de Friedland • 75008 Paris • France • Tel. +33 (0) 1 58 36 43 21 • www.esma.europa.eu

Table of Contents

I Requirements with respect to equivalence in the European Union ______________________ 4

II Previous reports on equivalence______________________________________________ 4

III Institutional framework in China _____________________________________________ 5

IV Evolution in the process of convergence of ASBEs to IFRS ____________________________ 6

V Enforcement experience of the ASBEs __________________________________________ 7

VI Co-operation with other parties ______________________________________________ 10

VII Preliminary conclusions ___________________________________________________ 11

Annex I: Roadmap for continuing convergence of the Chinese Accounting Standards for Business Enter-

prises with the International Financial Reporting Standards.

Annex II: List of detailed differences between the Chinese Accounting Standards for Business Enterprises

and the International Financial Reporting Standards - as prepared and provided by the MoF.

List of abbreviations and acronyms used in this report

ASBEs Accounting Standards for Business Enterprises

CASC Chinese Accounting Standards Committee

CESR Committee of the European Securities Regulators

CSRC Chinese Securities Regulatory Commission

ESMA European Securities and Markets Authority

HK CPA Hong Kong Institute of Certified Accountants

HK Ex Hong Kong Exchanges and Clearing

HK FRC Hong Kong Financial Reporting Council,

HK SFC Hong Kong Securities and Futures Commission

IASB International Accounting Standards Board

IFRS International Financial Reporting Standards

MoF Ministry of Finance of the People’s Republic of China

PRC People’s Republic of China

Date: 12 April 2011

ESMA/2011/116/Annex 1

3

Executive Summary

Following European Regulation No 1095/2010 of the European Parliament and of the Council, the Com-

mittee of the European Securities Regulators (CESR) has been transformed into the European Securities

and Markets Authority (“ESMA”) with effect from 1 January 2011. As the successor organisation to CESR,

ESMA will complete all engagements entered into by CESR in existence at the transition date.

This report fulfils a mandate received by CESR from the European Commission in June 2010 to provide it

with an update on the adoption or convergence programmes in several countries. The mandate aims to put

the Commission in a position to provide a progress report to the Council and the European Parliament in

line with its obligations under Commission Regulation (EC) 1569/2007 passed by the Parliament in De-

cember 2007. The mandate received in 2010 from the Commission identified the need to make on-the-

spot investigations in China.

In March 2008, at the European Commission’ request, CESR provided advice on the equivalence of Chi-

nese accounting standards to International Financial Reporting Standards (IFRS). In June 2009 and No-

vember 2010, CESR prepared update reports on the progress made by China in its process of convergence

to IFRS.

This report supplements the update report issued in November 2010. Consequently this report is intended

to be basically factual in nature, providing for information purposes much of the source material that has

been used to prepare it, and should not in any way be considered a formal advice or opinion on the pro-

gress achieved in China towards convergence with IFRS. As this report is designed to update, it should be

read in conjunction with the reports CESR has produced previously.

In preparing this report, ESMA has had recourse to information provided during or in conjunction with a

meeting held in January 2011 with representatives of the Chinese Ministry of Finance and the Chinese

Securities Regulatory Commission.

ESMA’s work indicates that China has taken a number of further steps in pursuit of its convergence pro-

gramme and in particular with respect to the following:

a. The Accounting Regulatory Department of the MoF has continued to work on the elimination of

the differences between the ASBEs and IFRS. With the exception of one major difference with respect to

the reversal of impairment, only a few minor differences remain, so the level of convergence achieved

could be considered satisfactory.

b. In terms of enforcement, significant steps have been undertaken to monitor entities leading to

improvements in the application of the ASBEs by companies.

c. China is continuing its active involvement in IASB activities and will monitor the development of

the standards currently under revision in order to take the necessary steps to further converge ASBEs to

IFRS

Further detail on the actions China has taken in the areas of convergence of its accounting standards and

in its enforcement processes are given in dedicated areas of this report.

This report should not be considered to constitute further advice by ESMA on the equivalence of the con-

verged accounting standards concerned.

4

I Requirements with respect to equivalence in the European Union

1. Following European Regulation 1095/2010 of the European Parliament and of the Council, the Com-

mittee of the European Securities Regulators (CESR) has been transformed into the European Securi-

ties and Markets Authority (“ESMA”) with effect from 1 January 2011. ESMA will complete all previous

engagements entered into by CESR. Consequently this report has been prepared pursuant to a mandate

received by CESR in June 2010.

2. Under both the European Prospectus and Transparency Directives, third country issuers who have

their securities admitted to trading on an EU regulated market or who wish to make a public offer of

their securities in Europe, are required to produce financial reports using either International Financial

Reporting Standards (“IFRS) adopted pursuant to EC Regulation 1606/2002 (hereinafter “EU IFRS”)

or a third country’s national accounting standards ("third country GAAP") deemed equivalent to those

standards.

3. In December 2007 the European Commission published Regulation (EC) 1569/2007 “Commission

Regulation establishing a mechanism for the determination of equivalence of accounting standards ap-

plied by third country issuers of securities pursuant to Directives 2003/71/EC and 2004/109/EC of the

European Parliament and of the Council” (“Commission Regulation on the mechanism”). This Regula-

tion established the conditions under which the GAAP of a third country can be considered equivalent

to IFRS pursuant to a definition of equivalence set out in article 2. The Regulation also set out condi-

tions in article 4 under which the accounting standards of other third countries could be considered ac-

ceptable for a limited period expiring no later than 31st December 2011.

4. The aim of granting this transitional period was to allow the standard setters and regulators of those

countries concerned more time to pursue their existing programmes either to converge their account-

ing standards with or to adopt IFRS. The countries concerned were Canada, China, India and South

Korea. In 2008, at the European Commission’s request, CESR provided advice on the equivalence of

the accounting standards of those four countries.

5. The Regulation also requires the European Commission to update the European Parliament at regular

intervals on the progress that is being made by these countries with regard to their respective pro-

grammes. Consequently, CESR has undertaken work and prepared advice or update reports at regular

intervals on the adoption or convergence of these third country GAAPs to IFRS.

6. Within ESMA, the operational group designated as the Corporate Reporting Standing Committee

chaired by Fernando Restoy, Vice-Chair of the Spanish CNMV, has been charged with fulfilling the

European Commission’s request with respect to advice or progress reports on equivalence of third

country accounting principles to IFRS.

II Previous reports on equivalence

7. The aim of this report is to supplement information provided previously regarding the process of con-

vergence in China. This update report is part of an on-going process of assessment of the equivalence of

Chinese GAAP which permits Chinese issuers to access European markets using financial statements

prepared under Chinese GAAP.

5

8. In its March 2008 advice ( CESR/08-179), CESR recommended the European Commission to postpone

a final decision on the equivalence of Chinese GAAP until there was more information on the applica-

tion of the new Chinese accounting standards. This recommendation was based on CESR’s belief that

evidence of adequate implementation was important in the context of an outcome-based definition of

equivalence. CESR however also recommended that the Commission allow Chinese issuers to continue

to use Chinese GAAP when accessing EU markets and therefore to accept Chinese GAAP under article 4

of the Commission Regulation on the mechanism until such time as there was adequate evidence to en-

able a decision to be made under article 2 thereof.

9. In June 2009, CESR provided the European Commission with an update report on the progress made

by China in the process of applying the converged Chinese standards. That report was approved and

endorsed by the European Parliament in June 2010.

10. In June 2010, CESR received a request from the European Commission to produce a second update

report. The new mandate made clear that CESR was required to have regard in its work to publicly

available information or to information made available by the regulators concerned upon request in

writing. It identified the potential need to make on-the-spot investigations in China.

11. In November 2010 and in response to the European Commission request, CESR provided a second

report on the progress made in Canada and South Korea towards adopting IFRS and in India and China

towards converging with IFRS (CESR 10-1301). The information related to China included in that re-

port was based only on publicly available information, an exchange of written information with repre-

sentatives of the Chinese authorities and a meeting with a representative of the IASB.

12. As stated in the introduction to this report, the European Commission has specifically requested CESR

to undertake limited additional work to assess whether Chinese Accounting Standards for Business En-

terprises (ASBEs) are being properly applied by Chinese issuers. In order to do this, ESMA was re-

quired to obtain appropriate evidence relating to the application of ASBEs by Chinese issuers. Although

ESMA’s report on ASBEs will be used by the Commission to supplement the information contained in

earlier reports made by CESR when it updates the European Parliament, this report will not be consid-

ered to constitute further advice by ESMA on the equivalence or otherwise of ASBEs.

13. Consequently this report, aimed at fulfilling ESMA’s obligations under the mandate received in June

2010, is intended to be basically factual in nature, providing for information purposes much of the

source information that has been used to prepare it, and does not in any way seek to opine on the pro-

gress towards convergence achieved by China. .

14. In order to fulfil the request made by the European Commission in the above mentioned mandate and

consequently to supplement its November 2010 report, ESMA has met with representatives of the Chi-

nese Ministry of Finance, the Chinese Securities Regulatory Commission and various Hong Kong au-

thorities in January 2011.

III Institutional framework in China

15. The institutions playing a role in the implementation and enforcement of accounting standards in

China are the Ministry of Finance (MoF) of the People’s Republic of China and the Chinese Securities

Regulatory Commission (CSRC).

6

16. The responsibilities of the MoF include developing principles, issuing regulations, setting standards,

ensuring compliance with financial reporting requirements, providing directions and setting require-

ments for the accounting and auditing profession. The Accounting Law provides the legal framework

under which all corporate entities are required to prepare and present financial statements in compli-

ance with nationally unified accounting standards set by the MoF.

17. The Accounting Regulatory Department of the MoF is in charge of the specific work related to drafting

and implementation of accounting standards, unifying the accounting system, and analysing the im-

plementation of the standards. The Accounting Regulatory Department also supervises the quality of

accounting information and regulates the accounting profession. The Supervision Department of the

MoF is in charge of the supervision of the financial reporting of all entities, within the Chinese territory,

including listed companies. The MoF also supervises all auditing firms within Chinese boundaries in-

cluding those firms that provide audit services to listed companies.

18. The CSRC is responsible for regulating China’s securities and futures markets, approving direct or indi-

rect issuance, or listing or trading, of securities by Chinese companies, establishing mechanisms for co-

operation with securities regulators in other countries or regions on cross-border regulation, and re-

viewing and approving, together with the MoF, applications from accounting firms for licenses to prac-

tice securities and futures business. The CSRC supervises listed entities in accordance with the provi-

sions set out in the Securities Law which requires listed companies to disclose their annual and interim

financial statements to the CSRC. The Accounting Department of the CSRC focuses on examining the

integrity of the financial reports of listed companies to ensure that public investors get a thorough un-

derstanding of the financial information published by listed companies.

IV Evolution in the process of convergence of ASBEs to IFRS

19. According to the statutory framework, the MoF is primarily responsible for regulating accounting prac-

tices in China. The responsibilities of the MoF include setting standards, a function which is performed

by the Accounting Regulatory Department and the Chinese Accounting Standards Committee (CASC).

In 2006, the CASC and the IASB signed a joint communiqué on convergence of accounting standards.

Members of the CASC have worked together with IASB members to ensure that the objective of conver-

gence is achieved. In April 2010 the MoF issued a “Roadmap for Continuing Convergence of ASBEs

with IFRS “ (Annex I) which reiterates the MoF’s commitment to continue the process of convergence

to IFRS.

20. The ASBEs comprise one Basic Standard, 38 specific standards and Implementation Guidance

which contain all the principles mentioned under IFRS. The Implementation Guidance follows IFRS

principles, with less detailed content in some cases. The Implementation Guidance is part of the legisla-

tion promulgated by the MoF and is therefore mandatory for all companies that apply the ASBEs. In

addition, the Accounting Regulatory Department of the MoF has issued an Interpretation Book of AS-

BEs, containing examples of how the standards are applied which were included in the IFRSs them-

selves but were not included in the Chinese standards and Implementation Guidance. All these individ-

ual items taken together (including the implementation Book) of ASBEs are substantially identical to

the IFRSs.

21. As of 31 December 2010, almost all differences between the ASBEs and the IFRS have been eliminated.

The major difference remaining relates to the reversal of impairment of long-term assets, which is not

7

allowed by the ASBEs. Retention of this difference is mainly due to analysis done by the Accounting

Regulatory Department of the MoF which concludes that there is significant potential for companies to

use the reversal of such impairment charges as a means of manipulating earnings. Consequently the

MoF does not expect to eliminate this difference in the near future. Other more minor differences exist

as well, a complete list of which has been provided to us by the Accounting Regulatory Department of

the MoF and is attached as Annex II to this report. Most of the remaining differences relate to the re-

moval of alternative treatments in some standards or some missing requirements in cases where the

type of transactions concerned does not exist in China. Such differences are not considered to amount

to non-compliance with IFRS.

22. The MoF has indicated to us that all current IFRS standards with an effective date before 1 January

2011 are subject to adoption as ASBEs. The Accounting Regulatory Department is continuously moni-

toring developments in IFRS to ensure continued convergence with all newly issued standards. The

MoF has set up research teams to discuss issues and perform a preliminary impact assessment based

on feedback received from companies and in cooperation with the CSRC and related regulators in the

banking and insurance areas.

23. Although not identical to IFRS, the ASBEs nonetheless adopt the principles contained in IFRS. As part

of the convergence process, a number of accounting issues have been identified and raised with the

IASB which result from the unique circumstances and environment that exist in China. Such issues in-

clude the disclosure of related party transactions, fair value measurements and business combinations

of entities under common control. The IASB officially released the revised IAS24 Related Party Disclo-

sures on 4 August 2009 which fundamentally removed the remaining barriers to convergence between

ASBEs and IFRSs in this particular area.

24. Representatives of the MoF meet with the IASB twice a year and Chinese members sits on the IFRS

Trustee, IASB , IFRS Advisory Council and IFRS Interpretation Committee. The MoF has been encour-

aging companies and accounting firms to comment to the IASB exposure drafts and discussion papers

and to become more heavily involved in the debate regarding IFRS. This international exchange of ex-

perience is thought to be vital for international convergence and should not, as far as the Chinese are

concerned, be a one way process. The IASB has also identified a number of accounting issues where

China, because of its unique circumstances and environment, could be particularly helpful in finding

high quality solutions for IFRSs.

25. China maintains its involvement in the IASB’s accounting projects. Regarding IFRS 9 – Financial in-

struments, the MoF has expressed some concerns about the impairment model currently proposed in

the standard. The MoF is closely following developments in the other phases of the financial instru-

ments project and will decide whether to adopt IFRS 9 when the whole project is finalised.. Other pro-

jects currently on the IASB’s agenda regarding revenue recognition and lease accounting are also being

carefully analysed in China and comment letters are being prepared for the IASB.

V Enforcement experience of the ASBEs

26. The role of supervising the financial information issued by entities in China to the market is performed

by the MoF and the CSRC. The supervision function is performed by the MoF pursuant to the Account-

ing Law and its scope comprises all entities filing financial reports. The CSRC supervisory function

8

arises from the Securities Law and its scope is limited to listed entities and securities and futures com-

panies.

27. The ASBEs were applied for the first time by Chinese listed entities for financial years commencing on

or after 1 January 2007. The scope of their application has been extended progressively each year to

now include all large and medium sized non-listed state owned enterprises, all non-listed commercial

banks, related financial institutions and all non-listed commercial insurance companies, rural credit

cooperatives and all other large and medium sized enterprises.

Ministry of Finance – enforcement activities

28. Enforcement of financial reporting requirements is undertaken by the Supervision Department of

the MoF which has a structure comprising some 35 commissioner officers and local offices employing

around 1200 inspectors. Commissioner offices are responsible for the supervision of the financial re-

porting on behalf of the MoF at the national level, while local financial departments supervise at the lo-

cal level. The Supervision Department of the MoF co-ordinates the enforcement process performed in

the territories by preparing guidance on how the process should be conducted. In addition, the Super-

vision Department also ensures co-ordination of enforcement activities for listed companies with the

CSRC. The commissioner offices focus on the application of the ASBEs by listed companies and state-

owned enterprises, and the audit practices of accounting firms which perform audit for listed compa-

nies. Since 2006, the commissioner offices have reviewed about 300 listed companies.

29. The selection of entities subject to the review process is based on different criteria including random

selection, specific situations or macro trends identified by both the Accounting Regulatory Department

and the Supervision Department of the MoF. The inspections consist generally of full reviews of the fi-

nancial statements and the preparation of reports on the internal controls of the companies selected. If

infringements are detected, the inspection might be further extended to the audit firm of the company

under review. Actions available to the enforcer range from corrections of the financial statements and

public announcements to requests to modify the audit opinion, cash penalties for practitioners and en-

terprises, and revocation of the qualifications of accountants, auditors or accounting firms.

30. The MoF conducts quality reviews of accounting information and of the operations of accounting

firms each year, and publishes an annual Accounting Information Quality Review Report regarding the

implementation of the Accounting Law of the PRC, of the Certified Public Accountants Law of the PRC,

the ASBEs, and the Practice Guidelines for Certified Public Accountants. The quality reviews are organ-

ized by the MoF, and conducted by the commissioner offices and local financial departments. The MoF

has already published 19 reports and those documents are available on the MoF’s website

(www.mof.gov.cn). As stated in Reports no.18 and no.19 published by the MoF on 9 November 2010,

the commissioner offices of the MoF have reviewed 78 enterprises and 43 accounting firms, and local

offices have reviewed 17 o89 enterprises (listed and non-listed) and 543 accounting firms. The review

concluded that most of the companies concerned had established effective internal control systems,

had complied with the Accounting Law of the PRC and the ASBEs, and that the risk management and

operating quality of the accounting firms had been enhanced. Only a few enterprises were found to

have deficiencies in their implementation of the regulation, and more specifically in the areas of inter-

nal control, financial management and the application of accounting principles.

31. The Accounting Regulatory Department of the MoF also plays a role in the assessment of the applica-

tion of accounting standards by reviewing a selected number of individual and consolidated financial

statements of listed and large or medium-sized companies. On the basis of this review, the Accounting

9

Regulatory Department issues a report every year on the implementation of the ASBEs. The conclu-

sions of the review are discussed with the Supervision Department to identify areas where the enforce-

ment process on the financial information reported for the following year should be concentrated.

32. The most recent report available is the “Analysis Report on the Implementation of Accounting Stan-

dards for Business Enterprises by Companies Listed in Mainland China in 2009”. The main conclu-

sions of this report were included in our progress report published in November 2010 (CESR 10-1301).

The report indicates that the ASBEs had been effectively implemented by over 1 700 listed companies

and that the process had been smooth and effective over the past three years. The report also identified

some areas where improvements were required, such as: fair value measurement and disclosure, im-

pairment of assets, business combinations, recognition of provisions for restructuring and onerous con-

tracts, capitalisation of development costs.

CSRC – enforcement activities

33. The CSRC is the regulator of the Chinese securities and futures markets. It has established an inte-

grated supervision system consisting of three levels:

a. The Accounting Department of CSRC charged with the identification of the main issues

and trends and with providing technical guidance to and ensuring co-ordination of the

CSRC’s regional offices or branches and the stock exchanges, and which organizes inspec-

tion teams to perform regular on-site comprehensive inspections or special inspections of

audit firms, while maintaining continuous off-site supervision of firms;

b. The CSRC regional offices (36 branches): in charge of monitoring compliance by listed en-

tities and the general supervision of audit firms; and

c. The stock exchanges (Shanghai and Shenzhen): responsible for reviewing and checking

the financial information provided by listed entities and who have the power to perform

further enquiries into the companies concerned.

34. In terms of monitoring of the annual reports of the issuers, the CSRC has established a regional respon-

sibility jurisdictional system via a 3-tier system. The first tier is the Stock Exchange and their responsi-

bility includes monitoring compliance with information disclosure requirements by means of an on-

line review of the annual reports issued by listed companies, by urging listed companies to disclose sig-

nificant information on a timely and proper basis and carrying out detailed desk-top reviews after the

completion of annual report disclosure. The second tier of the process is the regional offices whose re-

sponsibility includes on-site inspections of target companies after publication of their annual reports.

The regional offices will determine which companies will be subjected to on-site inspections based on

any significant doubts raised as a result of the reviews of annual reports conducted elsewhere under the

regulatory system as well as on the basis of any reasonable doubts harboured by the regional offices

themselves. The third tier of the system is represented by the Accounting Department of the CSRC,

which carries out individual reviews of the financial reports issued by listed companies. Such reviews

are conducted largely in accordance with guidelines which identify the key regulatory considerations

for the year in respect of disclosures of financial information relating to the implementation of the AS-

BEs.

35. The selection of the entities to be reviewed in any particular year is performed on the basis of the fol-

lowing principles: the stock exchanges and regional offices review the annual reports (including annual

10

financial statements) of all listed companies. The Department of Accounting of the CSRC performs “hot

reviews” on key areas identified in circulars and on special transactions considered to have a significant

influence on the financial performance of an entity. For 2010, the key areas monitored included: im-

pairment of assets, equity transactions, deferred tax recognition, revenue recognition and measure-

ment, presentation of comprehensive income, business combinations, disclosure of transactions with

related parties. In 2008, 2009 and 2010, 1547, 1 623 and 1 714 entities respectively were reviewed by

the stock exchanges and regional offices and 609, 665 and 1 356 entities reviewed by the CSRC. In

terms of infringements identified and actions taken, the statistics provided by the CSRC indicate 37 in-

fringements identified about which the CSRC communicated with the companies and required correc-

tion or future improvements to the financial statements.

36. In terms of the process of enforcement, the CSRC and MoF meet regularly to discuss complex issues.

Information on the main accounting issues identified during the enforcement process performed at the

level of the regional branches and the stock exchanges is collected and analysed by a Task Force in the

Accounting Department of the CSRC. This information is subsequently used for identifying trends and

areas for attention in future periods.

37. The Accounting Department of the CSRC has created a database which contains accounting issues and

enforcement cases related to the application of the ASBEs. Based on enforcement experience in 2010,

the main issues arising relate to the following areas:

a. accounting estimates, mainly related to impairment recognition on long-term assets (such

as goodwill and intangible assets) and credit loan provisions; insufficient disclosures of

the recoverable amount and reasons for impairment;

b. fair value recognition and measurement, such as the recognition and measurement of the

fair value for restricted shares is inconsistent in practice amongst companies; and

c. classification of financial instruments.

38.Following the issuance in October 2009 by the World Bank of its report entitled “Report on the obser-

vance of standards and codes (ROSC) – Accounting and Auditing” in which the Bank identified a num-

ber of areas of non-compliance in term of disclosures, the CSRC published several alerts and an-

nouncements to ensure companies took corrective measures.

VI Co-operation with other parties

39. The CASC and the China Auditing Standards Board signed joint declarations with the Hong Kong In-

stitute of Certified Public Accountants (HKICPA) on 6 December 2007 which officially record the mu-

tual recognition of each jurisdiction’s accounting and auditing standards. According to the information

provided in the Report prepared by the MoF, differences between the two sets of accounting standards

had gradually been reduced, promoting access by enterprises from Mainland China to the Hong Kong

capital market. We have been informed that as of 31 December 2010, due to the joint efforts of mem-

bers from the two parties the differences between ASBEs and HK GAAP have been eliminated.

40. Regulators in Mainland China and Hong Kong have been jointly exploring a possible mechanism

whereby financial statements prepared and audited under the rules applicable in one jurisdiction would

11

be accepted for the purpose of listing on a stock exchange in the other. Hong Kong Exchanges and

Clearing Limited (HKEx) announced its decision on 10 December 2010 to accept Mainland Chinese

ASBEs, auditing standards and audit firms for Mainland incorporated companies listed in Hong Kong.

The Financial Reporting Council of Hong Kong has established co-operation arrangements or mecha-

nisms with the MoF and the CSRC.

41. In practice, formal investigations into Mainland audit firms are carried out by the MoF and the CSRC,

either acting on a direct complaint or at the HK FRC’s or HK SFC’s (the Securities and Futures Com-

mission) request, to the extent permitted by Mainland laws. The responsibility for taking appropriate

disciplinary action and sanctions against Mainland audit firms also rests with the MoF and the CSRC,

which are government bodies independent of the profession.

42. Based on information received during a meeting held with the Hong Kong authorities (the Securities

and Futures Commission, the Financial Reporting Council, the Hong Kong Exchanges and Clearing

Houses and the Institute of Certified Accountants) we understand that in 2010 there were 163 Chinese

issuers listed on both Chinese and Hong Kong stock exchanges. In previous years, Chinese issuers have

had to file financial statements prepared under Hong Kong GAAP together with a reconciliation of any

financial information prepared using ASBEs to Hong Kong GAAP if issuers chose to include such in-

formation in their Hong Kong filings. As 2011 will be the first year when Chinese issuers will be permit-

ted to file financial statements prepared only using ASBEs, the HK FRC has indicated that they intend

to review all reports filed by Chinese issuers for that year.

VII Preliminary conclusions

43. On the basis of the information received during the meeting in China and subsequently, we can con-

clude that significant progress has been made in the process of convergence, and in particular with re-

spect to the following:

a. The Accounting Regulatory Department of the MoF has continued to work on the elimina-

tion of the differences between the ASBEs and IFRS. With the exception of one major dif-

ference with respect to the reversal of impairment, only a few minor differences remain, so

the level of convergence achieved could be considered satisfactory.

b. In terms of enforcement, significant steps have been undertaken to monitor entities lead-

ing to improvements in the application of the ASBEs by companies.

c. China is continuing its active involvement in IASB activities and will monitor the devel-

opment of the standards currently under revision in order to take the necessary steps to

further converge ASBEs to IFRS.

12

Annex I: Roadmap for continuing convergence of the Chinese Accounting Standards for Business Enter-

prises with the International Financial Reporting Standards.

Roadmap for Continuing Convergence of the Chinese Accounting Standards for Business Enterprises ("ASBEs") with the International Financial Reporting Standards ("IFRSs")

Convergence of local national accounting standards with the international standards is an essential tool to facilitate the growth of a nation's economy and to enhance its adaptability to the economic globalization. Since 2005, China has commenced the process of converging the ASBEs with the IFRSs. Subsequent to the broke out of the international financial crisis in 2008, the G20 summits and the Financial Stability Board ("FSB") initiated to establish a single set of high-quality global accounting standards to improve the transparency of accounting information which brought the importance of accounting standards to an unprecedented high level. The International Accounting Standards Board ("IASB"), the IFRSs setter, has taken a series of important actions to improve the quality of accounting standards. In this context, China released the "Roadmap for Continuing Convergence of the ASBEs with the IFRSs" in response to G20 and FSB's recommendations for the implementation of the continuing convergence of the ASBEs with its international counterpart.

I. The ASBEs have achieved convergence with the IFRSs

In 2005, the Ministry of Finance ("MOF") concentrated its effort in finalizing the system of ASBEs based on the experiences drawn from different aspects of the accounting reforms implemented over the past years. During 2005, IASB sent specialists to work with the Accounting Regulatory Department of the MOF several times. On 8 November 2005, the IASB and the China Accounting Standards Committee ("CASC") signed a joint statement depicted that the ASBE system established by China has achieved convergence with the IFRSs. In addition, the IASB identified a number of accounting issues for which China, because of its unique circumstances and environment, could be particularly helpful to the IASB in finding high quality solutions for IFRSs. These include disclosure of related party transactions, fair value measurements and business combinations of entities under common control. IASB officially released the revised IAS24 Related Party Disclosures on 4 August 2009 which fundamentally removed non-convergence issues between the ASBEs and the IFRSs. In 2001, the IASB through its annual improvements project revised the IFRS 1 First-time Adoption of International Financial Reporting Standards, to allow a company recognizing the revaluation values ascertained during the corporate restructuring process as deemed cost for the preparation of its initial public offering with retrospective restatements. Such revision effectively rectified the accounting issues arising from corporate restructuring revaluations of Chinese enterprises' assets during the initial public offering process.

The ASBE system has been applied by all listed companies, certain non-listed financial institutions and significant state-owned enterprises (SOEs) from 1 January 2007. The scope of such application has been expanding in steps and it now covers almost all of the large and medium-sized enterprises. The process of the ASBE implementation has been proven to be smooth and effective over the past three years. Such implementation has played an important role in regulating the accounting activities, promoting the quality of accounting information and enhancing the capital market. In May 2008, IASB sent experts to conduct a field study of the ASBE implementation by the listed companies in China. The results further confirmed that the implementation of the ASBE system was smooth and effective. In October 2009, the World Bank also issued an assessment report on the status of the ASBE convergence with IFRSs and the effectiveness of its implementation in China. The report clearly stated that "the

13

Chinese strategy for improving the quality of accounting and auditing standards and practices has evolved as a good practice model that may be followed by other countries".

Hong Kong has begun to adopt the IFRSs since 2005. After the successful convergence of the ASBEs system with the IFRSs and its effective implementation, a joint declaration on the equivalence of the accounting standards of the mainland China and Hong Kong was signed on 6 December 2007 to officiate the mutual recognition of the accounting standards. The European Union ("EU") allowed the listed companies to adopt IFRSs to prepare their financial statements in 2005 for the first time. After making assessment on the progress of the accounting convergence and effectiveness of the related implementation in China by the European Commission, the Commission issued regulation on equivalence with accounting standars of a third country on 12 December 2008, recognizing the equivalence between ASBEs and the IFRSs adopted by EU. In addition, Chinese enterprises are allowed to file their financial statements prepared under the ASBEs when entering the EU capital markets during the transitional period from 2009 to the end of 2011.

All the aforementioned events clearly demonstrated the facts that full convergence of the ASBEs with the IFRSs and smooth and effective implementation by the listed companies and non-listed large and medium-sized enterprises in China were widely recognized both at home and abroad.

II. China supports the establishment of a single set of high-quality global accounting standards in response to the international financial crisis and proactively promotes the continuing convergence of the ASBEs with the IFRSs

In response to the international financial crisis, the G20 Washington summit held in November 2008 analyzes and summarizes profoundly root causes of the crisis; put forward action plans which include improving the IASB governance and establishing a single set of high-quality global accounting standards. In June 2009, FSB, restructured from its predecessor Financial Stability Forum ("FSF"), held its inaugural meeting in Basel of Switzerland. FSB decided to set up a Standard Implementation Committee to promote convergence of various countries' national accounting standards with the IFRSs. At the G20 Pittsburgh summit held in September 2009, the G20 again urged the international accounting standard setter to work harder to establish a single set of high-quality global accounting standards through the independent standard setting procedures.

Based on the requirements of the G20 and FSB, the IASB proactively studied the accounting issues unveiled by this financial crisis. Plenty of work has been carried out to enhance the IFRSs with remarkable achievements which include the followings:

(1) the establishment of the Financial Crisis Advisory Group ("FCAG") which put forward the systematic approach to improve the financial reporting in response to the financial crisis;

(2) the setting of the accounting standards on fair value measurement which provide a standardized set of guidance for fair value measurement;

(3) reducing the complexity of accounting requirements for financial instruments under a comprehensive project with the aim to simplify the accounting standards on classification, measurement, impairments and hedge accounting of financial instruments;

(4) the comprehensive revision of accounting standards on financial statements presentation and consolidated financial statements which clarified the accounting treatments of off-balance-sheet transactions and special purpose entities;

(5) the acceleration of the pace in the standard setting of various projects, such as insurance contract standard.

14

The above convergence projects are to be completed by the end of June 2011. China fully praises and supports the unremitting efforts made by the IASB in response to the financial crisis and the implementation of the G20 and the FSB related recommendations.

As the largest developing country and emerging market economy in the world, China, has achieved convergence with the international accounting standards and undertaken continuous monitoring of any significant revisions and setting of the relevant accounting standards by the IASB. Certain project teams comprising of selected experts from both areas of accounting theories and practice were formed to carry out in-depth researches with reference to the practical circumstances in China. China also set up the Asian-Oceanian Standard Setters Group ("AOSSG") amongst the accounting standard setter of Asian and Oceanian countries or regions to reflect the local situations and advices. China always insists that the accounting convergence required interaction between the participated countries. China also advocates that in order to improve the quality, insure authoritativeness and gain global recognition of the IFRSs, the prescribed standards should take full account the economic realities of the developing countries and in particular, the emerging market economies. As such, China can maintain its continuing accounting convergence status.

III. Schedule for continuing convergence of the ASBEs with the IFRSs

Continuing convergence of the ASBEs with the IFRSs will be maintained in line with the pace of the IASB's progress. Relevant improvement projects to the ASBEs are to be accomplished by the end of 2011. In the meantime, necessary promotion and training will be conducted to ensure that all listed companies and non-listed large and medium-sized enterprises gain an understanding of the changes to relevant accounting standards and apply them effectively.

The revised ASBE system will still consist of three parts, i.e., the Basic Standard, Specific Standards and Implementation Guidance. The Basic Standard establish a conceptual framework of specifying the fundamental requirements for accounting recognition, measurement and reporting and provide the direction in setting the Specific Standards. The Specific Standards prescribe the specific requirements for accounting recognition, measurement and reporting of various types of transactions carried out by the entity. The Implementation Guidance provides illustrative examples and practical guidelines for addressing the important and difficult issues related to the Specific Standards.

ESMA • 11-13 avenue de Friedland • 75008 Paris • France • Tel. +33 (0) 1 58 36 43 21 • www.esma.europa.eu

Annex II: List of detailed differences between the Chinese Accounting Standards for Business Enterprises and the International Financial Re-

porting Standards – as prepared and provided by the MoF.

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference

Basic Standard IAS 1 ASBE - states the use of prudence. IAS - states the importance of fair presentation.

No change CAS 30 is the equivalent standard to IAS 1. There’s no difference between these two standards.

ASBE 2 - Long term Equity Investments

IAS 27

Separate financial statements of the Parent: ASBE 2 requires subsidiaries to be stated at cost. ASBE 2 requires use of equity method when taking into account associates and jointly controlled entities in the parent's separate financial statements. IAS 27 - account for subsidiaries, associates or JCEs to be stated at cost, and then carried using equity method or in accordance with IAS 39 (fair value). ASBE 2 does not address the accounting treatment for jointly controlled assets. Consolidation: ASBE only allows the equity method to account for a jointly controlled entity. Jointly controlled operations/assets: ASBE 2 does not recognise the accounting treatment for jointly controlled operations/assets

Amendments to IAS 27: June 2009 It has not been included in the ASBE, but the accounting treatment is the same.

Separate financial statements of the Parent: Same difference exist Jointly controlled operations/assets: Difference eliminated

16

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference

ASBE 3 - Investment Property

IAS 40

IAS 40 has a greater scope and states that uniformity of accounting treatment should be used. Land use rights held for rental purposes can be classified using cost model or fair value.

No change Difference eliminated

ASBE 4 - Fixed Assets

IAS 16 ASBE only allows for the cost model, not the revaluation model. IAS 16 allows for either cost or revaluation model.

No change ASBE chooses one model among the two alternatives.

ASBE 5 - Biological Assets

IAS 41

ASBE 5 states that the cost model should be used, unless there is evidence that the fair value can reliably obtained continually. IAS 41 states that the fair value be used unless it is clearly unreliable.

No change

ASBE 6 - Intangible Assets

IAS 38

ASBE 6 only allows for cost model whereas IAS 38 allows for cost or revaluation model (where fair value can be determined by pricing in an active market)

No change ASBE chooses one model among the two alternatives.

ASBE 7 - Exchange of non-monetary assets

IAS 16, IAS 38

Exchanges of non monetary assets are dealt with in IAS 16 (propeerty, plant and equipment) and 38 (intangible assets) as the need to create a separate accounting standard was not seen as important. Whilst the exchange of similar non monetary assets in IAS 16 and 38 is similar to ASBE 7 (for the assets to be recognised at fair value, they require the commercial substance test to be applied), this is not extended to IAS 18, which only recognises fair value on exchange of dissimilar non monetary assets.

No change Accounting principles for exchange of similar or dissimilar non-monetary assets stated in IFRS and ASBE are the same.

ASBE 8 - Asset Impairment

IAS 36 IAS 36 prohibits reversal of impairment loss for goodwill, but ASBE 8 prohibits reversal

No change Same difference exist

17

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference of all impairment loss

ASBE 9 - Employee Benefits

IAS 19 Does not recognise a defined benefit liability and the resulting expense throughout the service period of related employees

No change ASBE 9 does not recognise defined benefit liability because defined benefit plan does not exist in China.

ASBE 10 - Enterprise Annuity Fund

IAS 26 ASBE 10 does not recognise defined benefit plans because they do not exist in China.

No change

ASBE 11 - Share based payment

IFRS 2

ASBE 11 only covers accounting for share-based payment transactions for services, whereas IFRS 2 covers services and goods. Equity settled with cash alternatives are not addressed in ABSE 11.

Amendments - Vesting conditions and

cancellations (Dec 2008) - Group cash-settled

transactions(March 2010)

ASBE 11 only covers accounting for share-based payment transactions for services, whereas IFRS 2 covers services and goods: currently share-based payment for exchange of goods is not allowed in China. Equity settled with cash alternatives: difference eliminated. Amendments: No difference.

ASBE 12 - Debt Restructuring

IAS 39

IAS 39 is broadly similar to ASBE 12. However, IAS 39 states that financial assets (including debts) should be derecognised when: - the contractual rights to the cash flows from the debt expire - an issuer transfers the debt and transfers in substance the risks and rewards of the debt. ASBE 12 does not cover the above derecognition requirements nor the principles behind it.

No change Difference eliminated

ASBE - 13 Contingencies

IAS 37 No significant difference No change No difference

18

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference

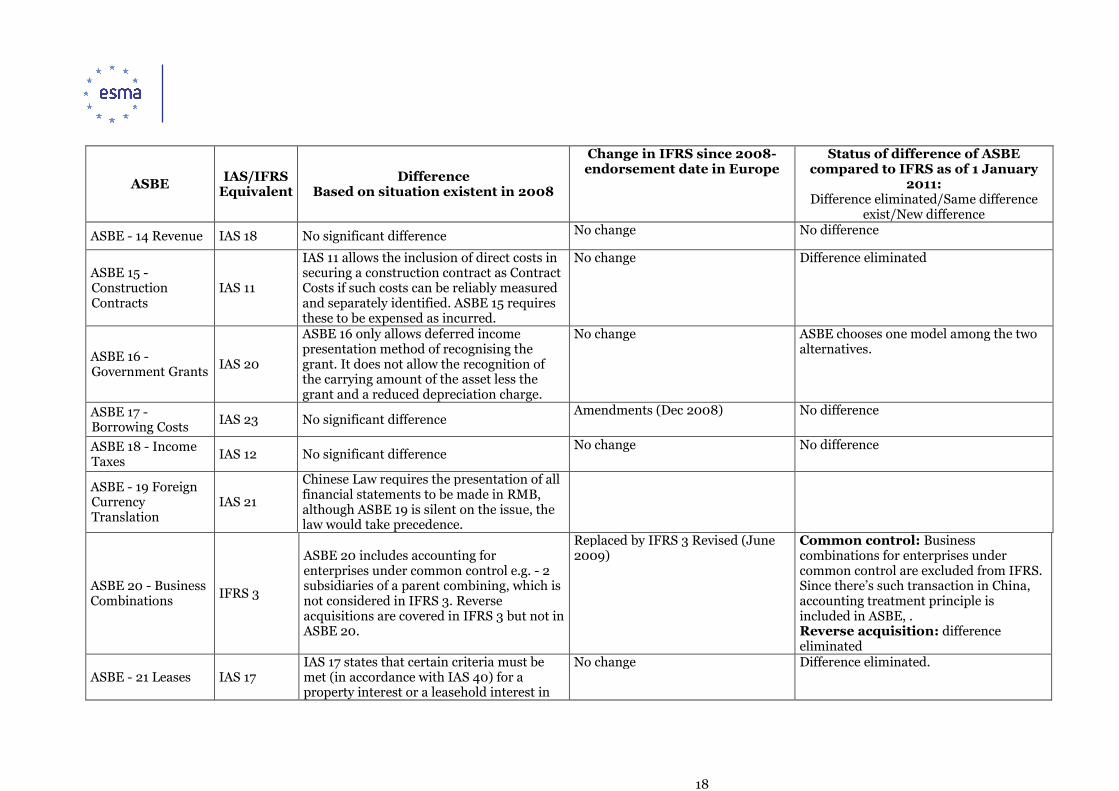

ASBE - 14 Revenue IAS 18 No significant difference No change No difference

ASBE 15 - Construction Contracts

IAS 11

IAS 11 allows the inclusion of direct costs in securing a construction contract as Contract Costs if such costs can be reliably measured and separately identified. ASBE 15 requires these to be expensed as incurred.

No change Difference eliminated

ASBE 16 - Government Grants

IAS 20

ASBE 16 only allows deferred income presentation method of recognising the grant. It does not allow the recognition of the carrying amount of the asset less the grant and a reduced depreciation charge.

No change ASBE chooses one model among the two alternatives.

ASBE 17 - Borrowing Costs

IAS 23 No significant difference Amendments (Dec 2008) No difference

ASBE 18 - Income Taxes

IAS 12 No significant difference No change No difference

ASBE - 19 Foreign Currency Translation

IAS 21

Chinese Law requires the presentation of all financial statements to be made in RMB, although ASBE 19 is silent on the issue, the law would take precedence.

ASBE 20 - Business Combinations

IFRS 3

ASBE 20 includes accounting for enterprises under common control e.g. - 2 subsidiaries of a parent combining, which is not considered in IFRS 3. Reverse acquisitions are covered in IFRS 3 but not in ASBE 20.

Replaced by IFRS 3 Revised (June 2009)

Common control: Business combinations for enterprises under common control are excluded from IFRS. Since there’s such transaction in China, accounting treatment principle is included in ASBE, . Reverse acquisition: difference eliminated

ASBE - 21 Leases IAS 17 IAS 17 states that certain criteria must be met (in accordance with IAS 40) for a property interest or a leasehold interest in

No change Difference eliminated.

19

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference land held under an operating lease to be recognised as an investment property. ASBE 6 states leasehold interests in land are to be accounted for as intangible assets unless they meet criteria for them to qualify as investment properties in accordance with ASBE 3.

ASBE 22 - Recognition and measurement of Financial Instruments

IAS 39 No significant difference

Amendments: - Reclassification of financial

instruments (Oct 2008) - Effective date and transition

(Sept 2009) - Embedded derivatives (Nov

2009)

Reclassification:. Embedded derivatives: No difference

ASBE 23 - Transfer of Financial Assets

IAS 39 No significant difference No change No difference

ASBE 24 - Hedging IAS 39 No significant difference

Amendment: - Recognition and measurement:

eligible hedged items (Sept 2009)

No difference

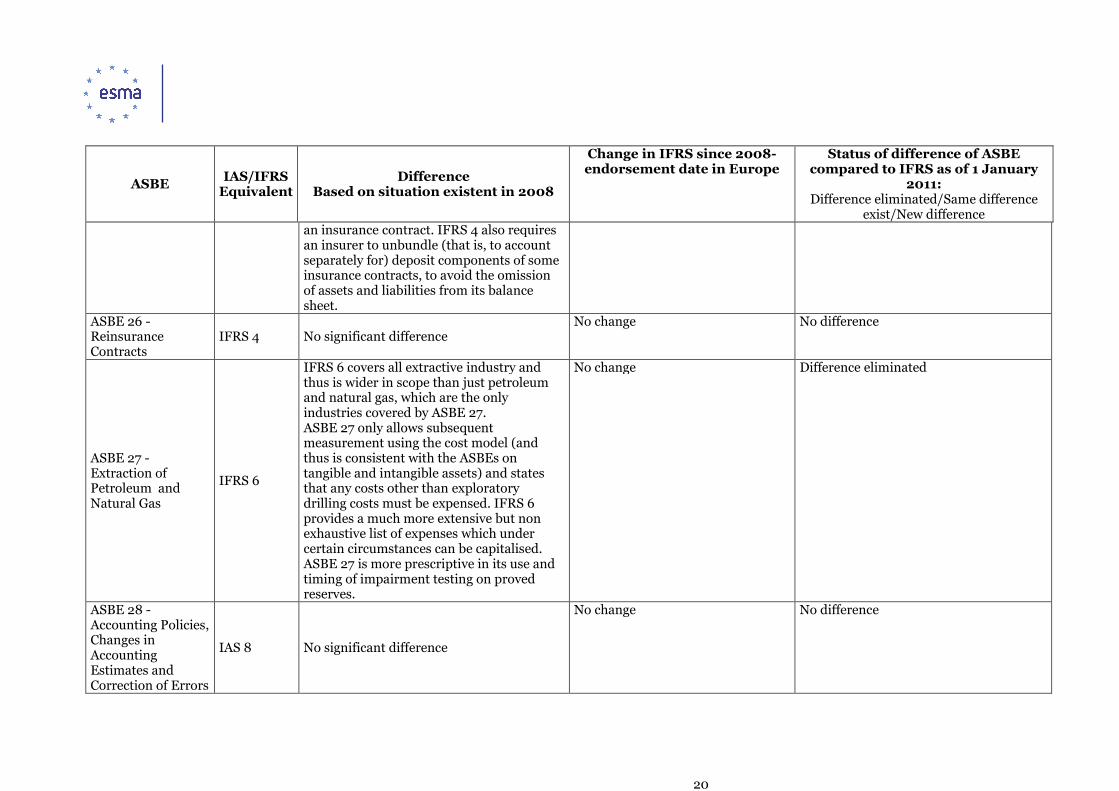

ASBE 25 - Direct Insurance Contracts

IFRS 4

ASBE 25 has specific requirements applying to recognition of income, reserves and costs, whereas IFRS 4 allows insurers to use existing accounting practice. IFRS 4 has additional guidance surrounding unbundling. It also clarifies that an insurer need not account for an embedded derivative separately at fair value if the embedded derivative meets the definition of

No change Difference eliminated

20

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference an insurance contract. IFRS 4 also requires an insurer to unbundle (that is, to account separately for) deposit components of some insurance contracts, to avoid the omission of assets and liabilities from its balance sheet.

ASBE 26 - Reinsurance Contracts

IFRS 4 No significant difference No change No difference

ASBE 27 - Extraction of Petroleum and Natural Gas

IFRS 6

IFRS 6 covers all extractive industry and thus is wider in scope than just petroleum and natural gas, which are the only industries covered by ASBE 27. ASBE 27 only allows subsequent measurement using the cost model (and thus is consistent with the ASBEs on tangible and intangible assets) and states that any costs other than exploratory drilling costs must be expensed. IFRS 6 provides a much more extensive but non exhaustive list of expenses which under certain circumstances can be capitalised. ASBE 27 is more prescriptive in its use and timing of impairment testing on proved reserves.

No change Difference eliminated

ASBE 28 - Accounting Policies, Changes in Accounting Estimates and Correction of Errors

IAS 8 No significant difference

No change No difference

21

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference ASBE 29 - Events after the Balance Sheet Date

IAS 10 No significant difference No change No difference

ASBE 30 - Presentation of Financial Statements

IAS 1 ASBE 30 is more prescriptive, only allowing expenses to be analysed by function, rather than nature of expenses or function.

Amendments to IAS 1: A revised presentation (Dec 2008)

ASBE chooses one model among the two alternatives. ASBE 30 requires expenses to be classified based on function in the Income Statement, and allows expenses to be disclosed based on nature in the notes.

ASBE 31 - Cash Flow Statements

IAS 7 ASBE 31 only allows the direct method of reporting cash from operating activities, whilst IAS allows both direct and indirect.

No change ASBE requires the direct method when preparing the Cash Flow Statement, and requires the indirect method of reporting cash from operating activities in the notes.

ASBE 32 - Interim Financial Reporting

IAS 34

Unlike IAS 34, ASBE 32 does not require a statement of changes in equity to be presented, but the interim balance sheet, income statement and cash-flow statement must be presented in a form compliant with that of annual financial statements, as opposed to the condensed version allowed by IAS 34.

No change

ASBE 33 - Consolidated Financial Statements

IAS 27

ASBE 33 states that reporting periods of the parent and subsidiaries must be the same, whereas IAS 27 allows the reporting date of subsidiaries and parent to be up to 3 months apart.

Amendments to IAS 27: June 2009 All companies in China has the same reporting period according to the Accounting Law of P.R.C. Therefore, it is not a difference.

ASBE 34 - Earnings per share

IAS 33

ASBE 34 requires an earnings per share calculation only to be made from net profit or loss for the current period. In addition, IAS 33 requires basic and diluted EPS to be

No change .

22

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference calculated on profit for continuing and discontinuing operations.

ASBE 35 - Segmental Reporting

IAS 14 No significant difference Replaced by IFRS 8 (Nov 2007) No difference

ASBE 36 - Related Party Disclosures

IAS 24

State controlled entities are not exempted from being a related party under IAS 24. Under ASBE 36, state-controlled entities are “related parties” if and only if the 2 companies have common business transactions or investment transactions, therefore if the result of one company directly affects the result of the other company.

Revised standard (July 2010) Difference eliminated

ASBE 37 - Presentation of Financial Instruments

IAS 32, IFRS 7

No significant difference

Amendments: - Classification of financial

instruments (Oct 2008) - Puttable financial instruments

(Jan 2009) - IFRS 7 : improvement of

disclosures (Nov 2009) - Classification of rights issues

(Dec 2009)

Reclassification:. Puttable financial instruments: no difference IFRS 7: No difference Classification of rights issues: No difference

ASBE 38 - First time adoption of ASBEs

IFRS 1 No significant difference

Revised IFRS 1 ( Nov 2009) Amendments: - Additional exemptions (June

2010)

No difference

IFRS 5 No equivalent standard No change Difference eliminated (please refer to

ASBE 4)

23

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference

IAS 29 No equivalent standard

No change There is no separate specific standard under the ASBE dealing with the financial reporting in hyperinflationary economies. As the economy in China is not consi-dered as a hyperinflationary economy, only "ASBE No. 19 – Foreign Currency Translation" and its application guidance specify the restatement and translation of the financial statements of foreign opera-tions in hyperinflationary economies.

SIC 10 No comment provided in 2008 No change No difference

SIC 12 No comment provided in 2008 No change No difference

SIC 13 No comment provided in 2008 No change No difference

SIC 15 No comment provided in 2008 No change No difference

SIC 21 No comment provided in 2008 No change No difference

SIC 25 No comment provided in 2008 No change No difference

SIC 27 No comment provided in 2008 No change No difference

SIC 29 No comment provided in 2008 No change No difference

SIC 31 No comment provided in 2008 No change No difference

24

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference

SIC 32 No comment provided in 2008 No change No difference

IFRIC 1 No comment provided in 2008 No change No difference

IFRIC 2 No comment provided in 2008 No change No difference

IFRIC 4 No comment provided in 2008 No change No difference

IFRIC 5 No comment provided in 2008 No change No difference

IFRIC 6 No comment provided in 2008 No change Currently, there are no such transactions

in China.

IFRIC 7

No comment provided in 2008 No change There is no separate specific standard under the ASBE dealing with the financial reporting in hyperinflationary economies. As the economy in China is not consi-dered as a hyperinflationary economy, only "ASBE No. 19 – Foreign Currency Translation" and its application guidance specify the restatement and translation of the financial statements of foreign opera-tions in hyperinflationary economies.

IFRIC 8 No comment provided in 2008 No change No difference

IFRIC 9 No comment provided in 2008 No change No difference

IFRIC 10 No comment provided in 2008 No change No difference

25

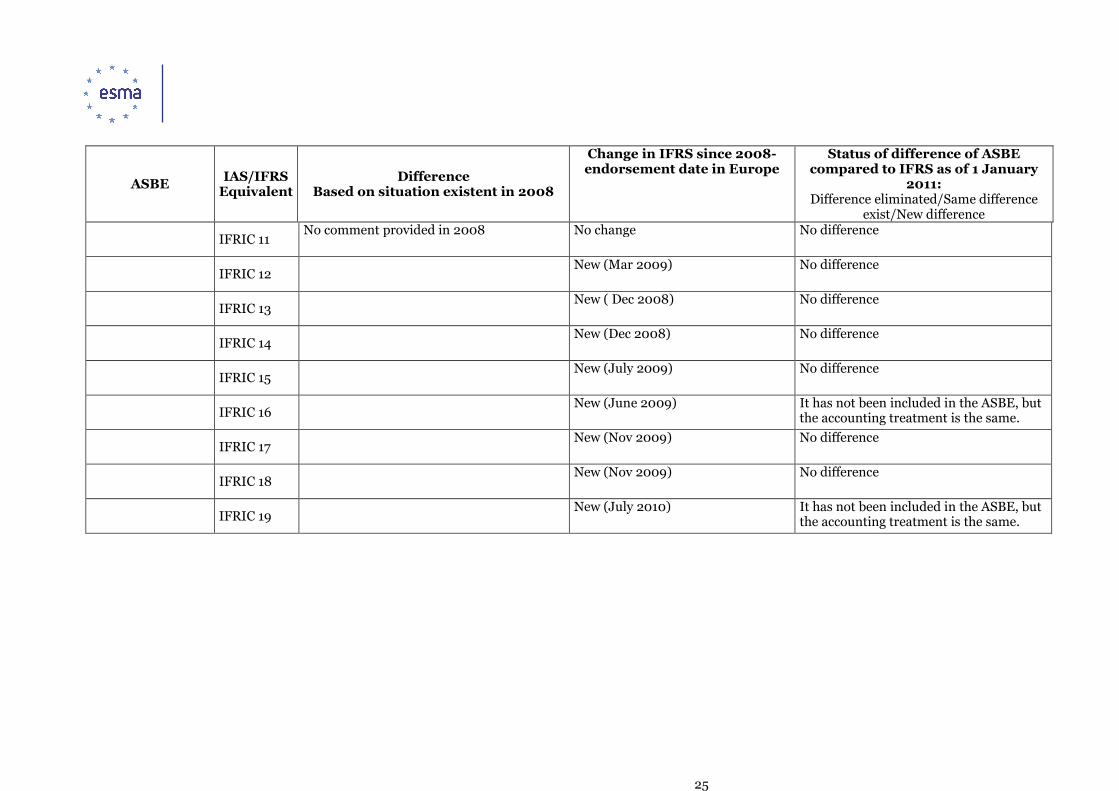

ASBE IAS/IFRS Equivalent

Difference Based on situation existent in 2008

Change in IFRS since 2008- endorsement date in Europe

Status of difference of ASBE compared to IFRS as of 1 January

2011: Difference eliminated/Same difference

exist/New difference

IFRIC 11 No comment provided in 2008 No change No difference

IFRIC 12 New (Mar 2009) No difference

IFRIC 13 New ( Dec 2008) No difference

IFRIC 14 New (Dec 2008) No difference

IFRIC 15 New (July 2009) No difference

IFRIC 16 New (June 2009) It has not been included in the ASBE, but

the accounting treatment is the same.

IFRIC 17 New (Nov 2009) No difference

IFRIC 18 New (Nov 2009) No difference

IFRIC 19 New (July 2010) It has not been included in the ASBE, but

the accounting treatment is the same.