©2010 LarsonAllen LLP 1 An Introduction to and Initial Results from Our Operational Excellence...

76

©2010 LarsonAllen LLP 1 An Introduction to and Initial Results from Our Operational Excellence Journey

-

Upload

silas-charles -

Category

Documents

-

view

214 -

download

0

Transcript of ©2010 LarsonAllen LLP 1 An Introduction to and Initial Results from Our Operational Excellence...

©20

10 L

arso

nA

llen

LLP

1

An Introduction to and Initial Results from Our Operational Excellence Journey

©20

10 L

arso

nA

llen

LLP

2

Introduction

• Share LarsonAllen’s Operational Excellence journey

• Like Lean, it’s not:– The only way– The “best” way

• It’s just “our” way– 20% is tools & techniques; 80% is people & culture; a

“can do” attitude– Hunger to find a “better” way

©20

10 L

arso

nA

llen

LLP

3

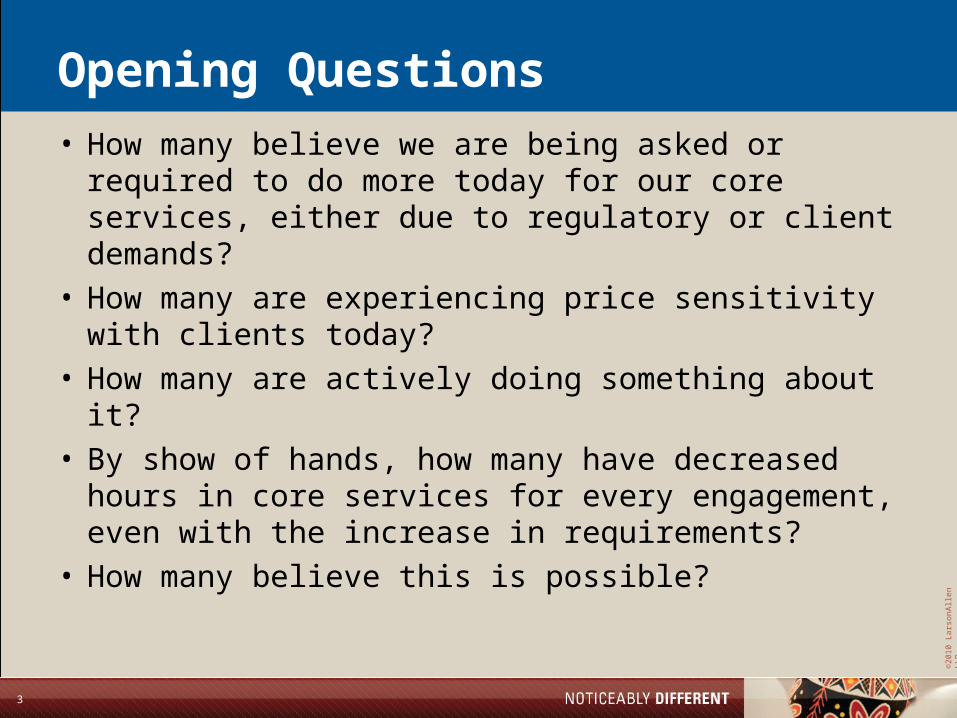

Opening Questions

• How many believe we are being asked or required to do more today for our core services, either due to regulatory or client demands?

• How many are experiencing price sensitivity with clients today?

• How many are actively doing something about it?• By show of hands, how many have decreased

hours in core services for every engagement, even with the increase in requirements?

• How many believe this is possible?

©20

10 L

arso

nA

llen

LLP

4

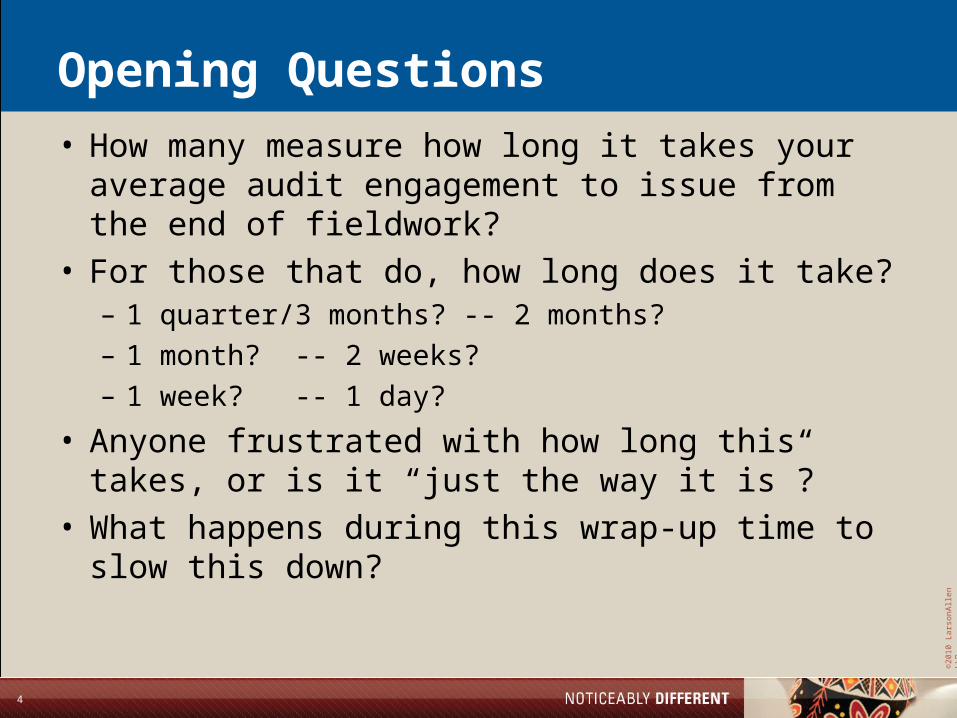

Opening Questions

• How many measure how long it takes your average audit engagement to issue from the end of fieldwork?

• For those that do, how long does it take?– 1 quarter/3 months? -- 2 months?– 1 month? -- 2 weeks?– 1 week? -- 1 day?

• Anyone frustrated with how long this takes, or is it “just the way it is”?

• What happens during this wrap-up time to slow this down?

©20

10 L

arso

nA

llen

LLP

5

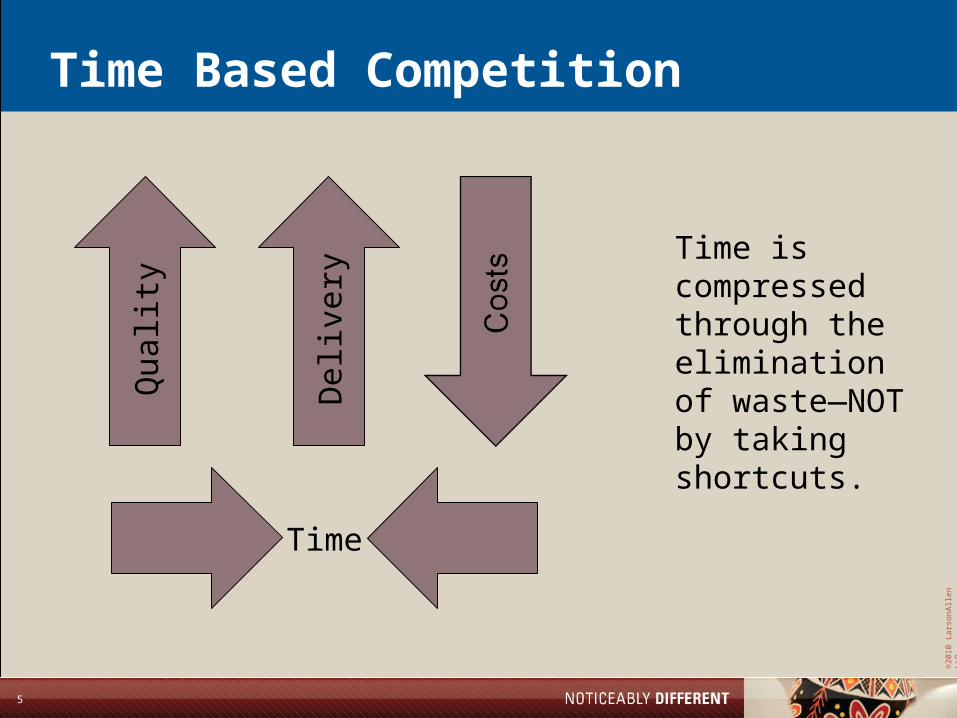

Time Based Competition

Qua

lity

Del

iver

y

Time

Time is compressed through the elimination of waste—NOT by taking shortcuts.

©20

10 L

arso

nA

llen

LLP

6

Continuous Improvement—Waste Reduction

VA WasteTypicalCompany

VATraditionalOperationalImprovement

Lean

Waste

OriginalLead Time

MinorImprovement

MajorImprovementVA Waste

©20

10 L

arso

nA

llen

LLP

7

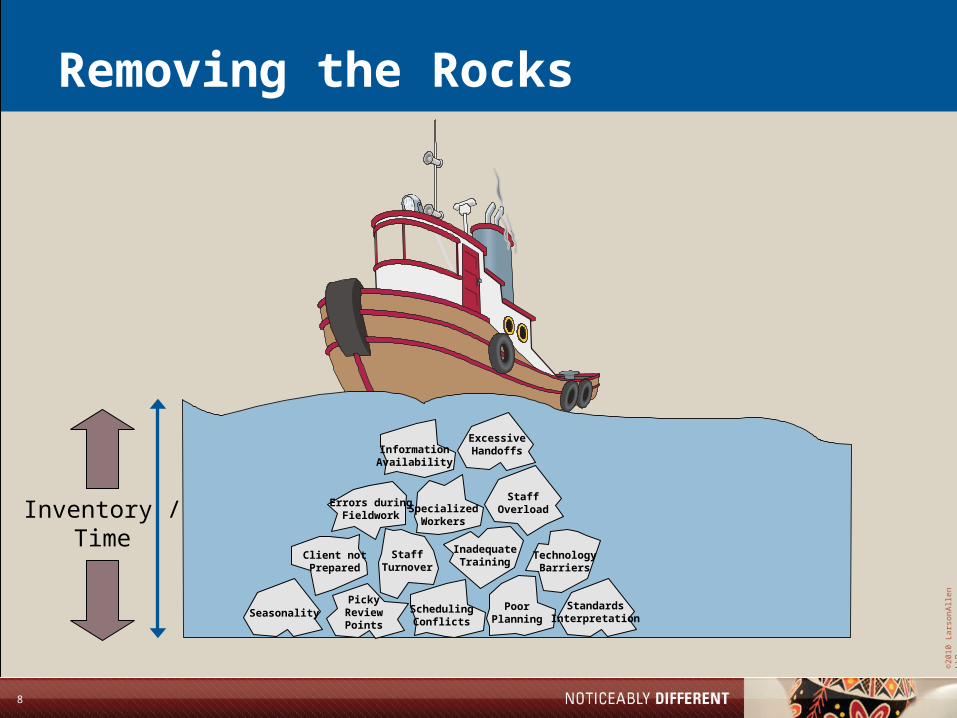

Phases of Operational Excellence

Remove the rocks

Reduce variation

Stabilize

Move the furniture

5 years

Repeat

Few-broad

Many-narrow

©20

10 L

arso

nA

llen

LLP

8

Removing the Rocks

Inventory /Time

SeasonalityPicky

ReviewPoints

SchedulingConflicts

PoorPlanning

StandardsInterpretation

Client notPrepared

StaffTurnover

InadequateTraining

TechnologyBarriers

Errors duringFieldwork

SpecializedWorkers

StaffOverload

ExcessiveHandoffsInformation

Availability

©20

10 L

arso

nA

llen

LLP

9

The Toyota Way

Overview*

*Some content from “The Toyota Way,” by Dr. Jeffrey Liker

©20

10 L

arso

nA

llen

LLP

10

The 14 Principles of the Toyota Way1. Long-term philosophy

2. Continuous flow

3. Pull systems

4. Level workload

5. Stop to fix problems

6. Standardized tasks

7. Visual control

8. Reliable and tested technologies

9. Leadership development

10. Team development

11. Respect for partners and suppliers

12. Go and see

13. Consensus decisions, rapid implementation

14. Learning organization and continuous improvement

McGraw-Hill Professional, 2004

©20

10 L

arso

nA

llen

LLP

11

Principle 1

Long-termPhilosophy

©20

10 L

arso

nA

llen

LLP

1212

Implementation Curve—Long-term view

1 2 3

Years Implementing Lean

OrganizationalAcceptance

©20

10 L

arso

nA

llen

LLP

13

Principle 2

ContinuousFlow

©20

10 L

arso

nA

llen

LLP

14

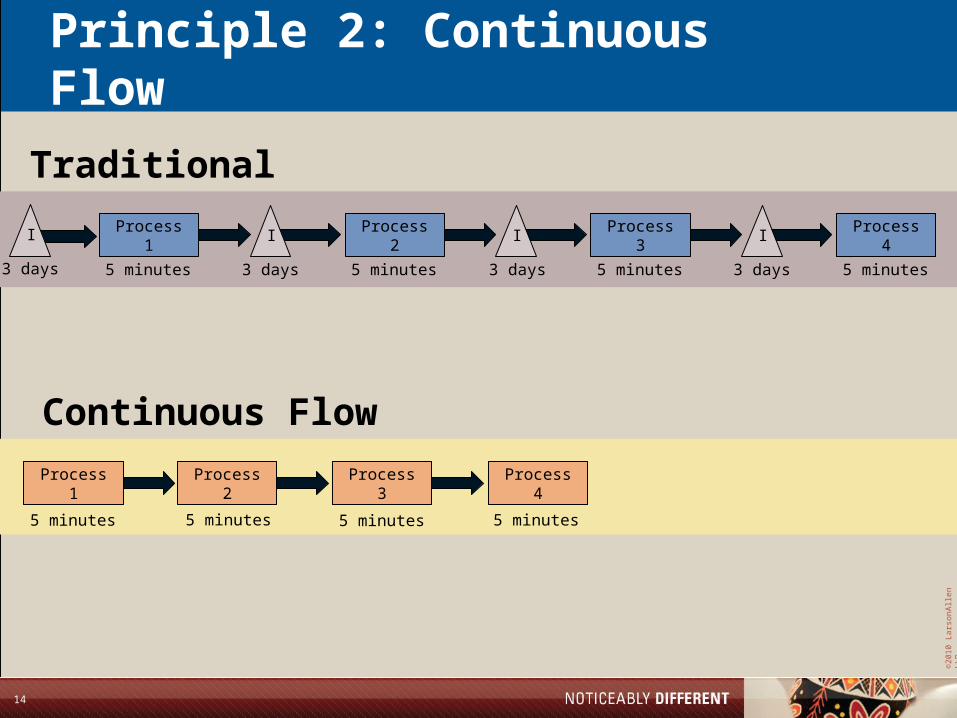

Principle 2: Continuous Flow

Process 1 I Process 2 I Process 3 I Process 4

Traditional

5 minutes 5 minutes 5 minutes 5 minutes3 days 3 days 3 days

I

3 days

Process 1 Process 2 Process 3 Process 4

Continuous Flow

5 minutes 5 minutes 5 minutes 5 minutes

©20

10 L

arso

nA

llen

LLP

15

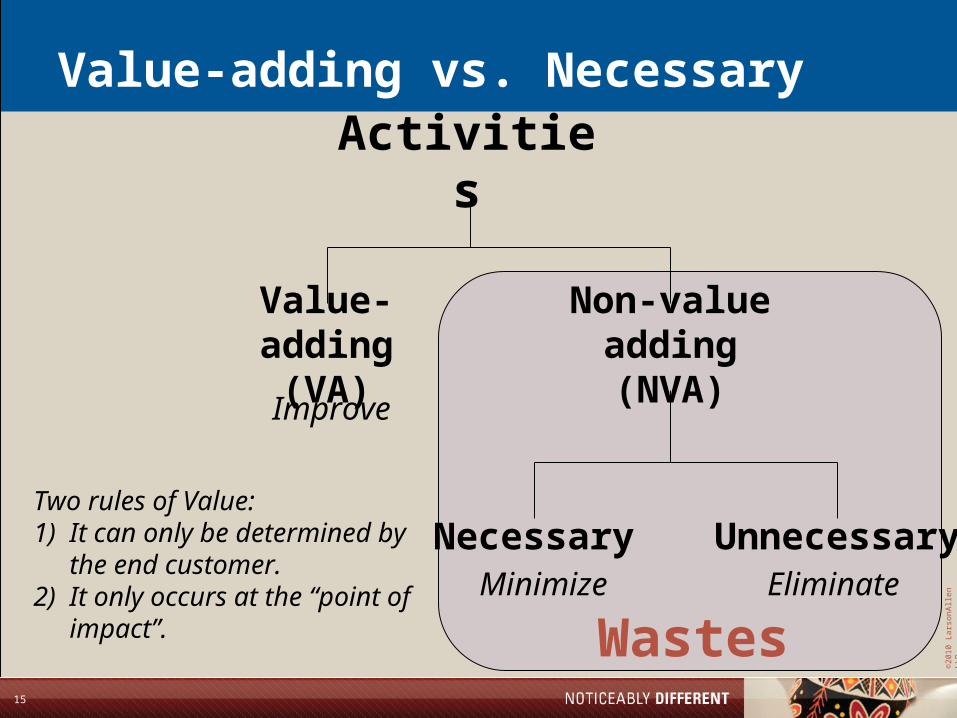

Value-adding vs. Necessary

Wastes

Necessary UnnecessaryEliminateMinimize

Two rules of Value:1) It can only be determined by

the end customer.2) It only occurs at the “point of

impact”.

Activities

Value-adding(VA)

Non-value adding(NVA)

Improve

©20

10 L

arso

nA

llen

LLP

16

Seven Wastes

• Waste of inventory• Waste of correction • Waste of transportation• Waste of over-processing• Waste of waiting• Waste of motion• All leading to …

the waste of a person

©20

10 L

arso

nA

llen

LLP

17

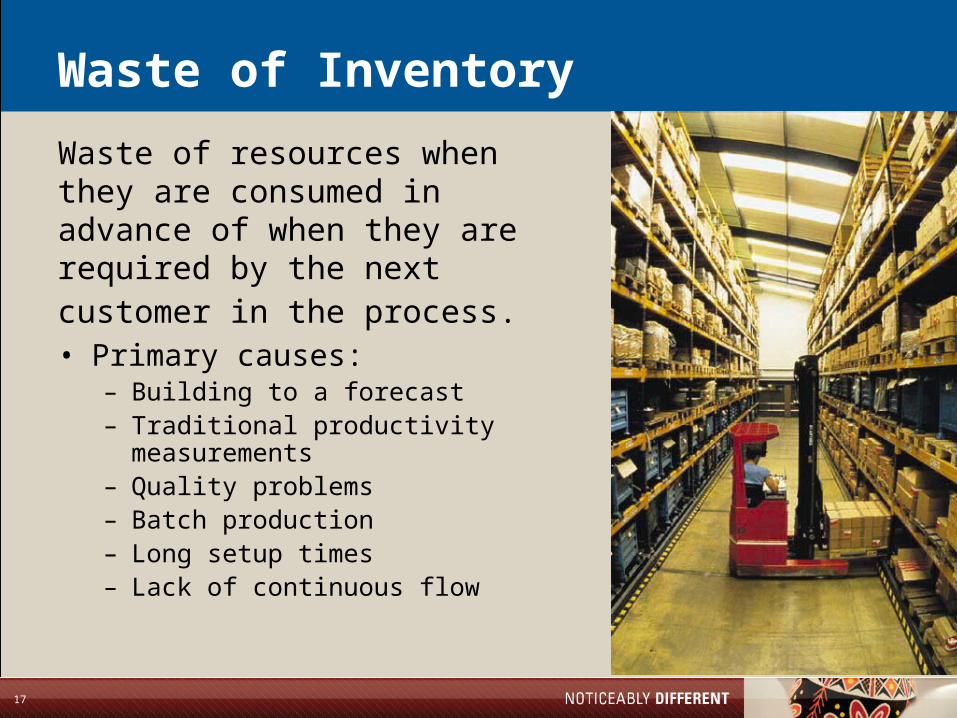

Waste of Inventory

• Primary causes:– Building to a forecast– Traditional productivity

measurements– Quality problems– Batch production– Long setup times– Lack of continuous flow

Waste of resources when they are consumed in advance of when they are required by the next customer in the process.

©20

10 L

arso

nA

llen

LLP

18

Waste of Correction

• Primary causes:– Lack of error proofing– Poor instructions and training– Lack of communication

between processes– Lack of standard work– Inadequate supplier quality– Need for adjustments

Waste that occurs when a product does not conform to proper specifications. The result could involve product rework or scrap.

©20

10 L

arso

nA

llen

LLP

19

Waste of Transportation

• Primary causes:– Inefficient facility layout– Inefficient facility location– Inefficient use of technology

Waste caused by unnecessary movement of material or product.

©20

10 L

arso

nA

llen

LLP

20

Waste of Over-Processing

• Primary causes:– Not identifying customer values– Not asking 5-why’s for a process

step– Variation within a process

Waste of unnecessary processes and operations.

©20

10 L

arso

nA

llen

LLP

21

Waste of Waiting

• Primary causes:– Operations not linked– Material and supplies do not arrive

in the quantity needed

Waste caused by not having all the material, supplies or information available exactly when needed for the worker to do their value-added job without interruption.

©20

10 L

arso

nA

llen

LLP

22

Waste of Motion

• Primary causes:– Inefficient workplace layout– Inefficient tools– Lack of standard work—

consistency

Waste caused by non-value added movement of workers and production machines.

©20

10 L

arso

nA

llen

LLP

23

Waste of Person

• Primary causes:– Lack of employee and

management involvement

Waste that is caused when a person performs any of the other seven wastes, thereby not being able to apply their knowledge and skills full-time to the task of adding-value.

©20

10 L

arso

nA

llen

LLP

24

Principle 4

LevelProduction

©20

10 L

arso

nA

llen

LLP

25

Principle 4: Level Production

• Enables continuous flow• Difficult, but critical to effective utilization of

resources• Internal policies and issues can lead to un-level

production– Scheduling– Batch processing– Process design

◊ .e.g. Lack of Interim Work

– Client mgmt practices

©20

10 L

arso

nA

llen

LLP

26

Principle 5

Stop and FixProblems

©20

10 L

arso

nA

llen

LLP

27

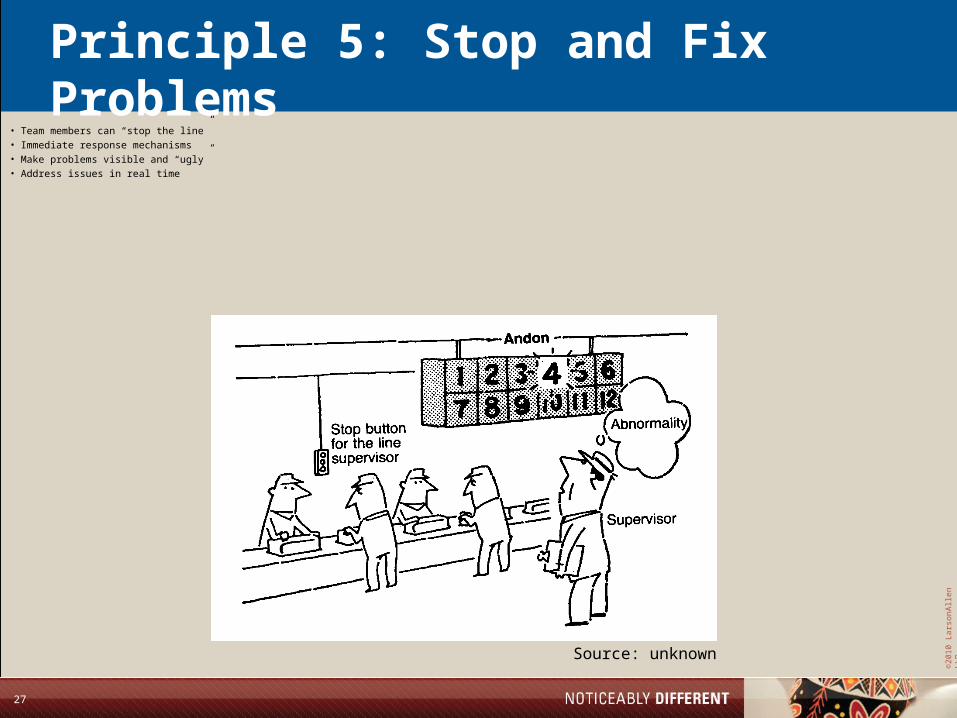

Principle 5: Stop and Fix Problems• Team members can “stop the line”

• Immediate response mechanisms

• Make problems visible and “ugly”

• Address issues in real time

Source: unknown

©20

10 L

arso

nA

llen

LLP

28

Stop and Fix Problems

• Sounds easy, natural, right?• Does anyone ever have an audit staff person that

has a question that stops their progress in one audit section or area? Or on that whole engagement?

• What do you have them do?• What would happen if all work on an audit

stopped if one person had a question that wasn’t answered or that interrupted their work?

• How would you respond? How quickly would you respond?

©20

10 L

arso

nA

llen

LLP

29

Challenges With “Stop to Fix Problems”

• Too many problems to address• People not skilled in problem solving• Not organized to react immediately• Fear of customer impacts• Cultural inertia to work around problems• Must have a blame-free environment

©20

10 L

arso

nA

llen

LLP

30

Principle 6

StandardizedTasks

©20

10 L

arso

nA

llen

LLP

31

Principle 6: Standardized Tasks

One best way, done by everybody,

until …

a better way is found.

©20

10 L

arso

nA

llen

LLP

32

www.istockphoto.comPurchased 10/19/2010By Rob Tracy

Standardization is Difficult

• Standardization creates the foundation for improvement

• Standardization is an enabler of change … not a barrier to change

• One of the most difficult cultural challenges

©20

10 L

arso

nA

llen

LLP

33

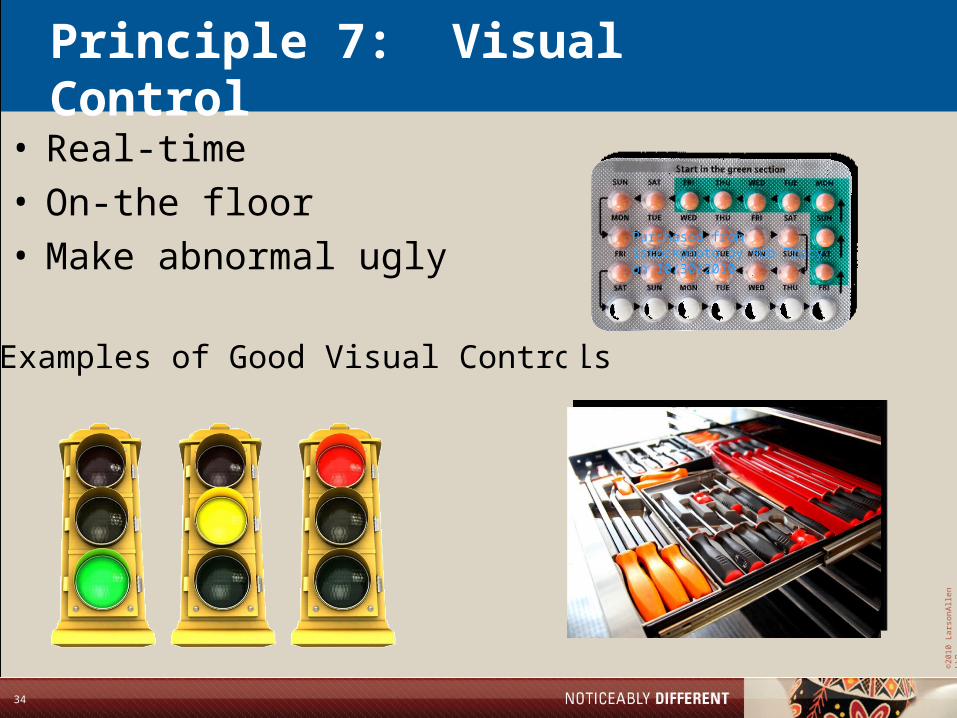

Principle 7

VisualControl

©20

10 L

arso

nA

llen

LLP

34

Principle 7: Visual Control

• Real-time• On-the floor• Make abnormal ugly

Examples of Good Visual Controls

Purchased from istockphoto by Rob Tracy on 10/30/2010

Pur

chas

ed f

rom

Ist

ockp

hoto

.com

by

Rob

Tra

cy o

n 10

/30/

2010

Purchased from istockphoto by Rob Tracy on 10/30/2010

©20

10 L

arso

nA

llen

LLP

35

Purchased from istockphoto by Rob Tracy on 10/30/2010

Purchased from istockphoto by Rob Tracy on 10/30/2010

Purchased from istockphoto by Rob Tracy on 10/30/2010

Principle 7: Visual Control

Examples of Poor Visual Controls

©20

10 L

arso

nA

llen

LLP

36

Principles 9 and 10

Leader &

Team Development

©20

10 L

arso

nA

llen

LLP

37

Principle 9: Leader Development• Champions of the Toyota Way• Understand the work• Teach to others• Use every opportunity as a coaching moment

Making things means making people.

—Fujio Cho, Chairman, Toyota

©20

10 L

arso

nA

llen

LLP

38

Principle 10: Team Development• Adjectives for associates

in a lean environment– Aligned

– Engaged

– Empowered

– Smart

– Skilled

– Valued

– Respected

Implementing the Toyota Way is 20% Tools and 80% People

President

Associates

Customers

©20

10 L

arso

nA

llen

LLP

39

Our Approach: Kaizen

©20

10 L

arso

nA

llen

LLP

40

What is Kaizen?

• Definition: Continuous Incremental Improvement• Literal Translation:

“Change” & “For The Better”• Kaizen structure

– One week– Focused– Cross-functional– Outcome oriented– Fast-paced– Results, not recommendations

©20

10 L

arso

nA

llen

LLP

41

Kaizen “rules”

• No stripes• Everyone participates & contributes• Seek to understand other’s perspectives• Treat others with respect• Consensus decision making

– If impasse is reached – majority rule

• Minimize the post-kaizen to-do list• Stay focused – no Blackberries• Be on time

©20

10 L

arso

nA

llen

LLP

42

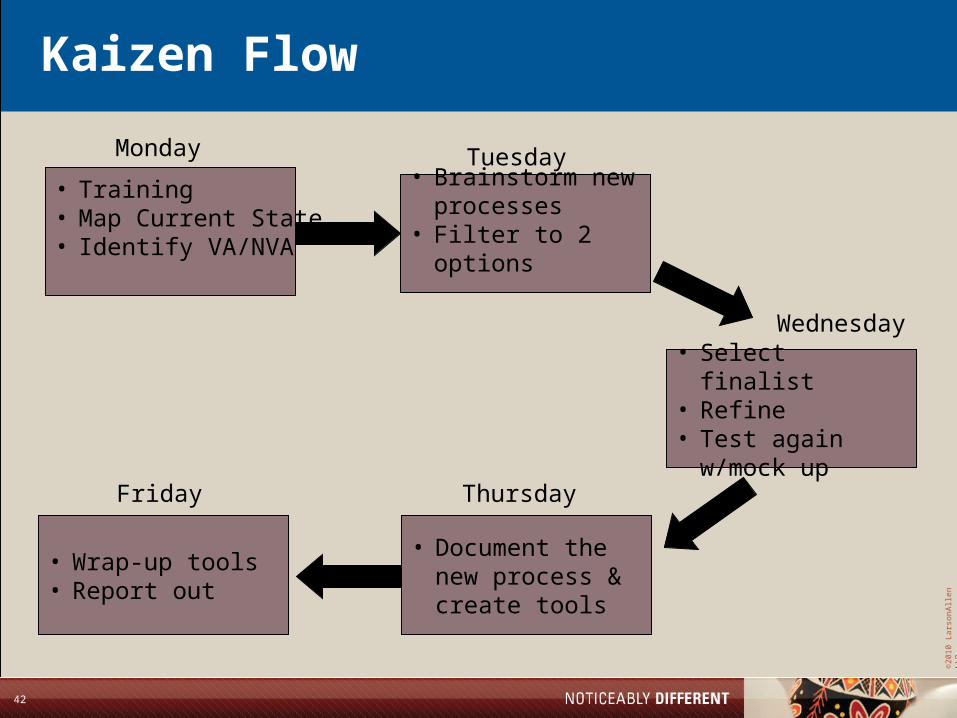

Kaizen Flow

• Training• Map Current State• Identify VA/NVA

• Brainstorm new processes

• Filter to 2 options

• Select finalist • Refine• Test again w/mock

up

• Document the new process & create tools

• Wrap-up tools• Report out

Monday Tuesday

Wednesday

ThursdayFriday

©20

10 L

arso

nA

llen

LLP

43

The Purpose of Process Mapping

• To describe the current process

– Document reality

• To build team understanding of the process

• To identify waste

• To stimulate identification of

countermeasures

©20

10 L

arso

nA

llen

LLP

44

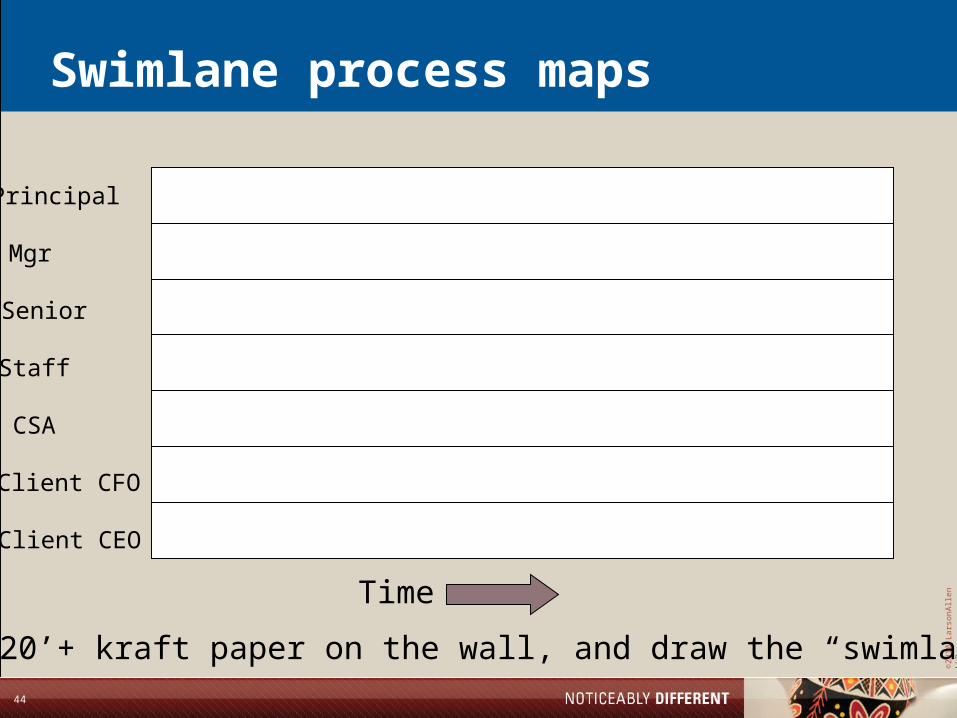

Swimlane process maps

Principal

Mgr

Senior

Staff

CSA

Client CFO

Client CEO

Tape 20’+ kraft paper on the wall, and draw the “swimlanes”

Time

©20

10 L

arso

nA

llen

LLP

45

Swimlane process maps

Principal

Mgr

Senior

Staff

CSA

Client CFO

Client CEO

Put tasks on post-it notes & place them on the map.

Time

©20

10 L

arso

nA

llen

LLP

46

The Kaizen Week

46

M T W

EmotionalEnergy

Th F

©20

10 L

arso

nA

llen

LLP

47

©20

10 L

arso

nA

llen

LLP

48

Kaizen Week Outputs

• Future State Process Map• Standard Work Instructions• Tools & Templates (as needed)• Project Charters for implementation• Communication plan and materials• Training plan and materials

©20

10 L

arso

nA

llen

LLP

49

Cultural Differences

Current state Future state

Principal preference Standard work

React Plan and execute with precision

My book of business Our book of business

Individuals Teams

Keep people busy Make work flow

Get jobs started Get jobs completed

Hard on the people Hard on the process

Problems are problems Problems are learningopportunities

©20

10 L

arso

nA

llen

LLP

50

How These Principles Relate to Us (some of our tools & techniques)

©20

10 L

arso

nA

llen

LLP

51

Principle 2

ContinuousFlow

©20

10 L

arso

nA

llen

LLP

52

Manage to the plan Manage to the plan & check in with& check in withthe client oftenthe client often

Don’t start untilDon’t start untilit is readyit is ready

Have a plan & gain Have a plan & gain client’s buy-inclient’s buy-in

Don’t stop untilDon’t stop untilit is completeit is complete

52

Cornerstones of Managing for Daily Improvement

MDI Cornerstones

©20

10 L

arso

nA

llen

LLP

53

Daily client service plan - completed

In-ChargeClient Name Client YE 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Nov-09 Dermott BRADMAN LAKE INC12/31 C P P P P I

Dec-09 Dermott BRADMAN LAKE INC12/31 P P P

Jan-10 Dermott BRADMAN LAKE INC12/31 F F F TA PF F F QT RD TP TP TR TR TC TR RD

Feb-10 Dermott BRADMAN LAKE INC12/31 RD TR

©20

10 L

arso

nA

llen

LLP

54

Principle 4

LevelProduction

©20

10 L

arso

nA

llen

LLP

55

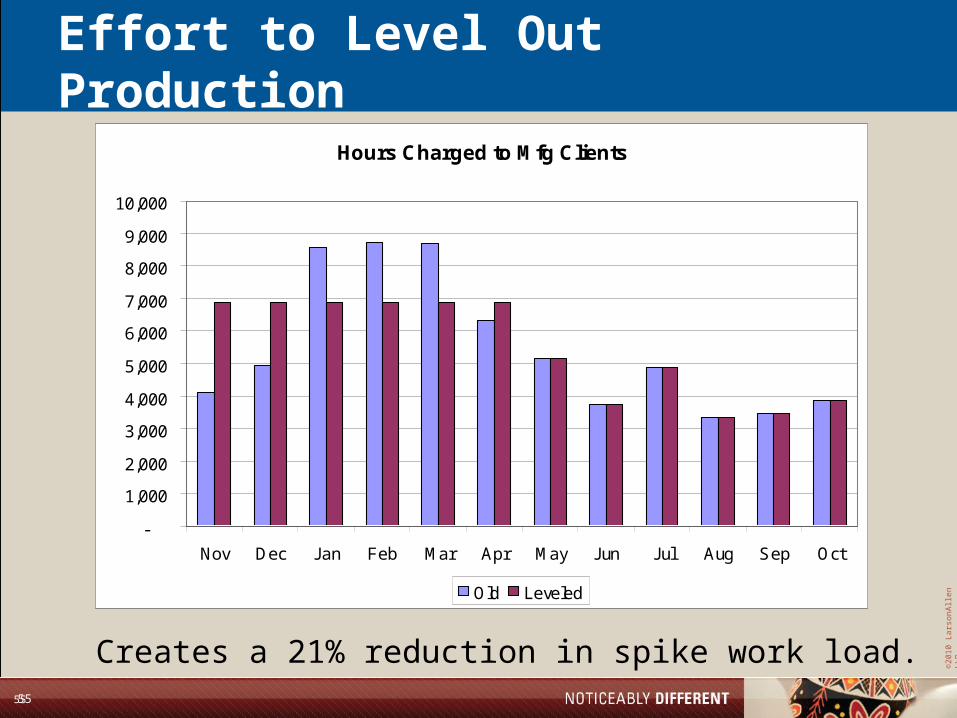

Effort to Level Out Production

Hours Charged to Mfg Clients

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Old Leveled

55

Creates a 21% reduction in spike work load.

©20

10 L

arso

nA

llen

LLP

56

Principle 5

Stop and FixProblems

©20

10 L

arso

nA

llen

LLP

57

Weekly Stand Up Meetings – 15 minutes

Charlotte Health Care MWI

Timeline Last Day ofCycle TimeExpectedIn-Charge Client Name Rec'd FieldworkBenchmarkCompletion 6/22 6/29 7/6 7/13 7/20 7/27 8/3 8/10 8/17 8/24 8/31 9/7 9/14 9/21 9/28 10/5 10/12 10/19 10/26 11/2

LederCommunity Blood Center of the CarolinasYes 10/22/10 14 11/5/10 KC/TS FC MC/IR IF MC FR/FS FFMorgan Cornelia Nixon Davis Yes 12/3/10 14 12/17/10 KC TS FC MC MC IFWoods Duplin General HospitalYes 11/22/10 14 12/6/10 TS KC IR FC IF MC FR FF/FS FS/FF

Linn Fairfield Memorial HospitalYes 12/10/10 14 12/24/10 KC IR TS FC MC IF MCClark FirstHealth of the CarolinasYes 11/24/10 14 12/8/10Szulak Johnston Health Yes 11/19/10 14 12/3/10 KC TS/FC IR IF MC MC MC MCMorganLaurens County Healthcare SystemYes 12/10/10 14 12/24/10 KC TS FC IR IF/MC MCMorgan Loris Healthcare SystemYes 11/24/10 14 12/8/10 TS IR/FC MC MC/IF MCHicks Lutheran Homes of SC Yes 11/5/10 14 11/19/10 KC IR TS/FC MC IF MC MC FR FF FFMageeMorehead Memorial HospitalYes 11/30/10 14 12/14/10 TS IR/FC MC MC IF MC MC

Linn Outer Banks Hospital Yes 11/19/10 14 12/3/10 FC MC IR/FC IF MC FR FF/FSWoods Pardee Memorial HospitalYes 12/3/10 14 12/17/10 KC TS IR/FC MC IF MCHicks Person Hospital Yes 10/29/10 14 11/12/10 KC TS FC IR MC/IF MC MC FR FFClark Rutherford Hospital Yes 12/10/10 14 12/24/10 KC TS FC/IR IF MC MC MC MCHicks Southminster, Inc. Yes 11/5/10 14 11/19/10 KC TS FC MC IR IF FS MC/FR FFClark Stanly Health Services Yes 11/5/10 14 11/19/10 KC TS FC MC MC FR FF FF FF/FSLinnUniversity Health Systems of Eastern CarolinaYes 11/19/10 14 12/3/10 FC IR IF MC FR FF/FSLinn Wake Ortho Yes 10/22/10 14 11/5/10 KC IR TS MC/IF FR FF/FS FF

Szulak WakeMed Yes 11/5/10 14 11/19/10 FF FF FFSzulak Wallace Thomson HospitalYes 12/10/10 14 12/24/10 KC/FC TS MC MC/IR IF MCMorgan Wayne Memorial HospitalYes 11/12/10 14 11/26/10 KC TS/FC IR MC MC/IF/FR FF FF

©20

10 L

arso

nA

llen

LLP

58

Principle 6

StandardizedTasks

©20

10 L

arso

nA

llen

LLP

59

Move from Individualized Processes…..

• Varied by office• Varied within each office by each industry• Varied within each office & industry for each

Principal• Varied within each office, industry & Principal for

each specific in-charge

©20

10 L

arso

nA

llen

LLP

60

Current Process Maps

©20

10 L

arso

nA

llen

LLP

61

Current Process Maps

©20

10 L

arso

nA

llen

LLP

62

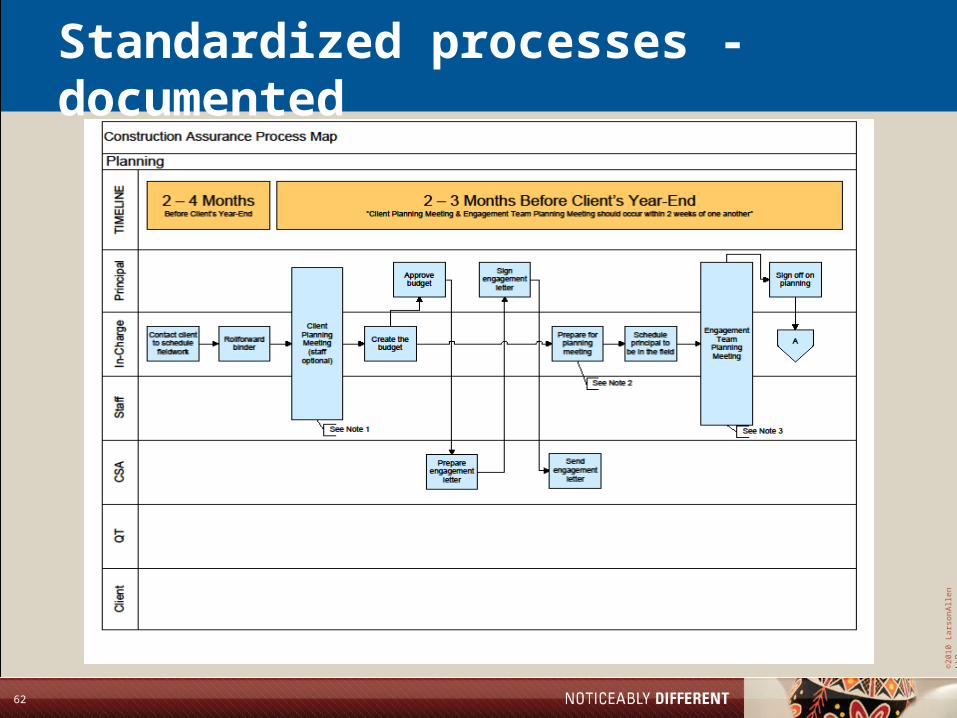

Standardized processes - documented

©20

10 L

arso

nA

llen

LLP

63

Principle 7

VisualControl

©20

10 L

arso

nA

llen

LLP

64

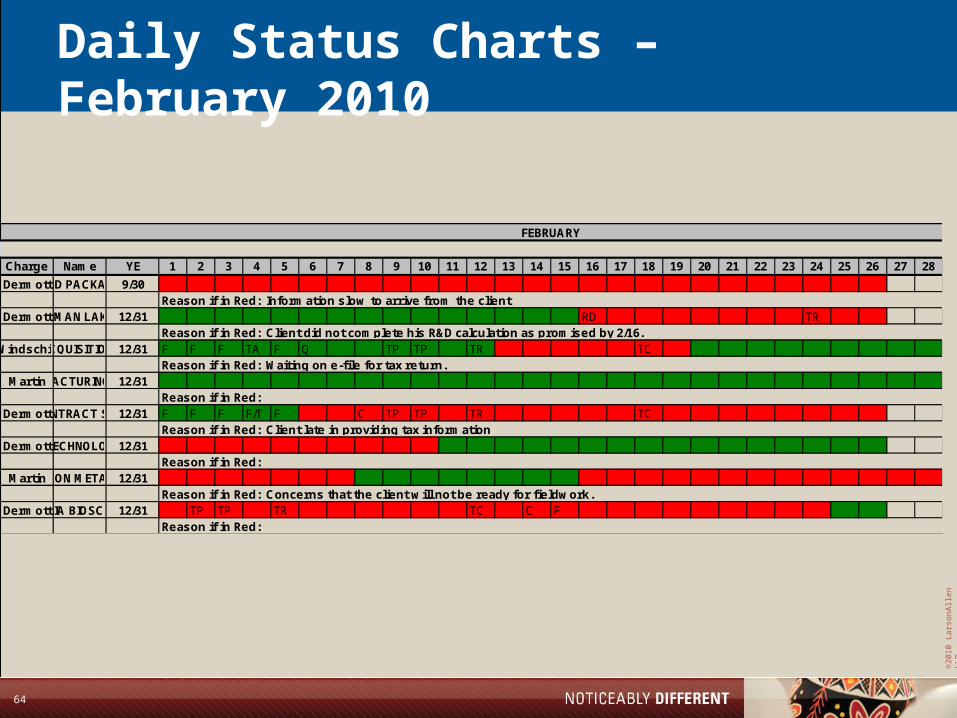

Daily Status Charts – February 2010

In-Charge

Client Name

Client YE 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28

DermottCOLOR AD PACKAGING INC9/30

DermottBRADMAN LAKE INC12/31 RD TR

WindschitlEAM ACQUISITION CORP12/31 F F F TA F Q TP TP TR TC

MartinHUBNER MANUFACTURING CORPORATION12/31

DermottINSOURCE CONTRACT SERVICES, LLC12/31 F F F F/T F C TP TP TR TC

DermottLEHIGH TECHNOLOGIES, INC12/31

MartinPARAGON METALS INC12/31

DermottPASTEURIA BIOSCIENCE INC12/31 TP TP TR TC C F

Reason if in Red: Client late in providing tax information

Reason if in Red:

Reason if in Red: Concerns that the client w ill not be ready for fieldwork.

Reason if in Red:

FEBRUARY

Reason if in Red: Information slow to arrive from the client

Reason if in Red: Client did not complete his R&D calculation as promised by 2/16.

Reason if in Red: Waiting on e-file for tax return.

Reason if in Red:

©20

10 L

arso

nA

llen

LLP

65

Principles 9 and 10

Leader &

Team Development

©20

10 L

arso

nA

llen

LLP

66

Language, Culture & Communication

• Focused, disciplined approach to improvement efforts

• Approach applied consistently• Defined support & cost required for each

improvement effort• Defined, targeted outcomes• Prescreening/approval• Oversight by Operational Excellence Advisory

Board

©20

10 L

arso

nA

llen

LLP

67

©20

10 L

arso

nA

llen

LLP

68

Detailed Implementation Plans

©20

10 L

arso

nA

llen

LLP

69

Examples of Our Results to Date

©20

10 L

arso

nA

llen

LLP

70

Kaizen Results – by Implementation Plan/AreaOE BOWLING CHART

Team Name: OEAB

No. Measure JOP Dec-09 Jan-10 Feb-10 M ar-10 Apr-10 M ay-10 Jun-10 Aug-10 Sep-10 Oct-10 Nov-10 Dec-10 Jan-11 Target

0.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 5.0% 5.0% 5.0%

0.0% 3.0% 7.3% 7.4% 4.9% ?? 7.9% 7.9%

N/A N/A 10% 15% 20% 20% 20% 20% 20% 20% 20% 20% 20%

N/A N/A -50% 14% 20%

N/A 5% 7% 10% 10% 12% 12% 15% 18% 18% 18% 18% 20%

N/a N/A 36% 25% 20%

N/A N/A 5% 10% 10% 10% 10% 10% 10% 10% 10% 10% 10%

N/A N/A 20% 12% 2%

N/A -15% -10% -5% 0% 0% 0% 0% 0% 0% 0% 0% 0%

-7.2% 9.5% ~10%

96 24 24 24 24 24 24 24 24 24 24 24 24

8.00 ??

20%

20%

20%

10%

0% 0.0

24 hours

Individual YTD realization up 4% (82.8% to 86.8%) 13%

Business YTD realization up 3.7% (90.6% to 94.3%), 25%

1

2

3

4

0%

0%

0%

M&D EngagementReduce same-job hours by 20% (YTD completed

eng.)(Erik)

M&D Tax - IndividualReduce same job hours for individual tax preparation/

review by 20%(Ben)

M&D Tax - BusinessReduce same-job hours

spent on business returns by 20%

(Ben)

6

MarketingProduce eFlash from

start to finish in a maximum of 24 hours.

(John R.)

120 hours

5

Dallas0% reduction in same-job hours (we don't go

backwards due to paperless conversion)

(Ben)

Business YTD realization up .5% (91.5/92.0). Individual YTD down .2% (93.6/93.4). Combined up .2%

(92.2/92.4).

Business YTD realization down 2.6% (83/80.4). Individual YTD up .4% (72.4/72.8).

Combined down 1.6% (78.7/77.1)

Phoenix TaxReduce same-job hours

by 10%(Terry)

0%

©20

10 L

arso

nA

llen

LLP

71

MWI results – CLT Manufacturing Year 1• Goal – issue audit reports within 14 days of

fieldwork• Results - recurring audit engagements, those

engagements in year 3 or more:– Decrease in hours from previous year: -16%

– Decrease in WIP dollars from previous year: -8%

– Days from end of fieldwork to report issuance: 19.X

• Lessons learned:– Involving clients in plan & timeline critical

– Managing clients and timeline poor

– Interim work poorly executed; incomplete

– Must resolve problems more often than weekly

©20

10 L

arso

nA

llen

LLP

72

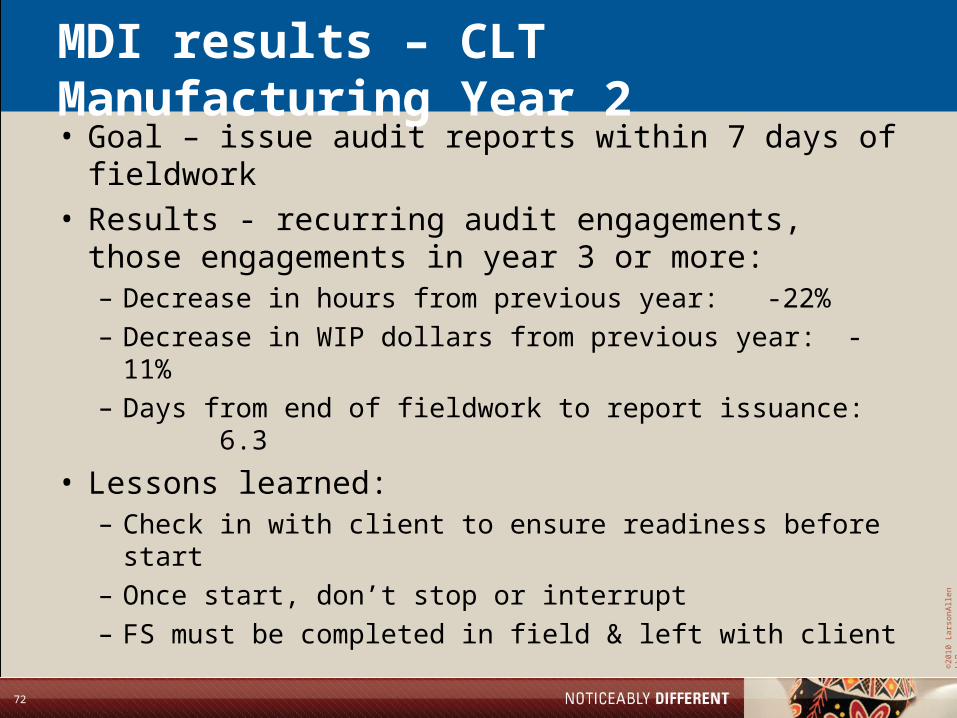

MDI results – CLT Manufacturing Year 2• Goal – issue audit reports within 7 days of

fieldwork• Results - recurring audit engagements, those

engagements in year 3 or more:– Decrease in hours from previous year: -22%– Decrease in WIP dollars from previous year: -11%– Days from end of fieldwork to report issuance: 6.3

• Lessons learned:– Check in with client to ensure readiness before start– Once start, don’t stop or interrupt– FS must be completed in field & left with client

©20

10 L

arso

nA

llen

LLP

73

MWI results – CLT Dealerships Year 1• Goal – issue audit reports within 14 days of

fieldwork• Results - recurring audit engagements, those

engagements in year 3 or more:– Decrease in hours from previous year: -49%– Decrease in WIP dollars from previous year: ??– Days from end of fieldwork to report issuance: 13.8

©20

10 L

arso

nA

llen

LLP

74

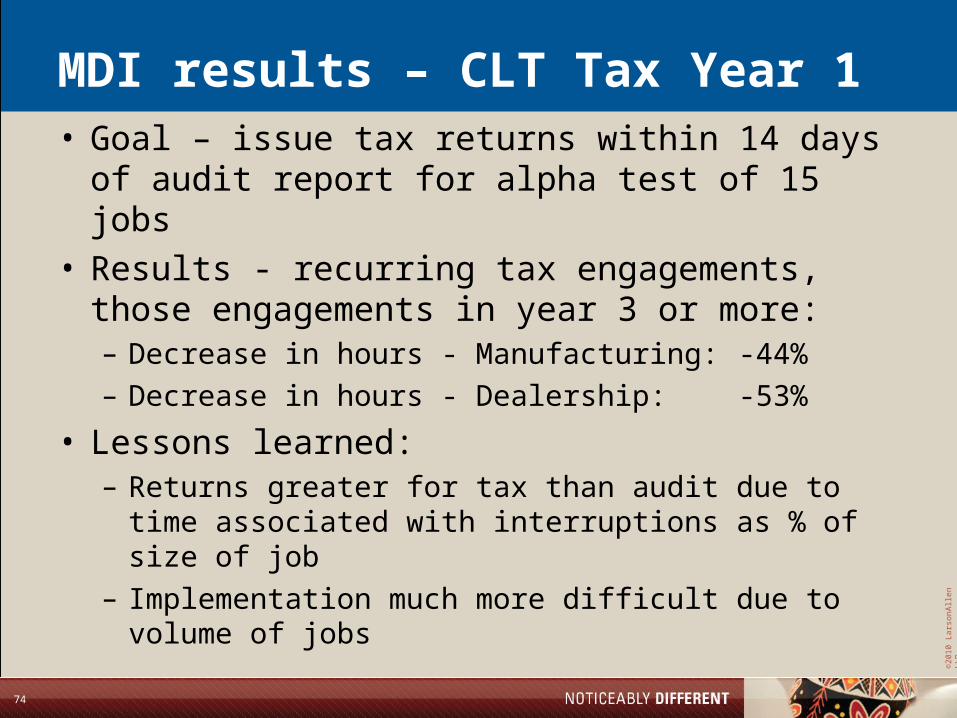

MDI results – CLT Tax Year 1• Goal – issue tax returns within 14 days of audit

report for alpha test of 15 jobs• Results - recurring tax engagements, those

engagements in year 3 or more:– Decrease in hours - Manufacturing: -44%– Decrease in hours - Dealership: -53%

• Lessons learned:– Returns greater for tax than audit due to time

associated with interruptions as % of size of job– Implementation much more difficult due to volume of

jobs

©20

10 L

arso

nA

llen

LLP

75

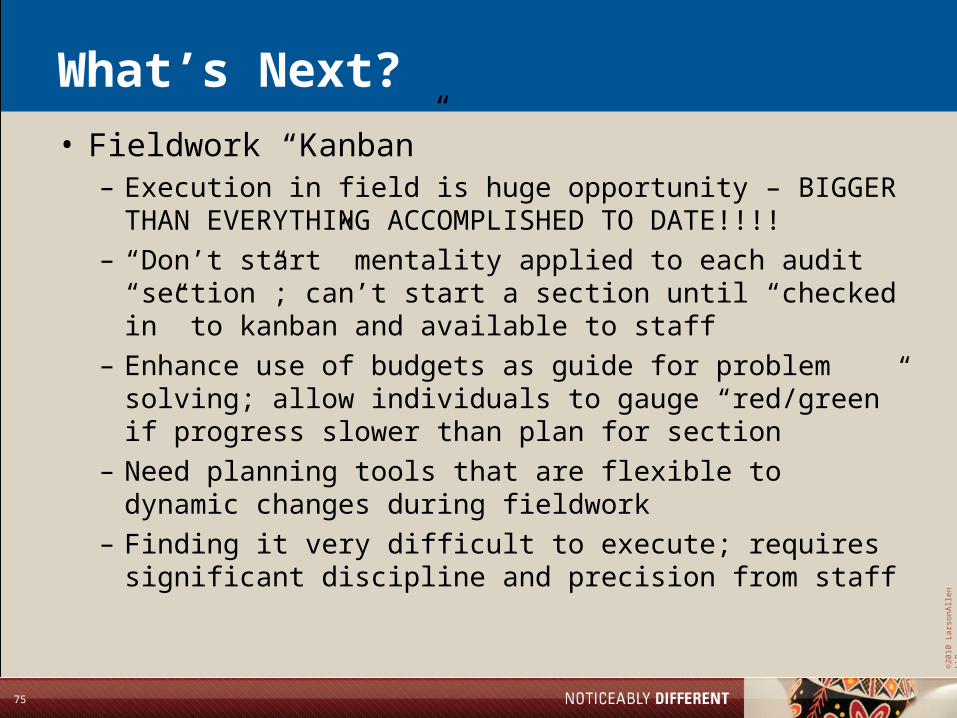

What’s Next?

• Fieldwork “Kanban”– Execution in field is huge opportunity – BIGGER THAN

EVERYTHING ACCOMPLISHED TO DATE!!!!– “Don’t start” mentality applied to each audit “section”;

can’t start a section until “checked in” to kanban and available to staff

– Enhance use of budgets as guide for problem solving; allow individuals to gauge “red/green” if progress slower than plan for section

– Need planning tools that are flexible to dynamic changes during fieldwork

– Finding it very difficult to execute; requires significant discipline and precision from staff

©20

10 L

arso

nA

llen

LLP

76

Closing Questions and Discussion

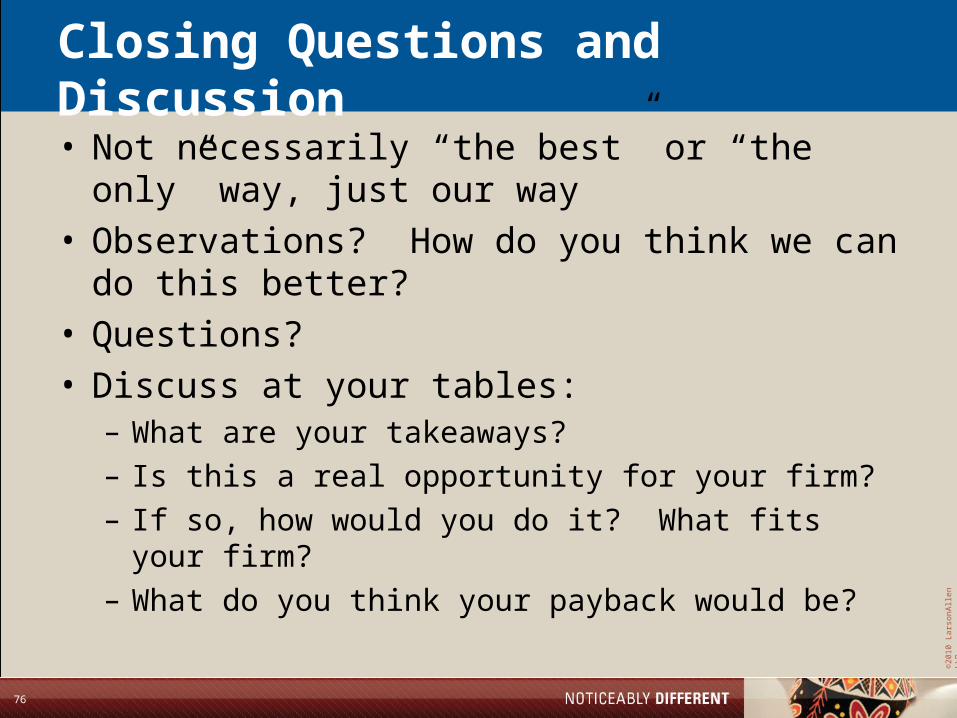

• Not necessarily “the best” or “the only” way, just our way

• Observations? How do you think we can do this better?

• Questions?• Discuss at your tables:

– What are your takeaways?– Is this a real opportunity for your firm?– If so, how would you do it? What fits your firm?– What do you think your payback would be?