2010 Jun 07 - OCBC - First Reit

27

Please refer to the important disclosures at the back of this document. First REIT SINGAPORE Company Update Results MITA No. 010/06 /2009 7 January 2011 Initiating Coverage BUY Current Price: S$0.74 Fair Value: S$0.84 SINGAPORE Company Report MITA No. 013/06/2010 Reuters Code FRET.SI ISIN Code AW9U Bloomberg Code SP Issued Capital (m) 622 Mkt Cap (S$m / US$m) 460 / 355 Major Shareholders Lippo Karawaci 21.7% Free Float (%) 90.2% Daily Vol 3-mth (‘000) 1,256 52 Wk Range 0.578 - 0.750 Leveraging on strong healthcare fundamentals Wong Teck Ching (Andy) (65) 6531 9817 e-mail: [email protected] 0 500 1000 1500 2000 2500 3000 3500 D e c 0 9 F e b - 1 0 A p r 1 0 J u n 1 0 A u g 1 0 O c t 1 0 D e c 1 0 0.5 0.6 0.6 0.7 0.7 0.8 STI First REIT Good quality assets. First REIT (FREIT) owns ten healthcare- related properties across Indonesia and Singapore. It derives some 86.4% of its gross revenues from Indonesia, with the remainder coming from Singapore. We believe that FREIT is well-positio ned to capitalise on the growing demand for higher quality healthcare from the middle-class in Indonesia as well as increasing eldercare needs in Singapore. With a well-defined acquisition strategy, FREIT has managed to complete the acquisitions of two Indonesian hospitals recently which we view as yield-accretive in nature. Strong and committed sponsor. We believe that FREIT would benefit largely from the support of its sponsor PT Lippo Karawaci Tbk (Lippo), which is the largest listed property company in Indonesia by total assets, revenue, net profit and market capitalisation. Lippo accounts for 86.4% of FREIT's FY09 gross rental income, and we see this as a level of income reliability for FREIT. Given Lippo's increasing commitment towards healthcare, we opine that this augurs well for FREIT. This is because FREIT has a right of first refusal on any assets sold by Lippo, which signifies the potential of quality hospital acquisitions out of Lippo's pipeline. Steady and sustainable income. FREIT has delivered consistent and stable distribution per unit (DPU) to its unitholders since its SGX-listing. We attribute this largely to the favourable master lease terms of its assets. All the master leases have a long tenure, 100% committed occupancy and are on a triple net basis, which has allowed FREIT to enjoy net property income (NPI) margins of 99.0% and above. Its leases are subjected to a yearly rental revision, which provides downside protection for its rental income. Moreover, FREIT has fixed the SGD-IDR exchange rate for its rental income, thus eliminating any forex risk. Potential upside ahead; initiate with BUY. We believe that FREIT represents a compelling investment story at current valuations. This is driven by its income stability as well as the positive prospects of Indonesia and Singapore's healthcare sector. We are sanguine about the committed support which Lippo provides and the potential assets in FREIT's pipeline. We also like management's strong execution capabilities and FREIT's attractive distribution yield, which is well above the S-REIT average. Our RNAV-derived fair value estimate of S$0.84 yields a potential upside of 13.7% and a total return of 22.6%. As such, we initiate coverage on FREIT with a BUY rating. (S$ m) FY08 FY09 FY10F FY11F Revenue 30.0 30.2 30.2 54.7 NPI 29.8 29.9 29.9 54.1 Distributions 20.8 21.0 21.0 41.3 Distr yield (%)* 10.3 10.3 4.6 8.8 P/NAV (x) 0.8 0.8 0.9 0.9 *Note: FY10F's yield is due to dilution from new rights issue which traded on 31 Dec 10

Transcript of 2010 Jun 07 - OCBC - First Reit

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 1/27

Please refer to the important disclosures at the back of this document.

First REIT

SINGAPORE Company Update Results MITA No. 010/06/2009

7 January 2011

Initiating Coverage

BUY

Current Price: S$0.74Fair Value: S$0.84

SINGAPORE Company Report MITA No. 013/06/2010

Reuters Code FRET.SI

ISIN Code AW9U

Bloomberg Code SP

Issued Capital (m) 622

Mkt Cap (S$m / US$m) 460 / 355

Major Shareholders

Lippo Karawaci 21.7%

Free Float (%) 90.2%

Daily Vol 3-mth (‘000) 1,256

52 Wk Range 0.578 - 0.750

Leveraging on strong healthcare fundamentals

Wong Teck Ching (Andy)(65) 6531 9817e-mail: [email protected]

0

500

10001500

2000

2500

3000

3500

D e c - 0 9

F e b - 1 0

A p r - 1 0

J u n - 1 0

A u g - 1 0

O c t - 1 0

D e c - 1 0

0.5

0.6

0.6

0.7

0.7

0.8STI

First REIT

Good quality assets. First REIT (FREIT) owns ten healthcare-

related properties across Indonesia and Singapore. It derives

some 86.4% of its gross revenues from Indonesia, with the

remainder coming from Singapore. We believe that FREIT is

well-positioned to capitalise on the growing demand for higher

quality healthcare from the middle-class in Indonesia as well

as increasing eldercare needs in Singapore. With a well-definedacquisition strategy, FREIT has managed to complete the

acquisitions of two Indonesian hospitals recently which we

view as yield-accretive in nature.

Strong and committed sponsor. We believe that FREIT

would benefit largely from the support of its sponsor PT Lippo

Karawaci Tbk (Lippo), which is the largest listed property

company in Indonesia by total assets, revenue, net profit and

market capitalisation. Lippo accounts for 86.4% of FREIT's

FY09 gross rental income, and we see this as a level of income

reliability for FREIT. Given Lippo's increasing commitment

towards healthcare, we opine that this augurs well for FREIT.

This is because FREIT has a right of first refusal on any assets

sold by Lippo, which signifies the potential of quality hospital

acquisitions out of Lippo's pipeline.

Steady and sustainable income. FREIT has delivered

consistent and stable distribution per unit (DPU) to its

unitholders since its SGX-listing. We attribute this largely to

the favourable master lease terms of its assets. All the master

leases have a long tenure, 100% committed occupancy and

are on a triple net basis, which has allowed FREIT to enjoy

net property income (NPI) margins of 99.0% and above. Its

leases are subjected to a yearly rental revision, which provides

downside protection for its rental income. Moreover, FREIThas fixed the SGD-IDR exchange rate for its rental income,

thus eliminating any forex risk.

Potential upside ahead; initiate with BUY. We believe that

FREIT represents a compelling investment story at current

valuations. This is driven by its income stability as well as the

positive prospects of Indonesia and Singapore's healthcare

sector. We are sanguine about the committed support which

Lippo provides and the potential assets in FREIT's pipeline.

We also like management's strong execution capabilities and

FREIT's attractive distribution yield, which is well above the

S-REIT average. Our RNAV-derived fair value estimate of S$0.84 yields a potential upside of 13.7% and a total return of

22.6%. As such, we initiate coverage on FREIT with a BUY

rating.

(S$ m) FY08 FY09 FY10F FY11F

Revenue 30.0 30.2 30.2 54.7NPI 29.8 29.9 29.9 54.1

Distributions 20.8 21.0 21.0 41.3

Distr yield (%)* 10.3 10.3 4.6 8.8

P/NAV (x) 0.8 0.8 0.9 0.9

*Note: FY10F's yield is due to dilution from new rights issue which traded

on 31 Dec 10

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 2/27

P age 2 7 Janua ry 2011

F i r s t REIT

Table of Contents

Page

Section A Company Profile 3

Section B Investment Highlights 5

Section C Industry Trends and Outlook 11

Section D SWOT Analysis 17

Section E Peer Comparison and Valuation 20

Section F Disclaimer 27

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 3/27

P age 3 7 Janua ry 2011

F i r s t REIT

Exhibit 1: FREIT's trust structure

Source: Company

Section A: Company Profile

First REIT (FREIT) is a Singapore-based REIT which seeks to invest in adiversified portfolio of income-producing real estate and/or real estate related

assets in Asia that are primarily used for healthcare and/or healthcare-

related purposes. FREIT's current portfolio consists of five hospitals and

one hotel/country club in Indonesia, as well as three nursing homes and

one cancer centre in Singapore. The total appraised value of FREIT's portfolio

stands at approximately S$612.8m as at 31 Dec 10. FREIT was listed on

the Singapore Exchange on 16 Dec 06.

FREIT's sponsor is PT Lippo Karawaci Tbk (Lippo), Indonesia's largest

broad-based property company listed on the Jakarta and Surabaya stock

exchanges, with a market cap of approximately Rp16.0t. FREIT's manager is Singapore-based Bowsprit Capital (Bowsprit), which is 80% owned by a

wholly-owned subsidiary of Lippo, hence making Bowsprit an indirect

subsidiary of Lippo.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 4/27

P age 4 7 Janua ry 2011

F i r s t REIT

Exhibit 2: Breakdown of FREIT's gross revenue by country

Source: Company, OIR

85.9% 86.6% 86.4% 86.7% 86.4%

14.1% 13.4% 13.6% 13.3% 13.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

FY07 FY08 FY09 9M10 9M09

Indonesia Singapore

Exhibit 3: Breakdown of FREIT's FY09 gross revenue by property type

Source: Company, OIR

78.9%

9.6%

11.5%

Hospitals Nursing homes Hotel/Country club

Indonesian assets as key driver. FREIT's gross revenue is mainly driven

by its Indonesian properties, which forms approximately 86.4% of its total

revenue (Exhibit 1). In terms of asset type, hospitals contributed 78.9% of total revenue (Exhibit 2). This should come as no surprise given that FREIT's

sponsor Lippo is one of the leading private hospital operators in Indonesia

via its Siloam Hospital division, which is the current master lessee of FREIT's

three Indonesian hospitals. Given that FREIT has recently completed the

acquisitions of two new hospitals in Indonesia, which will be leased to

Lippo's Siloam, we expect Indonesia to continue to form an integral part of

FREIT's revenue moving forward.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 5/27

P age 5 7 Janua ry 2011

F i r s t REIT

Section B: Investment Highlights

Good quality assets… FREIT's portfolio comprises of good quality assetsthat are well-positioned to capitalise on the growing demand for higher

quality healthcare from the middle- class in Indonesia as well as increasing

eldercare needs in Singapore. Its Indonesian hospitals are strategically

located with a large catchment of potential patients. They are operated by

Siloam Hospitals, which is a premier private hospital provider of high quality

healthcare services in Indonesia. Its current flagship hospital, Siloam

Hospitals Lippo Village (SHLV), is conveniently situated in the exclusive

township of Lippo Karawaci in the Tangerang region and is also the first

hospital in Indonesia to be granted the Joint Commission International (JCI)

accreditation. JCI is a renowned international accreditation body that

assesses whether a healthcare organisation has met a certain level of quality standard. On the other hand, FREIT's nursing homes in Singapore

are equipped with the facilities and trained healthcare professionals to

provide convalescent and rehabilitative care for its residents.

…backed by yield accretive acquisitions. With a well-defined acquisition

strategy, FREIT has managed to complete the acquisitions of two Indonesian

hospitals on 31 Dec 10. The first is Mochtar Riady Comprehensive Cancer

Centre (MRCCC), which was purchased at a discount of 19.7% to its average

valuation of S$212.3m. The other hospital is Siloam Hospitals Lippo

Cikarang (SHLC), with a purchase consideration of S$35.0m, implying a

discount of 13.8% to its average valuation. The acquisitions were fundedby a 5-for-4 rights issue and debt. Despite the dilution for existing

unitholders, we view the acquisitions positively given their accretive nature.

We estimate that the net property income (NPI) yield of MRCCC and SHLC

as a result of these acquisitions to be 10.8% and 10.7% respectively,

which is higher than the existing portfolio's NPI yield of 8.8% (as at FY09).

FREIT's distribution yield for FY11, when the new assets are expected to

contribute, is projected to be 8.8%. This is greater than the current

distribution yield of 8.1% as reported during its 3Q10 results. Hence we

view these acquisitions as being yield accretive.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 6/27

P age 6 7 Janua ry 2011

F i r s t REIT

Exhibit 4: MRCCC and SHLC

Source: Siloam Hospitals website

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 7/27

P age 7 7 Janua ry 2011

F i r s t REIT

Increased income stability and enlarged asset base. As a result of the

new acquisitions, FREIT will experience greater rental income stability.

This is due to the long 15+15 years master lease agreement for the twonew hospitals, which is similar to its existing Indonesian properties, offering

downside revenue protection. Hence, its weighted average lease expiry

(WALE) has increased from 10.6 years to 12.4 years. FREIT has also

highlighted that the increased size of its asset base will enhance its profile

and competitive positioning and reduce the weighted average age of the

properties (WAAP) by approximately 32.7% to 12.1 years as at 30 Sep

10.

Steady and sustainable income… FREIT has delivered consistent and

stable distribution per unit (DPU) to its unitholders since its listing in Dec

06 (Exhibit 5). One reason is due to the strong operators running itsIndonesian assets, which provides FREIT with a revenue sharing opportunity

if certain conditions are fulfilled. As highlighted earlier, FREIT's Indonesian

hospitals are run by Lippo's Siloam Hospitals division, which has

successfully grown its market position over the years. Lippo also runs the

Imperial Aryaduta Hotel and Country Club (IAHCC), which is located opposite

to SHLV. Management has highlighted that a medical block could possibly

be set up at IAHCC in the future to complement SHLV. Two of FREIT's

nursing homes are operated by units of Pacific Healthcare Holdings [NOT

RATED], which is an integrated healthcare provider offering a comprehensive

range of services. The third nursing home, The Lentor Residence, is leased

and operated by First Lentor Residence Pte Ltd while the Pacific Cancer Centre is operated by Health Promise Pte Ltd.

FREIT has also effectively eliminated any exchange rate risk and uncertainty

by securing the SGD-IDR exchange rate for its Indonesian rental income

for the full term of its master leases. This has been fixed at S$1 = Rp5,623.50

for its initial four Indonesian assets and S$1 = Rp6,600 for MRCCC and

SHLC.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 8/27

P age 8 7 Janua ry 2011

F i r s t REIT

Exhibit 5: Quarterly DPU breakdown, 1Q07 - 3Q10

1.601.65

1.72 1.761.85

1.91 1.92 1.941.88 1.92 1.90 1.92 1.90 1.92 1.94

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2.20

1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10

D P U ( S c e n t s )

Source: Company, OIR

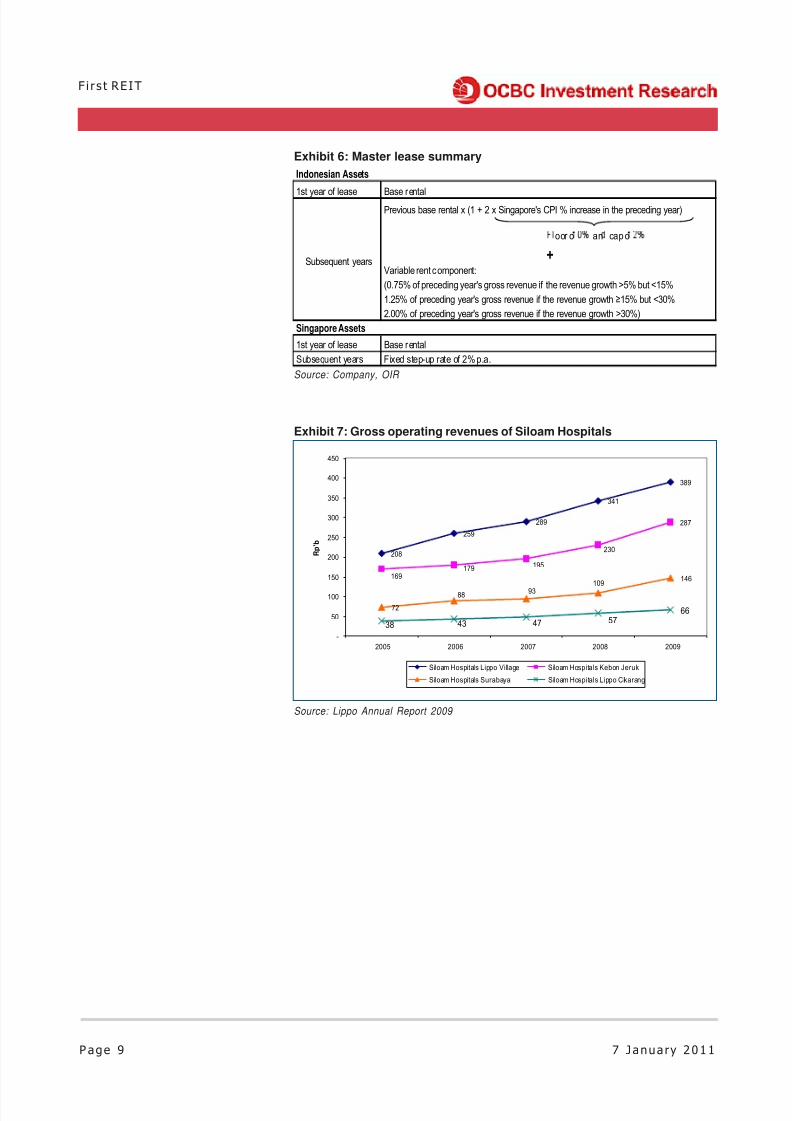

…driven by favourable master lease terms. But we opine that the main

reason for FREIT's stable and sustainable distribution income is attributed

to its favourable master lease terms. All of FREIT's properties are leased

out under a master lease agreement, with a committed occupancy of 100%.

The master leases are on a triple net lease basis, where the tenant is

responsible for any increases in insurance, tax or operating expenditure.

Hence, this explains why FREIT's NPI margin is consistently at 99.0% andabove. All of FREIT's master leases also offer a downside revenue protection,

which provides a level of support for FREIT's unitholders. The Singapore

assets are on a 10+10 years master lease, with a fixed 2% rental step-up

every year. The Indonesian assets are on a 15+15 years master lease, with

its base rental subjected yearly to a possible increment of two times

Singapore's Consumer Price Index (CPI) increase in the preceding year.

This is subjected to a floor of 0% and a cap of 2%. In addition, there is a

variable component based on the gross revenue growth of its Indonesian

assets (summarised in Exhibit 6). We view this positively given Indonesia's

growing healthcare market and Siloam Hospital's continual efforts to enhance

the quality of its healthcare services. Siloam's hospitals have thus experiencedgood revenue growth as illustrated in Exhibit 7. The earliest dates for FREIT's

renewal of its leases are 11 Apr 17 for its Singapore assets and 11 Dec 21

for its Indonesian assets.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 9/27

P age 9 7 Janua ry 2011

F i r s t REIT

Exhibit 6: Master lease summary

Source: Company, OIR

Indonesian Assets

1st year of lease Base rentalPrevious base rental x (1 + 2 x Singapore's CPI % increase in the preceding year)

oor o an cap o

+Variable rent component:

(0.75% of preceding year's gross revenue if the revenue growth >5% but <15%

1.25% of preceding year's gross revenue if the revenue growth ≥15% but <30%

2.00% of preceding year's gross revenue if the revenue growth >30%)

Singapore Assets

1st year of lease Base rental

Subsequent years Fixed step-up rate of 2% p.a.

Subsequent years

Exhibit 7: Gross operating revenues of Siloam Hospitals

Source: Lippo Annual Report 2009

208

259

289

341

389

287

72

146

66

179169

195

230

88 93

109

57474338

-

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009

R p ' b

Siloam Hospitals Lippo Village Siloam Hospitals Kebon Jeruk

Siloam Hospitals Surabaya Siloam Hospitals Lippo Cikarang

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 10/27

Page 1 0 7 Janua ry 2011

F i r s t REIT

Established and committed sponsor. We believe that FREIT would benefit

largely from the support of its sponsor Lippo, especially since it has the

right of first refusal on any assets sold by Lippo. Lippo recorded revenue

and net income of Rp2.6t and Rp388b respectively in FY09, highlighting its

strong financial position. This signifies the income resilience of FREIT given

that Lippo accounts for 86.4% of its FY09 gross rental income. Given Lippo's

increasing commitment towards healthcare, we believe this bodes well for

FREIT as it will be able to leverage on Lippo's expertise in this area. Lippo

plans to add around 20 hospitals to its assets within the next five years.

More notably, Lippo recently acquired two private hospitals in Jambi and

Balikpapan for US$18m and S$26m respectively. We view these two new

hospitals as potential acquisition targets by FREIT in the future, which

should provide a catalyst for its future growth.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 11/27

P age 1 1 7 Janua ry 2011

F i r s t REIT

Section C: Industry Trends and Outlook

We believe that FREIT can benefit largely from the underserved healthcare

market in Indonesia. There is good growth potential ahead as there is

increasing emphasis placed on the provision of proper healthcare services

there. FREIT's Singapore nursing homes can also gain from the aging

population and recent government initiatives. Although there is no variable

component for FREIT's nursing home leases, but the improving prospects

for its vendors will help to improve the stability of the rental income it receives.

Rising population and life expectancy. Indonesia's population has grown

at a compound annual grow rate (CAGR) of 1.3% from 2000 to 2009 to

230m people, which makes it the fourth most populous country after China,

India and US. Coupled with the increasing life expectancy of its population,

this means that there is a huge market to be captured due to greater

healthcare needs.

Exhibit 8: Population growth and life expectancy of Indonesia

Source: World Bank

205

208

211

214216

219

222

225227

230

67.4

67.9

68.3

68.869.2

69.770.1

70.8

70.4

190

195

200

205

210

215

220

225

230

235

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

N o o f m i l l i o n s

66.0

67.0

68.0

69.0

70.0

71.0

72.0

N o .

o f y e a r s

Population size (LHS) Life expectancy at birth (RHS)

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 12/27

Page 1 2 7 Janua ry 2011

F i r s t REIT

Increasing affluence to drive demand for high quality healthcare.

The emerging markets have rebounded strongly after the recent financial

crisis and Indonesia is no exception. The Jakarta Composite Index hasposted an impressive 46.1% return in 2010. Indonesians have also

experienced growing affluence as seen by the 15.9% CAGR in its GDP per

capita to US$2.35k from 2005 to 2009 (Exhibit 9). This has seen the

emergence of the middle class with greater spending power. Hence demand

for higher quality healthcare services will undoubtedly increase as standards

of living improve and affordability becomes less of an issue.

Exhibit 9: Rising affluence of Indonesians

1,304

2,2452,349

1,923

1,643

4.4

4.8

3.4

5.1

4.2

0

500

1,000

1,500

2,000

2,500

2005 2006 2007 2008 2009

U S $

0.0

1.0

2.0

3.0

4.0

5.0

6.0

%

GDP per capita (LHS) GDP per capita grow th rate (RHS)

Source: World Bank

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 13/27

P age 1 3 7 Janua ry 2011

F i r s t REIT

Underserved healthcare market has good growth potential… Although

there will be a foreseeable increase in demand for higher quality healthcare,

we believe that the Indonesian healthcare market is still underserved.

Indonesia's health expenditure as a percentage of its GDP stands at onlyaround 2.2% in 2007, which is much lower than its regional peers (Exhibit

10). Moreover, World Health Organisation's (WHO) World Health Statistics

2010 highlighted that there were only six hospitals per 10,000 people and

1 physician per 10,000 people in Indonesia. Hence Lippo entered the

healthcare business because it felt that it could address the issues of the

shortage of high quality hospitals and growing needs of Indonesians seeking

superior medical care. Backed by the growing brand awareness of its Siloam

Hospitals, we believe that the potential for growth is extensive in this

underserved market. Lippo is also exploring the possibility of providing

healthcare to the masses moving forward. Although gross margins are lower

for this segment, but we believe FREIT will be able to gain from this as itsvariable rent is subjected to topline increases.

Exhibit 10: Health expenditure as a percentage of GDP

2.2

3.1

3.7

1.92.0

3.23.3

4.14.3

4.44.5 4.4

4.3

3.73.5

4.14.1

4.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2005 2006 2007

%

Indones ia Singapore Malays ia China Thailand India

Source: World Bank

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 14/27

Page 1 4 7 Janua ry 2011

F i r s t REIT

Exhibit 11: Percentage of population with outpatient treatment

Source: Badan Pusat Statistik (Statistics Indonesia)

38.6%

38.2%

34.4%

34.1%

44.1%

44.4%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% 50.0%

2003

2004

2005

2006

2007

2008

…although thriving medical tourism poses challenges. While rising

affluence of Indonesians does signify stronger demand for higher quality

healthcare, there will likely be spillover effects to overseas countries. This

applies mainly to people of the upper income bracket, who are willing toincur higher expenses in exchange for healthcare treatment that is of higher

standard and sophistication in nature. According to industry data, medical

tourism in Asia is expected to be worth some US$4b by the year 2012. We

understand that the majority of Indonesians that seek medical treatment

overseas choose Singapore as their destination given its reputation as a

medical hub. Most of the remaining people seek their treatment in Malaysia.

Exhibit 12 highlights the growing medical tourism business in regional

countries, which will undoubtedly pose challenges to Indonesia's healthcare

sector.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 15/27

P age 1 5 7 Janua ry 2011

F i r s t REIT

Exhibit 12: Medical tourism statistics

Source: Frost & Sullivan

Aging population of Singapore. Singapore is fast becoming an aging

population (Exhibit 13) and with many living longer than before, this implies

an impending increase in palliative care services needs. Hence this augurs

well for nursing homes in Singapore as the availability of healthcare

professionals and facilities will help to cater to the convalescent needs of

the aged.

Exhibit 13: Aging population of Singapore

Source: Singapore Department of Statistics

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 16/27

Page 1 6 7 Janua ry 2011

F i r s t REIT

Government initiatives on nursing homes. It was recently reported that

two new nursing homes will be built in housing estates in the heartland of

Singapore, while four existing ones will be relocated to upgraded premises

in such areas. This highlights the increasing emphasis placed by the

government on nursing home care, which bodes well for FREIT. Staff will

also have their skills upgraded and we believe this would have positive

spillover effects for private nursing home operators. Singapore's Ministry of

Health (MOH) also highlighted that it hopes to increase the number of nursing

home beds from 9,300 to 14,000 by 2012. Hence FREIT could possibly

carry out asset enhancement initiatives (AEI) to capture a bigger share of

this market and increase its rental income in the future.

Health outlook. Given the positive trends highlighted as well as Lippo's

aggressive plans to cater to the rising demand for higher quality healthcare

services, we foresee FREIT's growth prospects to continue to be driven by

Indonesian hospitals as well as possible yield accretive AEI of existing

properties. We also believe that there is the possibility of acquisitions in

other parts of the region such as Malaysia and Australia should the right

opportunities come along.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 17/27

P age 1 7 7 Janua ry 2011

F i r s t REIT

Section D: SWOT Analysis

Exhibit 14: SWOT analysisStrengths Weaknesses

Extensive reach to middle-class Indonesians Concentration risk

Strong sponsor support Lack of quality doctors

Healthy gearing ratio Higher cost of debt due to perceived weakness of Indonesian assets

Long master leases with favourable terms

Good distribution yields - among the highest for S-REITs

Opportunities Threats

Potential acquisitions from sponsor pipeline Political risk

Yield accretive asset enhancement initiatives Change in regulation and government polices

Increased competition from private hospitals

Booming medical toursim overseas

Possible refinancing risks

Non-renewable of land titles upon expiry

Source: OIR

Strengths. FREIT's hospitals in Indonesia are able to benefit greatly fromthe growing demand for higher quality healthcare services there.This is via

the revenue sharing component of its master leases with Lippo's SiloamHospitals, which also highlights the strong sponsor support which FREITreceives. Siloam Hospitals recorded a 21% rise in revenue to Rp896b inFY09. We see potential for further growth given Siloam's investment in thelatest equipment and technology and extensive reach to the growing middle-class population. All of Siloam's hospitals also have an established Centreof Excellence, which seeks to enhance their patients' experience.

FREIT also leases out its assets with favourable master lease terms suchas the revenue sharing component just highlighted. This underpins FREIT'sincome stability as the master leases have long tenures; a downside revenueprotection; and possibility for annual base rental escalation. Please refer to the 'Investment highlights' section for a full elaboration of FREIT's

strengths.

Weaknesses. We view concentration risk as the biggest weakness of FREIT. This comes in the form of its strong dependence on its sponsor Lippo for the bulk of its rental income as well as the geographical risk of itsassets. Lippo contributed approximately 86.7% of FREIT's gross revenueas at 9M10. We foresee this figure to rise to 91.8% (taking into accountthe deferred rental income from Pacific Cancer Centre) in FY11. However Lippo is currently the largest listed property company in Indonesia by totalassets, revenues, net profit and market capitalisation. Lippo is also placingan increasing emphasis on its healthcare segment which will improve theoperational expertise of its hospitals. As the major shareholder of FREIT,we believe that its interests are aligned with other unitholders. This wouldprovide a level of support for FREIT's income.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 18/27

Page 1 8 7 Janua ry 2011

F i r s t REIT

Geographical risks exist due to the concentration of FREIT's assets in

Indonesia. Its indonesian assets made up 86.4% of its gross revenue and

84.0% of the total capital value of its portfolio in FY09. Hence FREIT issusceptible to negative events such as natural disasters, pandemics and

terrorist attacks etc.

Opportunities. We believe that FREIT's growth opportunities will be driven

by its strong executional capabilities to acquire quality assets, coupled

with its AEI. FREIT's goal is to increase its portfolio size to S$1b in two to

three years’ time. We opine that this target is likely to be achieved mainly

through the acquisition of yield accretive hospitals from Lippo, although

mangement has highlighted that they are also open to acquiring quality

assets that are non-sponsor related. This is due to Lippo's aggressive

healthcare expansion plans, which presents a pipeline of hospitals that

could possibly be injected into FREIT. Nursing homes in Singapore couldalso be a possibility, in our opinion, underpinned by Singapore's fast aging

population. FREIT's current debt-to-assets leverage of 16.3% (our FY10F

estimate) also offers sufficient debt headroom to its regulatory limit of 35%,

which provides the financial flexibility to undertake any future acquisitions.

FREIT is currently undertaking AEI works on its Pacific Cancer Centre and

is awaiting regulatory approval before embarking on an extension block at

its Lentor Residence nursing home. The former is a proposed modern three-

storey cancer centre with a GFA of 27,405 sq (from 13,412 sf), equipped

with facilities such as a Radiotherapy and Imaging Centre. This AEI is

expected to be completed around mid-2011, with a new 10+10 year lease

term to be signed. We estimate that the NPI yield of this AEI to be

approximately 8.4% as a result of an increase in base rental. As for theLentor Residence extension, we estimate its NPI yield to be 7.7%. Both

yields are higher than FREIT's 7.4% Singapore portfolio NPI yield, but lower

than the overall portfolio NPI yield of 8.8%. We believe this is justifiable as

FREIT's indonesian assets tend to command a higher yield premium to

compensate for their associated risks as compared to its Singapore assets.

Moreover the Pacific Cancer Centre AEI would be fully funded by debt while

the Lentor Residence by internal resources, with the yields being higher

than its cost of debt (approximately 3.8%). Management also explained

that the lower initial yield was viable due to the 2% annual rental escalation

stipulated in the leases.

Threats. We see increasing competition from private hospitals in Indonesiaand the booming medical tourism trade as key threats to FREIT as this

might adversely affect the variable rental revenues which it receives. While

SHLV was the first hospital in Indonesia to receive the JCI accreditation,

we note that two more hospitals have recently achieved this feat (Santosa

Hospital on 13 Nov 10 and Eka Hospital on 11 Dec 10). This implies that

there is an increasing focus by other private hospitals to tap on the increasing

healthcare needs of Indonesians. A large number of rich indonesians also

tend to seek their medical treatment overseas due to the higher standards

of treatment available and this rising trend would pose a challenge to Siloam

Hospitals.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 19/27

P age 1 9 7 Janua ry 2011

F i r s t REIT

FREIT might also face the possibility of refinancing risks as its gross

borrowings of S$56.8m (as at 30 Sep 10) all mature on Jun 2012. We also

foresee this figure to increase to approximately $70m as it draw downs its

term loan facility to finance the S$18.6m AEI of Pacific Cancer Centre. A

new term loan facility of up to S$50m has also been undertaken for the

acquisition of MRCCC, which is due in 2015. While we think that a more

spaced out debt-maturity profile would be ideal, we believe that FREIT's

healthy gearing ratio would provide sufficient headroom for their refinancing

needs.

Any non-renewable of land titles upon expiry would also pose a major

problem for FREIT. This is especially so for some of its Indonesian

properties, which sits on different land titles. Both its Pacific Healthcare

Nursing Homes also have a relatively short leasehold of 30 years, which

will expire in 2032-2033. However, given the increasing emphasis placed

on healthcare in Indonesia and nursing homes in Singapore, we believe

this would boost FREIT's chances of renewing its land titles upon expiry.

Management has guided that they managed to renew two such land titles

in Indonesia at minimal cost in 2009. Three of their Indonesian assets

(SHLV, IAHCC and SHLC) are also located inside Lippo's township, which

makes it easier to get renewal approval when due, in our opinion.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 20/27

Page 2 0 7 Janua ry 2011

F i r s t REIT

Section E: Peer Comparison and Valuation

Exhibit 15: Peer comparison

Bloomberg

Ticker

Last

Price Curr

Market

Cap

(in $m)

Equity

Free

Float Dist Freq

Latest

Announc

Qtr DPU

(in cents)

(Implied)

Annualised

Yield

(%)

Cons

FY-1 DPU

(in cents)

Cons

FY-2 DPU

(in cents)

FY-1

Yield

(%)

FY-2

Yield

(%)

Leverage

ratio (%)

Book value

per unit

(in S$)

Price-to-

book (x)

Office

Frasers Commercial Trust* FCOT SP 0.17 SGD 528 74.5% Semi-Anl 0.31 7.3% 1.00 1.10 5.9 6.5 38.3 0.39 0.44

CapitaCommercial Trust* CCT SP 1.53 SGD 4,320 67.9% Semi-Anl 1.99 5.2% 7.50 7.20 4.9 4.7 31.0 1.42 1.08

K-REIT Asia KREIT SP 1.44 SGD 1,953 24.3% Semi-Anl 1.69 4.7% 6.60 7.40 4.6 5.1 14.9 1.47 0.98

Suntec REIT* SUN SP 1.53 SGD 3,374 89.6% Quarter 1.68 5.9% 9.60 9.30 6.3 6.1 32.9 1.83 0.84

Indiabulls Properties Investment Trust IPIT SP 0.27 SGD 979 14.8% None 0.05 0.7% NA NA NA NA 13.3 0.52 0.52

Treasury China Trust TCT SP 1.87 SGD 479 65.6% Irreg 2.50 5.4% 5.00 10.00 2.7 5.3 33.3 3.91 0.48

Office Average 11,632 4.9% 4.9 5.5 27.3 1.59 0.72

Retail

CapitaMall Trust* CT SP 1.98 SGD 6,305 64.5% Quarter 2.36 4.8% 9.50 10.00 4.8 5.1 36.5 1.52 1.30

Frasers Centerpoint Trust* FCT SP 1.53 SGD 1,174 52.6% Quarter 2.16 5.7% 8.20 8.90 5.4 5.8 30.3 1.29 1.19

Starhill Global REIT* SGREIT SP 0.635 SGD 1,234 70.9% Quarter 1.00 6.3% 3.90 4.10 6.1 6.5 30.6 0.90 0.70

CapitaRetail China Trust CRCT SP 1.25 SGD 782 58.7% Semi-Anl 2.08 6.7% 8.30 8.30 6.6 6.6 34.3 1.08 1.16

Fortune REIT (in HK$) FRT SP 3.96 HKD 6,609 70.2% Semi-Anl 5.76 5.8% 24.50 25.50 6.2 6.4 21.5 5.67 0.70

Lippo-Mapletree Indonesia* LMRT SP 0.57 SGD 617 50.2% Quarter 1.09 7.7% 4.70 4.20 8.2 7.4 10.8 0.79 0.72

Retail Average 16,721 6.2% 6.2 6.3 27.3 1.88 0.96

Healthcare

Parkway Life REIT PREIT SP 1.74 SGD 1,052 52.8% Quarter 2.25 5.2% 8.70 9.70 5.0 5.6 35.1 1.38 1.26

Healthcare Average 1,052 5.2% 5.0 5.6 35.1 1.38 1.26

Hospitality

Ascott Residence Trust* ART SP 1.260 SGD 1395.9 51.9% Semi-Anl 1.85 5.9% 7.50 7.90 6.0 6.3 31.3 1.22 1.03

CDL Hospitality REIT CDREIT SP 2.070 SGD 1982.5 67.2% Semi-Anl 2.54 4.9% 10.20 11.90 4.9 5.7 21.0 1.46 1.42

Hospitality Average 3,378 5.4% 5.4 6.0 26.2 1.34 1.23

Industrial

Ascendas REIT* AREIT SP 2.17 SGD 4,067 79.3% Quarter 3.30 6.1% 13.70 14.00 6.3 6.5 34.1 1.57 1.38

Cambridge Industrial Trust CREIT SP 0.545 SGD 576 91.1% Quarter 1.19 8.7% 4.90 4.90 9.0 9.0 38.1 0.58 0.95

AIMS AMP Capital Indus REIT AAREIT SP 0.225 SGD 447 76.6% Quarter 0.40 7.1% 1.90 2.10 8.4 9.3 28.8 0.31 0.73

Mapletree Industrial Trust MINT SP 1.07 SGD 1,565 68.4% Not Yet 3.10 NM 3.10 7.46 6.6 7.0 38.5 0.86 1.24

Mapletree Logistics Trust* MLT SP 0.955 SGD 2,317 48.2% Quarter 1.78 6.5% 6.10 6.30 6.4 6.6 39.4 0.86 1.11

Cache Logistics Trust CACHE SP 0.965 SGD 612 72.7% Irreg 1.94 8.1% 6.70 8.20 6.9 8.5 22.7 0.92 1.05

Sabana Shariah Comp. Indus REIT SSREIT SP 0.98 SGD 620 84.0% None 0.00 NM 8.63 8.67 8.8 8.8 26.9 0.99 0.99

Ascendas India Trust AIT SP 0.925 SGD 708 63.5% Semi-Anl 1.70 7.4% 6.90 7.80 7.5 8.4 17.9 0.83 1.11

Industrial Average 10,912 7.3% 7.5 8.0 30.8 0.86 1.07

Residential

Saizen REIT SZREIT SP 0.165 SGD 185 88.6% Semi-Anl NA NA NA NA NA NA 35.5 0.40 0.41

Residential Average 185 NA NA NA 35.5 0.40 0.41

S-REITs Average 5.8% 5.80 6.29 30.4 1.24 0.94

First REIT FIRT SP 0.74 SGD 460 90.2% Quarter 1.94 10.5% 3.38 6.55 4.6 8.8 16.3 0.80 0.93

* Under OIR coverage

OIR estimates for FREIT, consensus estimates used for the rest. Note that FY10 figures for FREIT are due to dilution of new rights issue

Source: OIR estimates, Bloomberg consensus

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 21/27

P age 2 1 7 Janua ry 2011

F i r s t REIT

Healthy leverage ratio. FREIT has a healthy debt-to-assets leverage

ratio of 16.3%, which much lower than the S-REIT universe's average of

30.4%. Although FREIT has no credit rating and hence is restricted to aregulatory leverage ratio limit of 35%, we opine that there is ample headroom

for FREIT to continue its strategy of acquiring accretive healthcare-related

assets in the future. Management has guided that a comfortable long-term

leverage ratio would be 25%. We estimate that FREIT has a debt headroom

of around S$73.4m and S$181.6m before reaching management's target

and the regulatory limit respectively. Hence FREIT is well-equipped to grow

its portfolio size moving forward if the right opportunities come along, in our

opinion.

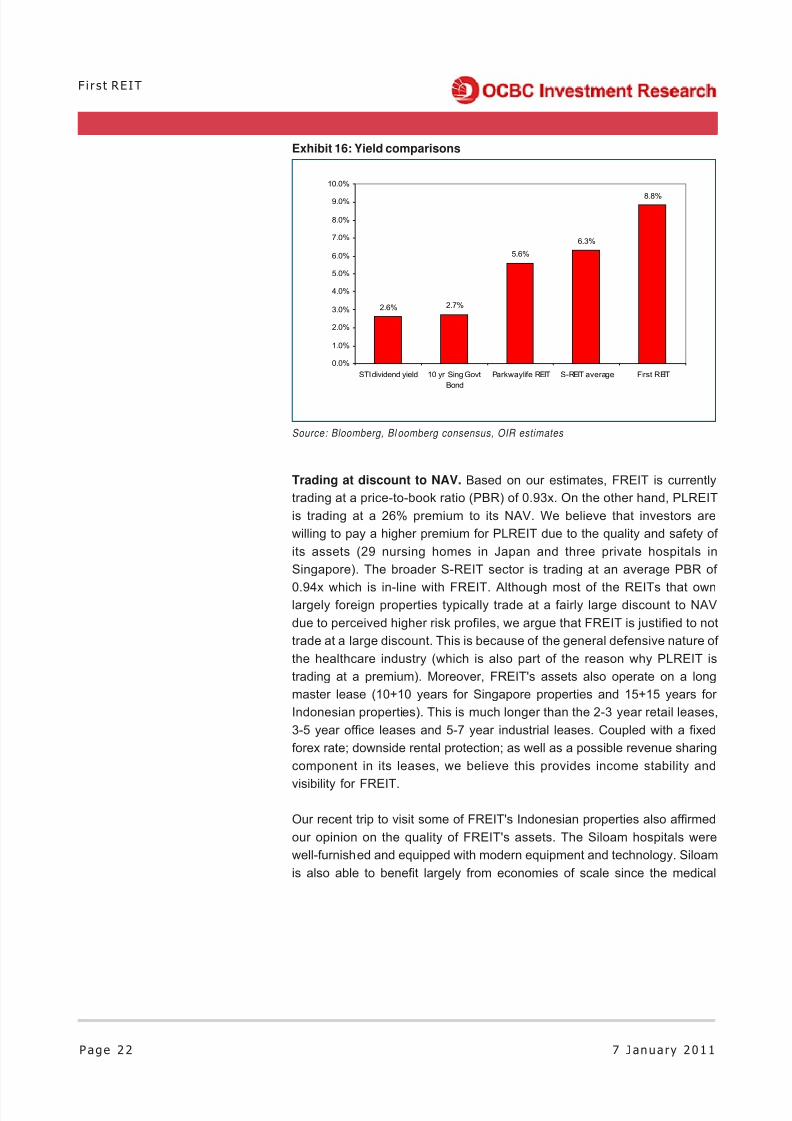

Attractive yields. Based on our DPU estimates, FREIT is trading at an

attractive forward yield of 8.8% for FY11. As FREIT's newly underwrittenrights units1 were issued and started trading on 31 Dec 10 (new units

accounted for in FY10's figures) while the rental revenue will only accrue in

FY11, we deem FY10's DPU and yield as not a meaningful gauge. FREIT's

FY11 distribution yield is an attractive 250 basis points (bp) above the S-

REIT average and 320 bp over ParkwayLife REIT (PLREIT) [NOT RATED],

its most directly comparable peer.

1 Recall that FREIT completed a 5-for-4 renounceable rights issue to fund the acquisitions

of MRCCC and SHLC. Hence a total of 345.7m new units were issued which rank pari

passu in all respects with the existing units.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 22/27

Page 2 2 7 Janua ry 2011

F i r s t REIT

Exhibit 16: Yield comparisons

Source: Bloomberg, Bl oomberg consensus, OIR estimates

2.6% 2.7%

5.6%

6.3%

8.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

STI dividend yield 10 yr Sing Govt

Bond

Parkwaylife REIT S-REIT average First REIT

Trading at discount to NAV. Based on our estimates, FREIT is currently

trading at a price-to-book ratio (PBR) of 0.93x. On the other hand, PLREIT

is trading at a 26% premium to its NAV. We believe that investors are

willing to pay a higher premium for PLREIT due to the quality and safety of

its assets (29 nursing homes in Japan and three private hospitals in

Singapore). The broader S-REIT sector is trading at an average PBR of

0.94x which is in-line with FREIT. Although most of the REITs that ownlargely foreign properties typically trade at a fairly large discount to NAV

due to perceived higher risk profiles, we argue that FREIT is justified to not

trade at a large discount. This is because of the general defensive nature of

the healthcare industry (which is also part of the reason why PLREIT is

trading at a premium). Moreover, FREIT's assets also operate on a long

master lease (10+10 years for Singapore properties and 15+15 years for

Indonesian properties). This is much longer than the 2-3 year retail leases,

3-5 year office leases and 5-7 year industrial leases. Coupled with a fixed

forex rate; downside rental protection; as well as a possible revenue sharing

component in its leases, we believe this provides income stability and

visibility for FREIT.

Our recent trip to visit some of FREIT's Indonesian properties also affirmed

our opinion on the quality of FREIT's assets. The Siloam hospitals were

well-furnished and equipped with modern equipment and technology. Siloam

is also able to benefit largely from economies of scale since the medical

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 23/27

P age 2 3 7 Janua ry 2011

F i r s t REIT

Exhibit 17: Indonesia property visit pictures

Source: OIR

Positive share price performance in 2010. Despite being touted largelyas defensive yield plays, the FTSE ST REIT Index has moved fairly in-line

with the broader market, posting a return of 10.6% in CY10 (10.1% for

STI). In particular, FREIT has returned an impressive gain of 19.1% while

PLREIT surged 35.2%. This could be attributed to both Healthcare REIT's

indirect play to the healthcare sector, which was the star performer of last

year. We believe that there could still be further upside potential ahead,

driven by the strong fundamentals of the healthcare sector.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 24/27

Page 2 4 7 Janua ry 2011

F i r s t REIT

Exhibit 18: Comparison of price performance - CY10

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

130.0%

140.0%

150.0%

3 1 / 1 2 / 2 0 0 9

3 1 / 0 1 / 2 0 1 0

2 8 / 0 2 / 2 0 1 0

3 1 / 0 3 / 2 0 1 0

3 0 / 0 4 / 2 0 1 0

3 1 / 0 5 / 2 0 1 0

3 0 / 0 6 / 2 0 1 0

3 1 / 0 7 / 2 0 1 0

3 1 / 0 8 / 2 0 1 0

3 0 / 0 9 / 2 0 1 0

3 1 / 1 0 / 2 0 1 0

3 0 / 1 1 / 2 0 1 0

First REIT STI Index FTSE ST REIT Index Parkwaylif e REIT

Source: Bloomberg

Earnings estimate. For the base rental, we assume a 2% increment p.a.

for the Indonesian portfolio based on our expectations of the CPI moving

forward. For the variable rent component, we estimate the Indonesian

hospitals and IAHCC to contribute an additional 1.25% and 0.75% of their

preceding year's gross revenue respectively. We also take into account

MRCCC and SHLC's base rental contribution accruing from FY11. These

considerations are underpinned by our view on the good growth potential of

Indonesia's healthcare sector.

Exhibit 19: FREIT financial data - FY07 - FY11F

28,29029,964 30,162 30,215

54,661

21,04220,96420,83119,277

41,276

0

10,000

20,000

30,000

40,000

50,000

60,000

FY07 FY08 FY09 FY10F FY11F

S $ ' 0 0 0

Gross Revenue Total distribution to Unitholders

Note: FY10F and FY11F's gross revenue estimates exclude deferred income by Pacific Cancer

Centre

Source: Company, OIR estimates

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 25/27

P age 2 5 7 Janua ry 2011

F i r s t REIT

Valuation methodology. We value FREIT using a RNAV-based valuation

model. For the purpose of valuing the investment properties, we assume a

WACC discount rate of 7.41% for its Singapore assets and a WACCdiscount rate of 10.41% for its Indonesian assets. As such, we derive a fair

value estimate of S$0.84.

Exhibit 20: RNAV fair value estimatein S$'000

Valuation of investment properties 652,593

Book value of investment properties 617,300

Surplus from investment properties attributableto unitholders 35,293

Book value 495,140

RNAV 530,433

No of Units in issue at end of period 630,373,997

RNAV per share (S$) 0.84

Current Price (S$) 0.740

Price Upside (%): 13.5%

Distribution Yield (%): 8.8%

Total Return (%): 22.4%

Source: OIR

Potential upside ahead; initiate with BUY. We believe that FREITrepresents a compelling investment story. This is driven by its income

stability due to its favourable master lease terms as well as the positive

prospects of Indonesia and Singapore's healthcare sector. We are sanguine

about the committed support which Lippo provides and the potential assets

in FREIT's pipeline. We also like management's strong execution capabilities

as demonstrated by the yield-accretive quality assets acquired over the

years. Our RNAV-derived fair value estimate of S$0.84 yields a potential

upside of 13.7% and a total return of 22.6%. As such, we initiate coverage

on FREIT with a BUY rating.

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 26/27

Page 2 6 7 Janua ry 2011

F i r s t REIT

First REIT's Key Financial Data

EARNINGS FORECAST BALANCE SHEET

Year Ended 31 Dec (S$m) FY08 FY09 FY10F FY11F As at 31 Dec (S$m) FY08 FY09 FY10F FY11F

Gross revenue 30.0 30.2 30.2 54.7 Investment properties 324.9 340.9 612.8 617.3

Property operating expenses -0.2 -0.3 -0.3 -0.6 Total non-current assets 324.9 340.9 612.8 617.3

Net property income 29.8 29.9 29.9 54.1 Cash and cash equivalents 12.4 11.5 14.4 8.9

Fees -3.1 -2.9 -3.0 -5.4 Total current assets 14.6 13.7 16.7 13.0

Net interest expense -1.6 -1.9 -3.8 -3.8 Total assets 339.5 354.7 629.5 630.3

Other expenses -0.6 -0.3 -0.5 -0.5 Current liabilities ex debt 10.6 10.2 10.3 11.8

Total return before tax 23.8 38.7 89.0 44.3 Debt 50.8 52.3 102.3 102.3

Income tax expense -0.8 -2.7 -17.8 -8.9 Total liabilities 84.4 83.6 133.7 135.2

Total return after tax 23.0 36.0 71.2 35.5 Total unitholders' funds 255.1 271.0 495.8 495.1

Total distribution to unitholders 20.8 21.0 21.0 41.3 Total equity and liabilities 339.5 354.7 629.5 630.3

CASH FLOW

Year Ended 31 Dec (S$m) FY08 FY09 FY10F FY11F KEY RATES & RATIOS* FY08 FY09 FY10F FY11F

Net cash from operations 20.6 22.7 10.5 44.1 DPU (S cents) 7.6 7.6 3.4 6.5

Increase in invt properties 0.0 -2.0 -205.5 -4.5 NAV per share (S$) 0.9 1.0 0.8 0.8

Net cash from investing 0.3 -2.0 -205.5 -4.4 Distr yield (%) 10.3 10.3 4.6 8.8

Proceeds from unitholders 0.0 0.0 172.8 0.0 P/CF (x) 9.8 9.0 44.1 10.6

Increase in borrowings 0.0 1.3 50.0 0.0 P/NAV (x) 0.8 0.8 0.9 0.9

Interest paid -1.8 -1.9 -3.9 -3.9 NPI margin (%) 99.3 99.0 99.0 99.0

Net cash from financing -22.1 -25.6 197.9 -45.2 Distr to revenue (%) 69.5 69.5 69.6 75.5

Net cash flow -1.2 -4.9 2.9 -5.5 Total debt/total assets (x) 15.0 14.7 16.3 16.2

Cash at beginning of year 13.6 12.4 11.5 14.4 ROE (%) 9.0 13.3 14.4 7.2

Cash at end of year 12.4 11.5 14.4 8.9 ROA (%) 6.8 10.1 11.3 5.6

Source: Company data, OIR estimates

*Note: FY10F's DPU and yield are due to dilution from new rights issue which traded on 31 Dec 10

8/8/2019 2010 Jun 07 - OCBC - First Reit

http://slidepdf.com/reader/full/2010-jun-07-ocbc-first-reit 27/27

F i r s t REIT

For OCBC Investment Research Pte Ltd

Carmen LeeHead of ResearchPublished by OCBC Investment Research Pte Ltd

SHAREHOLDING DECLARATION: The analyst/analysts who wrote this report holds NIL shares in the above security.

RATINGS AND RECOMMENDATIONS: OCBC Investment Research’s (OIR) technical comments and recommendations are short-term and trading oriented.- However, OIR’s f undamental views and ratings (Buy, Hold, Sell) are medium-term calls within a 12-month investment horizon. OIR’s Buy = More than 10% upside from the current price; Hold = Trade within +/-10% from the current price; Sel l = More than 10% downside from the current price.- For companies with less than S$150m market capitalization, OIR’s Buy = More than 30% upside from the current price; Hold = Trade within +/- 30% from the current price; Sell = More than 30% downside from the current price.

DISCLAIMER FOR RESEARCH REPORT This report is solely for information and general circulation only and may not be published, circulated,reproduced or distributed in whole or in part to any other person without our written consent. This report should not be construed as an offer or solicitation for the subscription, purchase or sale of the securities mentioned herein. Whilst we have taken all reasonable care to ensure that the information contained in this publication is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness, and you should not act on it without first independently verifying its contents. Any opinion or estimate contained in this report is subject to change without notice. We have not given any consideration to and we have not made any investigation of the investment objectives, financial situation or particular needs of the recipient or any class of persons, and accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of the recipient or any class of persons acting on such information or opinion or estimate. You may wish to seek advice from a financial adviser regarding the suitability of the securities mentioned herein, taking into consideration your investment objectives, financial situation or particular needs, before making a commitment to invest in the securities. OCBC Investment Research Pte Ltd, OCBC Securities Pte Ltd and their respective connected and associated corporations together with their respective directors and officers may have or take positions in the securities mentioned in this report and may also perform or seek to perform broking and other investment or securities related services for the corporations whose securities are mentioned in this report as well as other parties generally.

Privileged/Confidential information may be contained in this message. If you are not the addressee indicated in this message (or responsible for delivery of this message to such person), you may not copy or deliver this message to anyone. Opinions, conclusions and other information in this message that do not relate to the official business of my company shall not be understood as neither given nor endorsed by it.

Co.Reg.no.: 198301152E