![Frequently Asked Questions - AICPA...2 Introduction The Client Affiliates interpretation [AICPA, Professional Standards, ET sec. 1.224.010] under the Independence Rule” [AICPA, Professional](https://static.fdocuments.in/doc/165x107/5ed82c9b0fa3e705ec0df96e/frequently-asked-questions-aicpa-2-introduction-the-client-affiliates-interpretation.jpg)

2010 AICPA BEC Questions

43

2010 AICPA Newly Released Questions – Business Following are multiple choice questions recently released by the AICPA. These questions were released by the AICPA with letter answers only. Our editorial board has provided the accompanying explanation. Please note that the AICPA generally releases questions that it does NOT intend to use again. These questions and content may or may not be representative of questions you may see on any upcoming exams. 1 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

-

Upload

jklein2588 -

Category

Documents

-

view

476 -

download

3

description

Released BEC CPA Questions with explanation

Transcript of 2010 AICPA BEC Questions

2010 AICPA Newly Released Questions – Business

Following are multiple choice questions recently released by the AICPA. These

questions were released by the AICPA with letter answers only. Our editorial board has

provided the accompanying explanation.

Please note that the AICPA generally releases questions that it does NOT intend to use

again. These questions and content may or may not be representative of questions you

may see on any upcoming exams.

1 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

1. Which of the following economic terms describes a general decline in prices for goods and services and in the level of interest rates?

a. Expansion. b. Inflation. c. Deflation. d. Recession. Solution: Choice "c" is correct. Deflation is defined as a sustained decrease in the general prices of goods and services. It occurs when prices on average are falling over time. Most economists believe deflation is a much bigger economic problem than inflation.

Choice "a" is incorrect. Expansion describes the composition of business cycles.

Choice "b" is incorrect. Inflation is defined as a sustained increase in the general prices of goods and services. It occurs when prices on average are increasing over time.

Choice "d" is incorrect. Recession describes a business cycle.

2 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

2. The primary purpose of the consumer price index (CPI) is to: a. Establish a cost-of-living index. b. Identify the strength of an economic recovery. c. Help determine the Federal Reserve Bank's discount rate. d. Compare relative price changes over time. Solution: Choice "d" is correct. The CPI is a measure of the overall cost of a fixed basket of goods and services purchased by an average household. It is used to compare relative price changes over time.

Choice "a" is incorrect. The purpose of the CPI is not simply to establish a cost-of-living index, but also to compare relative price changes over time.

Choice "b" is incorrect. The CPI does not measure the strength of an economic recovery or any other phase of the business cycle.

Choice "c" is incorrect. Although CPI information may be considered by the Federal Reserve to determine the discount rate, that is not the primary purpose of the CPI.

3 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

3. Carter Co. paid $1,000,000 for land three years ago. Carter estimates it can sell the land for $1,200,000, net of selling costs. If the land is not sold, Carter plans to develop the land at a cost of $1,500,000. Carter estimates net cash flow from the development in the first year of operations would be $500,000. What is Carter's opportunity cost of the development? a. $1,500,000 b. $1,200,000 c. $1,000,000 d. $500,000 Solution: Choice "b" is correct. Opportunity cost is the potential benefit lost by selecting a particular course of action. In this question, opportunity cost is the revenue that will not occur ($1,200,000) if Carter develops the land instead of selling it.

Choice "a" is incorrect. The cost of development is not an opportunity cost of development.

Choice "c" is incorrect. The book value of the property is not an opportunity cost of development. The fair value that Carter can receive for the land is considered, not what the land originally cost.

Choice "d" is incorrect. The cash flow in the first year of operations is not an opportunity cost of development. It's an opportunity cost of selling the land.

4 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

4. What is the formula for calculating the profitability index of a project?

a. Subtract actual after-tax net income from the minimum required return in dollars. b. Divide the present value of the annual after-tax cash flows by the original cash invested in the project. c. Divide the initial investment for the project by the net annual cash inflow. d. Multiply net profit margin by asset turnover. Solution: Choice "b" is correct. The formula for the profitability index is:

=Present value of net future cash inflows Profitability indexPresent value of net inital investment

The profitability index is used to rank qualifying investments.

Note: The denominator maybe the "present value of the cash outflows" as opposed to "original cash invested" if the investment is not all made at the time of the initial investment.

Choice "a" is incorrect. Subtracting after tax net income from minimum required returns is an economic value added concept.

Choice "c" is incorrect. This is the formula for the payback period, not the profitability index.

Choice "d" is incorrect. Net profit times asset turnover is return on investment, not the profitability index.

5 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

5. Which of the following statements is correct regarding the weighted-average cost of capital (WACC)?

a. One of a company's objectives is to minimize the WACC. b. A company with a high WACC is attractive to potential shareholders. c. An increase in the WACC increases the value of the company. d. WACC is always equal to the company's borrowing rate. Solution: Choice "a" is correct. The optimal capital structure is the mix of financing instruments that produces the lowest WACC.

Choice "b" is incorrect. The opposite is true. A low WACC would indicate to potential shareholders that the company is being managed to produce the highest stockholder value.

Choice "c" is incorrect. The opposite is true. The mixture of debt and equity securities that produce the lowest WACC maximizes the value of the company.

Choice "d" is incorrect. The company's borrowing rate is a component of the WACC. Be careful of always, all, never, etc., answer choices. These answers are usually incorrect answer choices.

6 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

6. An increase in which of the following should cause management to reduce the average inventory?

a. The cost of placing an order. b. The cost of carrying inventory. c. The annual demand for the product. d. The lead time needed to acquire inventory. Solution: Choice "b" is correct. An increase in the cost of carrying inventory would lead to a reduction in average inventory. Suppose item A is required to be refrigerated so that it will not spoil. If electricity prices are rising, management would prefer to have a lower inventory of item A on hand because of the electricity (i.e., carrying) cost of that item.

Choice "a" is incorrect. An increase in the cost of placing an order would lead to an increase in average inventory. Management would increase the amount of inventory per order to reduce the number of orders, thereby causing the company to on average hold more inventory.

Choice "c" is incorrect. Increased demand would likely increase average inventory to avoid stockout costs.

Choice "d" is incorrect. An increase in lead-time would likely lead to an increase in average inventory. A higher safety stock likely would be needed to accommodate the lead-time to ensure that requirements are met.

7 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

7. Which of the following ratios would most likely be used by management to evaluate short-term liquidity?

a. Return on total assets. b. Sales to cash. c. Accounts receivable turnover. d. Acid test ratio. Solution: Choice "d" is correct. The acid test ratio evaluates short-term liquidity.

Choice "a" is incorrect. Return on total assets evaluates the profitability of a firm.

Choice "b" is incorrect. This is a distracter option. The sales to cash ratio does not evaluate liquidity.

Choice "c" is incorrect. Accounts receivable turnover is an activity ratio used to evaluate the overall efficiency of the firm. The number of days in the year, 365, divided by the accounts receivable turnover equals "days of sales outstanding."

8 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

8. Which of the following ratios would be used to evaluate a company's profitability?

a. Current ratio. b. Inventory turnover ratio. c. Debt to total assets ratio. d. Gross margin ratio. Solution: Choice "d" is correct. The gross margin ratio describes the ratio of gross margin to sales and serves to evaluate a company's profitability.

Choice "a" is incorrect. The current ratio evaluates a company's liquidity, not profitability.

Choice "b" is incorrect. Inventory turnover is an activity ratio used to evaluate the overall efficiency of the firm, not profitability. The number of days in the year, 365, divided by inventory turnover equals "days of inventory on hand."

Choice "c" is incorrect. Debt to total assets measures solvency, not profitability.

9 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

9. When a client's accounts payable computer system was relocated, the administrator provided support through a dial-up connection to a server. Subsequently, the administrator left the company. No changes were made to the accounts payable system at that time. Which of the following situations represents the greatest security risk?

a. User passwords are not required to be in alpha-numeric format. b. Management procedures for user accounts are not documented. c. User accounts are not removed upon termination of employees. d. Security logs are not periodically reviewed for violations. Solution: Choice "c" is correct. User accounts should immediately be disabled or removed upon termination of any employee. Enabled accounts for terminated employees present a great security risk since they allow unauthorized access to the system.

Choice "a" is incorrect. Passwords are usually required to be a combination of characters, but in comparison to failing to disable accounts for former employees, weak passwords do not present the greatest risk. Passwords, however weak they may be, provide at least some security.

Choice "b" is incorrect. While management procedures should always be documented, lack of documentation does not present a high security risk as long as there are procedures in place that are being used.

Choice "d" is incorrect. Security logs should be reviewed periodically by the administrator regardless of whether employees have left the company. While reviewing logs might detect unauthorized system access, allowing former employees to maintain active passwords has a high security risk of allowing the unauthorized access.

10 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

10. An entity doing business on the Internet most likely could use any of the following methods to prevent unauthorized intruders from accessing proprietary information except:

a. Password management. b. Data encryption. c. Digital certificates. d. Batch processing. Solution: Choice "d" is correct. An organization's use of batch processing has no effect on unauthorized access to proprietary information. Batch processing is a processing methodology not a security measure. Batch processing procedures include collection and grouping of input documents/transactions by type of transaction.

Choice "a" is incorrect. Password management is a method of preventing intrusion, since it regulates system access. Password management is the responsibility of the Security Administrator.

Choice "b" is incorrect. Data encryption is a method of preventing intrusion, since it uses a password or a digital key to scramble any readable data into a message unreadable to the intruder.

Choice "c" is incorrect. Digital certificates are forms of data security. They behave online in the same way driver's licenses, passports, and other trusted documents behave. Digital certificates are electronic documents, created and digitally signed by a trusted party that certifies the identity of the owners of a particular public key.

11 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

11. Which of the following information technology (IT) departmental responsibilities should be delegated to separate individuals?

a. Network maintenance and wireless access. b. Data entry and antivirus management. c. Data entry and application programming. d. Data entry and quality assurance. Solution: Choice "c" is correct. For internal control purposes, application programmers should not be allowed to enter data in production systems or unrestricted and uncontrolled access to application program change management systems. An application programmer is the person responsible for writing and/or maintaining application programs and should not be responsible for also controlling or handling data.

Choice "a" is incorrect. Network maintenance and wireless access are both responsibilities of the Network Administrator.

Choice "b" is incorrect. Data entry and antivirus management can safely be assigned to the same person, as they are not incompatible functions.

Choice "d" is incorrect. Data entry and quality assurance can safely be assigned to the same person, as they are not incompatible functions.

12 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

12. Which of the following transaction processing modes provides the most accurate and complete information for decision making?

a. Batch. b. Distributed. c. Online. d. Application. Solution: Choice "c" is correct. Online Processing (Online, Real-Time (OLRT) Processing) is an immediate processing method in which each transaction goes through all processing steps (data entry, data validation, and master file update) before the next transaction is processed. OLRT files are always current, and error detection is immediate.

Choice "a" is incorrect. Batch processing is most often found in "traditional" systems, such as payroll or general ledger systems, where the data in the system often is not totally current at all times.

Choice "b" is incorrect. Distributed is not a transaction processing mode.

Choice "d" is incorrect. Application is not a transaction processing mode. It typically represents a type of program used by an end user.

13 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

13. Which of the following is considered an application input control?

a. Run control total. b. Edit check. c. Report distribution log. d. Exception report. Solution: Choice "b" is correct. An edit check is an application input control that validates data before the data is successfully inputted. Batches containing transactions with errors, incorrect batch totals, and batches where debits do not equal credits are written to a suspended transaction file. These transactions are then corrected and resubmitted. All transactions must be corrected and resubmitted before end-of-month processing can begin.

Choice "a" is incorrect. A run control total is not an application input control, it is an output control. It is used to compare manual and computer-generated batch totals. With batch processing, a batch total for a transaction file is manually calculated and then an automated or manual comparison to a computer-generated batch control total is made. Any difference between the two totals indicates an error in accuracy, completeness, or both.

Choice "c" is incorrect. A report distribution log is not an application input control. Logs are used for data outputs.

Choice "d" is incorrect. An exception report is not an application input control. Exception reports are produced when a specific condition or exception occurs as a data output.

14 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

14. Which of the following terms refers to a site that has been identified and maintained by the organization as a data processing disaster recovery site but has not been stocked with equipment?

a. Hot. b. Cold. c. Warm. d. Flying start. Solution: Choice "b" is correct. A cold site is an off-site location that has all the electrical connections and other physical requirements for data processing, but does not have the actual equipment.

Choice "a" is incorrect. A hot site is an off-site location that is fully equipped to take over the company's data processing.

Choice "c" is incorrect. A warm backup site is a facility that is stocked with all the hardware necessary to create a reasonable facsimile of the primary data center. The warm backup site is the compromise between the hot backup site and the cold backup site.

Choice "d" is incorrect. Flying start is not a method of disaster recovery. This is a distracter.

15 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

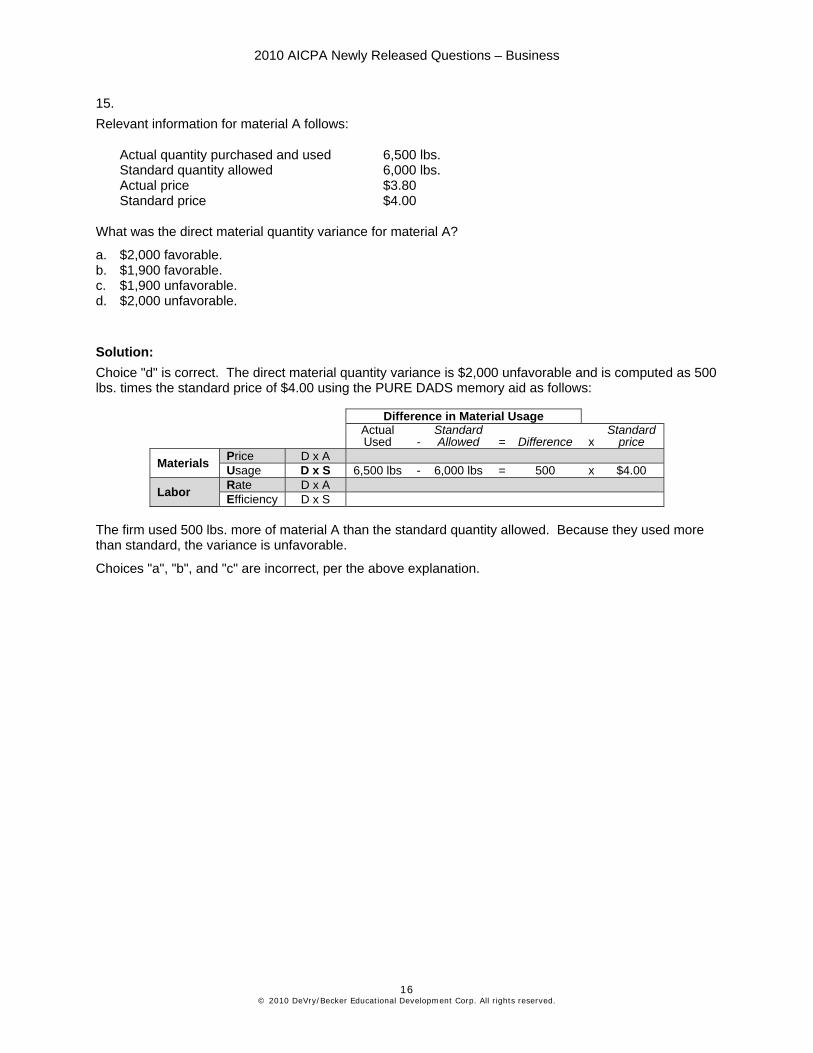

15. Relevant information for material A follows:

Actual quantity purchased and used 6,500 lbs. Standard quantity allowed 6,000 lbs. Actual price $3.80 Standard price $4.00

What was the direct material quantity variance for material A?

a. $2,000 favorable. b. $1,900 favorable. c. $1,900 unfavorable. d. $2,000 unfavorable. Solution: Choice "d" is correct. The direct material quantity variance is $2,000 unfavorable and is computed as 500 lbs. times the standard price of $4.00 using the PURE DADS memory aid as follows:

Difference in Material Usage Actual Used -

Standard Allowed = Difference x

Standard price

Materials Price D x A Usage D x S 6,500 lbs - 6,000 lbs = 500 x $4.00

Labor Rate D x A Efficiency D x S

The firm used 500 lbs. more of material A than the standard quantity allowed. Because they used more than standard, the variance is unfavorable.

Choices "a", "b", and "c" are incorrect, per the above explanation.

16 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

16. Smart Co. uses a static budget. When actual sales are less than budget, Smart would report favorable variances on which of the following expense categories? Sales commissions Building rent

a. Yes Yes b. Yes No c. No Yes d. No No Solution: Choice "b" is correct. Static budgets do not take changes in sales volume into account. Sales are less than budget, so sales commissions will also be less than budgeted. Sales commissions would have a favorable budget variance. Building rent is generally a fixed expense and is likely not influenced by the level of company sales. There would be no variance in building rent as a result of changes in sales volume.

Note: Favorable sales commission variance is not good news; it means actual sales are less than budgeted. Yet, variances from a static budget would show positive or "favorable" variances from budget. Flexible budget variances provide more meaningful information than static budget variances.

Choices "a", "c", and "d" are incorrect, per the above explanation.

17 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

17. An increase in production levels within a relevant range most likely would result in:

a. Increasing the total cost. b. Increasing the variable cost per unit. c. Decreasing the total fixed cost. d. Decreasing the variable cost per unit. Solution: Choice "a" is correct. An increase in production levels within the relevant range would likely cause variable costs to increase. While fixed costs would remain constant, total costs would increase.

Choice "b" is incorrect. Variable costs per unit would remain constant. However, total variable costs would increase.

Choice "c" is incorrect. Total fixed costs would remain constant.

Note: Fixed costs per unit would decrease.

Choice "d" is incorrect. Variable costs per unit would remain constant. Total variable costs will increase.

18 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

18. A CPA would recommend implementing an activity-based costing system under which of the following circumstances?

a. The client is a single-product manufacturer. b. Most of the client's costs currently are classified as direct costs. c. The client produced products that heterogeneously consume resources. d. The client produced many different products that homogeneously consume resources. Solution: Choice "c" is correct. ABC costing is recommended when more than one product is produced and those products do not uniformly consume indirect resources (heterogeneous consumption).

Example: Suppose 50 kilowatts of electricity is used to produce a single unit of item A and 500 kilowatts of electricity is used to produce a single unit of item B. To assign the cost of electricity (an indirect cost) based on the number of items produced would not reflect the true costs of producing the items.

Choice "a" is incorrect. ABC costing is most beneficial when multiple products are produced.

Choice "b" is incorrect. ABC costing is used to assign indirect costs based on the product's demands for resource-consuming activities. If the majority of the costs are direct, then ABC costing would not be recommended.

Choice "d" is incorrect. If resources are consumed in a homogeneous or uniform manner, ABC costing is not needed. A traditional cost system that uses a single cost driver would be appropriate in this situation.

19 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

19. A company that produces 10,000 units has fixed costs of $300,000, variable costs of $50 per unit, and a sales price of $85 per unit. After learning that its variable costs will increase by 20%, the company is considering an increase in production to 12,000 units. Which of the following statements is correct regarding the company's next steps?

a. If production is increased to 12,000 units, profits will increase by $50,000. b. If production is increased to 12,000 units, profits will increase by $100,000. c. If production remains at 10,000 units, profits will decrease by $50,000. d. If production remains at 10,000 units, profits will decrease by $100,000. Solution: Choice "d" is correct. Currently, the contribution margin per unit is $35 ($85 sales price minus $50 variable costs). If variable costs increase by 20%, the contribution margin per unit becomes $25 ($85 sales price minus $60 ($50 x 1.2) variable costs). The contribution margin will decrease by $10 per unit. If production remains at 10,000 units, profits will decrease by $100,000 (10,000 units times a $10 decrease in contribution margin per unit). Fixed costs are not relevant in this determination.

Choice "a" is incorrect. Increasing production by 2,000 units would decrease profit by $50,000 from the current levels (12,000 units times the new contribution margin of $25 per unit [$85 selling price minus the revised variable costs of $60 per unit] minus fixed costs of $300,000).

Choices "b" and "c" are incorrect, based on the above explanations.

20 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

20. A delivery company is implementing a system to compare the costs of purchasing and operating different vehicles in its fleet. Truck 415 is driven 125,000 miles per year at a variable cost of $0.13 per mile. Truck 415 has a capacity of 28,000 pounds and delivers 250 full loads per year. What amount is the truck's delivery cost per pound?

a. $0.00163 per pound. b. $0.00232 per pound. c. $0.58036 per pound. d. $1.72000 per pound. Solution: Choice "b" is correct. Delivery cost per pound is $0.00232 and is determined by dividing total variable costs by total delivered pounds. The computations are as follows:

• Total variable costs for Truck 415 is $16,250 (125,000 miles times $0.13 per mile). • Total pounds delivered are 7,000,000 (28,000 pounds times 250 loads). • Cost per delivered pound is $16,250 divided by 7,000,000, or $0.00232.

Choices "a", "c", and "d" are incorrect, based on the above explanation.

21 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

21. Which of the following is an assumption in a perfectly competitive financial market?

a. No single trader or traders can have a significant impact on market prices. b. Some traders can impact market prices more than others. c. Trading prices vary based on supply only. d. Information about borrowing/lending activities is only available to those willing to pay market prices. Solution: Choice "a" is correct. The inability of market participants (a single trader in this instance) to influence market prices is an attribute of perfect (pure) competition. Attributes of perfect competition also include a large number of suppliers, customers acting independently, very little product differentiation (homogeneous products), and no barriers to entry exist.

Choice "b" is incorrect. Market participants cannot influence prices in perfectly competitive markets.

Choice "c" is incorrect. Trading prices are based on both supply and demand in perfectly competitive markets.

Choice "d" is incorrect. Pricing information is available to all market participants in perfectly competitive markets.

22 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

22. A country's currency conversion value has recently changed from 1.5 to the U.S. dollar to 1.7 to the U.S. dollar. Which of the following statements about the country is correct?

a. Its exports are less expensive for the United States. b. Its currency has appreciated. c. Its imports of U.S. goods are more affordable. d. Its purchases of the U.S. dollar will cost less. Solution: Choice "a" is correct. The foreign country's exports will be less expensive for the United States since it will require fewer U.S. dollars to buy the foreign goods. If the conversion factor is 1.5 FCU to the USD, it takes $.666 to purchase one currency unit. When the conversion factor changes to 1.7 FCU to the USD, it takes $.588 to purchase one currency unit. Therefore, with the higher exchange rate the country's exports will be less expensive for the United States.

Choice "b" is incorrect. The currency has depreciated.

Choice "c" is incorrect. Imports of U.S. goods are less affordable. It will now require 1.7 units rather than the old 1.5 units to purchase every dollar of the same U.S. goods.

Choice "d" is incorrect. The currency of the foreign country will be able to buy fewer U.S. dollars per unit as a result of the change in the exchange rate.

23 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

23. Salem Co. is considering a project that yields annual net cash inflows of $420,000 for years 1 through 5, and a net cash inflow of $100,000 in year 6. The project will require an initial investment of $1,800,000. Salem's cost of capital is 10%. Present value information is presented below:

Present value of $1 for 5 years at 10% is .62. Present value of $1 for 6 years at 10% is .56. Present value of an annuity of $1 for 5 years at 10% is 3.79.

What was Salem's expected net present value for this project?

a. $83,000 b. ($108,200) c. ($152,200) d. ($442,000) Solution: Choice "c" is correct. Net present value is computed as the difference between project inflows and outflows, discounted to present value as follows:

Inflows: Years 1 through 5: $420,000 x 3.79 = $1,591,800 Year 6: $100,000 x .56 = $ 56,000 Present value of all inflows $1,647,800 Outflow (today, discount factor of 1.0) ($1,800,000) Net Present Value ($ 152,200)

Choices "a", "b", and "d" are incorrect, based on the above explanation.

24 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

24. SkyBound Airlines provided the following information about its two operating divisions:

Passenger Cargo Operating profit $40,000 $50,000 Investment 250,000 500,000 External borrowing rate 6% 8%

Measuring performance using return on investment (ROI), which division performed better?

a. The Cargo division, with an ROI of 10%. b. The Passenger division, with an ROI of 16%. c. The Cargo division, with an ROI of 18%. d. The Passenger division, with an ROI of 22%. Solution: Choice "b" is correct. The passenger division has an ROI of 16% ($40,000 operating profit divided by $250,000 investment). The cargo division has ROI of 10% ($50,000 operating profit divided by $500,000 investment). The passenger division performed better than the cargo division based on ROI.

Notice that a performance measure based on ROI considers the amount invested to yield return rather than the absolute amount of operating profit. Also note that the rate associated with financing is not relevant.

Choice "a" is incorrect. The cargo division ROI is 10%. However, the cargo division's ROI is lower than the passenger division's ROI of 16%. The passenger division performed better than the cargo division as measured by ROI.

Choices "c" and "d" are incorrect. Both answers incorrectly add the external borrowing rate.

25 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

25. Egan Co. owns land that could be developed in the future. Egan estimates it can sell the land for $1,200,000, net of all selling costs. If it is not sold, Egan will continue with its plans to develop the land. As Egan evaluates its options for development or sale of the property, what type of cost would the potential selling price represent in Egan's decision?

a. Sunk. b. Opportunity. c. Future. d. Variable. Solution: Choice "b" is correct. Opportunity cost is the potential benefit lost by selecting a particular course of action. If the land is developed rather than sold, the potential selling price foregone is an opportunity cost.

Choice "a" is incorrect. Sunk costs are those costs that have already been incurred, are unavoidable in the future and will not vary with the course of action taken. The potential selling price is not a sunk cost.

Choice "c" is incorrect. This is a distracter option.

Choice "d" is incorrect. Variable costs are costs of production that change in total with changes in volume. The potential selling price is not a variable cost.

26 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

26. Which of the following statements is correct regarding the payback method as a capital budgeting technique?

a. The payback method considers the time value of money. b. An advantage of the payback method is that it indicates if an investment will be profitable. c. The payback method provides the years needed to recoup the investment in a project. d. Payback is calculated by dividing the annual cash inflows by the net investment. Solution: Choice "c" is correct. The formula for calculating the payback period is:

Net Initial Investment / Increase in annual net after-tax cash flow

The payback method computes the years needed to recoup an investment. The net cash inflows are generally assumed to be constant for each period during the life of the project. It is often used for risky investments, since it shows how quickly the initial investment will be recouped.

Choice "a" is incorrect. The payback method does not consider the time value of money although a discounted payback method (which discounts the cash inflows) can be computed. The discounted payback method is identified as the discounted payback method.

Choice "b" is incorrect. The payback method does not measure profitability.

Choice "d" is incorrect. The payback formula is not computed as the ratio of annual cash flows to net investment.

27 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

27. Larson Corp. issued $20 million of long-term debt in the current year. What is a major advantage to Larson with the debt issuance?

a. The reduced earnings per share possible through financial leverage. b. The relatively low after-tax cost due to the interest deduction. c. The increased financial risk resulting from the use of the debt. d. The reduction of Larson's control over the company. Solution: Choice "b" is correct. Debt is generally the least expensive component of a company's capital structure. Debt typically commands a lower return than equity since debt contemplates a full return of principle over a specific period compared to equity that has no such guarantee and exposes the investor/creditor to lower risks. In addition, interest payments on debt are tax deductible, creating a tax shield for the debtor company. Lower rates reduced further by a tax shield give debt an advantage over equity financing.

Choice "a" is incorrect. Financial leverage presumes higher returns and earnings per share (EPS) as a result of issuing debt. Presuming increased net income because of the debt financed investment; EPS will increase since the number of shares issued and outstanding (the denominator) will not increase.

Choice "c" is incorrect. There is greater financial risk when debt is used.

Choice "d" is incorrect. The use of debt financing does not decrease control of the company. The use of equity financing decreases control of the company.

28 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

28. Green, Inc., a financial investment-consulting firm, was engaged by Maple Corp. to provide technical support for making investment decisions. Maple, a manufacturer of ceramic tiles, was in the process of buying Bay, Inc., its prime competitor. Green's financial analyst made an independent detailed analysis of Bay's average collection period to determine which of the following?

a. Financing. b. Return on equity. c. Liquidity. d. Operating profitability. Solution: Choice "c" is correct. A company's average collection period is used to evaluate the liquidity of the firm. Liquidity measurements focus on the ability of the company to meet obligations as they come due.

Choice "a" is incorrect. Average collection period does not evaluate financing.

Choice "b" is incorrect. Average collection period does not evaluate return on equity. Various returns on investment ratios would be used to evaluate return on equity.

Choice "d" is incorrect. Average collection period does not evaluate operating profitability. Gross margin measurements would give an indication of profitability.

29 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

29. Which of the following items would be most critical to include in a systems specification document for a financial report?

a. Cost-benefit analysis. b. Data elements needed. c. Training requirements. d. Communication change management considerations. Solution: Choice "b" is correct. Data elements should always be included in the system specification document for a financial report. Data elements define the building blocks of the information provided in a financial report.

Choice "a" is incorrect. Cost-benefit analysis would not be included in the system specification document. The determination that the benefits outweigh the costs of a particular system is determined before the development of specifications.

Choice "c" is incorrect. Training requirements would not be included in the systems specification document for a financial report. Training requirements associated with generating the report would be found in an implementation plan, but not in a systems specifications document.

Choice "d" is incorrect. Communication change management considerations would not be included in the specification document for a financial report. Change management contemplates the control monitoring procedures of the system, not the specifications of a financial report.

30 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

30. An enterprise resource planning (ERP) system has which of the following advantages over multiple independent functional systems?

a. Modifications can be made to each module without affecting other modules. b. Increased responsiveness and flexibility while aiding in the decision-making process. c. Increased amount of data redundancy since more than one module contains the same information. d. Reduction in costs for implementation and training. Solution: Choice "b" is correct. Enterprise Resource Planning (ERP) coordinates information to ensure timely and responsive reporting and data administration in support of decisions. An enterprise resource planning system is a cross-functional enterprise system that integrates and automates many business processes that work together in the manufacturing, logistics, distribution, accounting, finance, and human resource functions of a business. ERP software is comprised of a number of modules that can function independently or as an integrated system to allow data and information to be shared among all of the different departments and divisions of large businesses.

Choice "a" is incorrect. ERP presumes modifications affect other modules. In fact, the coordination of modules and information is how ERP adds value.

Choice "c" is incorrect. ERP systems store information in a central repository so that data may be accessed and used by various departments.

Choice "d" is incorrect. Implementation and training would increase, not reduce cost.

31 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

31. Which of the following structures refers to the collection of data for all vendors in a relational data base?

a. Record. b. Field. c. File. d. Byte. Solution: Choice "c" is correct. The collection of data for all vendors in a relational database is structured as a file. A file is a collection of related records, often arranged in some kind of sequence, such as a vendor file made up of vendor records and organized by vendor number.

Choice "a" is incorrect. A record is a group of fields that represents the data stored for a particular entity such as a vendor or an account payable.

Choice "b" is incorrect. A field is a group of bytes in which a specific data element such as a vendor number or name is stored

Choice "d" is incorrect. A byte is a group of eight bits that represent numbers or a letters, with the specific form dependent on what internal representation format is used. Sometimes, bytes are called characters.

32 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

32. During the annual audit, it was learned from an interview with the controller that the accounting system was programmed to use a batch processing method and a detailed posting type. This would mean that individual transactions were:

a. Posted upon entry, and each transaction had its own line entry in the appropriate ledger. b. Assigned to groups before posting, and each transaction had its own line entry in the appropriate

ledger. c. Posted upon entry, and each transaction group had a cumulative entry total in the appropriate ledger. d. Assigned to groups before posting, and each transaction group had a cumulative entry total in the

appropriate ledger. Solution: Choice "b" is correct. With batch processing, input documents/transactions are collected and grouped by type of transaction. These groups (called batches) are processed periodically (e.g., daily, weekly, monthly, etc.).

Example: A payroll system might use batch processing. Time sheets are batched in groups (batches), and inputted as single transactions. The individual transactions are then posted to a payroll record for tax and financial reporting.

Choices "a" and "c" are incorrect. Batch processing presumes grouping before posting. Posting upon entry is a characteristic of online real time processing.

Choice "d" is incorrect. Each transaction has its own line entry in the appropriate ledger and not a cumulative entry total. Transactions might be sorted by and regrouped by account for summary entry to various ledgers, but individual transactions maintain their identity.

33 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

33. A company has a significant e-commerce presence and self-hosts its web site. To assure continuity in the event of a natural disaster, the firm should adopt which of the following strategies?

a. Backup the server database daily. b. Store records off-site. c. Purchase and implement RAID technology. d. Establish off-site mirrored web server. Solution: Choice "d" is correct. An off-site mirrored web server allows the off-site web server to take over almost immediately in the event of a disaster, thereby providing nearly uninterrupted service and allowing for business continuity.

Choice "a" is incorrect. Backing up the server database daily will provide a second copy of the data; however, by storing it in the same location, it would also be at risk in the event of a natural disaster and would not be an effective business continuity strategy.

Choice "b" is incorrect. Records are stored off-site for many reasons and while it is important to have these records in the event of a disaster, it would take days or weeks to upload it into a new system, making it a poor strategy for business continuity.

Choice "c" is incorrect. RAID (Redundant Array of Independent Disks) is often used for disk storage. The basic idea of RAID is to combine multiple inexpensive disk drives into an array of disk drives to obtain performance, capacity and reliability that exceed that of a single large disk drive. This is implemented at the original location for disk storage and is not considered a disaster recovery and business continuity option.

34 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

34. Which of the following is the primary advantage of using a value-added network (VAN)?

a. It provides confidentiality for data transmitted over the Internet. b. It provides increased security for data transmissions. c. It is more cost effective for the company than transmitting data over the Internet. d. It enables the company to obtain trend information on data transmissions. Solution: Choice "b" is correct. Value Added Networks (VANs) are often used for electronic data interchange called EDI due to their increased security for data transmissions.

Choice "a" is incorrect. VANs are private networks while the Internet is a public network.

Choice "c" is incorrect. VANs normally charge a fixed fee plus a fee per transaction and can be prohibitively expensive for smaller companies. The Internet is a less secure but far cheaper option.

Choice "d" is incorrect. Trend information on data transmissions is likely available from value-added networks or most any data system that transmits information. The ability to obtain trend information is not unique and certainly not as advantageous as the security features associated with VANs.

35 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

35. Wexford Co. has a subunit that reported the following data for Year 1:

Asset (investment) turnover 1.5 times Sales $750,000 Return on sales 8%

The imputed interest rate is 12%. What is the division residual income for Year 1?

a. $60,000 b. $30,000 c. $20,000 d. $0 Solution: Choice "d" is correct. The residual income method measures the excess of actual income earned by an investment over the amount required to achieve a target or hurdle rate of return. The computation is simple; however, the fact pattern hides the basic information needed. Required data are computed as follows. Actual income earned is $60,000 (given sales of $750,000 times an 8% return on sales). The amount required to achieve the target rate of return is $60,000 (assets of $500,000 times 12%). Assets are computed to be $500,000 (sales of $750,000 divided by the asset turnover of 1.5). The imputed interest rate is the cost of capital or required return and is given at 12% of assets.

Based on the above, division residual income is $0 (actual income of $60,000 minus required income of $60,000).

Choices "a", "b", and "c" are incorrect, based on the above explanation.

36 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

36. The target capital structure of Traggle Co. is 50% debt, 10% preferred equity, and 40% common equity. The interest rate on debt is 6%, the yield on the preferred is 7%, the cost of common equity is 11.5%, and the tax rate is 40%. Traggle does not anticipate issuing any new stock. What is Traggle's weighted-average cost of capital?

a. 6.50% b. 6.77% c. 7.10% d. 8.30% Solution: Choice "c" is correct. The calculation is as follows:

Component % (1) After Tax Cost (2) Weighted Cost (1)*(2) Debt 50% 6% * (1-.4) = 3.6% 1.80% Preferred Equity 10% 7% .70% Common Equity 40% 11.5% 4.60% Total 7.10%

Note: Only the debt component is afforded a tax deduction and is multiplied by one minus the tax rate.

Choices "a", "b", and "d" are incorrect, based on the above explanation.

37 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

37. Galax, Inc. had operating income of $5,000,000 before interest and taxes. Galax's net book value of plant assets at January 1 and December 31 were $22,000,000 and $18,000,000, respectively. Galax achieved a 25 percent return on investment for the year, with an investment turnover of 2.5. What were Galax's sales for the year?

a. $55,000,000 b. $50,000,000 c. $45,000,000 d. $20,000,000 Solution: Choice "b" is correct. Sales are a component of the investment turnover ratio. The investment turnover formula is:

Investment turnover = sales / average investment

The fact pattern provides beginning and ending asset values and the amount of the investment turnover. The solution involves populating the variables in the investment turnover formula and solving for "x" (sales) as follows:

2.5 = sales / (($22,000,000 + $18,000,000)/2) 2.5 = sales / $20,000,000 Sales = $20,000,000 * 2.5 Sales = $50,000,000

Choices "a", "c", and "d" are incorrect, based on the above explanation.

38 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

38. Management has reviewed the standard cost variance analysis and is trying to explain an unfavorable labor efficiency variance of $8,000. Which of the following is the most likely cause of the variance?

a. The new labor contract increased wages. b. The maintenance of machinery has been inadequate for the last few months. c. The department manager has chosen to use highly skilled workers. d. The quality of raw materials has improved greatly. Solution: Choice "b" is correct. If machinery is inadequately maintained, there will be worker downtime for repairs. This will lead to an unfavorable efficiency variance.

Note: This is a logical theory type question that makes sense when it is logically thought through. Be sure to also think through the other options to see that they do not make sense!

Choice "a" is incorrect. New labor contracts that increase wages would lead to unfavorable rate variances, not efficiency variances.

Choice "c" is incorrect. Use of highly skilled workers should lead to a favorable efficiency variance because the workers are more proficient.

Choice "d" is incorrect. Raw materials of improved quality should lead to a favorable efficiency variance because the materials flow through the system easily and there would be less downtime and waste.

39 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

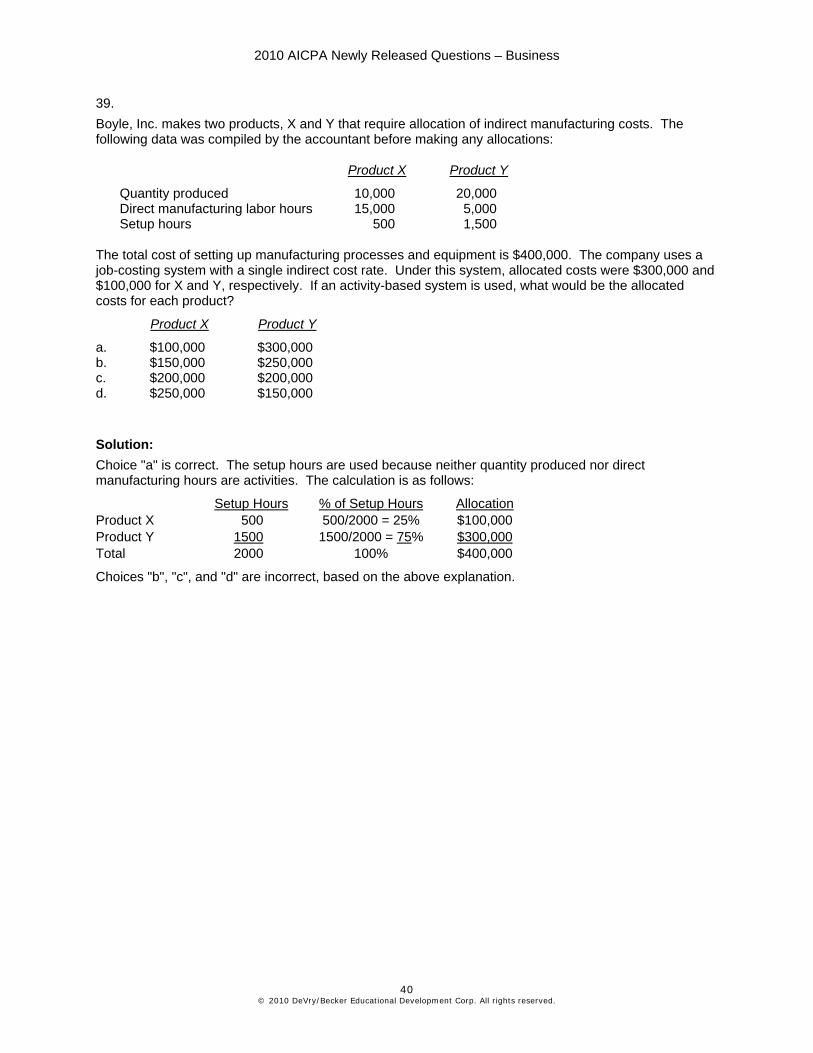

39. Boyle, Inc. makes two products, X and Y that require allocation of indirect manufacturing costs. The following data was compiled by the accountant before making any allocations:

Product X Product Y

Quantity produced 10,000 20,000 Direct manufacturing labor hours 15,000 5,000 Setup hours 500 1,500

The total cost of setting up manufacturing processes and equipment is $400,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were $300,000 and $100,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?

Product X Product Y

a. $100,000 $300,000 b. $150,000 $250,000 c. $200,000 $200,000 d. $250,000 $150,000 Solution: Choice "a" is correct. The setup hours are used because neither quantity produced nor direct manufacturing hours are activities. The calculation is as follows:

Setup Hours % of Setup Hours Allocation Product X 500 500/2000 = 25% $100,000 Product Y 1500 1500/2000 = 75% $300,000 Total 2000 100% $400,000

Choices "b", "c", and "d" are incorrect, based on the above explanation.

40 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

40. A company is offered a one-time special order for its product and has the capacity to take this order without losing current business. Variable costs per unit and fixed costs in total will be the same. The gross profit for the special order will be 10%, which is 15% less than the usual gross profit. What impact will this order have on total fixed costs and operating income?

a. Total fixed costs increase, and operating income increases. b. Total fixed costs do not change, and operating income increases. c. Total fixed costs do not change, and operating income does not change. d. Total fixed costs increase, and operating income decreases. Solution: Choice "b" is correct. Adding a job with a positive contribution margin within idle capacity will increase operating income. The company will still make a profit for the special order even though the gross profit percent will be lower. The question states that fixed costs in total will be the same (i.e., the company is operating within the relevant range). Variable costs per unit will be the same.

Note: Fixed costs per unit decrease with increased production.

Choices "a" and "d" are incorrect. Fixed costs will not increase within the relevant range.

Choice "c" is incorrect. Operating income will increase since the new job has a positive margin and is utilizing otherwise idle capacity.

41 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

41. According to the Sarbanes-Oxley Act of 2002, which of the following statements is correct regarding an issuer's audit committee financial expert?

a. The issuer's current outside CPA firm's audit partner must be the audit committee financial expert. b. If an issuer does not have an audit committee financial expert, the issuer must disclose the reason

why the role is not filled. c. The issuer must fill the role with an individual who has experience in the issuer's industry. d. The audit committee financial expert must be the issuer's audit committee chairperson to enhance

internal control. Solution: Choice "b" is correct. Sarbanes Oxley Section 407 requires that an issuer's audit committee have at least one financial expert, or disclose why that role is not filled. Section 407 requires that the financial expert have an understanding of GAAP and financial statements, be able to assess the application of accounting principles, have comparable experience applying accounting principles to entities that present a similar level of complexity of the issuer, and understand both internal controls and audit committee functions.

Choice "a" is incorrect. The audit committee is charged with negotiating the engagement of the external auditor and supervising their work. The auditor is accountable to the audit committee. The partner in charge of the audit firm engaged to do the audit should not be the financial expert on the audit committee.

Choice "c" is incorrect. Section 407 requires that the audit committee's financial expert understand the application of accounting principles to the issues representative of the complexity of the issuer but does not require specific experience in the industry. Section 407 defines four ways in which the necessary attributes of a financial expert can be achieved: education, experience supervising a financial officer, experience overseeing auditors, or other relevant experience.

Choice "d" is incorrect. Section 407 does not require that the audit committee's chairman be its financial expert.

42 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

2010 AICPA Newly Released Questions – Business

43 © 2010 DeVry/Becker Educational Development Corp. All rights reserved.

42. According to COSO, which of the following components of enterprise risk management addresses an entity's integrity and ethical values?

a. Information and communication. b. Internal environment. c. Risk assessment. d. Control activities.. Solution: Choice "b" is correct. Integrity and ethical values are addressed in the Internal Environment component of the Committee on Sponsoring Organizations Enterprise Risk Management Integrated Framework. Other elements of internal environment include risk management philosophy, risk appetite, organizational structure, assignment of authority and responsibility, and human resources standards.

Choice "a" is incorrect. The information and communication component of the Committee on Sponsoring Organizations Enterprise Risk Management Integrated Framework includes information and communications standards, not ethical values.

Choice "c" is incorrect. The risk assessment component of the Committee on Sponsoring Organizations Enterprise Risk Management Integrated Framework includes the identification of inherent and residual risk, the evaluation of likelihood and impact of risk, and data sources. Ethical values are not a primary component of this area.

Choice "d" is incorrect. The control activities component of the Committee on Sponsoring Organizations Enterprise Risk Management Integrated Framework includes types of control activities, policies and procedures, and integration of control issues with risk responses. Ethical values are not a primary component of this area.