©2010 @2014 Presented by: William H. Cooper, CPA, CGA, LLB And Moon Mah, CPA, CGA, LLB of Boughton...

19

©2010 @2014 @2014 Presented by: William H. Cooper, CPA, CGA, LLB And Moon Mah, CPA, CGA, LLB of Boughton Law Corporation a member of Meritas Law Firms Worldwide tax|mentor practical tax updates Trust and Estates Update Keeping Trust onside with the Income Tax Act Rules and the new Graduated Rate Rules A Brave New World

-

Upload

gabriel-french -

Category

Documents

-

view

216 -

download

0

Transcript of ©2010 @2014 Presented by: William H. Cooper, CPA, CGA, LLB And Moon Mah, CPA, CGA, LLB of Boughton...

©2010@2014@2014

Presented by:William H. Cooper, CPA, CGA, LLB

AndMoon Mah, CPA, CGA, LLBof Boughton Law Corporation

a member of Meritas Law Firms Worldwide

tax|mentor practical tax updates

Trust and Estates UpdateKeeping Trust onside with the Income Tax Act Rules and the new Graduated

Rate RulesA Brave New World

©2010@2014@2014

Table of Contents

VII. Distributions

VIII. Variations of a Trust

IX. The 21 year rule

X. Reporting and Record Keeping

XI. New rules for Testamentary Trusts

I. What is a Trust?

II. The Settlor

III. The Trustee(s)

IV. The Beneficiaries

V. Residence of a Trust

VI. The Trust Property

©2010

The Taxation of Trusts - A Tax Checklist

©2010@2014@2014

I. What is a Trust?

• A Trust is not a legal person/entity• A trust is a legal relationship between

Settlor, Trustee and Beneficiaries • A Trust is taxed as an Individual – s.104(2)• Using a trust in estate plannin

©2010@2014@2014

• The settlor establishes the trust relationship with the settlement of property

• Where is the initial Trust Settlement Property?

• Basic Rules on Settlements and Transfers to Trusts

• Keep the records of payments used to settle the Trust and provide initial funding

• Who loaned the initial start up funds – make sure it was a documented loan

• No funds transferred to trust except by commercial loan or return on investments

(cont…)

II. The Settlor

©2010@2014@2014

II. The Settlor (cont…)

Basic Rules (cont…)• Trace funds used to buy the initial trust

investment (shares) to ensure they didn’t come from a beneficiary or a trustee

• Avoid advisor loan funding

• Compliance Points — are there any reversionary

• interests that offend s.75(2)?• R. v. Sommerer, 2012 CarswellNat 2441, 2012

FCA 207, 2012 D.T.C. 5126, [2014] 1 F.C.R. 379, 2012 CAF 207 (Federal Court of Appeal) — s.75(2) does not apply to a genuine sale

• T12013-049921117 — a transfer for less than FMV may be a contribution

©2010@2014@2014

• Trustee(s) hold and manage assets for the benefit of the beneficiaries

• Who is conducting the affairs of the trust? – a principal of the Company (ie: client who caused the trust to be settled) or the trustees?

• Are the trustees aware of their duties and obligations and do they keep trustee minutes?

III. The Trustee(s)

©2010@2014@2014

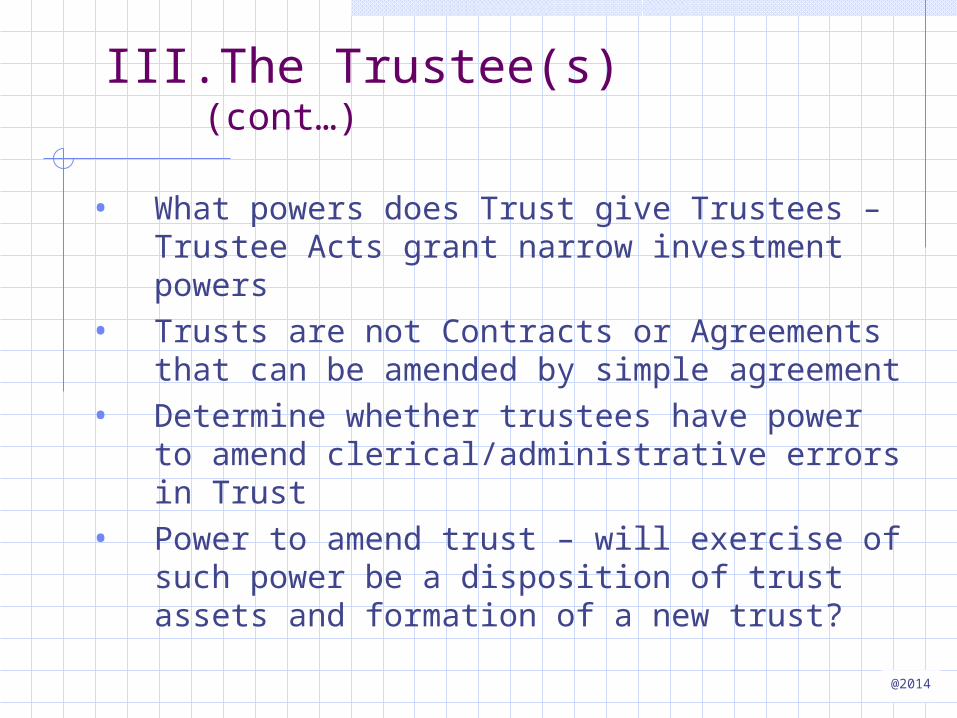

III. The Trustee(s) (cont…)

• What powers does Trust give Trustees – Trustee Acts grant narrow investment powers

• Trusts are not Contracts or Agreements that can be amended by simple agreement

• Determine whether trustees have power to amend clerical/administrative errors in Trust

• Power to amend trust – will exercise of such power be a disposition of trust assets and formation of a new trust?

©2010@2014@2014

III. The Trustee(s) (cont…)

• Compliance Points• Change of Trustee(s) — change of control and

deemed year end under s.249(4)?• Examine the association rules and the look-

through rules in s.256(1.2)

©2010@2014@2014

IV. The Beneficiaries

• Who are the beneficiaries, named, potential, contingent? Prepare a list

• Compliance Points• Have beneficiaries become non-resident of Canada

(withholding/ no rollout under s.107(5)/reporting obligations in the US)?

• Association look through rules in s.256(1.2)(f)(ii)

©2010@2014@2014

V. Residence of a Trust

• The residence of Trustees may determine Trust’s residence – but CRA may look to Central Management and Control

• Trustees should be actively engaged in their duties and understand their obligations

• Keep trustee resolutions and record all trustees actions and decisions

• If Trust residence not in “Principal’s” jurisdiction – i.e. BC Corp owned by Alberta Trust – make sure the AB Trustees are active managers - not order takers

©2010@2014@2014

V. Residence of a Trust (cont…)

• Compliance Points• Garron Family Trust (Trustee of) v. R., 2012

CarswellNat 953, 2012 SCC 14, 75 E.T.R. (3d) 1, [2012] 3 C.T.C. 265, 343 D.L.R. (4th) 670, 2012 D.T.C. 5064 (Fr.), 2012 D.T.C. 5063 (Eng.), 428 N.R. 202, [2012] 1 S.C.R. 520 (Supreme Court of Canada)

• Deemed resident under s.94

©2010@2014@2014

VI. The Trust Property

• Are shares included in the trust property?• Ensure assets are properly acquired by trust

to ensure no contributions or attribution• Obtain the articles, share registers and

director’s registers for any companies in which the trust holds shares

• Compliance Points• Loss of small business corporation status - QSBCs

and attribution under s.74.4(2) and s.74.5(5)?

©2010@2014@2014

VII. Distributions

• Basic Rules• Have there been trustee resolutions and

designations made to verify the nature of the income – i.e. s.104(19) for dividends?

• Has the company paying dividends prepared the appropriate dividend declaration resolutions?

• Have trust flow through payments been made in cash or by promissory note?

©2010@2014@2014

VII. Distributions (cont…)

• Basic Rules (cont…) • Does the “kiddie tax” apply to the trust – s.120.4?• Have distributions to minor beneficiaries been

properly documented where payments were made to adults on their behalf?

• Do the adult recipients have receipts, accounting or bank records to track the use of funds for the benefit of minors?

©2010@2014@2014

VIII. Variation of a Trust

• Variation may result in resettlement of trust?• Variation may result in disposition of interest

by beneficiary?

©2010@2014@2014

IX. The 21 Year Rule

• Record the settlement date and the 21 year deemed disposition date in a “Bring Forward”

• Make plans for the Trust property well in advance of the deemed disposition date

• Consider Trust’s provisions for distribution of the trust property – what is wind up date

• Examine the current circumstances of the beneficiaries – have plans for distribution changed?

• Can the trust capital be distributed tax free under s.107(2) or is s.75(2) a s.107(4.1) problem?

©2010@2014@2014

X. Reporting and Record Keeping

• Place the originally signed trust in safe place and include year of creation in the Trust Name

• Keep Trust Financial Statements to stay honest on funds in trust bank account

• File T3s even when no income – nil assessment will go statute barred

• Keep a separate trust bank account• Who keeps the records: the client, the accountant

or the lawyer? Should Trust keep a minute book?• Accountant to keep copy in current Trust accounting

file with notation as to location of original

©2010@2014@2014

XI. New Rules for Testamentary Trusts

• Elimination of graduated rates for testamentary trusts

• Graduated rate estate

• Tax accrued gains of certain trusts in the Deceased Beneficiary's terminal return rather than in the trust itself

• Possible allocation of charitable donations between deceased and estate

©2010@2014@2014

Trust and Estates Update - Keeping Trust onside with the Income Tax Act Rules and the new Graduated Rate Rules - A Brave New World

Thank -you

tax|mentor practical tax updates