2010-09-30-PH-S-SCC

5

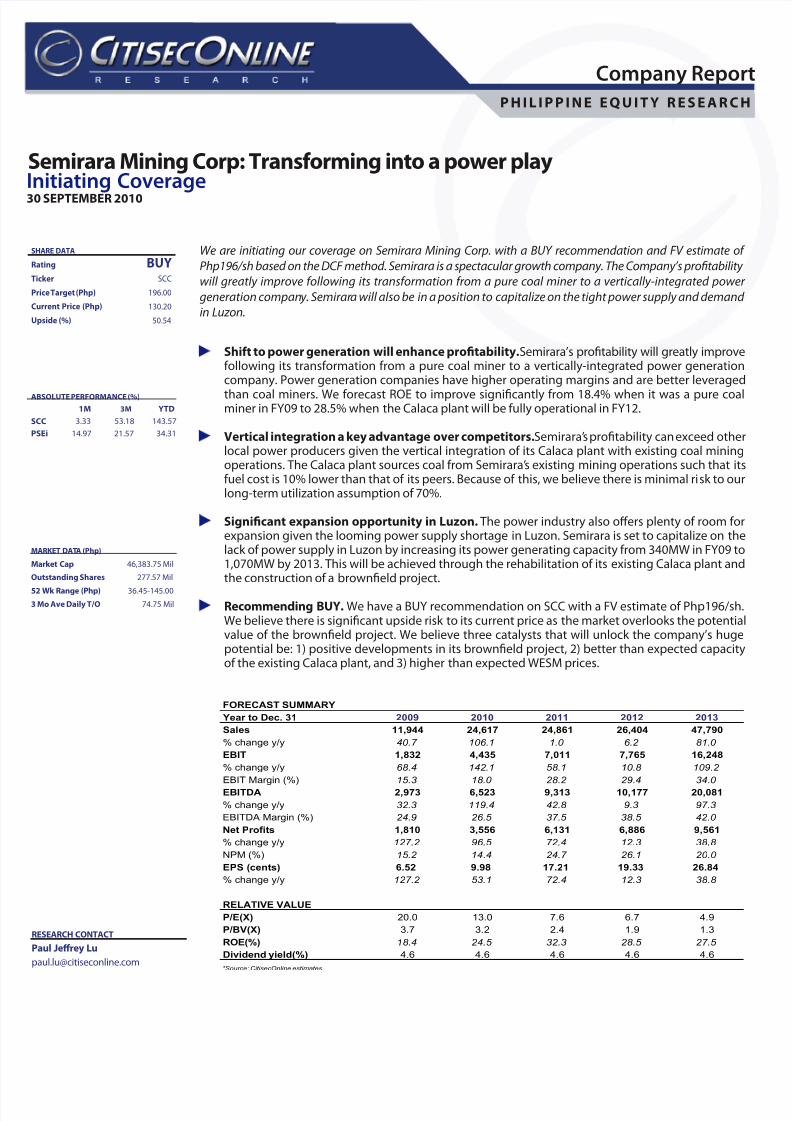

Company Report PHILIPPINE EQUITY RESEARCH Semirara Mining Corp: Trans orming into a power play Initiating Coverage RESEARCH CONTACT Paul Jerey Lu [email protected] Shit to power generation will enhance proftability.Semirara’s protability will greatly improve ollowing its transormation rom a pure coal miner to a vertically-integrated power generation company. Power generation companies have higher operating margins and are better leveraged than coal miners. We orecast ROE to improve signicantly rom 18.4% when it was a pure coal miner in FY09 to 28.5% when the Calaca plant will be ully operational in FY12. Vertical integration a key advantage over competitors. Semirara’ s protability can exceed other local power producers given the vertical integration o its Calaca plant with existing coal mining operations. The Calaca plant sources coal rom Semirara’ s existing mining operations such that its uel cost is 10% lower than that o its peers. Because o this, we believe there is minimal ri sk to our long-term utilization assumption o 70%. Signifcant expansion opportunity in Luzon. The power industry also oers plenty o room or expansion given the looming power supply shortage in Luzon. Semirara is set to capitalize on the lack o power supply in Luzon by increasing its power generating capacity rom 340MW in FY09 to 1,070MW by 2013. This will be achieved through the rehabilitation o its existing Calaca plant and the construction o a browneld project. Recommending BUY. We have a BUY recommendation on SCC with a FV estimate o Php196/sh. We believe there is signicant upside risk to its current price as the market overlooks the potential value o the browneld project. We believe three catalysts that will unlock the company’s huge potential be: 1) positive developments in its browneld project, 2) better than expected capacity o the existing Calaca plant, and 3) higher than expected WESM prices. We are initiating our coverage on Semirara Mining Corp. with a BUY recommendation and FV estimate o Php196/sh based on the DCF method. Semirara is a spectacular growth company. The Company’s proftability will greatly improve ollowing its transormation rom a pure coal miner to a vertically-integrated power generation compan y. Semirar a will also be in a position to capitalize on the tight power supply and demand in Luzon. 30 SEPTEMBER 2010 SHARE DATA Rating BUY Ticker SCC Price Target (Php) 196.00 Current Price (Php) 130.20 Upside (%) 50.54 ABSOLUTE PERFORMANCE (%) 1M 3M YTD SCC 3.33 53.18 143.57 PSEi 14.97 21.57 34.31 FORECAST SUMMARY Year to Dec. 31 2009 2010 2011 2012 2013 Sales 11,944 24,617 24,861 26,404 47,790 % change y/y 40.7 106.1 1.0 6.2 81.0 EBIT 1,832 4,435 7,011 7,765 16,248 % change y/y 68.4 142.1 58.1 10.8 109.2 EBIT Margin (%) 15.3 18.0 28.2 29.4 34.0 EBITDA 2,973 6,523 9,313 10,177 20,081 % change y/y 32.3 119.4 42.8 9.3 97.3 EBITDA Margin (%) 24.9 26.5 37.5 38.5 42.0 Net Profits 1,810 3,556 6,131 6,886 9,561 % change y/y 127.2 96.5 72.4 12.3 38.8 NPM (%) 15.2 14.4 24.7 26.1 20.0 EPS (cents) 6.52 9.98 17.21 19.33 26.84 % change y/y 127.2 53.1 72.4 12.3 38.8 RELATIVE VALUE P/E(X) 20.0 13.0 7.6 6.7 4.9 P/BV(X) 3.7 3.2 2.4 1.9 1.3 ROE(%) 18.4 24.5 32.3 28.5 27.5 Dividend yield(%) 4.6 4.6 4.6 4.6 4.6 *Source: CitisecOnline estimates MARKET DATA (Php) Market Cap 46,383.75 Mil Outstanding Shares 277.57 Mil 52 Wk Range (Php) 36.45-145.00 3 Mo Ave Daily T/O 74.75 Mil

Transcript of 2010-09-30-PH-S-SCC

8/8/2019 2010-09-30-PH-S-SCC

http://slidepdf.com/reader/full/2010-09-30-ph-s-scc 1/5

Company Repo

P H I L I P P I N E E Q U I T Y R E S E A R C

Semirara Mining Corp: Transorming into a power playnitiating Coverage

RESEARCH CONTACT

Paul Jerey Lu

Shit to power generation will enhance proftability. Semirara’s protability will greatly improveollowing its transormation rom a pure coal miner to a vertically-integrated power generationcompany. Power generation companies have higher operating margins and are better leveraged

than coal miners. We orecast ROE to improve signicantly rom 18.4% when it was a pure coaminer in FY09 to 28.5% when the Calaca plant will be ully operational in FY12.

Vertical integration a key advantage over competitors.Semirara’s protability can exceed othelocal power producers given the vertical integration o its Calaca plant with existing coal miningoperations. The Calaca plant sources coal rom Semirara’s existing mining operations such that ituel cost is 10% lower than that o its peers. Because o this, we believe there is minimal risk to oulong-term utilization assumption o 70%.

Signifcant expansion opportunity in Luzon. The power industry also oers plenty o room oexpansion given the looming power supply shortage in Luzon. Semirara is set to capitalize on thelack o power supply in Luzon by increasing its power generating capacity rom 340MW in FY09 to1,070MW by 2013. This will be achieved through the rehabilitation o its existing Calaca plant andthe construction o a browneld project.

Recommending BUY. We have a BUY recommendation on SCC with a FV estimate o Php196/shWe believe there is signicant upside risk to its current price as the market overlooks the potentiavalue o the browneld project. We believe three catalysts that will unlock the company’s hugepotential be: 1) positive developments in its browneld project, 2) better than expected capacityo the existing Calaca plant, and 3) higher than expected WESM prices.

We are initiating our coverage on Semirara Mining Corp. with a BUY recommendation and FV estimate o

Php196/sh based on the DCF method. Semirara is a spectacular growth company. The Company’s proftability

will greatly improve ollowing its transormation rom a pure coal miner to a vertically-integrated powe

generation company. Semirara will also be in a position to capitalize on the tight power supply and demand

in Luzon.

0 SEPTEMBER 2010

SHARE DATA Rating BUYTicker SCC

Price Target (Php) 196.00

Current Price (Php) 130.20

Upside (%) 50.54

ABSOLUTE PERFORMANCE (%)

1M 3M YTD

SCC 3.33 53.18 143.57

PSEi 14.97 21.57 34.31

FORECAST SUMMARY

Year to Dec. 31 2009 2010 2011 2012 2013

Sales 11,944 24,617 24,861 26,404 47,790

% change y/y 40.7 106.1 1.0 6.2 81.0

EBIT 1,832 4,435 7,011 7,765 16,248

% change y/y 68.4 142.1 58.1 10.8 109.2

EBIT Margin (%) 15.3 18.0 28.2 29.4 34.0

EBITDA 2,973 6,523 9,313 10,177 20,081

% change y/y 32.3 119.4 42.8 9.3 97.3

EBITDA Margin (%) 24.9 26.5 37.5 38.5 42.0

Net Profits 1,810 3,556 6,131 6,886 9,561

% change y/y 127.2 96.5 72.4 12.3 38.8

NPM (%) 15.2 14.4 24.7 26.1 20.0

EPS (cents) 6.52 9.98 17.21 19.33 26.84

% change y/y 127.2 53.1 72.4 12.3 38.8

RELATIVE VALUE

P/E(X) 20.0 13.0 7.6 6.7 4.9

P/BV(X) 3.7 3.2 2.4 1.9 1.3

ROE(%) 18.4 24.5 32.3 28.5 27.5

Dividend yield(%) 4.6 4.6 4.6 4.6 4.6

*Source: CitisecOnline estimates

MARKET DATA (Php) Market Cap 46,383.75 Mil

Outstanding Shares 277.57 Mil

52 Wk Range (Php) 36.45-145.00

3 Mo Ave Daily T/O 74.75 Mil

8/8/2019 2010-09-30-PH-S-SCC

http://slidepdf.com/reader/full/2010-09-30-ph-s-scc 2/5

8/8/2019 2010-09-30-PH-S-SCC

http://slidepdf.com/reader/full/2010-09-30-ph-s-scc 3/5

30 SEPTEMBER 20

SCC/Inititating Coverage/ page 3

Given Semirara’s entry into the more lucrative power industry,we orecast ROE to improve signicantly rom 18.4% when it wasa pure coal miner in FY09 to 28.5% when the Calaca plant will beully operational in FY12. During its rst year o operating the Calacaplant, we already orecast ROE to improve to 24.5%.

Vertical integration is a key advantage overcompetitors

Semirara’s protability can exceed other local power producersgiven the vertical integration o its Calaca plant with existing coalmining operations. The Calaca plant sources coal rom Semirara’sexisting mining operations such that its uel cost is 10% lower thanthat o its peers. Semriara’s vertically integrated nature also protects

its power business rom the threat o high coal prices. Pure powerproducers are vulnerable to margin squeeze should coal pricesincrease. However, the uel costs o vertically-integrated powergeneration companies are fat regardless o the movement in coalprices.

Semirara plans to use this advantage to optimize the utilization o itsplants. Management said it can reduce the selling price to improveits competitiveness in the market. Because o this, we believe thereis minimal risk to our long-term utilization assumption o 70%.

Exhibit 4: Calaca Plant Key Assumptions

Source: COL estimates

Signifcant expansion opportunity in Luzon

The power industry also oers plenty o room or expansion giventhe looming power supply shortage in Luzon. According to the DOE,capacity in the Luzon grid may not meet the demand and reservemargin requirement in 2011. With the 650MW Malaya Oil Thermalplant scheduled or retirement in 2011, dependable capacitywill decrease by 6.5% to 9,380MW, leaving the system in need o

300MW in terms o peaking capacity. In the next 20 years, the supplysituation could remain tight as the Luzon grid requires 12,500MWo additional capacity. Currently, only 600MW o additional capacity(to be completed by 4Q12) has been committed.

Exhibit 5: Luzon Grid Situation

Source: DOE

Semirara is set to capitalize on the lack o power supply in LuzonIt plans to increase its power generating capacity rom 340MW inFY09 to 1,070MW by 2013. The Company is already rehabilitatingthe Calaca plant to increase its capacity by at least 38.2% to 470MW

The rehabilitation is expected to cost US$120Mil and should becompleted by February 2011. Meanwhile the Company is alsoundertaking a easibility study to put up a 600MW coal-red plantnear the existing Calaca plant. Should plans push through, thebrowneld project is estimated to cost US$800Mil and should becompleted in 2013.

Exhibit 6: SCC Power Generation Capacity

Source: SCC, COL estimates

FY10 FY11 FY12

Effective Capacity 340MW 470MW 470MW

Average Utilization 34% 63% 70%

Contracted Price Php4.80/KWh Php4.80/KWh Php4.80/KWh

WESM Price Php6.40/KWh Php5.00/KWh Php5.00/KWh

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

2009 2010 2011 2012 2013 2014 2015 2016

Existi ng Capaci ty Commi tted Capaci ty

I nd ic ati ve Ca pa ci ty P ea k Dema nd +Req ui red Res er ve Ma rgi n

0

200

400

600

800

1,000

1,200

FY10E FY11E FY12E FY13E

8/8/2019 2010-09-30-PH-S-SCC

http://slidepdf.com/reader/full/2010-09-30-ph-s-scc 4/5

30 SEPTEMBER 20

SCC/Inititating Coverage/ page 4

The additional capacity rom the rehabilitation and expansion planswill be the main driver or uture earnings growth. The 130MWadditional capacity rom the rehabilitation plans (and the ull-yearoperation o the Calaca plant) will boost the power segment’searnings by a 2-year CAGR o 89.1% to Php4.9Bil in FY12. Meanwhile,the 600MW capacity o the browneld project should add anotherPhp2.7Bil to earnings in FY13.

Exhibit 7: Calaca Expansion Key Assumptions

Source: COL estimates

Signifcant upside potential rom the currentmarket price

Our FV estimate on Semirara is Php196/sh based on the DCFmethod. This estimate can be broken down to Php151/sh orexisting operations and Php45/sh or the browneld project. Thereis minimal risk to investors given that the current market price onlyrefects the value o Semirara’s existing operations. Meanwhile,there is signicant upside risk as the market overlooks the potentialvalue o the browneld project.

Our FV estimate or existing operations is conservative. At Php151/sh, existing operations would only be valued at 8.8X FY11 P/E.Despite its advantage o being a vertically-integrated powerproducer, Semriara is being valued lower than the 12.6X FY11 P/Eo local and regional peers. Furthermore, we used conservativeassumptions to value the existing Calaca plant. Our average sellingprice assumption o Php5.00/KWh is much lower than the Php5.50/KWh blended rate in 1H10. Our assumed 470MW capacity aterrehabilitation is also at the lower end o management’s guidanceo 470MW to 550MW.

Exhibit 8: Local and Regional Peers

Source: Bloomberg; COL estimates

Exhibit 9: Sensitivity Matrix for Existing Operations

Source: COL estimates

Semirara’s huge upside rom the current market price will stemrom the value o the browneld project. We believe there is astrong likelihood that the browneld project will push throughFirst, additional power generation capacity will urther increasethe value o its coal resources. The tight power supply and demand

situation in Luzon also makes the project an even more attractiveinvestment. Second, management is already in talks with Meralcoand Marubeni, which are expected to be strategic partners or theproject. Meralco will provide a willing taker or the generated powewhile Marubeni will provide lower cost o nancing the projectFinally, Semirara can und the project. Even by itsel, the Companyis projected to generate Php9Bil operating cash fow rom existingoperations annually and has a low debt-to-equity ratio o only 0.8X

Recommending a BUY

Our initiating coverage on Semirara calls or a BUY recommendationand an FV estimate o Php196/sh. Semirara’s transormation rom

a pure coal miner to a vertically-integrated power generationcompany and its aggressive expansion plan will uel rapidearnings growth until FY13. We believe three catalysts will unlockthe Company’s huge potential: 1) positive developments in itsbrowneld project, 2) better-than-expected capacity o the existingCalaca plant, and 3) higher-than-expected WESM prices.

FY13

Effective Capacity 600MW

Estimated Cost US$800Mil

Ownership 50%

Average Utilization 85%

Contracted Price Php4.80/KWh

470MW 490MW 510MW 530MW 550MW

4.00/KWh 131.10 136.31 141.52 146.73 151.93

4.50/KWh 141.10 146.74 152.37 158.00 163.63

5.00/KWh 151.10 157.16 163.22 169.27 175.33

5.50/KWh 161.10 167.58 174.07 180.55 187.03

6.00/KWh 171.10 178.00 184.91 191.82 198.73

FY11 P/E FY11 EPS Growth

Energy Development Corp. 14.1 -12.4%Aboitiz Power Corp. 8.1 -10.5%

China Resources Power Holdings 11.8 18.5%

China Power International Development 12.6 37.3%

Huaneng Power International Inc 13.4 11.0%

Datang International Power Generation Co. 15.9 36.8%

Average 12.6 13.5%

Semirara Mining Corp. 8.8 72.4%

8/8/2019 2010-09-30-PH-S-SCC

http://slidepdf.com/reader/full/2010-09-30-ph-s-scc 5/5

30 SEPTEMBER 20

SCC/Inititating Coverage/ page 5

INVESTMENT RATING DEFINITIONS

TOP PICK DEFINITIONA stock that is included in our “Top Pick” list has to meet the ollowing criteria: 1.) It must belong to a sector with neutral to positive outlook; 2.) It must

have double digit earnings growth or the current and the succeeding scal year; 3.) Its share price appreciation potential must be above 15% as o thedate it was included in the list; and 4.) It must have an upward intermediate term trend.

IMPORTANT DISCLAIMERSSecurities recommended, oered or sold by CitisecOnline are subject to investment risks, including the possible loss o the principal amount investedAlthough inormation has been obtained rom and is based upon sources we believe to be reliable, we do not guarantee its accuracy and it may be

incomplete or condensed. All opinions and estimates constitute the judgment o CitisecOnline’s Equity Research Department as o the date o the reportand are subject to change without notice. This report is or inormational purposes only and is not intended as an oer or solicitation or the purchase o

sale o a security. CitisecOnline and/or its employees not involved in the preparation o this report may have investments in securities or derivatives o

securities o companies mentioned in this report, and may trade them in ways dierent rom those discussed in this report.

HOLD SELLBUY

Over the next six to twelve

months, we expect the shareprice move within a range of

+/- 15%.

Over the next six to twelve

months, we expect the share

price to decline by morethan 15%.

Over the next six to twelve

months, we expect the shareprice to increase by 15% or

more.

2401-B Ea st Tower, Philippine Stock Exchange Center Exchange Road, Ortigas Center, Pasig City 1605 Philippines

Voice: +632 636 54 11 to 20 Fax: +632 635 4632 Interne t: http://ww w.citiseconl ine.com