2009 05 Electric Vehicles In Apac – Fad Or Reality Frost & Sullivan

16

Strategic Analysis of APAC Passenger Electric Vehicles Market: Fad or Reality? Vijayendra Rao, Industry Manager Automotive & Transportation 27 th May 2009 © 2009 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

-

Upload

alvin-chua -

Category

Documents

-

view

1.307 -

download

2

Transcript of 2009 05 Electric Vehicles In Apac – Fad Or Reality Frost & Sullivan

Strategic Analysis of APAC Passenger Electric Vehicles Market: Fad or Reality?

Vijayendra Rao, Industry Manager

Automotive & Transportation

27th May 2009

© 2009 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost &

Sullivan.

2

Focus Points

� Challenges and Solutions for EV Implementation

� Current Electric Vehicle Market Structure

� Product and Technology Roadmap

� Scenario Analysis for Electric Vehicles in APAC

� Market Breakdown By OEM and Type of Electric Vehicle

� Infrastructure and Business Model

� Opportunities in EV Market

� EV Customer Profile

� Conclusions and Recommendations

� Existing and Planned Powertrain Topics

� Q&A

3

Challenges and Likely Solutions for EV Implementation – Infrastructure, Battery Costs, Standardisation are key challenges for EV implementation

Lack of infrastructure to introduce electric vehicles

High costs of batteries and Electric Vehicles

Battery technology is not advanced enough to promote EVswith higher range and top speed

EV Technology is not proven and consumers are wary of buying Electric Vehicles

Price of oil at present is hovering around 50$/barrel that is likely to act as barrier for EV commercialisation

Global economic crisis is likely to put some of EV projects in the back burner

Mass commercialisation, Standardisation and Leasing model is likely to solve this issue

OEMs, Governments are running test fleets to showcase consumers that EV technology is proven for longer viability

EV Technology is a medium-long term strategy rather than short term. In the coming years, Oil prices are likely to increase to up to 100-150$/barrel

Better Place has taken initiatives to set up charging, swapping stations in Australia, Japan and likely to penetrate other APAC markets.

Most OEMs and suppliers have realised that EVs are likely to be a future viable option and are not shunning any projects due to the crisis.

OEMs and Battery suppliers are working extensively to improve the range and top speed of EVs. BYD claims their EV e6 has range of 250 miles.

Electric Vehicle Market: Challenges and Solutions (APAC), 2008

Source: Frost & Sullivan

4

Current Electric Vehicle Market Structure – Conglomeration of OEMs, Electric Utilities, Government, Battery Manufacturers required for increased electric vehicle penetration

Could work to improve charging time and safety

Infrastruct

ure

supplier

Key Responsibility:

Development of Charging Infrastructure

Key Responsibility:

Promotion of EV use

UtilitiesOthers: e.g. Project

Better PlaceOEMs

Battery Manufacturers

GovernmentCharging Station Manufacturers

Integrators to create partnerships with Utilities, OEMs

and Government

Subsidies for

EV purchase

and

investment in

R&D to

reduce

emissions

Lower fuel

dependency by

expanding the

use of

renewable

energy sourcesSupplies

infrastructure to

distribute their

energy

Cooperation to simultaneously promote EV use and electricity as a fuel

Development of

performing

batteries

Source: Frost & Sullivan

5

Product and Technology Roadmap – OEMs and Suppliers are working towards increased driving range and lower charging times going forward

Driving Distance/charge-up to 60 kms

Charge Time – 6 to 8 hrs

Slow charging - onboard

Infr

astr

uctu

reP

erf

orm

an

ce

So

urce:

Fro

st

& S

ulliv

an

Up to 130 kms

Battery Capacity – up to 16kWh

Motor Power- Up to 70 kW

2005 2010 2015

Fast charging – mostly off board

Battery Swapping

200 + kms

< 1 hour < 30 minutes

Up to 50 kWh 50 kWh +

70 kW – 140 kW

Neighbourhood Electric Vehicle

Pro

du

cts

City Electric Vehicle

Range extended Electric Vehicle

6

0

250

2008 2009 2010 2011 2012 2013 2014 2015

Conservative Frost & Sullivan Optimistic

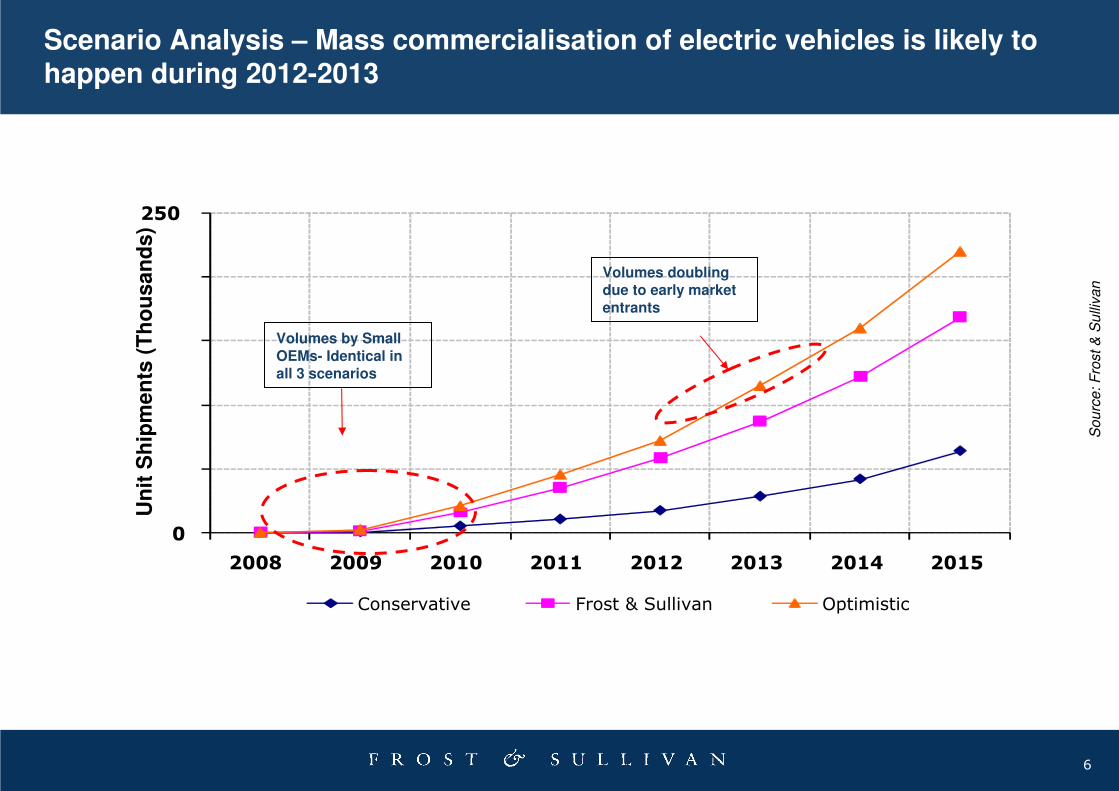

Scenario Analysis – Mass commercialisation of electric vehicles is likely to happen during 2012-2013

Volumes doubling due to early market entrants

Volumes by Small OEMs- Identical in all 3 scenarios

So

urc

e: F

rost &

Su

lliva

n

Un

it S

hip

me

nts

(T

ho

us

an

ds

)

7

Japan and China to be the biggest markets for Electric Vehicles in APAC

NEV Neighbourhood Electric Vehicle

CEV City Electric Vehicles

eREV/PHEV Extended Range/ Plug in Hybrid Electric VehiclesSource: Frost & Sullivan

20082015

650

~170K

0

10000

20000

30000

40000

50000

60000

70000

80000

Japan China India Korea Australia Others

NEVs CEVs PHEVs

75%

21%

4%

Others include Malaysia, Singapore

8

Infrastructure and Leasing Models in different APAC Regions – Conventional business model is likely to be successful in APAC except Australia

Country Infrastructure Business Model

With Better Place entering the Australian market and working closely with utility

companies and government, Australia is well positioned to provide infrastructure

to electric and plug-in hybrids in the coming years.

OEMs/ Distributors, Battery

Leasing, Battery+Car Leasing

OEMs and Government is working on pilot projects to provide infrastructure to

electric and plug-in hybrids. Better place is also setting up swapping stations for

long distance driving.

OEMs/Distributors, Battery

Swapping

There is no initiative either from government or any external agencies to set up

recharging stations in India. However, Hero Group (2-wheeler manufacturer) has

plans to set up recharging stations in India.

OEMs/ Distributors, Battery

Leasing

China has a great potential in terms of electric vehicles mainly due to availability

of raw materials, advanced motor technologies, competitive prices. However

there is no major initiative to set up recharging stations in China. There is a need

for government initiatives to drive the growth of EV Market in China.

OEMs/Distributors

South Korea is predominantly likely to adopt hybrid vehicles rather than electric

vehicles mainly due to the lack to infrastructure and no major initiative to set up

charging stations in South Korea.

OEMs/Distributors

9

Electric Vehicle market to create opportunities and attractiveness for industries like telematics, mobile phones, fleet businesses

MediumLow High

Low

Medium

HighUtilities

Effort required to develop EV business

Po

ten

tial to

ge

ne

rate

re

ve

nu

e

Telematics

Coach Builders

Marketing

Leasing Businesses

Financial

Mobile Phone

Fleet Businesses

Telematics

Swap Stations

Service/ Dealership

Recycling

Insurance

: Size of the bubble represents the impact on EV market

Potential for businesses to enter

EV market with relatively low

investment; strategise to partner

with OEMs

New business opportunities for

Utilities and Innovative financial-

leasing firms- To be resilient

before it makes profits

Innovative model but due to

demographics it requires good EV

penetration and customer

utilization- to have high impact if

successful

Source: Frost & Sullivan

Battery Rejuvenation

10

OWNERSHIP & MAIN USAGE• Driving the vehicle to work is his main priority

• Shopping during weekends.

FEEDBACK ON LEASING BATTERIES• Prefer to lease battery than source it directly

from manufacturer.

• Efforts to dispose and effect on environment key reasons

DEMOGRAPHICS• Male/female falling under the age group of 26-45

yrs

• Has a university degree

• Earning between $50K - $100K.

• Resides in Urban Area (Tokyo, Shanghai, Sydney)

• Flat /semi-detached house residence

SUGGESTIONS ON EV IMPROVEMENT• Reliability and after-sales service

• Latest battery to aid in greater distance travelled

• Improved and increased access to charging stations

• Improved interior designs for greater experience

• Navigation tools to improve access to P-O- I*NEEDS

• Reliability, price and fuel economy were the most important issues considered while purchasing EV

• Improved charging capability, provision of fast charger kits and maintenance free motors were features that consumers would consider to boost chances of EV purchase

Male/Female (26-45 yrs)

MOTIVATING FACTORS• Contribution to environment

• Reduced fuel cost

• Savings on tax and other Govt subsidies

• Free from congestion charging

• Compact and ease in parking

EV Customer Profile – Private

Source: Frost & Sullivan

11

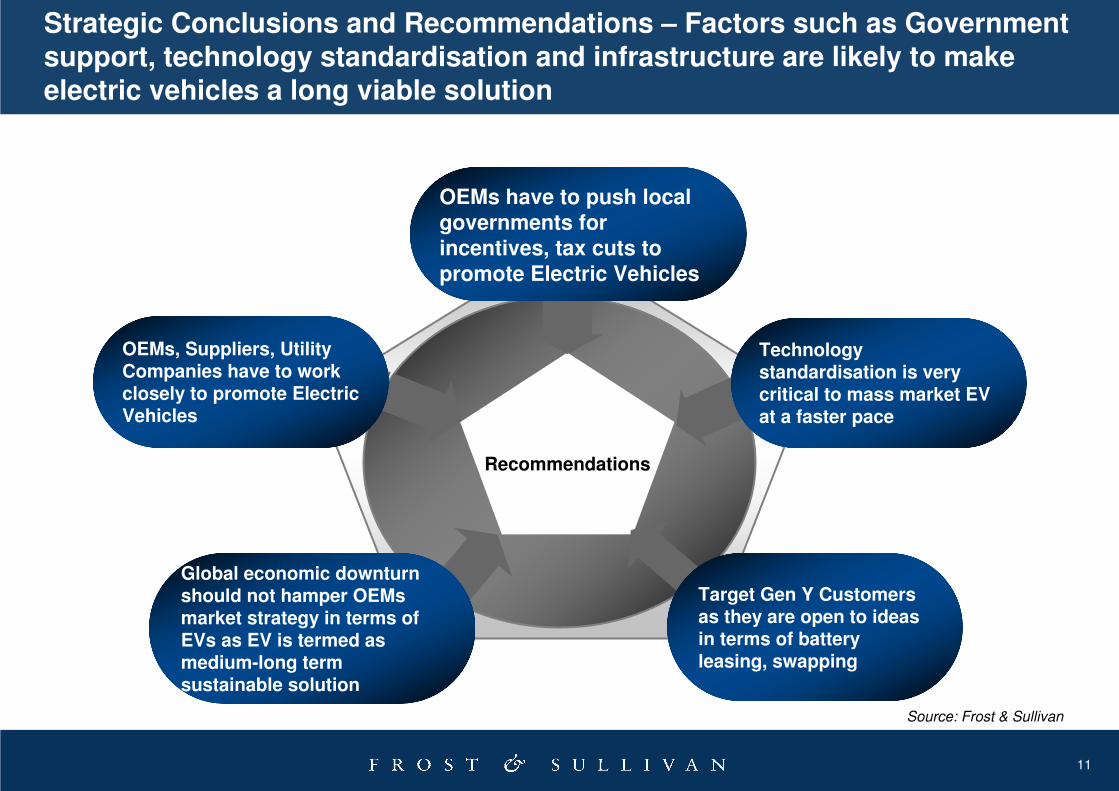

Strategic Conclusions and Recommendations – Factors such as Government support, technology standardisation and infrastructure are likely to make electric vehicles a long viable solution

Recommendations

Technology standardisation is very critical to mass market EV at a faster pace

Global economic downturn should not hamper OEMs market strategy in terms of EVs as EV is termed as medium-long term sustainable solution

OEMs, Suppliers, Utility Companies have to work closely to promote Electric Vehicles

OEMs have to push local governments for incentives, tax cuts to promote Electric Vehicles

Target Gen Y Customers as they are open to ideas in terms of battery leasing, swapping

Source: Frost & Sullivan

12

Research Titles Available to Date and Planned: Each Study is Average of 500 research hours

Already Published

1.Strategic Assessment of European Passenger Electric Vehicles Market - May 2008

2.Strategic Analysis of European Market for Electric Corner Modules - Oct 08

3.Strategic Analysis of Global Market for Fuel Cell Electric - Aug 2008

4.World Hybrid/Electric Vehicle Battery Markets -Jun 2008

5.Strategic Analysis of In Car Green Technologies - Jun 2008

6.Advances in Hybrid Electric Vehicles (Technical Insights)

7.Global Market Analysis of Plug in Hybrid Electric Vehicles Dec 2007

8.European Consumers’ Attitudes & Perceptions Towards Sustainability, Environment

and Alternate Power-trains - Includes section on Electric Vehicles

Research in Progress

1.Strategic Review of New EV Business Models in the Automotive Industry – Q1, 2009

2.Analysis of Electric Vehicles Infrastructure for Automotive Applications in Europe and Revenue Generation Opportunities for

Utilities – Q1, 2009

3.Strategic Analysis of the Fleet Market Opportunity for Electric Vehicles in Europe – Q2, 2009

4.Asia Pacific Market Analysis for Electric Vehicles for Fleets and Private Consumer – Q1, 2009

5.North American Market for Electric Vehicles for Fleets and Private Consumer – Q2, 2009

6.VOC Study on EVs – Customers Interest in Electric Vehicles and Acceptability to New Business Models

7.The Generation Y Consumer: Future Vehicle and Features Choice and Brand Marketing Positioning Study – Consumer

Study to have section on EVs – Q2, 2009

Note: new titles and schedule is subject to change and is not guaranteed

13

Next Steps

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keepabreast of innovative growth opportunities(www.frost.com/news)

� Register for the next Chairman’s Series on Growth on 16 June 2009: The CEO’s Marketing Team: Spearheading Profitable Growth

(visit http://www.frost.com/growthapac)

� Join us at a Growth, Innovation and Leadership 2009: A Frost & Sullivan Global Congress on Corporate Growth (visit www.frost-gil.coml)

� Request a proposal for a Growth Partnership Service to support you and your team to accelerate the growth of your company.

(email [email protected])

14

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

What would you like to see from Frost & Sullivan?

15

Contact Us

If you have questions or would like further information about anything we discussed, please send your query to the email provided below and we will get back to you shortly.

Alvin Chua

Account Manager

Automotive, Transportation & Logistics

DID: +65 6890 0997

Mob: +65 9199 4566

eMail: [email protected]

16

THANK YOU

We Accelerate Growth

Thank You