2008 Northeast Texas Entrepreneurship Assessment

64

Cass Bowie Lamar Miller Red River Hopkins Titus Hempstead Delta Little River Morris Franklin An Assessment of Rural Entrepreneurship in Northeast Texas and Southwest Arkansas JULY 2008

Transcript of 2008 Northeast Texas Entrepreneurship Assessment

Cass

Bowie

Lamar

Miller

Red River

HopkinsTitus

Hempstead

Delta

Little River

MorrisFranklin

An Assessment of Rural Entrepreneurship in Northeast Texas and Southwest Arkansas

JULY 2008

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 2

Acknowledgements The project team would like to thank the many individuals who took time to participate in the development of this document. We are particularly grateful to the Northeast Texas Workforce Development Board, the Local Activities Committee, and the many business owners and organizations who provided feedback and valuable insights regarding the community.

Staff: Kay O’Dell, Executive Director, Workforce Solutions David Vershaw, Project Manager, Workforce Solutions

Local Activities Committee: Ron Davis CEO, Titus Regional Medical Center Roger Feagley Executive Director, Sulphur Springs / Hopkins County EDC Bradley Hardin Community Relations, SWEPCO Peter Kampfer Executive Director, Paris EDC Steve Harris Director, Nash EDC Charles L. Smith Executive Director, Mount Pleasant Industrial Foundation Jerry Sparks Economic Development Director, Texarkana Chamber of Commerce Christy Wendell CEO, Harrison, Walker & Harper

About Us

TIP Strategies, Inc. (TIP) is a privately held Austin-based business and economic development consulting firm committed to providing quality solutions for both public- and private-sector clients.

Established in 1995, the firm’s areas of practice include economic development consulting, strategic planning, site selection, economic impact analysis, regional economic development, target industry analysis, cluster analysis, technology audit, transit-oriented development, workforce analysis, feasibility studies, market analysis, and redevelopment analysis and planning.

T.I.P STRATEGIES, INC. 7000 North MoPac, Suite 305

Austin, Texas, 78731 512.343.9113 (voice) 512.343.9190 (fax)

[email protected] www.tipstrategies.com

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 3

Table of Contents

Executive Summary ............................................................................................................ 4

Introduction ......................................................................................................................... 6

Asset Mapping .................................................................................................................... 7

Strategic Recommendations ............................................................................................. 23

Organizational Recommendations .................................................................................... 33

Implementation Guide....................................................................................................... 36

Appendices ....................................................................................................................... 39

Appendix A: Entrepreneurs Survey Responses............................................................... 40

Appendix B: Service Providers Survey Responses........................................................... 44

Appendix C: List of Bank Branches................................................................................... 45

Appendix D Potential Funding Sources ............................................................................ 55

Appendix E Data Analysis................................................................................................. 59

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 4

Executive Summary With growing interest in using entrepreneurship as a key economic development tool, Workforce Solutions Northeast Texas hired TIP Strategies, an Austin-based economic development consulting firm, to conduct an entrepreneurship assessment of the region and devise a set of strategies to strengthen the region’s entrepreneurship initiative.

As part of this assessment, TIP mapped the entrepreneurial assets of the region, identified any gaps in service, and made recommendations on how to better promote entrepreneurship in the region. The results of the asset mapping and gap analysis are summarized to the left.

To address these gaps, TIP recommended three primary goals and outlined strategies and actions to support these goals. A summary of these strategic recommendations is contained in the boxes below.

Asset Category Existing Gaps Capital Local banks

Informal angel network Small revolving loan funds

Formal angel network Regional revolving loan fund Financial literacy training

Business Services Legal

Accounting Marketing Human resources

Information technology Affordable healthcare Education about services

Education & Information Programs

SBDCs Higher education

institutions CORRE Paris incubator Sulphur Springs assistance

center Some youth e-ship training

Matching training offerings with entrepreneur needs

More regional access to training Entrepreneur boot camp Peer networking Formal mentor network Information clearinghouse Coordinated youth e-ship

initiative

GOAL ONE: DEVELOP AN EDS Design an online entrepreneurs portal Create a strong network of partners and

service providers Build capacity in regional communities to

better support entrepreneurs

GOAL TWO: AUGMENT SUPPORT SERVICES Develop a three-tiered support system for

entrepreneurs in the region. Strengthen and target support services for

each tier.

GOAL THREE: PROMOTE A MORE ENTREPRENEURIAL CLIMATE AND CULTURE Design a PR campaign to build awareness

of regional entrepreneurs’. Organize an annual business expo. Lower barriers to entry for new

entrepreneurs.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 5

To set up the organizational structure to implement the goals and strategies, TIP recommended that the region create a roundtable of stakeholders. This roundtable should meet regularly to track implementation progress. In addition, experienced staff dedicated to entrepreneurial issues should be hired. This staff person should be responsible for everything from fundraising to program design and should provide administrative support to the roundtable, as needed.

To ensure effectiveness, accountability measures should be identified and integrated into the design of the programs and initiatives that grow out of this report. These accountability measures will provide a feedback loop to modify the programs and initiatives, if needed, and allow stakeholders to track progress and results.

Finally, the region will need to raise funds necessary to support the programs and initiatives. The source of funds should be well-diversified in order to ensure the longevity of the programs and initiatives.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 6

Introduction The Northeast Texas region and the neighboring counties in Southwest Arkansas are facing significant job losses associated with the realignment of Red River Army Depot and Lone Star Army Ammunition Plant. In addition, the region has experienced recent layoffs in the manufacturing and retail sectors. In response, the region is seeking to strengthen its entrepreneurship initiative in an effort to bolster economic growth and job creation.

Entrepreneurship is becoming more commonly accepted as an essential tool in the economic development toolbox. Especially in rural areas, communities are recognizing that a “grow your own” strategy has a higher probability of success than recruiting a major employer to the area. In addition, entrepreneurship strategies that foster new business creations are often more cost effective than incentives paid to recruit businesses to a community. A recent study of the Appalachian Regional Commission’s Entrepreneurship Initiative found that the public cost of the initiative per job created ranged from $579 to $3,994.1

Past studies in the region have found an entrepreneurship initiative to have much promise. The 2005 report North East Texas: Building on Strengths and Working Together on Challenges found that entrepreneurship plays a significant role in the regional economy in terms of employment and income. Furthermore, the 2006 Texarkana Regional Community Plan revealed that 30 percent to 40 percent of workers to be affected by the base realignments were interested in starting their own businesses.

With this in mind, Workforce Solutions Northeast Texas hired TIP Strategies, an Austin-based economic development consulting firm, to conduct an entrepreneurship assessment of the region and devise a set of strategies to strengthen the region’s entrepreneurship initiative.

1 Creating an Entrepreneurial Appalachian Region by RUPRI’s Center for Entrepreneurship, April 2008.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 7

Asset Mapping METHODOLOGY

To assess the entrepreneurial assets in the region, the consulting team focused on collecting both qualitative and quantitative data through site visits, interviews, and primary and secondary data sources. These research activities included:

Data collection, analysis, and assessment

Stakeholder interviews (13)

Entrepreneurs focus groups (21 attendees)

Survey Entrepreneurs (106 respondents / 72 completed) Service providers (3 respondents)

With the information obtained through this discovery process, TIP created a map of the region’s entrepreneurial assets and identified any significant gaps in the spectrum of small business and entrepreneurship services. We classified assets into three categories - capital, business services, and education and information programs as shown in the asset checklist. In addition to these asset categories, we assessed the entrepreneurial climate of the region.

Once the service gaps were identified, TIP researched best practices for program design and delivery to address these gaps. We, then, developed recommendations for promoting entrepreneurship in the region through regional collaboration and enhanced programs and service delivery.

Build awareness of entrepreneurship

Board of DirectorsInvolvement

Basic Training

One-on-OneCounseling

BusinessNetworking

MentorPrograms

Adv. Training

Angel NetworkFacilitation

Where are the gaps?

Build awareness of entrepreneurship

Board of DirectorsInvolvement

Basic Training

One-on-OneCounseling

BusinessNetworking

MentorPrograms

Adv. Training

Angel NetworkFacilitation

Where are the gaps?

Entrepreneur ia l Asset Checkl is t

SOURCE: RUPRI Center for Rural Entrepreneurship.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 8

CAPITAL

Entrepreneurs need access to capital that is appropriate for the stage of growth that their business is in. Start-ups have different financing needs than established businesses. These financing needs are met through a variety of mechanisms from friends and family investment pools to debt issuances in international financial markets. The various financing sources by state of growth are presented on the chart to the left.

In the Entrepreneurs Survey, access to capital was perceived to be the primary obstacle to starting a business in the region.

Currently, traditional bank financing and small business loans are the primary source of financing available. However, there is no formal access to a venture capital network in the region. As a result, entrepreneurs in the region do not have adequate access to capital to fund the CONCEPT and INCEPTION stages of growth. In addition, companies with unique or unusual business models confront challenges in obtaining financing.

EQUITY CAPITAL

Entrepreneurial growth companies and other growth-oriented enterprises typically depend on equity capital to fund their needs through the concept and inception stages of growth. Equity capital is primarily available through “angel” investors and venture capital funds.

Focus group participants noted that many businesses in the region are generally hesitant to give up a portion of the ownership of their business in pursuit of equity investments. These comments highlight an important fact: equity investments are not for every business. For family-owned businesses and lifestyle businesses, debt financing may be adequate to meet their needs. However, for entrepreneurial growth companies and high-growth companies, selling equity in the company to fund start-up operations is often a necessary part of establishing a solid platform for growth. To create a business climate

Sources of F inancing by Stage of Growth

SOURCE: Adapted from PriceWaterhouseCoopers. (http://www.pwc.com/nz/eng/ins-sol/publ/pcs/CleverCompaniesDiagnosticChart.pdf)

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 9

that encourages the development of entrepreneurial growth and high-growth companies, the region should work to make equity capital accessible to promising entrepreneurs.

Angel Investors

The term “angel” refers to high-net worth individuals, or accredited investors, who typically invest in and support start-up companies in the very early stages (“seed stages”) of growth. In Northeast Texas and Southwest Arkansas, an informal angel investor network exists that provides early-stage funding for a select few promising entrepreneurs. Formalizing this network could enhance this type of capital’s accessibility and grow the base of “angels” as more investors become aware of investment opportunities in the regional economy.

Among their many benefits, formal angel investor networks provide opportunities for investors to pool their resources to support a wider range of financing needs in their region. They also provide entrepreneurs the opportunity to seek equity investments rather than rely on debt financing.

Venture Capital

Venture capital is also a type of equity capital. Venture capital investments are made by professional investors to promising high-growth companies who are beyond the seed stage of growth, but still considered to be start-ups.

While no venture capital funds are headquartered in the region, an entrepreneurial company that is prepared to actively solicit venture funds should be able to access funds outside of the immediate region in nearby metropolitan areas. Venture funds in the Dallas area and in Little Rock may consider making investments in regional companies. In Dallas, the North Texas Regional Center for Innovation and Commercialization functions as an outreach arm for the Texas Emerging Technologies Fund, a $200 million fund established to encourage the development of technology companies across the state. Dallas is also home to a number of venture capital firms, including an office of Sevin Rosen. In Little Rock, Diamond State Ventures, which is part of the Arkansas Capital Corporation Group (ACCG) provides capital for entrepreneurs across the state.

Three Things to Know about Capi ta l

1. Venture capitalists rarely invest outside of a two- to four-hour drive of the investor’s office. These investors need access to the entrepreneurs and management of the companies they are working with. Good investors are actively involved in helping the company succeed by adding management talent, making introductions to potential partners, and continuing to find other potential investors to lower the risk of failure.

2. Venture capital does not just happen in urban areas. There are groups that only invest in rural areas such as Meritus Ventures out of Kentucky and Tennessee and Sustainable Job Fund Ventures based in Durham, North Carolina, and New York.

3. Banks typically do not lend money to entrepreneurs in early stages especially companies working with intellectual property. An overwhelming majority of people think the only source of capital for entrepreneurs is a bank. In fact, most banks do not lend money to entrepreneurs who lack a certain net worth or entrepreneurs who usually lack any collateral that can be used as a guarantee of the loan.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 10

DEBT CAPITAL

In the region, debt capital is largely provided in the form of business loans. These loans are principally provided by banks, SBA loan programs, revolving loan funds, and non-traditional lenders.

Banks

Northeast Texas and Southwest Arkansas are home to many banks, including most large national commercial banks and many local and regional banks. (See Appendix C – List of Bank Branches.) From 2001 to 2007, the number of bank branches in the region grew from 123 to 143. In spite of this growth, the value and number of small business loans has declined since 2006. The value of loans underwritten dropped from $52 million in 2001 to $28 million in 2006, while the number of loans declined from 1,558 in 2001 to 726 in 2006. This likely indicates a tightening of credit in the region. In 2007 and 2008, this trend has likely continued due to national market conditions.

This tightening of credit will make it harder for companies in the CONCEPT and INCEPTION phases to access credit. Business loans for these types of start-ups are too risky for most banks to consider, in most cases. Banks that will consider business loans to start-up companies usually have requirements for collateral and equity contributions that are prohibitively high to new businesses, particularly service-oriented businesses. For these reasons, bank financing is generally considered to be more suited for companies in the later stages of growth.

Some focus group participants noted that obtaining bank financing can be challenging for businesses that are unique or unusual. These business owners commented bankers turned down their requests or provided less capital than requested based on “not understanding the business.” As a result, some of the most innovative companies in the region may not be able to secure financing to grow their businesses.

The region is, however, very fortunate to have a large number of independent local and regional banks. Generally, a strong presence of independent banks positively contributes to the entrepreneurial climate of a community because the decentralized, less automated underwriting process of local banks (in comparison to that of national banks) allows more flexible lending practices that can be tailored to the needs of local entrepreneurs. Focus

$0

$50,000

$100,000

$150,000

$200,000

$250,000

2001 2002 2003 2004 2005 20064,000

4,500

5,000

5,500

6,000

Value of Small BusinessLoans ('000s)# of Small Business Loans

NORTHEAST TEXAS / SOUTHWEST ARKANSAS REGION Small Business Loans, 2001-2006

SOURCE: FFIEC.

123

124

129

134

139

141

143

110 115 120 125 130 135 140 145

2001

2002

2003

2004

2005

2006

2007

NORTHEAST TEXAS / SOUTHWEST ARKANSAS REGION Number of Bank Branches, 2001-2007

SOURCE: FDIC.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 11

group participants cited over and over again the important role that the local and regional banks play in securing bank financing for their businesses. Many indicated that they had even been able to secure funding for their businesses when it was in the start-up stage. However, they also noted that some of these community banks rely on personal relationships with the perspective borrower to make underwriting decisions, which may exclude borrowers from surrounding communities or newcomers to the area. The exceptions to this kind of relationship banking are the local banks in Mount Pleasant, which participants explained are competing fiercely for small business loans and base underwriting decisions less on personal relationships.

SBA Loans and Non-Traditional Lenders

In addition to conventional bank financing, the SBA’s loan programs provide another source of debt capital for business owners in the region. Under these programs, the SBA acts as the primary guarantor of loans made by private institutions to small businesses. In this way, the SBA assumes much of the risk associated with small business lending in order to increase access to capital available to small businesses across the United States. The table to the left provides an overview of the SBA loan programs.

Both the Paris SBDC and the Southern Arkansas University SBDC provide loan packaging services to help their clients obtain SBA loans. They normally work with Borrego Springs Bank and the affiliates of ACCG to obtain SBA loans. The Ark-Tex Regional Development Company, which is part of the Ark-Tex Council of Governments, also underwrites SBA loans in the region.

Southern Financial Partners and ACCION Texas offer non-traditional small business loans in the region. Southern Financial Partners offers loans to small business owners within a 50-mile radius of their office in Arkadelphia, which includes parts of Hempstead, Little River, and Miller counties in Arkansas. ACCION Texas offers microloans from $500 to $50,000 to small businesses across the state of Texas. These nonprofit lending institutions provide capital to small businesses that do not have access to credit through conventional commercial banks or the SBA.

PROGRAM PERMITTED USES OF LOAN PROCEEDS LOCAL RESOURCES

7(a) Loan Guaranty, Max. $2,000,000

Working capital, machinery and equipment, furniture and fixtures, land and building (including purchase, renovation and new construction), leasehold improvements, and debt refinancing (under special conditions).

Borrego Springs Bank Arkansas Capital

Corporation (ACCG)

504 Loan Program, Max. $1,500,000

Purchase of real estate, machinery, and equipment

Ark-Tex Regional Development Corp.

Six Bridges Capital Corporation (ACCG)

ACCION Texas Greater East Texas

Certified Development Corp.

Microloan Program, Max. $35,000

Working capital or the purchase of inventory, supplies, furniture, fixtures, machinery and/or equipment

ACCION Texas

SOURCE: The Small Business Administration.

Summary of SBA Programs

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 12

Revolving Loan Funds

Four organizations across the region have established revolving loan funds in an effort to provide greater access to credit for small businesses. The funds were created by obtaining a grant from government agencies including the EDA, USDA, HUD, the U.S. Department of Agriculture, and private foundations. Once the funds are established, communities are then able to make loans to small businesses that do not otherwise have access to credit based on criteria established by the organizations themselves. The table to the left provides an overview of the revolving loan funds in the region.

While it is encouraging that these funds have been established across the region and that these resources are available, they will not be able to fill the existing credit gap. The size of the funds and the terms of the loans limit the ability of these funds to meet the needs of area business owners.

LITERACY

When asked about issues of access to credit, most focus participants were familiar only with conventional bank lending. In addition, the service providers interviewed commented that many business owners have poor credit, which prohibits them from being able to access credit from banks. Both these situations highlight gaps in financial literacy among area entrepreneurs – one in understanding different types of financing, another in understanding both personal and business financial management.

Currently, most financial literacy education for business owners occurs through the SBDCs and informal counseling. The SBDCs sponsor workshops to educate their clients most often on obtaining a bank loan and occasionally on financial management topics. Business owners in need of more intensive help with personal and business financial issues and credit repair often seek the help of informal mentors – sometimes bankers, SBDC counselors, bookkeepers, and accountants. However, education programs on non-bank financing and courses on very basic personal and financial management for business owners are not currently offered regularly across the region.

ORGANIZATION (Date Established) FUND AMOUNT LOANS MADE

Nash EDC (2002)

$300,000 15

Paris EDC (2000)

$200,000 3

Sulphur Springs EDC (2008)

$118,000 1 in process

North East Texas Economic Development District / Ark-Tex COG (1987)

$1,400,000 24

Chapman RLF (managed by Ark-Tex COG) (1995)

$1,400,000 22

SOURCE: TIP Research.

Summary of Loan Funds

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 13

BUSINESS SERVICES

Business services providers play a vital role in supporting local small businesses and entrepreneurs. Such services include accounting, bookkeeping, tax and legal advice, insurance, human resources, marketing, information technology, financing, succession planning, and market identification and development.

According to focus group participants, necessary business services are available locally, in nearby metropolitan areas, or online. In other words, area entrepreneurs have access to the business services that they need. The primary services not available locally are information technology related – from specialized equipment to network support services. However, many business owners have addressed this issue by traveling to the Dallas area to find needed equipment and by contracting with companies to provide remote assistance.

Another area of concern for focus group participants is health insurance. According to a recent survey by the National Federation of Independent Business, the cost of health insurance is the number one issue facing small businesses. In fact, the cost of health insurance can be a significant barrier to aspiring entrepreneurs considering starting their own business. In Texas, various chambers have begun to form Health Group Cooperatives, which allow them to offer employer health plans to their members. FirstCare Health Plans is one healthcare service provider that works with the Lubbock Chamber of Commerce, a partnership between the Permian Basin Petroleum Association and Odessa Chamber of Commerce, and a collaboration of 16 chambers in the Texas Midwest Community Network (Abilene / Waco area) to offer this kind of employer health plan.

The greatest gap in this asset category is that many business owners are not aware of the kinds of services available, why they may need these services, and where to find the services. For example, business succession and transfer planning is vital to the longevity of successful entrepreneurial ventures but not widely used by business owners. To address this lack of awareness, many communities plan annual small business expos, fairs, or conferences to expose small business owners to the types of services available and raise awareness of the need for these services. In addition, a directory of local services and informative newsletters can also raise awareness. Raising awareness

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 14

among business owners about the services available to them will increase the services’ accessibility and likely increase their usage rate.

EDUCATION AND INFORMATION PROGRAMS

Access to capital and business services are essential to creating a strong entrepreneurial climate in a region that provides the conditions in which entrepreneurial ventures can flourish. Creating a strong network of education and information programs is the next step in developing an effective entrepreneur support system. These programs are vital in building entrepreneurs skills and, thereby, increasing their chances of survival and success.

TRAINING & TECHNICAL ASSISTANCE

Various non-profit and public institutions offer area entrepreneurs training courses and more personalized technical assistance. The Small Business Development Centers are the primary service providers in the region. Most of their courses and services are offered at little or no cost to the entrepreneur. Regional higher education institutions also play a vital role in providing more advanced business courses to enhance entrepreneurs understanding of accounting, business management, marketing, and finance. In addition to these primary resources, a number of communities in the region are in the planning stages of new initiatives to serve business owners in their areas.

Small Business Development Centers

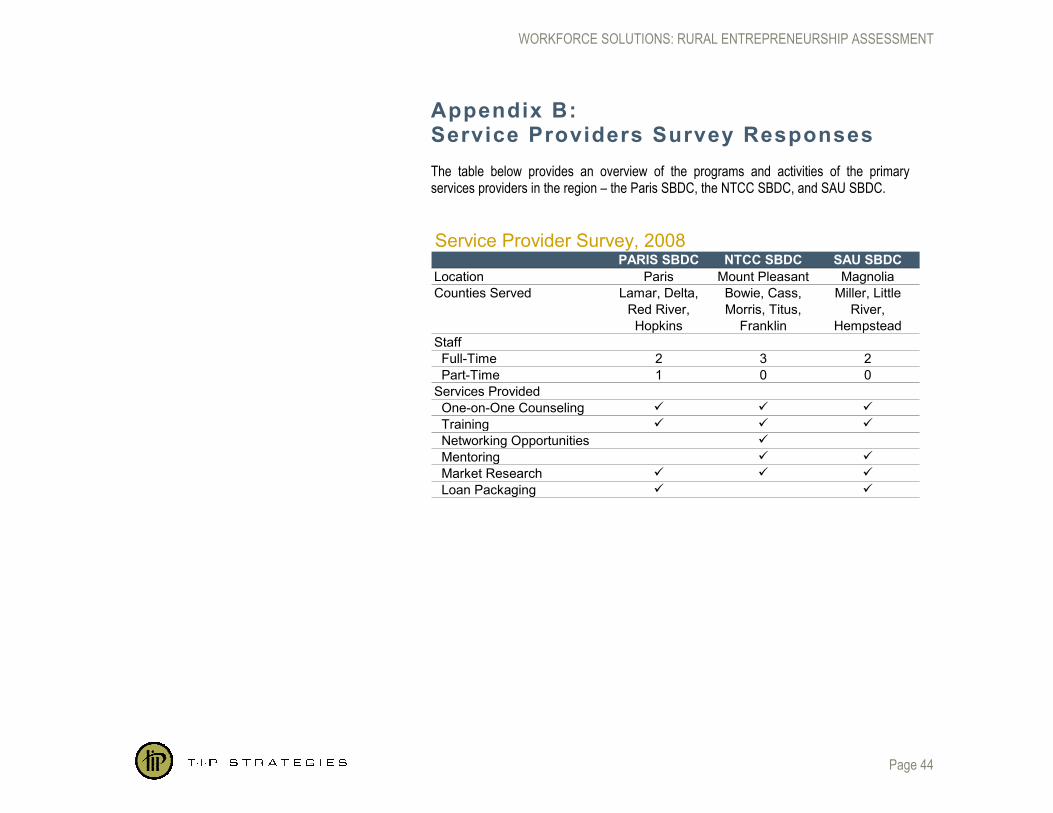

The Northeast Texas / Southwest Arkansas region is fortunate to have three organizations focused on providing assisting small businesses. These are the SBDCs. (See Appendix B – Service Providers Survey Responses.)

The Paris SBDC covers Lamar, Hopkins, Delta, and Red River counties. The center is headquartered at Paris Junior College. Training courses and counseling sessions are regularly offered

SBDC Coverage Areas

Cass

Bowie

Lamar

Miller

Red River

HopkinsTitus

Hempstead

Delta

Little River

MorrisFranklin

SOURCE: Small Business Administration.

Northeast Texas

Paris

Southern Arkansas University

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 15

in Paris, Sulphur Springs, Cooper, and Clarksville. They have two full-time and one part-time staff.

The Northeast Texas SBDC covers Franklin, Titus, Morris, Cass, and Bowie counties. The center is headquartered at Northeast Texas Community College. Training courses and counseling sessions are regularly offered in Mount Pleasant, Texarkana, Atlanta, and Naples. They have three full-time staff.

The Southern Arkansas University SBDC covers Little River, Hempstead, and Miller counties. It is headquartered outside of the region at Southern Arkansas University in Magnolia, Arkansas. Training courses and counseling sessions are regularly offered in Texarkana, Hope, and Ashdown. They have two full-time staff.

The SBDCs provides one-on-one counseling and training for potential entrepreneurs and business owners. Together the SBDCs provided counseling to 351 clients in 2007 and taught 110 training courses to 711 participants. In addition, they helped package 33 loans, securing almost $5 million in capital for small businesses. Local clients can also access the services of the North Texas Small Business Development Center Network that has specialty centers focused on government contracting, international trade, risk management, enterprise excellence, and technology.

Higher Education Institutions

The region’s universities and community colleges also provide education to entrepreneurs and aspiring entrepreneurs through their business and accounting programs. An overview of the degree programs offered in the region is provided on the following page. In addition to the topic areas covered by these degree programs, entrepreneurs may enroll in business classes for credit or as part of the institutions’ continuing education programs. These classes cover topics ranging from management and accounting to Quickbooks.

Of note among the higher education institutions is the new business school at Texas A&M – Texarkana. One of the near-term goals of the business school is to establish an entrepreneurship center and offer an entrepreneurship concentration. The center is currently in the nascent planning stage, and the school hopes to have this center up and running within the next 10 years.

CASE STUDY: the Hankamer School o f Business , Baylor Univers i ty

The Hankamer School of Business at Baylor University has received national recognition for its efforts to promote entrepreneurship. In addition to offering a course of study to prepare its undergraduate and graduate students for entrepreneurial careers, it houses the John F. Baugh Center for Entrepreneurship. This center offers two primary programs: the Innovation Evaluation Program and the Institute for Family Business. The Innovation Evaluation Program evaluates new products or ideas to determine the likelihood for commercial success. The Institute for Family Business provides educational opportunities for family business owners to strengthen their businesses across generations.

The entrepreneurship program at the Hankamer School was ranked 14th in the nation by U.S. News & World Report.

For more information: http://www.baylor.edu/business/entrepreneur/

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 16

Higher Educat ion Degree Programs

Texas A&M University - Commerce*

Texas A&M University - Texarkana

Texarkana College

Paris Junior College

Northeast Texas Community

College

Southern Arkansas

University - Magnolia*

University of Arkansas

Community College at Hope

Cossatot Technical

College BranchCITY Commerce Texarkana Texarkana Paris Mount Pleasant Magnolia Hope AshdownCOUNTY Hunt Bowie Bowie Lamar Titus Columbia Hempstead Little RiverGENERAL BUSINESS BBA BBA BBA

BUSINESS ADMINISTRATION BS, MBA BS, MS, MBA

MANAGEMENT BBA, MS BBA BBA

ACCOUNTING BBA BBA BBA TC

PROFESSIONAL ACCOUNTANCY BPA

ELECTRONIC COMMERCE MS

FINANCE BBA, MSF BBA BBA AAS

HUMAN RESOURCE MANAGEMENT BBA BBA

INDUSTRIAL MANAGEMENT BBA

INTERNATIONAL BUSINESS BBA CP AAS

MANAGEMENT INFORMATION SYSTEMS BBA BBA

MARKETING BBA, MS BBA AAS, CERT 1

BBA

PRODUCTION/OPERATIONS MANAGEMENT

BBA

REAL ESTATE CERT 1

BUSINESS ADMINISTRATION, MANAGEMENT, AND OPERATIONS

AAS, CERT 1

AAS, CERT 1

AAS AAS

BUSINESS OPERATIONS SUPPORT AND ASSISTANT SERVICES

AAS, CERT 1

AAS, CERT 1

AAS, CERT 1, CERT 3

* Located outside of study area, but provide access to higher education to residents in the study area.SOURCE: Texas Higher Education Coordinating Board, Arkansas Department of Higher Education.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 17

Other Initiatives

In addition to SBDCs and higher education institutions, three communities across the region are in the process of planning and developing other types of programs to provide training and technical assistance to entrepreneurs. A summary of these initiatives is provided below:

Coalition of Red River Entrepreneurs (CORRE), Red River County. A group of stakeholders from the Clarksville area has initiated the process to contract the Sirolli Institute to provide training on the Enterprise Facilitation Model. This model provides a framework for delivering “free, confidential, and professional management advice” to aspiring entrepreneurs and existing business owners in a region.

Business Incubator, Paris / Lamar County. The Paris EDC is in the process of designing a business incubator to service entrepreneurs in the immediate region. In addition to affordable office space, this incubator will provide technical assistance and other support services to participating business owners.

Entrepreneur Assistance Center, Sulphur Springs / Hopkins County. The Sulphur Springs EDC is planning a comprehensive technical assistance program for entrepreneurs. Aside from technical assistance, the program will make meeting and office space available for clients to use on an as-needed basis.

Training Offerings

With these existing and planned programs, the region should have the basic infrastructure to deliver a comprehensive training and technical assistance program. However, the specific offerings should be tailored to the needs of the different types of entrepreneurs. According to the Entrepreneurs Survey respondents, the most helpful training courses would be marketing on a shoestring, identifying new markets, and tax and legal issues. The majority of the training courses currently offered by the SBDCs are on starting a business. The North Texas SBDC offers a series of courses on business planning, and the Paris SBDC offers a variety of courses, including human resource management,

Tra in ing Needs

9%

18%

21%

24%

25%

27%

28%

32%

32%

38%

Intellectual property

Raising capital

Cash flow management

Retaining employees

Quickbooks

Hiring employees

Managing employees

Tax & legal issues

Identifying new markets

Marketing on a shoestring

Q: Which training courses would you find most helpful?

SOURCE: TIP Strategies research.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 18

intellectual property, government contracting, customer service, and getting a bank loan. The top three areas of interest for survey respondents, however, are not currently offered.

Furthermore, the course offerings are not uniform across the region because of the differing service areas for each of the SBDCs. For example, some of the classes that may be offered in Lamar County are not offered in Bowie and vice versa. As a result, accessibility of a wide range of training courses across the region is inequitable.

While current training course offerings provide valuable information for existing and aspiring business owners, comprehensive boot-camps for potential entrepreneurs are effective means of preparing start-up businesses. A number of excellent curricula exist that educate potential entrepreneurs and start-ups on the basics of entrepreneurship. Two popular curricula are FastTrac and NxLeveL. Both the SAU SBDC in Magnolia and the North Texas SBDC in Dallas are certified FastTrac Administrators. The Arkansas SBDC is a certified trainer of NxLevel. However, none of these courses are regularly offered in the region.

PEER NETWORKING & MENTORING

On the Entrepreneurs Survey, 41 percent of respondents ranked peer networking as the service that would be most helpful to their business. Peer networking provides entrepreneurs with the opportunity to exchange ideas, discuss issues they are confronting, share experiences, and generally support one another in a secure setting. While many chambers of commerce offer general networking opportunities, these networking events are geared toward cultivating business relationships rather than solving business issues. At this time, no peer networking events are offered in the region.

Successful entrepreneurs often cite their mentors as “the secret to their success.” Communities across the nation have found that facilitating a mentor network for entrepreneurs can be an effective and relatively low-cost way to enhance the entrepreneurial climate. There is not currently a formal mentor network that matches up entrepreneurs with successful mentors although the SBDCs provide some informal mentoring. Mentoring was not, however, one of the top needs that entrepreneurs indicated on the survey.

Tra in ing Curr icu la

One popular entrepreneurial training program is FastTrac. Founded by the Kauffman Foundation of Kansas City, Missouri, FastTrac is a boot camp for entrepreneurs. According to the foundation’s materials, 70 percent of companies that go through the program succeed beyond three years – the oft-touted threshold by which the majority of small businesses fail. The program can be brought to any town provided there is an organization willing to become certified to teach the program. (http://www.fasttrac.org/)

Another popular program is NxLeveL, a curriculum developed by the University of Colorado at Denver. NxLeveL includes seven different curriculum tailored for different types of entrepreneurs. Since 1996, over 80,000 students have participated in NxLeveL trainings. A third-party evaluation of the program shows that over 90 percent of business start-ups that participated in the program were still in business after three years. The program is taught by certified trainers in over 600 communities in 48 states. (http://www.nxlevel.org/)

Serv ice Needs

8%

9%

11%

11%

14%

35%

35%

41%

One-on-one counseling

Mentoring

Loan packaging

Help finding investors

Business plan preparation

Training courses

Market research

Peer networking opportunities

Q: What services would you find most helpful for your business?

SOURCE: TIP Strategies research.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 19

One of the largest mentoring networks for small business owners and entrepreneurs is the Service Corp of Retired Executives (SCORE), which is a resource partner of the SBA. SCORE has local chapters across the U.S. with a volunteer corps of retired executives that offer one-on-one counseling and mentoring. The region currently does not have a chapter of SCORE. One focus group participant commented that he found SCORE to be extremely helpful when he lived in an area with a chapter and that he has met with volunteers from the Dallas Chapter of SCORE to seek assistance. Strong mentoring programs, however, need not be composed of retirees. The figure to the left provides an overview of other successful mentoring programs.

ACCESS TO INFORMATION

In many communities, service providers find reaching business owners and entrepreneurs very difficult. Likewise, entrepreneurs and business owners find it difficult to locate needed services. Of the 72 respondents that completed the Entrepreneurs Survey, fewer than 20 had used any of the SBDCs’ services. During focus groups as well, this information gap was apparent as some participants commented that they could not find certain business services and others shared which business service providers they used.

Also, on the Entrepreneurs Survey, 35 percent of respondents find market research to be a service that would be most helpful to their businesses. However, access to the type of competitive information needed for market research is often expensive and not affordable to small business owners. There is not currently a competitive information resource geared specifically towards entrepreneurs.

Creating a central clearinghouse of information for entrepreneurs in the region can bridge these information gaps. A clearinghouse should provide information on sources of capital, business services, and training and technical assistance providers. It should also host a calendar of events and provide competitive information resources for entrepreneurs. In this way, service providers can more effectively and efficiently reach their potential clients and entrepreneurs can stay abreast of what resources are available to them.

YOUTH ENTREPRENEURSHIP TRAINING

Youth entrepreneurship programs are an important part of a long-term strategy for promoting entrepreneurship in general and building a more entrepreneur-friendly climate

EXAMPLE: Mentor ing

North Carolina’s Blue Ridge Entrepreneurial Council (BREC) connects local entrepreneurs with mentors during a monthly breakfast meeting. Called the Mentor BRECfast, the meetings feature a single mentor addressing topics such as marketing, sales, cash flow, and other topics of interest to aspiring entrepreneurs. Mentor BRECfast meetings frequently lead to direct mentoring relationships between the presenter and one or more attendees. (http://www.brecnc.com/)

A growing number of for-profit services are available to help connect entrepreneurs with potential mentors. One example is Minneapolis-based Menttium, which provides mentoring services to “high-performing female talent.” Programs include a year-long program designed to match protégés across the country with mentors based on a rigorous screening process.

EXAMPLE: Peer - to -Peer Networking

The Entrepreneurs’ Organization (www.eonetwork.org) is world-wide network of entrepreneurs whose mission is to “engage leading entrepreneurs to learn and grow.” The organization offers a wide range of services including executive education, events, an online exchange, and mentorship. One of its most successful programs is the Forum. Local chapter forum organizers assign members to peer forums of 8 to 12 business owners for peer-to-peer learning and support. Members are assigned to forums to ensure a good mix of business owners and avoid the inclusion of competitors in the forum. Through monthly forum meetings, participants explore business issues in a confidential, supportive atmosphere and share lessons learned.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 20

in a region. Entrepreneurship for school-aged youth can be integrated into existing curricula, be a stand-alone class, or be part of an after-school program.

The region has two primary avenues for educating youth about entrepreneurship – Junior Achievement and high school career and technology programs. Junior Achievement is a nonprofit organization with chapters across the United States that are “dedicated to educating students about workforce readiness, entrepreneurship and financial literacy through experiential, hands-on program.” In the region, the Texarkana area and Titus County both have active chapters of Junior Achievement. The Texarkana area chapter serves Texarkana, Pleasant Grove, and Liberty-Eylau, Texas, and Texarkana, Arkansas, school districts. The Titus County chapter serves Mount Pleasant, Chapel Hill, and Harts Bluff school districts. Both chapters work in both elementary and middle schools.

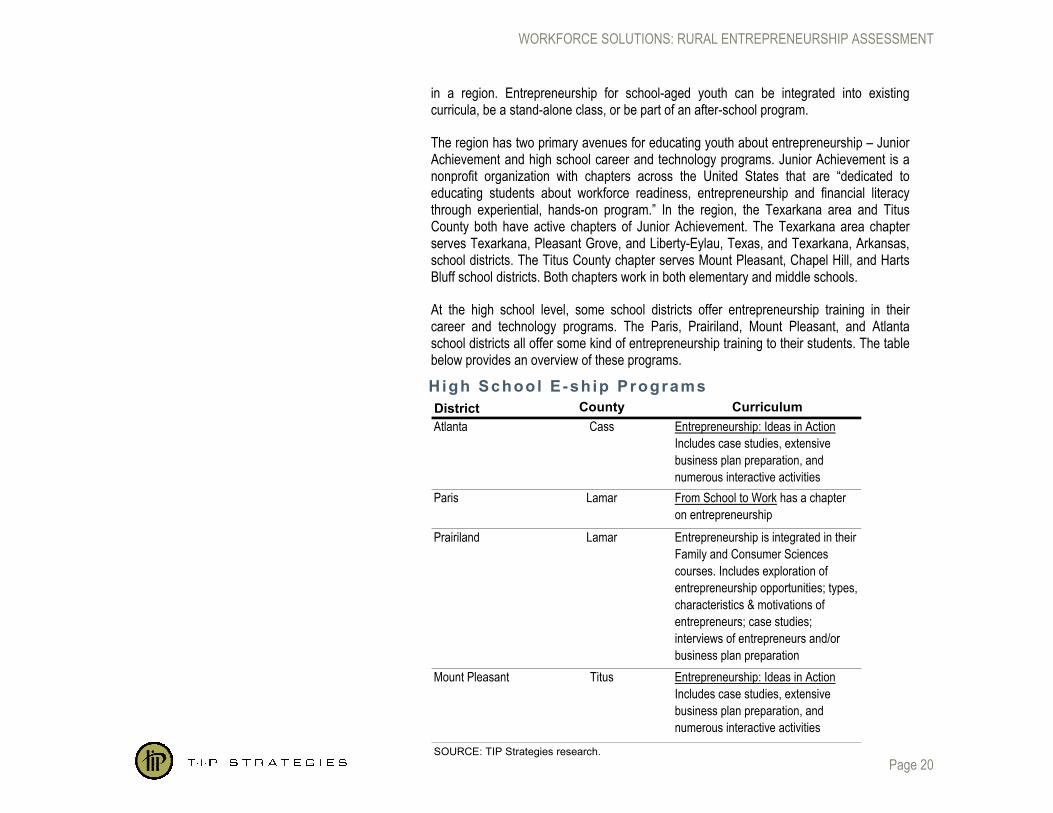

At the high school level, some school districts offer entrepreneurship training in their career and technology programs. The Paris, Prairiland, Mount Pleasant, and Atlanta school districts all offer some kind of entrepreneurship training to their students. The table below provides an overview of these programs.

District County CurriculumAtlanta Cass Entrepreneurship: Ideas in Action

Includes case studies, extensive business plan preparation, and numerous interactive activities

Paris Lamar From School to Work has a chapter on entrepreneurship

Prairiland Lamar Entrepreneurship is integrated in their Family and Consumer Sciences courses. Includes exploration of entrepreneurship opportunities; types, characteristics & motivations of entrepreneurs; case studies; interviews of entrepreneurs and/or business plan preparation

Mount Pleasant Titus Entrepreneurship: Ideas in ActionIncludes case studies, extensive business plan preparation, and numerous interactive activities

SOURCE: TIP Strategies research.

High School E-sh ip Programs

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 21

ENTREPRENEURIAL CLIMATE

The entrepreneurial climate of a community encompasses both the acceptance of entrepreneurs among community members and the regulatory environment created by local government.

Respondents to the Entrepreneurs Survey and participants in the focus groups found the Northeast Texas and Southwest Arkansas region to be entrepreneurial-friendly in terms of acceptance of the community. Community members actively support local businesses when possible, and business owners make a concerted effort to patronize each others’ businesses. The region does, however, lag somewhat in promoting an entrepreneurial climate through youth entrepreneurship programs. In addition, the entrepreneurs pipeline that is strengthened by an entrepreneur-friendly environment could also be improved.

From a regulatory standpoint, each county and city differed. Mount Pleasant’s entrepreneurs perceived the city and the community to be exceptionally supportive of small business. Other communities, however, noted the difficulty in navigating the permitting process. Some downtown business districts, in particular, were perceived to have very restrictive codes that made downtown storefronts and office space difficult to develop.

Perce ived Entrepreneur ia l C l imate Strongly Disagree Disagree Neutral Agree

Strongly Agree

Rating Average

Response Count

People in the community try to support local businesses.0.0% (0)

10.3% (7)

16.2% (11)

58.8% (40)

14.7% (10) 3.78 68

My community generally admires entrepreneurs.1.5% (1)

8.8% (6)

17.6% (12)

57.4% (39)

14.7% (10) 3.75 68

People are aware of successful entrepreneurs in the region.1.5% (1)

5.9% (4)

22.1% (15)

47.1% (32)

23.5% (16) 3.85 68

Our school district teaches children to value entrepreneurship.4.6% (3)

26.2% (17)

49.2% (32)

16.9% (11)

3.1% (2) 2.88 65

Many of my friends and family would like to start a business some day.

4.5% (3)

16.7% (11)

34.8% (23)

37.9% (25)

6.1% (4) 3.24 66

As a small business owner, I feel that the community is supportive of entrepreneurs.

1.5% (1)

6.0% (4)

28.4% (19)

53.7% (36)

10.4% (7) 3.66 67

SOURCE: TIP Strategies research.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 22

SUMMARY

Overall, most entrepreneurial assets are represented somewhere in the region. However, some areas of the region have access to assets that others do not. In addition, all of these assets available to entrepreneurs struggle to connect with their potential clients (entrepreneurs) as the entrepreneurs struggle to find the services and support that they need. Finally, many of the service providers work independently of one another and are not aware of what the others are doing. As a result, the entrepreneurship initiative for the region as a whole is fragmented and not effectively coordinated.

A summary of the gaps identified is presented below.

Asset Category Existing Gaps Capital Local banks

Informal angel network Small revolving loan funds

Formal angel network Regional revolving loan fund Financial literacy training

Business Services Legal

Accounting Marketing Human resources

Information technology Affordable healthcare Education about services

Education & Information Programs

SBDCs Higher education

institutions CORRE Paris incubator Sulphur Springs assistance

center Some youth e-ship training

Matching training offerings with entrepreneur needs

More regional access to training Entrepreneur boot camp Peer networking Formal mentor network Information clearinghouse Coordinated youth e-ship

initiative

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 23

Strategic Recommendations Through the work of the Kellogg Foundation, the Corporation for Enterprise Development (CFED), the Rural Policy Research Institute (RUPRI), and other leaders in rural entrepreneurship development, a consensus has emerged about what a comprehensive entrepreneurship development strategy must entail – “a coordinated infrastructure of public and private supports that facilitate entrepreneurship.”2 This infrastructure is referred to as an ENTREPRENEURSHIP DEVELOPMENT SYSTEM (EDS). These leaders in rural entrepreneurship development have further outlined a set of guiding principles for the creation of an EDS.

The Kellogg / CFED EDS team explain that “an EDS should be: Entrepreneur focused – driven by the true needs of entrepreneurs. Inclusive – of all types of entrepreneurial talent; of underrepresented populations

and communities; of all types of organizational leadership. Asset based – building on the region’s assets. Collaborative – (1) leadership across private, public and non-profit sectors and (2)

engagement of service providers. Comprehensive and integrated – addresses all elements of an EDS and integrates

entrepreneurship into other aspects of regional economy. Community-based but regionally-focused – rooted in communities but connected

to the resources of a region. Linked to policy – informing economic development policy (local and state) through

the demonstration of entrepreneurship in communities and regions. Sustainable over time – if entrepreneurship development is a long-term strategy, the

systems must be sustainable over time as well. Continuous improvement – articulating and measuring outcomes that reflect the

goals of EDS, and being flexible enough to revamp, retool, and rethink the practice as you move forward.“3

2 Mapping Rural Entrepreneurship, W. K. Kellogg Foundation and CFED, August 2003. 3 Kellogg EDS Collaboratives. http://www.cfed.org/focus.m?parentid=32&siteid=601&id=601

CASE STUDY: the Kel logg EDS Col laborat ives

In 2005, the Kellogg Foundation awarded $2 million grants to six collaborative entrepreneurship efforts. The objective of these grants is to enable the collaborations to promote entrepreneurial activity in their regions, showcase successful models of entrepreneurship activity to rural communities outside their area, leverage significant new investments, and stimulate state and national interest in rural entrepreneurship policies and strategies.

The groups that were awarded the grants were:

Empowering Business Spirit Initiative Collaborative, serving Northern New Mexico counties, pueblos, and tribes.

Connecting Oregon for Rural Entrepreneurship Collaborative, serving Lake County, Lincoln County, Northeast, Southwest, and North-Central Oregon.

Oweesta Collaborative, serving Pine Ridge and Cheyenne River reservations of South Dakota (Lakota Sioux), and the Wind River Reservation in Wyoming (Eastern Shoshone and Northern Arapahoe).

HomeTown Competitiveness Collaborative, serving 15 counties in Nebraska and the Winnebago, Omaha, and Santee Sioux reservations.

Advantage Valley Entrepreneurship Development System Collaborative, serving eight counties in West Virginia, Boyd and Greenup counties in Kentucky, and Lawrence County in Ohio.

North Carolina's Rural Outreach Collaborative, serving 85 rural counties of North Carolina, including seven rural Native American Tribes.

The experiences of these programs provide valuable best practices and lessons learned for other communities looking to start their own EDS.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 24

TIP incorporates these guidelines into its entrepreneurship strategies in order to create robust systems that serve the needs of local entrepreneurs and promote entrepreneurial – friendly climates.

As previously mentioned, the regional entrepreneurship initiative in Northeast Texas and Southwest Arkansas is fragmented. While many of the entrepreneurial assets are in place, they are not connected in a way that maximizes support for entrepreneurs. In order to create a unified entrepreneurship development initiative, TIP recommends adopting the following three goals:

Develop an entrepreneur development system.

Augment support services.

Promote a more entrepreneurial climate and culture.

On the following pages, we outline strategies and actions to support the above goals. Adopting these goals and strategies will help connect the region’s fragmented initiatives to create a more comprehensive, well-targeted system to support entrepreneurs.

GOAL ONE: DEVELOP AN ENTREPRENEUR DEVELOPMENT SYSTEM (EDS)

1. Design an online entrepreneurs portal Create a high-quality, user-friendly Web site for entrepreneurs. Choose an

easy-to-remember address. Include a directory of services providers, calendar of events, information resources, and forum for entrepreneurs to share information and exchange ideas.

Consider including a social networking platform to allow entrepreneurs to better connect with each other. Companies such as Small World Labs (www.smallworldlabs.com) offer software to create these platforms.

US Source Link (http://www.ussourcelink.com/) provides a model for linking service providers to each other and to clients through an online portal. The Wisconsin Entrepreneurs Network

CASE STUDY: the Empower ing your Business Spi r i t In i t ia t ive

Founded in 2005, the EBS initiative is a collaborative of 20 service providers dedicated to supporting entrepreneurs in North Central New Mexico.

The EBS collaborative came together to determine how best to nurture entrepreneurship in the region. In this spirit, they have identified two major initiatives: (1) teaching entrepreneurship and providing opportunities for entrepreneurship in schools; and (2) using a network facilitation model to support entrepreneurs in the region.

A corner stone of this collaborative is their small business portal that provides a link to all of the partners’ Web sites, updated news stories on topics relevant to entrepreneurs, and a calendar of events.

The initiative was initially funded by a grant from the Kellogg Foundation. However, donations from EBS partners now play a central role in supporting the initiative.

For more information: http://www.bizport.org/

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 25

(http://www.wenportal.org/) provides another example of a useful portal.

Update the Web site at least monthly to keep information current and relevant.

Launch an active region-wide outreach initiative to drive entrepreneurs to the Web site.

Send postcards with the Web address out to new businesses registered with regional counties.

Publish the Web site in service providers’ and partners’ newsletters and in local newspapers.

Provide links to the Web site from service providers and partners’ Web sites.

Distribute cards with the Web address to service providers and partners to hand out to their clients and members.

2. Create a strong network of partners and service providers

Service providers that should be included are the SBDCs, chambers of commerce, higher education institutions, economic development corporations, any entrepreneur-oriented non-profit organizations, and business bankers.

Educate service providers about each other’s services by convening service providers in a central location. Have each service provider introduce themselves, their organization, and their entrepreneurial initiative. Focus on clarifying exactly what services each provides and what kind of clients each serves. This self-education serves to connect service providers and craft a better referral network. This, in turn, helps to encourage a “no wrong door policy” for entrepreneurs seeking assistance.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 26

Schedule regular meetings and facilitate regular communication among service providers to explore partnership opportunities, share progress and highlight best practices.

3. Build capacity in regional communities to better support entrepreneurs

Train community leaders, economic development professionals, and policy-makers on how to promote entrepreneurship and an entrepreneurial climate in their communities.

The Kentucky Entrepreneurial Coaches Institute provides an excellent model.

The Texas Agrilife Extension’s Rural Entrepreneurship Support Network (http://www.tcre.org/Default.aspx?tabid=159) has a free training curriculum available to communities in Texas.

The Rural Policy Research Institute (RUPRI) also provides a training course to communities. These courses can be anything to half-day in-service trainings to full-week institutes. (http://www.energizingentrepreneurs.org/)

The Sirolli Institute trains communities on how to implement their trademarked Enterprise Facilitation model. (http://www.sirolli.com/) This is the model that the city of Clarksville is pursuing.

Once an initial training is held, schedule periodic conferences and seminars on topics of interest to keep entrepreneurship in the minds of the trainees. Allocate time for participants to share experiences and support one another.

GOAL TWO: AUGMENT SUPPORT SERVICES

1. Develop a three-tiered support system for entrepreneurs in the region. Different types of entrepreneurs have different needs. As a result, a one-size-fits-all approach to providing services to entrepreneurs will inevitably leave one or more groups with

CASE STUDY: Kentucky Entrepreneur ia l Coaches Inst i tute

In 2003, the College of Agriculture at the University of Kentucky founded the Kentucky Entrepreneurial Coaches Institute to promote economic diversification in Northeastern Kentucky. Since then, the program has expanded into South Central Kentucky as well.

The program trains coaches through an intensive series of seminars and a national education tour. Thirty participants are selected from the pool of applicants to receive a fellowship to attend the institute. These fellowships are funded through the Kentucky Agricultural Development Board.

The Entrepreneurial Coaches are volunteers who work with entrepreneurs. Rather than providing technical assistance, they serve as a resource for entrepreneurs, help them assess their businesses, and assist them in finding the technical support that they need.

The program was named one of the top programs in the nation by the Small Business Administration.

For more information: http://www.uky.edu/Ag/CLD/KECI/

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 27

ENTREPRENEURIAL TALENT

Limited Potential

PotentialEntrepreneurs

Business Owners

Entrepreneurs

Not Working Want to be an Employee

(Lack motivation and capacity)

Frustrated

Aspiring

Start-ups

Dreamers

Youth

(Motivations include dislocations, glass ceiling / dead end, desire for more, need to create it.)

Lifestyle

Re-starts

Survival

(Limited motivation to grow) (Unable to see how to grow)

Serial Growth-Oriented

Entrepreneurial Growth

Companies

Long-Term

Medium-Term

Short-Term

TYPE OF TALENT INTERVENTION TIME FRAME

SOURCE: RUPRI Center for Rural Entrepreneurship.

needs unmet. Developing a tiered-system will help to create a system that specifically targets the needs of each type of entrepreneurs.

The tiers should correspond to the type of entrepreneurial talent:

High-growth. Entrepreneurs who are motivated to rapidly expand and grow their businesses into something more than a family-owned company. Their businesses are often highly innovative and are export-oriented with customers beyond their local markets.

Potential. Entrepreneurs who are attracted to the idea of starting their own businesses or have just started their own businesses.

Business Owners. Entrepreneurs who have started businesses to supplement their incomes or maintain a certain lifestyle.

Develop a self-assessment tool that entrepreneurs can use to place themselves on the appropriate track. This tool may be accessed through the Web portal.

Using this assessment tool, entrepreneurs and aspiring entrepreneurs can identify their goals, motivations, and plans.

Based on the outcome of the assessment, entrepreneurs can be directed to the tier of services that will best suit their needs. In addition, it will provide the region with a record of entrepreneurs using the portal.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 28

2. Strengthen and target support services for each tier. This will ensure the needs of each group of entrepreneurs are better met. While the services will be specifically targeted, many of the services can support more than one type of entrepreneur at a time.

Tailor a tier of services specifically for high-growth entrepreneurs. At present, few services exist for this category of entrepreneurs. While this is the least common type of entrepreneurs, it is the type that has the highest economic impact, in terms of job and wealth creation. As a result, it is not necessary for each community in the region to provide all of these services; rather, the services should be provided at a regional level and accessible to all communities. In some cases, the demand for the service may be strong enough to support providing the service at the local level as well. The future entrepreneur center at Texas A&M University – Texarkana could be a good lead partner for developing this tier of services. The local economic development corporations would be good leads at the community level. The services that should be included are:

Peer networking opportunities. The objective of these opportunities should be to provide entrepreneurs with a forum to exchange ideas with one another in an effort to help each resolve salient business issues. A facilitator should be present to lay the ground rules and to help ensure that the opportunities do not become leads generation events. These could be held in-person or virtually through a teleconference or video conference. Groups should be kept relatively small (fewer than 15 participants). These could be offered at the community level, depending on demand.

Assistance raising capital. High-growth entrepreneurs will likely need to access equity capital to finance their companies through the CONCEPT and INCEPTION phases of development. The assistance provided should include education on the process; preparing a professional, compelling pitch; connecting with potential investors (both angels and venture capital); and structuring a deal. This should be offered at the regional level.

CASE STUDY: Ind iana Venture Center

Founded in 2003, the Indiana Venture Center is a non-profit organization that seeks to increase the number and quality of entrepreneurial, high-growth companies in Indiana.

Through its staff and collaboration with local universities, the center provides promising companies with assistance from exploring concept feasibility to raising capital. In addition, it has created AngelNet, an angel network that connects entrepreneurs with investors.

The center works closely with entrepreneurship programs and business schools at seven universities across the states to promote educational opportunities for entrepreneurs. Also through this collaboration, the center matches entrepreneurial companies with groups of student consultants to work on special projects as part of the Venture Creation Accelerator.

For more information: http://www.indianaventurecenter.org/

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 29

Angel investor network. Formalize the regional angel investor network to increase participation of angels and further support high-growth entrepreneurs. A helpful guide for creating a network can be found at http://www.kauffman.org/pdf/angel_guidebook.pdf. In addition, AngelSoft is a valuable resource for creating angel networks (http://www.angelsoft.net/). This network should operate at the regional level.

Advisory board resources. Advisory boards can serve as a valuable mentor for entrepreneurs and help to build stronger companies. This service should assist entrepreneurs in assembling an effective advisory board and should offer training to entrepreneurs and board members on their roles and responsibilities. This could be offered at the community level, depending on demand.

Enhance support services for potential entrepreneurs, including aspiring entrepreneurs and start-ups. Much of the existing services are geared towards this group of entrepreneurs. Community colleges and the SBDCs would be good community partners for hosting and/or facilitating these programs. The services that should be included in this tier are:

Entrepreneur boot camp. Contact one of the area’s certified trainers for FastTrac or NxLevel to explore offering these courses in the region. If those existing certified trainers cannot conduct classes in the region, arrange for one or more of the regional service providers to become a certified trainer. Set a goal of offering a course at least twice a year at first. Then, as demand grows, expand the course offerings.

Regional revolving loan fund. Create a regional revolving loan fund, establishing an effective structure and sound policies and procedures. This fund should be designed specifically to provide access to credit to those entrepreneurs who currently do not have access. If possible, seek the participation of existing loan funds to better leverage those resources in the region and share marketing expenses.

CASE STUDY: Blue Ridge Angel Investor Network (BRAIN)

Founded in 2002 by the AdvantageWest Economic Development Group, BRAIN has invested over $2 million and helped companies raise an additional $10 million in capital.

BRAIN members meet quarterly to review pre-screened business plans. While the group collaborates on due diligence, each member makes individual investment decisions.

For those entrepreneurs in whose companies BRAIN members invest, the members serve as mentors and coaches and assist them in team building, strategic planning, and fundraising.

BRAIN investments are focused on 10 industry clusters, thus reinforcing the greater economic development efforts of AdvantageWest.

For more information: http://www.brainnc.com/index.cfm

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 30

Numerous programs across the country exist and can be researched to identify best practices. In addition, the following resources are available to provide guidance and technical assistance:

― The Council of Development Finance Agencies: http://www.cdfa.net/cdfa/cdfaweb.nsf/pages/rlffactsheet.html

― The National Association of Development Organizations: http://www.nado.org/edfs/index.php

― Development Finance Training and Consulting, Inc.: http://devftc.com/economic.php

Coordinate a regional youth entrepreneurship initiative. Encourage the regional school districts to become involved in the regional initiative by incorporating entrepreneurship into their existing curricula and supporting the expansion of Junior Achievement in schools in the region.

Continue to support existing business owners, including lifestyle and survival businesses. The SBDCs already do an excellent job supporting these businesses with training courses and one-on-one counseling. However, a few services could be added to the offerings. These services include:

Formal mentor network. Develop a network of experienced entrepreneurs or businessmen and women who are willing to volunteer their time to work with entrepreneurs. Match the skills of these volunteer mentors with the needs of the participating entrepreneurs. Facilitate an initial meeting between volunteer and entrepreneur. Further meetings should be set up at the discretion of the volunteer and mentor.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 31

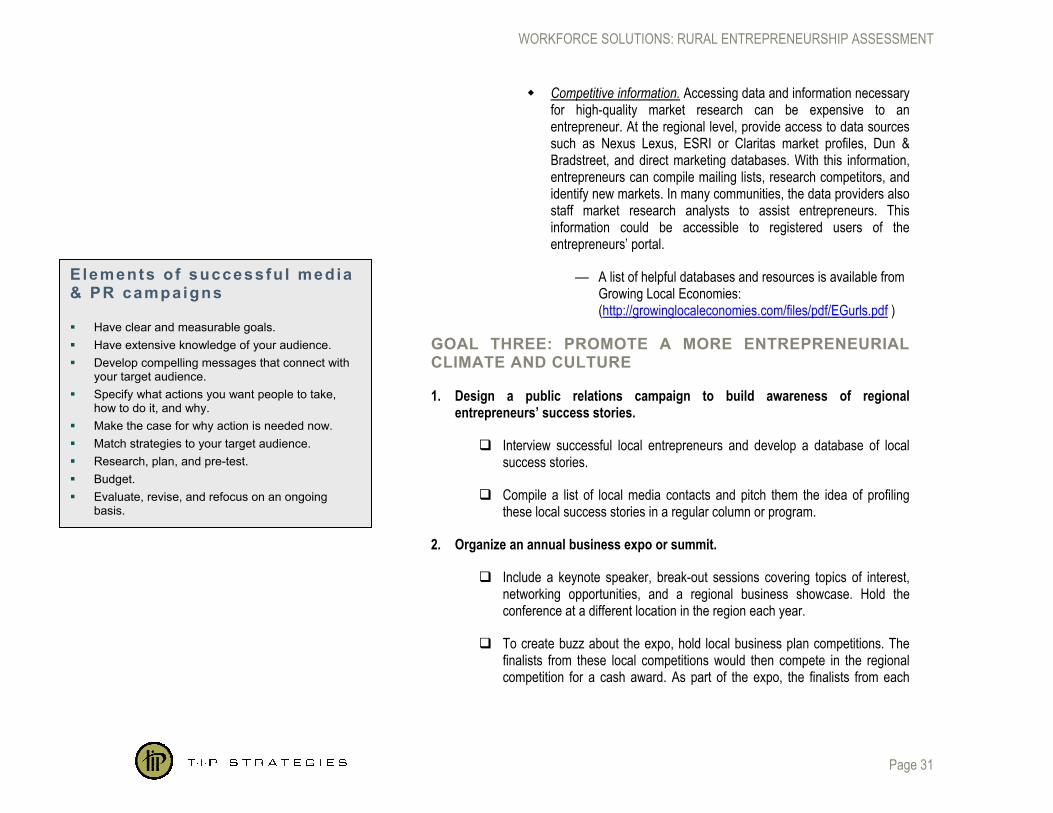

Competitive information. Accessing data and information necessary for high-quality market research can be expensive to an entrepreneur. At the regional level, provide access to data sources such as Nexus Lexus, ESRI or Claritas market profiles, Dun & Bradstreet, and direct marketing databases. With this information, entrepreneurs can compile mailing lists, research competitors, and identify new markets. In many communities, the data providers also staff market research analysts to assist entrepreneurs. This information could be accessible to registered users of the entrepreneurs’ portal.

― A list of helpful databases and resources is available from Growing Local Economies: (http://growinglocaleconomies.com/files/pdf/EGurls.pdf )

GOAL THREE: PROMOTE A MORE ENTREPRENEURIAL CLIMATE AND CULTURE

1. Design a public relations campaign to build awareness of regional entrepreneurs’ success stories.

Interview successful local entrepreneurs and develop a database of local success stories.

Compile a list of local media contacts and pitch them the idea of profiling these local success stories in a regular column or program.

2. Organize an annual business expo or summit.

Include a keynote speaker, break-out sessions covering topics of interest, networking opportunities, and a regional business showcase. Hold the conference at a different location in the region each year.

To create buzz about the expo, hold local business plan competitions. The finalists from these local competitions would then compete in the regional competition for a cash award. As part of the expo, the finalists from each

Elements of successfu l media & PR campaigns

Have clear and measurable goals. Have extensive knowledge of your audience. Develop compelling messages that connect with

your target audience. Specify what actions you want people to take,

how to do it, and why. Make the case for why action is needed now. Match strategies to your target audience. Research, plan, and pre-test. Budget. Evaluate, revise, and refocus on an ongoing

basis.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 32

local competition would have to make their pitch to be judged by a panel of successful entrepreneurs (perhaps nationally known). The pitch presentations should be open to the public and media.

Organize these business plan competitions for youth entrepreneurs as well as adults.

3. Lower barriers to entry for new entrepreneurs.

Create a Health Group Cooperative to provide small employers in the region with access to more affordable healthcare. Information on creating a cooperative can be found at the Texas Department of Insurance Web site: http://www.tdi.state.tx.us/health/indexlhcoop.html

On the entrepreneurs Web site, post information on registering businesses and obtaining necessary permits for each county. Include pertinent addresses and contact numbers to help new businesses navigate the process. Include a section where entrepreneurs can post advice on how to better navigate the system.

Establish a working group that will examine regulatory policies that affect small businesses in the region to ensure that these policies do not inadvertently negatively affect small businesses.

CASE STUDY: Lubbock Chamber Employer Heal th P lan

In 2006, the Lubbock Chamber of Commerce launched an employer health plan to help its members find affordable health insurance. Members with two or more employees may enroll in the plan and choose from seven different plan designs offered by FirstCare.

In order to offer this employer plan, the Chamber formed two Health Group Cooperatives, one for large employers and one for small employers. Health Group Cooperatives must have at least 10 employers and may grow to any size, but it will be considered a single large employer for the purposes of issuance of coverage and rating. This structure provides the opportunity for the cooperative to realize savings and obtain more flexibility in plan design.

As of June 2008, the Chamber has 10,242 lives enrolled in the plan, 20 percent of which were previously uninsured. The average business enrolled in the plan has 10 employees. Small business owners enrolled in the plan have been able to realize thousands of dollars of savings while covering more of the premium cost for their employees.

For more information: http://www.lubbockchamber.com/healthcare.htm http://www.tdi.state.tx.us/health/indexlhcoop.html

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 33

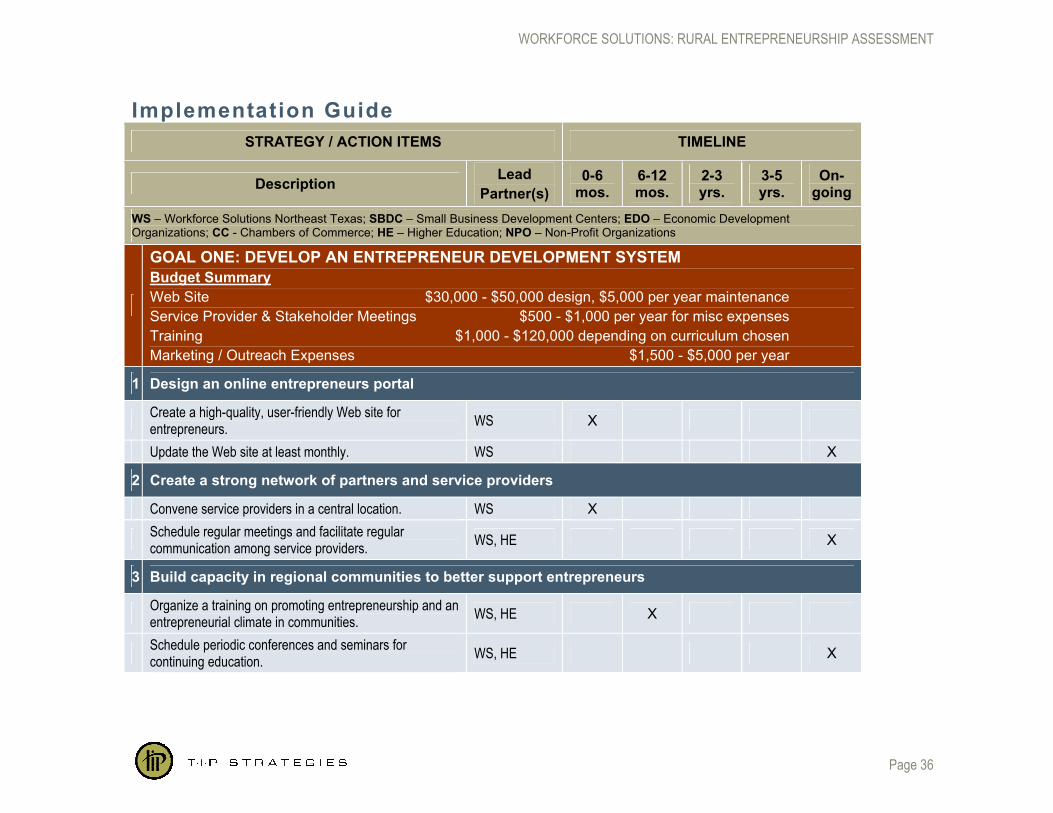

Organizational Recommendations In order to implement these strategies, the region must dedicate resources, both human and financial. TIP recommends the following actions:

1. Assemble a roundtable of representatives from participating counties.

This roundtable should meet on a regular basis (at least quarterly).

Initially, the roundtable should create working groups assigned with the responsibility of ensuring that specific strategies are implemented. These working groups should work with the relevant service providers and other partners to identify any additional resources needed and create an implementation work plan.

In subsequent meetings, each working group should report on progress, sharing any successes and discussing any implementation issues.

2. Consider hiring at least one full-time staff person devoted to the plan implementation.

This person would provide support for the roundtable working groups and the implementation of the initiative with responsibilities including:

Fund raising

Research

Coordination of meetings, training sessions, workshops, and events

Outreach

Updating the entrepreneurs portal

Basic administrative support

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 34

3. Identify accountability measures to track progress.

Choose performance measures that track both outputs and outcomes of the initiative. Such measures could include:

# of visitors to the Web site

# of entrepreneurs registered through the Web site

# of self-assessments completed through the Web site

# of trainings / networking events held and # of participants (by type – service provider, capacity building. and direct assistance to entrepreneurs)

# of mentor–entrepreneur relationships created through the network

# of youth participating in entrepreneurship classes and activities

Total # of clients assisted through service provider network

# of new businesses started

# of new jobs created

$ value of capital raised (angel, venture, revolving loan fund, loan packaging)

Track these measures on at least an annual basis and produce a report card to distribute to partners and funders. Publicize these achievements on the Web site.

At trainings and networking events (when appropriate), have participants complete an evaluation of the event. Use these evaluations as a means of feedback to ensure the events are useful for the participants.

WORKFORCE SOLUTIONS: RURAL ENTREPRENEURSHIP ASSESSMENT

Page 35

4. Raise funds needed to implement the plan.

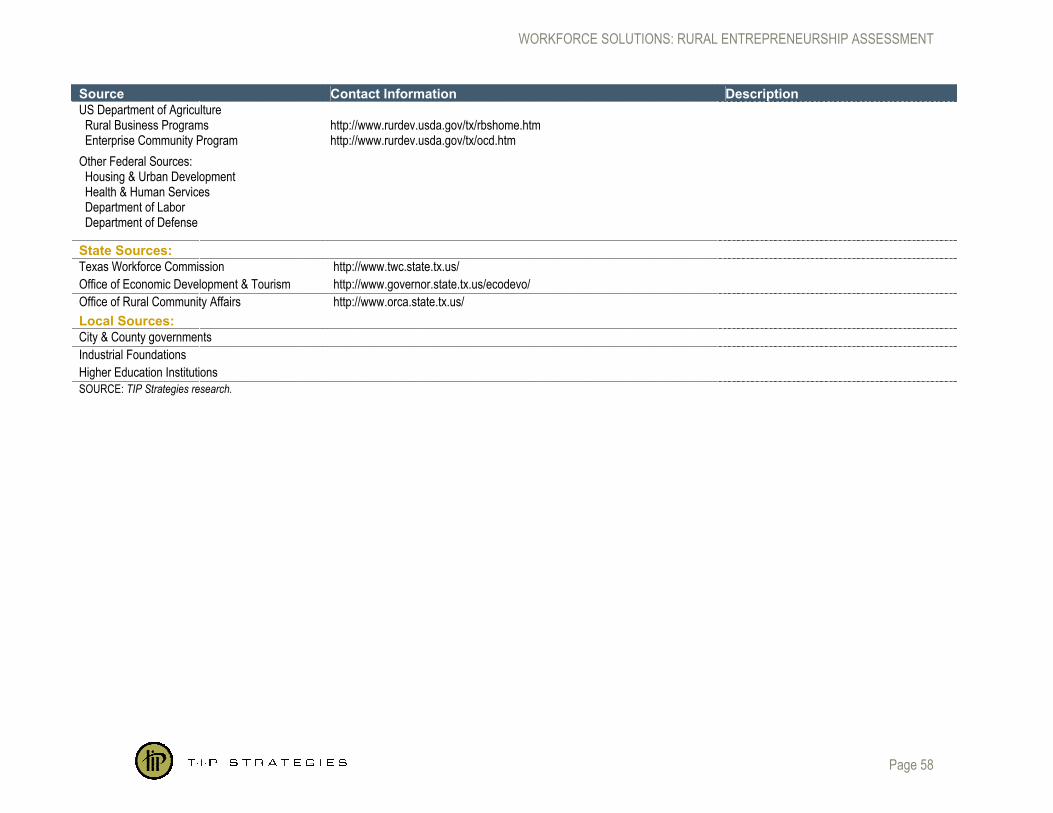

Seek funding from a mix of private and public funding sources (see Appendix D – Potential Funding Sources).

Launch a local fund raising campaign to tap into local community foundations, donors, and other resources.