2007 ELFA Lease Accountants Conference · 2007 ELFA Lease Accountants Conference Suresh Makam –...

44

Basics of Tax Leasing (1) 2007 ELFA Lease Accountants Conference Suresh Makam – 914-899-7912 Citi Bankers Leasing

Transcript of 2007 ELFA Lease Accountants Conference · 2007 ELFA Lease Accountants Conference Suresh Makam –...

Basics of Tax Leasing (1)

2007 ELFA Lease Accountants Conference

Suresh Makam – 914-899-7912Citi Bankers Leasing

Single Investor Lease

– Lessor purchases the equipment with equity or proceeds of recourse loan

– Lessor’s return depends upon Lessee’s credit andequipment value

– Lessor is 100% at risk• There are no non-recourse loan amounts

3

True Lease Issues Is the lease a “True Lease”?

IRS Guidelines

• As of May 7th, 2001, the following Revenue Procedures were superseded by Revenue Procedure 2001-28 and Revenue Procedure 2001-29:– Revenue Procedure 75-21– Revenue Procedure 75-28– Revenue Procedure 76-30– Revenue Procedure 79-48

IRS Guidelines

In Revenue Procedure 2001-28, the IRS stated that:• To qualify for an advance ruling regarding the tax• status of a leveraged lease, a lease contract must• adhere to the following guidelines:

a. Minimum unconditional “At Risk” investmenti. Minimum Investment must remain equal to at least 20% of the

cost of the property at all times throughout the entire lease term.

ii. Equipment must have a remaining useful life beyond the lease term of the longer of one year or 20% of the originally estimated useful life.

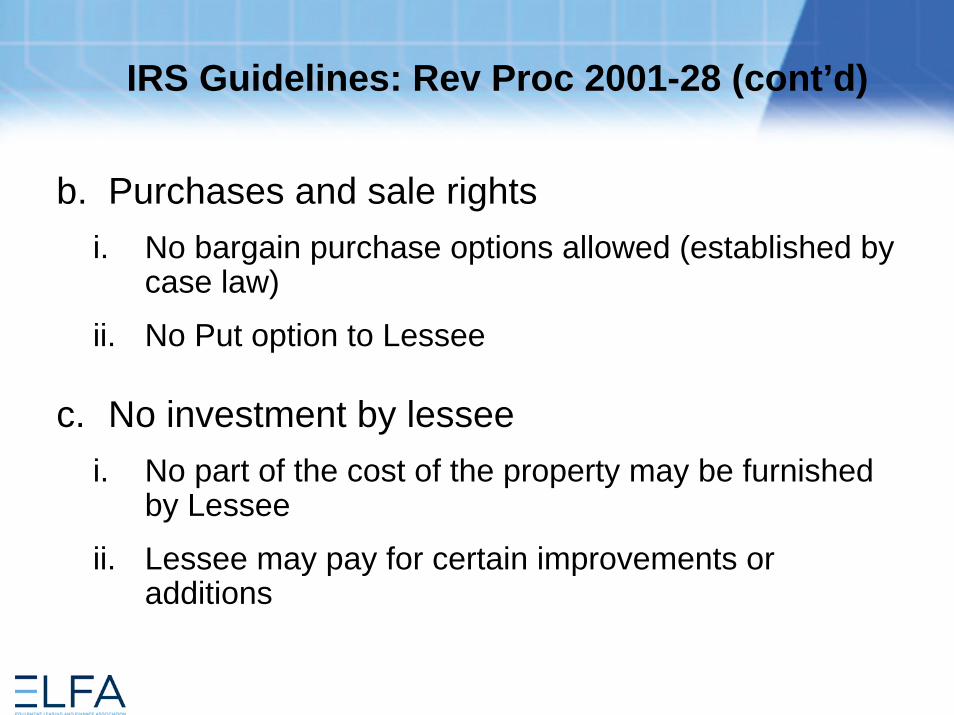

IRS Guidelines: Rev Proc 2001-28 (cont’d)

b. Purchases and sale rightsi. No bargain purchase options allowed (established by

case law)

ii. No Put option to Lessee

c. No investment by lesseei. No part of the cost of the property may be furnished

by Lessee

ii. Lessee may pay for certain improvements or additions

IRS Guidelines: Rev Proc 2001-28 (cont’d)

d. No lessee loans or guarantees

e. Profit requirement (complex IRS formula)

f. Positive cash flow (complex IRS formula)

g. No Limited Use property

IRS Guidelines: Rev Proc 2001-28 (cont’d)

– Rev Proc 2001-28 is best understood as a “bright line” test, but case law has been more flexible

– Neither the IRS nor the tax courts have worked out a fully comprehensive articulation of the differences between a true lease and a non-true lease

– Guidelines are safe harbor and are technically applicable only to leveraged leases

9

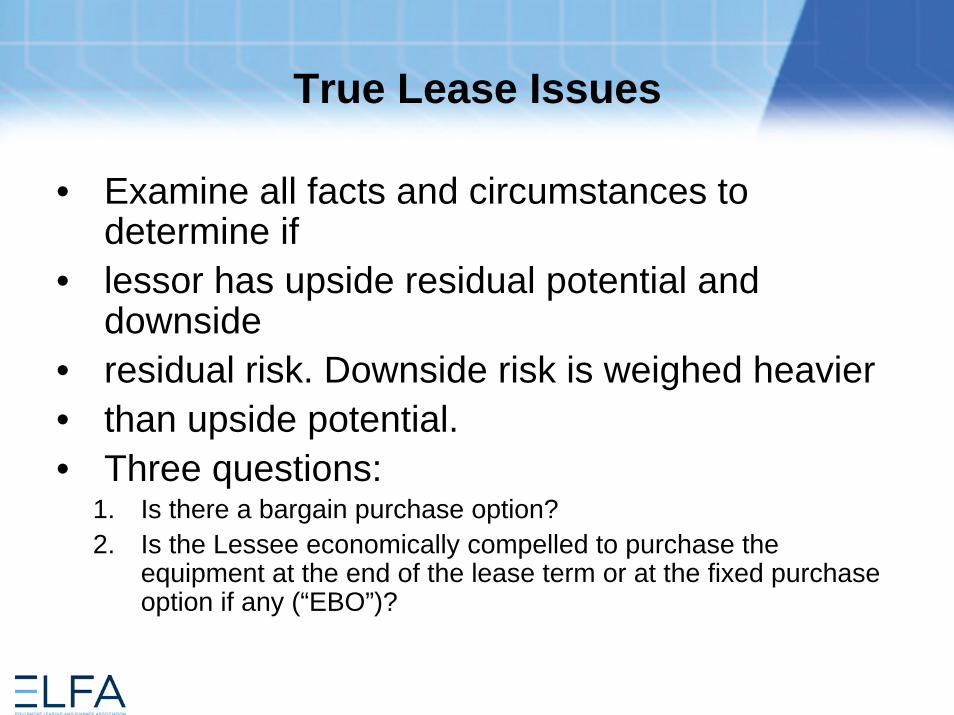

True Lease Issues

• Examine all facts and circumstances to determine if

• lessor has upside residual potential and downside

• residual risk. Downside risk is weighed heavier• than upside potential.• Three questions:

1. Is there a bargain purchase option?2. Is the Lessee economically compelled to purchase the

equipment at the end of the lease term or at the fixed purchase option if any (“EBO”)?

10

True Lease Issues (cont’d)

3. Is it commercially feasible that someone other than Lessee will use the property after thelease expires?

– Limited use property– Useful life– Residual value

11

Examples of True Lease Structures– Purchase option fixed at reasonable estimate of FMV

– Early termination at option of Lessee who guarantees sales price on sales to third party, by way of a cancellation payment

– Non-bargain purchase option (“EBO”) during the base term; provided that if purchase option is not exercised the term is extended with a Fair Market Value (FMV) option at the end of renewal term (first amendment)

– 3rd party residual guarantee (not a put)

– TRAC leases See IRC Sec. 7701(h)

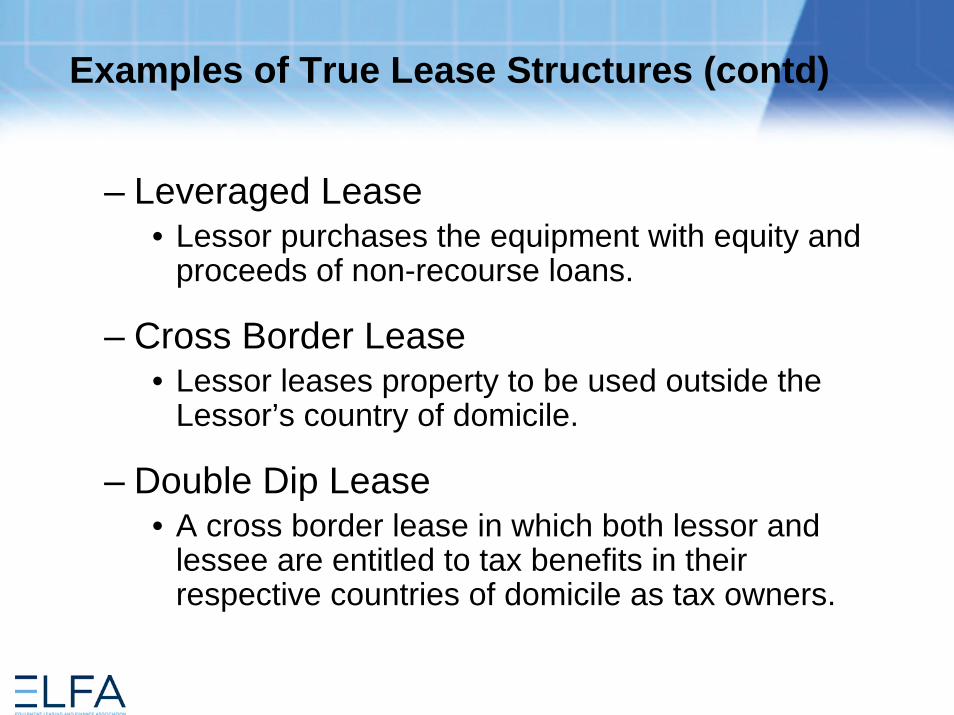

Examples of True Lease Structures (contd)

– Leveraged Lease• Lessor purchases the equipment with equity and

proceeds of non-recourse loans.

– Cross Border Lease• Lessor leases property to be used outside the

Lessor’s country of domicile.

– Double Dip Lease• A cross border lease in which both lessor and

lessee are entitled to tax benefits in their respective countries of domicile as tax owners.

13

Examples of Non-True Lease Structures

– Bargain Purchase option (including $1 out)

– Synthetic leases: Product term for a lease that takes advantage of inconsistencies in tax and accounting rules for the benefit of the lessee. Lease is structured as a conditional sale (or financing) for tax purposes, and an operating lease for lessee accounting purposes. Lessee has purchase option (upside) and guarantees a portion of residual value (the riskiest portion so that Lessee has predominant downside risk). Thus, the lessee takes the tax benefits of ownership, but gets off balance sheet accounting

– Loans and conditional sales agreements

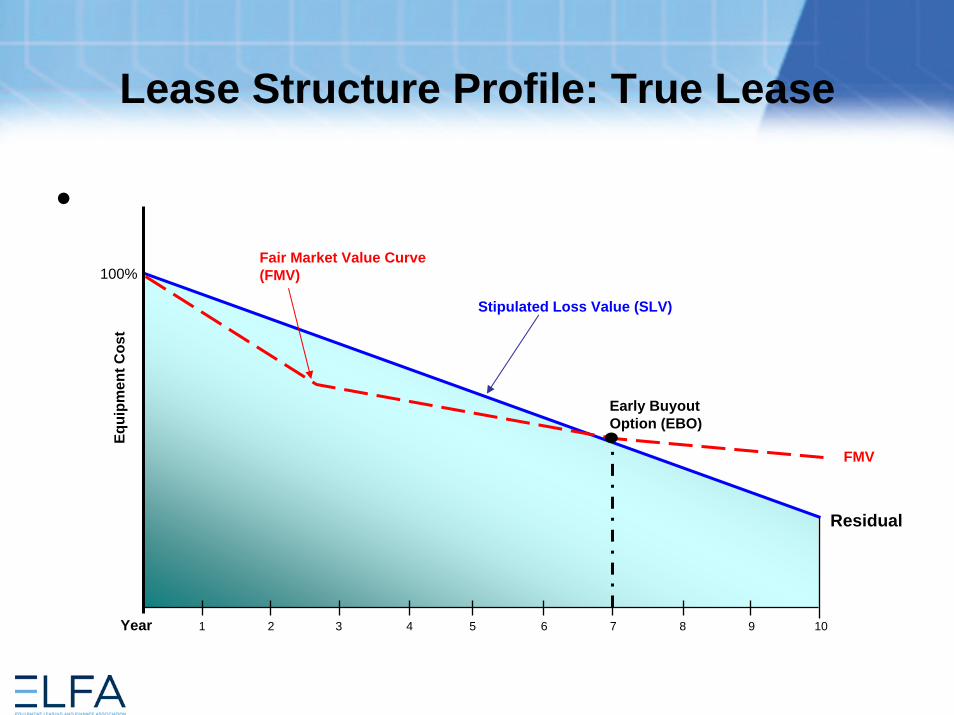

Lease Structure Profile: True Lease

•

1 2 3

Residual

Early BuyoutOption (EBO)

Stipulated Loss Value (SLV)

Fair Market Value Curve (FMV)

4 5 6 7 8 9 10

100%

Equi

pmen

t Cos

t

Year

FMV

Tax Accounting: True Lease

A. A true lease is accounted for as a lease for income tax purposes:

LESSOR LESSEE Rent

Taxable income as earned (advance rents – when collected; arrears rents – accrue into proper period)

Deducted as accrued

Fees Received

Taxable income when collected N/A

Residual: Sale/Purchase Taxable income when collected Establishes depreciable basis Re-lease

Taxable income as earned Deducted as accrued

Depreciation Yearly deductions (MACRS) Not available to lessee Fees paid Up front: Write off straight line over lease term N/A Over life

Deducted as paid N/A

Interest Expense Deductible using interest method N/A

Tax Accounting: Non-True Lease

B. A non-true lease or a synthetic lease is accounted for income tax purposes as an installment sale (i.e., a loan or financing):

LESSOR LESSEE Rent

Allocated between interest income and return of principal

Allocated between interest expense and payment of principal

Depreciation Not available to lessor, since it is not the owner for tax purposes

Yearly deductions (MACRS)

Interest Expense Deductible using the interest method

17

• Depreciation Issues

18

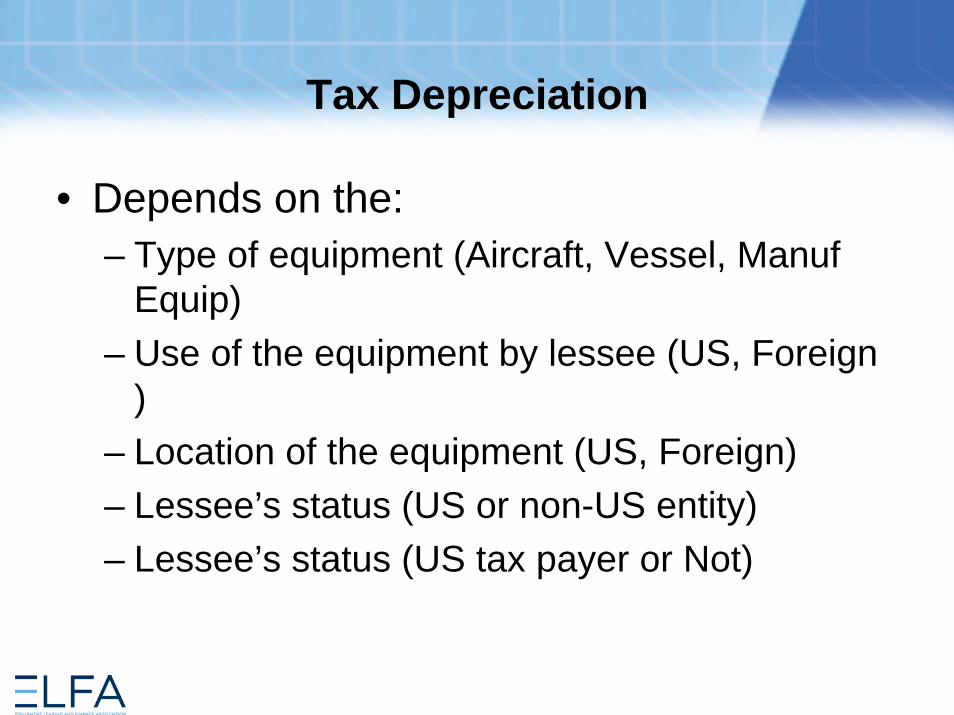

Tax Depreciation

• Depends on the:– Type of equipment (Aircraft, Vessel, Manuf

Equip)– Use of the equipment by lessee (US, Foreign

)– Location of the equipment (US, Foreign)– Lessee’s status (US or non-US entity)– Lessee’s status (US tax payer or Not)

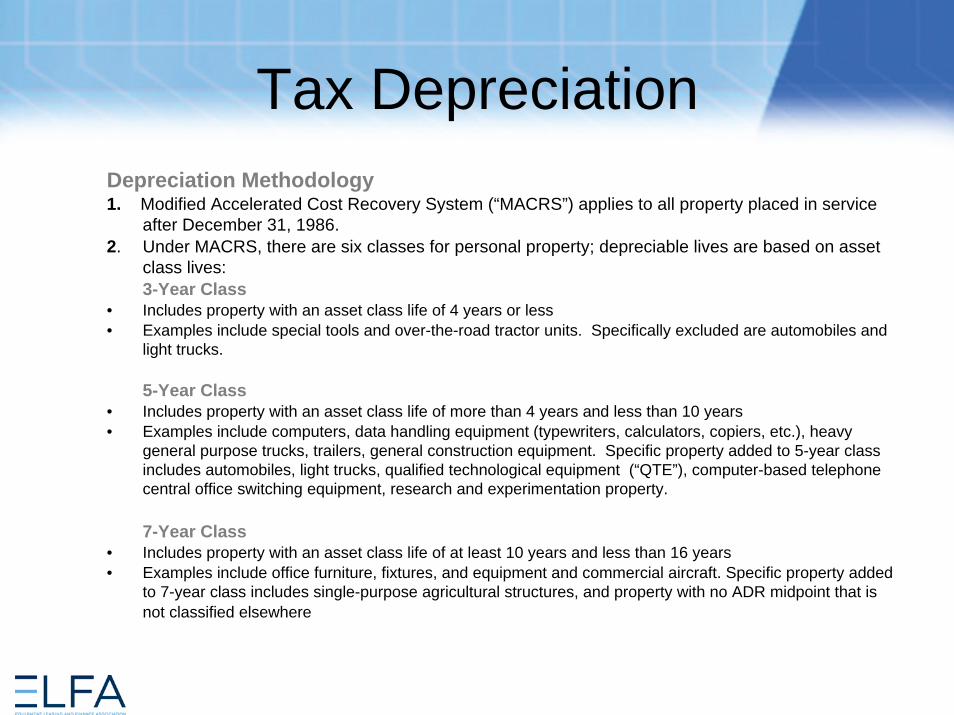

Tax Depreciation Depreciation Methodology1. Modified Accelerated Cost Recovery System (“MACRS”) applies to all property placed in service

after December 31, 1986.2. Under MACRS, there are six classes for personal property; depreciable lives are based on asset

class lives:3-Year Class

• Includes property with an asset class life of 4 years or less• Examples include special tools and over-the-road tractor units. Specifically excluded are automobiles and

light trucks.

5-Year Class• Includes property with an asset class life of more than 4 years and less than 10 years• Examples include computers, data handling equipment (typewriters, calculators, copiers, etc.), heavy

general purpose trucks, trailers, general construction equipment. Specific property added to 5-year class includes automobiles, light trucks, qualified technological equipment (“QTE”), computer-based telephone central office switching equipment, research and experimentation property.

7-Year Class • Includes property with an asset class life of at least 10 years and less than 16 years• Examples include office furniture, fixtures, and equipment and commercial aircraft. Specific property added

to 7-year class includes single-purpose agricultural structures, and property with no ADR midpoint that is not classified elsewhere

Tax Depreciation

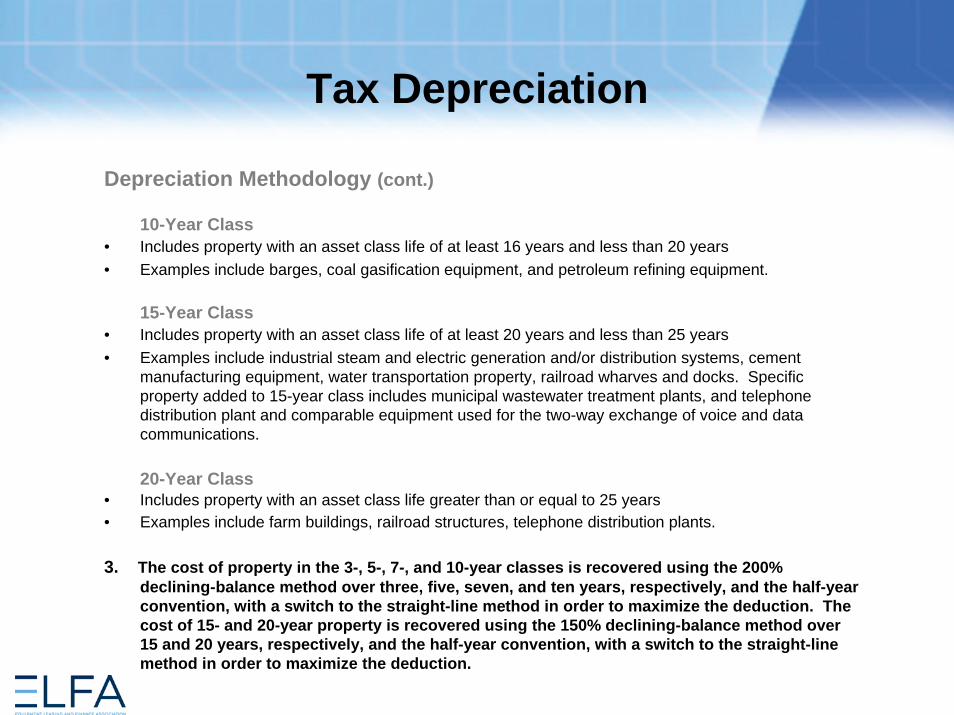

Depreciation Methodology (cont.)

10-Year Class• Includes property with an asset class life of at least 16 years and less than 20 years• Examples include barges, coal gasification equipment, and petroleum refining equipment.

15-Year Class• Includes property with an asset class life of at least 20 years and less than 25 years• Examples include industrial steam and electric generation and/or distribution systems, cement

manufacturing equipment, water transportation property, railroad wharves and docks. Specific property added to 15-year class includes municipal wastewater treatment plants, and telephone distribution plant and comparable equipment used for the two-way exchange of voice and data communications.

20-Year Class• Includes property with an asset class life greater than or equal to 25 years• Examples include farm buildings, railroad structures, telephone distribution plants.

3. The cost of property in the 3-, 5-, 7-, and 10-year classes is recovered using the 200% declining-balance method over three, five, seven, and ten years, respectively, and the half-year convention, with a switch to the straight-line method in order to maximize the deduction. The cost of 15- and 20-year property is recovered using the 150% declining-balance method over 15 and 20 years, respectively, and the half-year convention, with a switch to the straight-line method in order to maximize the deduction.

21

Depreciation Issues

• Alternative Depreciation System (ADS)– Property used predominantly outside the US, or– Lessee is a tax-exempt entity (includes foreign

entities)

• Depreciation under ADS is determined by using– Straight line method– Applicable convention– Recovery period equal to class life, but not less than

125% of the lease term in certain cases

Mid-Quarter Convention

• If more than 40% of all personal property placed in service during the year is placed in service in the last 3 months of the taxable year, all personal property placed in service during the year is subject to a mid-quarter convention.– Property placed in service and disposed of within the

same tax year is excluded in determining the 40% aggregate basis

– Test applies on a consolidated basis but withrespect to partnerships it generally applies at thepartnership level

Mid-Quarter Convention (cont’d)

• If the taxpayer triggers the mid-quarter convention, the half-year convention no longer applies. The first year depreciation amount for all personal property placed in service that year will be recalculated according to the quarter it was placed in service.

– 1st Qtr: 10.5 months– 2nd Qtr: 7.5 months– 3rd Qtr: 4.5 months– 4th Qtr: 1.5 months

Recent Changes In Tax Depreciation

• The Gulf Opportunity Zone Act Of 2005 for small business sector in Louisiana, Mississippi, And Alabama. Provisions of the GO-Zones Law will:

– Double small business expensing from $100,000 to $200,000 dollars for investments in new equipment;

– Provide a 50-percent bonus depreciation for businesses that invest in new equipment andnew structures.

Recent Changes in Tax Laws

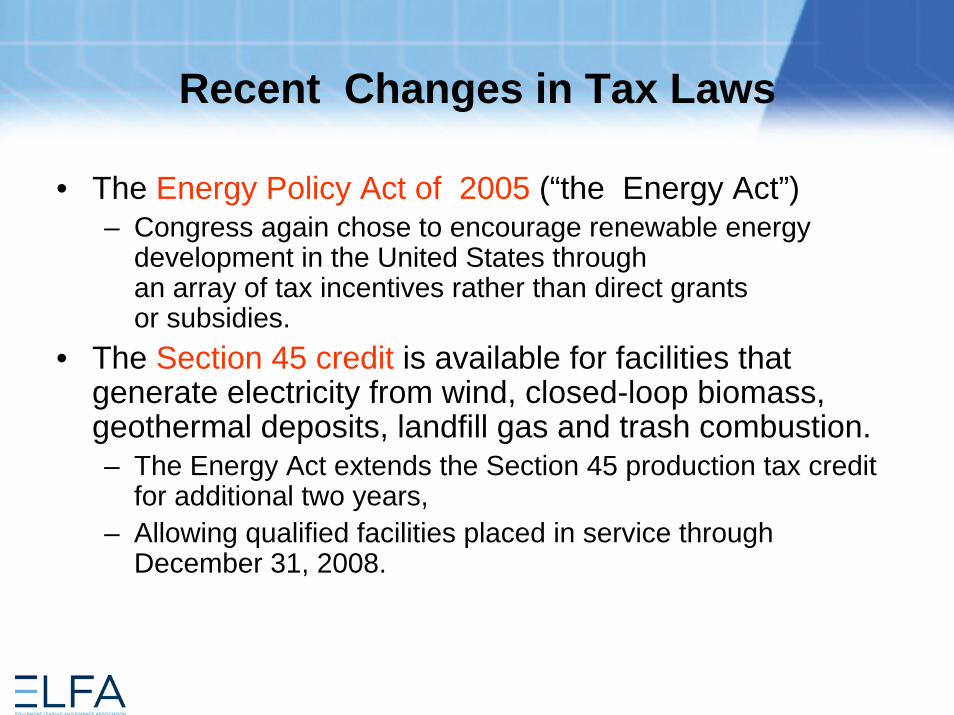

• The Energy Policy Act of 2005 (“the Energy Act”)– Congress again chose to encourage renewable energy

development in the United States throughan array of tax incentives rather than direct grantsor subsidies.

• The Section 45 credit is available for facilities that generate electricity from wind, closed-loop biomass, geothermal deposits, landfill gas and trash combustion.– The Energy Act extends the Section 45 production tax credit

for additional two years,– Allowing qualified facilities placed in service through

December 31, 2008.

Section 46 Investment Tax Credits

• The Energy Act adds the following investment tax credits to code Section 46:– 30% credit for solar energy property– 20% credit for integrated gasification combined

cycle projects,– 15% credit for other advanced coal-based

technologies,– 20% credit for certified gasification projects,– 30% credit for qualified fuel cell power plants, and– 10% credit for qualified stationery micro turbine

power plants.

27

• Income Recognition Issues• IRS Section 467

28

Rental Income - Section 467

• Rental income should be approximately levelover the term of the lease.

• Some forms of “uneven rent” are acceptable– Rents that vary:

• Due to third party costs• With an index• With asset use• Vary by a small amount

29

Rental Income - Section 467 (con’t)

• Rents that vary due to third party costs– Property taxes– Utility costs– Insurance costs– Maintenance costs

30

Rental Income - Section 467 (con’t)

• Rents that vary with an index – Consumers Price Index– Producers Price Index– Regional Price Index– Commodity Index (fuel or food prices)– Financial Index

31

Rental Income - Section 467 (con’t)

• Rents that vary with asset use or results– Variation with output of a leased equipment– Mileage on a vehicle– With sales (retail store)– Variation with profitability (retail store)

32

Rental Income - Section 467 (con’t)

• Rents that vary by a small amount• The “90-110 Test”

– 10% variation is allowed

– Determine the average annual rental rate

– Lowest annual rental must be at or above 90% ofthe Average

– Highest annual rental must be at or below 110% of the average rent

– Real Estate allows 15% variation (“85-115 Test”)

33

Rental Income - Section 467 (con’t)

• Rent variation beyond allowable– IRS may determine that the agreement is a

“Disqualified Agreement”

– If a “Disqualified Agreement,” The IRS may recalculate the rental income pattern (“Levelize”)

– If the agreement is a Disqualified Agreement, the entire agreement will be levelized.

Example of SITL - Assumptions

Asset: Corporate JetAsset Cost: $10,000,000.00Lease type: Single Investor Lease Term: 120 months or 10 yearsDelivery Date: 12/15/06Lease inception: 12/15/06Early Buy-out Option: (84 months from Lease inception)Depreciation: 5 year MACRS Depreciation

Half year ConventionLessor Tax Rate: 35%Rents: Monthly in arrearsTotal Residual: 50% or $5,000,000.00Fees Paid: .5% or $ 50,000.00 (Portion for ResidualGuarantee) Target yield: 6.5% pre-tax Multiple Investment Sinking FundLessee’s Incremental Borrowing Rate: 6.0% Lessee’s comparable debt cost

Example of 467 Rent - Results

Lessor can structure various rent patterns within the Sec. 467 guidelines to minimize Lessee’s cost by increasing the value of tax benefits.

Level Payments 90/110 ____ _

Rental Payment: $72,818.95 (1to 120) $66,232.47(1 to 60)

$80,951.12 (61 to 120)EBO amount: (mo. 84) $6,831,083 $7,206,012If EBO Exercised:PV of Rent + EBO 95.02% 94.54%Implicit Cost : 4.98% 4.92%

If Lease goes to end of term and returns the aircraft to Lessor:PV of min. lease payments 65.92% 65.30%IRR -2.65% -2.31%

Example of Lessor’s Tax Position•Lessor Accounting :

Monthly Payment: $ 72,818.95Implicit Rate: 4.88%PV of rents only : 69.29%

•Lessor’s Classification: Operating Lease

•To re-classify as Direct Finance Lease:•Lessor will require 3rd party residual Guarantee: $3,371,537.25•PV of Minimum payments: 90.1%

•Impact on PT Yield and Lessor’s tax position and asset acquisition patternHalf Year Mid Quarter AMTConvention Convention 2005 to 2010

•Pre-tax Yield 6.50% 6.36% 4.88%•Impact to Lessor 0% .14% 1.62%

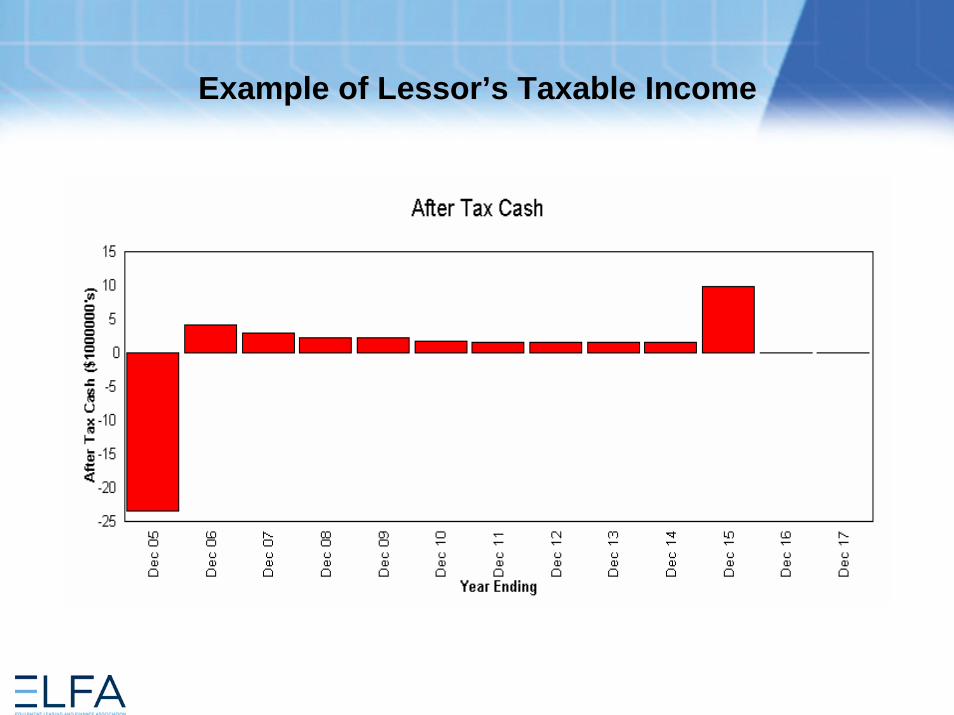

Example of Lessor’s Taxable Income

Difference Between Accounting and Tax

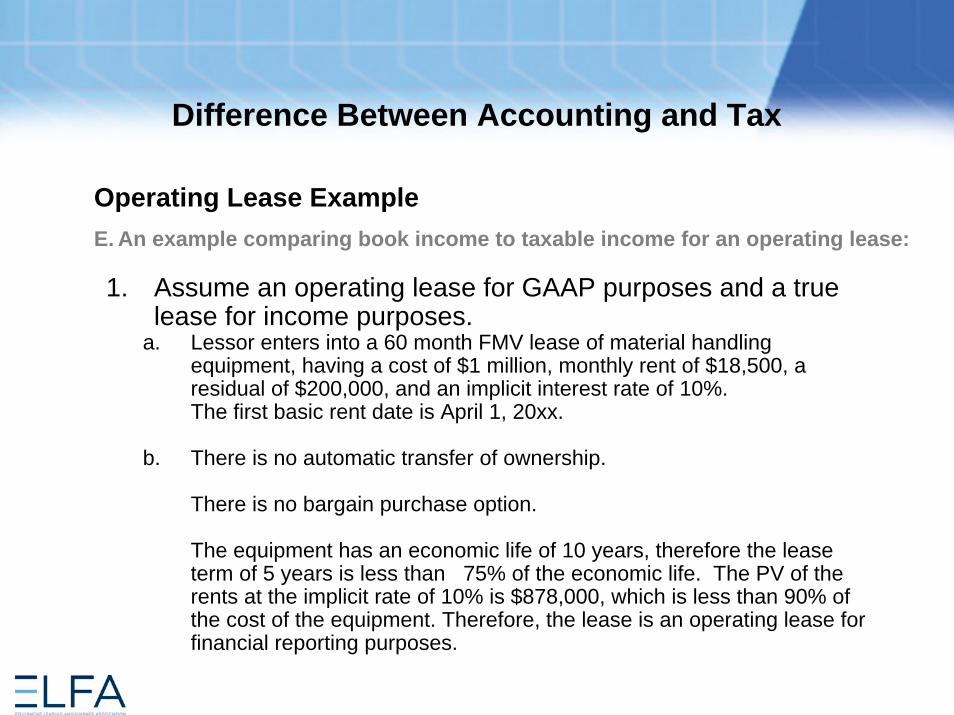

Operating Lease ExampleE. An example comparing book income to taxable income for an operating lease:

1. Assume an operating lease for GAAP purposes and a true lease for income purposes.

a. Lessor enters into a 60 month FMV lease of material handling equipment, having a cost of $1 million, monthly rent of $18,500, a residual of $200,000, and an implicit interest rate of 10%.The first basic rent date is April 1, 20xx.

b. There is no automatic transfer of ownership.

There is no bargain purchase option.

The equipment has an economic life of 10 years, therefore the lease term of 5 years is less than 75% of the economic life. The PV of the rents at the implicit rate of 10% is $878,000, which is less than 90% of the cost of the equipment. Therefore, the lease is an operating lease for financial reporting purposes.

Difference Between Accounting and Tax

Operating Lease Example (cont’d)E. An example comparing book income to taxable income for an operating lease:

2. Material handling equipment (generally) is five-year class property. MACRS depreciation rates (from the IRS table) are:

• Year %__ • 1st 20.00• 2nd 32.00• 3rd 19.20• 4th 11.52• 5th 11.52• 6th 5.76

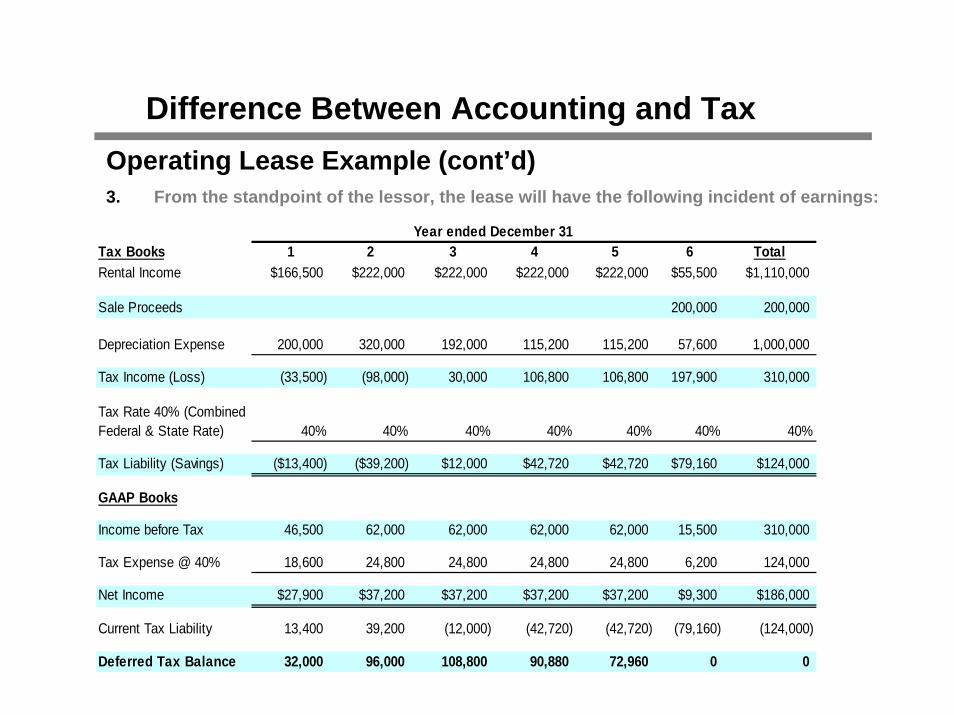

Difference Between Accounting and TaxOperating Lease Example (cont’d)3. From the standpoint of the lessor, the lease will have the following incident of earnings:

Year ended December 31Tax Books 1 2 3 4 5 6 TotalRental Income $166,500 $222,000 $222,000 $222,000 $222,000 $55,500 $1,110,000

Sale Proceeds 200,000 200,000

Depreciation Expense 200,000 320,000 192,000 115,200 115,200 57,600 1,000,000

Tax Income (Loss) (33,500) (98,000) 30,000 106,800 106,800 197,900 310,000

Tax Rate 40% (CombinedFederal & State Rate) 40% 40% 40% 40% 40% 40% 40%

Tax Liability (Savings) ($13,400) ($39,200) $12,000 $42,720 $42,720 $79,160 $124,000

GAAP Books

Income before Tax 46,500 62,000 62,000 62,000 62,000 15,500 310,000

Tax Expense @ 40% 18,600 24,800 24,800 24,800 24,800 6,200 124,000

Net Income $27,900 $37,200 $37,200 $37,200 $37,200 $9,300 $186,000

Current Tax Liability 13,400 39,200 (12,000) (42,720) (42,720) (79,160) (124,000)

Deferred Tax Balance 32,000 96,000 108,800 90,880 72,960 0 0

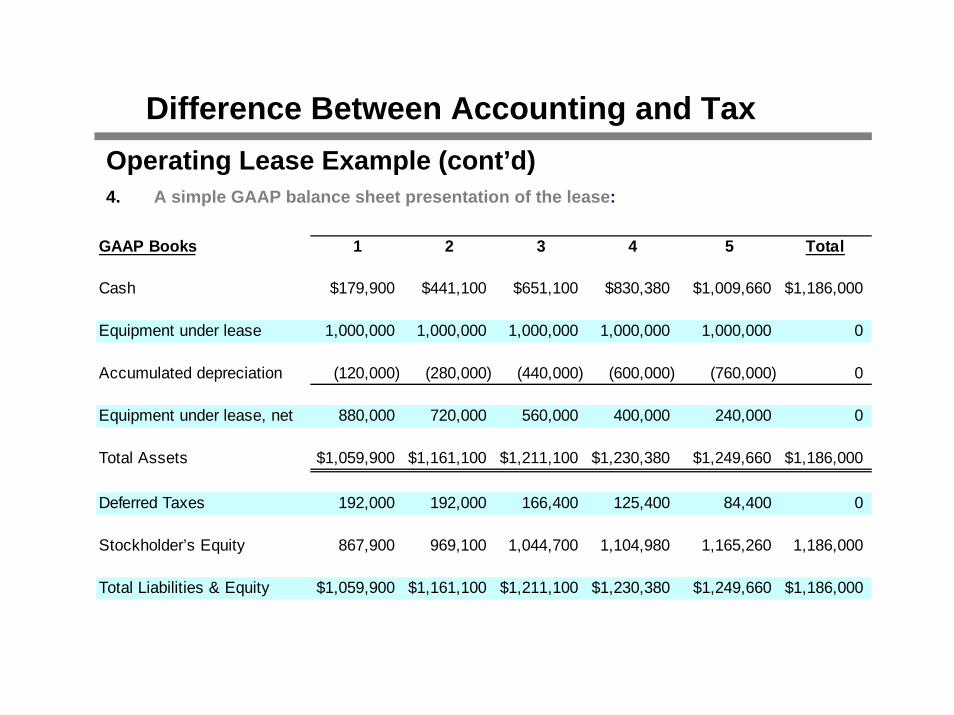

Difference Between Accounting and TaxOperating Lease Example (cont’d)4. A simple GAAP balance sheet presentation of the lease:

GAAP Books 1 2 3 4 5 Total

Cash $179,900 $441,100 $651,100 $830,380 $1,009,660 $1,186,000

Equipment under lease 1,000,000 1,000,000 1,000,000 1,000,000 1,000,000 0

Accumulated depreciation (120,000) (280,000) (440,000) (600,000) (760,000) 0

Equipment under lease, net 880,000 720,000 560,000 400,000 240,000 0

Total Assets $1,059,900 $1,161,100 $1,211,100 $1,230,380 $1,249,660 $1,186,000

Deferred Taxes 192,000 192,000 166,400 125,400 84,400 0

Stockholder’s Equity 867,900 969,100 1,044,700 1,104,980 1,165,260 1,186,000

Total Liabilities & Equity $1,059,900 $1,161,100 $1,211,100 $1,230,380 $1,249,660 $1,186,000

Difference Between Accounting and TaxDirect Finance Lease ExampleFrom the standpoint of the lessor, the direct finance lease will have the followingincident of earnings:

Taxable Income (Loss) (439,301) 81,049 145,049 183,549 183,549 151,350 305,244Tax Rate 40% (CombinedFederal & State rate) 40% 40% 40% 40% 40% 40% 40%Current Tax Liability (Savings) (175,720) 32,420 58,020 73,420 73,420 60,540 122,098GAAP Books

Income before Tax 73,253 84,247 67,398 48,738 28,074 3,534 305,244

Tax Expense @ 40% 29,301 33,699 26,959 19,495 11,230 1,414 122,098

Net Income $43,952 $50,548 $40,439 $29,243 $16,844 $2,121 $183,147

Current Tax Liability 175,720 (32,420) (58,020) (73,420) (73,420) (60,540) (122,098)

Deferred Tax Balance 205,021 206,301 175,240 121,316 59,126 0 0

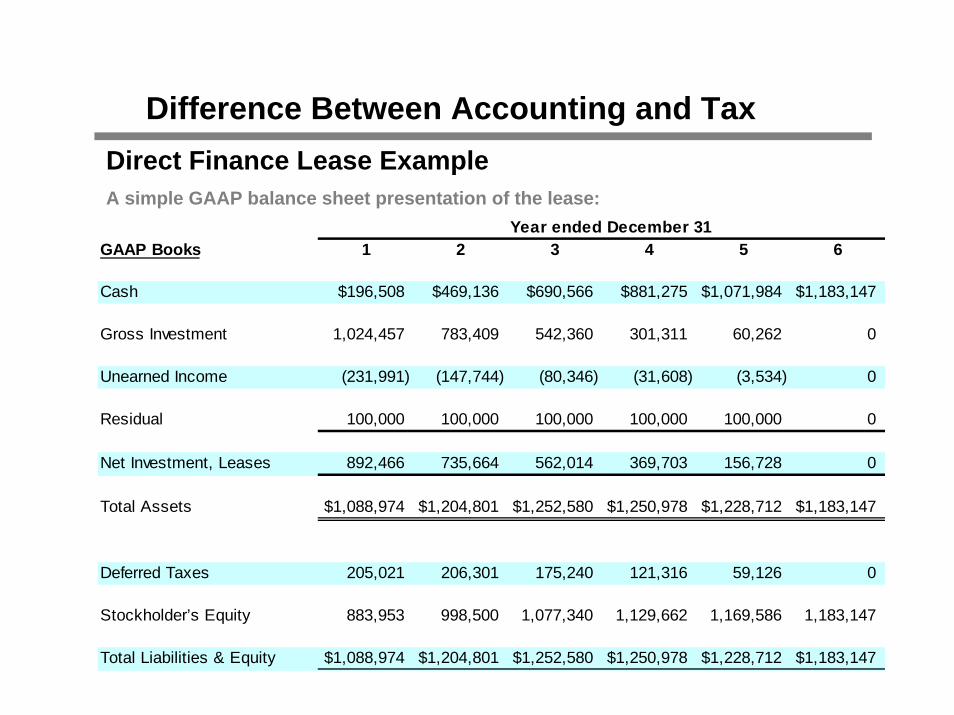

Difference Between Accounting and TaxDirect Finance Lease ExampleA simple GAAP balance sheet presentation of the lease:

Year ended December 31GAAP Books 1 2 3 4 5 6

Cash $196,508 $469,136 $690,566 $881,275 $1,071,984 $1,183,147

Gross Investment 1,024,457 783,409 542,360 301,311 60,262 0

Unearned Income (231,991) (147,744) (80,346) (31,608) (3,534) 0

Residual 100,000 100,000 100,000 100,000 100,000 0

Net Investment, Leases 892,466 735,664 562,014 369,703 156,728 0

Total Assets $1,088,974 $1,204,801 $1,252,580 $1,250,978 $1,228,712 $1,183,147

Deferred Taxes 205,021 206,301 175,240 121,316 59,126 0

Stockholder’s Equity 883,953 998,500 1,077,340 1,129,662 1,169,586 1,183,147

Total Liabilities & Equity $1,088,974 $1,204,801 $1,252,580 $1,250,978 $1,228,712 $1,183,147

62081 44

Q & A