2004 MPS Group Annual Report

60

2004 Annual Report

-

Upload

mark-stevens -

Category

Documents

-

view

53 -

download

1

Transcript of 2004 MPS Group Annual Report

2004 Annual Report

Our Business

MPS Group, Inc. is a leading provider of staffing,

consulting, and solutions in the disciplines of

information technology, accounting and finance, law,

engineering, and health care. MPS Group delivers its

services to government entities and businesses in

virtually every industry throughout the United States,

Canada, the United Kingdom, and Europe.

MPS Group is a Fortune 1000 company traded on

the New York Stock Exchange (NYSE:MPS).

Table of Contents

Financial Highlights 1

Letter to Shareholders 2

Breakdown of Revenue 7

Professional Services Division 8

Information Technology Services Division 10

Board of Directors and Corporate Officers 12

Discussion of the Company 13

Selected Financial Data 20

Management’s Discussion and Analysis ofFinancial Condition and Results of Operations 21

Quantitative and Qualitative DisclosuresAbout Market Risk 30

Report of Independent Registered CertifiedPublic Accounting Firm 31

Management’s Report on Internal Controlover Financial Reporting 33

Financial Statements 34

Notes to Consolidated Financial Statements 39

Reconciliation of Non-GAAP FinancialMeasure to GAAP Financial Measure 55

Common Stock Data and Other Information 56

1MPS Group

2004 Financial Highlights(dollar amounts in thousands except per share amounts)

Year 2004 2003

Revenue $ 1,426,842 $ 1,096,030Cost of revenue 1,066,055 808,890Gross profit 360,787 287,140Operating expenses 308,654 251,339Operating income $ 52,133 $ 35,801Income from continuing operations $ 35,420 $ 21,835Diluted income per common share from continuing operations (EPS) $ 0.33 $ 0.21

Revenue(in billions)

EPSEBITDA(in millions)

EBITDA is a non-GAAP financial measure representing earnings before interest, taxes, depreciation, and amortization. See page 55 for aschedule reconciling EBITDA used above and in the letter to shareholders to the most comparable GAAP financial measure.

To Our Shareholders:

In last year’s letter to shareholders, I wrote of the stepswe had taken to strengthen and diversify our business,and of the progress we were making. I also wrote aboutour expectations for an improved economy and a betteremployment environment in 2004. I am pleased to reportthat these two factors, and the efforts of our exceptionalconsultants, employees, and divisional leadership,combined to make 2004 an extremely successful yearfor MPS Group.

The following is a discussion of our accomplishmentsin 2004 and our plans and goals for the years ahead.

2004 Year In Review

As 2004 began, we saw immediate improvements inclient demand for our services as well as indications thatthe economy was improving. In order to take advantageof this upturn, we made investments in people and inour business units that were designed to help us maxi-mize our performance during this economic recovery.

Due in part to these investments, 2004 was a strongyear for top-line growth as we added new clientrelationships and increased market share within ourexisting client base. Overall, our revenue grew 30%versus 2003, to $1.427 billion. Revenue for ourProfessional Services Division, which provides staffingand recruiting services in the disciplines of accountingand finance, law, engineering, and health care,increased 40% from 2003. We also were encouraged bythe performance of our Information Technology (IT)Division, which increased revenue 22% versus 2003, agood indication that corporate technology spending isimproving after several years of soft demand. In bothour professional and technology businesses, we werepleased to see revenue grow sequentially for each quarterof 2004, confirming our belief that a general economicrecovery and an improvement in hiring were underway.

We also were pleased with our growth in earnings in2004. Diluted net income per common share fromcontinuing operations rose 57% in 2004, to $0.33from $0.21 in 2003. EBITDA grew from $53 millionin 2003, to $67 million in 2004, an increase of 27%.We believe our earnings might have increased even

2 MPS Group

Timothy D. Payne, President and Chief Executive Officer

The steps we have taken to

strengthen and diversify our

business, plus an improved

economy, combined to make

2004 an extremely successful

year for MPS Group.

3MPS Group

more in 2004 had it not been for the investments wemade in our business. However, we also believe thatthese investments have better positioned us to competeeffectively and maximize our performance for 2005and beyond.

Along with this growth in revenue and earnings in 2004,we also saw continuing improvement in the Company’soverall financial position. For the year, we generatedmore than $50 million in cash flow from operations.As we noted in last year’s letter to shareholders, weexpected to use our cash reserves to buy back Companystock, as appropriate, and complete strategic acquisitionsin the accounting, legal, and health care staffingmarkets. During 2004, we invested $50 million instrategic acquisitions and $31 million to buy back theCompany’s stock. After considering these investments,we closed the year with $106 million in cash reservesand no outstanding borrowings on our $150 millioncredit facility. We believe the Company is financiallystrong and well positioned to execute our strategy andcontinue our growth.

Finally, like all public companies, in 2004 we werefaced with new reporting and disclosure requirementsdriven by Section 404 of the Sarbanes-Oxley Act.Complying with this new regulation was costly and

required us to commit the time and energy of many ofour talented people. We are pleased to note that ourauditor’s report was favorable and that we identifiedno material weaknesses. Now that we have completedour first year under the new regulations, the burden ofcompliance will decrease, and we have strengthenedour internal audit function to make sure we meet ourfuture obligations.

Overall, we were pleased with our performance in 2004and with the progress we continue to make as a company.

Business Unit Performance

Beginning with the fourth quarter of 2004, wemodified our financial reporting segments in order tobetter align our reporting segments with the mannerin which we manage the Company. In doing so, wecreated two divisions: the Professional ServicesDivision and the Information Technology Division.Within these divisions, we further broke out ourbusiness into a North American segment and aEuropean (primarily United Kingdom) segment.

MPS Group provides highly specialized staffing andrecruitment services, and this is reflected in both ourbrand strategy and operating model. Each business unit

MPS Group’s 2004 Highlights

• Grew revenue by 30% to $1.427 billion and net income from continuing operations by 62% to $35.4 million

• Generated more than $50 million in cash flow from operations

• Invested in organic growth initiatives in all our business units

• Purchased seven leading professional staffing companies bringing us closer to our goal of growing Professional Services to 60% of our revenue

• Spent $31 million to buy back the Company’s stock

• Ended 2004 with over $106 million in cash and no borrowing on our $150 million credit facility

• Named best performing stock price in the staffing industry by Staffing Industry Report, January 14, 2005

goes to market under a brand name that is specific toits specialty and designed to attract both clients andpotential candidates. Likewise, each business unit’smanagement team is composed of individuals with a highdegree of experience and expertise in their specializeddiscipline. For example, our legal staffing business unitis Special Counsel, and its offices are generally led byindividuals who are attorneys or paralegals.

What follows is a breakout of the 2004 performancesof our key business units in both our ProfessionalServices and IT divisions:

Professional Services Division

In last year’s letter to shareholders, I wrote of our goalto create greater diversity in our business by increasingthe percentage of our revenuederived from our ProfessionalServices Division. The primaryreasons for doing this are tolessen the Company’s suscep-tibility to cyclical changes incorporate technology spending,to take advantage of therelatively greater shortagesof skilled professionals indisciplines such as accountingand health care, and tocapitalize on the greaterdemand for permanentemployee recruiting fees that exists in the professionaldisciplines. While we anticipate growth in both our ITand Professional divisions, we expect a faster growthrate from our Professional Services Division.

I am pleased to report real progress toward achievingour goal of creating greater diversity in our business.In 2000, 36% of our revenue was generated by ourProfessional Services Division and the remainder wasproduced by our IT Division. For the fourth quarterof 2004, revenue from our Professional ServicesDivision had grown to 51% of total revenue. By theend of 2006, we expect Professional Services revenueto rise to more than 60% of total Company revenue.

Special Counsel is North America’s largest providerof legal staffing and recruitment solutions, with morethan $100 million in 2004 revenue. This businessunit’s revenue grew 34% in 2004 versus 2003. In 2004,Special Counsel continued to broaden its array ofsolutions by adding new services such as depositiondigesting, law firm merger and partner placement,medical document review, and court reporting. Overalldemand for Special Counsel’s services is expected tocontinue to grow as leading law firms and corporatelegal departments increasingly embrace the concept ofutilizing contingent legal professionals. Special Counselshould benefit from anticipated increases in corporatemerger and acquisition activity.

Badenoch & Clark is quickly emerging as a leadingprovider of finance and accounting and professional

staffing services in the UnitedKingdom. Badenoch & Clark’srevenue rose 46% in 2004, to£157 million (US $289 million).During the year, this businessunit made substantial invest-ments by increasing itsgeographic footprint to 18offices, hiring a substantialnumber of revenue-generatingemployees, and adding a rangeof new service offerings. Theseinvestments are expected topay off in 2005 in the form

of continued growth and improved profitability.Badenoch & Clark was also recently honored for thesecond straight year by The Sunday Times as number 11on its list of “100 Best Companies To Work For” inthe United Kingdom — up from number 17 last year.

Entegee has produced consistently strong performancefor over ten years in the highly competitive engineeringstaffing market. In 2004, Entegee’s revenue grew 19%to over $200 million, driven by good execution andstronger demand from the defense and aerospaceindustries. Demand from the manufacturing sectorimproved slightly in 2004, and further strengtheningis anticipated in 2005.

4 MPS Group

“We believe the Company is financially strong andwell positioned to executeour strategy and continueour growth…we believe

our people are up tothe challenge.”

Accounting Principals made great strides during 2004,with strong organic growth as well as activity on theacquisition front. It has long been our strategic objectiveto boost our presence in the North American accountingand finance staffing market in order to take advantageof strong demand and a relatively short supply ofaccounting professionals. Accounting Principals greworganically by 26% in 2004. Combining this growthwith acquisitions, including the recent acquisition ofAccounting Solutions, a leading privately held financialstaffing company, Accounting Principals grew 88% in2004 and is now expected to generate over $100 millionin revenue in 2005. Accounting Principals enters 2005with the size and geographic footprint to be a fiercecompetitor able to gain market share from theindustry leader.

Soliant Health is our relatively new business unit thatspecializes in recruiting and placing health care pro-fessionals such as therapists, nurses, and techniciansthroughout the United States. Most of Soliant’shealth care professionals work on 13-week travelassignments. Due to a shortage of health care workersand an aging population, the overall health care staffingmarket is expected to grow for many years to come.For 2005, Soliant is projected to generate revenue ofover $70 million.

Information Technology Division

MPS Group’s IT Division offers IT staffing andrecruitment services, IT solutions, and workforceoptimization solutions. To the surprise of manyindustry analysts, our IT Division grew by over 20%in 2004. We attribute this to good execution by ourIT business units and an improved demand for ITservices. It is anticipated that demand for IT serviceswill continue to improve in 2005.

Modis is the largest business unit of MPS Group andone of the largest IT staffing companies in NorthAmerica, providing staffing and recruitment of bothcontingent and permanent IT professionals. Modisdelivers its services to Fortune 1000 companies,middle-market clients, and government entities. In 2004,Modis revenue grew 17%. We believe this growth is

the result of the quality of services provided by Modisas well as a fundamental change in client buyingpatterns over the past several years. In years past,buyers of IT services were willing to do business withmany small providers, making the market quitefragmented. Today, buyers want to do business withfewer providers and demand that those providers havethe size, scale, and financial stability to service theirIT needs across multiple physical locations. With$388 million in annual revenue in 2004 and 43 officesin North America, Modis has a high win rate whenbuyers select their providers.

Modis International is a leading provider of IT staffingacross the United Kingdom and continental Europe.The IT staffing marketplace in the United Kingdomdiffers from the market in North America in severalkey respects. From a financial standpoint, the resultsof these differences are lower gross margins and loweroperating margins across the entire United KingdomIT staffing industry. In this challenging environment,Modis International has a consistent track record ofprofitability with gross margins that are among thehighest in its peer group. In 2004, Modis Internationalrevenue grew 38%, rising to over £135 million (US$249 million) for the year. For 2005, we anticipatethat Modis International should grow at a slower rateversus 2004, but that we should see improvement ingross margin and operating margin trends.

Idea Integration provides IT solutions to clientsthroughout the United States. The IT solutions modeldiffers from the IT staffing model in two key respects.First, services typically are delivered to clients via salaried“bench” consultants. Second, IT solutions providerstypically tackle entire projects and accept responsibilityfor each project’s outcome. IT solutions providers his-torically have thrived during times of rapid technologicalchanges, such as the advent of ERP systems and theInternet boom. Because no such rapid technologicalchange is under way at present, Idea Integration has notreacted to the economic recovery as quickly as the restof our business units. The business unit did grow by 2%in 2004 and turned a slight profit for the year. As theeconomic recovery becomes more robust, we anticipategreater growth and improved profitability from Idea.

5MPS Group

Beeline is perhaps the most unique of our businessunits in that it does not provide staffing, recruitment,or consulting services. Beeline is an application serviceprovider (ASP) that designs and develops software forclients to use to optimize the deployment of theirworkforce. While the Beeline software attends to abroad range of client needs, at its heart is a powerfulapplication that automates the procurement andmanagement of contingent labor. Beeline customersuse this tool to streamline their processes and savemillions of dollars per year in contingent labor costs.Beeline’s revenue grew rapidly in 2004, and weanticipate further rapid growth in 2005, as well assolid profitability.

Our Goals

The overarching long-term goal that drives ourcompany is our desire to be the leading operatingcompany in our industry. To achieve this, we must finda way to consistently outperform our peers in clientservice, growth, and financial performance. The meansto achieving this goal will be to continually attract andretain the industry’s best people by providing a greathome and the opportunity for a great career with us.

With this said, we have a number of shorter-termgoals that drive our company as well. For 2005, ourgoal is to leverage the investments we have made inrecent years and achieve another strong year ofincreased revenue and profits. The path to meeting thisgoal is to grow our business without adding significantnew costs and to derive more of our revenue fromhighly profitable permanent placement fees. From2003 to 2004, revenue from permanent placement feesrose 60%, to approximately 3.3% of total revenue; wehope to see similar growth in 2005.

For 2006, we are focused on several goals as well. Wewould like to more than double the revenue contributionfrom our permanent placement fees. Achieving thiswould have a significant positive impact on our operatingmargins. A second goal for 2006 is to generate at least$2 billion in revenue. Our third goal, as previouslymentioned, is to continue to diversify our business andderive over 60% of our business from our professionalservices business units by 2006. All of these goals willbe tough to accomplish, but we believe our people areup to the challenge.

And perhaps most importantly, our goal is to drivevalue for our shareholders. The clear route to creatingshareholder value, in our view, is our determinationto consistently achieve operational excellence.

Thank you, our shareholders, for the trust and supportyou have placed in us by investing in MPS Group.

Sincerely,

Timothy D. Payne

President and Chief Executive Officer

April 15, 2005

6 MPS Group

8 MPS Group

Professional Services Division

North America

Accounting Principals is a leader in therecruitment and placement of accountingand finance professionals and offers acomplete range of workforce solutionsto the finance, accounting, and bankingindustries.

• In 2004, Accounting Principals acquiredAccounting Solutions, one of thenation’s largest privately held financeand accounting staffing companies.

• Accounting Principals expanded itsexecutive search and permanentplacement services to Atlanta, Dallas,Houston, Ft. Worth, Philadelphia,Nashville, Chicago, San Francisco,Tampa, and Washington, D.C.

• With this rapid growth, AccountingPrincipals is expected to drive morethan $100 million in revenue in 2005.

Special Counsel is the recognized leaderin providing customized legal workforcesolutions to corporate legal departmentsand law firms nationwide. SpecialCounsel provides contract, contract-to-hire, direct hire, and litigation supportservices, such as medical documentreview, deposition digesting, and courtreporting.

• Special Counsel is the largest U.S.-based provider of legal staffingservices, with anticipated 2005revenue of more than $120 million.

• The market for legal staffing servicesis growing as the concept of usingcontingent legal professionals isembraced by law firms and in-houselegal departments.

• Over 90% of the 100 largest lawfirms in the United States are clientsof Special Counsel.

Entegee provides technical and engineer-ing staffing services to manufacturers,defense contractors, and governmententities. Entegee also provides engineeringand drafting design services throughcompany-owned centers that utilizestate-of-the-art computer technology.

• Entegee generated superior resultsin 2004 due to good execution andstrong demand from the defense andaerospace industries.

• Entegee grew revenue by over 19%in 2004 while adding new offices inkey markets.

• Entegee consistently delivered highprofits driven by its efficient nationalservice center model.

Jeffrey B. Jackovich, PresidentJohn L. Marshall III, PresidentRobert L. Cecchini, President

9MPS Group

Soliant Health is a leading provider ofspecialized health care staffing servicesto hospitals and health care providers.By supplying traveling nurses andallied health care professionals on bothtemporary and direct hire assignments,Soliant Health delivers comprehensivehealth care staffing services to leadingmedical facilities across the United States.

• There is a shortage of licensed healthcare professionals in North America,creating strong demand for SoliantHealth’s services.

• Through a combination of organicgrowth and a targeted acquisitionstrategy, Soliant Health grew revenueby over 157% in 2004.

• Soliant launched several new serviceofferings in 2004, including a physiciansearch practice.

Badenoch & Clark specializes in profes-sional services recruitment on a directhire, temporary, and contract basis in theUnited Kingdom. Badenoch & Clark hasdelivered these services to the accounting,financial services, banking, insurance,legal, human resources, and technologymarkets for 22 years.

• Badenoch & Clark ranked 11th on theprestigious 2004 The Sunday Timeslist of “100 Best Companies To WorkFor” in the United Kingdom, up from17th last year.

• Badenoch & Clark opened offices inChelmsford, Essex and Cardiff, Walesin 2004.

• Badenoch & Clark made strategicinvestments to expand its workforcein 2004, resulting in 46% revenuegrowth for the year.

David K. Alexander, President Neil L. Wilson, President & Managing Director

Europe

Information Technology Services Division

North America

10 MPS Group

Modis, Inc. is one of the world’slargest and most respected providersof Information Technology ResourceManagement (ITRM) services andsolutions. Modis delivers world-classITRM solutions to more than 1,000clients in virtually every industryaround the world.

• In 2004, Modis was awarded contractsto provide IT staffing services tohundreds of companies and govern-ment entities, including the U.S.Department of Defense MilitaryHealth System, Emerson Direct, thestate of Ohio, University of TexasMedical Branch, Gwinnett County,Georgia, and the state of Delaware.

• Modis grew revenue by over 17% in2004, indicating improving demandfor IT services among corporate andgovernment clients.

Idea Integration is a technology solu-tions and systems integrator servingFortune 1000 companies, government,and middle-market clients. Idea spe-cializes in Web design and development,information management solutions,wireless workflow applications, andportal solutions.

• Idea Integration was named to the2004 VARBusiness 500, the industry’sdefinitive ranking by revenue of thetop 500 solution providers, IT con-sultants, integrators, and serviceorganizations in North America.

• Idea Integration received the 2004Galaxy Award by The InternationalAcademy of Communications Arts andSciences (IACAS) for its excellence inproduct and service marketing forSony Electronics.

John P. Cullen, President James D. Albert, President

Europe

11MPS Group

Beeline automates and streamlines theprocurement and management of bothcontingent and full-time workforces.This leading technology drives efficien-cies in human capital management,providing discipline and reductions inworkforce costs.

• Beeline grew rapidly in 2004 bywinning new contracts with Fortune1000 companies and by expandingexisting customer relationships.

• Recently, Beeline expanded itstechnology and service offerings byintroducing several new modules aswell as a solution targeted to thehealth care market.

Modis International is one of Europe’slargest and most respected providersof IT staffing services and solutions.Based in the United Kingdom, ModisInternational also does businessthroughout continental Europe.

• Modis International recently openedtwo offices in Europe to meet clientdemands for IT staffing services inStuttgart, Germany and Amsterdam,Holland.

• Modis International was recognizedby the Association of TechnologyStaffing Companies (ATSCo) fordemonstrating professional values inits delivery of IT staffing services.

• Based in the U.K., Modis Internationaldoes business with FTSE 1000 andgovernment entities throughout theU.K. and continental Europe.

Richard L. White, President Paul F. Chapman, President & Managing Director

12 MPS Group

Board of Directors

Derek E. DewanChairman of the Board — MPS Group, Inc.

Michael D. AbneyRetired Chief Financial Officer and

Senior Vice President — MPS Group, Inc.

T. Wayne Davis 1, 2, 3

President and Chairman —Tine W. Davis Family — WD Charities, Inc.

William M. Isaac 1, 2

Chairman — The Secura Group and Secura BurnettFormer Chairman — FDIC

John R. Kennedy 1, 2, 3

Retired President and Chief Executive Officer —Federal Paper Board Company, Inc.

Arthur B. Laffer 2Chairman — Laffer Associates

Darla D. Moore 3Partner and Executive Vice President — Rainwater, Inc.

Timothy D. PaynePresident and Chief Executive Officer —

MPS Group, Inc.

Peter J. Tanous 1, 2

President — Lynx Investment Advisory, Inc.

1 Member of the Corporate Governance and Nominating Committee2 Member of the Audit Committee3 Member of the Compensation Committee

MPS Group Corporate Officers

Timothy D. PaynePresident and Chief Executive Officer

Robert P. CrouchSenior Vice President and Chief Financial Officer

Richard L. WhiteSenior Vice President and Chief Information Officer

Gregory D. HollandSenior Vice President, Chief Legal Officer, and Secretary

Tyra H. TutorSenior Vice President, Corporate Development

Thomas M. BurkeVice President, Human Resources

Thomas M. Burke Tyra H. Tutor Robert P. Crouch Timothy D. Payne Richard L. White Gregory D. Holland

13MPS Group 13

Forward-Looking Statements

This Annual Report to Shareholders contains forward-looking statements that are subject to certain risks,uncertainties or assumptions and may be affected bycertain factors, including but not limited to the specificfactors discussed below, under “Risk Factors,” “Marketfor Registrant’s Common Equity, Related StockholderMatters and Issuer Purchases of Equity Securities,” and“Management’s Discussion and Analysis of FinancialCondition and Results of Operations—Liquidity andCapital Resources.” In some cases, you can identifyforward-looking statements by terminology such as“will,” “may,” “should,” “could,” “expects,” “plans,”“indicates,” “projects,” “anticipates,” “believes,” “estimates,”“appears,” “predicts,” “potential,” “continues,” “can,”“hopes,” “perhaps,” “would,” or “become,” or the negativeof these terms or other comparable terminology. Exceptfor historical facts, all information provided below, under“Quantitative and Qualitative Disclosures About MarketRisk” should also be considered forward-lookingstatements. In addition, statements in the letter toshareholders and discussions of our divisions appearing

earlier in this Annual Report to Shareholders containforward-looking statements, including statementsregarding future financial, business mix, and operationalobjectives for the Company and its business units.Should one or more of these risks, uncertainties or otherfactors materialize, or should underlying assumptionsprove incorrect, actual results, performance or achieve-ments of the Company may vary materially from anyfuture results, performance or achievements expressedor implied by such forward-looking statements.

Forward-looking statements are based on beliefs andassumptions of the Company’s management and oninformation currently available to such management.Forward-looking statements speak only as of the datethey are made, and the Company undertakes noobligation to publicly update any of them in light of newinformation or future events. Undue reliance shouldnot be placed on such forward-looking statements,which are based on current expectations. Forward-looking statements are not guarantees of performance.

Introduction

MPS Group, Inc. (MPS or the Company) is a leadingprovider of business services with over 185 officesthroughout the United States, Canada, the UnitedKingdom, and continental Europe. We deliver specialtystaffing, consulting and business solutions to virtuallyall industries in the following disciplines, through thefollowing primary brands:

Brand(s) DisciplineModis® Information Technology (IT)

ServicesBadenoch & Clark®, Accounting and FinanceAccounting Principals®Entegee® EngineeringSpecial Counsel® LegalIdea Integration® IT SolutionsSoliant Health® Health CareBeeline® Human Capital Automation

Our strategy is to focus on increasing revenue andprofits, through a combination of internal growth andacquisitions, primarily within our core disciplines and,to a lesser extent, expansion into new specialties.Specifically, we aim to maintain a leadership positionin our IT-related disciplines, while growing ourprofessional-related disciplines both organically andthrough acquisitions, which should result in theProfessional Services Division providing a largeroverall percentage contribution to our total revenues.

The key elements to our internal growth strategyinclude:

• increasing penetration of existing markets andcustomer segments,

• expanding current specialties into new andcontiguous geographic markets,

• concentrating on skill areas that value high levelsof service, and

• identifying and adding new practice areas.

While we look to strengthen relationships with ourclients, we are not dependent upon a single customeror a limited number of customers.

Pursuant to our acquisition strategy, we acquired tenbusinesses from 2002 to 2004: four legal staffingbusinesses acquired in February of 2003, August of2003, August of 2004, and October of 2004; threehealth care staffing businesses acquired in June of2002, February of 2004, and March of 2004; and threeaccounting staffing businesses acquired in February of2004, July of 2004, and October 2004. The businessesacquired in 2004, 2003, and 2002, had a combinedrevenue of $95 million, $22 million, and $18 millionat acquisition date, respectively.

In addition, we look to focus our efforts intensely onour core businesses. Toward this end, we have divestedcertain businesses we deemed not central to our

strategy, including the 2003 sale of our outplacementunit and the 2004 sale of our retained executive searchunit. We feel we are able to execute and profit from ourinternal growth and acquisition strategies due to ourstrong management team, our integrated and scalableback office support services, and to the continueddevelopment of our strategic management systems.

In all of our markets and disciplines, we encounteraggressive and capable competition, with a number offirms offering services similar to ours on a national,regional or local basis. Our ability to competesuccessfully depends on our reputation, pricing andquality of service provided, our understanding ofclients’ specific job requirements, and our ability toprovide qualified personnel in a timely manner.

The Company was incorporated under the laws of theState of Florida in 1992 under the name AccustaffIncorporated, and changed its name to MPS Group, Inc.in 2002. Our principal executive offices are located inJacksonville, Florida. Strategically, our operations arecoordinated primarily from facilities in Jacksonville,Florida, and London, United Kingdom, and to alesser extent, Burlington, Massachusetts. Both of ourJacksonville and London facilities provide support andcentralized services to our offices in the administrative,marketing, public relations, accounting, training andlegal areas. Regional and local office managers are

responsible for most activities of their offices, includingsales, local and regional marketing and recruitment.

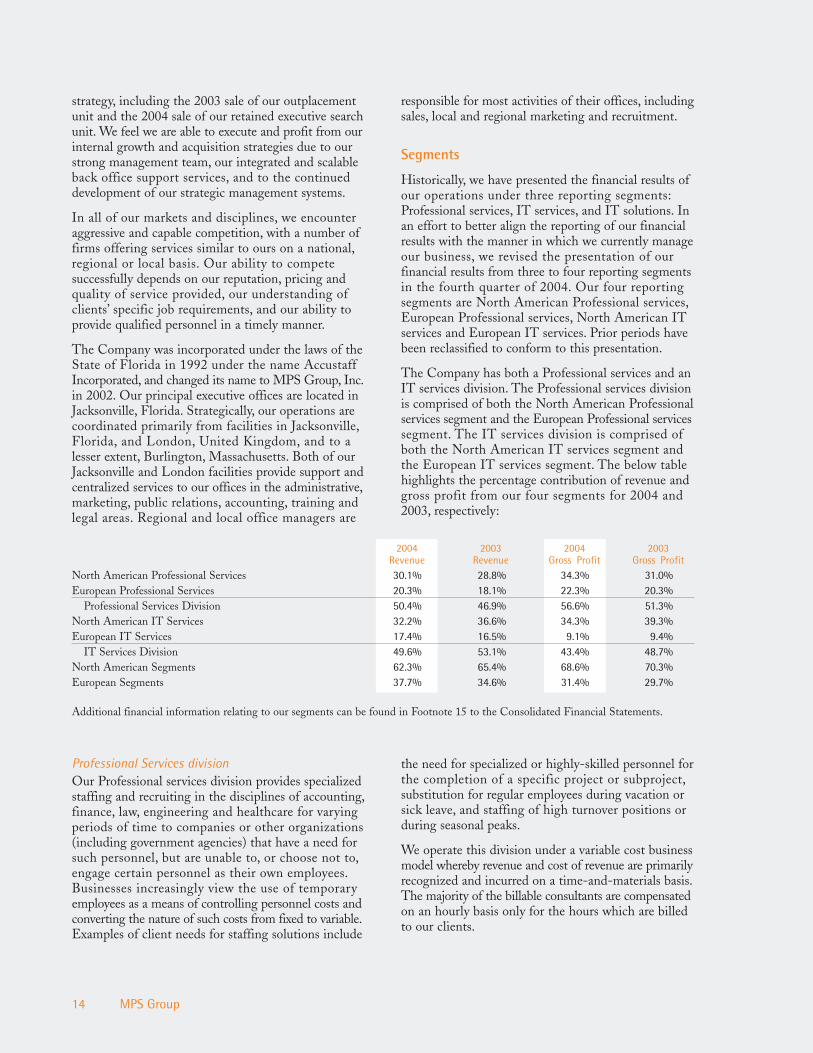

Segments

Historically, we have presented the financial results ofour operations under three reporting segments:Professional services, IT services, and IT solutions. Inan effort to better align the reporting of our financialresults with the manner in which we currently manageour business, we revised the presentation of ourfinancial results from three to four reporting segmentsin the fourth quarter of 2004. Our four reportingsegments are North American Professional services,European Professional services, North American ITservices and European IT services. Prior periods havebeen reclassified to conform to this presentation.

The Company has both a Professional services and anIT services division. The Professional services divisionis comprised of both the North American Professionalservices segment and the European Professional servicessegment. The IT services division is comprised ofboth the North American IT services segment andthe European IT services segment. The below tablehighlights the percentage contribution of revenue andgross profit from our four segments for 2004 and2003, respectively:

14 MPS Group

Professional Services division Our Professional services division provides specializedstaffing and recruiting in the disciplines of accounting,finance, law, engineering and healthcare for varyingperiods of time to companies or other organizations(including government agencies) that have a need forsuch personnel, but are unable to, or choose not to,engage certain personnel as their own employees.Businesses increasingly view the use of temporaryemployees as a means of controlling personnel costs andconverting the nature of such costs from fixed to variable.Examples of client needs for staffing solutions include

the need for specialized or highly-skilled personnel forthe completion of a specific project or subproject,substitution for regular employees during vacation orsick leave, and staffing of high turnover positions orduring seasonal peaks.

We operate this division under a variable cost businessmodel whereby revenue and cost of revenue are primarilyrecognized and incurred on a time-and-materials basis.The majority of the billable consultants are compensatedon an hourly basis only for the hours which are billedto our clients.

2004 2003 2004 2003Revenue Revenue Gross Profit Gross Profit

North American Professional Services 30.1% 28.8% 34.3% 31.0%European Professional Services 20.3% 18.1% 22.3% 20.3%

Professional Services Division 50.4% 46.9% 56.6% 51.3%North American IT Services 32.2% 36.6% 34.3% 39.3%European IT Services 17.4% 16.5% 9.1% 9.4%

IT Services Division 49.6% 53.1% 43.4% 48.7%North American Segments 62.3% 65.4% 68.6% 70.3%European Segments 37.7% 34.6% 31.4% 29.7%

Additional financial information relating to our segments can be found in Footnote 15 to the Consolidated Financial Statements.

Clients also hire our skilled consultants on a permanentbasis, whether it is from a conversion of a temporaryassignment to, or a direct placement of, a full-timeposition. We earn a one-time fee for these services.These fees represent approximately 6% of thisdivision’s revenue.

The principal national and international competitors ofour Professional services division include Robert HalfInternational Inc., Resources Connection, Inc.,Spherion Corporation, Wallace Law Registry, AjilonConsulting (a wholly owned subsidiary of Adecco SA),Michael Page International, Robert Walters PLC,Hays PLC, Cross Country Healthcare, Inc., and CDICorporation.

North American Professional Services segment Our North American Professional Services segmentgoes to market under the primary brands and operatingunits Entegee, Special Counsel, Accounting Principals,and Soliant Health. The demands of our clients (theneed for confidentiality, accuracy and reliability, cost-effectiveness, and frequent peak workload periods) aresimilar among the brands/operating units within thissegment.

Entegee Our Entegee brand/operating unit providesstrategic workforce solutions for technical andengineering needs. From on-site managementconsulting and in-house project services to temporaryand direct placement, Entegee combines industryknowledge and experience to fill highly skilledtechnical and engineering positions. These positionsinclude, but are not limited to, engineers, designers,drafters, inspectors and assemblers. Entegee operatesthrough a domestic network of national practicebranches with offices in 10 markets, and employsapproximately 2,400 billable consultants. Entegeealso provides engineering and drafting design servicesthrough company-owned centers, in Iowa andMinnesota, that utilize state-of-the-art computertechnology. Certain of its client base includesgovernment and defense contractors, manufacturingand engineering companies.

Special Counsel Our Special Counsel brand/operating unit specializes in placing temporary andfull-time employees in attorney, paralegal, legaladministrative and legal secretarial positions forworkload management, litigation support, businesstransaction support, pre-litigation and documentmanagement support, as well as medical documentreview, deposition digesting, and other trial-relatedservices. Special Counsel has a network of 34 officeslocated across the United States, and employsapproximately 1,400 billable consultants. Its clientsinclude Fortune 1000 companies and law firms.

In 2004, we expanded Special Counsel’s geographicfootprint with the acquisition of Legal Networks inAugust and expanded its service offering with theacquisition of Alderson Court Reporting, a premierprovider of court reporting, legal videography andlitigation support services, in October. In addition,Alderson is the official court reporter of the UnitedStates Supreme Court.

Accounting Principals Our Accounting Principalsbrand/operating unit specializes in placing temporaryand full-time employees in accounting, finance, andbanking positions. Accounting Principals has anetwork of 47 offices located across the United States,and employs approximately 1,900 billable consultants.

In 2004, we expanded Accounting Principals’geographic footprint with the acquisitions ofAccounting Alternatives in July and AccountingSolutions in October. The Accounting Solutionsacquisition added 17 net new markets across theUnited States. We also expanded AccountingPrincipals’ service offering in 2004 with the acquisitionof Lillian Kloock, a provider of medical billing andmedical collection professionals to leading facilitiesprimarily in the Southeastern United States.

Soliant Health Our Soliant Health brand/operatingunit specializes primarily in placing traveling healthcareprofessionals, in the areas of nursing, physical andoccupational therapy, along with imaging technicians.Soliant Health employs approximately 500 consultants,and its clients include hospitals and healthcareproviders across the United States.

In 2004, we expanded Soliant Health’s geographicfootprint with the acquisitions of Sunbelt StaffingSolutions and Management Search in February andMarch. During the year, we also expanded its serviceoffering to include school therapists and thepermanent placement of physicians.

Dispositions In 2003, we sold certain operating assets and transferredcertain operating liabilities of our then outplacementunit. The decision to sell our outplacement unit was inkeeping with our long-term strategy of focusing onour core businesses. As a result of the sale of ouroutplacement unit and in accordance with GenerallyAccepted Accounting Principles (GAAP), ourConsolidated Financial Statements and Management’sDiscussion and Analysis of Financial Condition andResults of Operations report the results of operationsof this unit as Discontinued Operations for all periodspresented. In June 2004, we sold certain assets andtransferred certain liabilities of our retained executivesearch brand.

15MPS Group

European Professional Services segment Our European Professional services segment is comprisedof our Badenoch & Clark brand/operating unit. Since1980, Badenoch & Clark has been specializing inplacing temporary, full-time, contract and interimrecruitment employees in positions such as accountingand finance, financial services, legal, human resources,marketing, not-for-profit and public-sector. Withthe 2004 opening of offices in Essex and Wales,Badenoch & Clark has 18 offices located across theUnited Kingdom. It also has 1 office in Luxembourg.Badenoch & Clark employs approximately 4,000billable consultants.

IT Services division Our IT services division provides specialty staffing,consulting and business solutions under the brands/operating units Modis, Modis International, IdeaIntegration and Beeline. We utilize the brand Modisin both our North American and European segments;however, the overall business culture distinguishes theoperation of these two segments.

We operate this division primarily under a variable costbusiness model whereby revenue and cost of revenueare primarily recognized and incurred on a time-and-materials basis. The majority of the billable consultantsare compensated on an hourly basis only for the hourswhich are billed to our clients. Less than 1% of thisdivision’s revenue is generated from fees for clientsdirectly hiring our consultants.

The principal national and international competitors ofour IT services division include Keane, Inc., ComputerHorizons Corp., Comsys IT Partners, Inc., CIBER, Inc.,Computer People (a division of Ajilon Group), HaysPLC, Elan, Lorien PLC, and Sapient Corporation.In addition, we may compete against the internalmanagement information services and IT departmentsof clients and potential clients.

North American IT Services segment Modis Our Modis brand/operating unit specializesin the placement of IT contract consultants for ITproject support and staffing, recruitment of full-timepositions, project-based solutions, supplier managementsolutions, and on-site recruiting support in the areasof application development, systems integration, andenterprise application integration. Modis has a networkof 45 offices located across the United States, andemploys approximately 3,700 billable consultants.

Idea Integration Our Idea Integration brand/operating unit formerly comprised the IT Solutionssegment. Idea specializes in Web design anddevelopment, information management solutions,wireless workflow applications, portal solutions, andenterprise resource management. Idea utilizes bothsalaried and hourly consultants to deliver solutionsprimarily under time-and-materials contracts and toa lesser extent under fixed-fee contracts. It operatesin certain markets across the United States and itsclients include Fortune 1000 companies, governmentand middle-market companies.

Beeline Our Beeline brand/operating unit provides asoftware-based human capital management servicessolution that automates the acquisition and manage-ment of both full-time and contingent workers.Beeline operates primarily in the United States andits’ clients are principally Fortune 1000 companies.

Beeline maintains a full-time staff to support itsoperations and seeks to collect a service chargebased upon the usage of this service. Subsequent tothe initial start up costs and time, minimal cost andresources are required for the usage of Beeline’s services.

European IT Services segment Our European IT services segment is comprised ofModis International. Modis International, headquarteredin the United Kingdom, specializes in providing ITcontract consultants throughout the United Kingdomand certain continental European markets. ModisInternational has been in operation for over 30 years.It has 10 offices located across the United Kingdom,and an office each in Belgium, Germany, Poland, andthe Netherlands. It employs approximately 1,900billable consultants.

Employees

MPS employs approximately 16,400 consultants andapproximately 2,500 full-time staff employees.Approximately 250 of the employees work atcorporate headquarters.

As described below, in most jurisdictions, we, as theemployer of the consultants or as otherwise requiredby applicable law, are responsible for employmentadministration. This administration includes collectionof withholding taxes, employer contributions for socialsecurity or its equivalent outside the United States,unemployment tax, maintaining workers’ compensationand fidelity and liability insurance, and other govern-mental requirements imposed on employers. Full-timeemployees are covered by life and disability insuranceand receive health insurance and other benefits.

16 MPS Group

Government Regulations

Outside of the United States and Canada, the staffingservices industry is closely regulated. These regulationsdiffer among countries but generally may regulate: (i) therelationship between us and our temporary employees;(ii) registration, licensing, record keeping, and reportingrequirements; and (iii) types of operations permitted.Regulation within the United States and Canada hasnot materially impacted our operations.

In many countries, including the United States and theUnited Kingdom, staffing services firms are consideredthe legal employers of the temporary consultants whilethe consultant is on assignment with a company client.Therefore, laws regulating the employer/employeerelationship, such as tax withholding or reporting,social security or retirement, anti-discrimination, andworkers’ compensation, govern us. In other countries,staffing services firms, while not the direct legalemployer of the consultant, are still responsible forcollecting taxes and social security deductions andtransmitting such amounts to the taxing authorities.

Intellectual Property

We seek to protect our intellectual property throughcopyright, trade secret and trademark law and throughcontractual non-disclosure restrictions. Our servicesoften involve the development of work and materialsfor specific client engagements, the ownership of whichis frequently assigned to the client. We do at times, andwhen appropriate, negotiate to retain the ownership orcontinued use of development tools or know howcreated or generated by us for a client in the deliveryof our services, which we may then license or use inthe delivery of our services to other clients.

Seasonality

Our quarterly operating results are affected by thenumber of billing days in the quarter and the seasonalityof our customers’ businesses. Demand for our serviceshas historically been lower during the calendar year-end, as a result of holidays, through February of thefollowing year, as our customers approve annualbudgets. Extreme weather conditions may also affectdemand in the early part of the year as certain of ourclients’ facilities are located in geographic areas subjectto closure or reduced hours due to inclement weather.In addition, we experience an increase in our cost ofsales and a corresponding decrease in gross profit andgross margin in the first fiscal quarter of each year, as aresult of certain state and federal employment tax resets.

Access to Company Information

Our common stock is listed on the New York StockExchange (‘NYSE’) under the ticker symbol ‘MPS’.Our Internet address is www.mpsgroup.com. We makeavailable through our Internet website our annual reportson Form 10-K, quarterly reports on Form 10-Q, andcurrent reports on Form 8-K, as soon as reasonablypracticable after filing such material with, or furnishingit to, the Securities and Exchange Commission. Theinformation contained on our website, or on otherwebsites linked to our website, is not part of thisdocument.

Risk Factors

We are subject to various risks and uncertainties thataffect our business. The most important of these risksand uncertainties are as follows:

Demand for our services is affected by the economicclimate in the industries and markets we serve. Thedemand for our services, in particular our staffingservices, is highly dependent upon the state of economyand upon the staffing needs of our clients. Anyvariation in the economic condition or unemploymentlevels of the United States or of any of the foreigncountries in which our brands/operating units dobusiness, or in the economic condition of any regionof any of the foregoing, or in any specific industry,may severely reduce the demand for our services andthereby significantly decrease our revenues and profits.

Our market is highly competitive with low barriersto entry. Our industry is intensely competitive andhighly fragmented, and because it is a service business,the barriers to entry are quite low. There are manycompetitors, and new ones are entering the marketconstantly. In addition, some of these competitorshave greater resources than us. Competition ariseslocally, regionally, nationally, internationally and incertain cases from remote locations, particularly fromoffshore locations such as India.

Certain of our contracts are awarded on the basis ofcompetitive proposals, which can be periodically re-bidby the client. There can be no assurance that existingcontracts will be renewed on satisfactory terms or thatadditional or replacement contracts will be awarded tous. In addition, long-term contracts form a negligibleportion of our revenue. Therefore, there can be noassurance that we will be able to retain clients or marketshare in the future. Nor can there be any assurancethat we will, in light of competitive pressures, be ableto remain profitable or, if profitable, maintain ourcurrent profit margins.

17MPS Group

Our business requires a qualified candidate pool, whichwe may not be able to recruit or maintain. Our staffingservices consist of the placement of individuals seekingemployment in specialized IT and professional positions.Some of these sectors are characterized by a shortageof qualified candidates. There can be no assurance thatsuitable candidates for employment will continue to beavailable or will continue to seek employment throughus. Candidates generally seek temporary or regularpositions through multiple sources, including us andour competitors. Any shortage of qualified candidatescould materially adversely affect us.

Our business depends on key personnel, includingexecutive officers, local managers and field personnel.We are engaged in the services business. As such, oursuccess or failure is highly dependent upon theperformance of our management personnel andemployees, rather than upon technology or upontangible assets (of which we have few). There can beno assurance that we will be able to attract and retainthe personnel that are essential to our success.

We have to comply with existing governmentregulation and are exposed to increased regulation ofthe workplace. Our business is subject to regulation orlicensing in many states and in certain foreigncountries. While we have had no material difficultycomplying with regulations in the past, there can beno assurance that we will be able to continue to obtainall necessary licenses or approvals or that the cost ofcompliance will not prove to be material. Any inabilityto comply with government regulation or licensingrequirements could materially adversely affect us.Additionally, our staffing services entails employingindividuals on a temporary basis and placing suchindividuals in clients’ workplaces. Increased governmentregulation of the workplace or of the employer-employeerelationship could materially adversely affect us.

We are exposed to employment-related claims andcosts and other litigation. Our staffing services entailsemploying individuals on a temporary basis andplacing such individuals in clients’ workplaces. Ourability to control the workplace environment is limited.As the employer of record of our temporary employees,we incur a risk of liability to our temporary employeesfor various workplace events, including claims of physicalinjury, discrimination, harassment, or retroactiveentitlement to employee benefits. We also incur a riskof liability to our clients resulting from allegations oferrors, omissions, misappropriation, or theft of propertyor information by our temporary employees. Wemaintain insurance with respect to many of such claims.While such claims have not historically had a materialadverse effect on us, there can be no assurance that wewill continue to be able to obtain insurance at a cost

that does not have a material adverse effect upon us orthat such claims (whether by reason of us not havinginsurance or by reason of such claims being outsidethe scope of our insurance) will not have a materialadverse effect upon us.

We depend on our reputation to sell our services. Thesuccess of our brands is highly dependent upon theirreputations. The reputations of our staffing businessesin turn depend upon the perceived quality of theprofessionals we employ and staff with our customers—consequently, if our customers are dissatisfied with ouremployees, our brands will be harmed. Any event thatadversely impacts the reputation of a brand couldmaterially affect our results of operations.

The price of our common stock may fluctuatesignificantly. The market price for our common stockcan fluctuate as a result of a variety of factors, includingfactors listed in these “Risk Factors,” many of whichare beyond our control. These factors include actual oranticipated variations in quarterly operating results;announcements of new services by our competitors orus; announcements relating to strategic relationshipsor acquisitions; changes in financial estimates or otherstatements by securities analysts; and other changes ingeneral economic conditions. Because of this, we mayfail to meet or exceed the expectations of our shareholdersor of our securities analysts, and the market price forour common stock could fluctuate as a result.

Properties

Our corporate headquarters, located in Jacksonville,Florida, is on lease through 2012. Our business servicesare conducted through more than 185 offices locatedin the United States, Canada, the United Kingdom,and continental Europe. Almost all of our offices areon lease, with the terms of an average office leasebeing from three to six years.

We believe that our facilities are generally adequatefor our needs and do not anticipate difficulty replacingsuch facilities or locating additional facilities, ifneeded. Additional information on lease commitmentscan be found in Footnote 6 to the ConsolidatedFinancial Statements.

Legal Proceedings

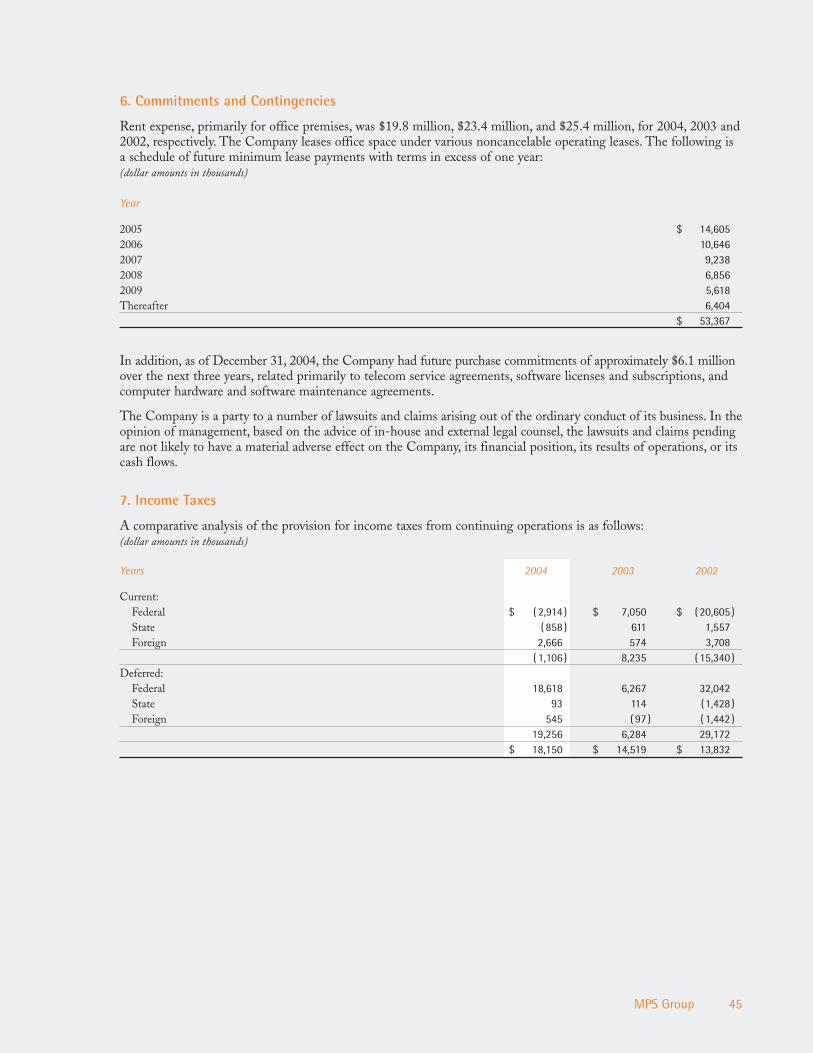

We are a party to a number of lawsuits and claimsarising out of the ordinary conduct of our business. Inthe opinion of management, based on the advice ofin-house and external legal counsel, the lawsuits andclaims pending are not likely to have a material adverseeffect on us, our financial position, our results ofoperations, or our cash flows.

18 MPS Group

Submission of Matters to a Vote of Security Holders

No matters were submitted to a vote of security holders during the fourth quarter of 2004.

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of EquitySecurities

Market Price and Related Matters The following table sets forth the high and low sale prices of our Common Stock, as reported by the NYSE, duringthe two years ended December 31, 2004:

See the factors set forth above in ‘Risk Factors,’ for factors that may impact the price of our Common Stock.As of March 1, 2005, there were approximately 889 holders of record of our Common Stock.

We have not paid to-date a cash dividend or other cash distribution with respect to our Common Stock. Wecurrently intend to retain any earnings to provide for the operation and expansion of our business and do notanticipate paying any cash dividends in the foreseeable future.

Issuer Repurchases of Equity Securities In 1999, our Board of Directors authorized the repurchase of up to $65 million of our Common Stock.Beginning in the third quarter of 2002 through the year-end of 2004, approximately 5.1 million shares at a cost of$39.9 million have been repurchased under this authorization. The following table sets forth information aboutour Common Stock repurchases for the three months ended December 31, 2004. There is no expiration date forthis authorization.

19MPS Group

Maximum Number (orTotal Number of Approximate DollarShares Purchased Value) of Shares That

Total Number Part of Publicly May Yet be Purchasedof Shares Average Price Announced Under the

Period (1) Repurchased Paid per Share Plans or Programs Plans or Programs

October 1, 2004 to October 31, 2004 462,682 $8.67 462,682 $25,058,171November 1, 2004 to November 30, 2004 — — — 25,058,171December 1, 2004 to December 31, 2004 — — — 25,058,171Total 462,682 $8.67 462,682 $25,058,171

(1) Based on trade date, not settlement date.

Year 2004 High LowFirst quarter $ 11.21 $ 9.35

Second quarter 12.12 9.96

Third quarter 11.62 7.87

Fourth quarter 12.38 8.92

Year 2003 High LowFirst quarter $ 6.24 $ 4.75

Second quarter 7.58 5.20

Third quarter 10.10 6.83

Fourth quarter 10.65 8.55

Selected Financial Data(in thousands, except per share amounts)

Years Ended 12-31-2004 12-31-2003 12-31-2002 12-31-2001 12-31-2000

Consolidated Statements of Operations data:Revenue $ 1,426,842 $ 1,096,030 $ 1,119,156 $ 1,500,615 $ 1,777,540Cost of revenue 1,066,055 808,890 834,318 1,105,781 1,269,760Gross profit 360,787 287,140 284,838 394,834 507,780Operating expenses 309,551 251,623 255,929 342,918 388,338Amortization of goodwill (1) — — — 37,312 35,937

Impairment of investment — — 16,165 — ( 694 )Exit costs (recapture) ( 897 ) ( 284 ) 8,967 — —Asset write-down related to sale of

discontinued operations — — — — 13,122Operating income 52,133 35,801 3,777 14,604 71,077Other income (expense), net 1,437 553 ( 3,947 ) ( 9,199 ) ( 21,621 )Income (loss) from continuing operations

before income taxes and cumulative effectof accounting change 53,570 36,354 ( 170 ) 5,405 49,456

Provision (benefit) for income taxes 18,150 14,519 13,832 3,102 ( 65,834 )Income (loss) from continuing

operations before cumulativeeffect of accounting change 35,420 21,835 ( 14,002 ) 2,303 115,290

Discontinued operations: (2)

Income (loss) from discontinued operations, net of tax — ( 2,395 ) 1,410 6,040 4,463

Gain (loss) on sale of discontinued operations, net of tax — ( 20,675 ) — — —

Income (loss) before cumulative effect of accounting change 35,420 ( 1,235 ) ( 12,592 ) 8,343 119,753

Cumulative effect of accounting change,net of tax (1) — — ( 553,712 ) — —

Net income (loss) $ 35,420 $ ( 1,235 ) $ ( 566,304 ) $ 8,343 $ 119,753

Basic income (loss) per common share:From continuing operations $ 0.34 $ 0.21 $ ( 0.14 ) $ 0.02 $ 1.19From discontinued operations $ — $ ( 0.02 ) $ 0.01 $ 0.06 $ 0.05From sale of discontinued operations $ — $ ( 0.20 ) $ — $ — $ —From accounting change $ — $ — $ ( 5.49 ) $ — $ —

Basic income (loss) per common share $ 0.34 $ ( 0.01 ) $ ( 5.62 ) $ 0.09 $ 1.24Diluted income (loss) per common share:

From continuing operations $ 0.33 $ 0.21 $ ( 0.14 ) $ 0.02 $ 1.18From discontinued operations $ — $ ( 0.02 ) $ 0.01 $ 0.06 $ 0.05From sale of discontinued operations $ — $ ( 0.20 ) $ — $ — $ —From accounting change $ — $ — $ ( 5.49 ) $ — $ —

Diluted income (loss) per common share $ 0.33 $ ( 0.01 ) $ ( 5.62 ) $ 0.08 $ 1.23Basic average common shares outstanding 102,804 101,680 100,833 97,868 96,675Diluted average common shares outstanding 106,842 104,518 100,833 98,178 97,539

20 MPS Group

December 31, 2004 2003 2002 2001 2000(in thousands)

Consolidated Balance Sheet data:Working capital $ 232,133 $ 216,879 $ 171,154 $ 200,887 $ 242,872Total assets 954,604 893,151 892,974 1,533,863 1,645,414Long term debt — — — 101,000 194,000Stockholders’ equity(1) 835,663 793,462 781,559 1,310,811 1,303,218

(1) The Company recognized an impairment loss associated with its adoption of Statement of Financial Accounting Standards (SFAS)No. 142 “Goodwill and Other Intangible Assets,” effective January 1, 2002. This loss was recorded as a Cumulative Effect of AccountingChange, and Reduced Stockholders’ Equity. In addition, SFAS No. 142 discontinued the periodic amortization of goodwill.

(2) The income (loss) from discontinued operations for the periods presented above and the 2003 loss on sale related to the discontinuedoutplacement unit, sold in December 2003.

21MPS Group

Management’s Discussion and Analysis ofFinancial Condition and Results of Operations

MPS Group, Inc. (the Company) is a leading providerof business services with over 185 offices throughoutthe United States, Canada, the United Kingdom, andcontinental Europe. We deliver specialty staffing,consulting and business solutions to virtually allindustries in the following disciplines, through thefollowing primary brands:

Brand(s) DisciplineModis® Information Technology (IT)

ServicesBadenoch & Clark®, Accounting and FinanceAccounting Principals®Entegee® EngineeringSpecial Counsel® LegalIdea Integration® IT SolutionsSoliant Health® Health CareBeeline® Human Capital Automation

Historically, we have presented the financial results ofour operations under three reporting segments:Professional services, IT services, and IT solutions. Inan effort to better align the reporting of our financialresults with the manner in which we currently manageour business, we revised the presentation of ourfinancial results from three to four reporting segmentsin the fourth quarter of 2004. Our four reportingsegments are North American Professional services,European Professional services, North American ITservices and European IT services. Prior periods havebeen reclassified to conform to this presentation.

Non-GAAP Financial Measures From time to time we may measure certain financialinformation on a ‘constant currency’ basis. Such constantcurrency financial data is not a U.S. generally acceptedaccounting principles (GAAP) financial measure.

Constant currency removes from financial data theimpact of changes in exchange rates between the U.S.dollar and the functional currencies of our foreignsubsidiaries, by translating the current period financialdata into U.S. dollars using the same foreign currencyexchange rates that were used to translate the financialdata for the previous period. We believe presentingcertain results on a constant currency basis is useful toinvestors because it allows a more meaningful comparisonof the performance of our foreign operations from periodto period. Additionally, certain internal reporting andcompensation targets are based on constant currencyfinancial data for our various foreign subsidiaries.However, constant currency measures should not beconsidered in isolation or as an alternative to financialmeasures that reflect current period exchange rates, orto other financial measures calculated and presentedin accordance with GAAP.

From 2002 to 2004, we acquired ten businesses for ourNorth American professional services segment (together,the “Acquisitions”): four legal staffing businessesacquired in February of 2003, August of 2003, Augustof 2004, and October of 2004; three health carestaffing businesses acquired in June of 2002, Februaryof 2004, and March of 2004; and three accountingstaffing businesses acquired in February of 2004, Julyof 2004, and October 2004. From time to time wemay measure certain financial information excludingthe effect of acquisitions. Such financial data thatexcludes the effect of businesses we acquire is not aGAAP financial measure. We believe presenting someresults excluding the effects of businesses we acquire ishelpful to investors because it permits a comparison ofthe performance of our core internal operations fromperiod to period. Additionally, certain internal reportingand compensation targets are based on the performanceof core internal operations. The effect of a business weacquire is excluded for the first 12 months followingthe acquisition date. Subsequent to this, a business is

considered to be integrated for reporting purposes.Again however, such measures should be consideredonly in conjunction with the correlative measures thatinclude the results from acquisitions, as calculated andpresented in accordance with GAAP.

Additionally, from time to time we may use EBITDAto measure results of operations. EBITDA is a non-GAAP financial measure that is defined as earningsbefore interest, taxes, depreciation and amortization.We believe EBITDA is a meaningful measure ofoperating performance as it gives management aconsistent measurement tool for evaluating the operatingactivities of the business as a whole, as well as, thevarious operating units, before the effect of investingactivities, interest and taxes. In addition, we believeEBITDA provides useful information to investors,analysts, lenders, and other interested parties becauseit excludes transactions that management considersunrelated to core business operations, thereby helpinginterested parties to more meaningfully evaluate, trendand analyze the operating performance of our business.We also use EBITDA for certain internal reportingpurposes, and certain compensation targets may bebased on EBITDA. Finally, certain covenants in ourdebt facility are based on EBITDA performancemeasures. EBITDA, as with all non-GAAP financialmeasures, should be considered only in conjunction withthe comparable measures, as calculated and presentedin accordance with GAAP, including net income.

Discontinued Operations In December 2003, we sold certain operating assets andtransferred certain operating liabilities of our outplace-ment unit. As a result of the sale of this unit and inaccordance with GAAP, the Consolidated FinancialStatements and Management’s Discussion and Analysisof Financial Condition and Results of Operationsreport the results of operations of our outplacementunit as Discontinued Operations for all periodspresented. Revenue generated by this unit was $21.0million and $35.8 million, in 2003 and 2002, respectively.Income (loss) before taxes was $(3.7) million and $2.2million, for 2003 and 2002, respectively. We recordedcontract termination costs of $732,000 in 2002, and,as a result of the sale, an additional $705,000 in 2003.Additional information on contract termination costscan be found in Exit Costs below. Additional informationon Discontinued Operations can be found in Footnote17 to the Consolidated Financial Statements.

Critical Accounting Policies We prepare our financial statements in conformitywith accounting principles generally accepted in theUnited States of America. Associated with this, webelieve the following are our most critical accountingpolicies in that they are the most important to the

portrayal of our financial condition and results andrequire management’s most difficult, subjective orcomplex judgments.

Revenue Recognition We recognize substantially all revenue at the timeservices are provided, and on a time and materials basis.In most cases, the consultant is our employee and allcosts of employing the worker are our responsibility andare included in cost of revenue. Revenues is generatedwhen we permanently place an individual with a clientare recorded at the time of start.

In addition and to a lesser extent, we are involved infixed price or lump-sum engagements. The services werender under the relevant contracts generally requireperformance spanning more than one accountingperiod. We recognize revenue for these engagementsunder the proportional performance accounting model.

Allowance for Doubtful Accounts We regularly monitor and assess our risk of notcollecting amounts we are owed by our customers.This evaluation is based upon a variety of factorsincluding: an analysis of amounts current and past duealong with relevant history and facts particular to thecustomer. Based upon the results of this analysis, werecord an allowance for uncollectible accounts for thisrisk. This analysis requires us to make significantestimates, and changes in facts and circumstancescould result in material changes in the allowance fordoubtful accounts.

Income Taxes The provision for income taxes is based on incomebefore taxes as reported in the ConsolidatedStatements of Operations. Deferred tax assets andliabilities are recognized for the expected future taxconsequences of events that have been included in thefinancial statements or tax returns. Under this method,deferred tax assets and liabilities are determined basedon the differences between the financial statementcarrying amounts and the tax basis of assets andliabilities using enacted tax rates in effect for the yearin which the differences are expected to reverse. Anassessment is made as to whether or not a valuationallowance is required to offset deferred tax assets. Thisassessment includes anticipating future income.

Significant management judgment is required indetermining the provision for income taxes, deferredtax assets and liabilities and any valuation allowancerecorded against our deferred tax assets. Managementevaluates all available evidence to determine whetherit is more likely than not that some portion or all ofthe deferred income tax assets will not be realized.The establishment and amount of a valuation allowance

22 MPS Group

requires significant estimates and judgment and canmaterially affect our results of operations. Our effectivetax rate may vary from period to period based, forexample, on changes in estimated taxable income orloss, changes to the valuation allowance, changes tofederal, state or foreign tax laws, completion of federal,state or foreign audits, deductibility of certain costs andexpenses by jurisdiction, and as a result of acquisitions.

We have a net deferred tax asset as of December 31,2004 and 2003, primarily due to the impairment lossrecorded as a change in accounting principle associatedwith our adoption of Statement of Financial AccountingStandards (SFAS) No. 142 in 2002. This impairmentreduced the financial statement-carrying amount ofgoodwill, which resulted in the tax basis of tax-deductiblegoodwill being greater than the financial statement-carrying amount. Our tax basis in tax-deductiblegoodwill will be deducted in our income tax returns,generating $370.4 million of future tax deductionsover the next 15 years.

We are subject to periodic review by federal, state,foreign and local taxing authorities in the ordinarycourse of business. In 2002, we recorded an $8.7million charge for an agreed upon adjustment relatedto an audit of our prior years’ tax returns. Additionalinformation on Income Taxes can be found inFootnote 7 to the Consolidated Financial Statements.

Stock Option Plans We have historically issued stock options to employeesand directors as an integral part of our compensationprograms. U.S. GAAP allows alternative methods ofaccounting for these plans. We have chosen to accountfor our stock option plans under Accounting PrinciplesBoard Opinion No. 25, Accounting for Stock Issued toEmployees (“APB 25”). Under APB 25, the intrinsicvalue of the options is used to record compensationexpense and, as a result, no compensation expenserelated to stock options is included in determining netincome and net income per share in the ConsolidatedFinancial Statements. Restricted stock grants areaccounted for in accordance with APB 25, whichmandates that restricted stock grants with performanceconditions be calculated using the intrinsic value. Asrequired by SFAS No. 148, Accounting for Stock-BasedCompensation—Transition and Disclosure (“SFAS148”), calculations of pro forma net income (loss) andnet income (loss) per share, computed in accordancewith the method prescribed by SFAS No. 123,Accounting for Stock-Based Compensation (“SFAS 123”),are set forth in Footnote 2 to the ConsolidatedFinancial Statements.

We expect to adopt the provisions of SFAS No. 123(revised 2004), Share-Based Payments (“SFAS 123R”),which replaces SFAS No. 123 and supercedes APBOpinion No. 25. SFAS 123R requires all share-basedpayments to employees, including grants of employeestock options, to be recognized in the financialstatements based on their fair values, beginning withthe first interim or annual period after June 15, 2005.The pro forma disclosures previously permitted underSFAS 123 no longer will be an alternative to financialstatement recognition. Under SFAS 123R, we mustdetermine the appropriate fair value model to be usedfor valuing share-based payments, the amortizationmethod for compensation cost and the transition methodto be used at the date of adoption. The transitionmethods include prospective and retroactive adoptionalternatives. Under the retroactive alternatives, priorperiods may be restated either as of the beginning ofthe year of adoption or for all periods presented. Theprospective method requires that compensation expensebe recorded for all unvested stock options and restrictedstock at the beginning of the first quarter of adoptionof SFAS 123R, while the retroactive methods wouldrecord compensation expense for all unvested stockoptions and restricted stock beginning with the firstperiod restated. We are evaluating the requirements ofSFAS 123R and have not yet determined the methodof adoption or the effect of adopting SFAS 123R, norhave we determined whether the adoption will resultin amounts that are similar to the current pro formadisclosures under SFAS 123.

Impairment of Tangible and Intangible Assets For acquisitions, we allocate the excess of cost overthe fair market value of the net tangible assets first toidentifiable intangible assets, if any, and then togoodwill. In connection with SFAS No. 142, Goodwilland Other Intangible Assets, we are required to perform, atleast annually, goodwill impairment reviews utilizing afair-value approach. Additionally, SFAS No. 142required a transitional goodwill impairment reviewupon adoption.

We adopted SFAS No. 142 as of January 1, 2002.After performing the required transitional goodwillimpairment tests, we recognized a loss of $553.7million, net of an income tax benefit of $113.0 million,and recorded the loss (net of the related tax benefit) asa cumulative effect of an accounting change in theConsolidated Statement of Operations for 2002. Weperformed additional valuation testing during thefourth quarter of 2002, 2003 and 2004 (our designatedtiming of the annual impairment test under SFAS No.142) and did not incur any further impairment. Weplan to perform our next annual impairment reviewduring the fourth quarter of 2005. An impairment

23MPS Group

review prior to our next scheduled annual review maybe required if certain events occur, including lowerthan forecasted earnings levels for various reportingunits. In addition, changes to other assumptions couldsignificantly impact our estimate of the fair value of ourreporting units. Such a change may result in a goodwillimpairment charge, which could have a significantimpact on the reportable segments that include therelated reporting units and the Consolidated FinancialStatements.

As part of our goodwill impairment reviews, fair valuewas calculated using an equally blended value of adiscounted cash flow analysis and market comparables.In contrast to SFAS 142, the prior accounting standard(SFAS No. 121) required the use of undiscountedcash flow estimates over the remaining useful life ofthe goodwill and other long-lived assets as a step 1test for possible impairment. Under SFAS No. 121,the concept of recoverability of the goodwill over theuseful life of the asset was the underlying test forimpairment as opposed to fair value under SFAS No.142. This fundamental difference in the underlyingmethodologies of testing for impairment of goodwillin SFAS No. 121 and SFAS No. 142 caused us toattribute the resulting impairment from the initialvaluation completed on January 1, 2002 to a change inaccounting principle upon the adoption of SFAS No.142. Projected cash flows, used for both SFAS No. 121and No. 142 testing, considered the effects from thethen downturn in our business.

As mentioned above, we used an equally blendedvalue of a discounted cash flow analysis and marketcomparables to arrive at fair value for SFAS No. 142.For the discounted cash flow analysis, significantassumptions included expected future revenue growthrates, reporting unit profit margins, working capitallevels and a discount rate. The revenue growth ratesand reporting unit profit margins are based, in part, onour expectation of an improving economic environment.Market comparables included a comparison of themarket ratios and performance fundamentals fromcomparable companies. The use of these measurementcriteria is consistent with the underlying concepts usedin determining the fair value of a company or reportableunit under the market approach. The market ratioswe used refer to the multiples of revenue and earningsof comparable companies and the performancefundamentals refer to the consideration of the effectsof the differences in the operating metrics, i.e. growthrates, operating margins, gross margins, etc. on ourvalue versus the comparable companies. Additionalinformation on Goodwill can be found in Footnote 5to the Consolidated Financial Statements.

We amortize the cost of identifiable intangible assets(either through acquisition or as part of intellectualproperty) over their estimated useful lives unless suchlives are deemed indefinite. We review our long-livedassets and identifiable intangibles for impairmentwhenever events or changes in circumstances indicatethat the carrying amount of the asset may not berecoverable. In performing the review for recoverability,we estimate the future cash flows expected to resultfrom the use of the asset and its eventual disposition.If the sum of the expected future cash flows(undiscounted and without interest charges) is lessthan the carrying amount of the asset, an impairmentloss is recognized. Otherwise, an impairment loss isnot recognized. Measurement of an impairment lossfor long-lived assets and identifiable intangibles wouldbe based on the fair value of the asset.

Exit Costs In 2001 and 2002, we experienced a material decreasein demand for our domestic operations. To reflect thisdecreased demand, we made attempts to realign our realestate capacity needs and thus vacate and reorganizecertain office space.