2004 Annual Report...Board includes other asset classes such as bonds, real estate, and resource...

178

2004 Annual Report Minnesota State Board of Investment

Transcript of 2004 Annual Report...Board includes other asset classes such as bonds, real estate, and resource...

2004Annual Report

Minnesota StateBoard of Investment

2004 Annual Report

Table of Contents

Introduction ............................................................................................. 1

Funds Under Management ....................................................................... 2

Combined Funds ...................................................................................... 5

Basic Retirement Funds ........................................................................... 9

Post Retirement Fund ............................................................................ 12

Investment Pools .................................................................................... 15

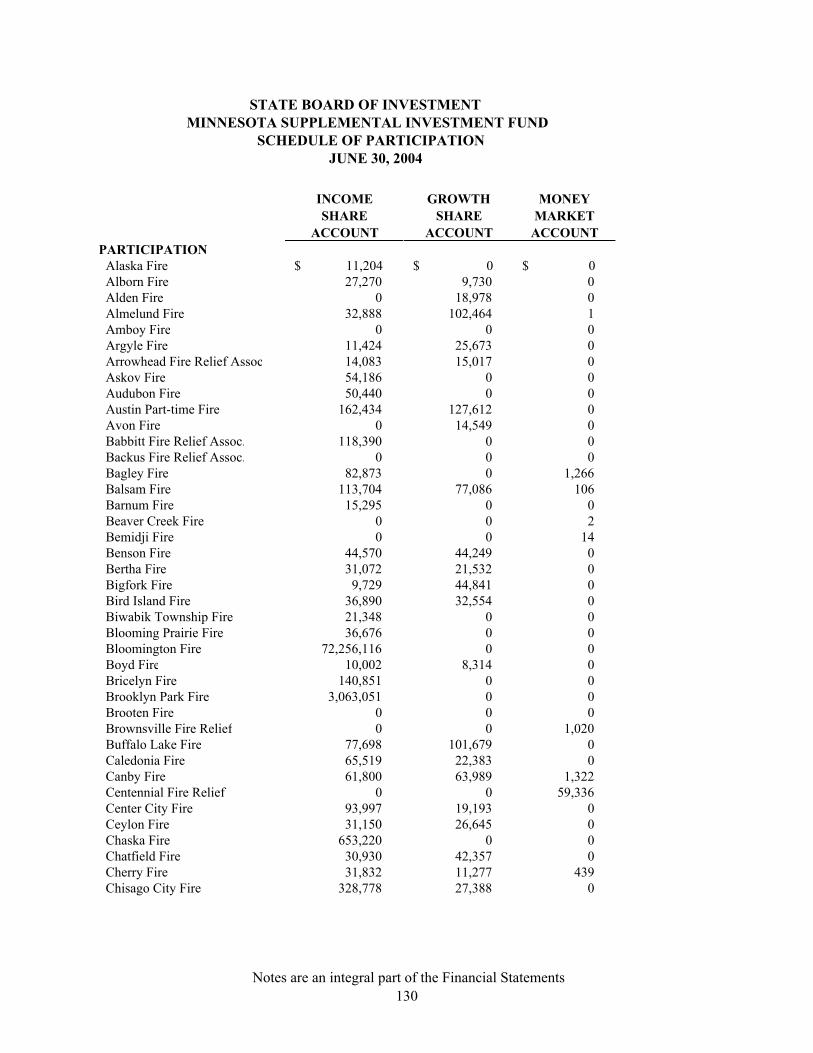

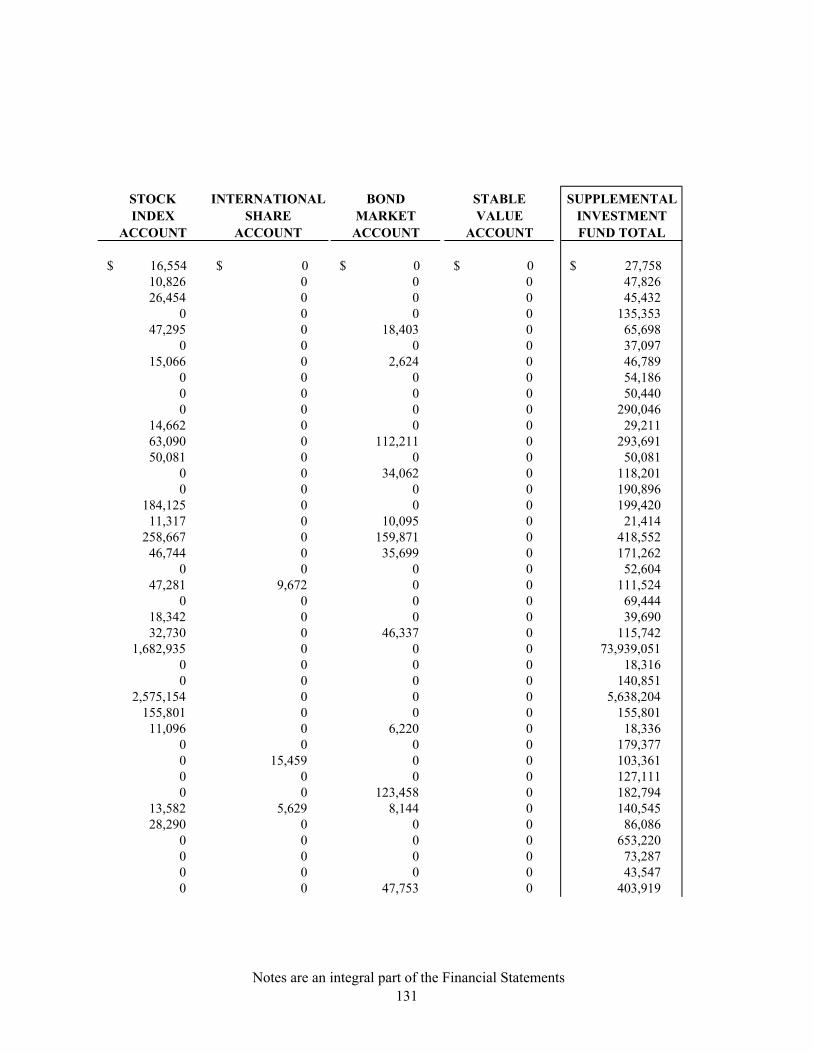

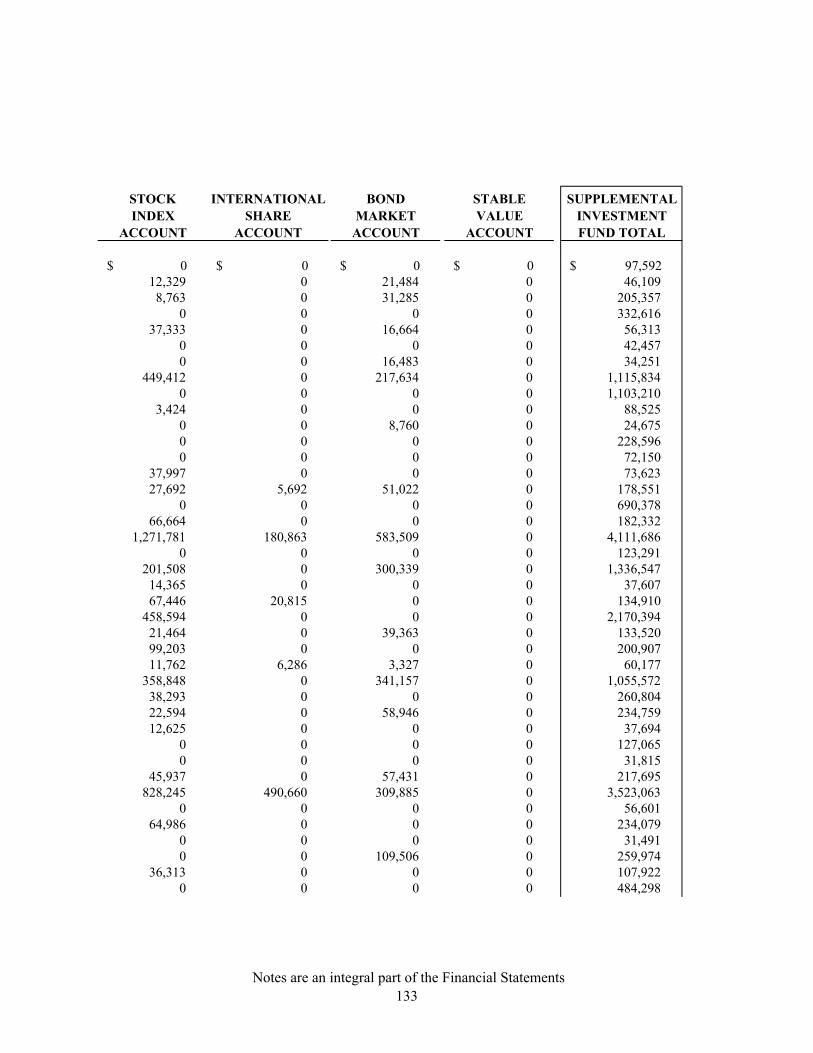

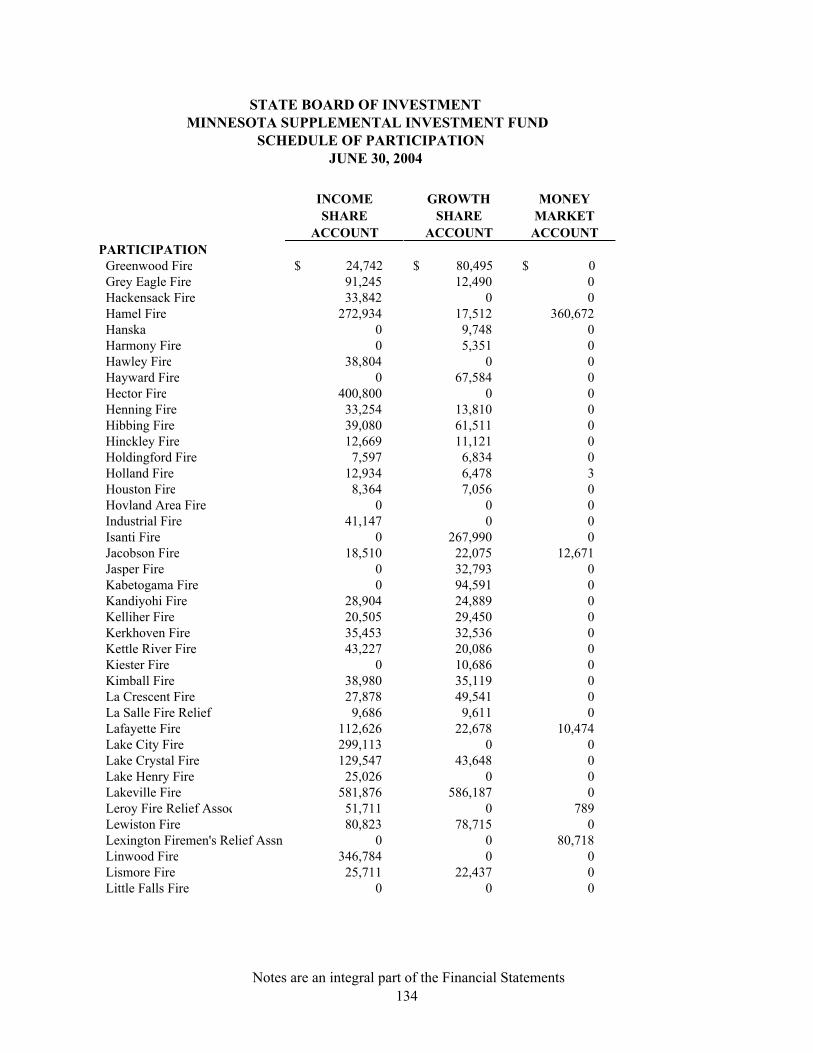

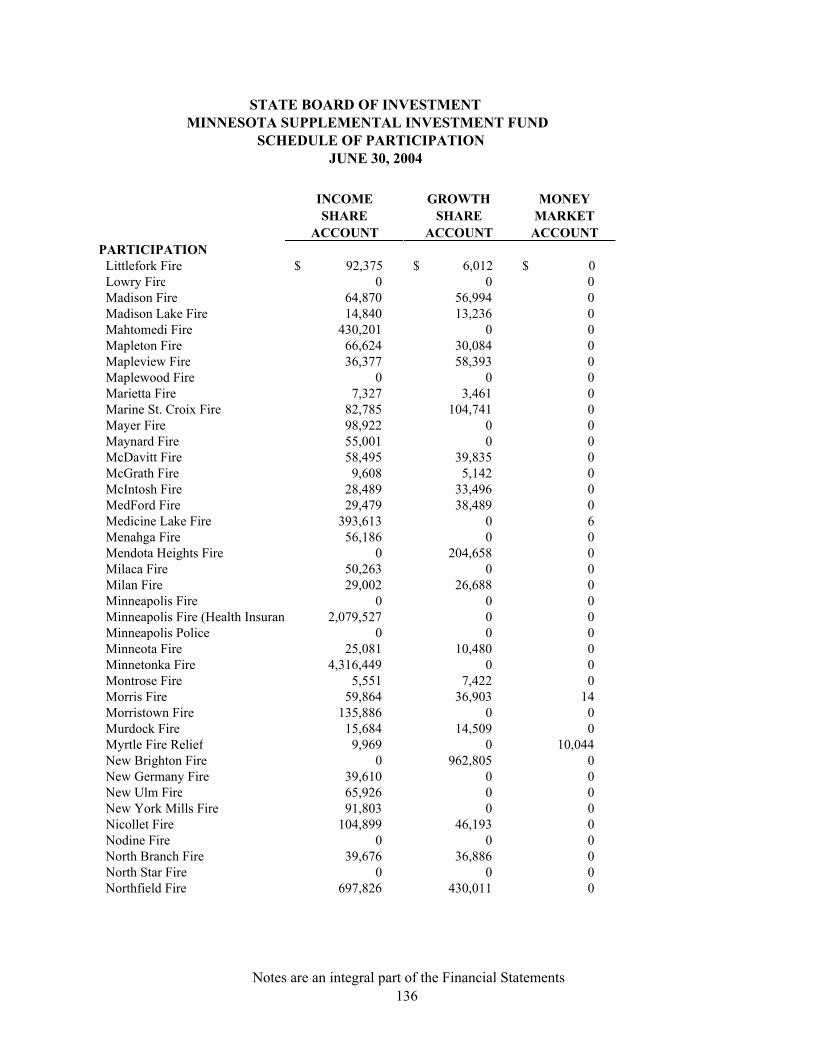

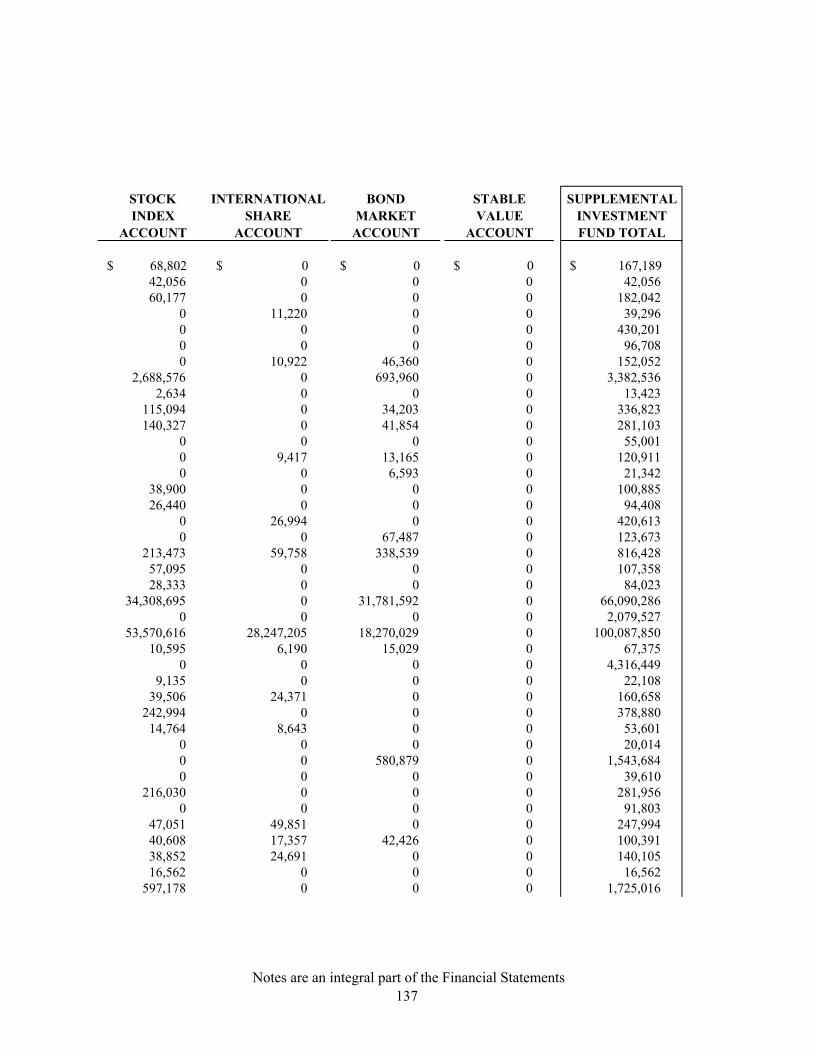

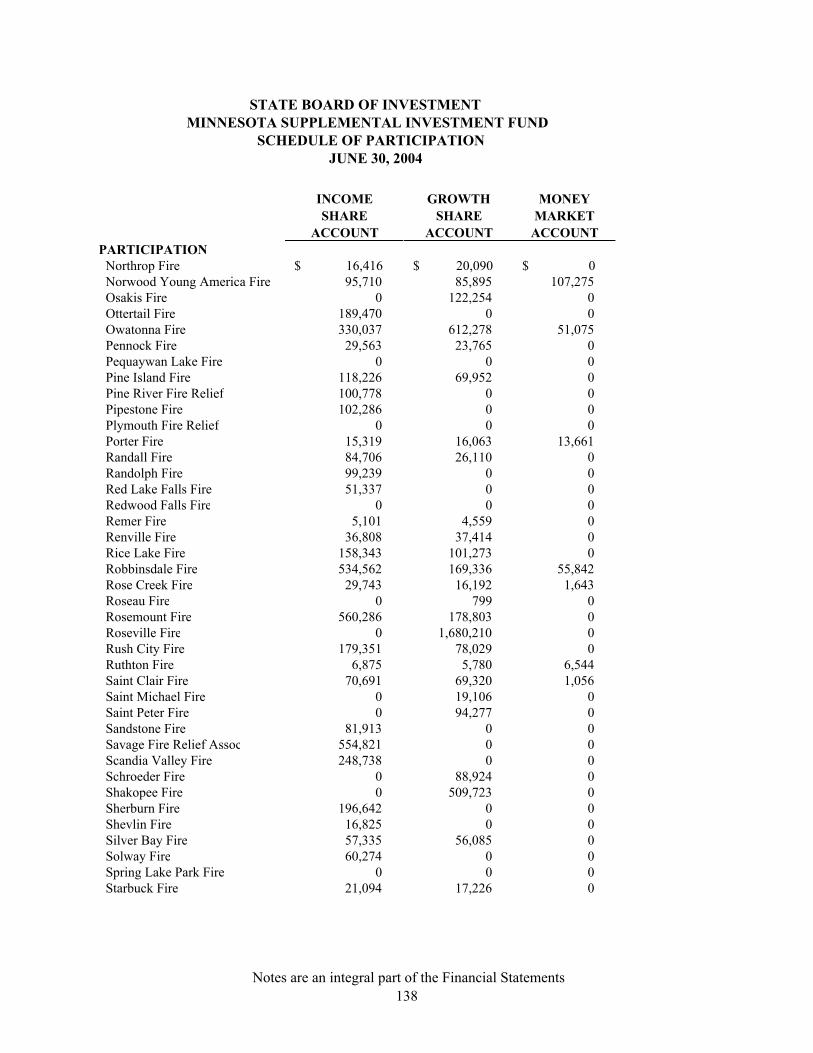

Supplemental Investment Fund .............................................................. 25

State Deferred Compensation Plan ........................................................ 34

Assigned Risk Plan ................................................................................ 37

Permanent School Fund ......................................................................... 39

Environmental Trust Fund ..................................................................... 41

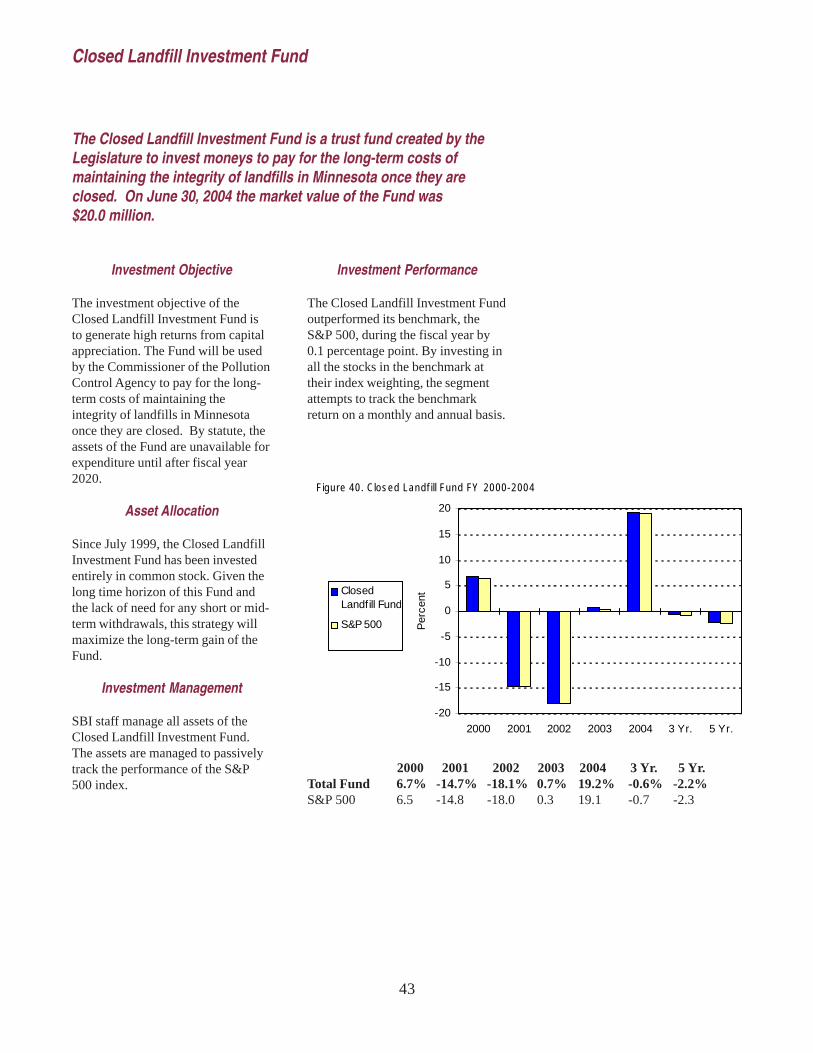

Closed Landfill Investment Fund........................................................... 43

CashManagement and Related Programs ............................................. 44

Other Deferred Compensation Programs ............................................... 46

Major Policy Initiatives ......................................................................... 47

Investment Manager Summaries ............................................................ 54

StatisticalData ....................................................................................... 71

Section II ............................................................................................. 113

Auditor’s Report .................................................................................. 114

Financial Statements ............................................................................ 116

Footnotes to Financial Statements ....................................................... 119

Supplemental Financial Statements ..................................................... 123

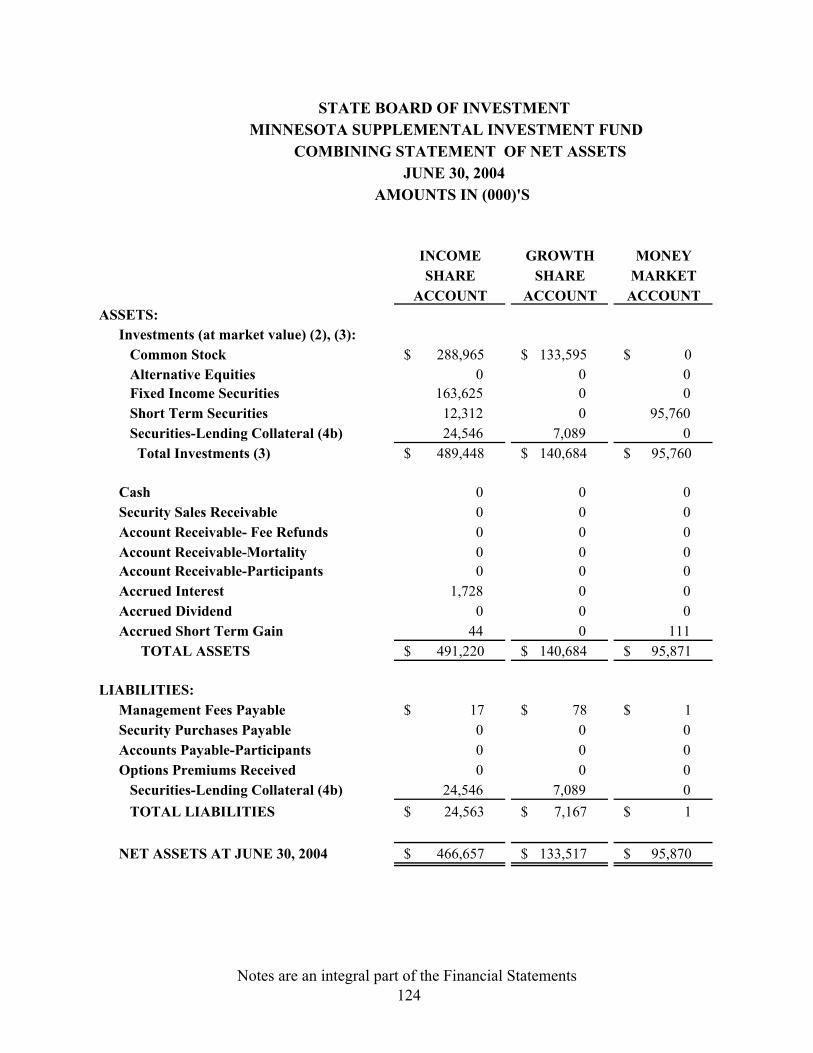

Supplemental Investment FundCombining Statements ................. 124

Pooled Investment Account Schedules ........................................... 142

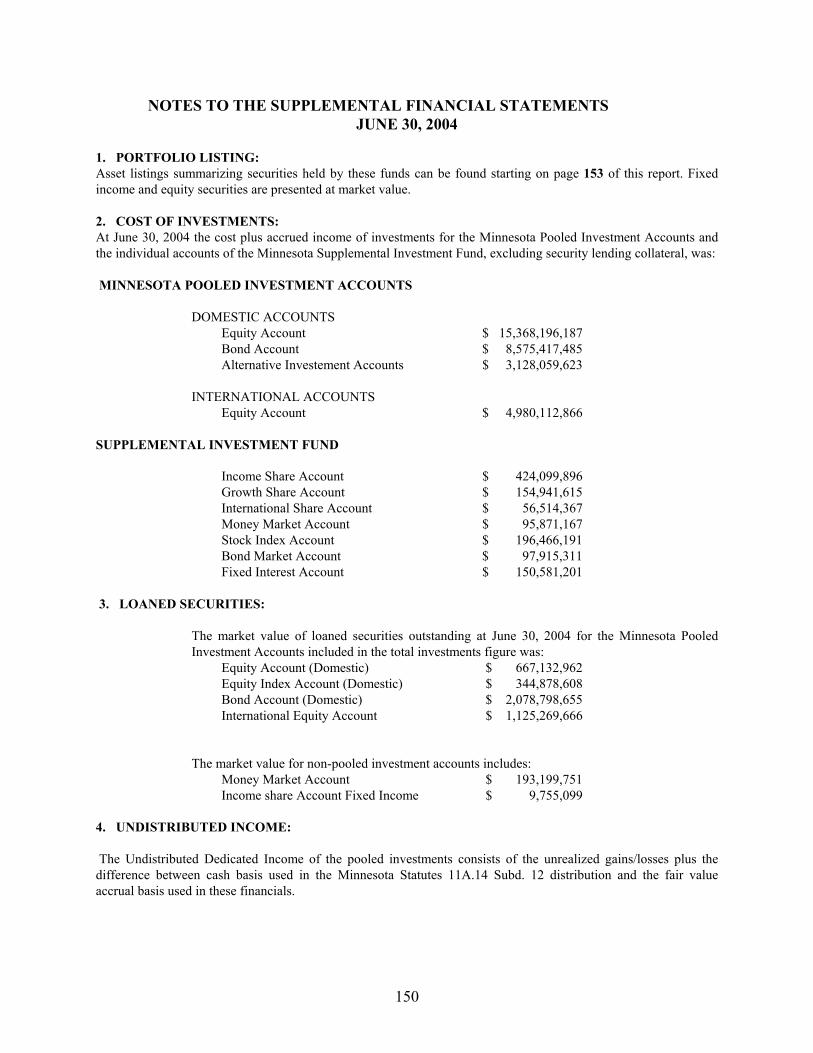

Footnotes to Supplemental Financial Statements ........................... 150

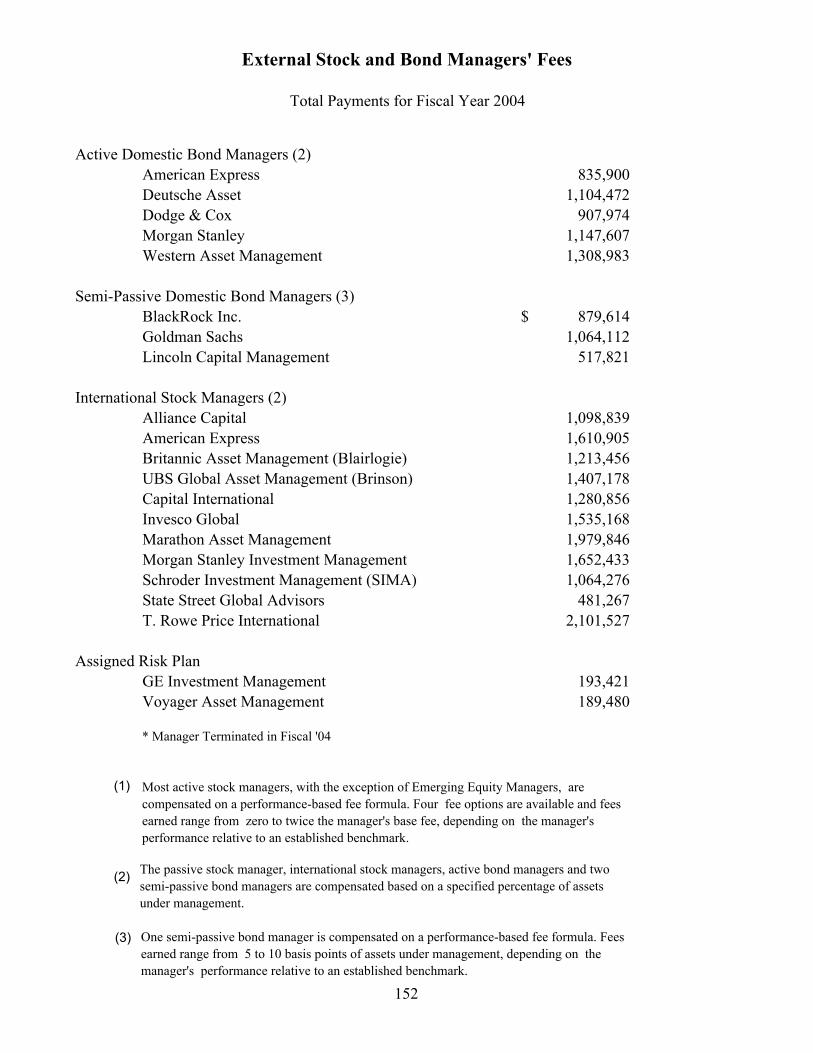

Manager Fees ....................................................................................... 151

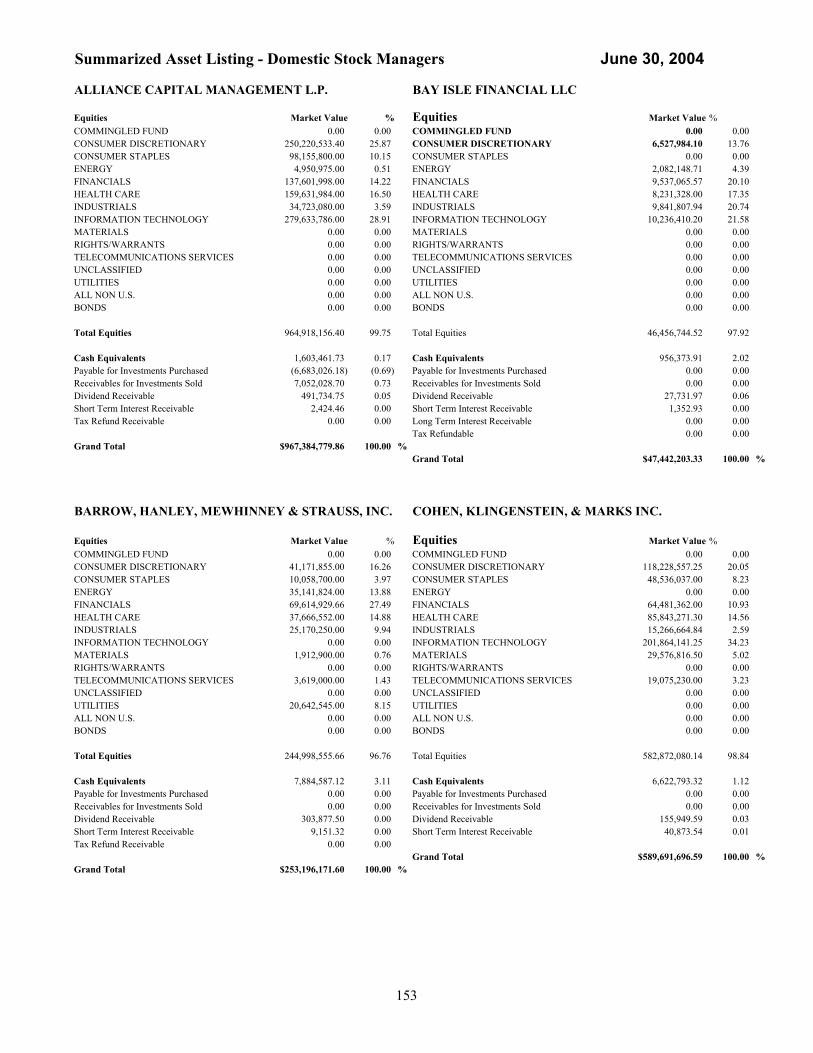

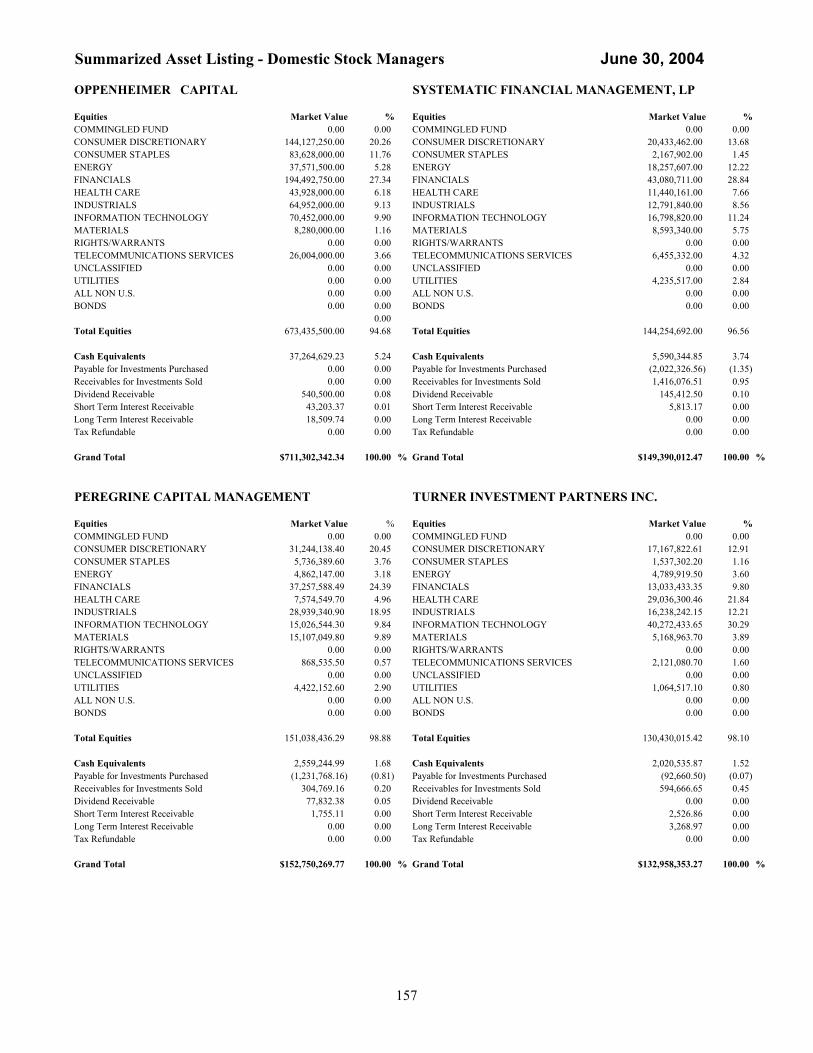

SummarizedAsset Listings .................................................................. 153

This annual report can be accessed on our website at www.sbi.state.mn.us

MINNESOTASTATEBOARD OFINVESTMENT

Board MembersGovernorTim Pawlenty

State AuditorPatricia Anderson

Secretary of StateMary Kiffmeyer

Attorney GeneralMike Hatch

Executive Director

Howard J. Bicker

60 Empire DriveSuite 355

St. Paul, MN 55103(651) 296-3328

FAX (651) 296-9572E-mail:

An Equal OpportunityEmployer

December, 2004

The Minnesota State Board of Investment (SBI) is pleased to present its report forthe fiscal year ending June 30, 2004.

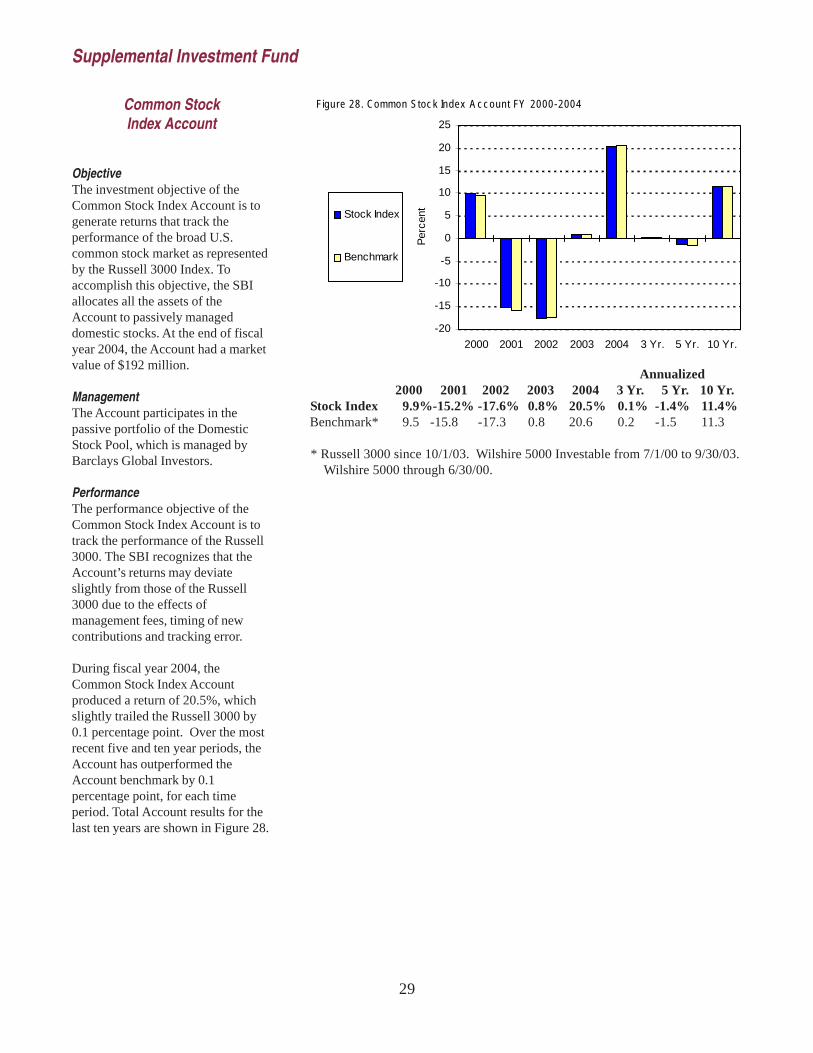

Investment EnvironmentAfter three years of lackluster performance, the U.S. and international stock markets providedstrong returns during Fiscal Year 2004. The U.S. stock market increased 20.5%, as measured bythe Russell 3000. The market improvement was a result of the U.S. economic recovery, strongconsumer confidence and improving unemployment data. This strong performance was somewhatmuted by concerns about terrorism, the war in Iraq, the presidential election, record high oil prices,and a 25 basis point increase in the federal funds rate.

International stock markets were very strong during the year. The Morgan Stanley CapitalInternational (MSCI) All Country World Index excluding the United States (ACWI Ex U.S.),which represents the developed and emerging international markets outside the U.S., returned32.1% for the fiscal year.

The U.S. bond market, as measured by the Lehman Brothers Aggregate Bond Index, returned0.3% for the fiscal year. The economic recovery and higher commodity pricing raised fears ofinflation which resulted in higher inflation rates. Mortgage securities and corporate bonds outpacedU.S. Treasury securities to allow the overall market to end in positive territory.

SBI ResultsWithin this investment environment, the retirement assets under the Board’s control improved asfollows:

• The Basic Retirement Funds increased 16.6% during fiscal year 2004. Over the latest ten year period, the Funds have experienced an annualized return of 9.8%. (See page 9.)

• The Post Retirement Fund was up 16.3% for the year. Overall, the Fund provided a ten year annualized return of 9.4%. (See page 12.)

• The lifetime Post Retirement benefit increase for Fiscal Year 2004 will be 2.5%. The increasewill be payable to eligible retirees effective January 1, 2005.

On June 30, 2004, assets under management totaled $47.1 billion. This total is the aggregateof several separate pension funds, trust funds and cash accounts, each with different investmentobjectives. In establishing a comprehensive management program, the Board develops an investmentstrategy for each fund which reflects its unique requirements. The primary purpose of thisannual report is to communicate the investment goals, policies and performance of eachfund managed by the Board. Through the investment programs presented in this report, theMinnesota State Board of Investment seeks to enhance the management and performance of thefunds under its control.

Sincerely,

Howard BickerExecutive Director

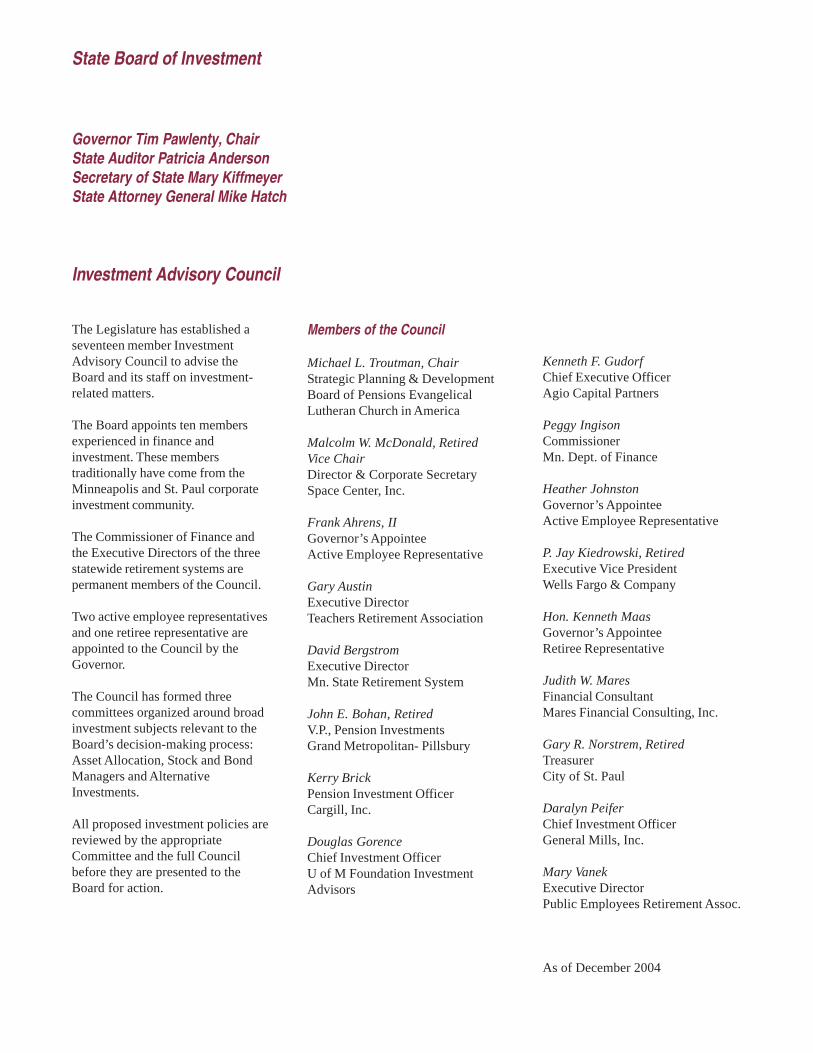

The Legislature has established aseventeen member InvestmentAdvisory Council to advise theBoard and its staff on investment-related matters.

The Board appoints ten membersexperienced in finance andinvestment. These memberstraditionally have come from theMinneapolis and St. Paul corporateinvestment community.

The Commissioner of Finance andthe Executive Directors of the threestatewide retirement systems arepermanent members of the Council.

Two active employee representativesand one retiree representative areappointed to the Council by theGovernor.

The Council has formed threecommittees organized around broadinvestment subjects relevant to theBoard’s decision-making process:Asset Allocation, Stock and BondManagers and AlternativeInvestments.

All proposed investment policies arereviewed by the appropriateCommittee and the full Councilbefore they are presented to theBoard for action.

Governor Tim Pawlenty, ChairState Auditor Patricia AndersonSecretary of State Mary KiffmeyerState Attorney General Mike Hatch

Investment Advisory Council

State Board of Investment

Members of the Council

Michael L. Troutman, ChairStrategic Planning & DevelopmentBoard of Pensions EvangelicalLutheran Church in America

Malcolm W. McDonald, RetiredVice ChairDirector & Corporate SecretarySpace Center, Inc.

Frank Ahrens, IIGovernor’s AppointeeActive Employee Representative

Gary AustinExecutive DirectorTeachers Retirement Association

David BergstromExecutive DirectorMn. State Retirement System

John E. Bohan, RetiredV.P., Pension InvestmentsGrand Metropolitan- Pillsbury

Kerry BrickPension Investment OfficerCargill, Inc.

Douglas GorenceChief Investment OfficerU of M Foundation InvestmentAdvisors

Kenneth F. GudorfChief Executive OfficerAgio Capital Partners

Peggy IngisonCommissionerMn. Dept. of Finance

Heather JohnstonGovernor’s AppointeeActive Employee Representative

P. Jay Kiedrowski, RetiredExecutive Vice PresidentWells Fargo & Company

Hon. Kenneth MaasGovernor’s AppointeeRetiree Representative

Judith W. MaresFinancial ConsultantMares Financial Consulting, Inc.

Gary R. Norstrem, RetiredTreasurerCity of St. Paul

Daralyn PeiferChief Investment OfficerGeneral Mills, Inc.

Mary VanekExecutive DirectorPublic Employees Retirement Assoc.

As of December 2004

Staff, Consultants & Custodians

���������������������������

�������������� ������������������������

Investment Staff

Public Equities+��,����������� ������,����� ������#6������

+�����+��� ������,�$��������#6������

Fixed Income andInternal Investments��������#���������� �,����� �������������

������!������ �������,�"�����������

Alternative Assets# ���*�����-�� )�� �,���� �����������������

�����)�����������������,���� �����������������

Cash Management+�� ���%�������� �,� �� ���� ����������

Public Programs#�����$�(�����-��"�� �,�!�����! �� ��

��- ��������-�� )�����,� � ����� � � �����

Administrative Staff

Finance and Accounting���������+�������������� �����$� ����

��������*�� ������������ ��� ���� ,� ����

�� ���*�) ��������������0����� ,����� ������

*������� �������������0����� ,����� ������

%��������.�����������0����� ,����� ������

# ���! �� ���������������0�����

Support Services���������/�� ��������� ��������������������#���������$� ����

��� ��*��� �0�������������� ����� �������,���� ������

+ �������"���������� � � ������ �������

Consultants

&��� ������������������0�������������������,�������

�����! �(�������������'���� ��� �������"��������� ����������,����� ��

Custodian Banks

.��� ���������� ����"����+�����+������!����0�������� ������,������������

�������������������������" �0�� �,��� ���!�,���������

������$������ �3445

1

Introduction

The Minnesota State Board of Investment is responsible for theinvestment management of various retirement funds, trust funds andcash accounts. On June 30, 2004, the market value of all assets was$47.1 billion.

Constitutional and StatutoryAuthorityThe Minnesota State Board ofInvestment (SBI) is established byArticle XI of the MinnesotaConstitution to invest all state funds.Its membership as specified in theConstitution is comprised of theGovernor (who is designated as chairof the Board), State Auditor,Secretary of State and State AttorneyGeneral.

All investments undertaken by theSBI are governed by the prudentperson rule and other standardscodified in Minnesota Statutes,Chapter 11A and Chapter 356A.

Prudent Person RuleThe prudent person rule, as codifiedin Minnesota Statutes Section11A.09, requires all members of theBoard, Investment Advisory Council,and SBI staff to “...act in good faithand ...exercise that degree ofjudgment and care, undercircumstances then prevailing,which persons of prudence,discretion and intelligence exercisein the management of their ownaffairs, not for speculation, but forinvestment, considering the probablesafety of their capital as well as theprobable income to be derivedtherefrom.” Minnesota StatutesSection 356A.04 contains similarcodification of the prudent personrule applicable to the investment ofpension fund assets.

Authorized InvestmentsIn addition to the prudent personrule, Minnesota Statutes Section

11A.24 contains a specific list ofasset classes available forinvestment, including commonstocks, bonds, short term securities,real estate, private equity, andresource funds. The statutesprescribe the maximum percentageof fund assets that may be investedin various asset classes and containspecific restrictions to ensure thequality of the investments.

Investment PoliciesWithin the requirements defined bystate law, the State Board ofInvestment, in conjunction with SBIstaff and the Investment AdvisoryCouncil, establishes investmentpolicies for all funds under itsmanagement. These investmentpolicies are tailored to the particularneeds of each fund and specifyinvestment objectives, risk tolerance,asset allocation, investmentmanagement structure and specificperformance standards.

The Board has adopted guidelinesconcerning investments in stockmarkets outside the U.S. Theguidelines do not prohibit investmentin any market, but do require thatadditional notification and/orpresentation be provided to SBI staffor the SBI Administrative Committeein certain cases (refer to page 52 formore information on theseguidelines).

The Board, its staff, and theInvestment Advisory Council haveconducted detailed analyses of eachof the funds under the SBI’s controlthat address investment objectives,

asset allocation policy andmanagement structure. These studiesguide the on-going management ofthese funds and are updatedperiodically.

Important NotesReader should note that the SBI’sreturns in this report are shown aftertransactions costs and fees arededucted. Performance is computedand reported after all applicablecharges to assure that the Board’sfocus is on true net returns.

Due to the large number ofindividual securities owned by thefunds managed by the SBI, thisreport contains only summarizedasset listings. A complete list ofsecurities is available upon requestfrom the State Board ofInvestment.

2

Market ValueJune 30, 2004

Basic Retirement Funds $18.8 billionThe Basic Retirement Funds contain the pension assets of thecurrently working participants in eight statewide retirement plans:

Teachers Retirement Fund $6.883 billionPublic Employees Retirement Fund 4.912 billionState Employees Retirement Fund 4.163 billionPublic Employees Police and Fire Fund 2.294 billionHighway Patrol Retirement Fund 218 millionCorrectional Employees Fund 247 millionPublic Employees Correctional Fund 73 millionJudges Retirement Fund 35 million

Post Retirement Fund $18.4 billionThe Post Retirement Investment Fund is composed of the reserves forretirement benefits to be paid to retired employees. Lifetime retirementbenefit increases are permitted based on both inflation and investmentperformance.

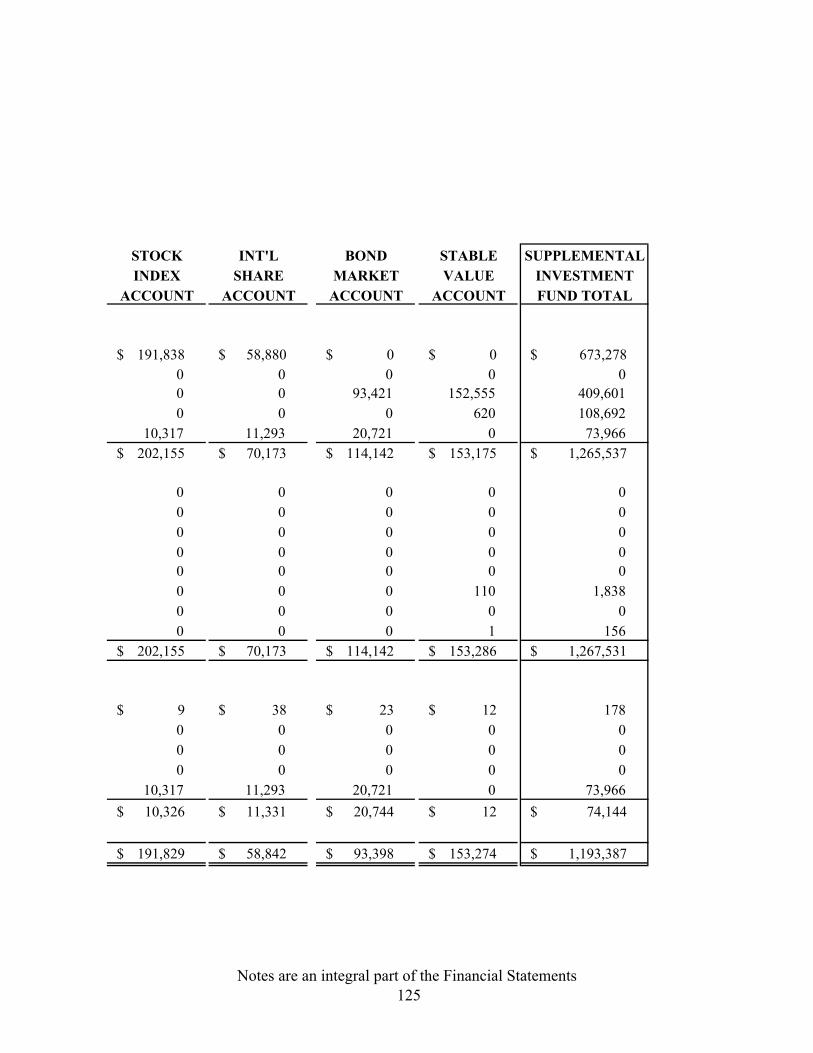

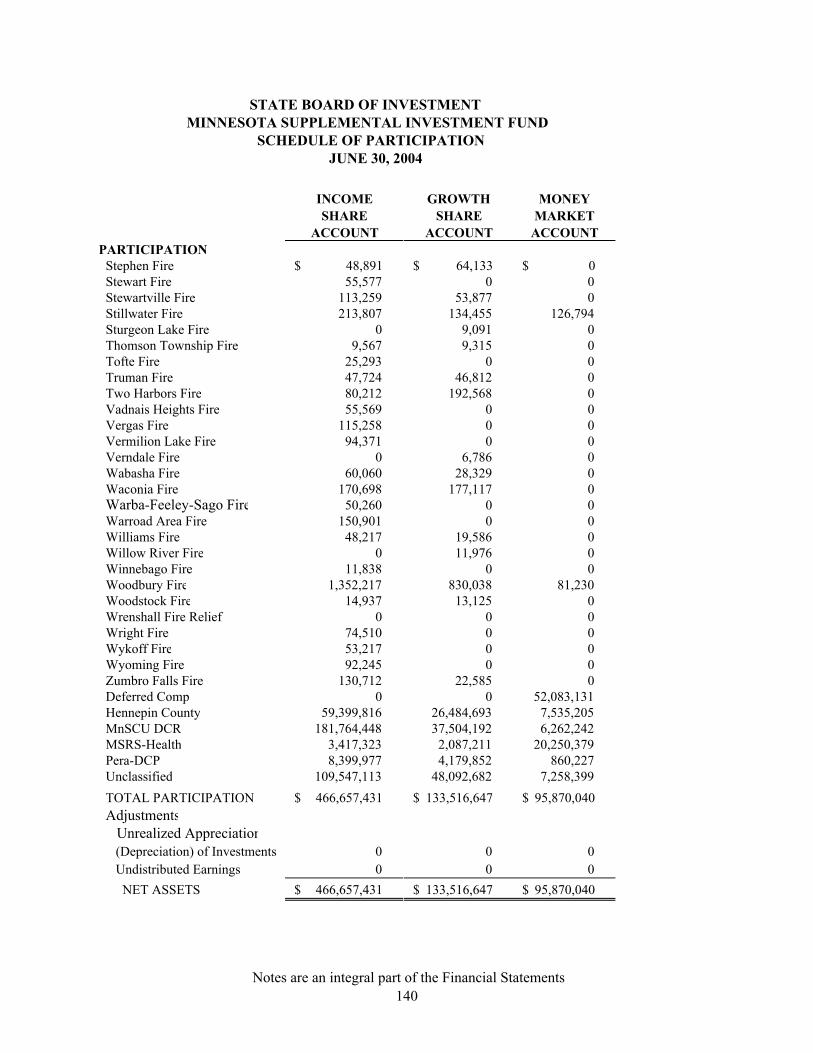

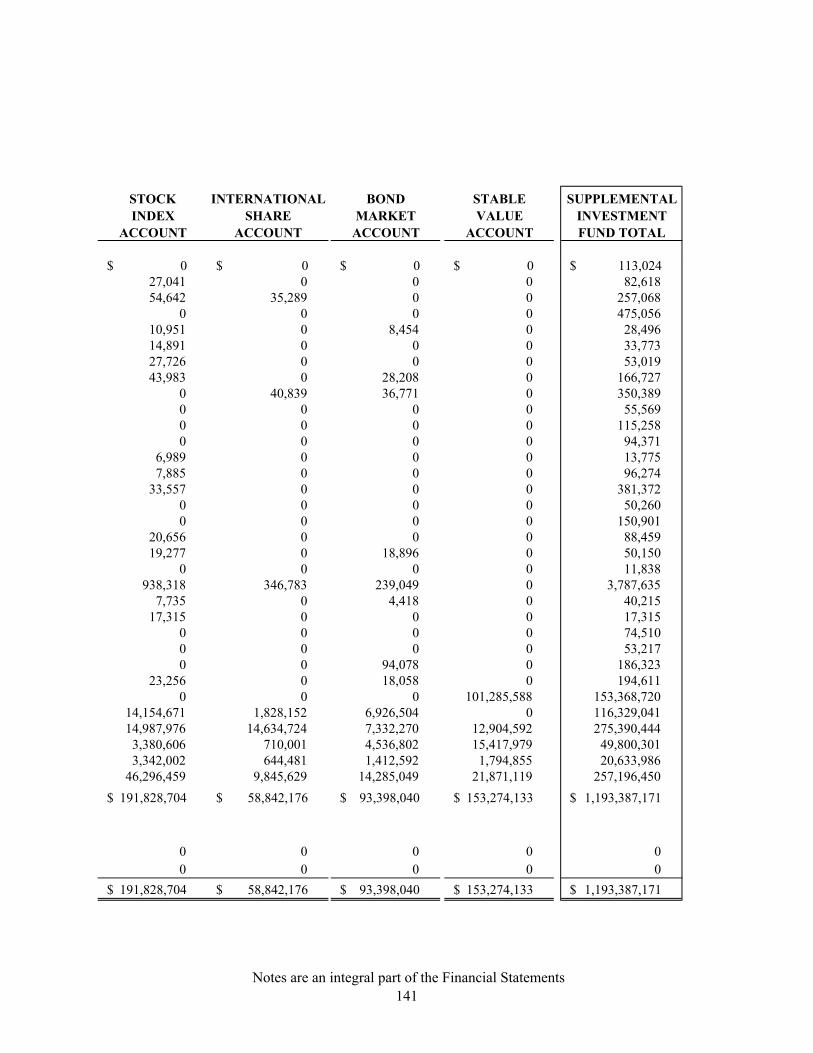

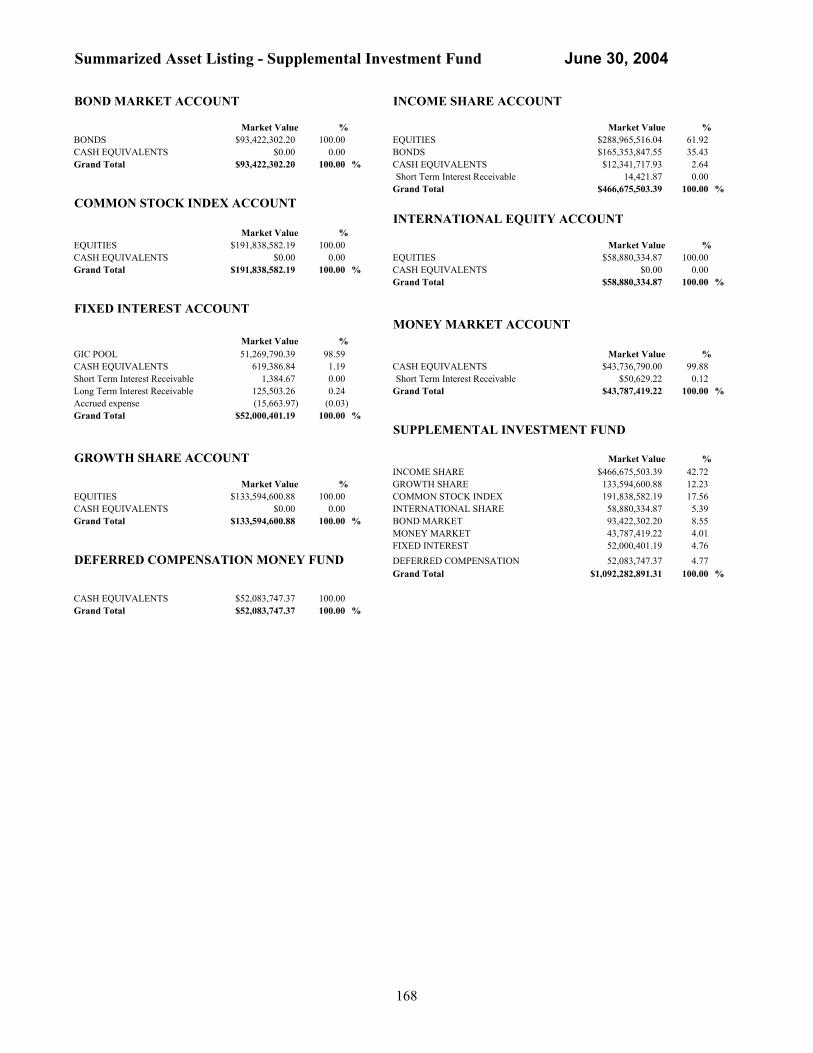

Supplemental Investment Fund (SIF) $1.0 billionThe Supplemental Investment Fund includes assets of the unclassifiedstate employees retirement plan, other defined contribution retirementplans, and various retirement programs for local police andfirefighters. Participants may choose among seven separate accountswith different investment objectives designed to meet a wide range ofparticipant needs and objectives.

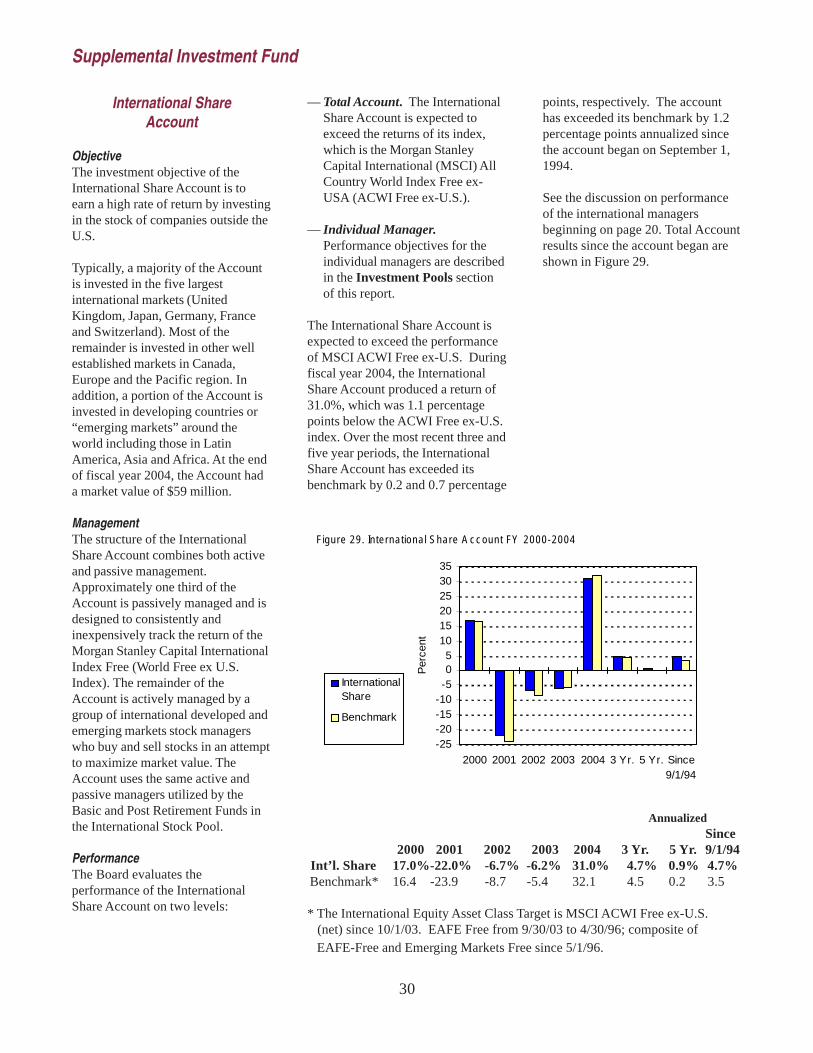

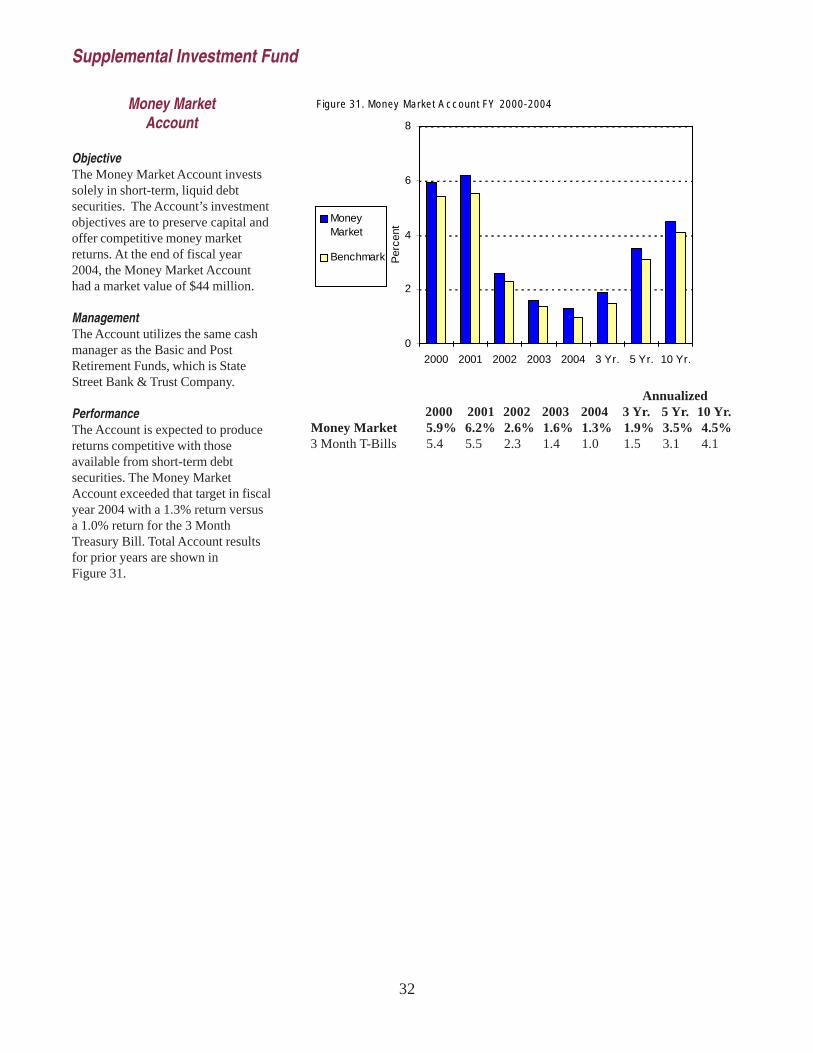

Income Share Account stocks and bonds $467 millionCommon Stock Index Account passively managed stocks 192 millionGrowth Share Account actively managed stocks 136 millionBond Market Account actively managed bonds 93 millionInternational Share Account non-U.S. stocks 59 millionFixed Interest Account stable value investments 52 millionMoney Market Account short-term debt securities 44 million

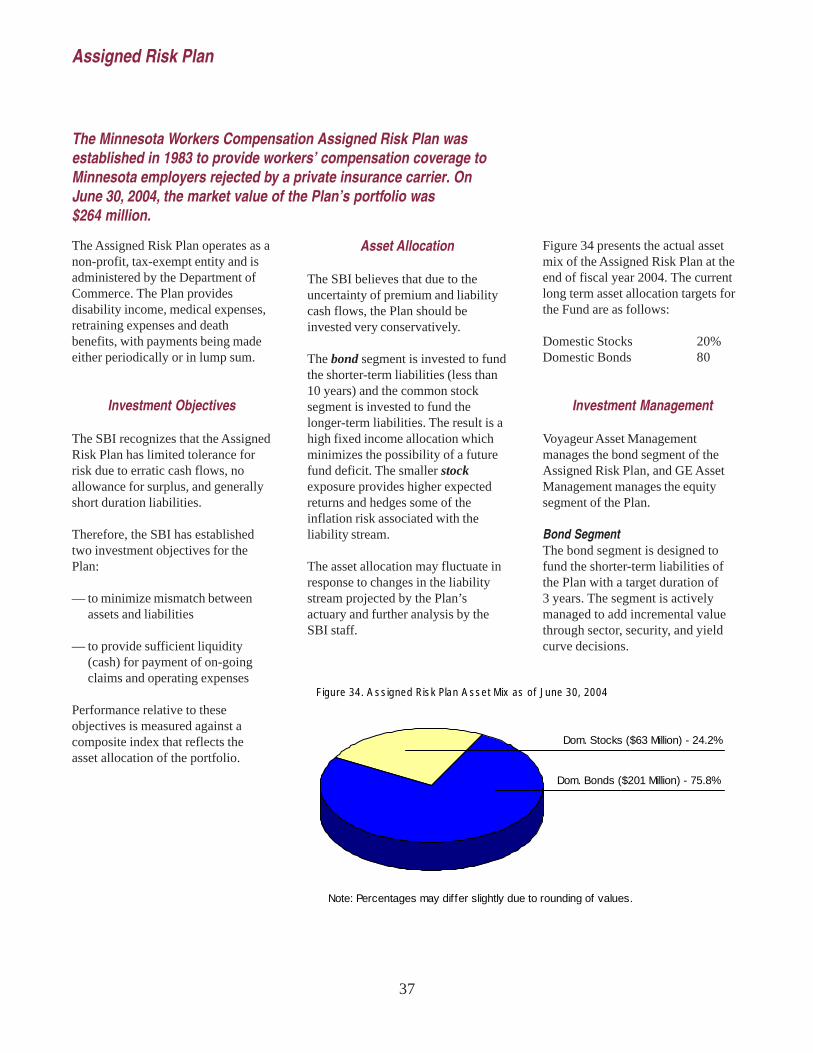

Non-Retirement Funds $1.6 billionAssigned Risk Plan $263 millionThe Minnesota Workers Compensation Assigned Risk Planprovides worker compensation insurance for companies unableto obtain coverage through private carriers.

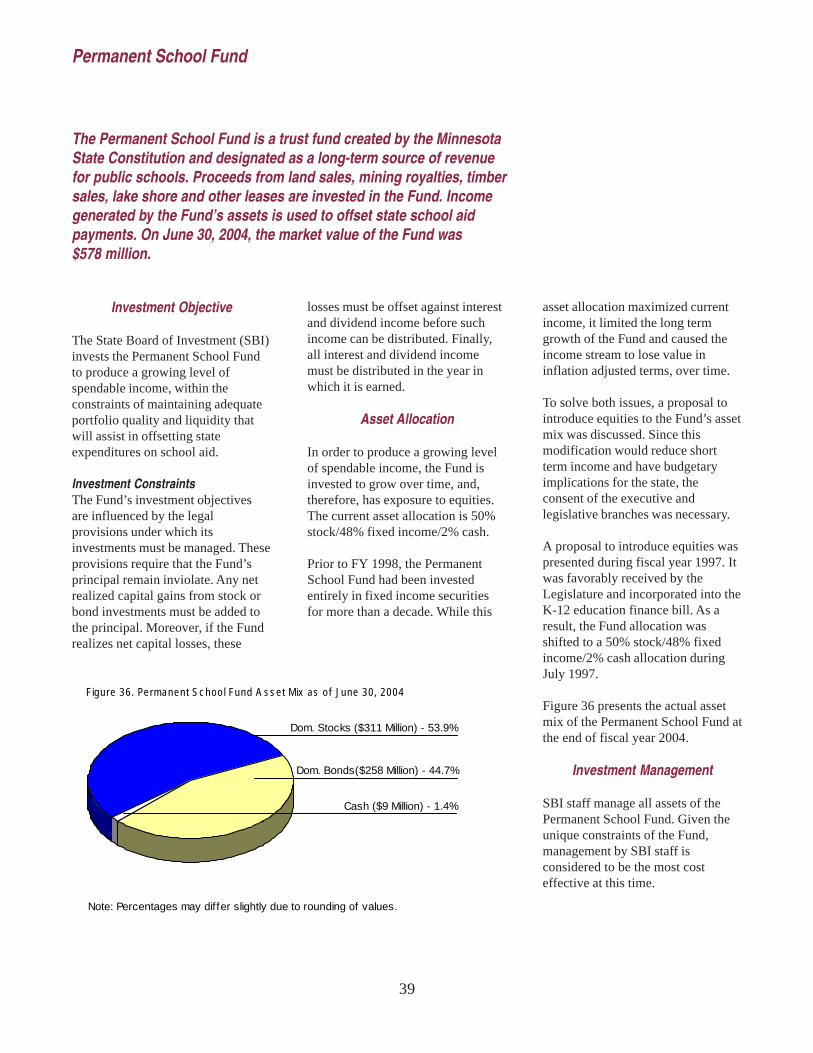

Permanent School Fund $578 millionThe Permanent School Fund is a trust established for the benefitof Minnesota public schools.

Environmental Trust Fund $342 millionThe Environmental Trust Fund is a trust established for theprotection and enhancement of Minnesota’s environment. It isfunded with a portion of the proceeds from the state’s lottery.

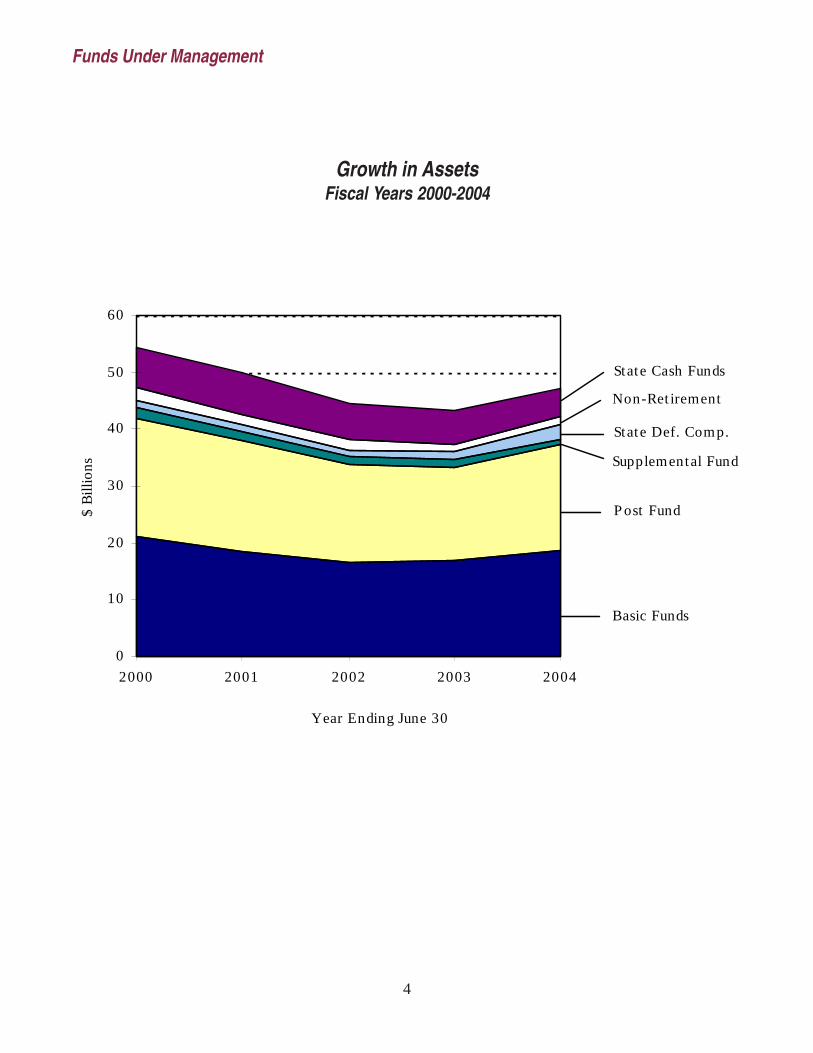

Funds Under Management

3

Market ValueJune 30, 2004

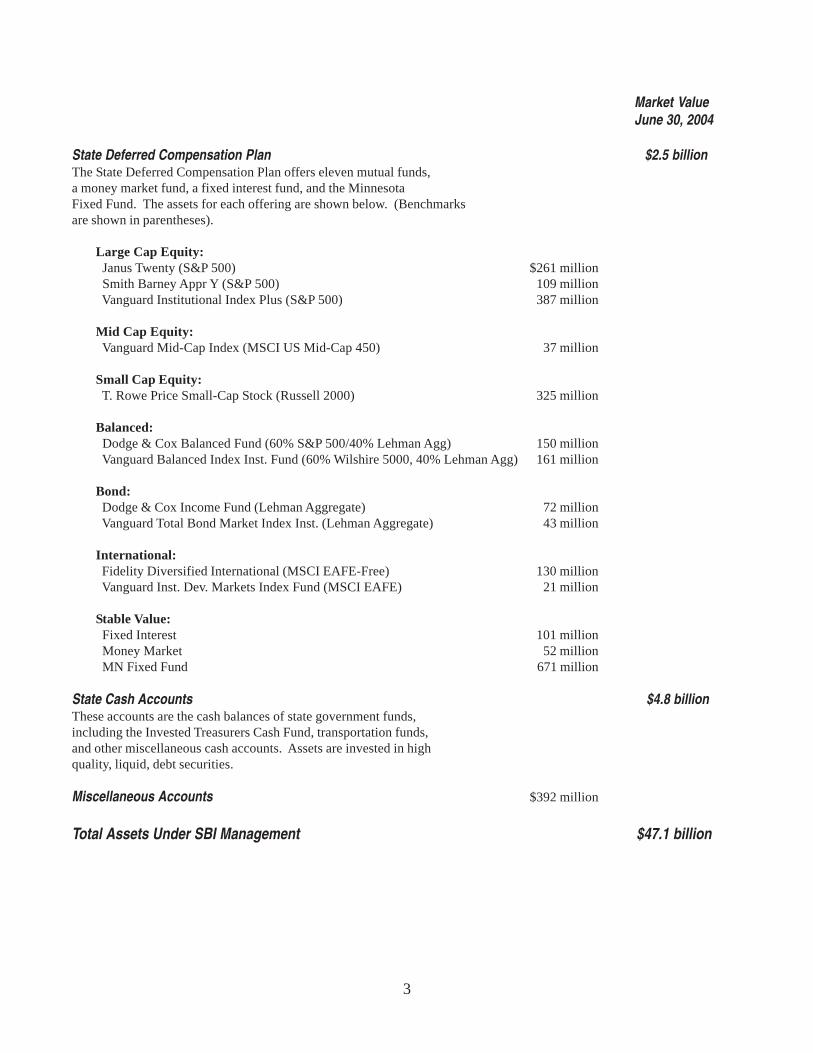

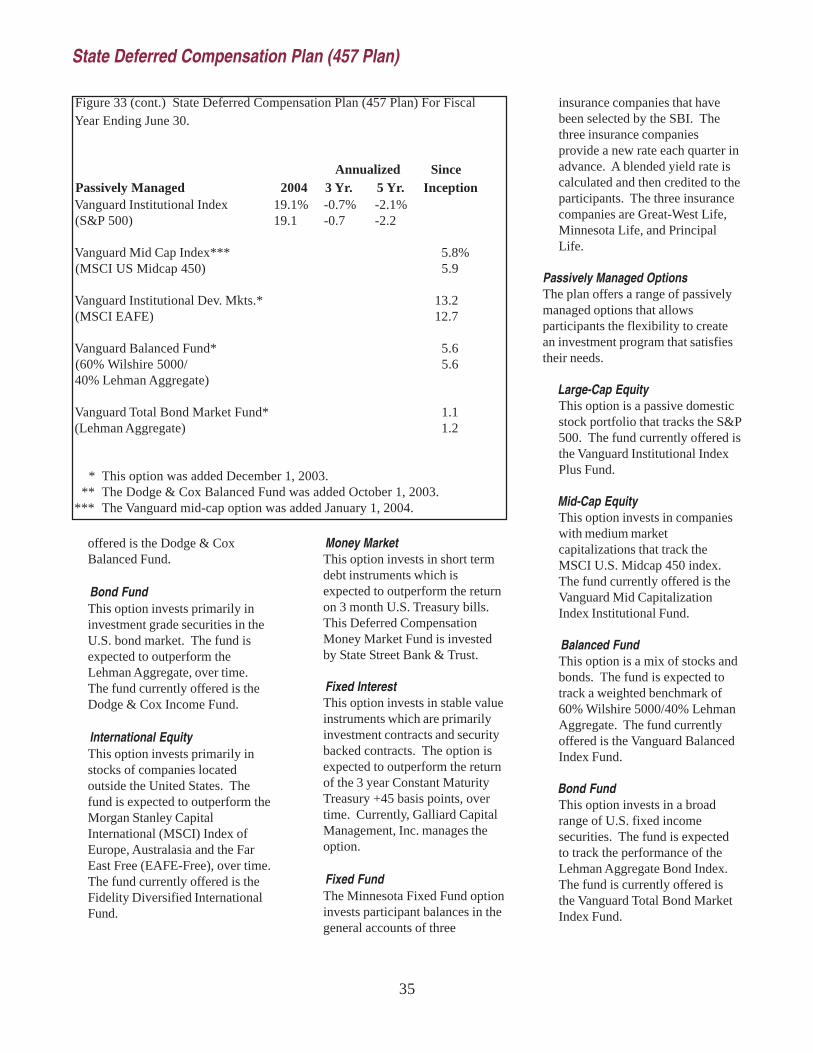

State Deferred Compensation Plan $2.5 billionThe State Deferred Compensation Plan offers eleven mutual funds,a money market fund, a fixed interest fund, and the MinnesotaFixed Fund. The assets for each offering are shown below. (Benchmarksare shown in parentheses).

Large Cap Equity: Janus Twenty (S&P 500) $261 million Smith Barney Appr Y (S&P 500) 109 million Vanguard Institutional Index Plus (S&P 500) 387 million

Mid Cap Equity: Vanguard Mid-Cap Index (MSCI US Mid-Cap 450) 37 million

Small Cap Equity: T. Rowe Price Small-Cap Stock (Russell 2000) 325 million

Balanced: Dodge & Cox Balanced Fund (60% S&P 500/40% Lehman Agg) 150 million Vanguard Balanced Index Inst. Fund (60% Wilshire 5000, 40% Lehman Agg) 161 million

Bond: Dodge & Cox Income Fund (Lehman Aggregate) 72 million Vanguard Total Bond Market Index Inst. (Lehman Aggregate) 43 million

International: Fidelity Diversified International (MSCI EAFE-Free) 130 million Vanguard Inst. Dev. Markets Index Fund (MSCI EAFE) 21 million

Stable Value: Fixed Interest 101 million Money Market 52 million MN Fixed Fund 671 million

State Cash Accounts $4.8 billionThese accounts are the cash balances of state government funds,including the Invested Treasurers Cash Fund, transportation funds,and other miscellaneous cash accounts. Assets are invested in highquality, liquid, debt securities.

Miscellaneous Accounts $392 million

Total Assets Under SBI Management $47.1 billion

4

Funds Under Management

Growth in AssetsFiscal Years 2000-2004

0

10

20

30

40

50

60

2000 2001 2002 2003 2004

$ B

illio

ns

Basic Funds

P ost Fund

Supplemental Fund

State Cash Funds

Non-Ret irement

State Def. Comp.

Year Ending June 30

5

The Combined Funds are so namedbecause they represent the combinedassets of both the Basic RetirementFunds (the funds for activeemployees) and Post RetirementFund (the fund for retiredemployees). Unlike most other publicand corporate pension plans, theassets of active and retiredemployees are separated understatute and therefore managed andaccounted for separately. Moreinformation on the structure andperformance of the Basic and PostFunds is contained in the followingchapters.

While the Combined Funds do notexist under statute, the Board finds itinstructive to review asset mix andperformance of all defined benefit

The “Combined Funds” represent the assets of both active andretired public employees who participate in the defined benefit plansof three state-wide retirement systems: Teachers RetirementAssociation (TRA), Public Employees Retirement Association (PERA)and the Minnesota State Retirement System (MSRS). OnJune 30, 2004, the Combined Funds had a market value of $37.2billion.

pension assets under its control. Thismore closely parallels the structure ofother public and corporate pensionplan assets and therefore allows formore meaningful comparison withother pension fund investors. Thecomparison universe used by the SBIis the Master Trust portion of theTrust Universe Comparison Service(TUCS). This universe containsinformation on public and corporatepension and trust funds with abalanced asset mix and over$1 billion in size.

It is important to note that thehistorical data on the CombinedFunds presented in this reportreflect only the Basic RetirementFunds through fiscal year 1993.Both the Basic and Post Funds areincluded thereafter.

This distinction is necessary due tothe very different asset allocationstrategies employed by the two fundsin the past. The Basic Funds havealways been managed to maximizetotal rates of return over the long-term and, therefore, its assetallocation has historically included asubstantial stock segment. Incontrast, until the post retirementbenefit increase formula was changedin 1993, the Post Retirement Fundwas managed to maximize currentincome which necessitated a largecommitment to bonds. As a result,the investment goals of the two fundswere incompatible for analyticalpurposes until fiscal year 1994.

Combined Funds

Cumulative Returns

0

100

200

300

400

500

Jun-

94

Dec

-94

Jun-

95

Dec

-95

Jun-

96

Dec

-96

Jun-

97

Dec

-97

Jun-

98

Dec

-98

Jun-

99

Dec

-99

Jun-

00

Dec

-00

Jun-

01

Dec

-01

Jun-

02

Dec

-02

Jun-

03

Dec

-03

Jun-

04

Percent

U.S. Stocks Cash Equivalents Consumer Price Index U.S. Bonds Int'l. Stocks

Figure 1. Performance of Capital Markets -FY 1995-2004

6

MedianCombined Allocation Funds in TUCS*

Domestic Equity 49.7% 47.5%International Equity 15.3 12.6Bonds 22.8 26.2Alternatives** 8.6 5.8Cash 3.6 4.7

* Represents the median allocation by asset class, and does not add to 100%. ** TUCS may include assets other than alternatives.

Combined Funds

Asset Allocation

As illustrated in Figure 1 on the priorpage, historical evidence stronglyindicates that U.S. common stockswill provide the greatest opportunityto maximize investment returns overthe long-term. As a result, the Boardhas chosen to incorporate a largecommitment to common stocks in itsasset allocation policy for theretirement funds. In order to limit theshort run volatility of returnsexhibited by common stocks, theBoard includes other asset classessuch as bonds, real estate, andresource investments in the totalportfolio. These assets diversify theFunds and reduce wide fluctuationsin investment returns on a year toyear basis. This diversificationshould not impair the Funds’ abilityto meet or exceed their actuarialreturn targets over the long-term.

Asset Mix Compared toOther Pension FundsComparisons of the CombinedFunds’ actual asset mix to themedian allocation to stocks, bondsand other assets of the funds inTUCS on June 30, 2004 aredisplayed in Figure 2.

It shows that the Combined Fundswere overweighted in domesticequities, international equities, andalternative investments relative to themedian allocation in TUCS andunderweighted in their allocation tobonds. Historical data on theCombined Funds’ asset mix is shownin Figure 3.

Return Objectives

The Combined Funds are evaluatedrelative to the following total rate ofreturn objectives:

—Provide Real Returns. Over atwenty year period, the CombinedFunds are expected to producereturns that exceed inflation by3-5 percentage points on anannualized basis.

010

20304050

607080

901 00

Ju n -0 0 Jun - 0 1 Ju n -0 2 Ju n -0 3 Jun - 0 4

Per

cent

A lt. A s s e ts

Ca s h

B o n d s

In t'l. S to c ks

Do m. S toc ks

Fig u re 3 . Co mb in e d Fu n d s His to r ic a l A s s e t Mix FY 2 0 0 0 -2 0 0 4

0

10

20

30

40

50

60

Dom. Eq . Int 'l Eq. Bonds Alternatives Cash

Per

cent

Combined Funds

TUCS Median

Figure 2. Combined Funds A s s et Mix Compar is on as of June 30, 2004

�

��� ��+��$�,�� &�,�� -�,�� $.�,��

���������9�����6���������5��$�����1��G &<�� ?<�� <&�� (*��

�G����������������������������������"����������;%�������#�"�����������

Combined Funds

H������������������������������I�������������������#�����������9����������.��������������.������������������$����������!��"��������"����������.��������������9�����

Investment Results

Comparison to InflationI�����������!���������#�����������9������.�����������������<�%��������"������#��������!��������.�����������������0����������������>�������������������������������������!����9�"����,�

Comparison to Other Funds/��������� ��������������!���!������������������������������������#������������������������������������!��"��������������������!���������������!������������������!�������������J������44���"��K��$������������:

�H��������� ���������������������������������������������������������������$�����"��������������1��������������"�������-)4*)E#�������!�������"�����������"����������������������#�������������������������������������������������������"�����������������1���������������������������������"�������

H����������� ����� �����=����������������������������������������!�������������������$���������������������������������������������������.���������������.�!������"���������������������������#���������������$��"��������������������������������!�!������������������������"������"4���������������

��� ��+��$�,�� &�,�� -�,�� $.�,�� /.�,��

���������" ���* %(�'0 &�%0 -�-0 *�(0 $$�/0��������� &�& -�% -�? -�' &�%

����������� �����9������������"��(2&)2*&#� ���������6������9��������������

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1 Y r. 3 Y r. 5 Y r. 10 Y r. 20 Y r.

Per

cent

CombinedFunds*

Inf lation

F ig u r e 4 . Co m b in e d Fu n d s Pe r f o r m a n c e v s . In f la t io n

0

25

50

75

100

Median

CombinedFunds Rank*

1 Yr. 3 Yr. 5 Yr. 10 Yr.

Figu r e 5 . Co mb ine d Funds Pe r f o rmanc e Compared to O the r Pens ion Fun ds

������������1�����'��������������2 ���&.3�/..4

��5� ������������������ �����1 ������1�6��*

�7��������$� 5�������&))) ')�)E

���3�����$� �������/��9�����.��1��� %'�)

�7������ ��� A�������""��"�� -,�'

�������������������� ������������������� <�'

�1������������� &������4 ���� -�)

���� %))�)E

���G�/��"������������������������������������������������������������������������������������������� ���������6��9�����

��� ��+��$�,�� &�,�� -�,�� $.�,��

��������" ���* $7�-0 &�$0 /�/0 %�70�����������. %(�) &�- -�% *�,

Combined Funds

/���������������������������#��������������������������9������������������������������������������������!������;%�����������������������������������������1������������������9�"����'����������������"������!����������������9������������$������!�����������������������������������

Comparison to Market Returns������������9����3�������������������������������������������������$����������!�������!��"������������������������������������������������������������9������6��������������������������$�!�����������������.�������!����9�"����(��������������9�����.���������������������.����)�-�������"����������������������������#��������#������������������������"��������9�����.���������������������.�������������������������)�%��������"����#��������)�'��������"�����������������������������������������������������"���������������������������������������������"�����������������������.������������������$����������������

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1 Yr. 3 Yr. 5 Yr. 10 Yr.

Per

cent

CombinedFunds*

CompositeIndex

Figu re 6 . Comb ined Fun ds Pe r f o rmanc e v s . Comp os ite Inde x

9

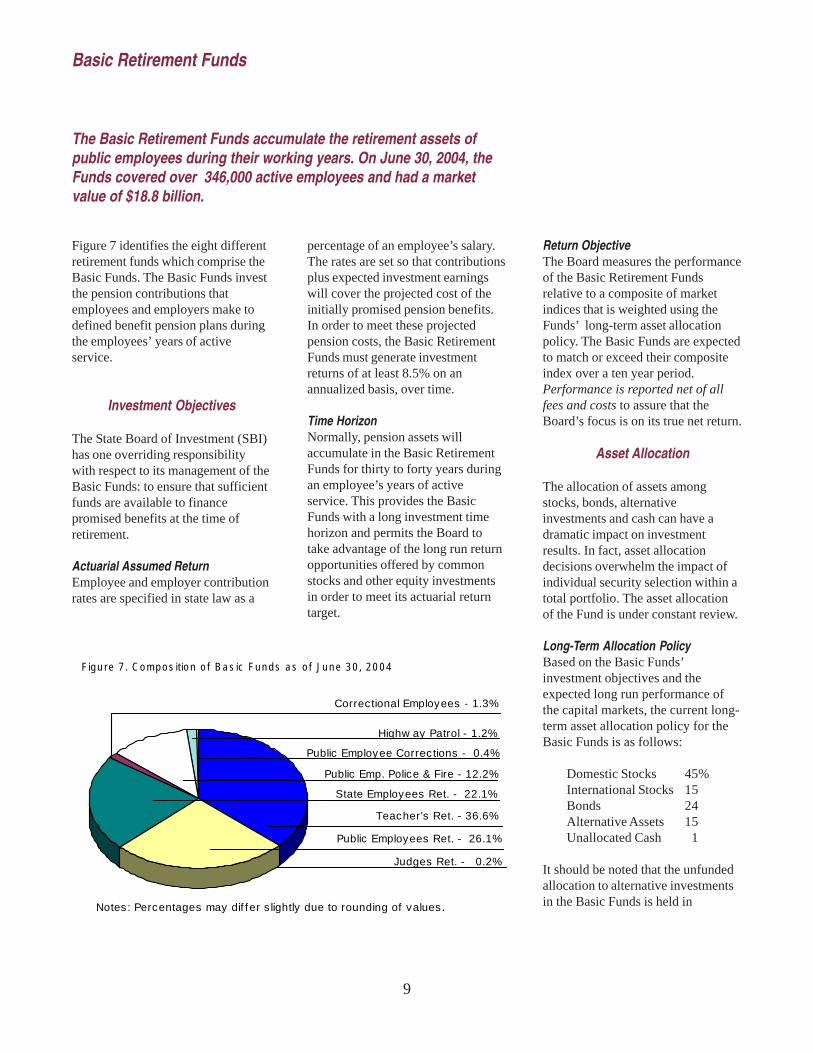

Figure 7 identifies the eight differentretirement funds which comprise theBasic Funds. The Basic Funds investthe pension contributions thatemployees and employers make todefined benefit pension plans duringthe employees’ years of activeservice.

Investment Objectives

The State Board of Investment (SBI)has one overriding responsibilitywith respect to its management of theBasic Funds: to ensure that sufficientfunds are available to financepromised benefits at the time ofretirement.

Actuarial Assumed ReturnEmployee and employer contributionrates are specified in state law as a

The Basic Retirement Funds accumulate the retirement assets ofpublic employees during their working years. On June 30, 2004, theFunds covered over 346,000 active employees and had a marketvalue of $18.8 billion.

percentage of an employee’s salary.The rates are set so that contributionsplus expected investment earningswill cover the projected cost of theinitially promised pension benefits.In order to meet these projectedpension costs, the Basic RetirementFunds must generate investmentreturns of at least 8.5% on anannualized basis, over time.

Time HorizonNormally, pension assets willaccumulate in the Basic RetirementFunds for thirty to forty years duringan employee’s years of activeservice. This provides the BasicFunds with a long investment timehorizon and permits the Board totake advantage of the long run returnopportunities offered by commonstocks and other equity investmentsin order to meet its actuarial returntarget.

Return ObjectiveThe Board measures the performanceof the Basic Retirement Fundsrelative to a composite of marketindices that is weighted using theFunds’ long-term asset allocationpolicy. The Basic Funds are expectedto match or exceed their compositeindex over a ten year period.Performance is reported net of allfees and costs to assure that theBoard’s focus is on its true net return.

Asset Allocation

The allocation of assets amongstocks, bonds, alternativeinvestments and cash can have adramatic impact on investmentresults. In fact, asset allocationdecisions overwhelm the impact ofindividual security selection within atotal portfolio. The asset allocationof the Fund is under constant review.

Long-Term Allocation PolicyBased on the Basic Funds’investment objectives and theexpected long run performance ofthe capital markets, the current long-term asset allocation policy for theBasic Funds is as follows:

Domestic Stocks 45%International Stocks 15Bonds 24Alternative Assets 15Unallocated Cash 1

It should be noted that the unfundedallocation to alternative investmentsin the Basic Funds is held in

Basic Retirement Funds

F ig u r e 7 . C o m p o s it io n o f B a s ic Fu n d s a s o f Ju n e 3 0 , 2 0 0 4

Correctional Employees - 1.3%

Highw ay Patrol - 1.2%

Teacher's Ret. - 36.6%

Public Emp. Police & Fire - 12.2%

State Employees Ret. - 22.1%

Public Employees Ret. - 26.1%

Judges Ret. - 0.2%

Public Employee Corrections - 0.4%

Notes: Percentages may dif f er s lightly due to rounding of values.

10

domestic stocks until it is needed forinvestment. As a result, the actualamount invested in domestic stockswas above its long-term target.

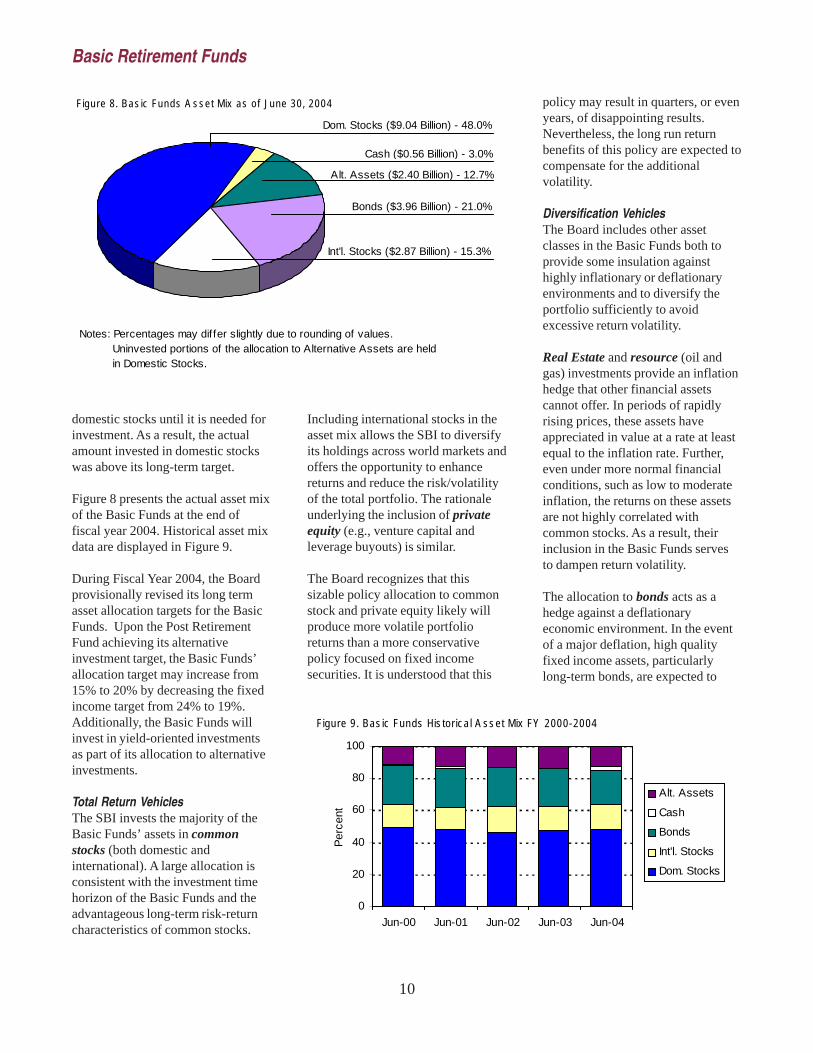

Figure 8 presents the actual asset mixof the Basic Funds at the end offiscal year 2004. Historical asset mixdata are displayed in Figure 9.

During Fiscal Year 2004, the Boardprovisionally revised its long termasset allocation targets for the BasicFunds. Upon the Post RetirementFund achieving its alternativeinvestment target, the Basic Funds’allocation target may increase from15% to 20% by decreasing the fixedincome target from 24% to 19%.Additionally, the Basic Funds willinvest in yield-oriented investmentsas part of its allocation to alternativeinvestments.

Total Return VehiclesThe SBI invests the majority of theBasic Funds’ assets in commonstocks (both domestic andinternational). A large allocation isconsistent with the investment timehorizon of the Basic Funds and theadvantageous long-term risk-returncharacteristics of common stocks.

Including international stocks in theasset mix allows the SBI to diversifyits holdings across world markets andoffers the opportunity to enhancereturns and reduce the risk/volatilityof the total portfolio. The rationaleunderlying the inclusion of privateequity (e.g., venture capital andleverage buyouts) is similar.

The Board recognizes that thissizable policy allocation to commonstock and private equity likely willproduce more volatile portfolioreturns than a more conservativepolicy focused on fixed incomesecurities. It is understood that this

policy may result in quarters, or evenyears, of disappointing results.Nevertheless, the long run returnbenefits of this policy are expected tocompensate for the additionalvolatility.

Diversification VehiclesThe Board includes other assetclasses in the Basic Funds both toprovide some insulation againsthighly inflationary or deflationaryenvironments and to diversify theportfolio sufficiently to avoidexcessive return volatility.

Real Estate and resource (oil andgas) investments provide an inflationhedge that other financial assetscannot offer. In periods of rapidlyrising prices, these assets haveappreciated in value at a rate at leastequal to the inflation rate. Further,even under more normal financialconditions, such as low to moderateinflation, the returns on these assetsare not highly correlated withcommon stocks. As a result, theirinclusion in the Basic Funds servesto dampen return volatility.

The allocation to bonds acts as ahedge against a deflationaryeconomic environment. In the eventof a major deflation, high qualityfixed income assets, particularlylong-term bonds, are expected to

Basic Retirement Funds

0

20

40

60

80

100

Jun-00 Jun-01 Jun-02 Jun-03 Jun-04

Per

cent

Alt. Assets

Cash

Bonds

Int'l. Stocks

Dom. Stocks

Figure 9 . Bas ic Funds His tor ic a l A s s et Mix FY 2000-2004

Figure 8. Bas ic Funds A s s et Mix as o f June 30 , 2004

Notes: Percentages may differ slightly due to rounding of values. Uninvested portions of the allocation to Alternative Assets are held in Domestic Stocks.

Dom. Stocks ($9.04 Billion) - 48.0%

Cash ($0.56 Billion) - 3.0%

Alt. Assets ($2.40 Billion) - 12.7%

Int'l. Stocks ($2.87 Billion) - 15.3%

Bonds ($3.96 Billion) - 21.0%

11

protect principal and generatesignificant capital gains. Bonds, likereal estate and resource funds, undernormal financial conditions, help todiversify the Basic Funds, therebycontrolling return volatility.

Yield oriented alternativeinvestments provide the opportunityfor higher long term returns thanthose typically available from bondsyet still generate sufficient currentincome. Typically, these investments(e.g., subordinated debt, mezzanineor resource income investments suchas producing properties) arestructured more like fixed incomesecurities with the opportunity toparticipate in the appreciation of theunderlying assets. While theseinvestments may have an equitycomponent, they display a returnpattern more like a bond. As such,they will help reduce the volatility ofthe total portfolio, but should alsogenerate higher returns relative tomore traditional bond investments.

Investment Management

All assets in the Basic RetirementFunds are managed externally byoutside money management firmsretained by contract. In order to gaingreater operating efficiency, theBasic Funds share the same domesticstock, international stock, fixedincome, and alternative investmentmanagers with the Post Fund.

More information on the structure,management and performance ofthese pools of managers is includedin the Investment Pool section ofthis report.

Investment Performance

As stated earlier, the Basic Funds areexpected to match or exceed thereturn of a composite of marketindices over a ten year period.Performance relative to this standardwill measure two effects:

Annualized2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Basic Funds 10.5% -7.4% -8.2% 1.9% 16.6% 3.0% 2.3% 9.8% Composite Index 10.6 -8.4 -8.1 2.4 16.3 3.0 2.1 9.6

Basic Retirement Funds

— The ability of the managersselected by the SBI, in aggregate,to add value to the returnsavailable from the broad capitalmarkets.

— The impact of the SBI’s re-balancing activity. The SBIrebalances the total fund whenmarket movements take the stock(domestic and international),bond, or cash segments above orbelow long term asset allocationtargets. This policy imposes alow risk discipline of “buy low-sell high” between asset classeson a total fund basis.

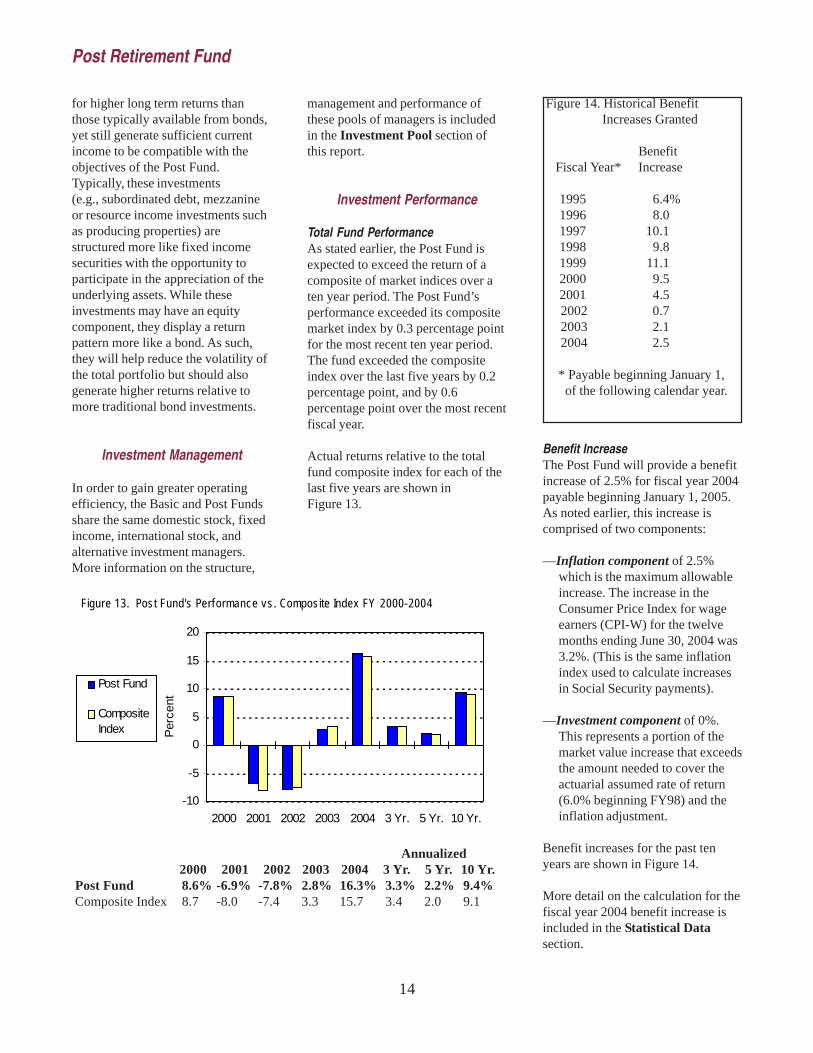

For the ten year period endingJune 30, 2004, the Basic Fundsoutperformed the composite index by0.2 percentage point annualized. TheFund exceeded the composite indexby 0.2 percentage point over the lastfive years, and by 0.3 percentagepoint over the most recent fiscal year.Actual returns relative to the totalfund composite index for each of thelast five years are shown inFigure 10.

-10

-5

0

5

10

15

20

2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Per

cent

Basic Funds

Composite

Figure 10 . Bas ic Funds ' Per f ormanc e v s . Compos ite Index FY 2000-2004

12

The Post Retirement Fund includesthe assets of retired public employeescovered by nine statewide retirementplans; the eight plans whichparticipate in the Basic RetirementFunds as well as the Legislative andSurvivors Retirement Fund.

Benefit Increase Formula

The retirement benefit increaseformula of the Post Retirement Fundis based on a combination of twocomponents:

— Inflation Component. Each year,retirees receive an inflation-basedadjustment equal to 100% ofinflation, up to a maximumspecified in statute. The inflationcomponent is granted regardlessof investment performance. Thecap is necessary to maintain theactuarial soundness of the entireplan. It is the difference betweenthe return assumption for theBasic Funds, and the returnassumption for the Post Fund.

The return assumption in theBasic Funds is 8.5%. The returnassumption for the Post Fund was5.0% through fiscal year 1997. Infiscal year 1998, the returnassumption for the Post Fund waschanged to 6.0%. This means thecap on the inflation adjustmentwas 3.5% for fiscal years 1993-1997. Since fiscal year 1998, theinflation cap has been 2.5%.

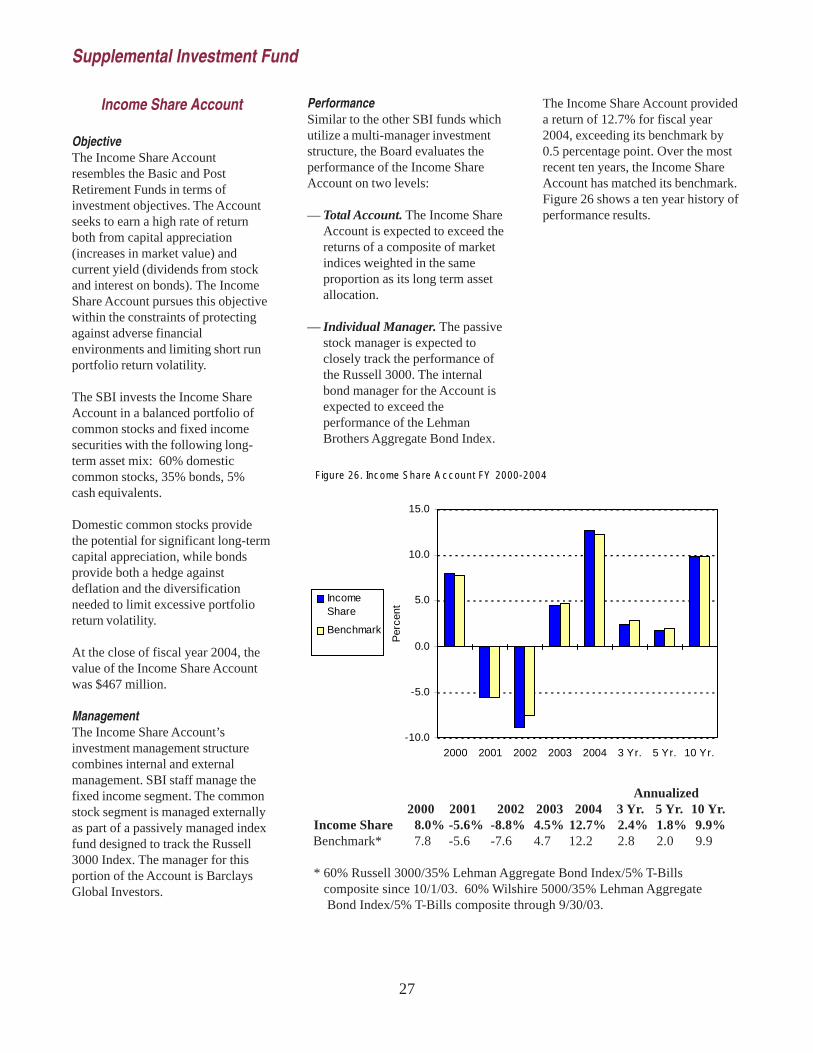

The assets of the Post Retirement Fund are used to finance monthlyannuities to retired public employees. These annuities may beadjusted upwards over the life of a retiree based on a formula thatreflects both inflation and investment performance. On June 30, 2004,the Post Fund had a market value of $18.4 billion and more than121,000 retiree participants.

Retirees were given a one timepermanent adjustment in theirpension to compensate them forthe reduction in the inflationadjustment cap.

— Investment Component. Eachyear, retirees can also receive aninvestment-based adjustment,provided net investment gains areabove the amount needed tofinance the Post Fund’s actuarialassumption and the inflationadjustment. Investment gains andlosses are spread over five yearsto smooth out the volatility ofreturns. In addition, allaccumulated investment losses

must be recovered before aninvestment-based adjustment isgranted.

Investment Objective

Time HorizonThe time horizon of the Post Fund is15 to 20 years and corresponds to thelength of time a typical retiree can beexpected to draw benefits. While thisis shorter than the time horizon of theBasic Funds, it is still sufficientlylong to allow the Board to takeadvantage of the long run returnopportunities offered by commonstocks in order to meet its actuarialreturn target as well as to financeretirement benefit increases.

Post Retirement Fund

Figure 11. Pos t Fund A s s et Mix as o f June 30 , 2004

Notes: Percentages may dif fer slightly due to rounding of values. Uninvested portions of the Alternative Assets allocation are held in Bonds.

Alt. Assets ($0.79 Billion) - 4.3%

Bonds ($4.53 Billion) - 24.6%

Dom. Stocks ($9.48 Billion) - 51.4%

Int'l. Stocks ($2.85 Billion) - 15.5%

Cash ($0.78 Billion) - 4.2%

13

Return ObjectiveThe Board measures the performanceof the Post Retirement Fund relativeto a composite of market indicesusing its long-term asset allocationpolicy. The Post Fund is expected tomatch or exceed its composite indexover a ten year period. Performanceis reported net of all fees and costs toassure that the Board’s focus is ontrue net return.

Asset Allocation

The current long-term assetallocation for the Post Fund is asfollows:

Domestic Stocks 45%Int’l. Stocks 15Bonds 25Alternative Assets 12Unallocated Cash 3

The Post Fund’s year-end asset mixis presented in Figure 11 on theprevious page. Historical asset mixdata are shown in Figure 12.

The SBI invests the majority of thePost Fund’s assets in common stocks(both domestic and international). Alarge allocation is consistent with themoderately long time horizon of thePost Fund and the advantageous longterm risk-return characteristics ofcommon stocks. Includinginternational stocks in the asset mixallows the SBI to diversify itsholdings across world markets andoffers the opportunity to enhancereturns and reduce the risk/volatilityof the total portfolio.

As with the Basic Funds, the Boardrecognizes that this sizable allocationwill be likely to produce morevolatile portfolio returns than a moreconservative policy focused on fixedincome securities. It is understoodthat this policy may result inquarters, or even years, ofdisappointing results. Nevertheless,the long run return benefits of thispolicy are expected to compensatefor the additional volatility. The assetallocation is under constant review.During Fiscal Year 2004, the SBIrevised its long term asset allocationtargets for the Post Fund. The

allocation target for alternativeinvestments was increased from 5%to 12%, while decreasing domesticequity from 50% to 45% anddecreasing fixed income from 27%to 25%. Additionally, the Post Fundwill invest in private equity, realestate, and resource investments aswell as yield-oriented investments aspart of its allocation to alternativeinvestments.

Diversified VehiclesThe Board includes other assetclasses in the Post Fund both toprovide some insulation againsthighly deflationary environments andto diversify the portfolio sufficientlyto avoid excessive return volatility.Including private equity in the PostFund is intended to enhance returnsand reduce the risk of the totalportfolio.

Real Estate and resource (oil andgas) investments provide an inflationhedge that other financial assetscannot offer. In periods of rapidlyrising prices, these assets haveappreciated in value at a rate at leastequal to the inflation rate. Further,even under more normal financialconditions, such as low to moderateinflation, the returns on these assetsare not highly correlated withcommon stocks. As a result, theirinclusion in the Post Fund also servesto dampen return volatility.

The bonds in the Post Fund act as ahedge against a deflationaryeconomic environment. In the eventof a major deflation, high qualityfixed income assets, particularly longterm bonds, are expected to protectprincipal and generate significantgains. And, under more normalfinancial conditions, bonds diversifythe Post Fund, thereby controllingreturn volatility on a year-to-yearbasis.

Yield oriented alternativeinvestments provide the opportunity

Post Retirement Fund

0

10

20

30

40

50

60

70

80

90

100

Jun-00 Jun-01 Jun-02 Jun-03 Jun-04

Per

cent

A lt. Assets

Cash

Bonds

Int'l. Stocks

Dom. Stocks

Fig u r e 1 2 . Po s t Fu n d His to r ic a l A s s e t M ix FY 2 0 0 0 - 2 0 0 4

14

for higher long term returns thanthose typically available from bonds,yet still generate sufficient currentincome to be compatible with theobjectives of the Post Fund.Typically, these investments(e.g., subordinated debt, mezzanineor resource income investments suchas producing properties) arestructured more like fixed incomesecurities with the opportunity toparticipate in the appreciation of theunderlying assets. While theseinvestments may have an equitycomponent, they display a returnpattern more like a bond. As such,they will help reduce the volatility ofthe total portfolio but should alsogenerate higher returns relative tomore traditional bond investments.

Investment Management

In order to gain greater operatingefficiency, the Basic and Post Fundsshare the same domestic stock, fixedincome, international stock, andalternative investment managers.More information on the structure,

management and performance ofthese pools of managers is includedin the Investment Pool section ofthis report.

Investment Performance

Total Fund PerformanceAs stated earlier, the Post Fund isexpected to exceed the return of acomposite of market indices over aten year period. The Post Fund’sperformance exceeded its compositemarket index by 0.3 percentage pointfor the most recent ten year period.The fund exceeded the compositeindex over the last five years by 0.2percentage point, and by 0.6percentage point over the most recentfiscal year.

Actual returns relative to the totalfund composite index for each of thelast five years are shown inFigure 13.

Benefit IncreaseThe Post Fund will provide a benefitincrease of 2.5% for fiscal year 2004payable beginning January 1, 2005.As noted earlier, this increase iscomprised of two components:

—Inflation component of 2.5%which is the maximum allowableincrease. The increase in theConsumer Price Index for wageearners (CPI-W) for the twelvemonths ending June 30, 2004 was3.2%. (This is the same inflationindex used to calculate increasesin Social Security payments).

—Investment component of 0%.This represents a portion of themarket value increase that exceedsthe amount needed to cover theactuarial assumed rate of return(6.0% beginning FY98) and theinflation adjustment.

Benefit increases for the past tenyears are shown in Figure 14.

More detail on the calculation for thefiscal year 2004 benefit increase isincluded in the Statistical Datasection.

Figure 14. Historical Benefit Increases Granted

Benefit Fiscal Year* Increase

1995 6.4% 1996 8.0 1997 10.1 1998 9.8 1999 11.1 2000 9.5 2001 4.5

2002 0.72003 2.12004 2.5

* Payable beginning January 1, of the following calendar year.

Annualized2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Post Fund 8.6% -6.9% -7.8% 2.8% 16.3% 3.3% 2.2% 9.4% Composite Index 8.7 -8.0 -7.4 3.3 15.7 3.4 2.0 9.1

Post Retirement Fund

-10

-5

0

5

10

15

20

2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Per

cent

Post Fund

CompositeIndex

Figure 13. Post Fund's Perf ormance vs. Composite Index FY 2000-2004

15

The Basic Retirement Funds, PostRetirement Fund and SupplementalInvestment Fund share many of thesame stock and bond managers. Thisis accomplished by groupingmanagers together, by asset class,into several Investment Pools. Theindividual funds participate in theInvestment Pools by purchasing“units” which function much likeshares of a mutual fund.

This investment managementstructure allows the State Board ofInvestment (SBI) to gain greateroperating efficiency within assetclasses and to keep managementcosts as low as possible for allparticipants.

DomesticStock Pool

The Basic Retirement Funds haveparticipated in the Domestic StockPool since its inception in January1984. The Post Retirement Fund hasparticipated in the Pool since July1993. In addition, the Growth ShareAccount, Common Stock IndexAccount, and the stock portion of theIncome Share Account in theSupplemental Investment Fund haveutilized a portion of the Pool.

As of June 30, 2004, the dollar valueof each fund’s participation in thePool was:

Basic Funds $9.0 billion(active, passive and semi-passive)

To gain greater operating efficiency, external managers are groupedinto several “Investment Pools” which are segregated by asset class.The various retirement funds participate in one or more of the poolscorresponding to their individual asset allocation strategies.

Post Fund $9.5 billion(active, passive and semi-passive)

Growth ShareAccount $134 million(active and semi-passive)

Common StockIndex Account $192 million(passive)

Stock portion ofthe Income ShareAccount $289 million(passive)

Management StructureThe SBI uses a three-part approachto the management of the DomesticStock Pool:

— Active Management. At the endof fiscal year 2004, approximately33% of the Domestic Stock Poolwas actively managed by a groupof external money managers. Theassets allocated to each of themanagers ranged from $30 to$900 million. The activelymanaged segment of the Poolincludes managers in the SBI’sEmerging Manager Program.Generally, firms designated asEmerging Managers by the SBIare smaller organizations ormanaging newer products than thelarger active domestic equitymanagers in the Domestic StockPool.

— Semi-Passive Management. Atthe end of fiscal year 2004,approximately 33% of theDomestic Stock Pool was

managed by a group of threesemi-passive external moneymanagers with portfolios rangingfrom $1.8 to $2.5 billion.

— Passive Management. At the endof fiscal year 2004, approximately34% of the Stock Pool wasmanaged passively by a singlemanager with a portfolio of$6.5 billion.

The goal of the Domestic Stock Poolis to add value to the asset classtarget which is the Russell 3000Index since October 1, 2003. TheRussell 3000 Index can besegmented into sub-indexes orRussell style indexes. Each activemanager is expected to addincremental value over the long runrelative to a Russell style indexwhich reflects its investmentapproach or style.

Assets are allocated to managerswithin each Russell style index in thesame proportion as the Russell 3000Index. This is done to minimize themisfit or style bias that the DomesticStock Pool may experience.

Prior to October 1, 2003, theperformance of active managers inthe Domestic Stock Pool wasmeasured against customizedbenchmarks which reflected themanager’s unique investmentapproach or style. This type ofactive manager structure could resultin misfit or style bias. “Misfit” isdefined as the difference between theaggregate benchmarks of the activemanagers and the asset class targets.

Investment Pools

16

The SBI attempted to compensate foractive manager misfit through the useof a completeness fund. A“completeness fund” is so namedbecause it is intended to fill in, orcomplete, any areas of marketexposure that are not being coveredby the aggregate benchmarks of theactive managers. The completenessfund has not been used sinceDecember 31, 2003. Since that time,the SBI has attempted to controlmisfit by allocating assets on thebasis of managers’ investment styleindexes.

The SBI’s completeness fund waspassively managed when it was firstintroduced in October 1990 untilDecember 1994. During fiscal year1995, the completeness fund movedfrom being entirely passivelymanaged to a structure that was halfpassive/half semi-passive. At the startof fiscal year 1996, the completenessfund was allocated entirely to semi-passive management. Semi-passiveapproaches provide the potential tooutperform the completeness fundbenchmark, but also incorporateprocedures that constrain the level ofrisk/volatility relative to thebenchmark.

During fiscal year 1997, severalcurrent active managers modifiedtheir investment processes in order toincrease the probability of producingvalue added in their portfolios.Three managers (Alliance CapitalMgmt., Franklin Portfolio Assoc.,and Oppenheimer Capital) wereasked to increase the level of activerisk in their portfolio resulting in areduction in the number of issuesheld at any one time. During fiscalyear 2000, Brinson (now UBSGlobal Asset Mgmt.) was asked toeliminate investments in small post-venture companies (about 7% oftheir portfolio) and to increase theactive risk in their portfolio as well.In effect, these managers now hold

more concentrated portfolios andmake larger bets on their “best”stock ideas.

A description of each domestic stockmanager’s investment approach isincluded in the InvestmentManager Summaries section.

FY 2004 ChangesDuring fiscal year 2004, there wereseveral changes made to theDomestic Stock Pool. The Boardretained nine new active managers: • Barrow, Hanley, Mewhinney &

Strauss, Inc. • Lord Abbett & Co. LLC • LSV Asset Management; • Systematic Financial Mgmt., L.P. • McKinley Capital Management • Turner Investment Partners • Goldman Sachs Asset Mgmt. • Hotchkis & Wiley Capital Mgmt. • Martingale Asset Management;

and two emerging managers: • Kenwood Capital Management/

American Express Asset Mgmt. • U.S. Bancorp Asset Management.

The Board also terminatedinvestment management relationshipswith three active managers: • FLA Asset Management, LLC • GeoCapital Corporation • Lincoln Equity Mgmt., LLC;

and three emerging managers: • Artemis Investment Mmgt. LLC • Valenzuela Capital Partners, LLC • U.S. Bancorp Asset Management.

Investment PerformanceA comprehensive monitoring systemhas been established to ensure thatthe many elements of the DomesticStock Pool conform to the SBI’sinvestment policies. Publishedperformance benchmarks are usedfor each active, emerging and semi-passive stock manager. Thesebenchmarks enable the SBI toevaluate the managers’ results, bothindividually and in aggregate, withrespect to risk incurred and returnsachieved.

Investment Pools

Annualized2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Stock Pool 8.2% -15.2% -18.0% 0.4% 20.3% -0.3% -1.9% 10.9% Domestic 8.6 -15.8 -17.3 0.8 20.6 0.2 -1.7 11.2 Equity Asset Class Target

* Reflects Wilshire 5000 as reported prior to FY 2000, the Wilshire 5000 Investable from 7/1/2000 thru 9/30/03; and the Russell 3000 since 10/1/2003.

-20

-15

-10

-5

0

5

10

15

20

25

2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Per

cent

Stock Pool

Asset ClassTarget

Figure 15 . Domes tic Stoc k Poo l Per f ormanc e FY 2000-2004

17

Two primary long run risk objectiveshave been established for thedomestic stock managers:

— Investment Approach. Eachmanager (active, emerging, semi-passive, or passive) is expected tohold a portfolio that is consistent,in terms of risk characteristics,with the manager’s statedinvestment approach. In the shortrun, the active stock managersmay depart from their risk targetsas part of their specific investmentstrategies.

— Diversification. The passive andsemi-passive managers areexpected to hold highlydiversified portfolios, while eachactive domestic stock manager isexpected to hold a less diversifiedportfolio.

The domestic stock managerssuccessfully fulfilled their long-termrisk objectives during fiscal year2004. In general, the managersconstructed portfolios consistent withtheir stated investment approachesand maintained levels ofdiversification that were appropriateto their respective active, semi-passive and passive approaches.

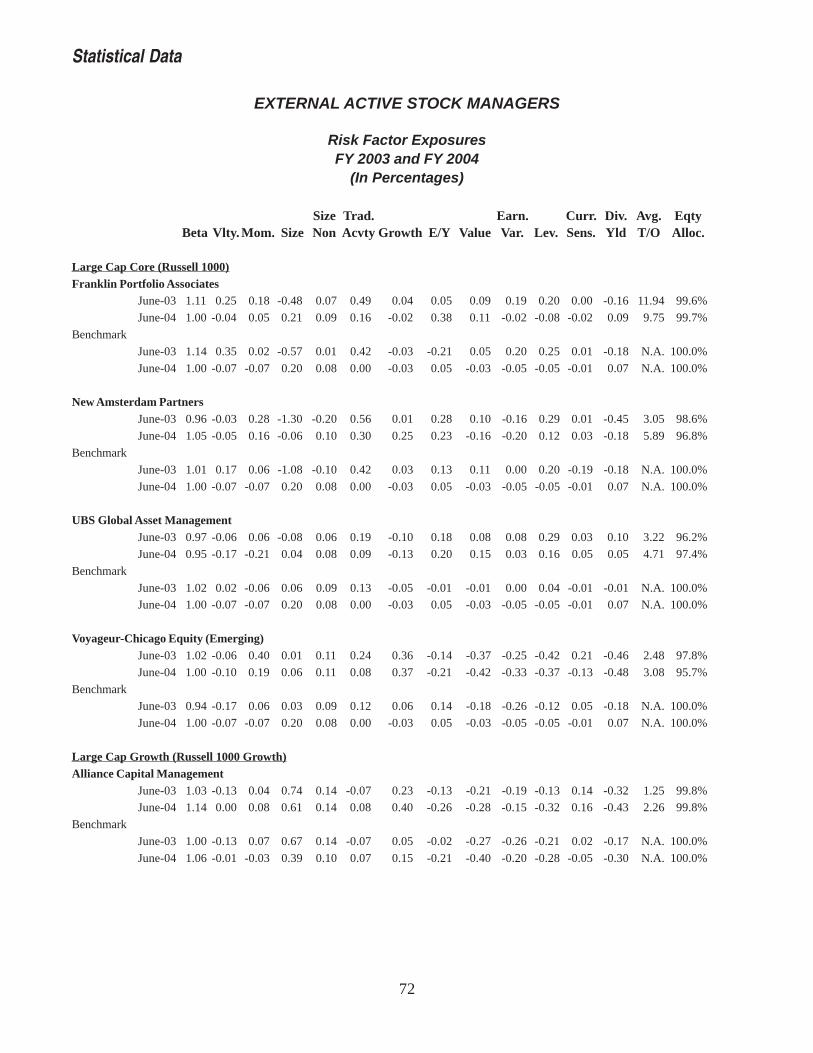

The Board’s return objectives for itsactive and semi-passive stockmanagers are measured against theperformance of published Russellstyle indices that represent amanager’s specific investmentapproach. This index is commonlyreferred to as a “benchmarkportfolio.” A benchmark portfoliotakes into account the equity marketforces that at times favorably orunfavorably impact certaininvestment styles. Thus, a Russellstyle index or benchmark is a moreappropriate return target againstwhich to judge a manager’sperformance than a broad marketindex.

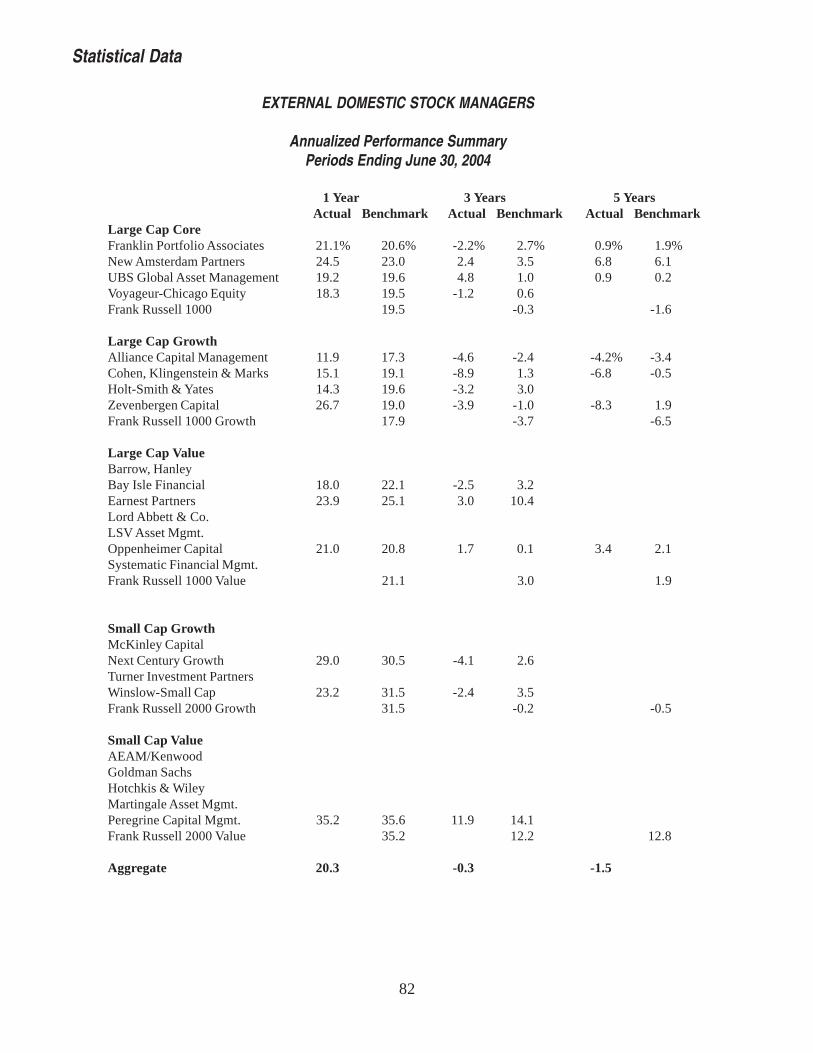

Figure 16. Domestic Stock Manager Performance FY 2004

Actual BenchmarkReturn Return

Active Managers Large Cap Core (Russell 1000) Franklin Portfolio Associates 21.1% 20.6% New Amsterdam Partners 24.5 23.0 UBS Global Asset Management 19.2 19.6 Voyageur-Chicago Equity (Emerging) 18.3 19.5

Large Cap Growth (Russell 1000 Growth) Alliance Capital Management 11.9 17.3 Cohen Klingenstein & Marks 15.1 19.1 Holt-Smith & Yates (Emerging) 14.3 19.6 Zevenbergen Capital (Emerging) 26.7 19.0

Large Cap Value (Russell 1000 Value) Barrow, Hanley* 2.7 0.9 Bay Isle Financial (Emerging) 18.0 22.1 Earnest Partners (Emerging) 23.9 25.1 Lord Abbett & Co.* 1.7 0.9 LSV Asset Mgmt.* 2.0 0.9 Oppenheimer Capital 21.0 20.8 Systematic Financial Mgmt.* 1.2 0.9

Small Cap Growth (Russell 2000 Growth) McKinley Capital** 4.0 5.7 Next Century Growth (Emerging) 29.0 30.5 Turner Investment Partners** 4.6 5.7 Winslow-Small Cap (Emerging) 23.2 31.5

Small Cap Value (Russell 2000 Value) AEAM/Kenwood (Emerging)** 10.6 7.8 Goldman Sachs** 5.2 7.8 Hotchkis & Wiley** 11.0 7.8 Martingale Asset Mgmt.** 12.3 7.8 Peregrine Capital Mgmt. (Emerging)** 35.2 35.6

Semi-Passive Managers (Russell 1000) Barclays Global Investors 20.2 19.5 Franklin Portfolio Associates 19.1 19.5 J.P. Morgan Investment Mgmt. 19.5 19.5

Passive Manager (Russell 3000) Barclays Global Investors 20.5 20.6

Historical Aggregate 20.3 20.5

SBI Domestic Equity Asset Class Target 20.6

* Manager was retained April 1, 2004. ** Manager was retained January 1, 2004.

Investment Pools

18

Individual active managers areexpected to exceed their benchmarkby 0.50-1.00 percentage pointannualized, over time. The semi-passive managers are expected toexceed their benchmark by 0.15-0.30percentage point, over time, and thepassive manager is expected to trackits index within 0.10 percentagepoint annualized, over time.

In aggregate, the Domestic StockPool underperformed the Russell3000 Index by 0.3 percentage pointfor the fiscal year. The active andpassive component underperformedtheir respective benchmarks, whilethe semi-passive componentoutperformed. Relative to theiraggregate benchmarks, the activemanager group’s underperformancewas due to a small cash holding,negative security selection, and aslight overweight in technologystocks, which performed poorly. Thesemi-passive managers outperformeddue to good security selection. Thepassive segment tracked the indexduring the year. Figure 15 providesmore detail on the historicalperformance of the entire pool.Individual manager performancerelative to their respectivebenchmarks was disappointing.Eleven active managersoutperformed their benchmarks whilethirteen underperformed. One semi-passive manager outperformed, onematched, and one underperformedthe benchmark. The passive managertrailed its target, the Russell 3000index. Individual managerperformance for fiscal year 2004 isshown in Figure 16.

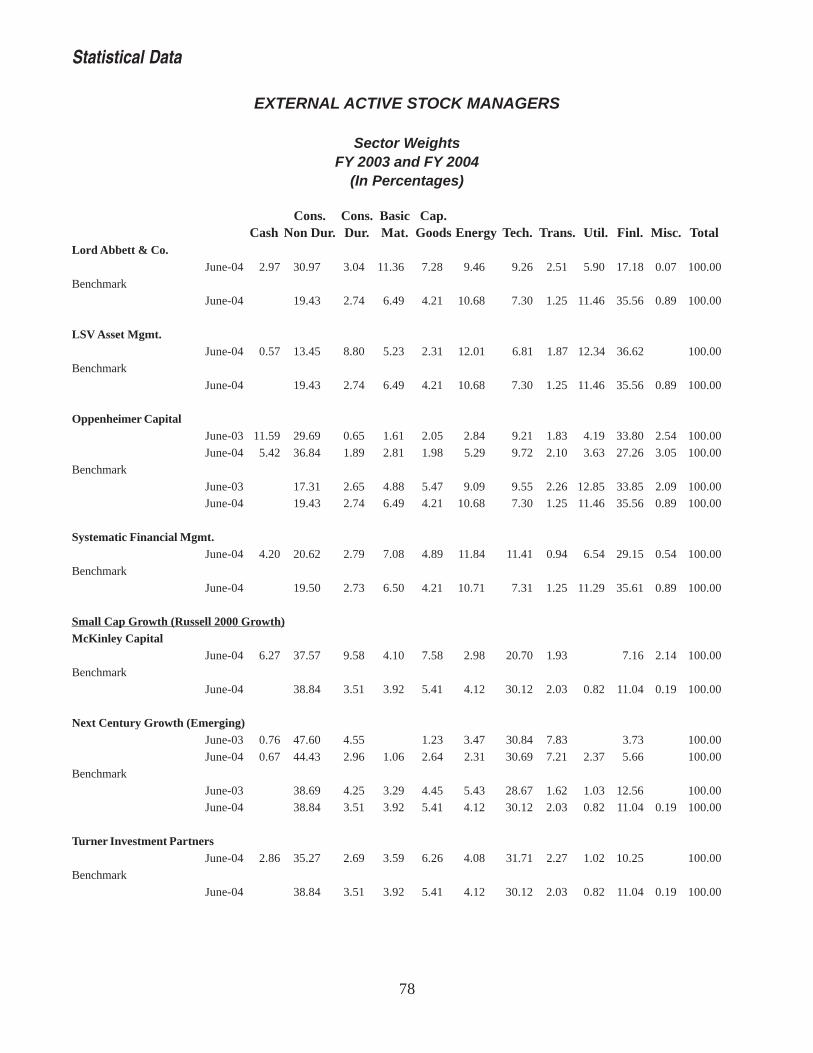

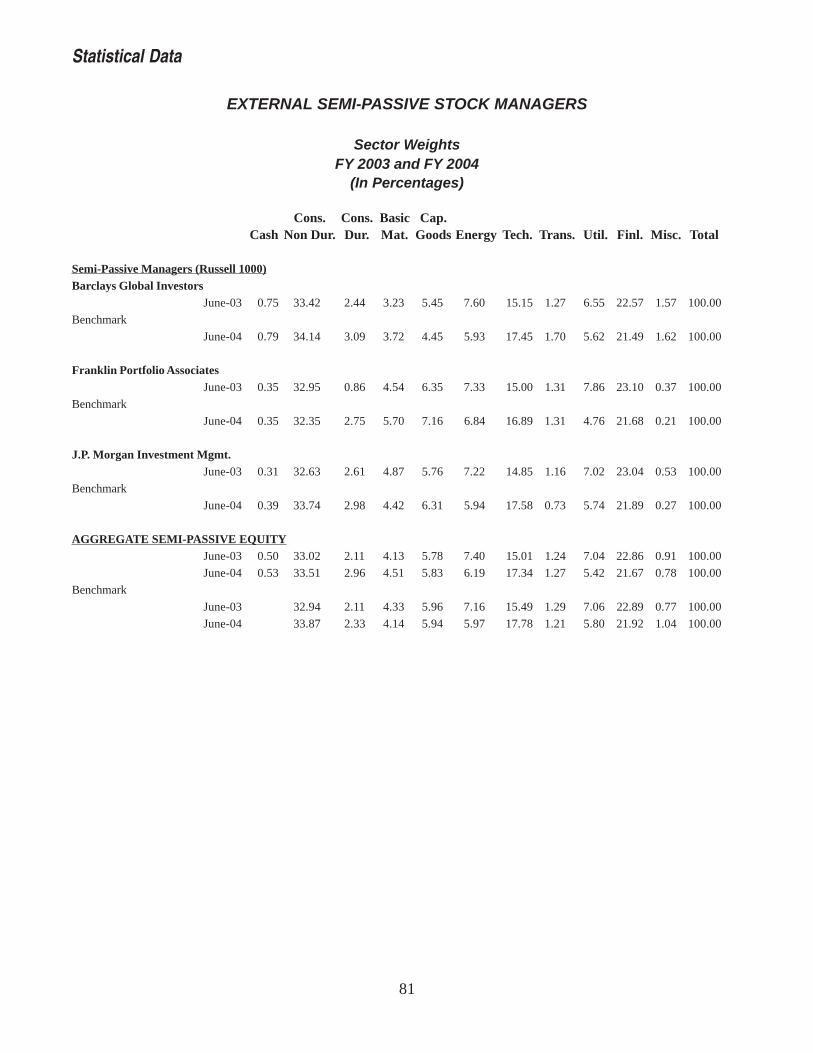

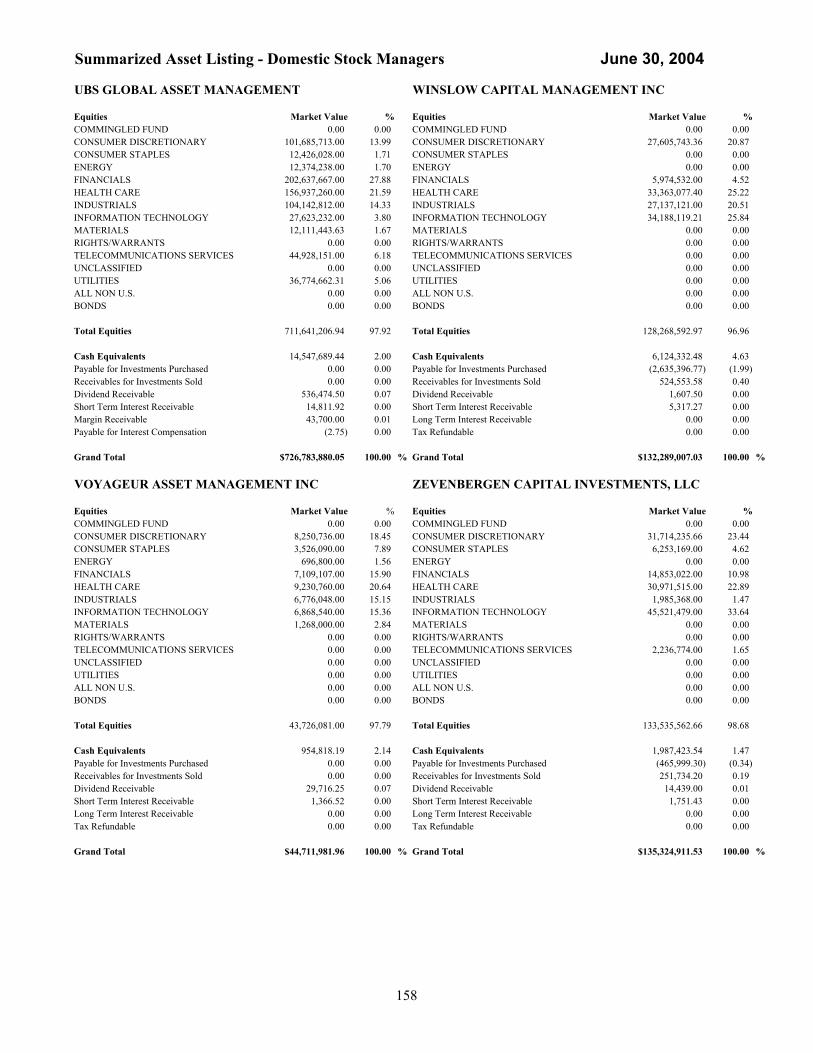

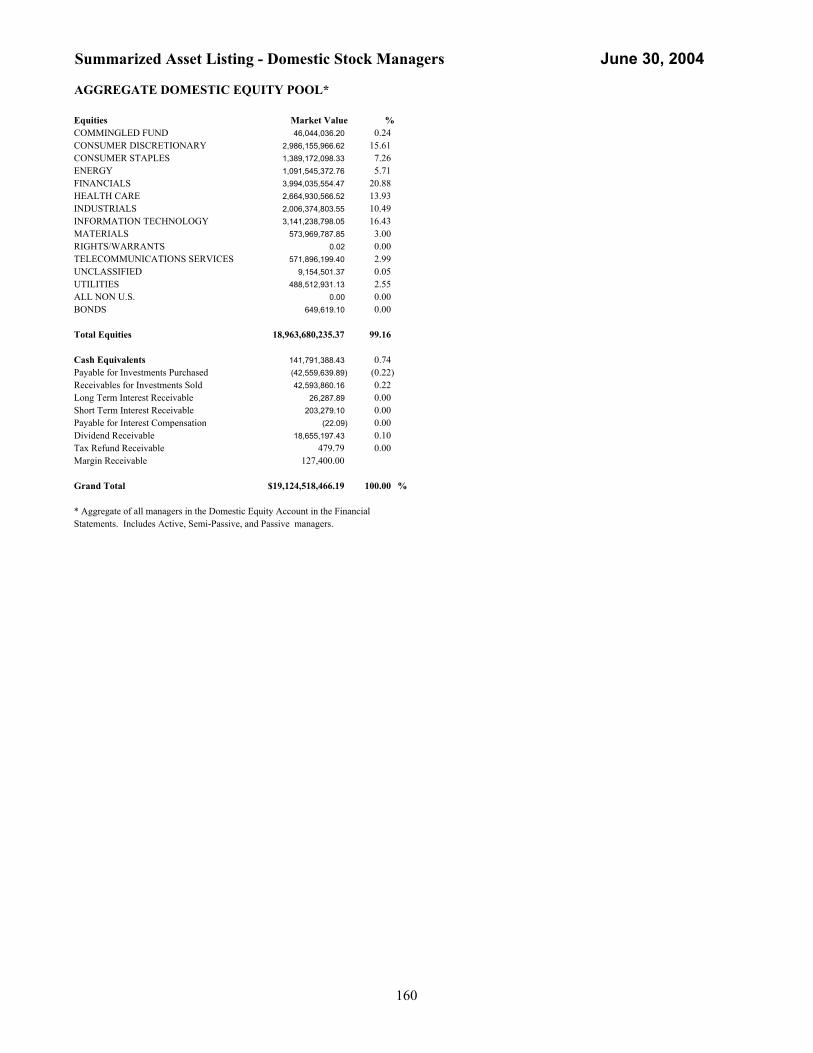

Historical information on individualmanager performance and portfoliocharacteristics is included in theStatistical Data section. Section IIof the Annual Report providesSummarized Asset Listings for eachmanager and the Pool in aggregate.

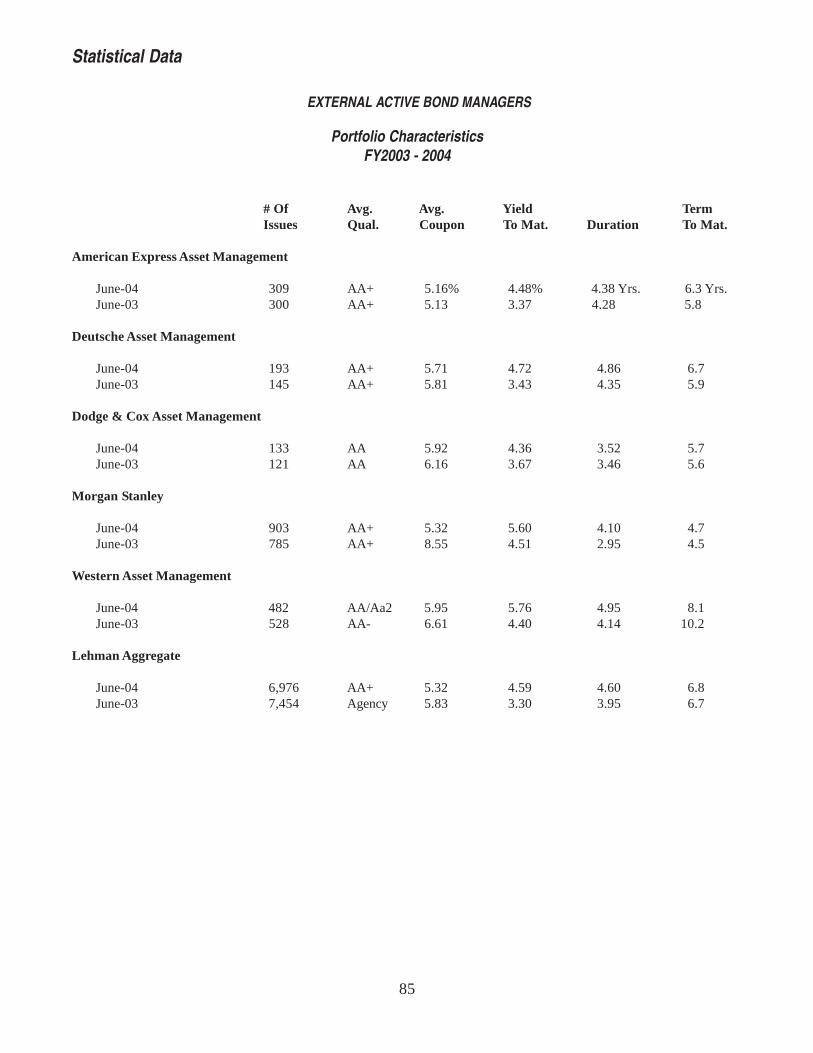

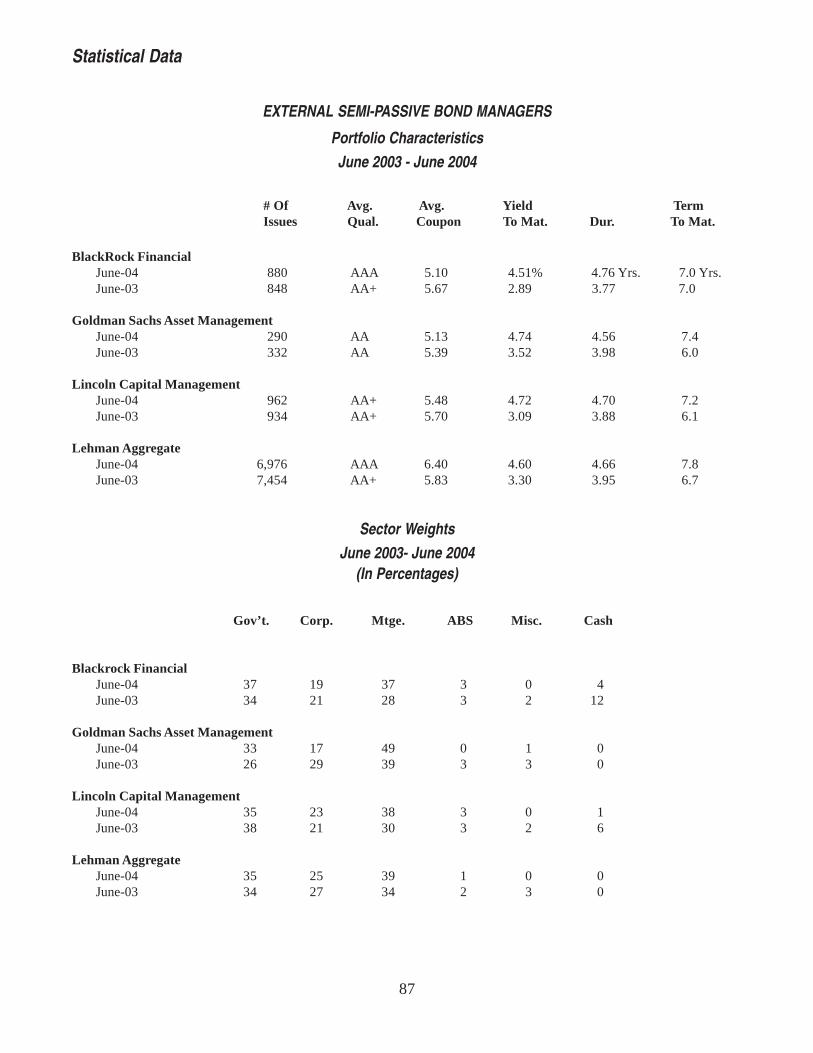

Bond Pool

The Basic Retirement Funds haveparticipated in the Bond Pool sinceits inception in July 1984. The PostRetirement Fund has participated inthe Pool since July 1993. In addition,the Bond Market Account in theSupplemental Investment Fund hasutilized portions of the Pool sinceJuly 1986.

As of June 30, 2004, the dollar valueof each fund’s participation in thePool was:

Basic Funds $4.0 billion(active and semi-passive)

Post Fund $4.5 billion(active and semi-passive)

Bond Market $93 millionAccount(active and semi-passive)

Investment ManagementThe SBI uses a two-part approach forthe management of the Bond Pool:

— Active Management. No morethan one-half of the Bond Poolwill be actively managed. At theend of fiscal year 2004,approximately 50% of the BondPool was actively managed by agroup of five external moneymanagers with portfolios of$635 million to $1.3 billion each.

— Semi-Passive Management. Atleast one-half of the assetsallocated to the Bond Pool will bemanaged by semi-passivemanagers. At the end of fiscalyear 2004, approximately 50% ofthe bond segment was invested bythree managers with portfolios ofapproximately $1.4 billion each.

The group of active bond managersis retained for its blend of investmentstyles. Each active manager has thegoal of adding incremental value tothe Lehman Aggregate Bond Indexby focusing on high quality fixedincome securities across all sectorsof the market. The managers vary,however, in the emphasis they place

Annualized2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Bond Pool 4.7% 11.8% 8.2% 10.7% 1.5% 6.7% 7.3% 7.7% Asset Class Target* 4.6 11.2 8.6 10.4 0.3 6.4 6.9 7.4

* Lehman Brothers Aggregate Bond Index.

Investment Pools

0

3

6

9

12

15

2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Per

cent

Bond Pool

AssetClassTarget

Figure 17. Bond Pool Per f ormanc e FY 2000-2004

19

on interest rate anticipation and inthe manner in which they approachissue selection and sector weightingdecisions. In keeping with theobjective of utilizing the Bond Poolas a deflation hedge, the activemanagers are restricted regarding theduration of their portfolios. Thisrequirement is designed to preventthe total pool from assuming anexcessively short-lived position andthus, severely diluting its deflationhedge capacity. In addition, theduration restriction helps to avoidextreme variability in total returns.The SBI constrains the durationrange of the active managers’portfolios to a band of plus or minustwo years around the duration of theLehman Aggregate. The active bondmanagers focus on high quality(BBB or better) rated bonds. Somemanagers have been grantedauthority to invest a limited portionof their portfolios in BB and B rateddollar denominated debt or in non-dollar denominated issues. The

managers use this additionalauthority on a tactical basis.The goal of the semi-passivemanagers is to add incremental valueto the Lehman Brothers AggregateBond Index through superior bondselection and sector allocation. Semi-passive managers’ portfolios areconstrained to plus or minus 0.2years around the duration of theLehman Aggregate. Semi-passivemanagers seek to add value byexploiting perceived mispricingsamong individual securities or bymaking alterations in the sectorweightings within the portfolio.Although the managers seek toexceed the performance of the index,the possibility exists that the semi-passive approach may slightly under-perform the target index during someperiods.

A description of each bondmanager’s investment approach isincluded in the InvestmentManager Summaries section.

Investment PerformanceThe SBI constrains the risk of theactive bond managers’ portfolios toensure that they fulfill their deflationhedge and total fund diversificationroles. As noted earlier, the managersare restricted in terms of the durationof their portfolios and the quality oftheir fixed income investments. Theactive and semi-passive bondmanagers successfully fulfilled theirlong-term risk objectives duringfiscal year 2004. The managersconstructed portfolios consistent withtheir stated investment approachesand maintained appropriate levels ofquality and duration.

The returns of each of the Board’sbond managers are compared to theLehman Aggregate. Due to the broaddiversification of each manager,customized benchmarks are notdeemed necessary for the bondmanagers at this time. Individualactive managers are expected toexceed the target by 0.25 percentagepoint annualized, over time, and eachsemi-passive manager is expected toexceed the target by 0.10 percentagepoint annualized, over time.In total, the Pool outperformed theLehman Aggregate index by 1.2percentage points for the recent fiscalyear. Relative to the benchmark, thepool benefited from several of theportfolios short duration positioning.The pool also benefited fromoverweighting corporates andsecurity selection across severalsectors.

Performance over longer periods hasbeen positive, exceeding thebenchmark by 0.3 percentage pointover the ten year period endingJune 30, 2004. In general, themanager’s decision to hold portfolioswith a modestly longer duration thanthe index, along with exposure andsecurity selection in the spreadsectors (corporate and mortgage

Figure 18. Bond Manager Performance FY 2004

Actual BenchmarkReturn Return

Active Managers American Express Asset Mgmt. 0.5% 0.3% Deutsche Asset Mgmt. 1.0 0.3 Dodge & Cox Investment Mgmt. 2.0 0.3 Morgan Stanley Investment Mgmt. 2.6 0.3 Western Asset Mgmt. 3.8 0.3

Semi-Passive Managers BlackRock Financial Mgmt. 0.5 0.3 Goldman Sachs Asset Mgmt. 1.5 0.3 Lincoln Capital Mgmt. 0.6 0.3

Aggregate Bond Pool 1.5 0.3

Asset Class Target Lehman Aggregate 0.3

Investment Pools

20

securities) accounted for the relativeperformance over the longer term.The relative performance ofindividual active managers retainedby the Board over the fiscal year wasgood; all five managers exceeded thebenchmark’s performance. Amongthe semi-passive managers, all threemanagers outperformed the indexover the fiscal year.

Figure 17 shows historicalperformance for the entire Pool.Individual manager performance forfiscal year 2004 is shown inFigure 18.

Historical information on individualmanager performance and portfoliocharacteristics is included in theStatistical Data section. Section IIof this report provides SummarizedAsset Listings for each manager andthe Pool in aggregate.

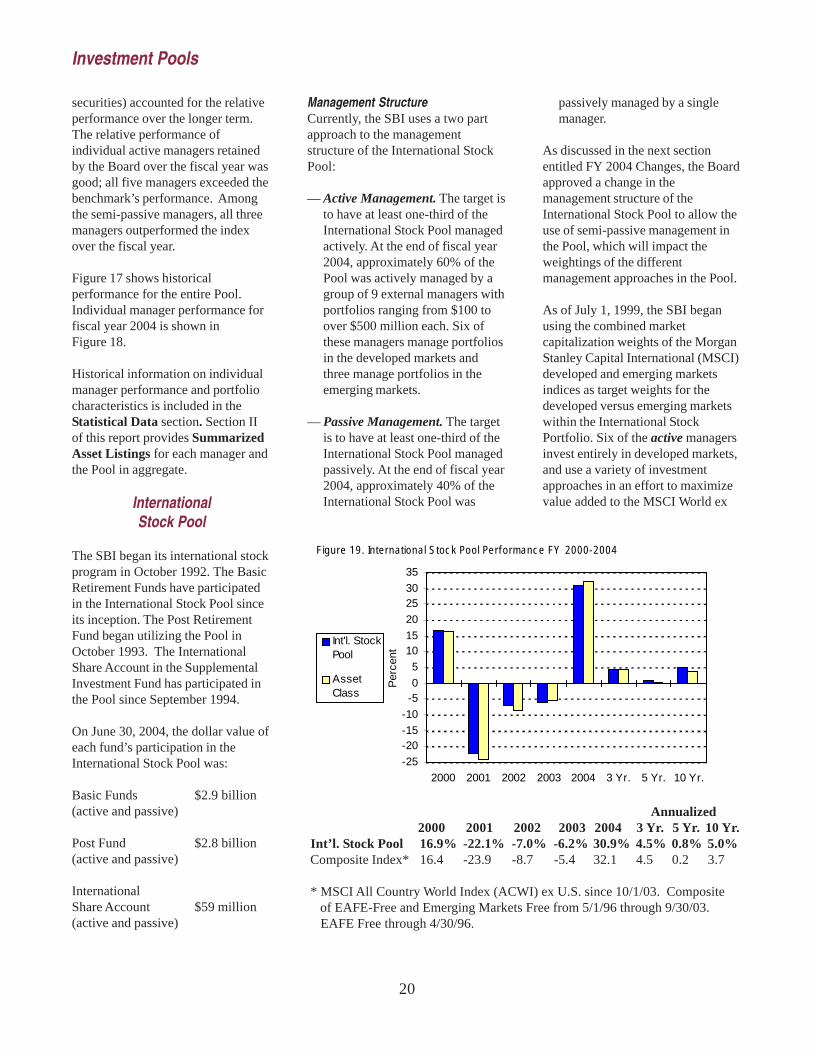

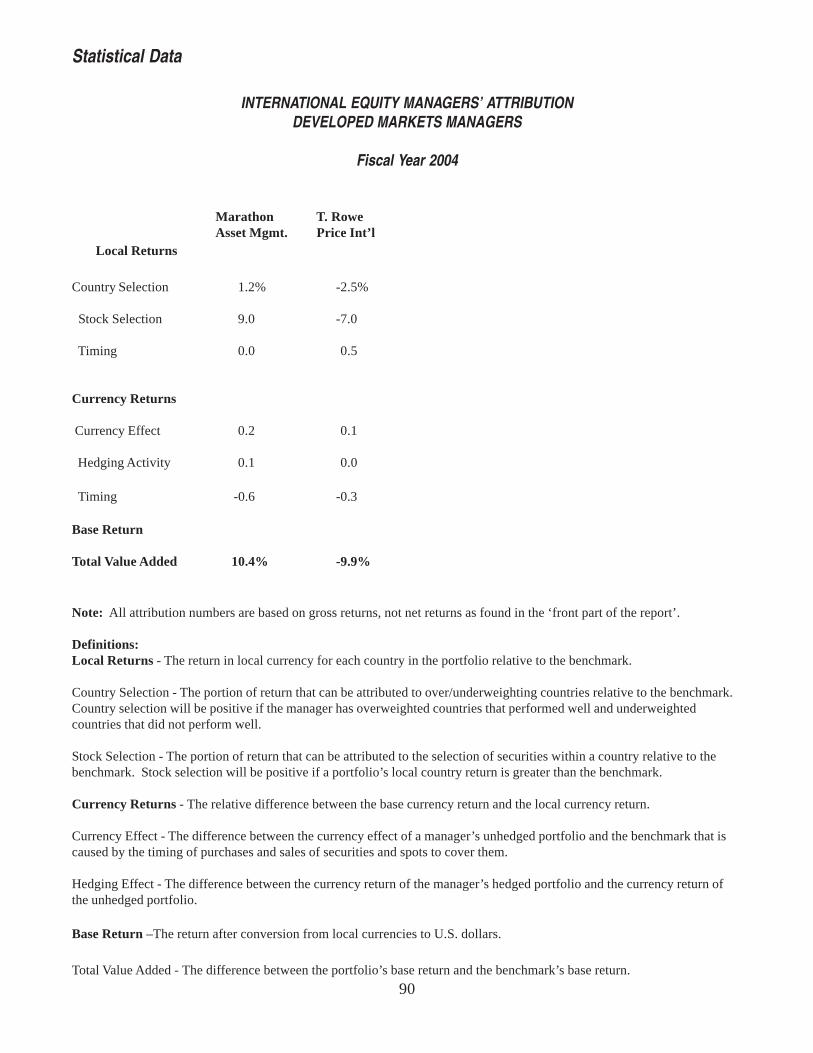

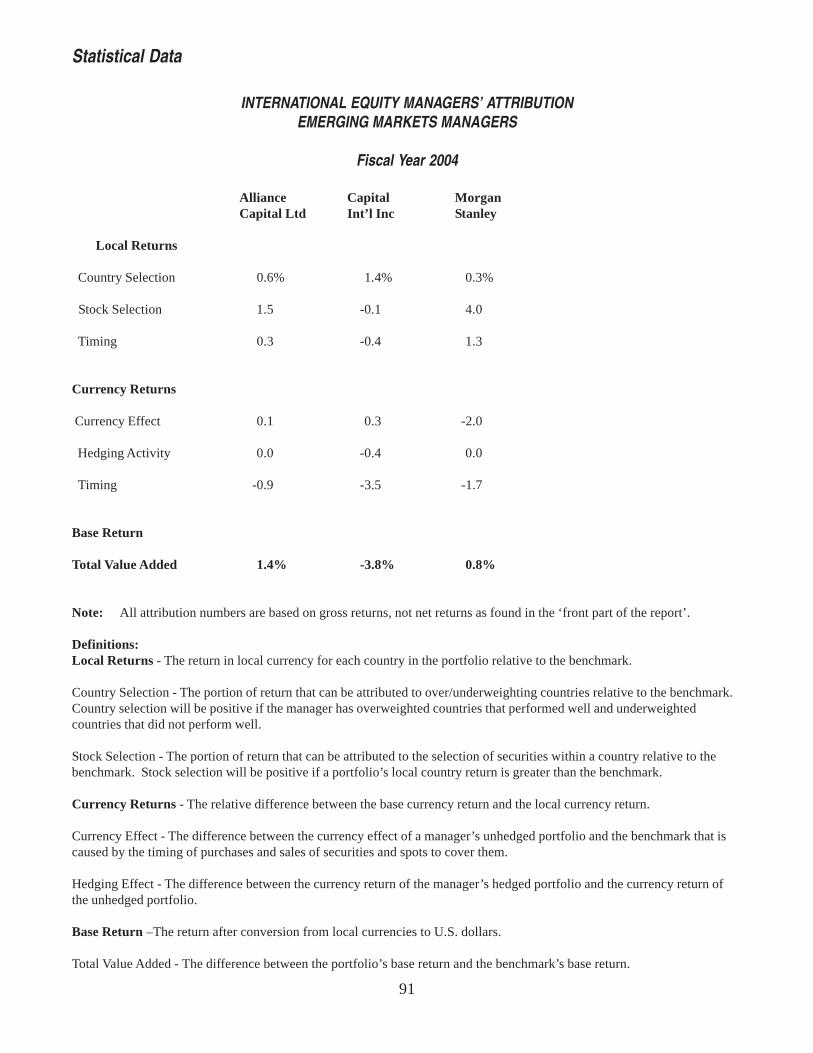

InternationalStock Pool

The SBI began its international stockprogram in October 1992. The BasicRetirement Funds have participatedin the International Stock Pool sinceits inception. The Post RetirementFund began utilizing the Pool inOctober 1993. The InternationalShare Account in the SupplementalInvestment Fund has participated inthe Pool since September 1994.

On June 30, 2004, the dollar value ofeach fund’s participation in theInternational Stock Pool was:

Basic Funds $2.9 billion(active and passive)

Post Fund $2.8 billion(active and passive)

InternationalShare Account $59 million(active and passive)

Management StructureCurrently, the SBI uses a two partapproach to the managementstructure of the International StockPool:

— Active Management. The target isto have at least one-third of theInternational Stock Pool managedactively. At the end of fiscal year2004, approximately 60% of thePool was actively managed by agroup of 9 external managers withportfolios ranging from $100 toover $500 million each. Six ofthese managers manage portfoliosin the developed markets andthree manage portfolios in theemerging markets.

— Passive Management. The targetis to have at least one-third of theInternational Stock Pool managedpassively. At the end of fiscal year2004, approximately 40% of theInternational Stock Pool was

passively managed by a singlemanager.

As discussed in the next sectionentitled FY 2004 Changes, the Boardapproved a change in themanagement structure of theInternational Stock Pool to allow theuse of semi-passive management inthe Pool, which will impact theweightings of the differentmanagement approaches in the Pool.

As of July 1, 1999, the SBI beganusing the combined marketcapitalization weights of the MorganStanley Capital International (MSCI)developed and emerging marketsindices as target weights for thedeveloped versus emerging marketswithin the International StockPortfolio. Six of the active managersinvest entirely in developed markets,and use a variety of investmentapproaches in an effort to maximizevalue added to the MSCI World ex

Annualized2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Int’l. Stock Pool 16.9% -22.1% -7.0% -6.2% 30.9% 4.5% 0.8% 5.0% Composite Index* 16.4 -23.9 -8.7 -5.4 32.1 4.5 0.2 3.7

* MSCI All Country World Index (ACWI) ex U.S. since 10/1/03. Composite of EAFE-Free and Emerging Markets Free from 5/1/96 through 9/30/03. EAFE Free through 4/30/96.

Investment Pools

-25

-20-15

-10

-50

5

1015

20

2530

35

2000 2001 2002 2003 2004 3 Yr. 5 Yr. 10 Yr.

Per

cent

Int'l. StockPool

AssetClass

Figure 19. In ternational Stoc k Pool Per f ormanc e FY 2000-2004

21

U.S. index, over time. Thesemanagers address currencymanagement as part of theirinvestment process. Their views oncurrency may be factored into theircountry and security selection, orthey may explicitly hedge currencyexposure on an opportunistic basis.

Three of the nine active managersinvest entirely in emerging markets.They are expected to add incrementalvalue, over time, relative to theMCSI Emerging Markets Free indexof markets in developing countriesthroughout the world.

The passive manager in theInternational Stock Pool designs itsportfolio to consistently andinexpensively track the MSCI Worldex U.S. index. Previously, a portionof the currency exposure of the indexfund was managed in a dynamichedging program designed to avoidcurrency losses during periods ofU.S. dollar strength. The currencyoverlay program was terminated asof December 1999. All contracts thatwere in place matured by December2000.

A description of each internationalstock manager’s investment approach

is included in the InvestmentManager Summaries section.

FY 2004 ChangesDuring the fiscal year 2004, theBoard terminated one activeemerging markets equity manager,Schroders Investment Management.

Following a review of theInternational Equity Programstructure, the Board approved achange to add Canada to thedeveloped markets benchmark and tothe asset class target. As of October 1, 2003 the developedmarkets managers’ benchmarkchanged from the MSCI EAFE Free(net) index to the MSCI World exU.S. (net) index. Marathon AssetManagement, a developed marketsmanager who previously wasmeasured against a custom index, isalso being benchmarked to the MSCIWorld ex U.S. index as of October 1,2003. As of the same date, theProgram’s asset class target changedfrom the MSCI EAFE Free + EMF(net) index to the MSCI All CountryWorld Index (ACWI) ex U.S. (net).In addition, the Board approved upto a 10% allocation to semi-passivemanagement, which has not yet beenfunded. Going forward, at least 25%of the Program will remain passivelymanaged. In aggregate, at least 33%of the program will be passively andsemi-passively managed and at least33% of the program will be activelymanaged. The program has been atleast 33% actively managed and atleast 33% passively managed.

Investment PerformanceSimilar to the Domestic Stock Pool,two long term risk objectives havebeen established for the internationalstock managers:

— Investment Approach. Eachmanager (active or passive) isexpected to hold a portfolio that isconsistent with the manager’sstated investment approach.

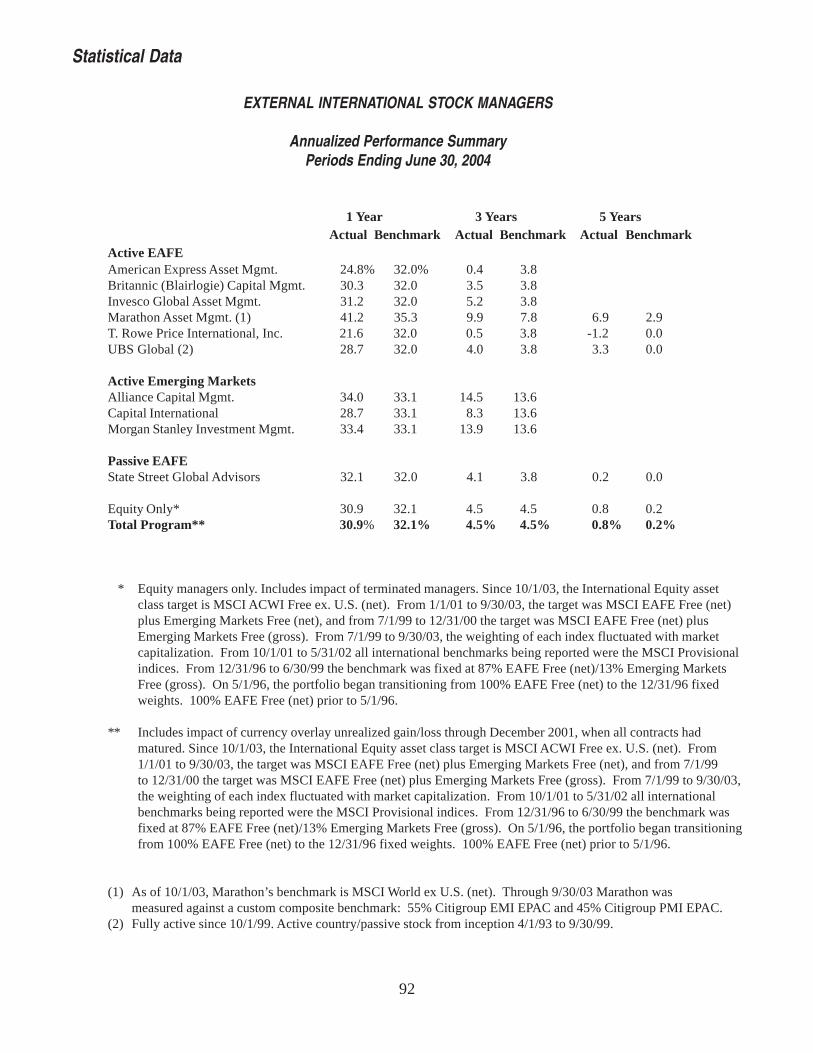

Figure 20. International Manager Performance FY 2004

ActualReturn Benchmark

Active Managers: Developed Markets American Express Asset Mgmt. 24.8% 32.0% Britannic Capital Mgmt. 30.3 32.0 Invesco Global Asset Mgmt. 31.2 32.0 Marathon Asset Mgmt.* 41.2 35.3 T. Rowe Price International, Inc. 21.6 32.0 UBS Global Asset Mgmt. 28.7 32.0

Active Managers: Emerging Markets Alliance Capital Mgmt. 34.0 33.1 Capital International 28.7 33.1 Morgan Stanley Investment Mgmt. 33.4 33.1

Passive EAFE Manager State Street Global Advisors 32.1 32.0

Aggregate International Pool 30.9

Asset Class Target** 32.1

* Marathon’s performance was measured against a custom benchmark through 9/30/03 and against the MSCI World ex U.S. index (net) beginning 10/1/03.

** The asset class target was comprised of the EAFE Free and Emerging Markets Free (EMF) index through 9/30/03 and the MSCI All Country World Index (ACWI) ex U.S. beginning 10/1/03. The weighting of each index fluctuates with changes in market capitalization.

Investment Pools

22

— Diversification. While the indexmanager is expected to hold awell diversified portfolio whichclosely tracks its target index,each active manager is expectedto hold a more concentratedportfolio.

The international stock managerssuccessfully fulfilled their long-termrisk objectives during fiscal year2004. In general, the managersconstructed portfolios consistent withtheir stated investment approachesand maintained appropriate levels ofdiversification.

The Board’s return objectives for theinternational stock program arestated relative to the Morgan StanleyCapital International (MSCI) indices.The indices are capitalizationweighted and measured in U.S. dollarterms, with currencies unhedged.

Individual active managers areexpected to exceed their index by atleast 1.00 percentage pointannualized, over time, and the indexmanager is expected to track itsindex by ±0.50 percentage point,annually.

Performance results for theInternational Stock Pool are shown inFigure 19, (on page 20). Inaggregate, performance over the lastfive and ten year periods exceededthe benchmark by 0.6 and 1.3percentage points annualized,respectively. The Poolunderperformed the target for theyear by 1.2 percentage points.

Individual manager performanceduring fiscal year 2004 is shown inFigure 20, (on page 21). Overall,the fiscal year proved to be a periodof strong market performance, whichwas helped by U.S. dollar weakness.The markets were influenced bysigns of structural change and

economic recovery in Japan, stronggrowth across Asian economies ledby China, and the integration ofCentral European countries into theEuropean Union. The relativeperformance of the active managerswas mixed. Five of the sixdeveloped markets managersunderperformed their respectivebenchmarks for the year. Howeverthree of the four emerging marketsmanagers outperformed the MSCIEmerging Markets Free index, whichreturned 33.1% for the year. In thedeveloped markets, the market’s biasto small cap lesser quality stocks,which perform well in periods ofeconomic recovery, hurt the activemanagers who tend to focus onlarger, well established companieswith high quality earnings. Thepassively managed portion of theprogram had positive tracking errorof 0.1% for the year relative to theMSCI World ex U.S. index.

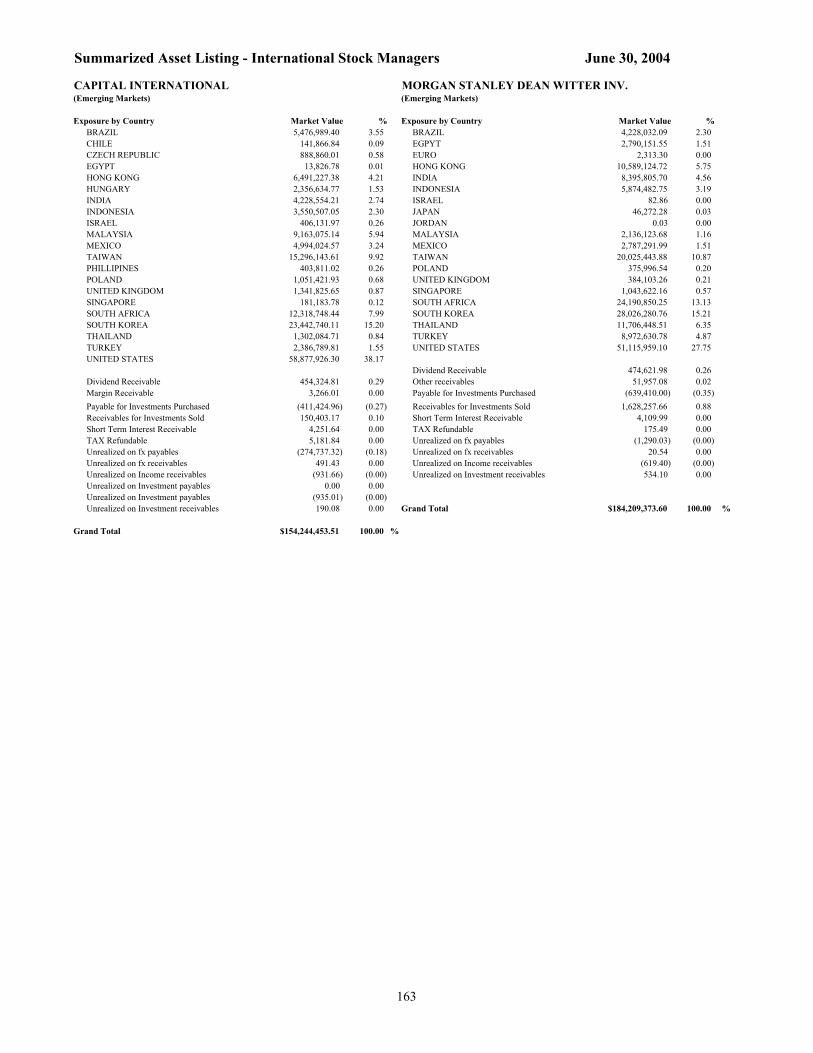

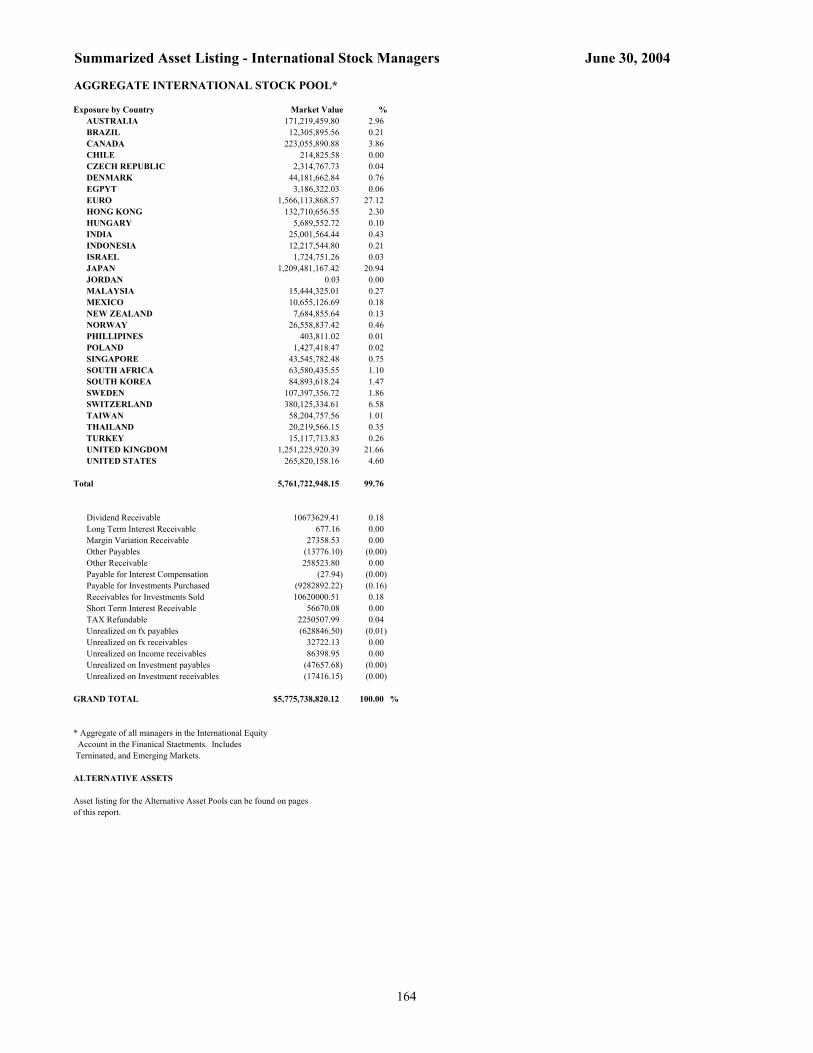

More information on theperformance and portfoliocomposition of individual managersis included in the Statistical Datasection. Section II of this reportprovides Summarized AssetListings for each manager and thePool in aggregate.

AlternativeInvestment Pools

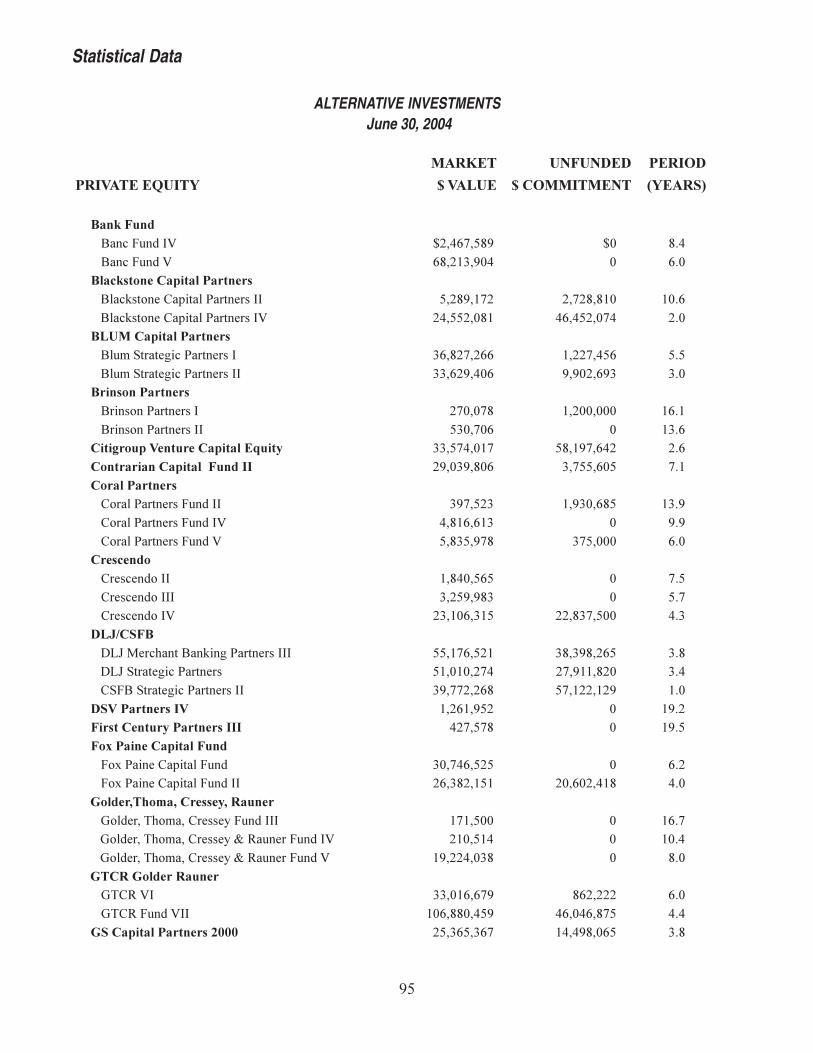

Like the stock and bond segments,alternative assets (private equity, realestate, resource fund and yield-oriented investments) are alsomanaged on a pooled basis. In July2003, separate pools that had beenestablished for the Basic and PostRetirement Funds were combined tocreate one alternative investmentpool.

Statutory ConstraintsThe statutory constraints regardingthe SBI’s investments to alternative

assets are the same in both the Basicand Post Funds:

Generally, each investment mustinvolve at least four other investorsand the SBI’s participation in aninvestment may not exceed 20% ofthe total investment.

Management Structure

The Basic and Post RetirementFunds have participated in theAlternative Investment Pool since itsinception in July 2003. TheAlternative Investment Pool wascreated in July 2003 from separatepools that had been previouslyestablished for the Basic and PostRetirement Funds.

Given their long investment timehorizon, the Basic and Post Fundsare especially well suited toalternative investments. As of June30, 2004, up to 15% of the marketvalue of the Basic Retirement Fundsare targeted for alternativeinvestments compared to an actualinvested percentage of 12.7%.Market value plus unfundedcommitments can be 1.5 times themarket value allocation.

For the Post Fund, as of June 30,2004, the Board has allocated up to12% of the market value of the Fundto alternative investments comparedto an actual invested percentage of4.3%. Market value plus unfundedcommitments can be 1.5 times themarket value allocation.

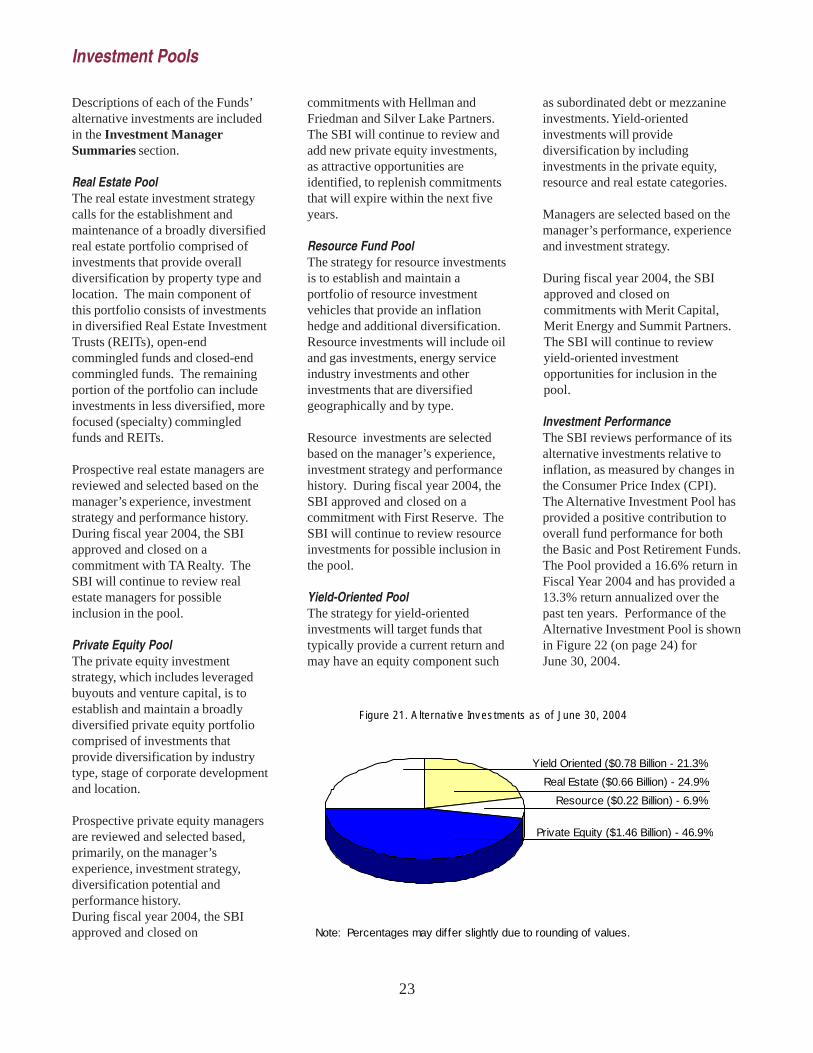

A breakdown of the combined Postand Basic Funds segment is shown inFigure 21 (on page 23). As of June30, 2004, the market value of currentalternative investments was $3.2billion, or 8.6% of the CombinedFunds.

Investment Pools

23

Descriptions of each of the Funds’alternative investments are includedin the Investment ManagerSummaries section.

Real Estate PoolThe real estate investment strategycalls for the establishment andmaintenance of a broadly diversifiedreal estate portfolio comprised ofinvestments that provide overalldiversification by property type andlocation. The main component ofthis portfolio consists of investmentsin diversified Real Estate InvestmentTrusts (REITs), open-endcommingled funds and closed-endcommingled funds. The remainingportion of the portfolio can includeinvestments in less diversified, morefocused (specialty) commingledfunds and REITs.

Prospective real estate managers arereviewed and selected based on themanager’s experience, investmentstrategy and performance history.During fiscal year 2004, the SBIapproved and closed on acommitment with TA Realty. TheSBI will continue to review realestate managers for possibleinclusion in the pool.

Private Equity PoolThe private equity investmentstrategy, which includes leveragedbuyouts and venture capital, is toestablish and maintain a broadlydiversified private equity portfoliocomprised of investments thatprovide diversification by industrytype, stage of corporate developmentand location.

Prospective private equity managersare reviewed and selected based,primarily, on the manager’sexperience, investment strategy,diversification potential andperformance history.During fiscal year 2004, the SBIapproved and closed on

commitments with Hellman andFriedman and Silver Lake Partners.The SBI will continue to review andadd new private equity investments,as attractive opportunities areidentified, to replenish commitmentsthat will expire within the next fiveyears.

Resource Fund PoolThe strategy for resource investmentsis to establish and maintain aportfolio of resource investmentvehicles that provide an inflationhedge and additional diversification.Resource investments will include oiland gas investments, energy serviceindustry investments and otherinvestments that are diversifiedgeographically and by type.

Resource investments are selectedbased on the manager’s experience,investment strategy and performancehistory. During fiscal year 2004, theSBI approved and closed on acommitment with First Reserve. TheSBI will continue to review resourceinvestments for possible inclusion inthe pool.

Yield-Oriented PoolThe strategy for yield-orientedinvestments will target funds thattypically provide a current return andmay have an equity component such

as subordinated debt or mezzanineinvestments. Yield-orientedinvestments will providediversification by includinginvestments in the private equity,resource and real estate categories.

Managers are selected based on themanager’s performance, experienceand investment strategy.

During fiscal year 2004, the SBIapproved and closed oncommitments with Merit Capital,Merit Energy and Summit Partners.The SBI will continue to reviewyield-oriented investmentopportunities for inclusion in thepool.

Investment PerformanceThe SBI reviews performance of itsalternative investments relative toinflation, as measured by changes inthe Consumer Price Index (CPI).The Alternative Investment Pool hasprovided a positive contribution tooverall fund performance for boththe Basic and Post Retirement Funds.The Pool provided a 16.6% return inFiscal Year 2004 and has provided a13.3% return annualized over thepast ten years. Performance of theAlternative Investment Pool is shownin Figure 22 (on page 24) forJune 30, 2004.

Investment Pools