20-11-2014. Amortized Loans An amortized loan is a loan paid off in equal payments – consequently,...

21

20-11-2014

-

Upload

frederick-townsend -

Category

Documents

-

view

218 -

download

0

Transcript of 20-11-2014. Amortized Loans An amortized loan is a loan paid off in equal payments – consequently,...

20-11-2014

Amortized Loans

• An amortized loan is a loan paid off in equal payments – consequently, the loan payments are an annuity.

• In an amortized loan:– The present value can be thought of as the

amount borrowed, – n is the number of periods the loan lasts for, – i is the interest rate per period, and – Payment is the loan payment that is made.

2

Example

Example 25 Suppose you plan to get a $9,000 loan from a furniture dealer at 18% annual interest with annual payments that you will pay off in over three years. What will your annual payments be on this loan?

PMT = $4139.315

3

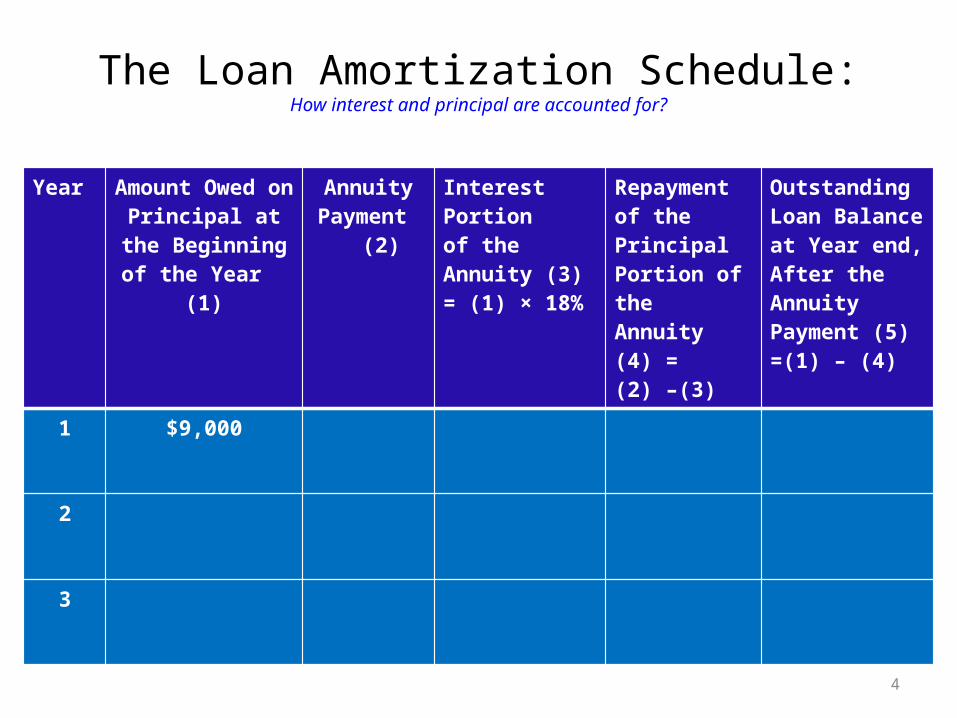

The Loan Amortization Schedule:How interest and principal are accounted for?

Year Amount Owed on Principal at the Beginning of the Year

(1)

Annuity Payment

(2)

Interest Portion of the Annuity (3) = (1) × 18%

Repayment of the Principal Portion of the Annuity (4) = (2) –(3)

Outstanding Loan Balance at Year end, After the Annuity Payment (5)=(1) – (4)

1 $9,000

2

3

4

The Loan Amortization ScheduleHow interest and principal are accounted for?

• We can observe the following from the table:– Size of each payment remains the same.– However, Interest payment declines each year as

the amount owed declines and more of the principal is repaid.

5

Practice

• Question 5-34, 5-22, 5-8 (HW)

EAR AND APR

EAR and APR

• APR (Annual Percentage Rate also known as the nominal, quoted rate or stated rate) is the rate banks say they charge on loans.

• APR = iper x n– You should NEVER divide the effective rate by the number of periods per year – it will NOT

give you the periodic rate.

• EAR (Effective annual rate) is the rate actually being earned as opposed to quoted rate.

• . 1 m

APR 1 EAR

m

EAR and APR

• The use of an example will help to clear the difference between EAR and APR.

• There are 2 banks, Bank A and Bank B, both offer loan at nominal/APR of 12%.

• However, Bank A compounds loan semi-annually and Bank B compounds loan quarterly.

• So are these banks charging the same true rate? • No! They both charge a different true rate (EAR).• How? Let’s see.

EAR and APR

• The example helps us to identify that in order to compare loans across lenders we should first calculate the EAR.

• We can calculate EAR from APR and APR from EAR.

• Note:– If a loan uses annual compounding its nominal rate =

effective rate. (Example)– If compounding on a loan occurs more than once an

year, EAR > APR. (Example)

11

Computing APRs

• What is the APR if the monthly rate is .5%? .5(12) = 6%

• What is the APR if the semiannual rate is .5%? .5(2) = 1%

• What is the monthly rate if the APR is 12% with monthly compounding? 12 / 12 = 1%

12

Things to Remember

• You ALWAYS need to make sure that the interest rate and the time period match.• If you are looking at annual periods, you need an annual rate.• If you are looking at monthly periods, you need a monthly

rate.

13

EAR - Formula

1 m

APR 1 EAR

m

Remember that the APR is the quoted rate

m is the number of compounding periods per year

14

Decisions, Decisions!

• You are looking at two savings accounts. One pays 5.25%, with daily compounding. The other pays 5.3% with semiannual compounding. Which account should you use and why?

15

Computing APRs from EARs

• If you have an effective rate, how can you compute the APR? Rearrange the EAR equation and you get:

1 - EAR) (1 m APR m

1

16

APR - Example

• Suppose you want to earn an effective rate of 12% and you are looking at an account that compounds on a monthly basis. What APR must they pay?

11.39%or

8655152113.1)12.1(12 12/1 APR

Practice

• Question 5-17, 5-27, 5-28.

Challenging Problems

• Question 5-33, 5-32, 5-31, 5-29, 5-36, 5-26• Prepare for the Quiz (Due Anytime)

FORMULAS

20

Number

Time Value of

Money Formula For:

Annual Compounding

Compounded (m) Times per Year

(semi-annually, quarterly, monthly, daily)

1 Future Value of a Lump Sum. ( FVIFi,n )

) +1 ( VP = VF ni *First calculate n = N * m *then calculate iper = APR / m Now insert the value of ‘n’ and

‘iper’ in the formula. 2

Present Value of a Lump Sum. ( PVIFi,n )

) +1 FV/( = PV i *First calculate n = N * m *then calculate iper = APR / m Now insert the value of ‘n’ and

‘iper’ in the formula. 3

Future Value of an ordinary Annuity. ( FVIFAi,n )

1 -)+1 ( =FVA

i

iPMT

n *First calculate n = N * m *then calculate iper = APR / m Now insert the value of ‘n’ and ‘iper’ in the formula.

4 Present Value of an ordinary Annuity. ( PVIFAi,n )

i

iPMT

n)) +1 /(1(-1 =PVA *First calculate n = N * m *then calculate iper = APR / m Now insert the value of ‘n’ and

‘iper’ in the formula. 5

Effective Annual Rate given the APR. APR = EAR 1 -+1 = EAR

m

im

21

6. For Future value of Annuity due Future value of ordinary annuity * (1+i)7. For Present value of Annuity due Present value of ordinary annuity * (1+i)8. Present Value of a Perpetuity =