2. Lattice Methods - YorkU Math and Statshmzhu/Math-5300/lectures/Lecture2/2... · 2008-06-13 ·...

21

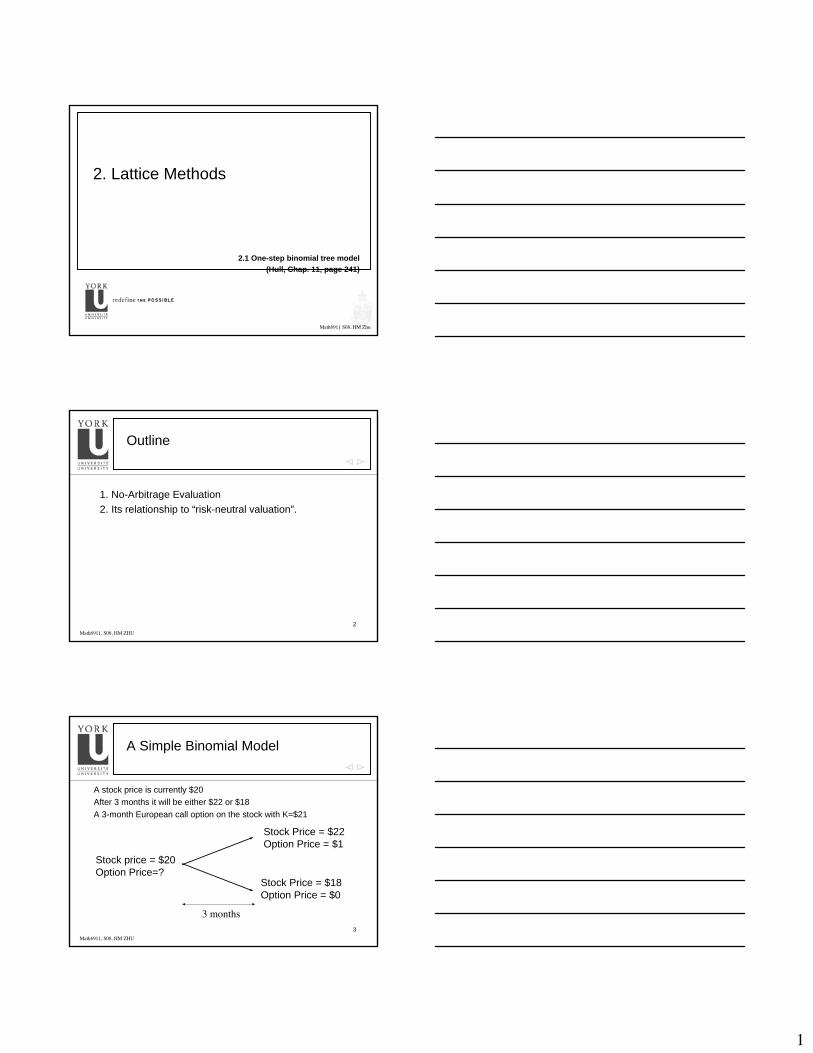

1 Math6911 S08, HM Zhu 2.1 One-step binomial tree model (Hull, Chap. 11, page 241) 2. Lattice Methods 2 Math6911, S08, HM ZHU Outline 1. No-Arbitrage Evaluation 2. Its relationship to “risk-neutral valuation”. 3 Math6911, S08, HM ZHU Stock Price = $22 Option Price = $1 Stock Price = $18 Option Price = $0 Stock price = $20 Option Price=? A Simple Binomial Model A stock price is currently $20 After 3 months it will be either $22 or $18 A 3-month European call option on the stock with K=$21 3 months

Transcript of 2. Lattice Methods - YorkU Math and Statshmzhu/Math-5300/lectures/Lecture2/2... · 2008-06-13 ·...

1

Math6911 S08, HM Zhu

2.1 One-step binomial tree model(Hull, Chap. 11, page 241)

2. Lattice Methods

2Math6911, S08, HM ZHU

Outline

1. No-Arbitrage Evaluation2. Its relationship to “risk-neutral valuation”.

3Math6911, S08, HM ZHU

Stock Price = $22Option Price = $1

Stock Price = $18Option Price = $0

Stock price = $20Option Price=?

A Simple Binomial Model

A stock price is currently $20After 3 months it will be either $22 or $18A 3-month European call option on the stock with K=$21

3 months

2

4Math6911, S08, HM ZHU

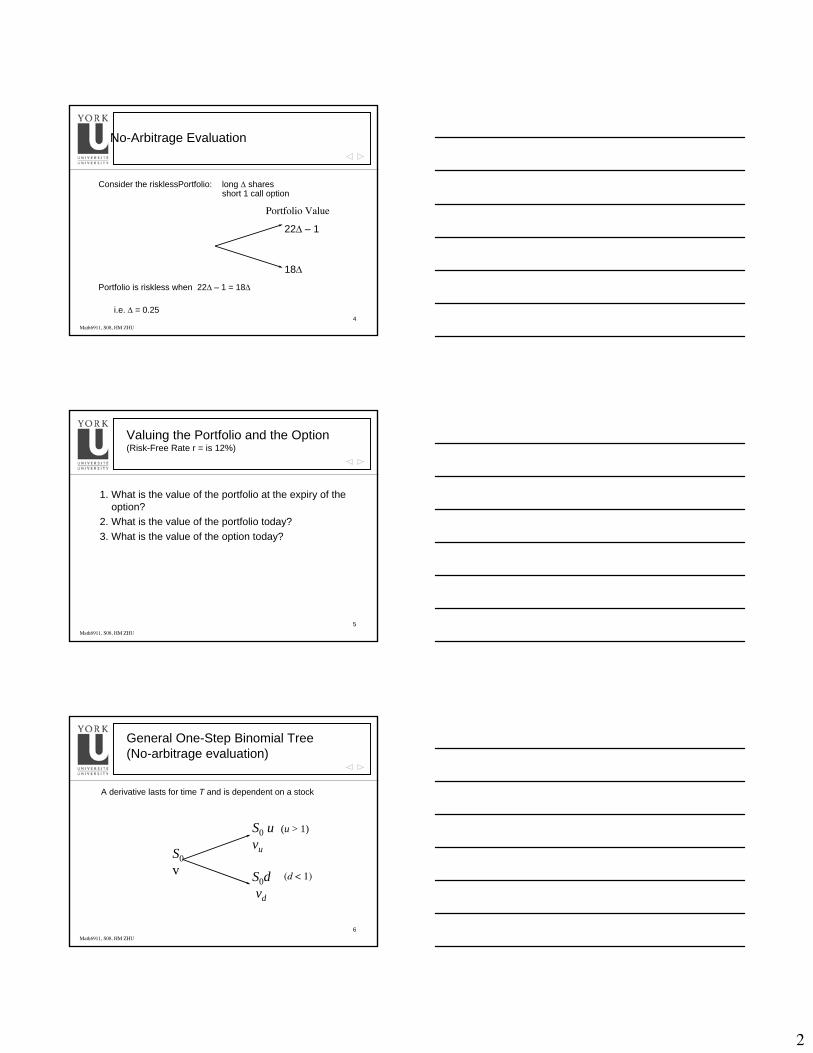

Consider the risklessPortfolio: long ∆ sharesshort 1 call option

Portfolio is riskless when 22∆ – 1 = 18∆

i.e. ∆ = 0.25

No-Arbitrage Evaluation

22∆ – 1

18∆

Portfolio Value

5Math6911, S08, HM ZHU

Valuing the Portfolio and the Option(Risk-Free Rate r = is 12%)

1. What is the value of the portfolio at the expiry of the option?

2. What is the value of the portfolio today? 3. What is the value of the option today?

6Math6911, S08, HM ZHU

General One-Step Binomial Tree(No-arbitrage evaluation)

A derivative lasts for time T and is dependent on a stock

S0 u (u > 1)vu

S0dvd

S0v (d < 1)

3

7Math6911, S08, HM ZHU

General One-Step Binomial Tree(No-arbitrage evaluation)

Consider the portfolio: long ∆ shares, short 1 derivative

The portfolio is riskless when S0u ∆ – vu = S0d ∆ – vd or

dSuSvv du

00 −−

=∆

S0 u∆ – vu

S0d∆ – vd

S0∆– v

8Math6911, S08, HM ZHU

Value of the portfolio at time T: S0u ∆ – vu

Value of the portfolio today:

S0 ∆– v =(S0u ∆ – vu )e–rT

Hence

v = S0 ∆ – (S0u ∆ – vu )e–rT

General One-Step Binomial Tree(No-arbitrage evaluation)

9Math6911, S08, HM ZHU

Substituting for ∆, we obtain

Where

• The variables p and (1 – p ) can be interpreted as the risk-neutral probabilities of up and down movements

• The value of a derivative can be considered as its expected payoff in a risk-neutral world discounted at the risk-free rate

p e du d

r T

=−

−

( )[ ] rTdu evppvv −−+= 1

Another approach: risk-neutral evaluation

S0uvu

S0dvd

S0v

p

(1 – p )

4

10Math6911, S08, HM ZHU

Comments and example

• Note: When we are valuing an option in terms of the underlying stock the expected return on the stock is irrelevant

• Use risk-neutral evaluation to calculate option price in the original example (r = 12%, T = 3/12):

S0u = 22vu = 1

S0d = 18vd = 0

S0v

p

(1 – p )

11Math6911, S08, HM ZHU

Original example revisited(risk-neutral evaluation)

6523.09.01.1

9.00.250.12

=−

−=

−−

=×e

dudep

rT

S0u = 22vu = 1

S0d = 18vd = 0

S0v

0.6523

0.3477

[ ]6330

034770165230isoption theof value theTherefore,

123120

. . . ev /.-

=×+×= ×

12Math6911, S08, HM ZHU

Risk-neutral evaluation

• In a risk-neutral world, all investors are indifferent to risk, i.e., investors require no compensation for risk and the expected returns of all securities is the risk-free interest rate

• The option price resulted from risk-neutral evaluation is correct not only in the risk-neutral world, but also in other world as well

• Further reading: Cox, Ross, and Rubinstein, “Option pricing: a simplified approach”, J. of Financial Economics 7:229-264 (1979)

5

Math6911 S08, HM Zhu

2.2 Binomial Methods(Hull, Sec 11.7, Sec. 17.1)

2. Lattice Methods

14Math6911, S08, HM ZHU

Outline

1. Extension to N-step binomial method2. Determine the parameters3. Binomial methods in option pricing

15Math6911, S08, HM ZHU

Binomial Trees

• Binomial trees are frequently used to approximate the movements in the price of a stock or other asset

• In each small interval of time (∆t) the stock price is assumed to move up by a proportional amount u or to move down by a proportional amount d

uS

dS

S

p

1 – p

Stock movements in time ∆t

6

16Math6911, S08, HM ZHU

Assumption 1

To model a continuous walk by a discrete walk in the following fashion :

T=M ∆ttime

0 ∆t 2 ∆t

SuS

dS

p

1-p

u2Sp

p u d S

d2S1-p

yprobabilit :11

pdu

<>

M≥30

1-p

17Math6911, S08, HM ZHU

Assumption 1 (cont)

The parameters , and in such a way that mean and variance of the discrete random walk coincide with those of the continuous random walk

u d , p

18Math6911, S08, HM ZHU

Assumption 2: Risk-Neutral Valuation

We may assume investors are risk-neutral (even though most are not)

In terms of option pricing (or other derivatives), we can assume: • The expected return from all traded securities is the risk-free

interest rate

• Future cash flows can be valued by discounting their expected values at the risk-free interest rate

The tree is designed to represent the behavior of a stock price in risk-neutral world

7

19Math6911, S08, HM ZHU

Binomial Method: Assumption 2

( )1

Under the assumption of risk-neutral world, the value of the put option at the expected value of option at 1 discount

m

m

V m tV m t+

∆ =

+ ∆

1

ed by the risk-free interest rate

m r t m

r

V E e V− ∆ +⎡ ⎤= ⎣ ⎦

20Math6911, S08, HM ZHU

1 1

The parameters and in such a way that mean and variance of the discrete random walk coincide with those of the continuous random walk in risk-neutral world, i.e.,:

and

m m m mc b

u, d , p

E S S E S S

v

+ +⎡ ⎤ ⎡ ⎤=⎣ ⎦ ⎣ ⎦

1 1

The parameters , , and must give correct values for the mean and variance of stock price changes during

m m m mc bar S S var S S

p u dt.

+ +⎡ ⎤ ⎡ ⎤=⎣ ⎦ ⎣ ⎦

∆

Tree parameters p, u, and d for non-dividend paying stock

21Math6911, S08, HM ZHU

( )( )

1 1

1

1 (1)

m m m mc b

r t m m

r t

E S S E S S

e S pu p d S

e pu p d

+ +

∆

∆

⎡ ⎤ ⎡ ⎤=⎣ ⎦ ⎣ ⎦⎡ ⎤⇒ = + −⎣ ⎦

⇒ = + −

Tree parameters u, d, and p

8

22Math6911, S08, HM ZHU

Tree parameters u, d, and p

( ) ( ) ( ) ( )( ) ( )

2

2

1 1

2 22 2 2 2

2 2 2

1 1

1 2

In order to determine these three unknowns uniquely, we need to add another condition (somewhat arbitrary)

m m m mc b

m r t t r t m

r t t

var S S var S S

S e e pu p d e S

e pu p d

.

σ

σ

+ +

∆ ∆ ∆

∆ + ∆

⎡ ⎤ ⎡ ⎤= ⇒⎣ ⎦ ⎣ ⎦

⎡ ⎤⇒ − = + − −⎣ ⎦

⇒ = + −

( ) ( )

( ) ( ) ( )222

Note: follows a lognormal distribution. It can be shown that1) The expected value of :

E2) The variance of :

1

T

T

T tT

T

T t T tT

SS

S SeS

var S S e e

µ

µ σ

−

− −

=

⎡ ⎤= −⎣ ⎦

23Math6911, S08, HM ZHU

One further condition:

2 2

0

2 2

1One of the popular choices is .

It generates a symmetric tree w.r.t. the initial value S :

= , =

[reference: Cox, Ross and Rubinstein (1979)]Ofte

r tt r t t r t

ud

e du e d e , p .u d

σ σσ σ⎛ ⎞ ⎛ ⎞

∆∆ + − ∆ − ∆ + − ∆⎜ ⎟ ⎜ ⎟⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠

=

−=

−

2n, ignoring the terms in and higher power of gives

= , =

Note: If t is too large, or 1 0. The binomial method fails.

r tt t

t te du e d e , p .u d

p ( - p )

σ σ∆

∆ − ∆

∆ ∆

−=

−∆ <

du 1

=

24Math6911, S08, HM ZHU

Symmetric Tree: d

u 1=

9

25Math6911, S08, HM ZHU

Another further condition:

( ) ( )[ ]

2 2

1One of the popular choices is .2

It generates an asymmetric tree, oriented in the direction of the drift:1= 1 1 , = 1 12

Kwok, 1998; Wilmott et al, 1995

Note: If is too large,

r t t r t t

p

u e e d e e , p

t

σ σ∆ ∆ ∆ ∆

=

+ − − − =

∆ 0. The binomial method fails.d <

21

=p

26Math6911, S08, HM ZHU

Asymmetric Tree:21

=p

Math6911 S08, HM Zhu

2.3 General Binomial Tree Models(Hull, Sec. 17.1, , page 391)

2. Lattice Methods

10

28Math6911, S08, HM ZHU

The Idea of Binomial Methods

1. Build a tree of possible values of asset prices and their probabilities, given an initial asset price

2. Once we know the value of the option at the final nodes, work backward through the tree using risk-neutral valuation to calculate the value of the option at each node, testing for early exercise when appropriate

Advantages: easily deal with possibility of early exercise and with dividend payments

29Math6911, S08, HM ZHU

Binomial Method for valuing non-dividend-paying options

00

00

Step 1. Build up a tree of possible asset prices for all time points and their probabilities, given the initial price

S for 0 1

S the n-th possible value of S

m n m nn

mn

S

u d S n , , ,m

:

−= =

at m-th time-step

30Math6911, S08, HM ZHU

Build A Complete Tree of Asset Prices

S0

S0u

S0d S0 S0

S0u2

S0d2

S0u2

S0u3 S0u4

S0d2

S0u

S0d

S0d4

S0d3

Tree structure used the relationship u = 1/d

11

31Math6911, S08, HM ZHU

Step 2: Valuing an European option:

( )

( )1 11

2.1. Value the option at expiry, i.e, time-step

Put: - 0 0 1

Call:2.2. Find the expected value of the option at a time step prior to expiry

1

M Mn n

m r t m r t m mn n n n

M t

V max K S , n , , M

V E e V e pV p V− ∆ + − ∆ ++

∆

= =

⎡ ⎤= = + −⎣ ⎦

…

1

and so on, back to time-step 0.

+⎡ ⎤⎣ ⎦

Step 2. Use this tree to calculate the possible value of option at expiry. Then work back down the tree to caculate the price of the option

32Math6911, S08, HM ZHU

Example 1: European 2-year Put Option

S0 = 50; K = 52; r =5%; σ = 30%; T = 2 years; ∆t = 1 year

The parameters imply 0 3 1

0 05 1

1 3499 1 0 7408

1 3499 1 0513

1 053 0 7408 0 50971 3499 0 7408

1- 0 4903

.

.

u e . ;

d . ;.

a e . ;. .p .

. .p .

×

×

= =

= =

= =−

= =−

=

33Math6911, S08, HM ZHU

Example 1: European 2-year Put Option

50? A

B

C

D

E

F

1 year 1 year

12

34Math6911, S08, HM ZHU

Example 2: European Put Option

S0 = 50; K = 50; r =10%; σ = 40%; T = 5 months = 0.4167; ∆t = 1 month = 0.0833

The parameters imply

1 1224

0 8909 1 0084

0 5076

1- 0 4924

t

t

r t

u e . ;

d e . ;a e . ;

a dp .u d

p .

σ

σ

∆

− ∆

∆

= =

= =

= =−

= =−

=

35Math6911, S08, HM ZHU

Example 2: European Put Option

89.070.00

79.350.00

70.70 70.700.00 0.00

62.99 62.990.64 0.00

56.12 56.12 56.122.16 1.30 0.00

50.00 50.00 50.004.49 3.77 2.66

44.55 44.55 44.556.96 6.38 5.45

39.69 39.6910.36 10.31

35.36 35.3614.64 14.64

31.5018.50

28.0721.93

36Math6911, S08, HM ZHU

Example 2: European Put Option

89.070.00

79.350.00

70.70 70.700.00 0.00

62.99 62.990.64 0.00

56.12 56.12 56.122.16 1.30 0.00

50.00 50.00 50.004.49 3.77 2.66

44.55 44.55 44.556.96 6.38 5.45

39.69 39.6910.36 10.31

35.36 35.3614.64 14.64

31.5018.50

28.0721.93

9.90

18.08

6.18

13.81

9.86

3.67

6.66

4.32

2.11

13

37Math6911, S08, HM ZHU

Step 2: Valuing an American put option

( ) ( )

1

At time step and at asset price S , there are two possibilities:1. Exercise the option which yield a profit

- 0

2. Retain the option, the value of the option is then

ki

m mn n

m r t mn

k

payoff S max K S ,

V E e V− ∆ +

=

⎡= ( )

( ) ( )( )

1 11

1 11

1

Therefore, the value of the option is the maximum oftwo possibilities

1

r t m mn n

m m r t m mn n n n

e pV p V

,i.e.,

V max payoff S , e pV p V

− ∆ + ++

− ∆ + ++

⎤ ⎡ ⎤= + −⎣ ⎦ ⎣ ⎦

⎡ ⎤= + −⎣ ⎦

38Math6911, S08, HM ZHU

Example 1: American 2-year Put Option

1 year

91.110

50?

67.49

37.04

502

27.4424.56

?

?

A

B

C

D

E

F

1 year

S0 = 50; K = 52; r =5%, σ=30%, T = 2 years, ∆t = 1 year

39Math6911, S08, HM ZHU

Example 2: American put option of the same stock: S0 = 50; K = 50; r =10%; σ = 40%; T = 5 months; ∆t = 1 month

89.070.00

79.350.00

70.70 70.700.00 0.00

62.99 62.990.64 0.00

56.12 56.12 56.122.16 1.30 0.00

50.00 50.00 50.004.49 3.77 2.66

44.55 44.55 44.556.96 6.38 5.45

39.69 39.6910.36 10.31

35.36 35.3614.64 14.64

31.5018.50

28.0721.93

14

40Math6911, S08, HM ZHU

Step 2: Valuing an American call option

( )

?.,.,iespossibilit two

of maximum theisoption theof value theTherefore,?

thenisoption theof value theoption, Retain the 2.?

profit a yieldch option whi theExercise 1.:iespossibilit twoare there,S priceasset at and step At time

=

=

=

mn

mn

mn

ki

Vei

V

Spayoff

k

41Math6911, S08, HM ZHU

Exercise 2: American call option of the same stock: S0 = 50; K = 50; r =10%; σ = 40%; T = 5 months; ∆t = 1 month

89.070.00

79.350.00

70.70 70.700.00 0.00

62.99 62.990.64 0.00

56.12 56.12 56.122.16 1.30 0.00

50.00 50.00 50.004.49 3.77 2.66

44.55 44.55 44.556.96 6.38 5.45

39.69 39.6910.36 10.31

35.36 35.3614.64 14.64

31.5018.50

28.0721.93

42Math6911, S08, HM ZHU

Convergence of the Price of the American Put on Non-Dividend-Paying Option Example

15

Math6911 S08, HM Zhu

2. Lattice Methods

2.4 Dealing with Options on Dividend-paying Stocks(Hull, Sec. 17.3, page 401)

44Math6911, S08, HM ZHU

With Continuous Dividend Yields

( )

0

0

Assume there is a constant dividend yield paid on the underlying. Then the expected return of the underlying is at the rate

To accommodate the constant dividend yield in the tree model,1. Repl

D

r D .−

( )0

0ace by in the parameters , , and in the tree construction of stock prices. For example, in the case 1 , it becomes:

= , =

1 For the case when , it be2

r D tt t

r r D u d pu / d

e du e d e , p .u d

p

σ σ− ∆

∆ − ∆

−=

−=

−

=

( ) ( ) ( ) ( )2 20 0

comes:

= 1 1 , = 1 1r D t r D tt tu e e d e e .σ σ− ∆ − ∆∆ ∆+ − − −

45Math6911, S08, HM ZHU

2. Use this tree to calculate the possible value of option at expiry. Then work back down the tree to caculate the present value of the option at previous time points is obtained using

m ?nV E e−= 1t m

nV∆ +⎡ ⎤⎣ ⎦

With Continuous Dividend Yields

16

46Math6911, S08, HM ZHU

2. Use this tree to calculate the possible value of option at expiry. Then work back down the tree to caculate the present value of the option at previous time points is obtained using

m rnV E e−= 1t m

nV∆ +⎡ ⎤⎣ ⎦

With Continuous Dividend Yields

47Math6911, S08, HM ZHU

A better procedure:– Draw the tree for the stock price less the present

value of the dividends– Create a new tree for the stock price by adding the

present value of the dividends at each node

This ensures that the tree recombines and makes assumptions similar to those when the Black-Scholes model is used

With Dollar Dividend

48Math6911, S08, HM ZHU

With Dollar Dividend

( )

*

*

Assume that there is one ex-dividend date, , during the life of the option.-- Construct a tree for the uncertain component , . .,

, if , if

r i t

S i e

S De i tSS i t

τ

τ

ττ

− − ∆⎧ − ∆ <= ⎨

∆ >* *

*

*0

Using the volatility of , a tree can be constructed in usual way to model .-- To model , we simply add back the present value of future dividend, . .,

n i n

in

SS

Si e

S u d DeS

σ

−−

⎪

⎪⎩

+=

( )

*0

, if , 0,1, ,, if

r i t

n i n

i t n iS u d i t

τ ττ

− ∆

−

⎧ ∆ <⎪ =⎨∆ >⎪⎩

17

Example 1: American put option on a stock: S0 = 52; K = 50; D = $2.06r =10%; σ∗ = 40%; T = 5 months;τ = 3.5 months∆t = 1 month

50Math6911, S08, HM ZHU

Example 1: Tree model for S*

89.070.00

79.350.00

70.70 70.700.00 0.00

62.99 62.990.64 0.00

56.12 56.12 56.122.16 1.30 0.00

50.00 50.00 50.004.49 3.77 2.66

44.55 44.55 44.556.96 6.38 5.45

39.69 39.6910.36 10.31

35.36 35.3614.64 14.64

31.5018.50

28.0721.93

+$2.05

Example 1: American put option on a stock: S0 = 52; K = 50; D = $2.06r =10%; σ∗ = 40%; T = 5 months;τ = 3.5 months∆t = 1 month

18

Math6911 S08, HM Zhu

2. Lattice Methods

2.5 Further Comments

53Math6911, S08, HM ZHU

Delta (∆)

• An important parameter in the pricing and hedging of options

• It is the ratio of the change in the price of a stock option to the change in the price of the underlying stock

• It is # of the units of the stock we should hold for each option shorted to create a riskless hedge. Such a construction of riskless hedging is called “delta hedging”.

• ∆ of a call option is positive whereas ∆ of a put option is negative

54Math6911, S08, HM ZHU

Valuing Delta’s

Value at ∆t:

Values at 2∆t: If upward movement over the first time step,

Otherwise,

2.0257 0 0.506422 18

−∆ = =

−

24.23.2

201.2823

22

18

19.80.0

16.20.0

2.0257

0.0

A

B

C

D

E

F

3.2 0 0.727324.2 19.8

−∆ = =

−

0 0 019.8 16.2

−∆ = =

−

19

55Math6911, S08, HM ZHU

Delta

• The value of ∆ varies over time and from node to node

• To maintain a riskless hedge using an option and the underlying stock, we need to adjust our holdings in the stock periodically

56Math6911, S08, HM ZHU

Trees for Options on Indices, Currencies and Futures Contracts (Hull, Sec. 11.9, Sec. 17.2)

As with Black-Scholes:– For options on stock indices, replace the

continuous dividend yield D0 with the dividend yield on the index

– For options on a foreign currency, D0 equals the foreign risk-free rate rf

– For options on futures contracts D0 = r

57Math6911, S08, HM ZHU

Time Dependent Interest Rate and Dividend Yield (page 409)

• Making interest rate r or dividend yield D a function of time does not affect the geometry of the tree. The probabilities on the tree become functions of time

• Discounting factor becomes a function of time as well

20

58Math6911, S08, HM ZHU

Time Dependent Volatility (page 409)

• Changing σ at each time step does affect the geometry of the tree. (The probabilities on the tree become functions of time)

• Or we can make σ a function of time by making the lengths of the time steps inversely proportional to the variance rate.

59Math6911, S08, HM ZHU

Trinomial Tree (see Technical Note 9, www.rotman.utoronto.ca/~hull)

61

212

32

61

212

/1

2

2

2

2

3

+⎟⎟⎠

⎞⎜⎜⎝

⎛ σ−

σ∆

−=

=

+⎟⎟⎠

⎞⎜⎜⎝

⎛ σ−

σ∆

=

== ∆σ

rtp

p

rtp

udeu

d

m

u

t

S S

Sd

Su

pu

pm

pd

Math6911, S08, HM ZHU

Explicit FDM =Trinomial Tree

Vi , j Vi +1, j

Vi +1, j –1

Vi +1, j +1

Explicit Method

21

61Math6911, S08, HM ZHU

Further Reading

1. D. Leisen and M. Reimer. Applied Mathematical Finance, 1996(developed a general convergence rate theory)

2. L. Clewlow and C. Strickland. Implementing Derivatives Models. Wiley, Chichester, West Sussex, England, 1998 (relationship between finite differences and trinomial trees)

3. D J Higham. Nine Ways to Implement the Binomial Method for Option Valuation in Matlab. SIAM review, 44:661-677, 2002 (issues of implementing binomial trees)

4. G. Levy. Computational Finance. Numerical Methods for Pricing Financial Instruments. Elsevier Butterworth-Heinemann, oxford, 2004 (implied lattices and efficient implementations)

62Math6911, S08, HM ZHU

Adaptive Mesh Model

• This is a way of grafting a high resolution tree on to a low resolution tree

• We need high resolution in the region of the tree close to the strike price and option maturity

• Numerically efficient over a binomial or trinomial tree• Figlewski and Gao, “The adaptive mesh model: a

new approach to efficient option pricing”, J. of Financial Ecomonics, 53:313-351 (1999)

![Estimating Proportions - YorkU Math and Stats … · Title: Microsoft PowerPoint - Chapter 10.pps [Compatibility Mode] Author: gam Created Date: 3/7/2012 12:59:59 AM](https://static.fdocuments.in/doc/165x107/5b1655067f8b9a5e6d8b50ba/estimating-proportions-yorku-math-and-title-microsoft-powerpoint-chapter.jpg)