2 form 5500 update 06.18.15dp

27

Form 5500 update Presented by Debbie Packer & Cindy Herendeen June 18, 2015 www.pwc.com

-

Upload

carol-buckmann -

Category

Documents

-

view

161 -

download

2

Transcript of 2 form 5500 update 06.18.15dp

Form 5500 update

Presented by Debbie Packer & Cindy HerendeenJune 18, 2015

www.pwc.com

PwC

Agenda

Overview of the 2014 Form 5500

• Tips for 2014 Form 5500

• Review of Schedules

• Highlights of processing system

• Form 8955-SSA

• Updates to delinquent filer program

PwC

When are audited financial statements required ?

• Large pension plans (100 or more participants)

• 80-to-120 rule

• Small pension plans that do not meet the conditions for the audit waiver

• Large funded welfare plans (100 or more participants)

- VEBAs or taxable trusts

• 80-to-120 rule different for welfare plans because small fully insured or unfunded welfare plans are not required to file

- Only small funded welfare plans required to file may take advantage of this rule

3

June 18, 2015

4PwC

Small pension plan audit waiver summary

Is the plan a pension plan?

Is the Schedule I required as part of the plan’s annual report?

Do at least 95% of the assets of the plan constitute 'qualifying plan assets'?

Small pension plan audit waiver conditions do not apply.

Is each person who handles non-qualifying plan assets properly bonded in an amount that is at least equal to the value of the non-qualifying plan assets?

The conditions for the waiver have not been satisfied.

The conditions for the waiver of IQPA audit and report have been satisfied.

Does the administrator disclose the required information in the SAR and on request?

No

Yes

No

No

No

No

Yes

Yes

Yes

Yes

June 18, 2015

PwC

EFAST2

The IRS has all responsibility for the 5500-EZ and Form 5558 and their processing. Please call the IRS for questions regarding these Forms

EFAST2 Help Line

• Can’t answer questions regarding Third Party Software

• Can’t view your filing prior to submission to EFAST2

• Can’t see your password or challenge question

• Can answer questions about IFILE

• Can answer questions about Filing Status

• Staffed help line at 1-866-GO-EFAST (between 8:00 AM and 8:00 PM Eastern Standard)

5

June 18, 2015

PwC

EBSA Website

Check EFAST2 Website for:

• FAQs

• User Guides

• Tutorials

• DFVCP Info

6

June 18, 2015

PwC

Check the filing status after filing is submitted• Important to check the status of your submission attempt and make sure

they are accepted

• DOL requires at least one electronic signature be valid

• Various ways to check the status :

◦ Through the software you used to send your filing◦ Through the EFAST2 Filing Search webpage◦ Through EFAST2 Submissions webpage

› If you submitted through IFILE

› If you signed the filing

• Also, monitor your email later for correspondence from the EFAST2/DRC email address

7

June 18, 2015

PwC

Check the filing status after filing is submitted

• Note that the signed auditor’s report with financial statements must be attached as a pdf file

• The pdf file cannot be encrypted or password protected

- “Unprocessable error”

- Remember to pdf in portrait not landscape format

- Print heavy letterheads may result in rejection

8

June 18, 2015

PwC

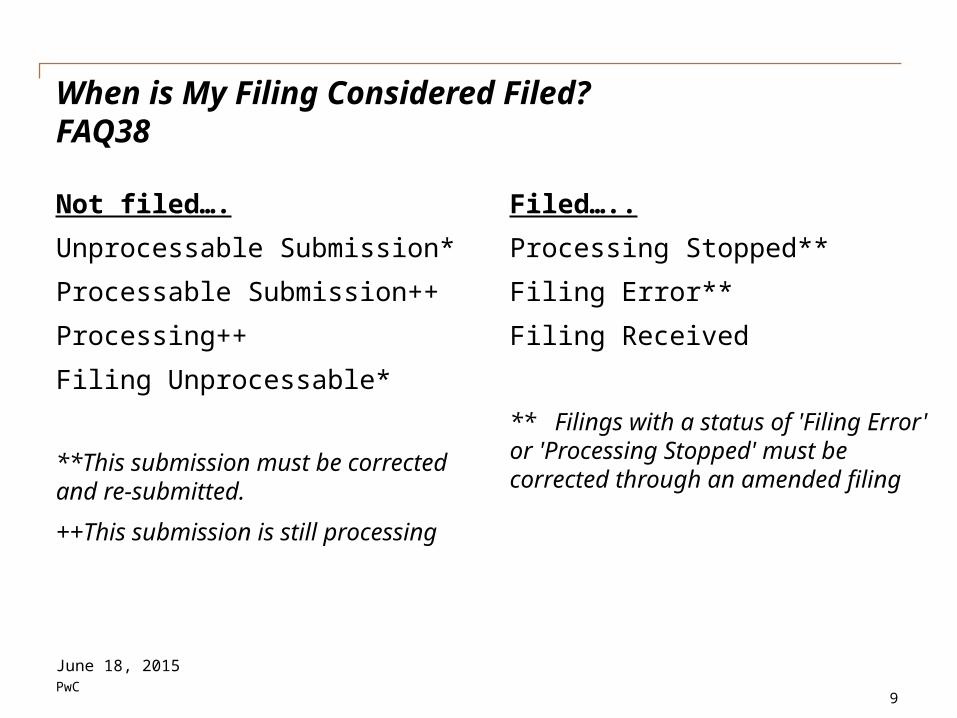

When is My Filing Considered Filed? FAQ38

Not filed….

Unprocessable Submission*

Processable Submission++

Processing++

Filing Unprocessable*

**This submission must be corrected and re-submitted.

++This submission is still processing

Filed…..

Processing Stopped**

Filing Error**

Filing Received

** Filings with a status of 'Filing Error' or 'Processing Stopped' must be corrected through an amended filing

9

June 18, 2015

PwC

EFAST2 user responsibilities

Document retention

• Plan administrators and DFEs must retain a copy of the filing signed by the Filing Signer and any acknowledgements received from DOL, along with all other documents required by IRC and ERISA

• Signer must retain copy of signed Schedule SB or MB

• Must retain copy of Form 5558, if filed (not attached to filing)

10

June 18, 2015

PwC

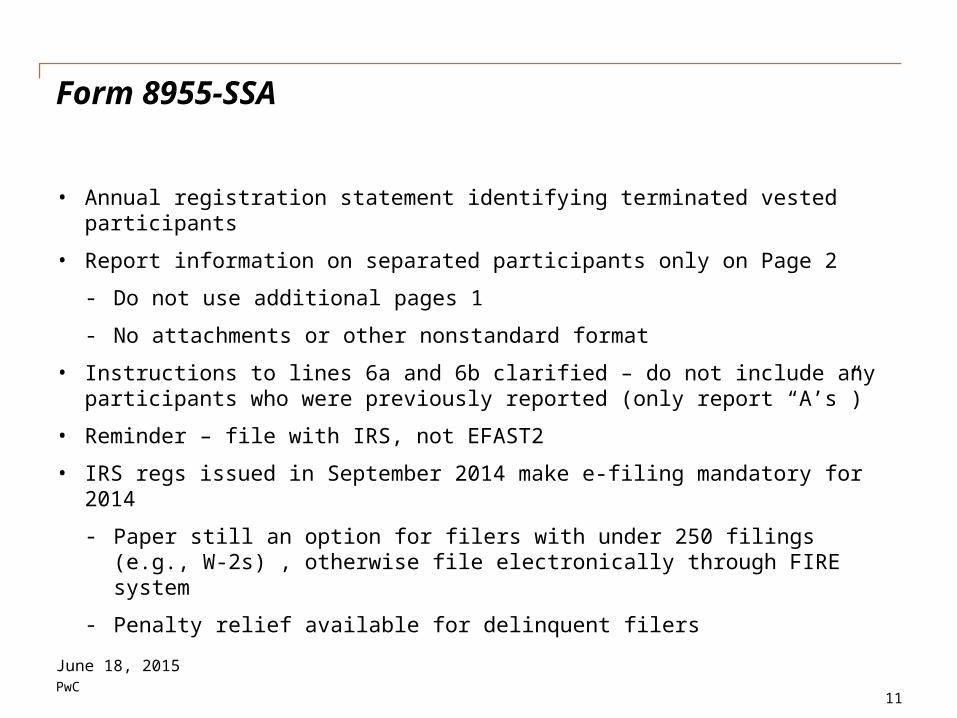

Form 8955-SSA

• Annual registration statement identifying terminated vested participants

• Report information on separated participants only on Page 2

- Do not use additional pages 1

- No attachments or other nonstandard format

• Instructions to lines 6a and 6b clarified – do not include any participants who were previously reported (only report “A’s”)

• Reminder – file with IRS, not EFAST2

• IRS regs issued in September 2014 make e-filing mandatory for 2014

- Paper still an option for filers with under 250 filings (e.g., W-2s) , otherwise file electronically through FIRE system

- Penalty relief available for delinquent filers

11

June 18, 2015

PwC

DOL enforcement

15 Day Letters - Incomplete Filings

• Missing Information

• Missing Accountant’s Report

15 Day Letters - Filings with Errors

45 Day Letters

• 45 Days to electronically file if filing was incorrectly filed on paper

• 45 Days to electronically sign the form with a valid signature

Note these are only electronic notices, DOL no longer sends paper notices

Email address used to transmit Form 5500 is the one that is used by DOL to send notices

Make sure to monitor the email account!!

12June 18, 2015

PwC

Amended filings

In response to DOL correspondence, you must amend your filing if correcting any errors.

The Entire filing must be filed

If you file Form 5500/5500-SF and receive 'Filing Error,' or 'Processing Stopped' status, you must check Box B on Form 5500/5500-SF to indicate “amended return” when submitting revised forms

Do not file as an amended return if previous submission attempts were not successfully received by EFAST2 due to transmission errors

13

June 18, 2015

PwC

DFVCP filings

• When filing, filer must check box on line C, Part 1 (Special Extension) of the Form 8955-SSA and enter “DFVCP” in the space provided on Line C

• Pilot program for non-ERISA plan filings – now permanent in Rev. Proc. 2015-32

- IRS provides late filing relief for plans not covered by DFVCP

◦ Penalty payment required - $500 per return up to a maximum of $1500

◦ “one participant” plans - covering only a 100% business owner (or owner and spouse) or one or more partners in a partnership (or partners and their spouses), and foreign plans

› Must file complete Form 5500 return, paper version and a transmittal schedule for each return (Form 14704 found on IRS website)

14

June 18, 2015

PwC

• IRS Notice 2014-35 provides relief for delinquent Forms 8955-SSA

• Penalties waived if DOL DFVCP requirements met for related Form 5500 series filing

• Paper Form 8955-SSA filed with IRS

• Must file delinquent Form s8955-SSA no later than 30 days after DFVCP filing

- Check the box in part 1, Line C and enter “DFVCP” in description

Delinquent Form 8955-SSA filings

15

June 18, 2015

PwC

What is auditor’s responsibility regarding the Form 5500?

• Notes to the financial statements must disclose differences, if any, between the financial statements and the Schedule H

◦ Remember, Schedule H must show actual dollar figures and not rounded dollar figures which are permitted on audited financial statements

• Common differences

- Due to timing differences related to methods of accounting

◦ If Form 5500 prepared on cash basis but financial statements prepared on an accrual basis

- Benefits payable

◦ Must be reported on Form 5500 but not on financial statements

16

June 18, 2015

PwC

Don’t just look at the Schedule H

• Codes used in Form 5500, Line 8a and 8b describe the benefits/features of the plan

◦ FYI - If new employee rolling over account from prior employer, the plan administrator can check the prior employer’s Form 5500 on EBSA see if “not intended to be qualified” code “3C” is listed

• Schedule C – expense information

• Schedule D – existence of master trust, DFEs

• Schedule G – prohibited transactions, leases or loans in default

• Schedule SB and H for contributions & receivables

17

June 18, 2015

PwC

Take a look at Schedule C

• Facilitates annual review of plan’s fees and expenses as part of a fiduciary’s on-going obligation to monitor service provider arrangements with the plan

• Report terminated accountants and actuaries

18

June 18, 2015

PwC

Expenses on Schedules H and C

Schedule H

• Reports expenses paid directly by plan/trust or where employer paid an expense and is reimbursed by plan

• Includes taxes (UBIT or foreign taxes paid on investments)

• Includes PBGC premiums

• Usually prepared on accrual basis, consistent with financial statements

Schedule C

• Frequently prepared on cash basis

• Includes indirect fees

• Does not include taxes or PBGC premiums

• Note – DOL has sent letters to plan sponsors where no fees shown on Form 5500

19

June 18, 2015

PwC

A word about delinquent participant contributions

• All delinquent contributions, whether or not corrected, must be reported on Line 4a of Schedule H until the year corrected

• Do not report on Line 4d (or Schedule G)

• Delinquent contributions that were corrected using VFCP and PTE 2002-51 are not considered PTs, so are not disclosed on a supplemental schedule

• Others may be reported on a separate schedule, see the instructions for the required format

• Filers may also include delinquent loan repayments

• Failure to make deferrals are not the same as delinquent contributions

20

June 18, 2015

PwC

Master trusts/DFEs

• Expenses reported at master trust level should not also be reported at plan level

• All expenses must be reported – either at trust level or at plan level

• Master trust footnote – review Schedule H for consistency

• Remember master trusts must always file Form 5500 DFEs

- Form 5500 filing is optional for 103-12 IE, CCTs and PSAs

- 103-12 IEs must attach audited financials

21

June 18, 2015

PwC

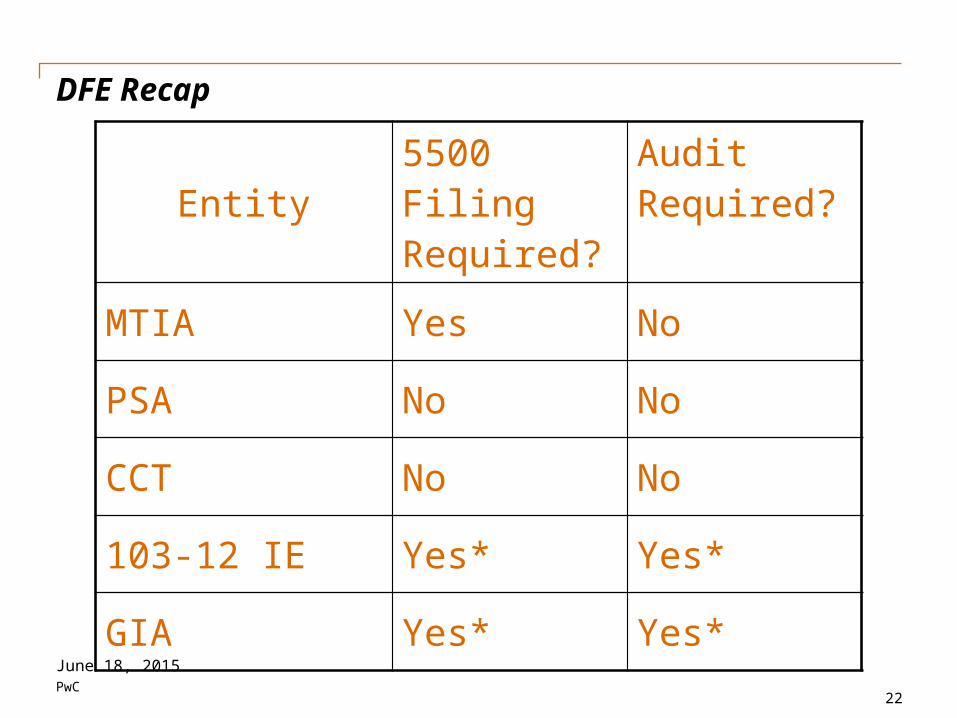

Entity5500 Filing Required?

Audit Required?

MTIA Yes No

PSA No No

CCT No No

103-12 IE Yes* Yes*

GIA Yes* Yes*

DFE Recap

22

June 18, 2015

PwC

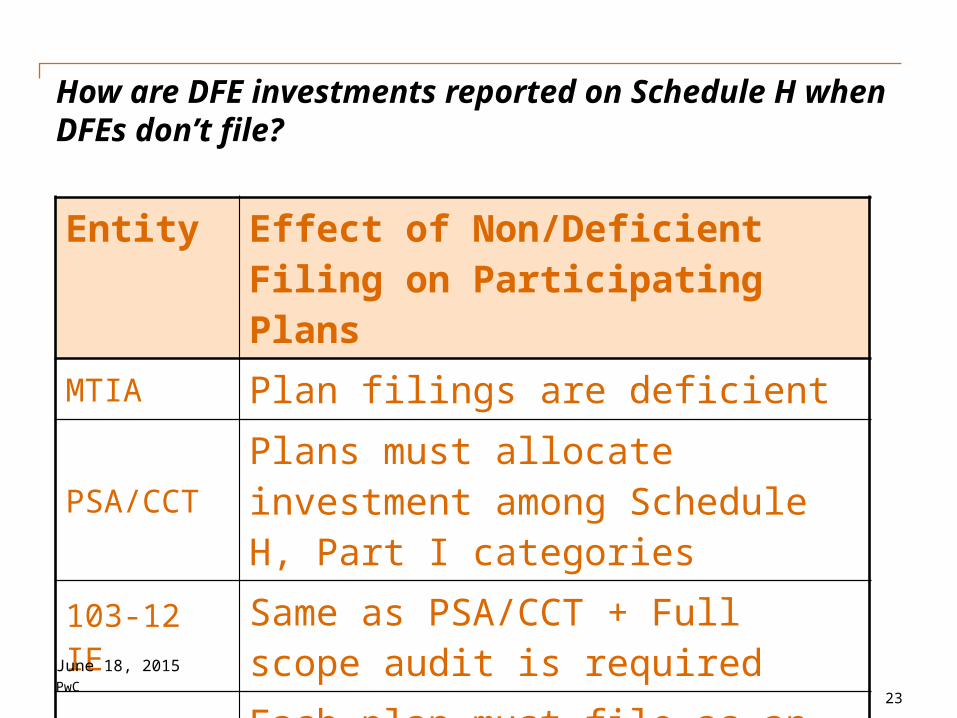

Entity Effect of Non/Deficient Filing on Participating Plans

MTIA Plan filings are deficient

PSA/CCTPlans must allocate investment among Schedule H, Part I categories

103-12 IESame as PSA/CCT + Full scope audit is required

GIA Each plan must file as an individual plan

How are DFE investments reported on Schedule H when DFEs don’t file?

23

June 18, 2015

PwC

Emerging issues

• IRS Form 8822-B was revised in October 2014

- Filing requirements that relate to business entities with an EIN, such as plan sponsors

◦ Abandoned EINs, or incorrect addresses

- Report address change, change in responsible party

- Currently no penalty for failure to file

• DOL focus on plan’s internal control environment

- Lost participants

- Uncashed benefit payment checks

- ERISA spending accounts

- Quality of audits

24

June 18, 2015

PwC

Other Developments

• DOL issued proposed regulations in September 2014 that would require electronic filing for top-hat and apprenticeship and training plan notices

- No changes in content

- Filers may immediately start using electronic systems to satisfy current paper filing requirement

- The new electronic filing system for both types of notices is accessible via the EBSA website

25

June 18, 2015

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.