2. engagement letter

11

-

Upload

syed-osama-rizvi -

Category

Education

-

view

174 -

download

1

Transcript of 2. engagement letter

APPOINTMENT LETTEROfficial written intimation by the

management to the auditor informing of his appointment as an auditor

Should be issued within 60 days of incorporation when the first

auditors are appointed or when a casual vacancy filled or when appointment is made by shareholders in

AGM orWhere SECP appoint (due to non-compliance)

ENGAGEMENT LETTERLetter sent by an auditor to his client, after

his appiontmentSpelling out the extent of his

responsibilities Confirming the acceptence of appointmentObjective and scope of auditThe extent of responsibilitiesForm of reports made to the client

CONTENTSAuditor’s ResponsibilityMangement’s ResponsibilityScope of an AuditManagement’s RepresentationIrregularities and FraudOther ServicesFeesClients Confirmation

CONTENTS (Additional)Arrangement regarding planning of auditConfirm the terms of letter by issuing

acknowledging recieptsForm of reportInvolvement of other auditors and experts Involvement of internal auditor and staffAny resteriction of the auditor’s liabilityAny further agreements between them

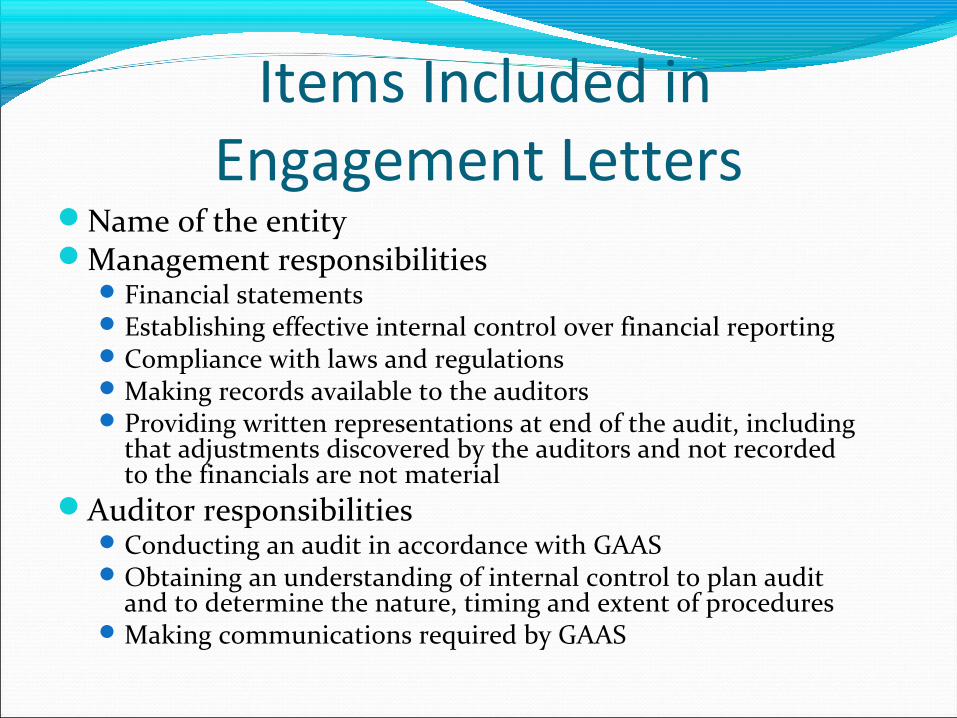

Items Included inEngagement Letters

Name of the entityManagement responsibilities

Financial statementsEstablishing effective internal control over financial reportingCompliance with laws and regulationsMaking records available to the auditorsProviding written representations at end of the audit, including

that adjustments discovered by the auditors and not recorded to the financials are not material

Auditor responsibilitiesConducting an audit in accordance with GAASObtaining an understanding of internal control to plan audit

and to determine the nature, timing and extent of proceduresMaking communications required by GAAS

Engagement LettersOptional Items

Arrangements regardingConduct of the audit (e.g., timing, client assistance)Use of specialists or internal auditorsObtaining information from predecessor auditorsFees and billing

Other services to be provided, such as examination of internal control over financial reporting

Limitation of or other arrangements regarding liability of auditors or client

Conditions under which access to the auditors’ working papers may be granted to others

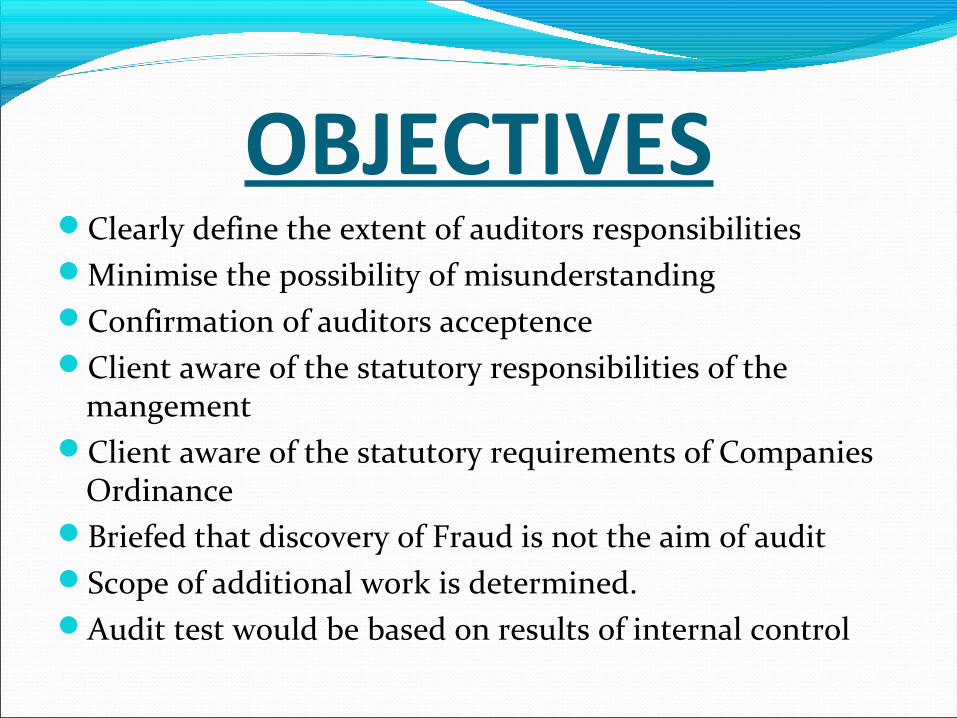

OBJECTIVESClearly define the extent of auditors responsibilities Minimise the possibility of misunderstandingConfirmation of auditors acceptenceClient aware of the statutory responsibilities of the

mangementClient aware of the statutory requirements of Companies

OrdinanceBriefed that discovery of Fraud is not the aim of auditScope of additional work is determined.Audit test would be based on results of internal control

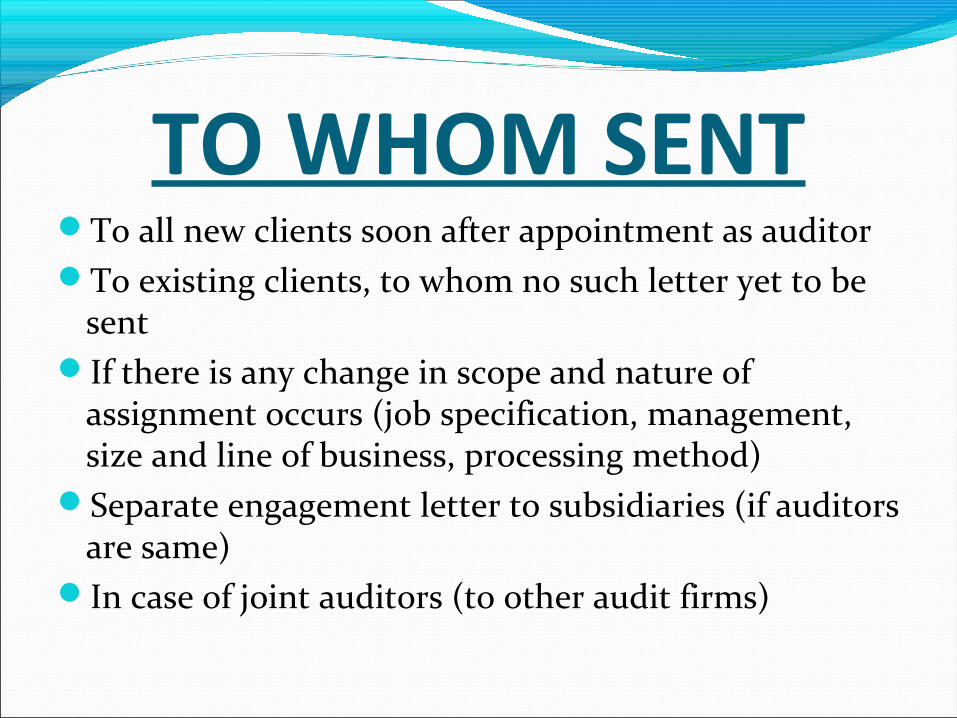

TO WHOM SENTTo all new clients soon after appointment as auditorTo existing clients, to whom no such letter yet to be

sentIf there is any change in scope and nature of

assignment occurs (job specification, management, size and line of business, processing method)

Separate engagement letter to subsidiaries (if auditors are same)

In case of joint auditors (to other audit firms)

Big 8 (until 1987)The firms were called the Big 8 for most of the 20th century, reflecting the international dominance of the eight largest accountancy firms:1.Arthur Andersen2.Arthur Young & Co.3.Coopers & Lybrand4.Ernst & Whinney (until 1979 Ernst & Ernst in the US and Whinney Murray in the UK)5.Deloitte Haskins & Sells (until 1978 Haskins & Sells in the US and Deloitte Plender Griffiths in the UK)6.Peat Marwick Mitchell, later Peat Marwick, then KPMG7.Price Waterhouse8.Touche Ross

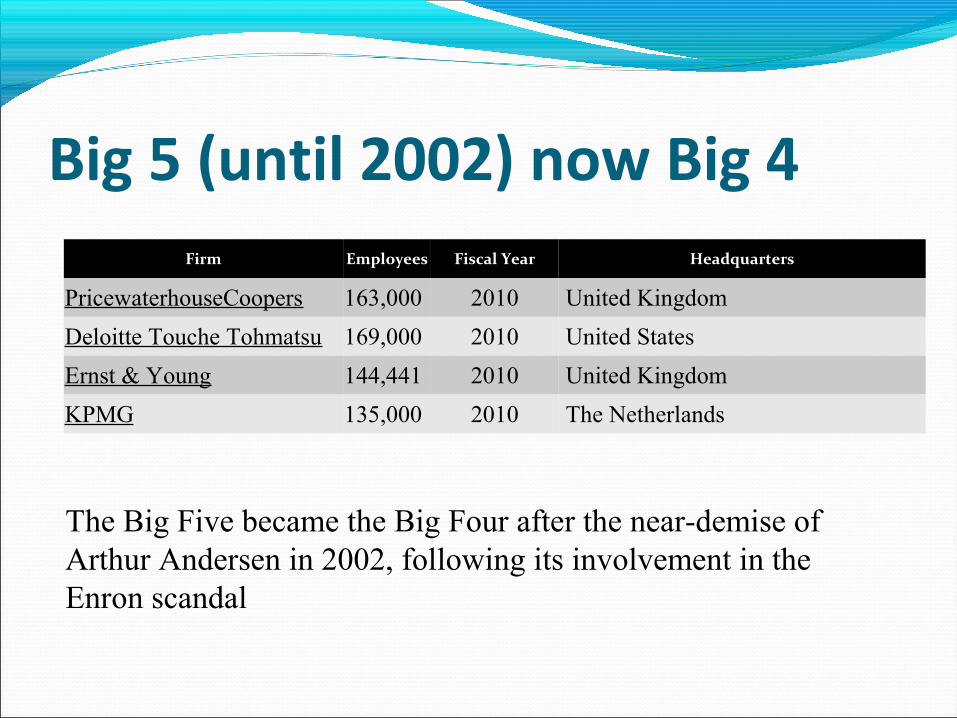

Firm Employees Fiscal Year Headquarters

PricewaterhouseCoopers 163,000 2010 United Kingdom

Deloitte Touche Tohmatsu 169,000 2010 United States

Ernst & Young 144,441 2010 United Kingdom

KPMG 135,000 2010 The Netherlands

Big 5 (until 2002) now Big 4

The Big Five became the Big Four after the near-demise of Arthur Andersen in 2002, following its involvement in the Enron scandal