2 Basic Managerial Accounting Concepts · HANS NELEMAN/THE IMAGE BANK/GETTY Chapter 2 Basic...

47

HANS NELEMAN/THE IMAGE BANK/GETTY Chapter 2 Basic Managerial Accounting Concepts After studying Chapter 2, you should be able to: ä 1 Explain the meaning of cost and how costs are assigned to products and services. ä 2 Define the various costs of manufacturing products and providing services as well as the costs of selling and administration. ä 3 Prepare income statements for manufacturing and service organizations. 28 NEL

Transcript of 2 Basic Managerial Accounting Concepts · HANS NELEMAN/THE IMAGE BANK/GETTY Chapter 2 Basic...

HA

NS

NE

LEM

AN

/TH

E IM

AG

E B

AN

K/G

ETT

Y

Chapter2 Basic ManagerialAccounting Concepts

After studying Chapter 2,you should be able to:

� 1 Explain the meaning of costand how costs are assigned toproducts and services.

� 2 Define the various costs ofmanufacturing products andproviding services as well asthe costs of selling andadministration.

� 3 Prepare income statements formanufacturing and serviceorganizations.

28 NEL

Experience Managerial DecisionsCanada’s Worst Cell Phone Bill

If you are reading this, the chances are that you own a

cell phone. About 75 percent of Canadians—some 25

million people—have a cell phone. Worldwide there are

some 5 billion cell phones. This makes the cell phone

industry one of the most profitable in the world.

The first mobile phone was produced by Motorola in

1973. It took about 10 years for the first cell phone (the

Motorola Dyna TAC) to become commercially available. In

the 1990s, commercially viable cellular networks mush-

roomed and cell usage took off, penetrating not only devel-

oped nations’ markets but also the developing economies.

The modern cell phone is not just a phone. It is also a

watch, a camera, a calculator, a calendar, and an alarm

clock. Modern mobile phones also support many other

services such as e-mail, Internet access, and gaming.

Bluetooth and infrared technology offer more advanced

computing ability through so-called ‘‘smart phones.’’

‘‘Canada’s Worst Cell Bill’’ (CBC Marketplace video)

offers insight into the exorbitant and questionable billing

practices of many cell service providers—practices that

will make you reconsider the details of your own cell plan.

How Does Your Plan Work?

. If it is a pay-as-you-go plan, do you have to add

more money so that the unused minutes you have

paid for do not expire?

. If you are using your cell phone abroad, what are

the roaming charges?

. If you have signed a contract, are you sure you

know what you have signed up for? And what are

your cancellation fees?

. Are incoming calls and texting really free?

. Overall, why do cell phone customers seem to be

so confused about the myriad charges they face?

What Is the Real Cost of a Cell Phone?

. How much does it cost you? And how little does it

cost the phone company?

. Is your cell company charging too much?

. What is the true cost of the service your cell com-

pany is providing?

. What drives the costs of cell usage?

. If the cost to you is 15 cents per minute and the

cost to the company is only one-third of a cent, is

the markup of 4,400 percent justified?

These and many such questions are dealt with through-

out this text. Through your managerial accounting stud-

ies, you will soon become a cost expert and be able to

answer these questions yourself.

NEL 29

The Meaning and Uses of Cost

One of the most important tasks of managerial accounting is to determine the costof products, services, customers, and other items of interest to managers. Therefore,we need to understand the meaning of cost and the ways in which costs can be usedto make decisions, both for small entrepreneurial businesses and for large interna-tional businesses. For example, consider a small gourmet restaurant and its ownerCourtney, who also is the head chef. In addition to understanding the complexitiesof gourmet food preparation, Courtney needs to understand the breakdown of therestaurant’s costs into various categories in order to make effective operating decisions.Cost categories of particular interest include direct costs (food and beverages) and indi-rect costs (laundry of linens). On a larger scale, local banks operating in universitycommunities often look at the cost of providing basic chequing account services to stu-dents. These accounts typically lose money—that is, the accounts cost more to servicethan they yield in fees and interest revenue. However, the bank finds that students al-ready banking with them are more likely to take out student loans through the bank,and these loans are very profitable. As a result, the bank may actually decide to expandits offerings to students when the related loan business is considered. Now, let’s define‘‘cost’’ and more fully describe its managerial importance.

CostCost is the amount of cash or cash equivalent sacrificed for goods and/or servicesthat are expected to bring a current or future benefit to the organization. If a furni-ture manufacturer buys lumber for $10,000, then the cost of that lumber is $10,000cash. Sometimes, one asset is traded for another asset. Then the cost of the new assetis measured by the value of the asset given up (the cash equivalent). If the samemanufacturer trades office equipment valued at $8,000 for a forklift, then the cost ofthe forklift is the $8,000 value of the office equipment traded for it. Cost is a dollar

Here’s The Real KickerKicker collects and analyzes many types ofcosts. In the manufacturing area, the companykeeps track of direct materials, direct labour,and overhead. These costs, of course, make upthe cost of goods sold that goes on Kicker’s monthlyincome statement. Nonmanufacturing costs include thecosts of selling and administration. However, this informa-tion is decomposed into a series of accounts that helpsKicker’s management in budgeting and decision making.

The sales function, for example, is broken down intothree areas: selling, customer service, and marketing. Sell-ing works directly with dealers and outside sales represen-tatives. Customer service handles calls from dealers anddecides whether or not a problem is covered under war-ranty. Marketing is responsible for advertising, promotions,and tent shows. One of the largest marketing events isKicker’s annual Big Air Bash, an extravaganza of music,food, cars, and extreme sports demonstrations. Held inconjunction with the Specialty Equipment Market Associa-tion (SEMA) show, the Big Air Bash is held outside of theHard Rock Hotel and Casino in Las Vegas. The expensesassociated with the show include the modification of showcars in Kicker’s in-house garage. Kicker mechanics custom-ized cars to make room for speakers and heavy-duty amps.With a souped-up engine, new fibreglass exterior, and

trick paint, the cars are ready for show. Other‘‘veteran’’ show cars and pickup trucks arerefreshed with additional trick paint, larger tires,and Kicker’s newest amps and speakers. You

can feel the music from outside the truck.Tent shows are smaller-scale affairs often held several

times a year throughout North America. Kicker brings itssemitrailer full of products and sound equipment as wellas a couple of show trucks. Then, a large tent is set up tosell Kicker merchandise, explain products, and sell the pre-vious year’s models at greatly reduced prices. Fun andrelaxed, the tent shows appeal to Kicker’s customer baseand provide a chance to look at the new models. The costof each tent show is carefully tracked and compared withthat show’s revenue. Sites that don’t provide sales revenuegreater than cost are not booked for the coming year.

Like many of today’s companies, Kicker tracks costscarefully for use in decision making. The general cost cate-gories discussed in this chapter help the company organ-ize cost information and relate it to decision making.

O B J E C T I V E � 1Explain the meaning of cost and howcosts are assigned to products andservices.

KIC

KE

R1

30 Chapter 2 Basic Managerial Accounting Concepts

NEL

measure of the resources used to achieve a given benefit. Managers strive to minimizethe cost of achieving benefits. Reducing the cost required to achieve a given benefitmeans that a firm is becoming more efficient.

Costs are incurred to produce future benefits. In a profit-making firm, those ben-efits usually mean revenues. As costs are used up in the production of revenues, theyare said to expire. Expired costs are called expenses. On the income statement,expenses are deducted from revenues to determine income (also called profit). For acompany to remain in business, revenues must be larger than expenses. In addition,the income earned must be large enough to satisfy the owners of the firm.

We can look more closely at the relationship between cost and revenue by focusingon the units sold. The revenue per unit is called price. In our everyday conversation,we have a tendency to use cost and price as synonyms, because the price of an item(e.g., a cell phone) is the cost to us. However, accounting courses take the viewpointof the owner of the company. In that case, cost and price are not the same. Instead, forthe company, revenue and price are the same. Price must be greater than cost in orderfor the firm to earn income. Hence, managers need to know cost and trends in cost.For example, the price a consumer pays for a fleece jacket from Roots might be $200,while the total cost that the company incurs to design, manufacture, deliver, andservice that jacket is much lower than the $200 price it charges consumers.

Accumulating and Assigning CostsAccumulating costs is the way that costs are measured and recorded. The accountingsystem typically does this job quite well. When a telephone bill comes into the com-pany, the bookkeeper records an addition to the telephone expense account and anaddition to the liability account, Accounts Payable. In this way, the cost is accumu-lated. It would be easy to tell, at the end of the year, the total spending on telephoneexpense. Accumulating costs tells the company what was spent. However, that usuallyis not enough information. The company also wants to know why the money wasspent. In other words, it wants to know how costs were assigned to cost objects.

Assigning costs is the way that a cost is linked to some cost object. A cost objectis something for which a company wants to know the cost. For example, of the totaltelephone expense, how much was for the sales department, and how much was formanufacturing? Assigning costs tells the company why the money was spent. In thiscase, cost assignment tells whether the money spent on telephone expense was tosupport the manufacturing or the selling of the product. As we will discuss in laterchapters, cost assignment typically is more difficult than cost accumulation.

Cost ObjectsManagerial accounting systems are structured to measure and assign costs to entitiescalled cost objects. A cost object is any item such as a product, customer, department,project, geographic region, plant, and so on, for which costs are measured andassigned. For example, if the Royal Bank of Canada wants to determine the cost ofa platinum credit card, then the cost object is the platinum credit card. All costsrelated to the platinum card are added in, such as the cost of mailings to potentialcustomers, the cost of telephone lines dedicated to the card, the portion of the com-puter department that processes platinum card transactions and bills, and so on. In amore personal example, suppose that you are considering taking a course during thesummer session. Taking the course is the cost object, and the cost would includetuition, books, fees, transportation, and (possibly) housing. Notice that you couldalso include the forgone earnings from a summer job (assuming that you cannotwork while taking summer classes), which would be an opportunity cost. (The con-cept of opportunity cost will be discussed more fully later in this chapter.)

We will discuss various methods of assigning costs to cost objects in the succeed-ing chapters.

Chapter 2 Basic Managerial Accounting Concepts 31

NEL

Assigning Costs to Cost ObjectsCosts can be assigned to cost objects in a number of ways. Relatively speaking, somemethods are more accurate, and others are simpler. The choice of a method dependson a number of factors, such as the need for accuracy. The notion of accuracy is a rela-tive concept and has to do with the reasonableness and logic of the cost assignmentmethods used. The objective is to measure and assign costs as well as possible, givenmanagement objectives. For example, suppose you and three of your friends go out todinner at a local pizza parlor. When the bill comes, everything has been added togetherfor a total of $36. How much is your share? One easy way to find your share is todivide the bill evenly among you and your friends. In that case, you each owe$9 ($36/4). But suppose that one of you had a small salad and drink (totalling $5),while another had a specialty pizza, appetizer, and beer (totalling $15). Clearly, it is pos-sible to identify what each person had and assign costs that way. The second method ismore accurate, but also more work. Which method you choose will depend on howimportant it is to you to assign the specific meal costs to each individual. It is the sameway in accounting. There are a number of ways to assign costs to cost objects. Somemethods are quick and easy but may be inaccurate. Other methods are much more accu-rate, but involve much more work (in business, more work equals more expense).

Cost ClassificationA cost is a payment of cash or the commitment to pay cash in the future for the pur-pose of generating revenues. For example, cash or a note payable signed to purchasesupplies is the cost of supplies. In managerial accounting, costs are classified accord-ing to the decision-making needs of management.

Different costs are used for different purposes. Cost definitions can vary accord-ing to the objective being served. Thus costs can be classified into groups using avariety of criteria. The classification of costs helps make sense of the great varietyof costs, which facilitates decision making.

The following cost groups and terms are introduced and defined later in thischapter:

. Direct costs (material and labour)

. Indirect costs (material and labour)

. Prime costs

. Conversion costs

. Product costs

. Period costs

. Variable costs (step costs and not)

. Fixed costs (committed and discretionary)

. Mixed costs

. Selling costs

. Administrative costs

It should be emphasized that there is only one pool of costs. Then, using differ-ent criteria, we can ‘‘break out’’ the pool into various categories. So the pool of costscan be classified as—for example—‘‘Direct or Indirect Costs,’’ ‘‘Prime or ConversionCosts,’’ ‘‘Product or Period Costs,’’ ‘‘Selling or Administrative Costs,’’ or ‘‘Variable,Fixed, or Mixed Costs.’’

To facilitate control, selling and administrative expenses may be reported by levelof responsibility. For example, selling expenses may be reported in terms of products,salespersons, departments, divisions, or territories. Likewise, administrative expensesmay be reported in terms of areas such as human resources, computer services, legal,accounting, or finance.

Step costs are costs that vary at quantity intervals. For example, if a hotel house-keeper is expected to clean 10 rooms per shift, the cost of hiring an additional house-keeper changes with every 11th, 21st, and 31st room that is occupied. The costremains the same, however, for any occupancy rate between zero and 10, 11 and 20,21 and 30 rooms, and so on.

32 Chapter 2 Basic Managerial Accounting Concepts

NEL

Committed fixed costs cannot be avoided. For example, an executive’s salary andthe amount of amortization represent committed fixed costs. Discretionary fixed costscan be modified. For example, research and development costs and advertising costscan be curtailed under budgetary constraints.

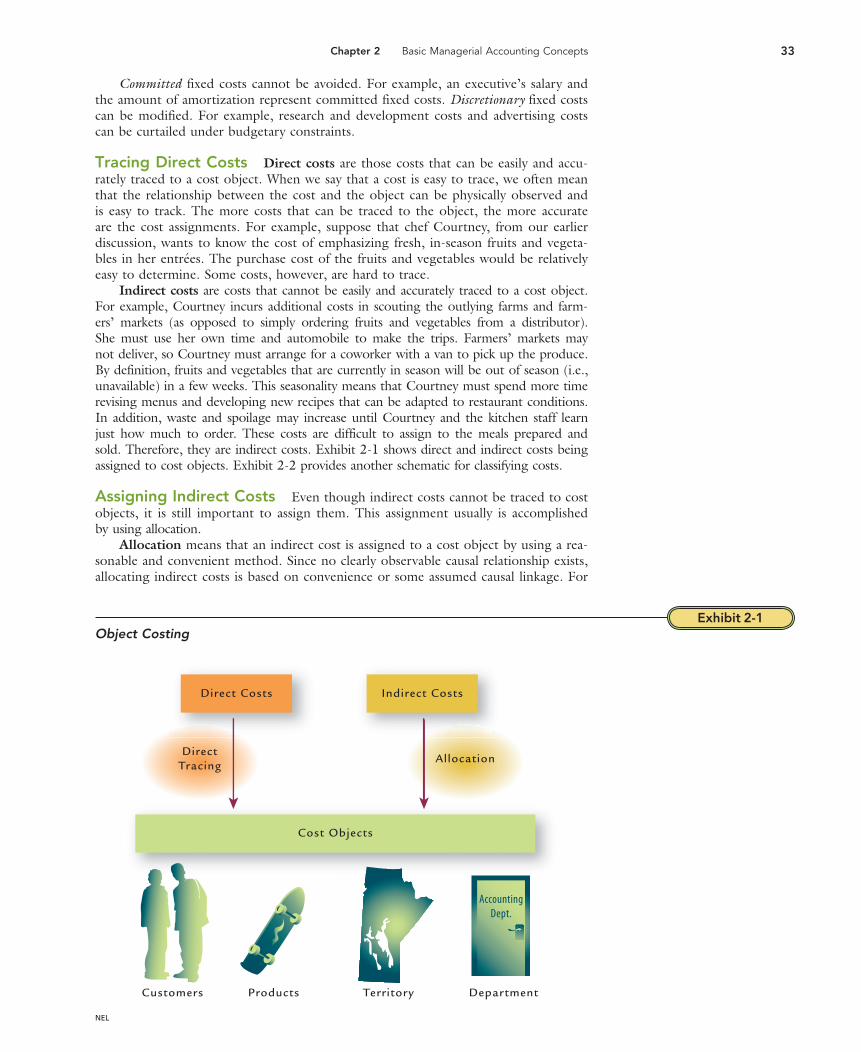

Tracing Direct Costs Direct costs are those costs that can be easily and accu-rately traced to a cost object. When we say that a cost is easy to trace, we often meanthat the relationship between the cost and the object can be physically observed andis easy to track. The more costs that can be traced to the object, the more accurateare the cost assignments. For example, suppose that chef Courtney, from our earlierdiscussion, wants to know the cost of emphasizing fresh, in-season fruits and vegeta-bles in her entrees. The purchase cost of the fruits and vegetables would be relativelyeasy to determine. Some costs, however, are hard to trace.

Indirect costs are costs that cannot be easily and accurately traced to a cost object.For example, Courtney incurs additional costs in scouting the outlying farms and farm-ers’ markets (as opposed to simply ordering fruits and vegetables from a distributor).She must use her own time and automobile to make the trips. Farmers’ markets maynot deliver, so Courtney must arrange for a coworker with a van to pick up the produce.By definition, fruits and vegetables that are currently in season will be out of season (i.e.,unavailable) in a few weeks. This seasonality means that Courtney must spend more timerevising menus and developing new recipes that can be adapted to restaurant conditions.In addition, waste and spoilage may increase until Courtney and the kitchen staff learnjust how much to order. These costs are difficult to assign to the meals prepared andsold. Therefore, they are indirect costs. Exhibit 2-1 shows direct and indirect costs beingassigned to cost objects. Exhibit 2-2 provides another schematic for classifying costs.

Assigning Indirect Costs Even though indirect costs cannot be traced to costobjects, it is still important to assign them. This assignment usually is accomplishedby using allocation.

Allocation means that an indirect cost is assigned to a cost object by using a rea-sonable and convenient method. Since no clearly observable causal relationship exists,allocating indirect costs is based on convenience or some assumed causal linkage. For

Exhibit 2-1Object Costing

DirectTracing

Customers

Direct Costs

Cost Objects

Indirect Costs

Allocation

Products Territory Department

AccountingDept.

Chapter 2 Basic Managerial Accounting Concepts 33

NEL

example, consider the cost of heating and lighting a plant in which five products aremanufactured. Suppose that this utility cost is to be assigned to these five products.It is difficult to see any causal relationship between utility costs and each unit of productmanufactured. Therefore, a convenient way to allocate this cost is to assign it in propor-tion to the direct labour hours used by each product. This method is relatively easy andaccomplishes the purpose of ensuring that all costs are assigned to units produced. Allo-cating indirect costs is important for a variety of reasons. For example, allocating indirectcosts to products is needed to determine the value of inventory and of cost of goodssold. Perhaps more important, as companies become more complex in the number andtypes of products and services they offer to customers, the need to understand, allocate,and effectively control indirect costs becomes increasingly important. In addition, indirectcosts represent an increasingly large percentage of total costs for many companies.

Direct and indirect costs occur in service businesses as well. For example, abank’s cost of printing and mailing monthly statements to chequing account holdersis a direct cost of the product—chequing accounts. However, the cost of office furni-ture in the bank is an indirect cost for the chequing accounts.

Other Categories of Cost In addition to being categorized as either director indirect, costs are often analyzed with respect to their behaviour patterns, or theway in which a cost changes when the level of the output changes.

A variable cost is one that increases in total as output increases and decreases intotal as output decreases. For example, the denim used in making jeans is a variablecost. As the company makes more jeans, it needs more denim.

A fixed cost is a cost that does not increase in total as output increases and does notdecrease in total as output decreases. For example, the cost of property taxes on the fac-tory building stays the same no matter how many pairs of jeans the company makes.How can that be, since property taxes can and do change? While the cost changes, it isnot because output changes. Rather, it changes because the city or county governmentdecides to raise taxes. Variable and fixed costs are covered more extensively in Chapter 3.

Most costs are neither fixed nor variable; they are mixed, having both variableand fixed components.

An opportunity cost is the benefit given up or sacrificedwhen one alternative is chosen over another. For example, anopportunity cost of being in accounting class may be the wagesyou would have earned during that time if you were workingrather than going to school. Opportunity cost differs fromaccounting cost in that the opportunity cost is never includedin the accounting records, because it is the cost of somethingthat did not occur. Opportunity costs are important to decisionmaking, as we will see more clearly in Chapter 9.

We will discuss various methods of assigning costs to costobjects in the succeeding chapters.

Make a list of the costs you are incurring for your classes thisterm. Which costs are direct costs for your university course(s)?Which costs are indirect? Now, from your list of total costs, whichones are direct costs of this course? Which are indirect?

Answers on pages 711 to 715.

Exhibit 2-2Cost Classification

Cost Classification Types of Costs

A. In relation to cost object Direct (easily traceable)Indirect (nontraceable needs to be allocated)

B. In relation to changes of activity Fixed (total remains constant in the relevant range)Variable (total varies according to the level of activity)Mixed (part variable, part fixed)Step (it increases at certain activity levels)

C. In relation to the classification in the financial statements Product (inventorial)PrimeConversion

Period (expensed)

34 Chapter 2 Basic Managerial Accounting Concepts

NEL

Product and Service Costs

Output represents one of the most important cost objects. There are two types of out-put: products and services.

Products are goods produced by converting raw materials through the use oflabour and indirect manufacturing resources, such as the manufacturing plant, land,and machinery. Televisions, hamburgers, automobiles, computers, clothes, and furni-ture are examples of products.

Services are tasks or activities performed for a customer or an activity performedby a customer using an organization’s products or facilities. Insurance coverage, med-ical care, dental care, funeral care, and accounting are examples of service activitiesperformed for customers. Car rental, video rental, and skiing are examples of serviceswhere the customer uses an organization’s products or facilities.

Organizations that produce products are called manufacturing organizations.Organizations that provide services are called service organizations. Managers ofboth types of organizations need to know how much individual products or servicescost. Accurate cost information is vital for profitability analysis and strategic decisionsconcerning product design, pricing, and product mix. Incidentally, retail organiza-tions, such as La Senza, buy finished products from other organizations, such asmanufacturers, and then sell them to customers. The accounting for inventory and costof goods sold for retail organizations, often referred to as merchandisers, is much simplerthan for manufacturing organizations and is usually covered extensively in introductoryfinancial accounting courses. Therefore, the focus here is on manufacturing and serviceorganizations.

Services differ from products in many ways. First, a service is intangible. Thebuyers of services cannot see, feel, hear, or taste a service before it is bought. Second,services are perishable; they cannot be stored for future use by a consumer but mustbe consumed when performed. Inventory valuation, so important for products, is notan issue for services. In other words, because service organizations do not produceand sell products as part of their regular operations, they have no inventory asset onthe balance sheet. Third, providers of services and buyers of services must usually bein direct contact for an exchange to take place. For example, an eye examinationrequires both the patient and the optometrist to be present. However, producers ofproducts need not have direct contact with the buyers of their goods. Thus, buyersof automobiles never need to have contact with the engineers and assembly lineworkers that produced their automobiles. The overall way in which a company costsservices in terms of classifying related costs as either direct or indirect is very similarto the way in which it costs products. The main difference in costing is that productshave inventories, and services do not.

ETHICS Tracking costs can also act as an early warning system for unauthorizedactivity and possible ethical problems. For example, Metropolitan Life InsuranceCompany was dismayed to learn that some of its agents were selling policies asretirement plans. This practice is illegal, and it cost the company more than $20 mil-lion in fines as well as $50 million in refunds to policyholders.1 More accurate andcomprehensive data tracking regarding sales, individual agents, types of policies, andpolicyholders could have alerted Metropolitan Life to a potential problem. Thus, wecan see that tracking costs can serve many different and important purposes.u

Product CostsManagerial accountants must decide what types of managerial accounting informationto provide to managers, how to measure such information, and when and to whomto communicate the information. For example, when making most strategic andoperating decisions, managers typically rely on managerial accounting informationthat is prepared in whatever manner the managerial accountant believes provides the

O B J E C T I V E � 2Define the various costs ofmanufacturing products and providingservices as well as the costs of selling andadministration.

1Roush, Chris, ‘‘Fields of Green—and Disaster Areas,’’ Business Week (January 9, 1995): 94.

Chapter 2 Basic Managerial Accounting Concepts 35

NEL

best analysis for the decision at hand. Therefore, the majority of the managerialaccounting issues explained in this book do not reference a formal set of externalrules, but instead consider the context of the given decision (relevant vs. irrelevantcost information for make-or-buy decisions, full cost vs. functional cost informationfor pricing decisions, etc.).

However, there is one major exception. Managerial accountants must follow spe-cific external reporting rules (i.e., generally accepted accounting principles) whentheir companies provide outside parties with cost information about the amount ofending inventory on the balance sheet and the cost of goods sold on the incomestatement. In order to calculate these two amounts, managerial accountants mustsubdivide costs into functional categories: production and period (i.e., nonproduc-tion). The following section describes the process for categorizing costs as eitherproduct or period in nature.

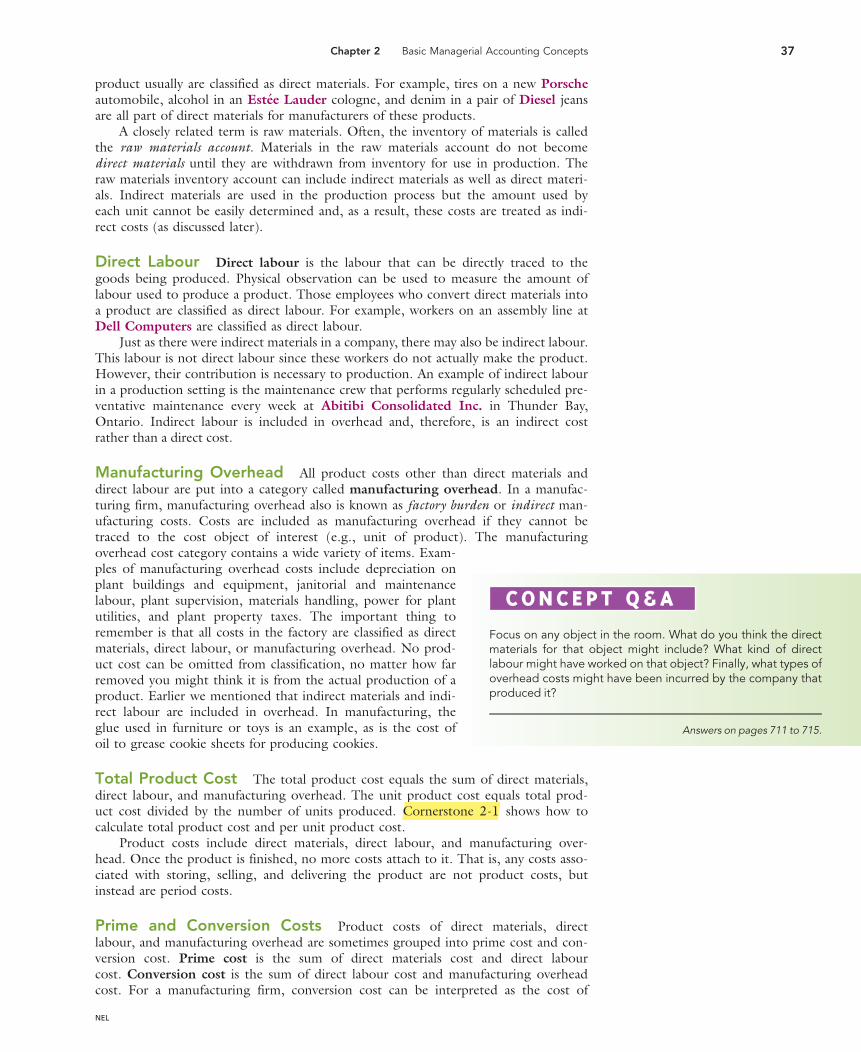

Product (manufacturing) costs are those costs, both direct and indirect, ofproducing a product in a manufacturing firm or of acquiring a product in a mer-chandising firm and preparing it for sale. Therefore, only costs in the production sec-tion of the value chain are included in product costs. A key feature of product costsis that they are inventoried. Product costs initially are added to an inventory accountand remain in inventory until they are sold, at which time they are transferred tocost of goods sold (COGS). Product costs can be further classified as direct materi-als, direct labour, and manufacturing overhead, which are the three cost elementsthat can be assigned to products for external financial reporting (e.g., inventories orCOGS). Exhibit 2-3 shows how direct materials, direct labour, and overhead becomeproduct costs.

Direct Materials Direct materials are those materials that are a part of the finalproduct and can be directly traced to the goods being produced. The cost of thesematerials can be directly charged to products because physical observation can beused to measure the quantity used by each product. Materials that become part of a

Exhibit 2-3Product Costs Include Direct Materials, Direct Labour, and Overhead

Direct Materials

Product CostDirect Labour

Overhead

Jeep

36 Chapter 2 Basic Managerial Accounting Concepts

NEL

product usually are classified as direct materials. For example, tires on a new Porscheautomobile, alcohol in an Estee Lauder cologne, and denim in a pair of Diesel jeansare all part of direct materials for manufacturers of these products.

A closely related term is raw materials. Often, the inventory of materials is calledthe raw materials account. Materials in the raw materials account do not becomedirect materials until they are withdrawn from inventory for use in production. Theraw materials inventory account can include indirect materials as well as direct materi-als. Indirect materials are used in the production process but the amount used byeach unit cannot be easily determined and, as a result, these costs are treated as indi-rect costs (as discussed later).

Direct Labour Direct labour is the labour that can be directly traced to thegoods being produced. Physical observation can be used to measure the amount oflabour used to produce a product. Those employees who convert direct materials intoa product are classified as direct labour. For example, workers on an assembly line atDell Computers are classified as direct labour.

Just as there were indirect materials in a company, there may also be indirect labour.This labour is not direct labour since these workers do not actually make the product.However, their contribution is necessary to production. An example of indirect labourin a production setting is the maintenance crew that performs regularly scheduled pre-ventative maintenance every week at Abitibi Consolidated Inc. in Thunder Bay,Ontario. Indirect labour is included in overhead and, therefore, is an indirect costrather than a direct cost.

Manufacturing Overhead All product costs other than direct materials anddirect labour are put into a category called manufacturing overhead. In a manufac-turing firm, manufacturing overhead also is known as factory burden or indirect man-ufacturing costs. Costs are included as manufacturing overhead if they cannot betraced to the cost object of interest (e.g., unit of product). The manufacturingoverhead cost category contains a wide variety of items. Exam-ples of manufacturing overhead costs include depreciation onplant buildings and equipment, janitorial and maintenancelabour, plant supervision, materials handling, power for plantutilities, and plant property taxes. The important thing toremember is that all costs in the factory are classified as directmaterials, direct labour, or manufacturing overhead. No prod-uct cost can be omitted from classification, no matter how farremoved you might think it is from the actual production of aproduct. Earlier we mentioned that indirect materials and indi-rect labour are included in overhead. In manufacturing, theglue used in furniture or toys is an example, as is the cost ofoil to grease cookie sheets for producing cookies.

Total Product Cost The total product cost equals the sum of direct materials,direct labour, and manufacturing overhead. The unit product cost equals total prod-uct cost divided by the number of units produced. Cornerstone 2-1 shows how tocalculate total product cost and per unit product cost.

Product costs include direct materials, direct labour, and manufacturing over-head. Once the product is finished, no more costs attach to it. That is, any costs asso-ciated with storing, selling, and delivering the product are not product costs, butinstead are period costs.

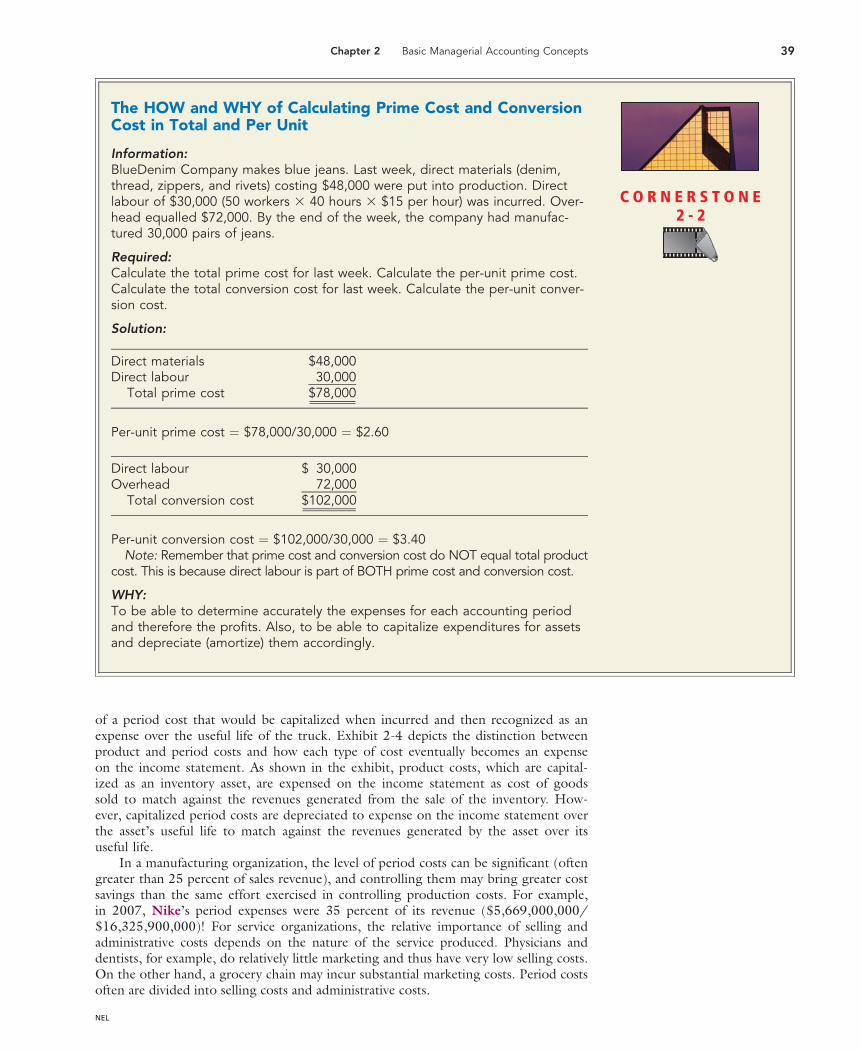

Prime and Conversion Costs Product costs of direct materials, directlabour, and manufacturing overhead are sometimes grouped into prime cost and con-version cost. Prime cost is the sum of direct materials cost and direct labourcost. Conversion cost is the sum of direct labour cost and manufacturing overheadcost. For a manufacturing firm, conversion cost can be interpreted as the cost of

Focus on any object in the room. What do you think the directmaterials for that object might include? What kind of directlabour might have worked on that object? Finally, what types ofoverhead costs might have been incurred by the company thatproduced it?

Answers on pages 711 to 715.

Chapter 2 Basic Managerial Accounting Concepts 37

NEL

converting raw materials into a final product. Cornerstone 2-2shows how to calculate prime cost and conversion cost for amanufactured product.

Period CostsThe costs of production are assets that are carried in inventoriesuntil the goods are sold. There are other costs of running acompany, referred to as period costs, that are not carried in in-ventory.

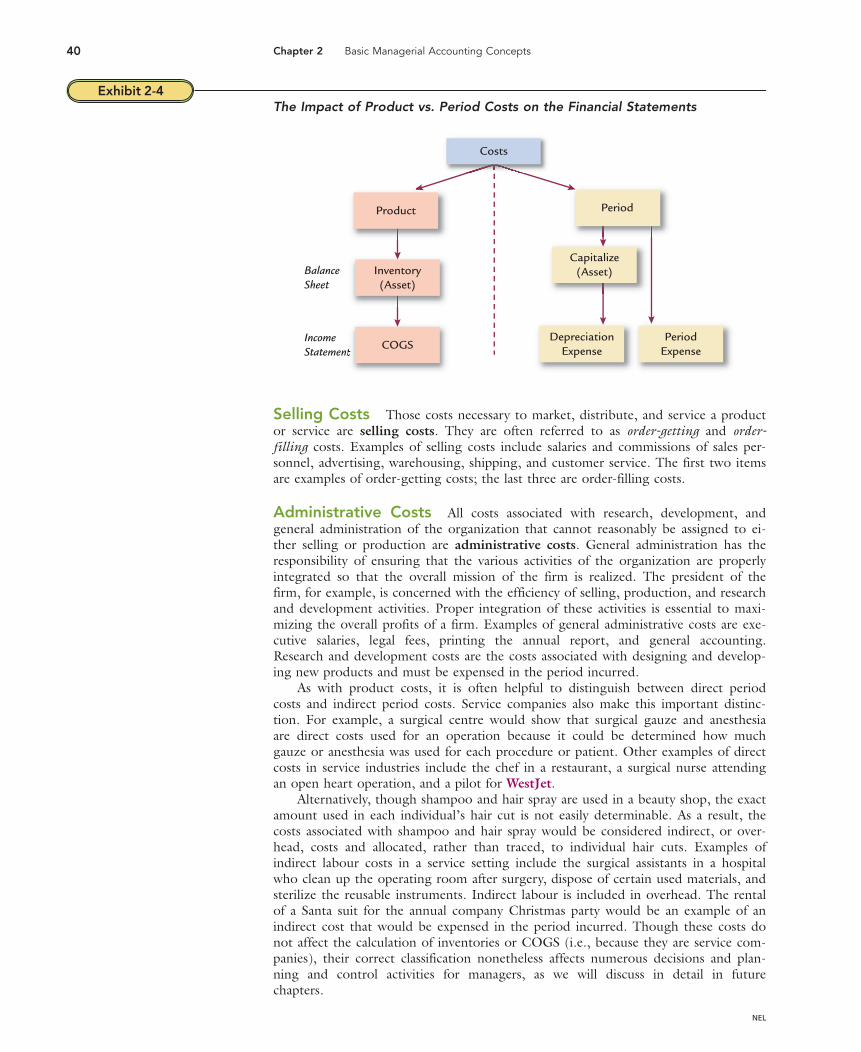

Period costs are all costs that are not product costs (i.e.,all areas of the value chain except for production). The cost of office supplies,research and development activities, the CEO’s salary, and advertising are examples ofperiod costs. For example, a 30-second advertisement during highly watched showssuch as the Super Bowl costs $1 million or so. The Super Bowl’s ratings are high,with many millions of people watching; even so, there are some who question thewisdom of spending such high sums of money for 30 seconds of advertising expo-sure. Managerial accountants help executives at companies like Apple Computerdetermine whether such costly advertising campaigns generate enough additionalsales revenue over the long run to make them profitable.

Period costs cannot be assigned to products or appear as part of the reported val-ues of inventories on the balance sheet. Instead, period costs typically are expensed inthe period in which they are incurred. However, if a period cost is expected to pro-vide an economic benefit (i.e., revenues) beyond the next year, then it is recorded asan asset (i.e., capitalized) and allocated to expense through depreciation throughoutits useful life. The cost associated with the purchase of a delivery truck is an example

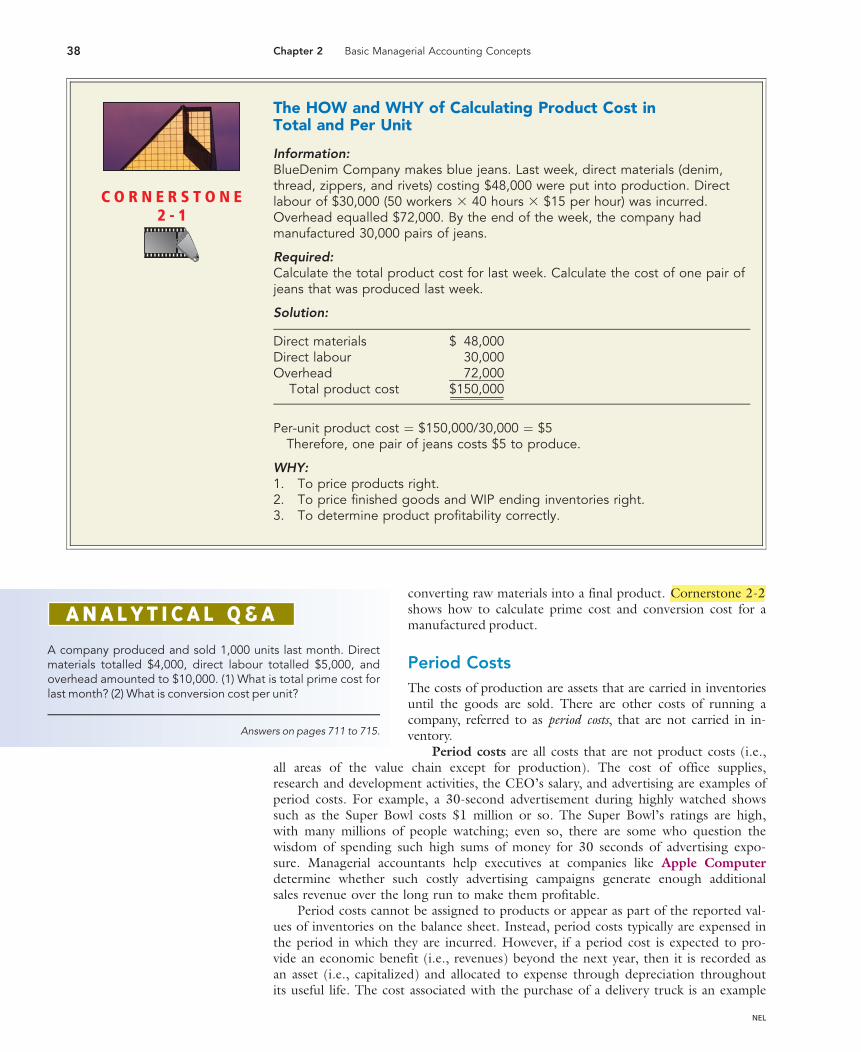

The HOW and WHY of Calculating Product Cost inTotal and Per Unit

Information:BlueDenim Company makes blue jeans. Last week, direct materials (denim,thread, zippers, and rivets) costing $48,000 were put into production. Directlabour of $30,000 (50 workers 3 40 hours 3 $15 per hour) was incurred.Overhead equalled $72,000. By the end of the week, the company hadmanufactured 30,000 pairs of jeans.

Required:Calculate the total product cost for last week. Calculate the cost of one pair ofjeans that was produced last week.

Solution:

Direct materials $ 48,000Direct labour 30,000Overhead 72,000

Total product cost $150,000

Per-unit product cost ¼ $150,000/30,000 ¼ $5Therefore, one pair of jeans costs $5 to produce.

WHY:1. To price products right.2. To price finished goods and WIP ending inventories right.3. To determine product profitability correctly.

C O R N E R S T O N E2 - 1

A company produced and sold 1,000 units last month. Directmaterials totalled $4,000, direct labour totalled $5,000, andoverhead amounted to $10,000. (1) What is total prime cost forlast month? (2) What is conversion cost per unit?

Answers on pages 711 to 715.

38 Chapter 2 Basic Managerial Accounting Concepts

NEL

of a period cost that would be capitalized when incurred and then recognized as anexpense over the useful life of the truck. Exhibit 2-4 depicts the distinction betweenproduct and period costs and how each type of cost eventually becomes an expenseon the income statement. As shown in the exhibit, product costs, which are capital-ized as an inventory asset, are expensed on the income statement as cost of goodssold to match against the revenues generated from the sale of the inventory. How-ever, capitalized period costs are depreciated to expense on the income statement overthe asset’s useful life to match against the revenues generated by the asset over itsuseful life.

In a manufacturing organization, the level of period costs can be significant (oftengreater than 25 percent of sales revenue), and controlling them may bring greater costsavings than the same effort exercised in controlling production costs. For example,in 2007, Nike’s period expenses were 35 percent of its revenue ($5,669,000,000/$16,325,900,000)! For service organizations, the relative importance of selling andadministrative costs depends on the nature of the service produced. Physicians anddentists, for example, do relatively little marketing and thus have very low selling costs.On the other hand, a grocery chain may incur substantial marketing costs. Period costsoften are divided into selling costs and administrative costs.

The HOW and WHY of Calculating Prime Cost and ConversionCost in Total and Per Unit

Information:BlueDenim Company makes blue jeans. Last week, direct materials (denim,thread, zippers, and rivets) costing $48,000 were put into production. Directlabour of $30,000 (50 workers 3 40 hours 3 $15 per hour) was incurred. Over-head equalled $72,000. By the end of the week, the company had manufac-tured 30,000 pairs of jeans.

Required:Calculate the total prime cost for last week. Calculate the per-unit prime cost.Calculate the total conversion cost for last week. Calculate the per-unit conver-sion cost.

Solution:

Direct materials $48,000Direct labour 30,000

Total prime cost $78,000

Per-unit prime cost ¼ $78,000/30,000 ¼ $2.60

Direct labour $ 30,000Overhead 72,000

Total conversion cost $102,000

Per-unit conversion cost ¼ $102,000/30,000 ¼ $3.40Note: Remember that prime cost and conversion cost do NOT equal total product

cost. This is because direct labour is part of BOTH prime cost and conversion cost.

WHY:To be able to determine accurately the expenses for each accounting periodand therefore the profits. Also, to be able to capitalize expenditures for assetsand depreciate (amortize) them accordingly.

C O R N E R S T O N E2 - 2

Chapter 2 Basic Managerial Accounting Concepts 39

NEL

Selling Costs Those costs necessary to market, distribute, and service a productor service are selling costs. They are often referred to as order-getting and order-filling costs. Examples of selling costs include salaries and commissions of sales per-sonnel, advertising, warehousing, shipping, and customer service. The first two itemsare examples of order-getting costs; the last three are order-filling costs.

Administrative Costs All costs associated with research, development, andgeneral administration of the organization that cannot reasonably be assigned to ei-ther selling or production are administrative costs. General administration has theresponsibility of ensuring that the various activities of the organization are properlyintegrated so that the overall mission of the firm is realized. The president of thefirm, for example, is concerned with the efficiency of selling, production, and researchand development activities. Proper integration of these activities is essential to maxi-mizing the overall profits of a firm. Examples of general administrative costs are exe-cutive salaries, legal fees, printing the annual report, and general accounting.Research and development costs are the costs associated with designing and develop-ing new products and must be expensed in the period incurred.

As with product costs, it is often helpful to distinguish between direct periodcosts and indirect period costs. Service companies also make this important distinc-tion. For example, a surgical centre would show that surgical gauze and anesthesiaare direct costs used for an operation because it could be determined how muchgauze or anesthesia was used for each procedure or patient. Other examples of directcosts in service industries include the chef in a restaurant, a surgical nurse attendingan open heart operation, and a pilot for WestJet.

Alternatively, though shampoo and hair spray are used in a beauty shop, the exactamount used in each individual’s hair cut is not easily determinable. As a result, thecosts associated with shampoo and hair spray would be considered indirect, or over-head, costs and allocated, rather than traced, to individual hair cuts. Examples ofindirect labour costs in a service setting include the surgical assistants in a hospitalwho clean up the operating room after surgery, dispose of certain used materials, andsterilize the reusable instruments. Indirect labour is included in overhead. The rentalof a Santa suit for the annual company Christmas party would be an example of anindirect cost that would be expensed in the period incurred. Though these costs donot affect the calculation of inventories or COGS (i.e., because they are service com-panies), their correct classification nonetheless affects numerous decisions and plan-ning and control activities for managers, as we will discuss in detail in futurechapters.

Exhibit 2-4The Impact of Product vs. Period Costs on the Financial Statements

Period

PeriodExpense

BalanceSheet

IncomeStatement

Costs

Capitalize(Asset)

DepreciationExpense

Product

Inventory(Asset)

COGS

40 Chapter 2 Basic Managerial Accounting Concepts

NEL

Preparing Financial Statements forManufacturing Operations

The earlier definitions of product, selling, and administrative costs provide a goodconceptual overview of these important costs. However, the actual calculation ofthese costs in practice is a bit more complicated. Let’s take a closer look at just howcosts are calculated for purposes of preparing the external financial statements, focus-ing first on manufacturing firms.

Financial Statements for Manufacturing OperationsThe operations of a business can be classified as one of the following:

. service

. merchandising

. manufacturing

The accounting for service and merchandising businesses is described and illus-trated in basically all financial accounting courses. This text focuses mainly on manu-facturing businesses. However, most of the managerial accounting concepts discussedin this text also apply to service and merchandising businesses.

The cost of a manufactured product includes the cost of materials used in makingthe product. It also includes the cost of converting those materials into a finishedproduct. Thus, the cost of a finished product includes the following:

. Direct materials cost

. Direct labour cost

. Factory overhead cost

Direct Materials Cost Manufactured products begin with raw materials, whichare converted into finished products. The cost of any material that is an integral part ofthe finished product is classified as a direct materials cost. Direct materials costsinclude, for example, the cost of the electronic components in a television, and the tireson an automobile. To be classified as a direct materials cost, the material must:

(a) be easily traceable and recognizable, as well as integral to the finished product, and(b) reflect a significant portion of the total cost of the product.

Insignificant costs such as the glue used to produce a TV or the lubricants usedto make automobile tires shine might be classified as factory overhead costs.

Direct Labour Cost Most manufacturing products use employee labour to con-vert materials into finished products. The wages of employees who are integral to thefinished product are classified as a direct labour cost. For example, machine operators’wages for assembling a TV are direct labour costs, and so are mechanics’ wages for man-ufacturing an automobile. As with direct materials cost, a direct labour cost must:

(a) be easily traceable to production, as well as an integral part to the finished prod-uct; and

(b) reflect a significant portion of the total cost of the product.

The wages of the cleaning staff who clean the car or TV factory are not a directlabour cost, nor are those of the security staff who guard the factory at night. This isbecause cleaning and security costs are not an integral part of, or a significant cost of,each TV or car. Instead, such costs are classified as a factory overhead cost.

Factory Overhead Cost (Manufacturing Overhead) Costs other thandirect materials cost and direct labour cost that are incurred in the manufacturingprocess are combined and classified as factory overhead cost. All factory overhead costsare indirect costs of the product. Factory overhead costs may include the following:

O B J E C T I V E � 3Prepare income statements formanufacturing and service organizations.

Chapter 2 Basic Managerial Accounting Concepts 41

NEL

. Heat and light for the factory

. Power to run the machines

. Salaries for factory supervisors

. Factory caretaking wages

. Equipment repair and maintenance

. Property taxes on factory buildings and land

. Insurance on factory buildings

. Amortization of factory plant and equipment

Factory overhead cost also includes costs for materials that do not enter directlyinto the finished product. Examples include lubricants, glue, buffing compounds, andmachine coolants.

When you total direct material, direct labour, and factory overhead, you arrive atmanufacturing costs.

The retained earnings and cash flow statements for a manufacturing business aresimilar to those illustrated in financial accounting courses for service and merchandis-ing businesses. However, the balance sheet and income statement for a manufacturingbusiness are more complex.

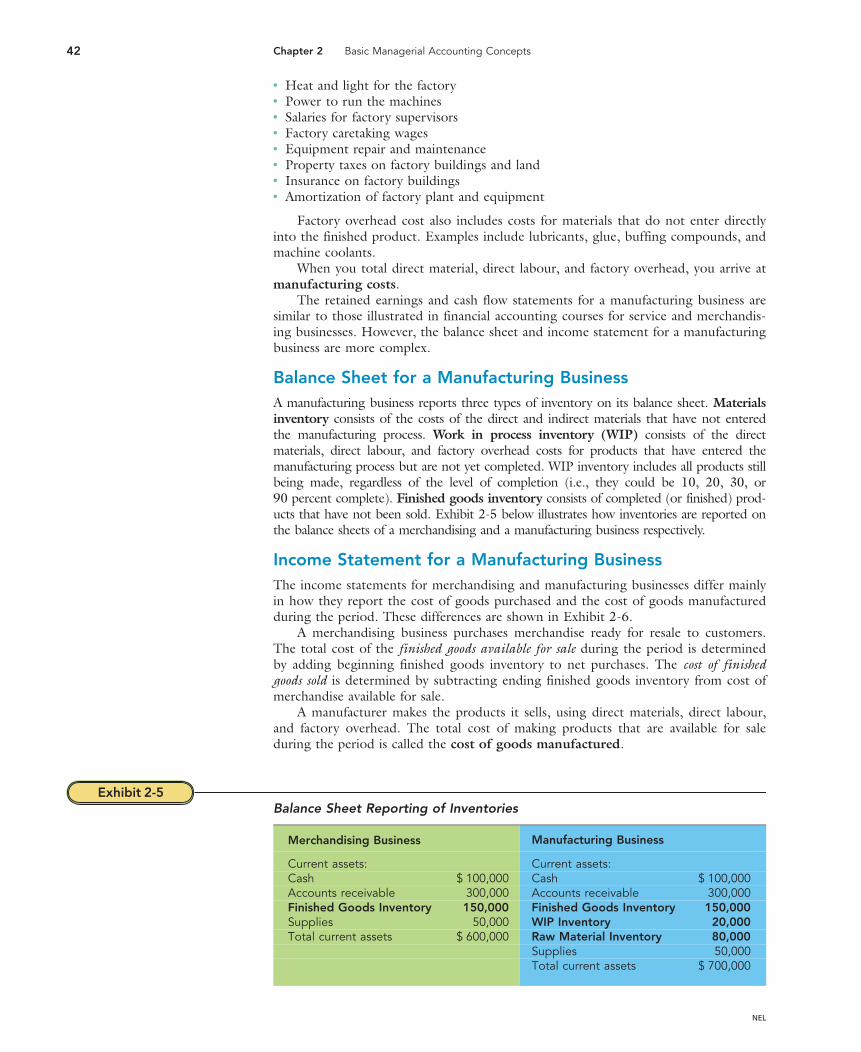

Balance Sheet for a Manufacturing BusinessA manufacturing business reports three types of inventory on its balance sheet. Materialsinventory consists of the costs of the direct and indirect materials that have not enteredthe manufacturing process. Work in process inventory (WIP) consists of the directmaterials, direct labour, and factory overhead costs for products that have entered themanufacturing process but are not yet completed. WIP inventory includes all products stillbeing made, regardless of the level of completion (i.e., they could be 10, 20, 30, or90 percent complete). Finished goods inventory consists of completed (or finished) prod-ucts that have not been sold. Exhibit 2-5 below illustrates how inventories are reported onthe balance sheets of a merchandising and a manufacturing business respectively.

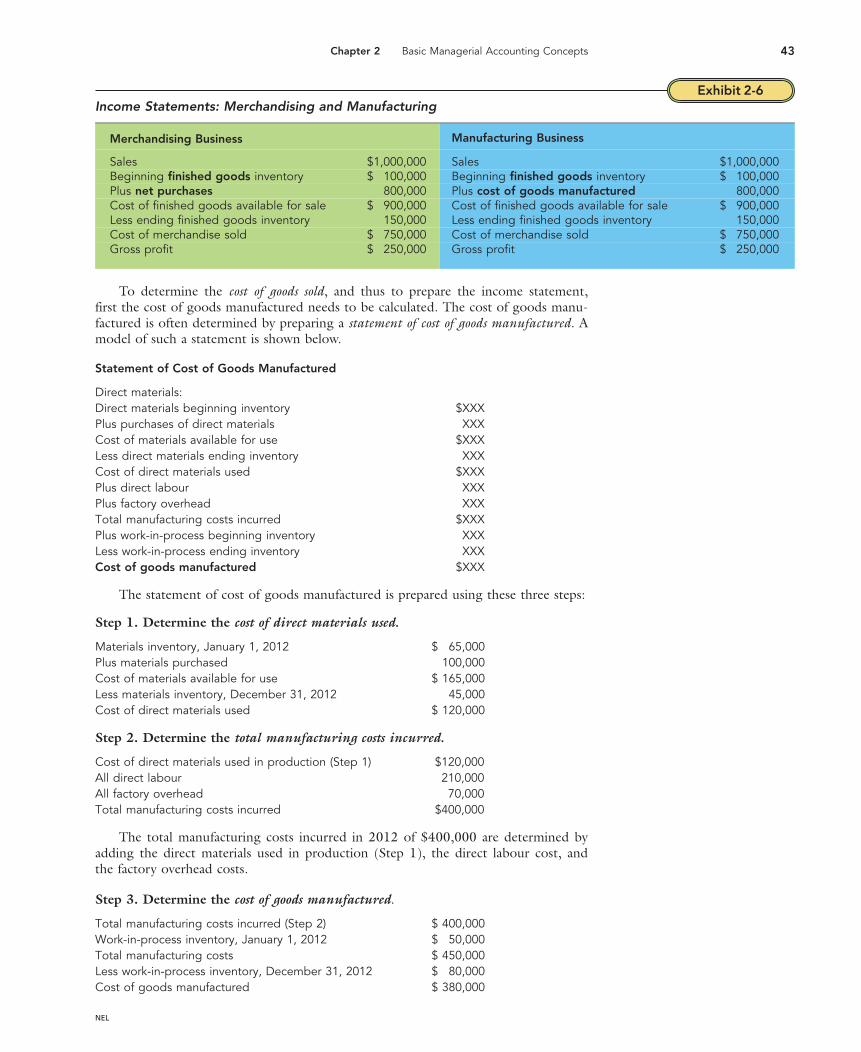

Income Statement for a Manufacturing BusinessThe income statements for merchandising and manufacturing businesses differ mainlyin how they report the cost of goods purchased and the cost of goods manufacturedduring the period. These differences are shown in Exhibit 2-6.

A merchandising business purchases merchandise ready for resale to customers.The total cost of the finished goods available for sale during the period is determinedby adding beginning finished goods inventory to net purchases. The cost of finishedgoods sold is determined by subtracting ending finished goods inventory from cost ofmerchandise available for sale.

A manufacturer makes the products it sells, using direct materials, direct labour,and factory overhead. The total cost of making products that are available for saleduring the period is called the cost of goods manufactured.

Exhibit 2-5Balance Sheet Reporting of Inventories

Merchandising Business Manufacturing Business

Current assets: Current assets:Cash $ 100,000 Cash $ 100,000Accounts receivable 300,000 Accounts receivable 300,000Finished Goods Inventory 150,000 Finished Goods Inventory 150,000Supplies 50,000 WIP Inventory 20,000Total current assets $ 600,000 Raw Material Inventory 80,000

Supplies 50,000Total current assets $ 700,000

42 Chapter 2 Basic Managerial Accounting Concepts

NEL

To determine the cost of goods sold, and thus to prepare the income statement,first the cost of goods manufactured needs to be calculated. The cost of goods manu-factured is often determined by preparing a statement of cost of goods manufactured. Amodel of such a statement is shown below.

Statement of Cost of Goods Manufactured

Direct materials:Direct materials beginning inventory $XXXPlus purchases of direct materials XXXCost of materials available for use $XXXLess direct materials ending inventory XXXCost of direct materials used $XXXPlus direct labour XXXPlus factory overhead XXXTotal manufacturing costs incurred $XXXPlus work-in-process beginning inventory XXXLess work-in-process ending inventory XXXCost of goods manufactured $XXX

The statement of cost of goods manufactured is prepared using these three steps:

Step 1. Determine the cost of direct materials used.

Materials inventory, January 1, 2012 $ 65,000Plus materials purchased 100,000Cost of materials available for use $ 165,000Less materials inventory, December 31, 2012 45,000Cost of direct materials used $ 120,000

Step 2. Determine the total manufacturing costs incurred.

Cost of direct materials used in production (Step 1) $120,000All direct labour 210,000All factory overhead 70,000Total manufacturing costs incurred $400,000

The total manufacturing costs incurred in 2012 of $400,000 are determined byadding the direct materials used in production (Step 1), the direct labour cost, andthe factory overhead costs.

Step 3. Determine the cost of goods manufactured.

Total manufacturing costs incurred (Step 2) $ 400,000Work-in-process inventory, January 1, 2012 $ 50,000Total manufacturing costs $ 450,000Less work-in-process inventory, December 31, 2012 $ 80,000Cost of goods manufactured $ 380,000

Exhibit 2-6Income Statements: Merchandising and Manufacturing

Merchandising Business Manufacturing Business

Sales $1,000,000 Sales $1,000,000Beginning finished goods inventory $ 100,000 Beginning finished goods inventory $ 100,000Plus net purchases 800,000 Plus cost of goods manufactured 800,000Cost of finished goods available for sale $ 900,000 Cost of finished goods available for sale $ 900,000Less ending finished goods inventory 150,000 Less ending finished goods inventory 150,000Cost of merchandise sold $ 750,000 Cost of merchandise sold $ 750,000Gross profit $ 250,000 Gross profit $ 250,000

Chapter 2 Basic Managerial Accounting Concepts 43

NEL

The cost of goods manufactured of $380,000 is determined by adding to themanufacturing costs the WIP beginning inventory and subtracting the WIP endinginventory. Thus the statement of cost of goods manufactured is shaped as follows:

Statement of Costs of Goods ManufacturedFor the Year Ended December 31, 2012

Materials inventory, January 1, 2012 $ 65,000Plus materials purchased 100,000Cost of materials available for use $ 165,000Less materials inventory, December 31, 2012 45,000Cost of direct materials used $ 120,000Plus direct labour 210,000Plus factory overhead 70,000Total current manufacturing costs incurred $ 400,000Plus work-in-process inventory, January 1, 2012 $ 50,000Total manufacturing costs $ 450,000Less work-in-process inventory, December 31, 2012 $ 80,000Cost of goods manufactured $ 380,000

Income StatementFor the Year Ended December 31, 2012

Sales $700,000Cost of goods sold:Finished goods inventory, January 1, 2012 $100,000Cost of goods manufactured 380,000Cost of finished goods available for sale 480,000Less finished goods inventory, December 31, 2012 80,000Cost of goods sold $400,000Gross profit 300,000Operating expenses:Selling expenses 120,000Administrative expenses 90,000Total operating expenses $210,000Net income $ 90,000

The cost of finished goods available for sale is determined by adding the beginning fin-ished goods inventory to the cost of goods manufactured during the period. The cost ofgoods sold is determined by subtracting the ending finished goods inventory from thecost of finished goods available for sale.

Cost of Goods Manufactured: A Second LookThe cost of goods manufactured represents the total product cost of goods completedduring the current period and transferred to finished goods inventory. The only costsassigned to goods completed are the manufacturing costs of direct materials, directlabour, and manufacturing overhead. So, why don’t we just add together the currentperiod’s costs of direct materials, direct labour, and manufacturing overhead to arriveat cost of goods sold? The reason is inventories of materials and work in process. Forinstance, some of the materials purchased in the current period likely were used inproduction (i.e., transferred from materials inventory to work-in-process inventoryduring the period). However, other materials likely were not used in production, andthus remain in materials inventory at period end. Also, some of the units that wereworked on (and thus allocated labour and manufacturing overhead costs) in the cur-rent period likely were completed during the period (i.e., transferred from work-in-process inventory to finished goods inventory during the period). However, otherunits worked on during the period likely were not completed during the period, andthus remain in work-in-process inventory at period end. In calculating cost of goods

44 Chapter 2 Basic Managerial Accounting Concepts

NEL

sold, we need to distinguish between the total manufacturing cost for the current pe-riod and the manufacturing costs associated with the units that were completed duringthe current period (i.e., cost of goods manufactured).

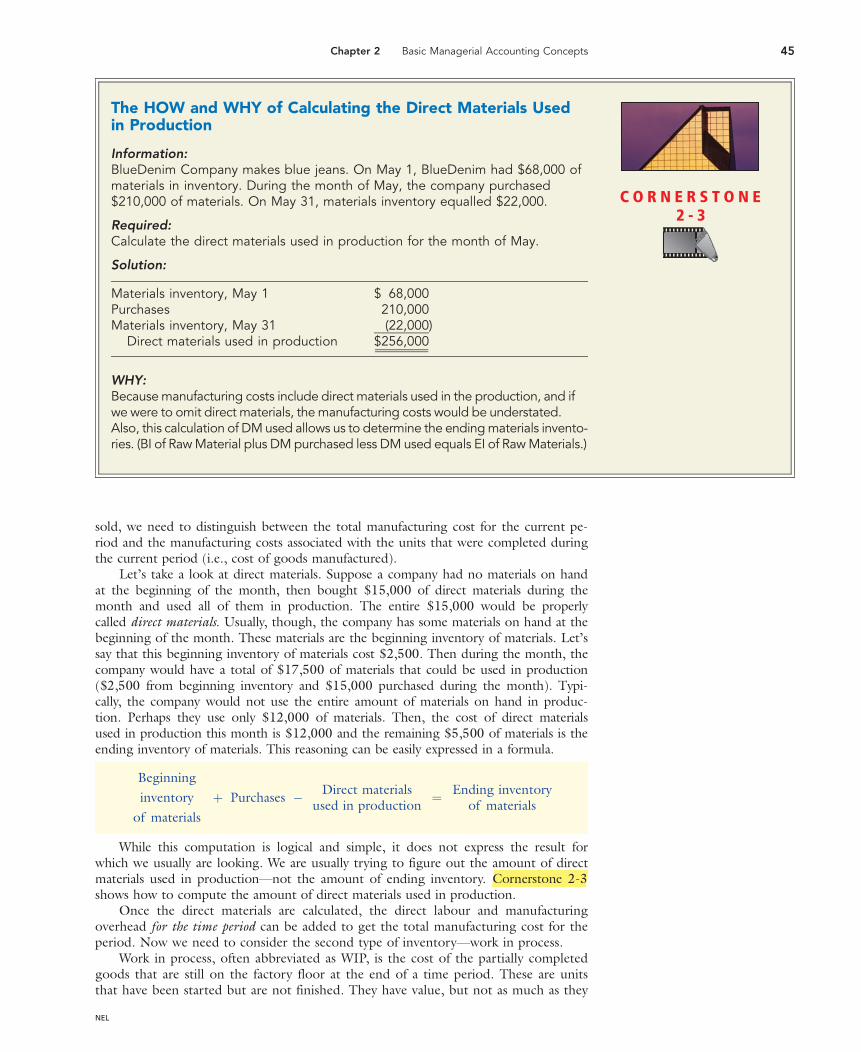

Let’s take a look at direct materials. Suppose a company had no materials on handat the beginning of the month, then bought $15,000 of direct materials during themonth and used all of them in production. The entire $15,000 would be properlycalled direct materials. Usually, though, the company has some materials on hand at thebeginning of the month. These materials are the beginning inventory of materials. Let’ssay that this beginning inventory of materials cost $2,500. Then during the month, thecompany would have a total of $17,500 of materials that could be used in production($2,500 from beginning inventory and $15,000 purchased during the month). Typi-cally, the company would not use the entire amount of materials on hand in produc-tion. Perhaps they use only $12,000 of materials. Then, the cost of direct materialsused in production this month is $12,000 and the remaining $5,500 of materials is theending inventory of materials. This reasoning can be easily expressed in a formula.

Beginning

inventory

of materials

þ Purchases � Direct materialsused in production

¼ Ending inventoryof materials

While this computation is logical and simple, it does not express the result forwhich we usually are looking. We are usually trying to figure out the amount of directmaterials used in production—not the amount of ending inventory. Cornerstone 2-3shows how to compute the amount of direct materials used in production.

Once the direct materials are calculated, the direct labour and manufacturingoverhead for the time period can be added to get the total manufacturing cost for theperiod. Now we need to consider the second type of inventory—work in process.

Work in process, often abbreviated as WIP, is the cost of the partially completedgoods that are still on the factory floor at the end of a time period. These are unitsthat have been started but are not finished. They have value, but not as much as they

The HOW and WHY of Calculating the Direct Materials Usedin Production

Information:BlueDenim Company makes blue jeans. On May 1, BlueDenim had $68,000 ofmaterials in inventory. During the month of May, the company purchased$210,000 of materials. On May 31, materials inventory equalled $22,000.

Required:Calculate the direct materials used in production for the month of May.

Solution:

Materials inventory, May 1 $ 68,000Purchases 210,000Materials inventory, May 31 (22,000)

Direct materials used in production $256,000

WHY:Because manufacturing costs include direct materials used in the production, and ifwe were to omit direct materials, the manufacturing costs would be understated.Also, this calculation of DM used allows us to determine the ending materials invento-ries. (BI of Raw Material plus DM purchased less DM used equals EI of Raw Materials.)

C O R N E R S T O N E2 - 3

Chapter 2 Basic Managerial Accounting Concepts 45

NEL

will when they are completed. Just as there are beginning and ending inventories ofmaterials, there are beginning and ending inventories of WIP. We must adjust the totalmanufacturing cost for the time period for the inventories of WIP. When that is done, wewill have the total cost of the goods that were completed and transferred from work-in-process inventory to finished goods inventory during the time period. Cornerstone 2-4shows how to calculate the cost of goods manufactured for a particular time period.

Cost of Goods SoldTo meet external reporting requirements, costs must be classified into three catego-ries: production, selling, and administration. Remember that product costs are ini-tially put into inventory. They become expenses only when the products are sold,which matches the expenses of manufacturing the product to the sales revenue gener-ated by the product at the time it is sold. Therefore, the expense of manufacturing isnot the cost of goods manufactured; instead it is the cost of the goods that are sold.

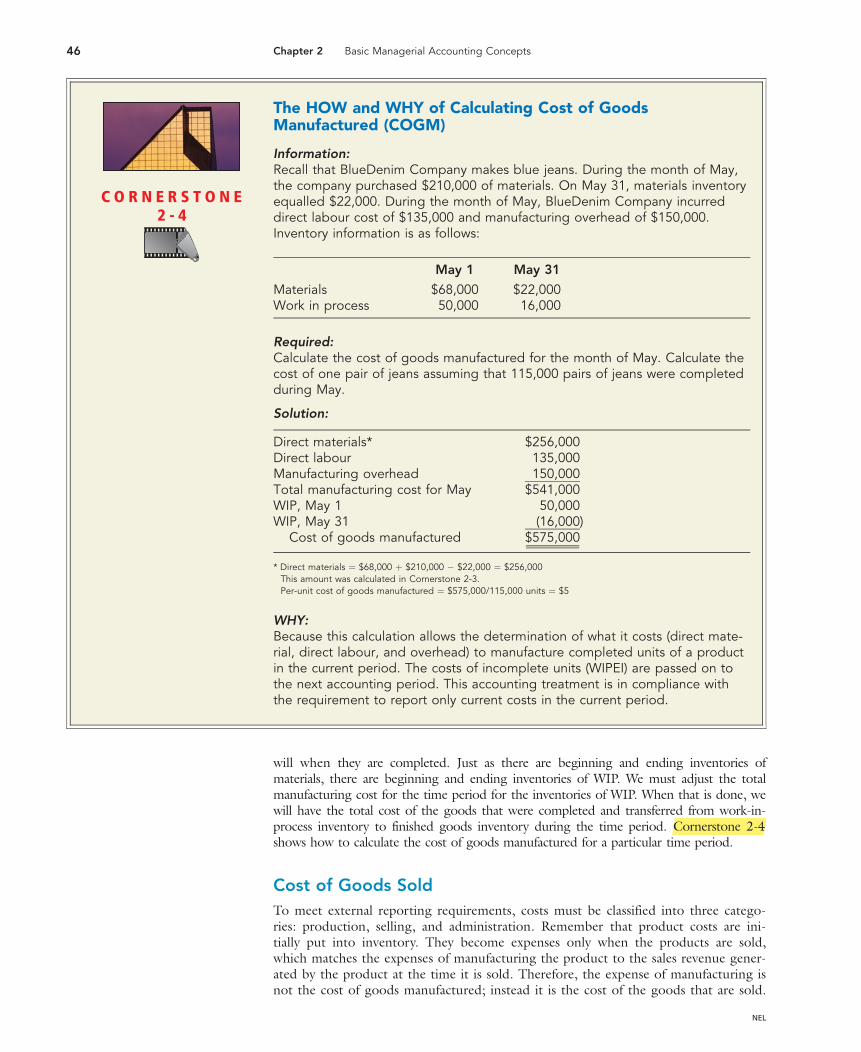

The HOW and WHY of Calculating Cost of GoodsManufactured (COGM)

Information:Recall that BlueDenim Company makes blue jeans. During the month of May,the company purchased $210,000 of materials. On May 31, materials inventoryequalled $22,000. During the month of May, BlueDenim Company incurreddirect labour cost of $135,000 and manufacturing overhead of $150,000.Inventory information is as follows:

May 1 May 31

Materials $68,000 $22,000Work in process 50,000 16,000

Required:Calculate the cost of goods manufactured for the month of May. Calculate thecost of one pair of jeans assuming that 115,000 pairs of jeans were completedduring May.

Solution:

Direct materials* $256,000Direct labour 135,000Manufacturing overhead 150,000Total manufacturing cost for May $541,000WIP, May 1 50,000WIP, May 31 (16,000)

Cost of goods manufactured $575,000

* Direct materials ¼ $68,000 þ $210,000 � $22,000 ¼ $256,000This amount was calculated in Cornerstone 2-3.Per-unit cost of goods manufactured ¼ $575,000/115,000 units ¼ $5

WHY:Because this calculation allows the determination of what it costs (direct mate-rial, direct labour, and overhead) to manufacture completed units of a productin the current period. The costs of incomplete units (WIPEI) are passed on tothe next accounting period. This accounting treatment is in compliance withthe requirement to report only current costs in the current period.

C O R N E R S T O N E2 - 4

46 Chapter 2 Basic Managerial Accounting Concepts

NEL

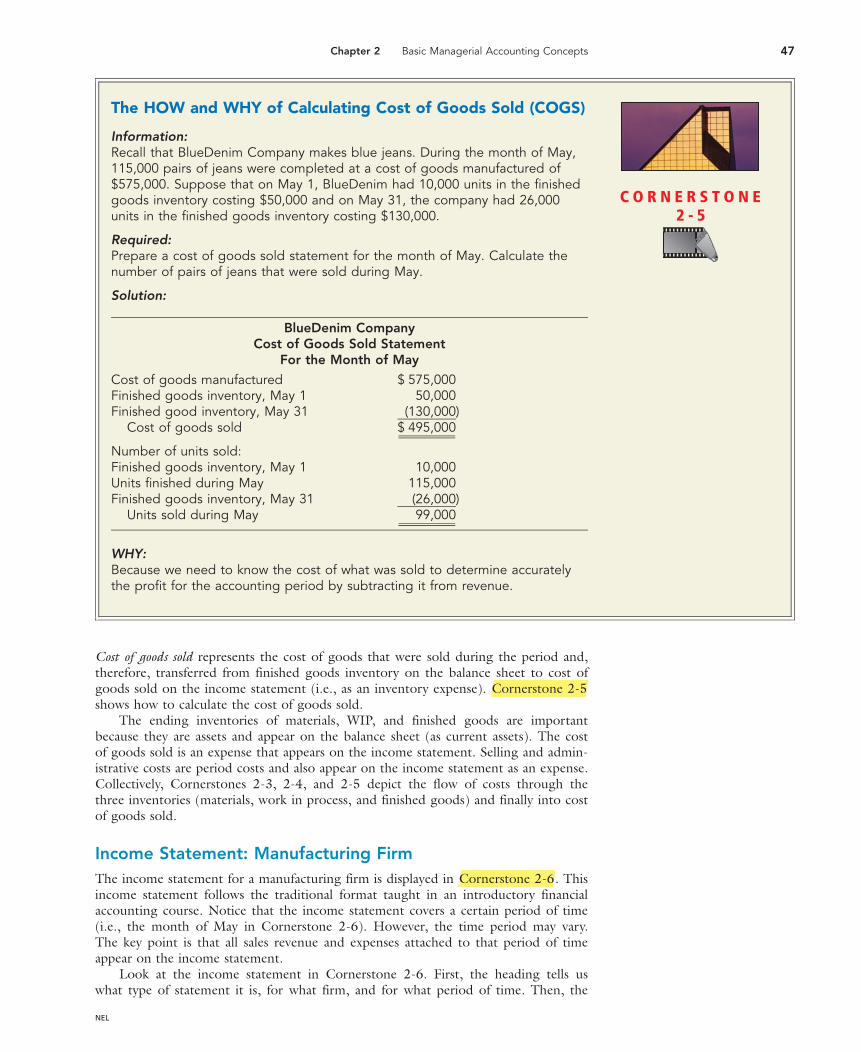

Cost of goods sold represents the cost of goods that were sold during the period and,therefore, transferred from finished goods inventory on the balance sheet to cost ofgoods sold on the income statement (i.e., as an inventory expense). Cornerstone 2-5shows how to calculate the cost of goods sold.

The ending inventories of materials, WIP, and finished goods are importantbecause they are assets and appear on the balance sheet (as current assets). The costof goods sold is an expense that appears on the income statement. Selling and admin-istrative costs are period costs and also appear on the income statement as an expense.Collectively, Cornerstones 2-3, 2-4, and 2-5 depict the flow of costs through thethree inventories (materials, work in process, and finished goods) and finally into costof goods sold.

Income Statement: Manufacturing FirmThe income statement for a manufacturing firm is displayed in Cornerstone 2-6. Thisincome statement follows the traditional format taught in an introductory financialaccounting course. Notice that the income statement covers a certain period of time(i.e., the month of May in Cornerstone 2-6). However, the time period may vary.The key point is that all sales revenue and expenses attached to that period of timeappear on the income statement.

Look at the income statement in Cornerstone 2-6. First, the heading tells uswhat type of statement it is, for what firm, and for what period of time. Then, the

The HOW and WHY of Calculating Cost of Goods Sold (COGS)

Information:Recall that BlueDenim Company makes blue jeans. During the month of May,115,000 pairs of jeans were completed at a cost of goods manufactured of$575,000. Suppose that on May 1, BlueDenim had 10,000 units in the finishedgoods inventory costing $50,000 and on May 31, the company had 26,000units in the finished goods inventory costing $130,000.

Required:Prepare a cost of goods sold statement for the month of May. Calculate thenumber of pairs of jeans that were sold during May.

Solution:

BlueDenim CompanyCost of Goods Sold Statement

For the Month of May

Cost of goods manufactured $ 575,000Finished goods inventory, May 1 50,000Finished good inventory, May 31 (130,000)

Cost of goods sold $ 495,000

Number of units sold:Finished goods inventory, May 1 10,000Units finished during May 115,000Finished goods inventory, May 31 (26,000)

Units sold during May 99,000

WHY:Because we need to know the cost of what was sold to determine accuratelythe profit for the accounting period by subtracting it from revenue.

C O R N E R S T O N E2 - 5

Chapter 2 Basic Managerial Accounting Concepts 47

NEL

income statement itself always begins with ‘‘sales revenue’’ (or ‘‘sales’’ or ‘‘revenue’’).The sales revenue is the price multiplied by the units sold. After the sales revenue isdetermined, the firm must calculate expenses for the period.

Notice that the expenses are separated into three categories: production (cost ofgoods sold), selling, and administrative. The first type of expense is the cost of pro-ducing the units sold, or the cost of goods sold. This amount was computed andexplained in Cornerstone 2-5. Remember that the cost of goods sold is the cost ofproducing the units that were sold during the time period. It includes direct mate-rials, direct labour, and manufacturing overhead. It does not include any selling oradministrative expenses. In the case of a retail (i.e., a merchandising) firm, the cost ofgoods sold represents the total cost of the goods sold when they were purchasedfrom an outside supplier. Therefore, the cost of goods sold for a retailer equals thepurchase costs adjusted for the beginning and ending balances in its single inventoryaccount. A merchandising firm, such as Old Navy, has only one inventory accountbecause it does not transform the purchased good into a different form by addingmaterials, labour, and overhead, as does a manufacturing firm.

Gross margin is the difference between sales revenue and cost of goods sold. Itshows how much the firm is making over and above the cost of the units sold. Grossmargin does not equal operating income or profit. Selling and administrative expenseshave not yet been subtracted. However, gross margin does provide useful informa-tion. If gross margin is positive, the firm at least charges prices that cover the prod-uct cost. In addition, the firm can calculate its gross margin percentage (gross

The HOW and WHY of Preparing an Income Statementfor a Manufacturing Firm

Information:Recall that BlueDenim Company sold 99,000 pairs of jeans during the month ofMay at a total cost of $495,000. Each pair sold at a price of $8. BlueDenim alsoincurred two types of selling costs: commissions equal to 10 percent of thesales price, and other selling expenses of $120,000. Administrative expensetotalled $85,000.

Required:Prepare an income statement for BlueDenim for the month of May.

Solution:

BlueDenim CompanyIncome Statement

For the Month of May

Sales revenue (99,000 3 $8) $792,000Cost of goods sold 495,000

Gross margin $297,000Less:Selling expense

Commissions (0.10 3 $792,000) $ 79,200Fixed selling expense 120,000 199,200

Administrative expense 85,000Operating income $ 12,800

WHY:Because it is mandatory for reporting purposes (to the Canada Revenue Agency).Also, because it is fundamental in determining the firm’s profitability andtherefore its income tax liability.

C O R N E R S T O N E2 - 6

48 Chapter 2 Basic Managerial Accounting Concepts

NEL

margin/sales revenue), as shown in Cornerstone 2-7, and compare it with the aver-age gross margin percentage for the industry to see if its experience is in the ballparkwith other firms in the industry. Gross margin percentage varies significantly byindustry. Grocery stores such as Sobeys traditionally have low profit margins. Theyearn only a few pennies per food item (e.g., a bag of sugar). Luxury stores such asjewellery stores enjoy a high profit margin of 300 percent and over. The overall prof-itability of low-margin companies is driven by high turnover, that is, high sales (agrocery store sells many bags of sugar). The overall profitability of a jewellery store isdriven by the high profit margin since a jewellery store sells fewer pieces of jewellerythan a grocery store sells grocery items.

Finally, selling expense and administrative expense for the period are subtractedfrom gross margin to arrive at operating income. Operating income is the key figurefrom the income statement; it is profit, and shows how much the owners are actuallyearning from the company. Again, calculating the percentage of operating income(i.e., operating income/sales revenue) and comparing it to the average for the indus-try gives the owners valuable information about relative profitability.

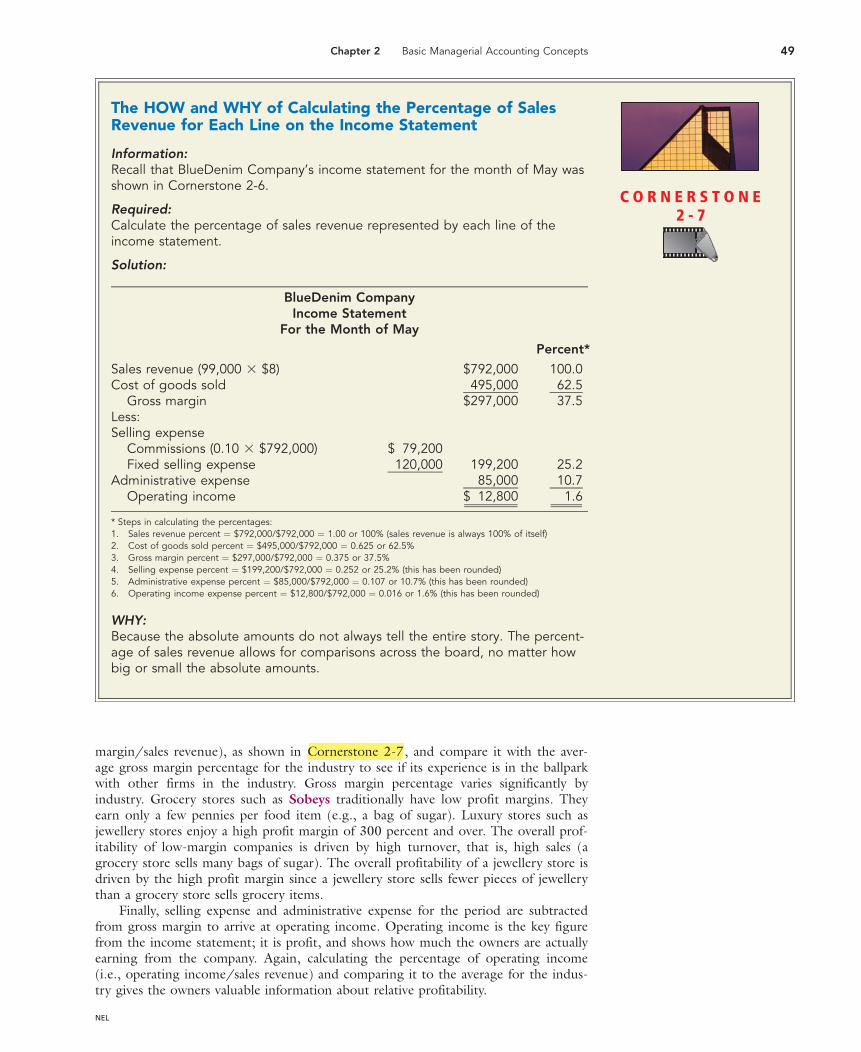

The HOW and WHY of Calculating the Percentage of SalesRevenue for Each Line on the Income Statement

Information:Recall that BlueDenim Company’s income statement for the month of May wasshown in Cornerstone 2-6.

Required:Calculate the percentage of sales revenue represented by each line of theincome statement.

Solution:

BlueDenim CompanyIncome Statement

For the Month of May

Percent*

Sales revenue (99,000 3 $8) $792,000 100.0Cost of goods sold 495,000 62.5

Gross margin $297,000 37.5Less:Selling expense

Commissions (0.10 3 $792,000) $ 79,200Fixed selling expense 120,000 199,200 25.2

Administrative expense 85,000 10.7Operating income $ 12,800 1.6

* Steps in calculating the percentages:1. Sales revenue percent ¼ $792,000/$792,000 ¼ 1.00 or 100% (sales revenue is always 100% of itself)2. Cost of goods sold percent ¼ $495,000/$792,000 ¼ 0.625 or 62.5%3. Gross margin percent ¼ $297,000/$792,000 ¼ 0.375 or 37.5%4. Selling expense percent ¼ $199,200/$792,000 ¼ 0.252 or 25.2% (this has been rounded)5. Administrative expense percent ¼ $85,000/$792,000 ¼ 0.107 or 10.7% (this has been rounded)6. Operating income expense percent ¼ $12,800/$792,000 ¼ 0.016 or 1.6% (this has been rounded)

WHY:Because the absolute amounts do not always tell the entire story. The percent-age of sales revenue allows for comparisons across the board, no matter howbig or small the absolute amounts.

C O R N E R S T O N E2 - 7

Chapter 2 Basic Managerial Accounting Concepts 49

NEL

The income statement can be analyzed further by calculating the percentage ofsales revenue represented by each line of the statement, as was done in Cornerstone 2-7.How can management use this information? The first thing that jumps out is that oper-ating income is less than 2 percent of sales revenue. That’s a very small percentage.Unless this is common for the blue jeans manufacturing business, BlueDenim’s manage-ment should work hard to increase the percentage. Selling expense is a whopping 25.2percent of sales! Do commissions really need to be that high? Or is the price too low(compared to competitors’ prices)? Can cost of goods sold be reduced? Is 62.5 percentreasonable? These are questions that are suggested by Cornerstone 2-7, but notanswered. Answering the questions is the job of management.

Income Statement: Service FirmIn a service organization, there is no product to purchase(e.g., a merchandiser like RONA) or to manufacture (e.g.,Toshiba), and, therefore, there are no beginning or endinginventories. As a result, there is no cost of goods sold orgross margin on the income statement. Instead, the cost ofproviding services appears along with the other operatingexpenses of the company. For example, Southwest Airlines’2007 income statement begins with total operating revenuesof $9,861,000,000 and subtracts total operating expenses of$9,070,000,000 to arrive at an operating income of$791,000,000. An income statement for a service firm isshown in Cornerstone 2-8.

Your friend, Ted, mentioned that Zellers department storemarks up sweaters by 100 percent. ‘‘Wow,’’ said Ted, ‘‘So asweater that costs them $25 is sold for $50—they’re making$25 in profit (operating income)!’’Is Ted correct? Refer to theincome statement from Cornerstone 2-7. What line wouldinclude the $50 price of the sweater? What line would includethe $25 original cost (to the store) of the sweater? What linewould include the $25 that is over and above the cost?

Answers on pages 711 to 715.

The HOW and WHY of Preparing an Income Statementfor a Service Organization

Information:Komala Information Systems designs and installs human resources software forsmall companies. Last month, Komala had software licensing costs of $5,000,service technicians costs of $35,000, and research and development costs of$55,000. Selling expenses were $5,000, and administrative expenses equalled$7,000. Sales totalled $130,000.

Required:Prepare an income statement for Komala Information Systems for the past month.

Solution:

Komala Information SystemsIncome StatementFor the Past Month

Sales revenues: $130,000Less operating expenses:

Software licensing $ 5,000Service technicians 35,000Research and development 55,000Selling expenses 5,000Administrative expenses 7,000 107,000

Operating income $ 23,000

WHY:Because it is mandatory for reporting purposes (CRA). Also, because it is funda-mental in determining the firm’s profitability and therefore its income tax liability.

C O R N E R S T O N E2 - 8

50 Chapter 2 Basic Managerial Accounting Concepts

NEL

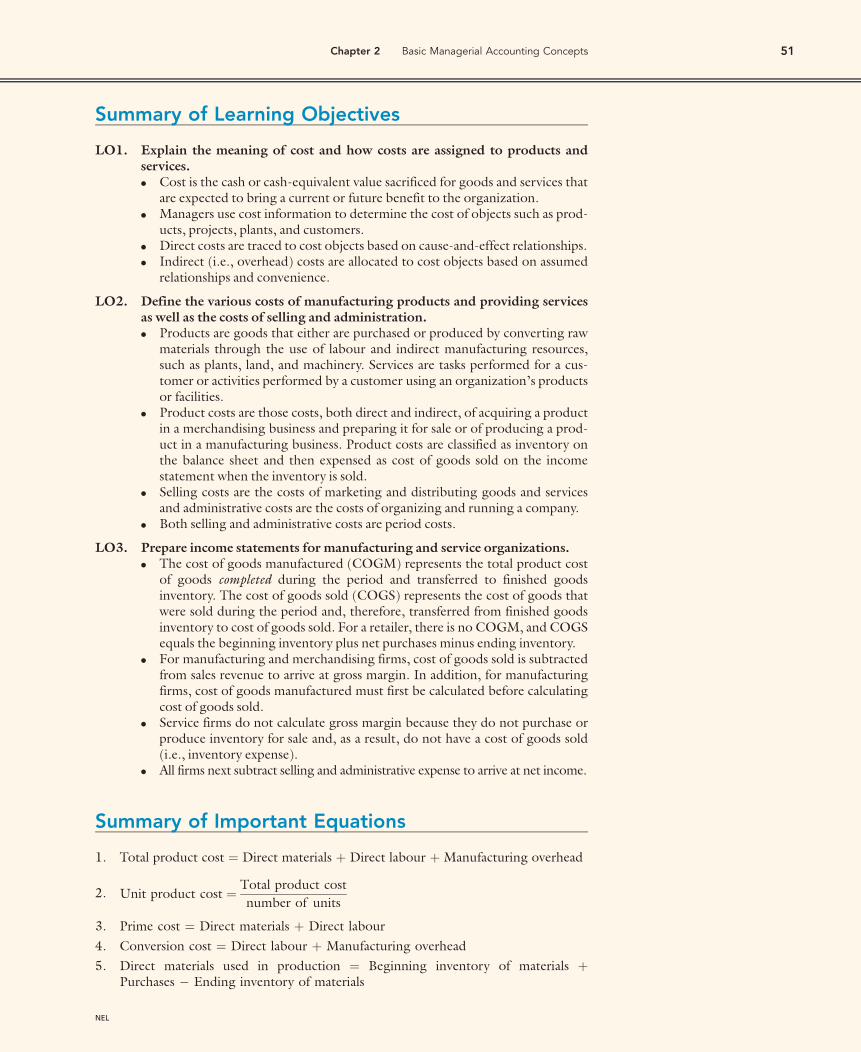

Summary of Important Equations

1. Total product cost ¼ Direct materials þ Direct labour þ Manufacturing overhead

2. Unit product cost ¼ Total product cost

number of units

3. Prime cost ¼ Direct materials þ Direct labour

4. Conversion cost ¼ Direct labour þ Manufacturing overhead

5. Direct materials used in production ¼ Beginning inventory of materials þPurchases � Ending inventory of materials

Summary of Learning Objectives

LO1. Explain the meaning of cost and how costs are assigned to products andservices.. Cost is the cash or cash-equivalent value sacrificed for goods and services that

are expected to bring a current or future benefit to the organization.. Managers use cost information to determine the cost of objects such as prod-

ucts, projects, plants, and customers.. Direct costs are traced to cost objects based on cause-and-effect relationships.. Indirect (i.e., overhead) costs are allocated to cost objects based on assumed

relationships and convenience.

LO2. Define the various costs of manufacturing products and providing servicesas well as the costs of selling and administration.. Products are goods that either are purchased or produced by converting raw

materials through the use of labour and indirect manufacturing resources,such as plants, land, and machinery. Services are tasks performed for a cus-tomer or activities performed by a customer using an organization’s productsor facilities.

. Product costs are those costs, both direct and indirect, of acquiring a productin a merchandising business and preparing it for sale or of producing a prod-uct in a manufacturing business. Product costs are classified as inventory onthe balance sheet and then expensed as cost of goods sold on the incomestatement when the inventory is sold.

. Selling costs are the costs of marketing and distributing goods and servicesand administrative costs are the costs of organizing and running a company.

. Both selling and administrative costs are period costs.

LO3. Prepare income statements for manufacturing and service organizations.. The cost of goods manufactured (COGM) represents the total product cost

of goods completed during the period and transferred to finished goodsinventory. The cost of goods sold (COGS) represents the cost of goods thatwere sold during the period and, therefore, transferred from finished goodsinventory to cost of goods sold. For a retailer, there is no COGM, and COGSequals the beginning inventory plus net purchases minus ending inventory.

. For manufacturing and merchandising firms, cost of goods sold is subtractedfrom sales revenue to arrive at gross margin. In addition, for manufacturingfirms, cost of goods manufactured must first be calculated before calculatingcost of goods sold.

. Service firms do not calculate gross margin because they do not purchase orproduce inventory for sale and, as a result, do not have a cost of goods sold(i.e., inventory expense).

. All firms next subtract selling and administrative expense to arrive at net income.

Chapter 2 Basic Managerial Accounting Concepts 51

NEL

6. Cost of goods manufactured ¼ Direct materials used in production þ Directlabour used in production þ Manufacturing overhead costs used in production þBeginning WIP inventory � Ending WIP inventory

7. Cost of goods sold ¼ Beginning finished goods inventory þ Cost of goodsmanufactured � Ending finished goods inventory

CORNERSTONE 2-1 The HOW and WHY of calculating product cost in total andper unit, page 38

CORNERSTONE 2-2 The HOW and WHY of calculating prime cost andconversion cost in total and per unit, page 39

CORNERSTONE 2-3 The HOW and WHY of calculating the direct materials usedin production, page 45

CORNERSTONE 2-4 The HOW and WHY of calculating cost of goodsmanufactured (COGM), page 46

CORNERSTONE 2-5 The HOW and WHY of calculating cost of goods sold(COGS), page 47

CORNERSTONE 2-6 The HOW and WHY of preparing an income statement fora manufacturing firm, page 48

CORNERSTONE 2-7 The HOW and WHY of calculating the percentage of salesrevenue for each line on the income statement, page 49

CORNERSTONE 2-8 The HOW and WHY of preparing an income statement fora service organization, page 50

Key Terms

Accumulating costs, 31

Administrative costs, 40

Allocation, 33

Assigning costs, 31

Conversion cost, 37

Cost, 30

Cost object, 31

Cost of goods manufactured, 42

Cost of goods sold, 44

Direct costs, 33

Direct labour, 37

Direct labour cost, 41

Direct materials, 36

Direct materials cost, 41

Expenses, 31

Factory overhead cost, 41

Finished goods inventory, 42

Fixed cost, 34

Gross margin, 48

Indirect costs, 33

Manufacturing costs, 42

Manufacturing organizations, 35

Manufacturing overhead, 37

Materials inventory, 42

Opportunity cost, 34

Period costs, 38

Price, 31

Prime cost, 37

Product (manufacturing) costs, 36

Products, 35

Selling costs, 40

Service organizations, 35

Services, 35

Variable cost, 34

Work in process inventory (WIP), 42

C O R N E R S T O N E SF O R C H A P T E R 2

52 Chapter 2 Basic Managerial Accounting Concepts

NEL

Review Problem

Product Costs, Cost of Goods Manufactured Statement, and the IncomeStatement

Brody Company makes industrial cleaning solvents. Various chemicals, detergent, andwater are mixed together and then bottled in 10-gallon drums. Brody provided thefollowing information for last year:

Raw materials purchases $250,000Direct labour 140,000Depreciation on factory equipment 45,000Depreciation on factory building 30,000Depreciation on headquarters building 50,000Factory insurance 15,000Property taxes:

Factory 20,000Headquarters 18,000

Utilities for factory 34,000Utilities for sales office 1,800Administrative salaries 150,000Indirect labour salaries 156,000Sales office salaries 90,000Beginning balance, Raw Materials 124,000Beginning balance, WIP 124,000Beginning balance, Finished Goods 84,000Ending balance, Raw Materials 102,000Ending balance, WIP 130,000Ending balance, Finished Goods 82,000

Last year, Brody completed 100,000 units. Sales revenue equalled $1,200,000, andBrody paid a sales commission of 5 percent of sales.

Required:

1. Calculate the direct materials used in production for last year.2. Calculate total prime cost.3. Calculate total conversion cost.4. Prepare a cost of goods manufactured statement for last year. Calculate the unit

product cost.5. Prepare a cost of goods sold statement for last year.6. Prepare an income statement for last year. Show the percentage of sales that each line

item represents.

Solution:

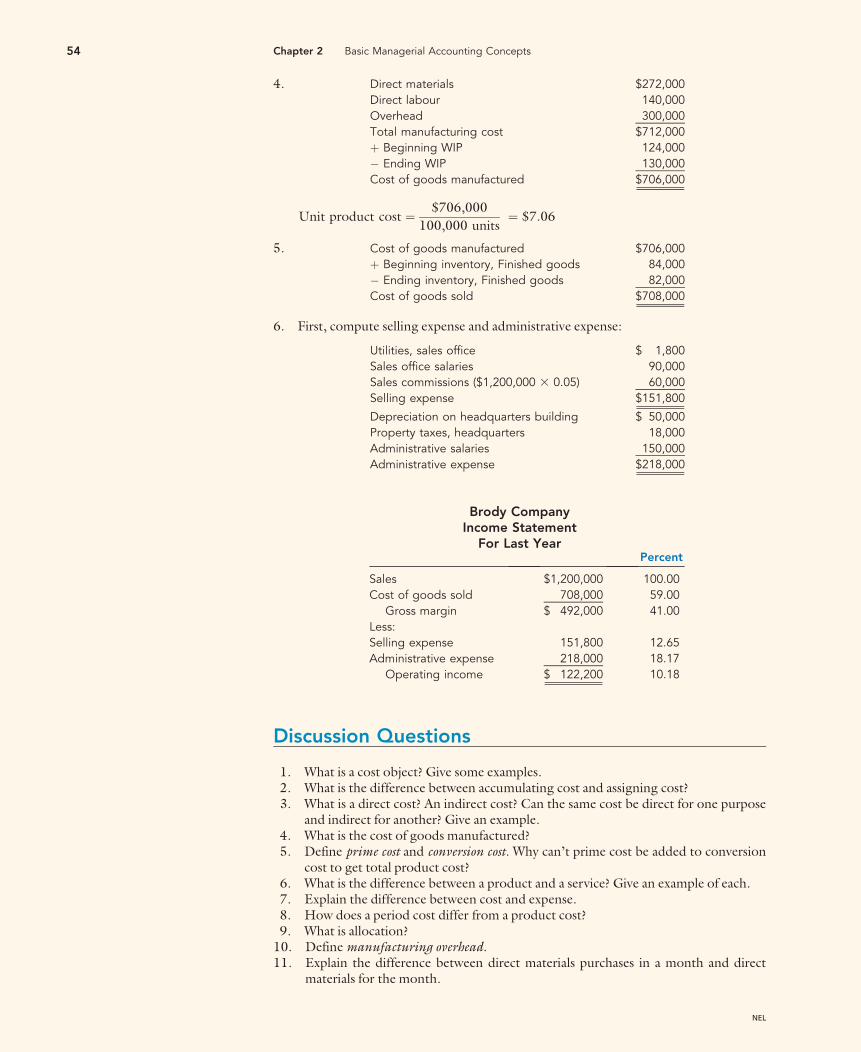

1. Direct materials¼ $124,000þ $250,000� $102,000¼ $272,0002. Prime cost¼ $272,000þ $140,000¼ $412,0003. First, calculate total overhead cost:

Depreciation on factory equipment $ 45,000Depreciation on factory building 30,000Factory insurance 15,000Factory property taxes 20,000Factory utilities 34,000Indirect labour salaries 156,000

Total overhead $300,000

Conversion cost ¼ $140,000 þ $300,000 ¼ $440,000

Chapter 2 Basic Managerial Accounting Concepts 53

NEL

Discussion Questions