2 0 0 7 S P R I N G C O N S T R U C T I O N F O R E C A S T C O N F E R E N C E A p r i l 2 6, 2 0 0...

32

2 0 0 7 S P R I N G C O N S T R U C T I O N F O R E C A S T C O N F E R E N C E A p r i l 2 6, 2 0 0 7 T H E N A T I O N A L O U T L O O K, 2 0 0 7 S P R I N G C O N S T R U C T I O N F O R E C A S T Jim Glassman [email protected] 212-270-0778 Growth Without Housing

Transcript of 2 0 0 7 S P R I N G C O N S T R U C T I O N F O R E C A S T C O N F E R E N C E A p r i l 2 6, 2 0 0...

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

EA p r i l 2 6, 2 0 0 7

T H E N A T I O N A L O U T L O O K, 2 0 0 7 S P R I N G C O N S T R U C T I O N F O R E C A S T C O N F E R E N C E, N A H B, D C

Jim Glassman

212-270-0778

Growth Without Housing

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

2

Surprises in housing’s turmoil… looking for bubbles in all the wrong places

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

3

Real estate stopped rising in 2006, as advertised …

Existing house prices (percent change from 12 months earlier)Existing house prices (percent change from 12 months earlier)

Sources: Standard and Poor’s; National Association of Realtors

-5

0

5

10

15

20

2000 2001 2002 2003 2004 2005 2006 2007

-5

0

5

10

15

20Case-Shiller national repeat sales price indexNAR's median price index of existing single family units

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

4

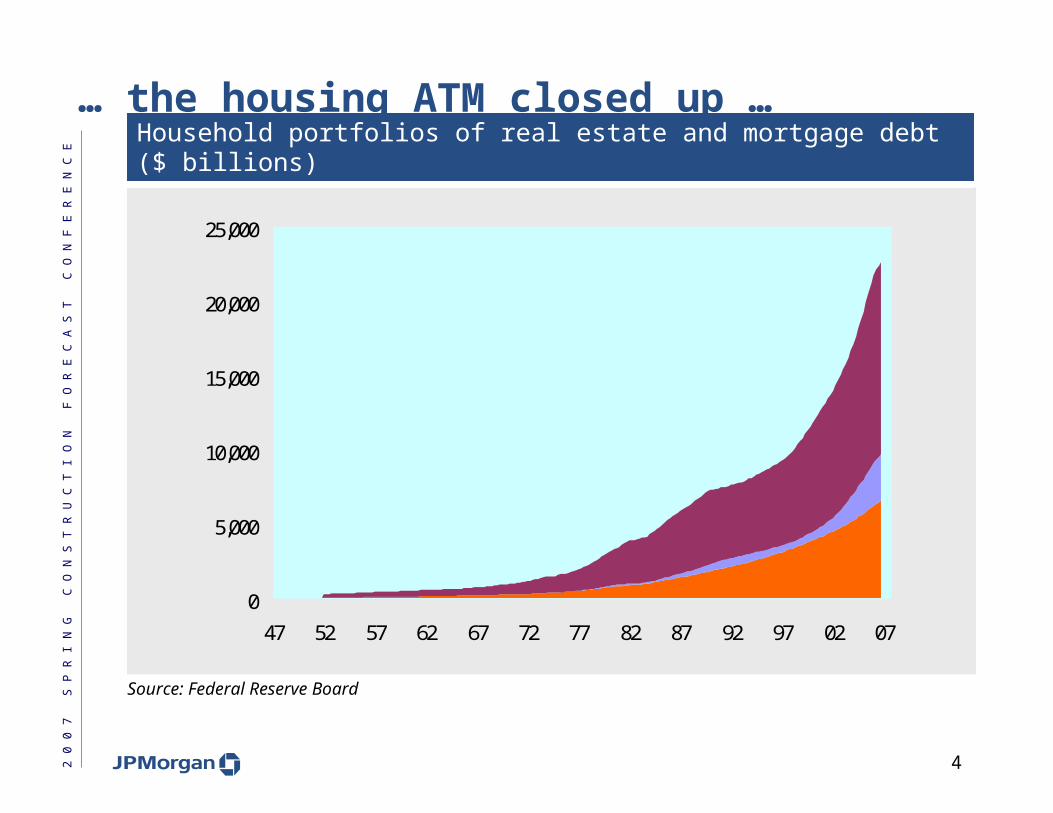

… the housing ATM closed up …

Household portfolios of real estate and mortgage debt ($ billions)Household portfolios of real estate and mortgage debt ($ billions)

Source: Federal Reserve Board

0

5,000

10,000

15,000

20,000

25,000

47 52 57 62 67 72 77 82 87 92 97 02 07

Real estate net worth of householdsMortgage equity withdrawn (now represented by debt obligations)Other mortgage debt (e.g., debt taken to finance new residential investment)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

5

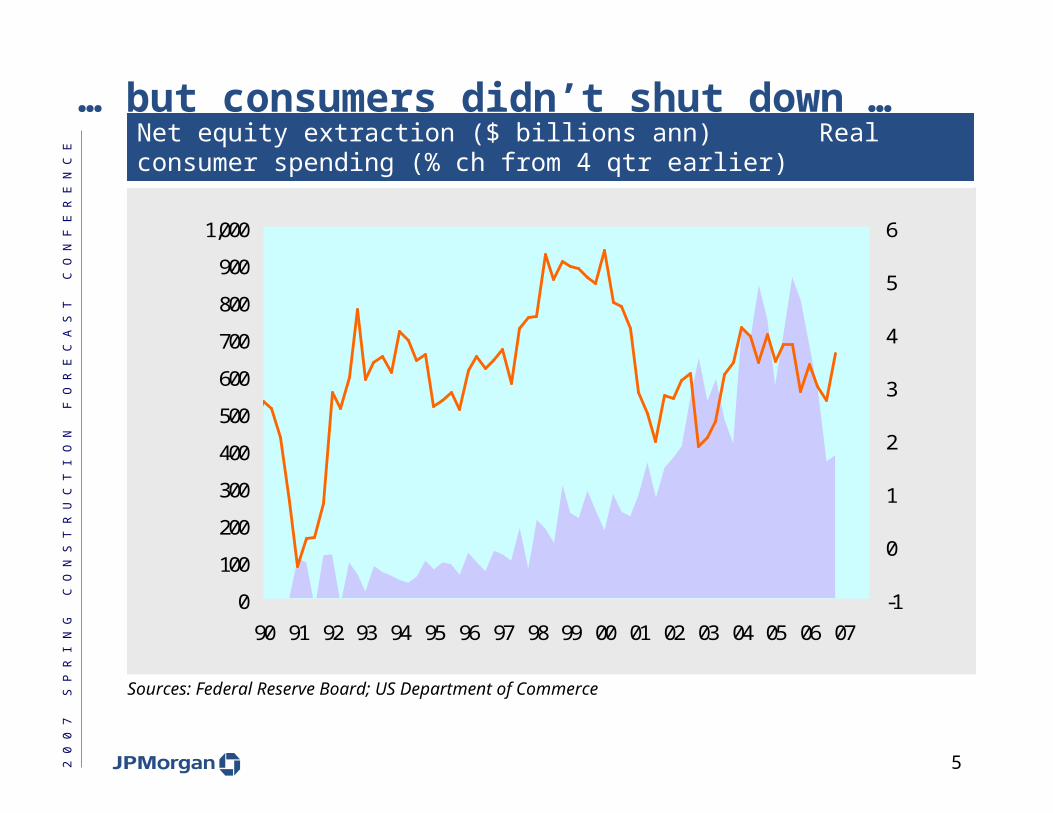

… but consumers didn’t shut down …

Net equity extraction ($ billions ann) Real consumer spending (% ch from 4 qtr earlier)Net equity extraction ($ billions ann) Real consumer spending (% ch from 4 qtr earlier)

Sources: Federal Reserve Board; US Department of Commerce

0

100

200

300

400

500

600

700

800

900

1,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

-1

0

1

2

3

4

5

6

Real consumer spending (right)

Mortgage equity withdrawal (left)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

6

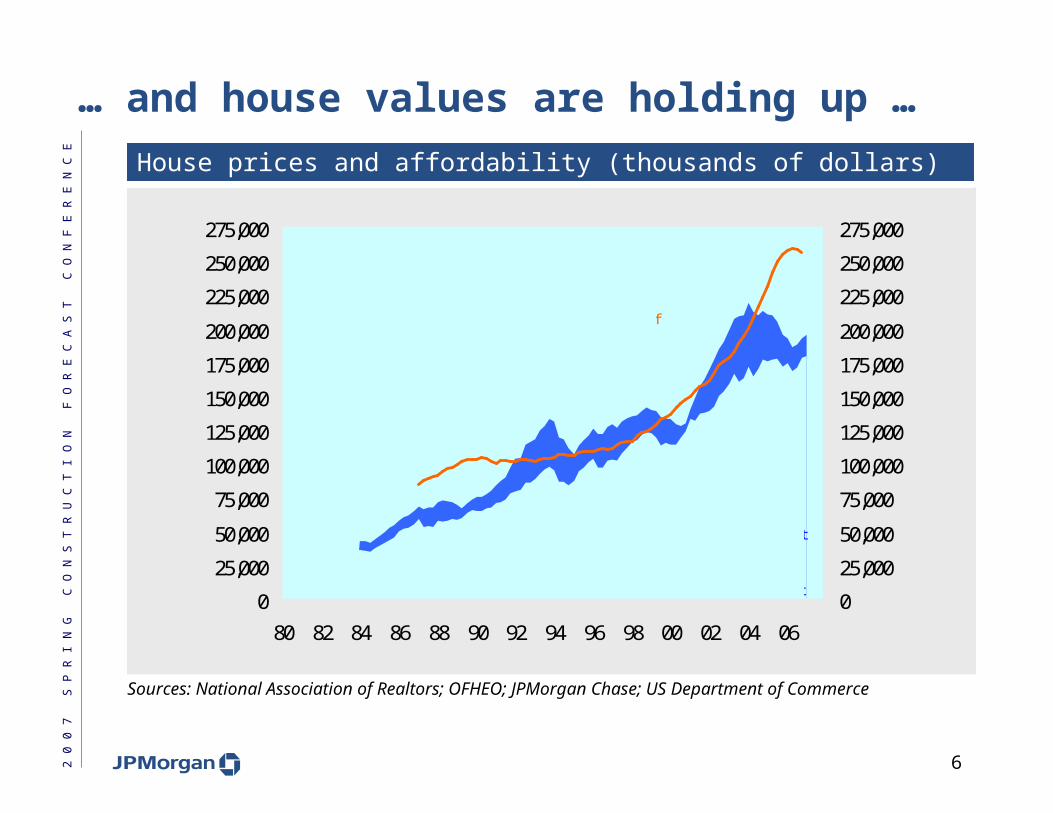

… and house values are holding up …

House prices and affordability (thousands of dollars)House prices and affordability (thousands of dollars)

Sources: National Association of Realtors; OFHEO; JPMorgan Chase; US Department of Commerce

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

250,000

275,000

80 82 84 86 88 90 92 94 96 98 00 02 04 06

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

250,000

275,000

Median price of existing single-family houses in thousands of dollars (National Association of Realtors and Shiller)

What someone earning the median per capita income could afford at prevailing ARM rates (top boundary of shaded region) or at the 30-year conventional fixed rate (bottom boundary), assuming monthly

payments cannot exceed 33% of income and a 20% down payment

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

7

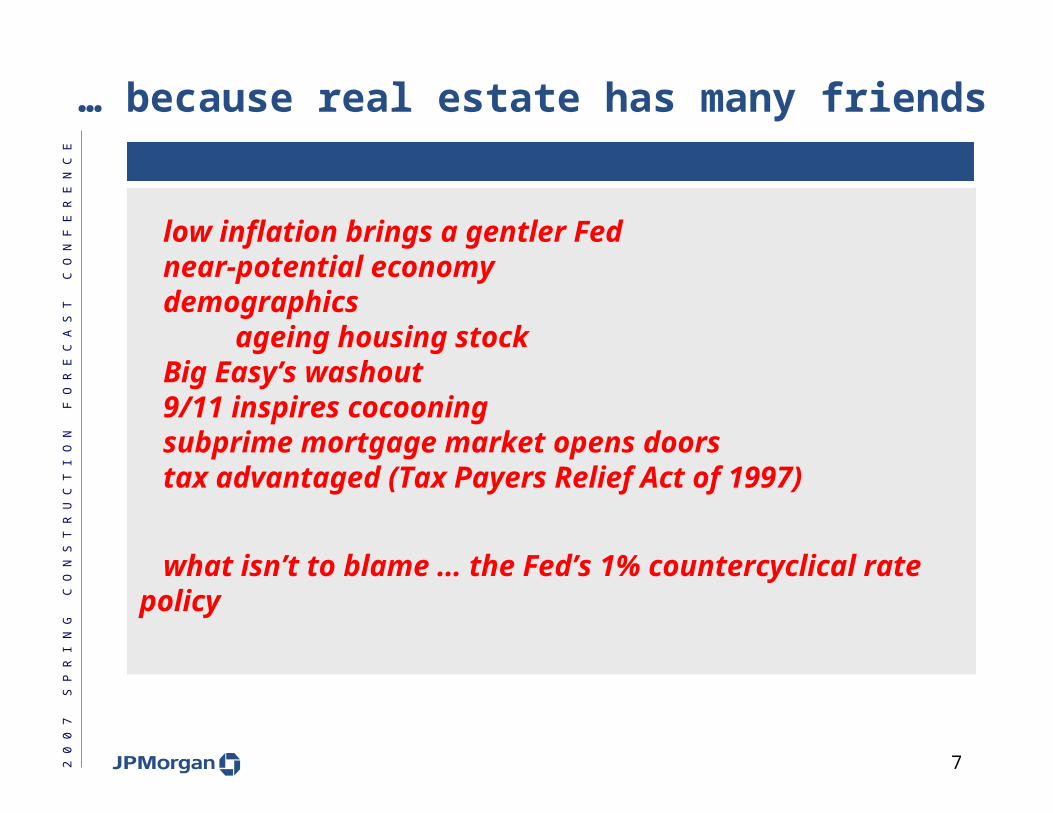

… because real estate has many friends

low inflation brings a gentler Fednear-potential economy

demographics ageing housing stock

Big Easy’s washout9/11 inspires cocooningsubprime mortgage market opens doorstax advantaged (Tax Payers Relief Act of 1997)

what isn’t to blame … the Fed’s 1% countercyclical rate policy

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

8

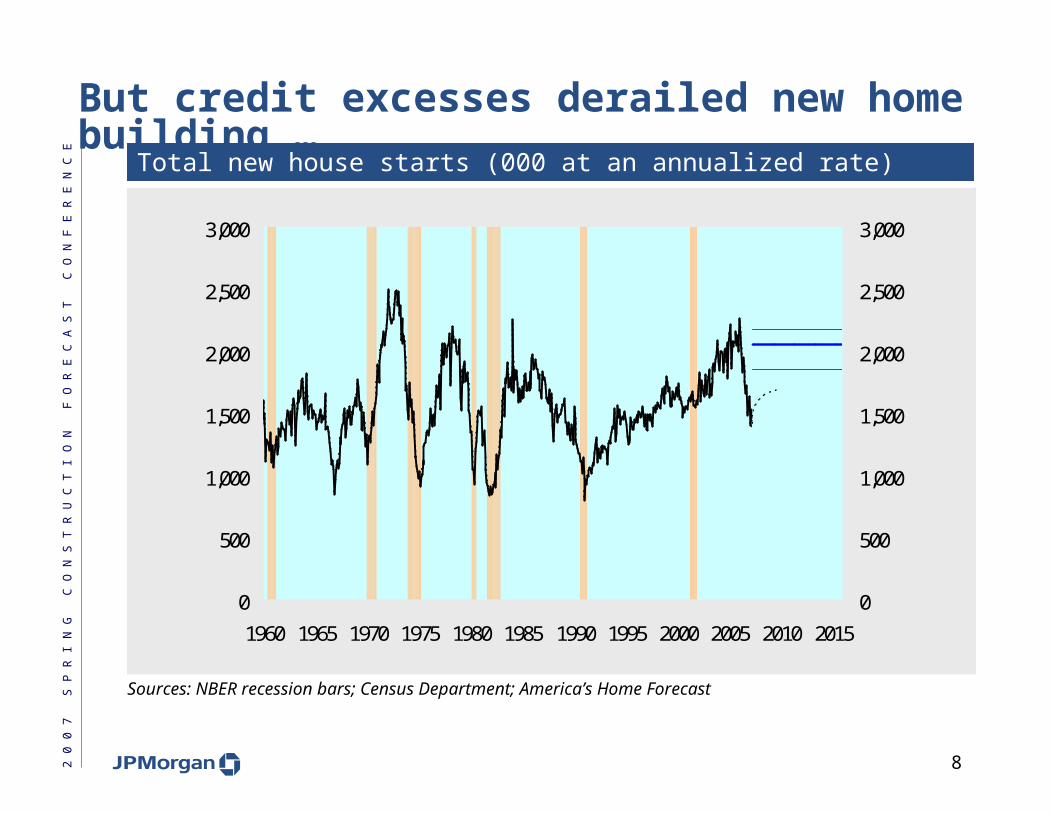

But credit excesses derailed new home building …

Total new house starts (000 at an annualized rate)Total new house starts (000 at an annualized rate)

Sources: NBER recession bars; Census Department; America’s Home Forecast

0

500

1,000

1,500

2,000

2,500

3,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

0

500

1,000

1,500

2,000

2,500

3,000

Scenarios for StartsHigh* (left)Base case (left)Low (left)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

9

… which slowed, but didn’t derail the economy

Real GDP (percent change from four quarters earlier)Real GDP (percent change from four quarters earlier)

Sources: US Department of Commerce, Federal Reserve Board

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

6.5

7.5

8.5

2000 2001 2002 2003 2004 2005 2006 2007 2008

-1.25

-1.00

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

Contribution of residential

construction to real GDP growth over the quarter (right scale)

% change in real GDP from previous quarter (left scale)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

10

Housing recession ≠ national recession

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

11

#1 The economy is bigger than housing …

Real GDP (percent change from four quarters earlier)Real GDP (percent change from four quarters earlier)

Sources: US Department of Commerce, Federal Reserve Board

0

1

2

3

4

5

2003 2004 2005 2006 2007 2008

-2

-1

0

1

2

3

4

5

6

tj

FOMC's most recent central tendency real GDP forecast (Q4/Q4

basis)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

12

… and unemployment tells the story

Unemployment rate (percent of the civilian labor force)Unemployment rate (percent of the civilian labor force)

Sources: US Department of Labor, Federal Reserve Board

4.00

4.25

4.50

4.75

5.00

5.25

5.50

5.75

6.00

6.25

6.50

2003 2004 2005 2006 2007 2008

4.00

4.25

4.50

4.75

5.00

5.25

5.50

5.75

6.00

6.25

6.50

tj

aj

t

j

a

FOMC's most recent central tendency unemployment forecast (Q4 of year shown)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

13

#2 Beyond our shores, a world back in business …

Global real GDP (percentage change from four quarters earlier)Global real GDP (percentage change from four quarters earlier)

Source: JPMorgan Chase

-1

0

1

2

3

4

5

6

1990 1992 1994 1996 1998 2000 2002 2004 2006

-1

0

1

2

3

4

5

6

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

14

… industrial economies and newly industrialized

Real GDP in selected regions (percentage change from four quarters earlier)Real GDP in selected regions (percentage change from four quarters earlier)

Source: JPMorgan Chase

-4-3-2-10123456789

2000 2001 2002 2003 2004 2005 2006 2007

-4-3-2-10123456789

Japan

Emerging economies in Asia, Eastern Europe and Latin America

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

15

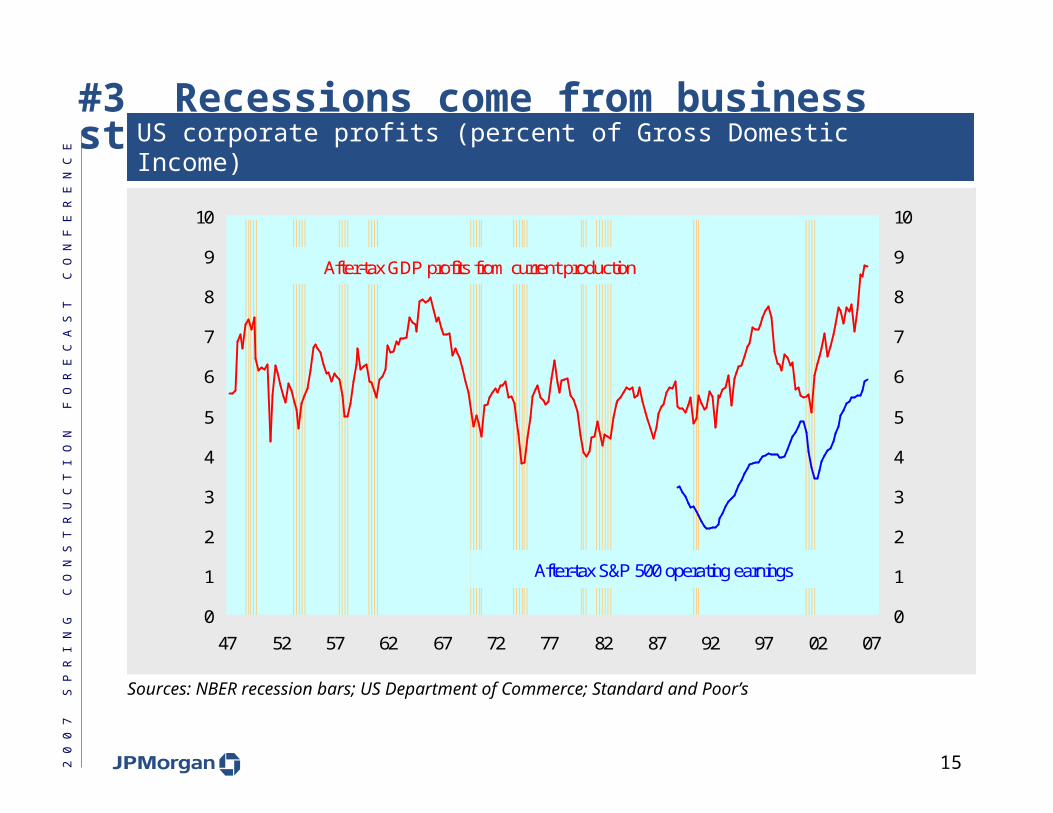

#3 Recessions come from business stress … find it

US corporate profits (percent of Gross Domestic Income)US corporate profits (percent of Gross Domestic Income)

Sources: NBER recession bars; US Department of Commerce; Standard and Poor’s

0

1

2

3

4

5

6

7

8

9

10

47 52 57 62 67 72 77 82 87 92 97 02 070

1

2

3

4

5

6

7

8

9

10

After-tax S&P 500 operating earnings

After-tax GDP profits from current production

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

16

#4 Longevity is a story about inflation not age …

Duration of economic cycles (months from trough to peak of cycle)Duration of economic cycles (months from trough to peak of cycle)

Sources: NBER, Joseph Davis, “An Improved Annual Chronology of US Business Cycles Since the 1790s”, NBER Working Paper Number 11157.

0

20

40

60

80

100

120

14019

1918

1018

2118

3818

4619

1218

6718

9419

0818

9119

0019

2718

5818

8519

2118

2318

2618

3418

4318

9719

5818

8819

2418

5419

0418

7017

9618

0418

1218

7919

7019

4519

5419

1419

4918

6118

2919

3319

7518

4820

0119

3819

8219

6119

91

Current expansion

Trough Year of Business Cycle

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

17

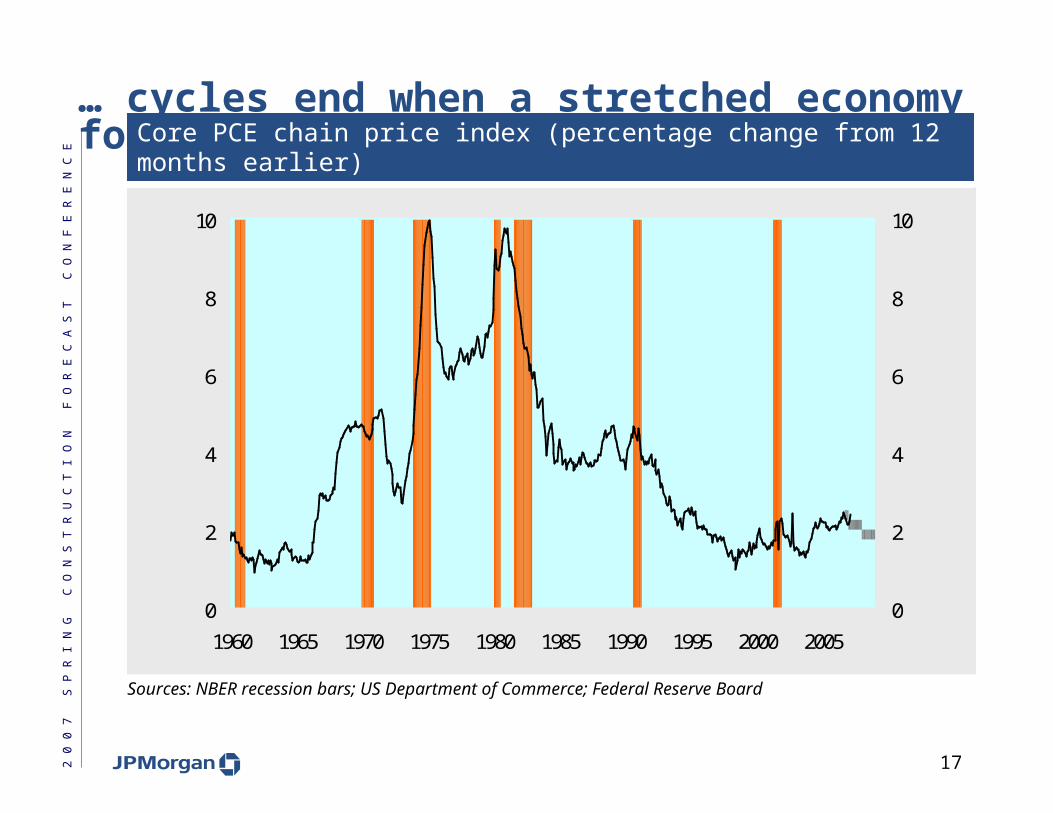

… cycles end when a stretched economy forces the Fed

Core PCE chain price index (percentage change from 12 months earlier)Core PCE chain price index (percentage change from 12 months earlier)

Sources: NBER recession bars; US Department of Commerce; Federal Reserve Board

0

2

4

6

8

10

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

0

2

4

6

8

10

The FOMC's central

tendency forecast

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

18

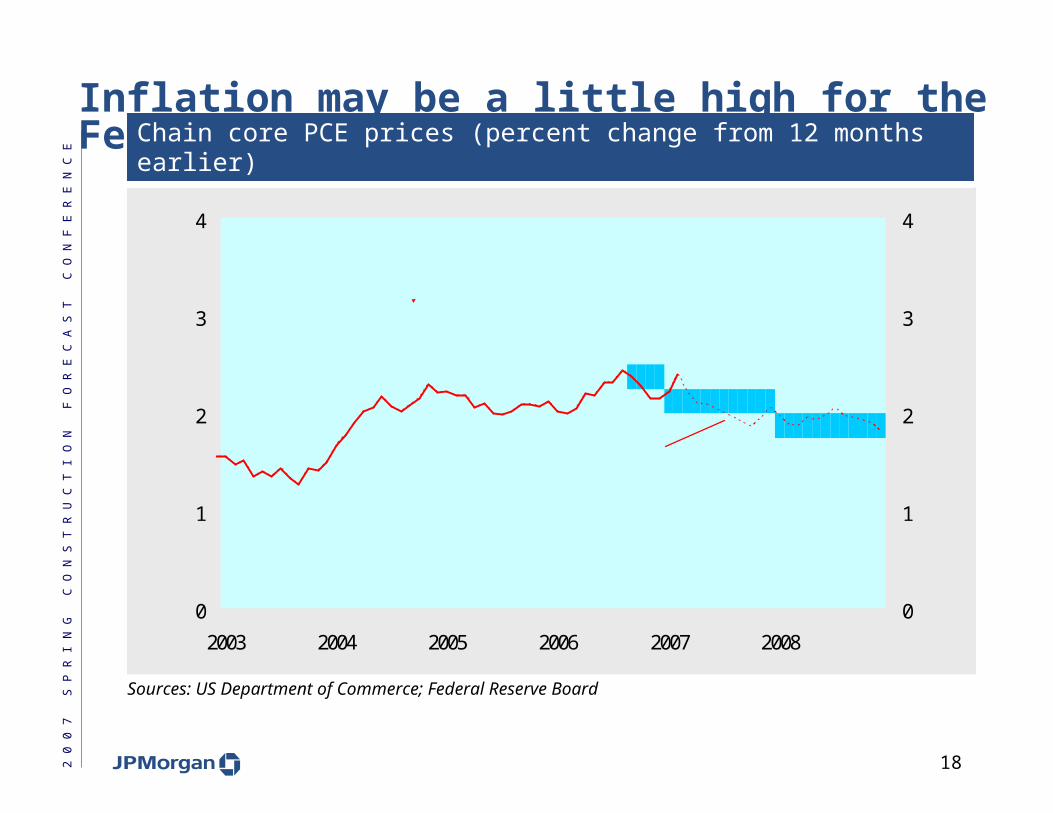

Inflation may be a little high for the Fed’s taste …

Chain core PCE prices (percent change from 12 months earlier)Chain core PCE prices (percent change from 12 months earlier)

Sources: US Department of Commerce; Federal Reserve Board

0

1

2

3

4

2003 2004 2005 2006 2007 2008

0

1

2

3

4

Band is FOMC central tendency

forecast

Dashed line is forecast (monthly changes average 0.154%)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

19

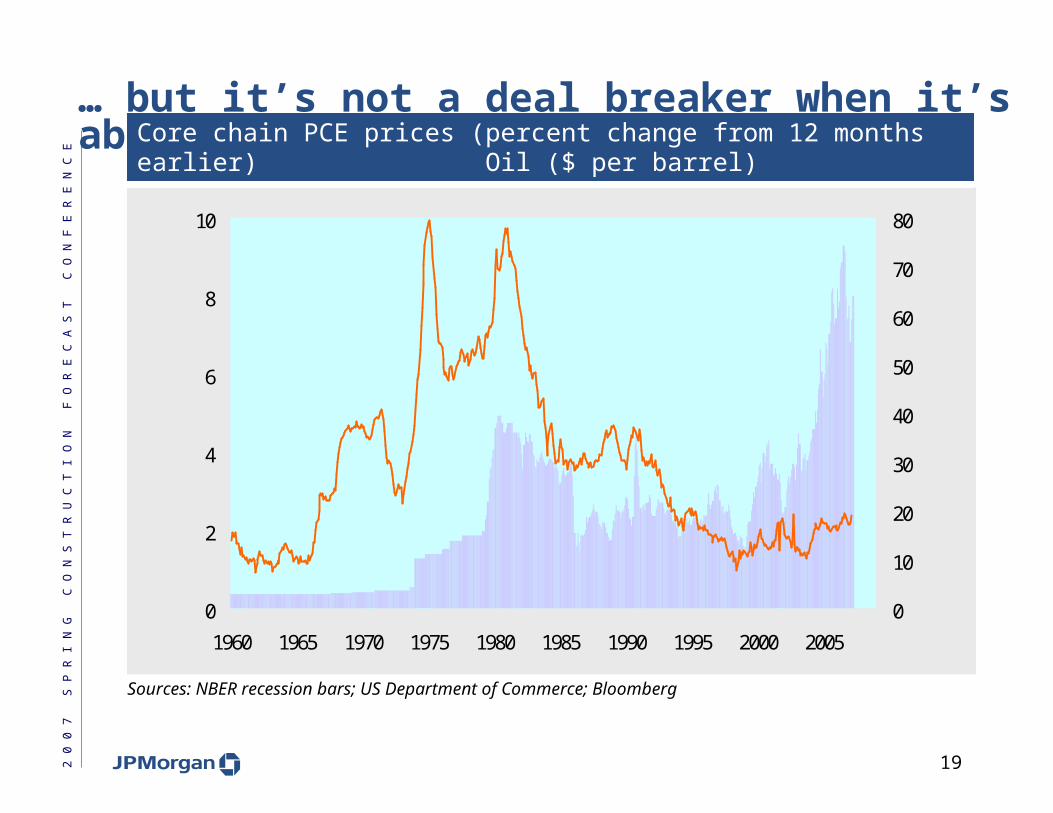

… but it’s not a deal breaker when it’s about relative prices …

Core chain PCE prices (percent change from 12 months earlier) Oil ($ per barrel)Core chain PCE prices (percent change from 12 months earlier) Oil ($ per barrel)

Sources: NBER recession bars; US Department of Commerce; Bloomberg

0

2

4

6

8

10

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

0

10

20

30

40

50

60

70

80

Petroleum (right)Core PCE chain prices

(left)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

20

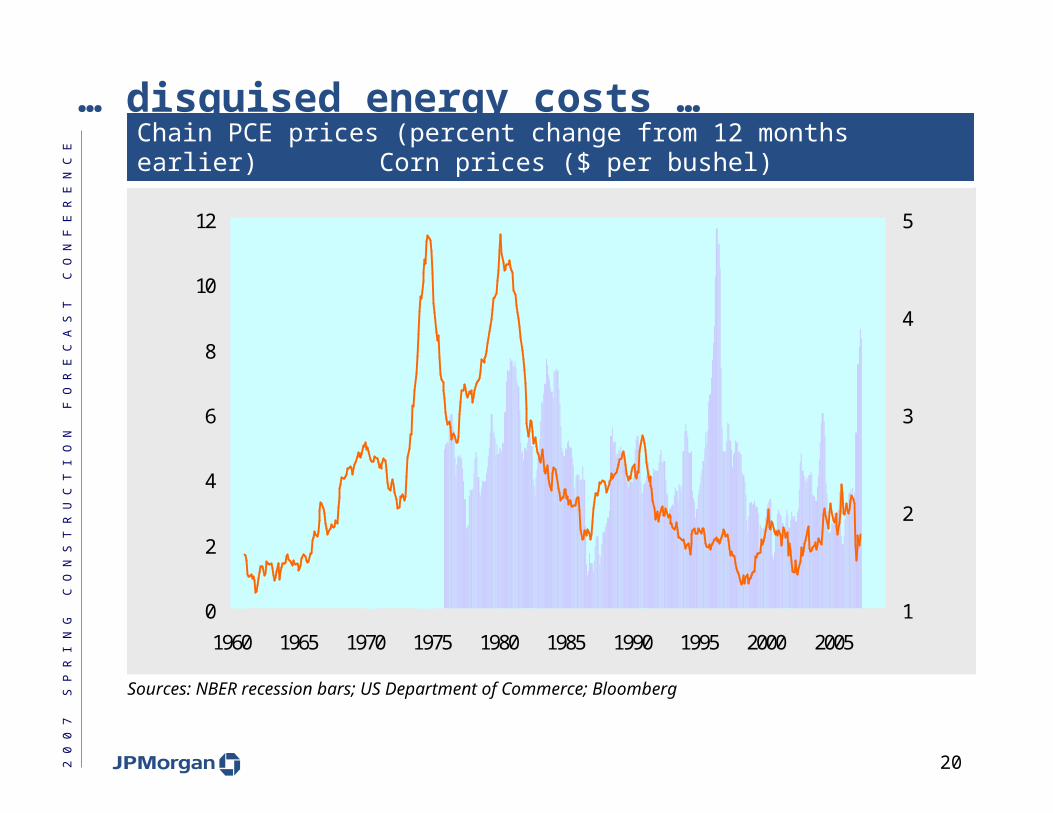

… disguised energy costs …

Chain PCE prices (percent change from 12 months earlier) Corn prices ($ per bushel)Chain PCE prices (percent change from 12 months earlier) Corn prices ($ per bushel)

Sources: NBER recession bars; US Department of Commerce; Bloomberg

0

2

4

6

8

10

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

1

2

3

4

5

Corn (right)Chain PCE prices (left)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

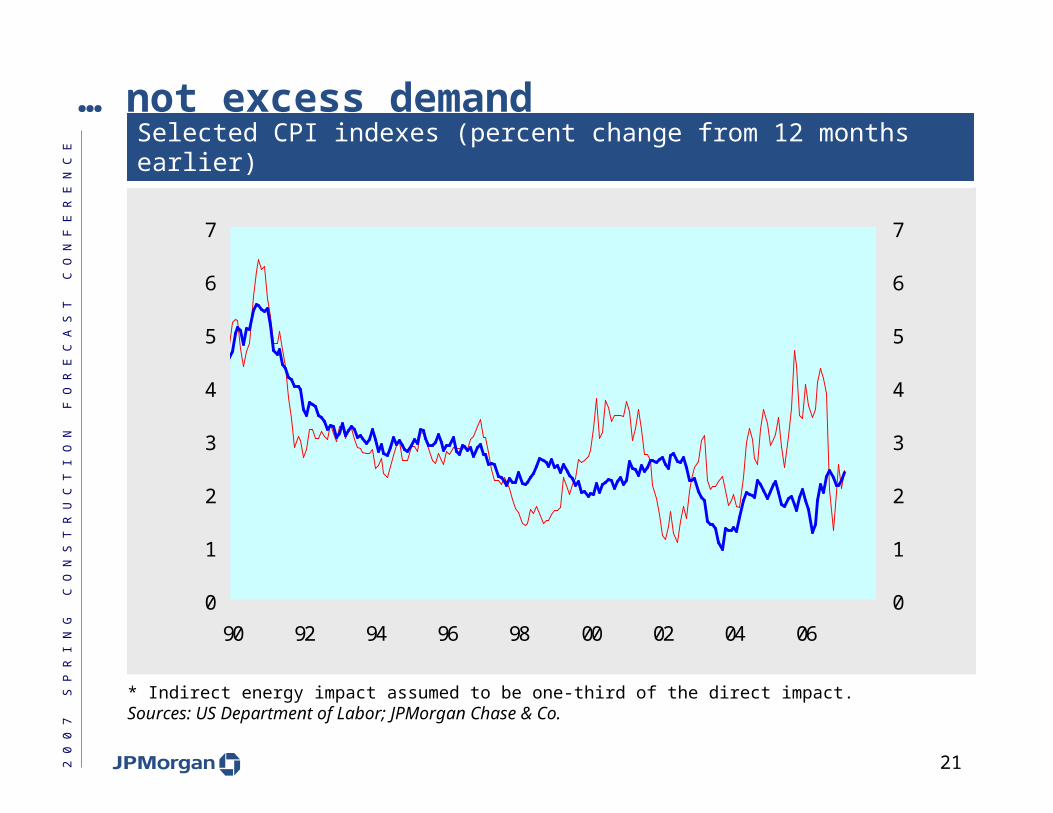

21

… not excess demand

Selected CPI indexes (percent change from 12 months earlier)Selected CPI indexes (percent change from 12 months earlier)

* Indirect energy impact assumed to be one-third of the direct impact.Sources: US Department of Labor; JPMorgan Chase & Co.

0

1

2

3

4

5

6

7

90 92 94 96 98 00 02 04 06

0

1

2

3

4

5

6

7

CPI

Excluding direct and indirect energy*

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

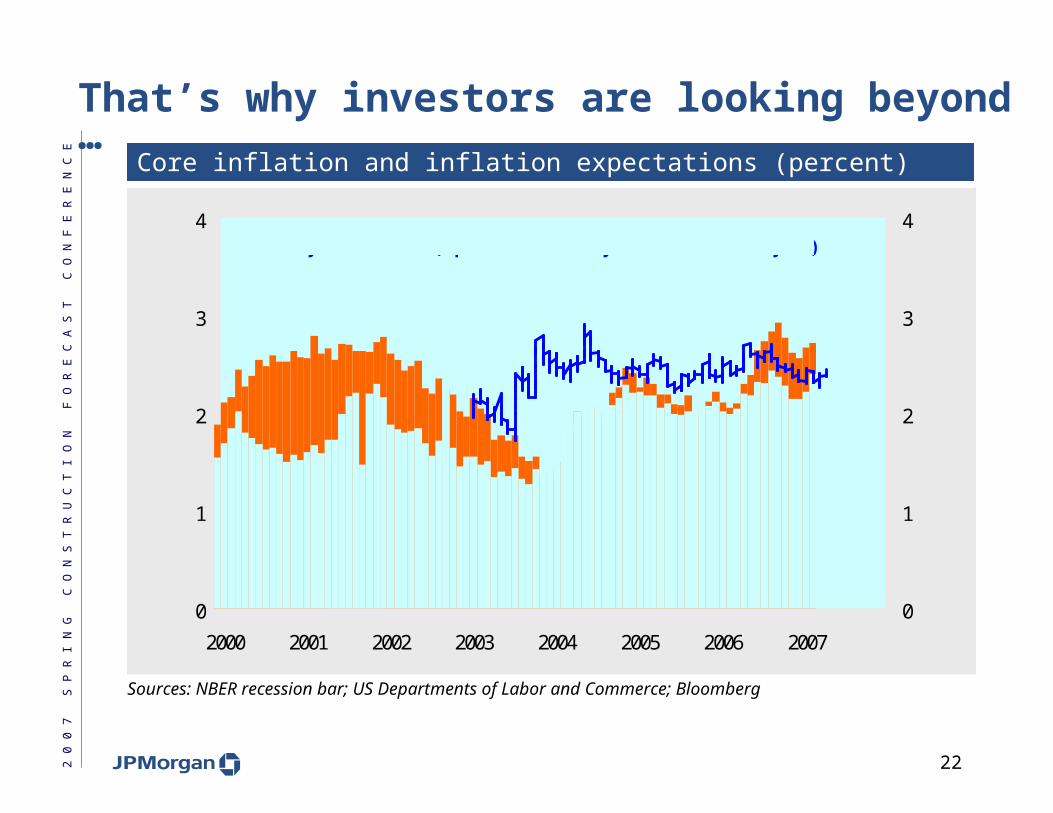

22

That’s why investors are looking beyond …

Core inflation and inflation expectations (percent)Core inflation and inflation expectations (percent)

Sources: NBER recession bar; US Departments of Labor and Commerce; Bloomberg

0

1

2

3

4

2000 2001 2002 2003 2004 2005 2006 2007

0

1

2

3

4

Core CPI, % ch. from 12 months earlier (upper boundary)

Core chain PCE prices, % ch. from 12 months earlier (lower boundary)

Five-by-five breakeven (expected inflation five years from now and beyond)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

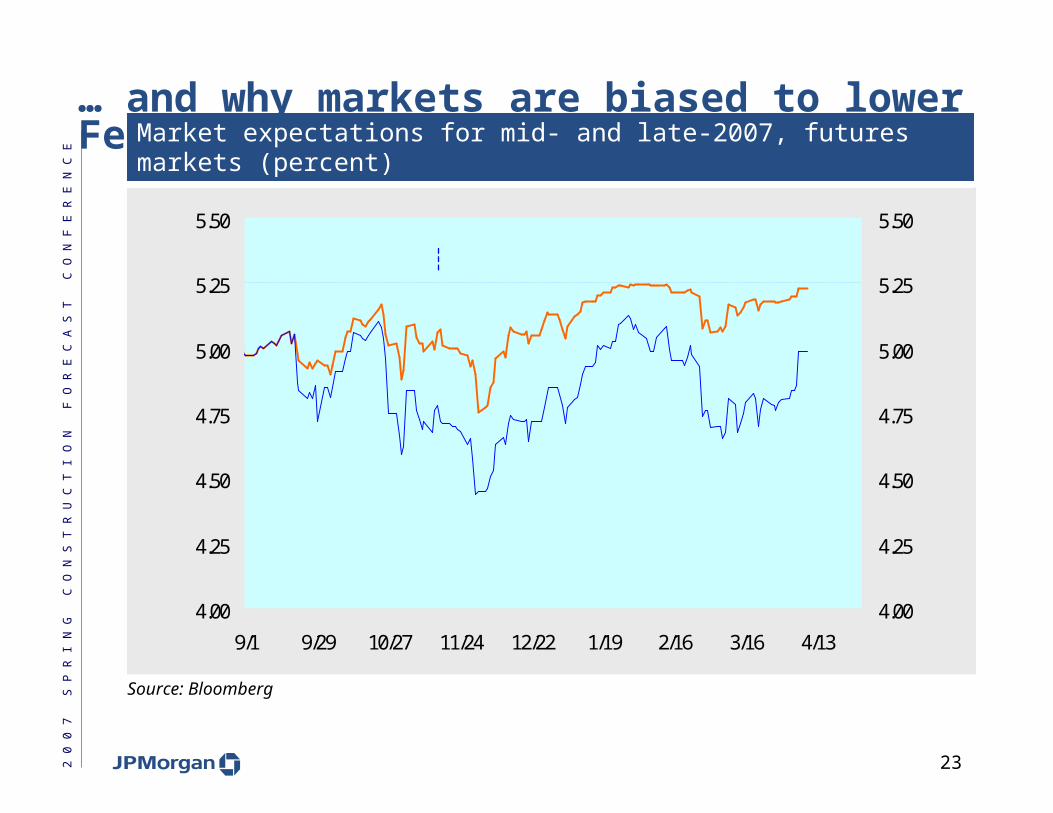

23

… and why markets are biased to lower Fed rates

Market expectations for mid- and late-2007, futures markets (percent)Market expectations for mid- and late-2007, futures markets (percent)

Source: Bloomberg

4.00

4.25

4.50

4.75

5.00

5.25

5.50

9/1 9/29 10/27 11/24 12/22 1/19 2/16 3/16 4/13

4.00

4.25

4.50

4.75

5.00

5.25

5.50

Actual fed funds target rate

Implied fed funds futures rate by June 30, 2007

Implied fed funds futures rate by December 31, 2007

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

24

Growth—the old way—needs lower interest rates… yet another friend of housing

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

25

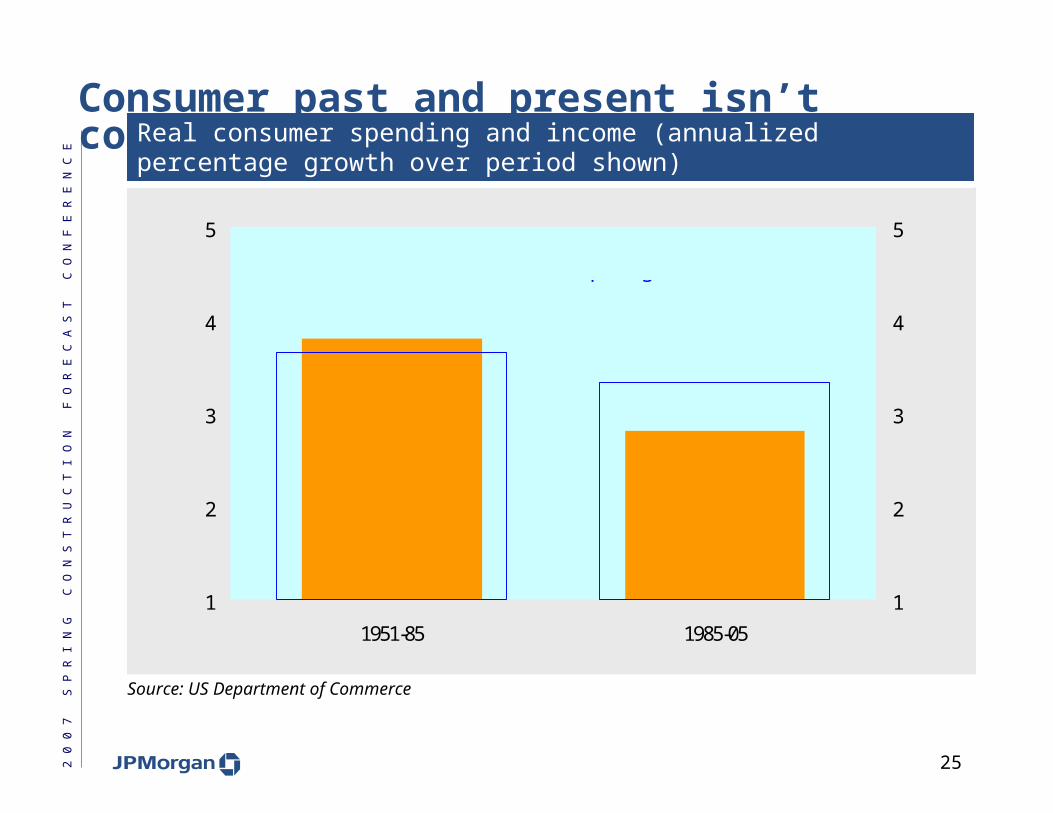

Consumer past and present isn’t consumer future

Real consumer spending and income (annualized percentage growth over period shown)Real consumer spending and income (annualized percentage growth over period shown)

Source: US Department of Commerce

1

2

3

4

5

1951-85 1985-05

1

2

3

4

5

Real consumer spending

Real income

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

26

Two decades of above-normal asset gains lifted savings

Saving rate (% of disposable income) Net worth (ratio to disposable income)Saving rate (% of disposable income) Net worth (ratio to disposable income)

Sources: US Department of Commerce; Federal Reserve Board

-4

0

4

8

12

16

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

4.0

4.5

5.0

5.5

6.0

6.5Ratio of net worth to income (right)

Saving rate (left)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

27

No mystery in the asset boom … but that was then

The Great Disinflation’s windfall

Economic liberalization’s transforming hand

Global awakening

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

28

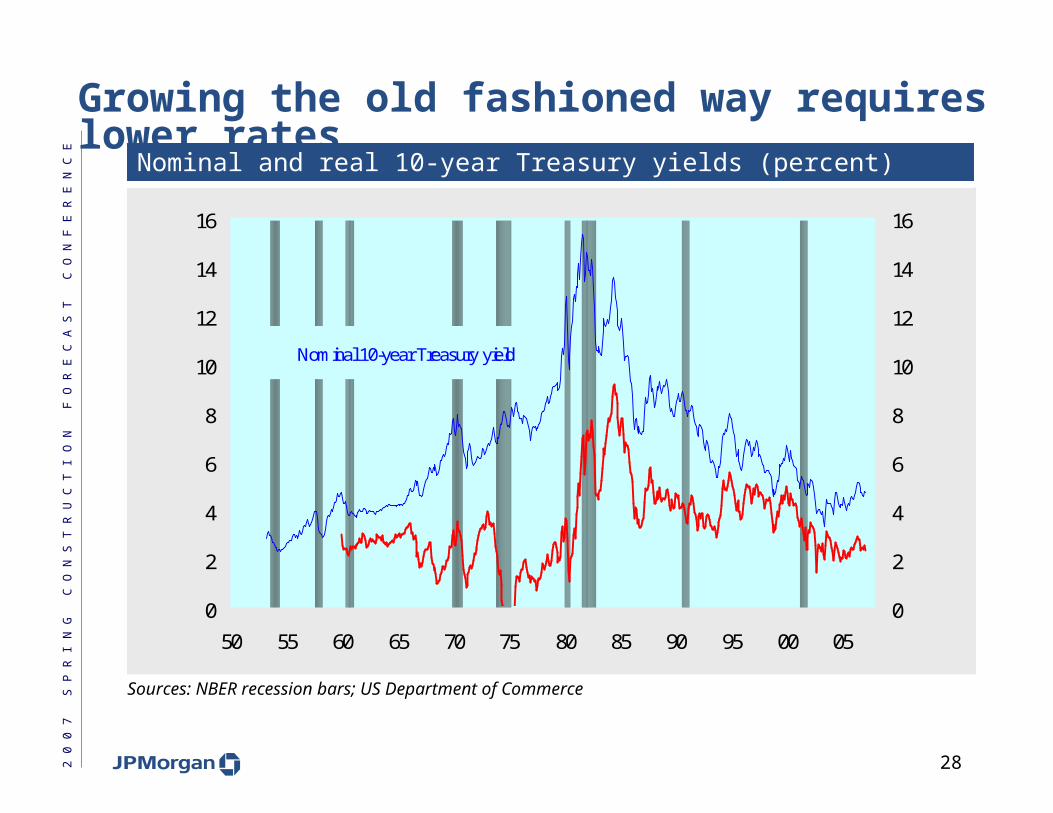

Growing the old fashioned way requires lower rates

Nominal and real 10-year Treasury yields (percent)Nominal and real 10-year Treasury yields (percent)

Sources: NBER recession bars; US Department of Commerce

0

2

4

6

8

10

12

14

16

50 55 60 65 70 75 80 85 90 95 00 05

0

2

4

6

8

10

12

14

16

Nominal 10-year Treasury yield

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

29

Conclusion … what investors see

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

30

Investors see good news …

Non-investment grade debt yield less 10-year swap rate (basis points)Non-investment grade debt yield less 10-year swap rate (basis points)

Sources: Ibbotson Associates, JPMorgan

200

300

400

500

600

700

800

900

1,000

1,100

1990 1992 1994 1996 1998 2000 2002 2004 2006200

300

400

500

600

700

800

900

1,000

1,100

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

31

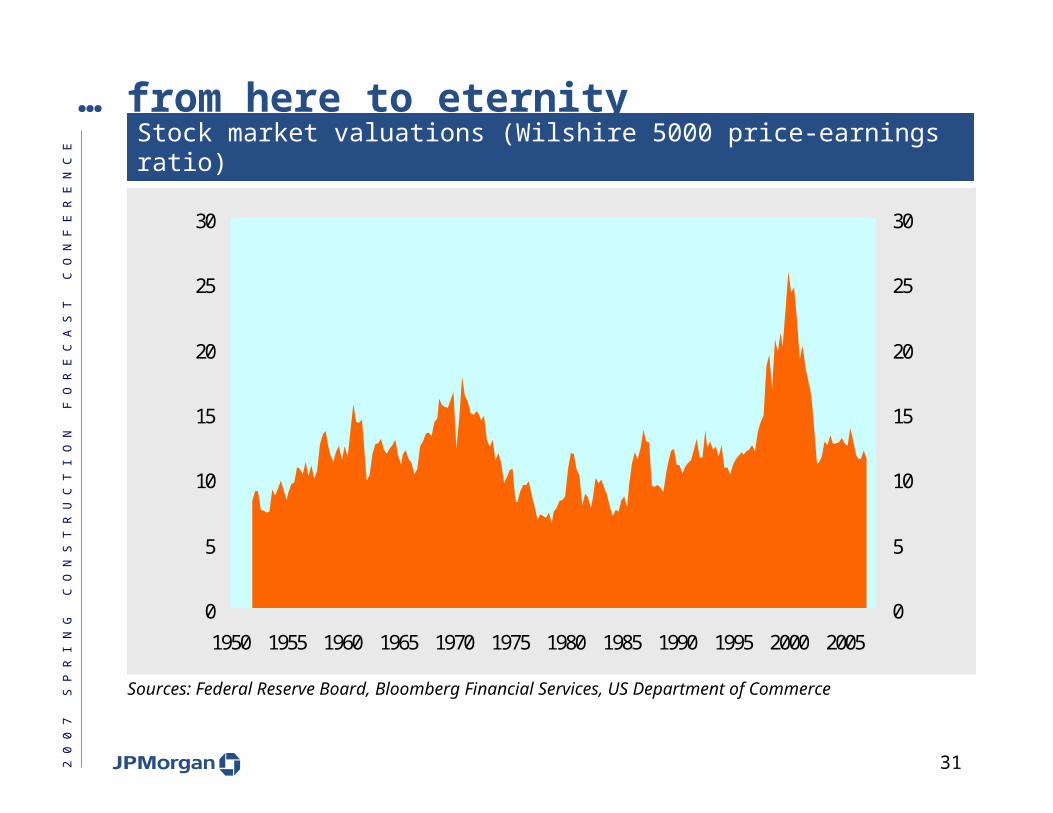

… from here to eternity

Stock market valuations (Wilshire 5000 price-earnings ratio)Stock market valuations (Wilshire 5000 price-earnings ratio)

Sources: Federal Reserve Board, Bloomberg Financial Services, US Department of Commerce

0

5

10

15

20

25

30

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

0

5

10

15

20

25

30

After-tax economic GDP profits (right)

2 0

0 7

S P

R I

N G

C

O N

S T

R U

C T

I O

N

F O

R E

C A

S T

C

O N

F E

R E

N C

E

32

Analysts’ Compensation: The research analysts responsible for the preparation of this report receive compensation based upon various factors, including the quality and accuracy of research, client feedback, competitive factors and overall firm revenues. The firm’s overall revenues include revenues from its investment banking and fixed income business units. Principal Trading: JPMorgan and/or its affiliates normally make a market and trade as principal in the securities discussed in this report.

Legal Entities: JPMorgan is the marketing name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. J.P. Morgan Securities Inc. is a member of NYSE and SIPC. JPMorgan Chase Bank, N.A. is a member of FDIC and is authorized and regulated in the UK by the Financial Services Authority. J.P. Morgan Futures Inc. is a member of the NFA. J.P. Morgan Securities Ltd. (JPMSL) is a member of the London Stock Exchange and is authorized and regulated by the Financial Services Authority. J.P. Morgan Equities Limited is a member of the Johannesburg Securities Exchange and is regulated by the FSB. J.P. Morgan Securities (Asia Pacific) Limited (CE number AAJ321) is regulated by the Hong Kong Monetary Authority. JPMorgan Chase Bank, Singapore branch is regulated by the Monetary Authority of Singapore. J.P. Morgan Securities Asia Private Limited is regulated by the MAS and the Financial Services Agency in Japan. J.P. Morgan Australia Limited (ABN 52 002 888 011/AFS License No: 238188) (JPMSAL) is a licensed securities dealer

General: Information has been obtained from sources believed to be reliable but JPMorgan does not warrant its completeness or accuracy except with respect to any disclosures relative to JPMSI and/or its affiliates and the analyst’s involvement with the issuer. Opinions and estimates constitute our judgment as at the date of this material and are subject to change without notice. Past performance is not indicative of future results. The investments and strategies discussed here may not be suitable for all investors; if you have any doubts you should consult your investment advisor. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. JPMorgan and/or its affiliates and employees may act as placement agent, advisor or lender with respect to securities or issuers referenced in this report. Clients should contact analysts at and execute transactions through a JPMorgan entity in their home jurisdiction unless governing law permits otherwise. This report should not be distributed to others or replicated in any form without prior consent of JPMorgan. U.K. and European Economic Area (EEA): Investment research issued by JPMSL has been prepared in accordance with JPMSL’s Policies for Managing Conflicts of Interest in Connection with Investment Research. This report has been issued in the U.K. only to persons of a kind described in Article 19 (5), 38, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 (all such persons being referred to as “relevant persons”). This document must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this document relates is only available to relevant persons and will be engaged in only with relevant persons. In other EEA countries, the report has been issued to persons regarded as professional investors (or equivalent) in their home jurisdiction. Australia: This material is issued and distributed by JPMSAL in Australia to “wholesale clients” only. JPMSAL does not issue or distribute this material to “retail clients.” The recipient of this material must not distribute it to any third party or outside Australia without the prior written consent of JPMSAL. For the purposes of this paragraph the terms “wholesale client” and “retail client” have the meanings given to them in section 761G of the Corporations Act 2001. Korea: This report may have been edited or contributed to from time to time by affiliates of J.P. Morgan Securities (Far East) Ltd, Seoul branch.

Copyright 2007 JPMorgan Chase & Co. All rights reserved. Additional information available upon request.