1Q11 Results Conference Call

16

1Q11 Earnings Conference Call

-

Upload

pineriweb -

Category

Economy & Finance

-

view

55 -

download

0

Transcript of 1Q11 Results Conference Call

1Q11

Earnings Conference Call

Content

Financial Information

1Q11 Highlights Page 4

1Q11 Highlights – Corporate Business Page 5

Credit Portfolio Page 6

Credit Portfolio Profile Page 7

Credit Portfolio Quality Page 8

2/16Investor Relations| 1Q11 |

Credit Portfolio Quality Page 8

Payroll Deductible Loan Portfolio Page 9

Funding Page 10

Funding and Credit Portfolio Maturities Page 11

Capital Adequacy Ratio (BIS) Page 12

Other Highlights

2011 Guidance – BR GAAP Page 14

1Q11 Events and Highlights Page 15

1Q11 – Financial Information

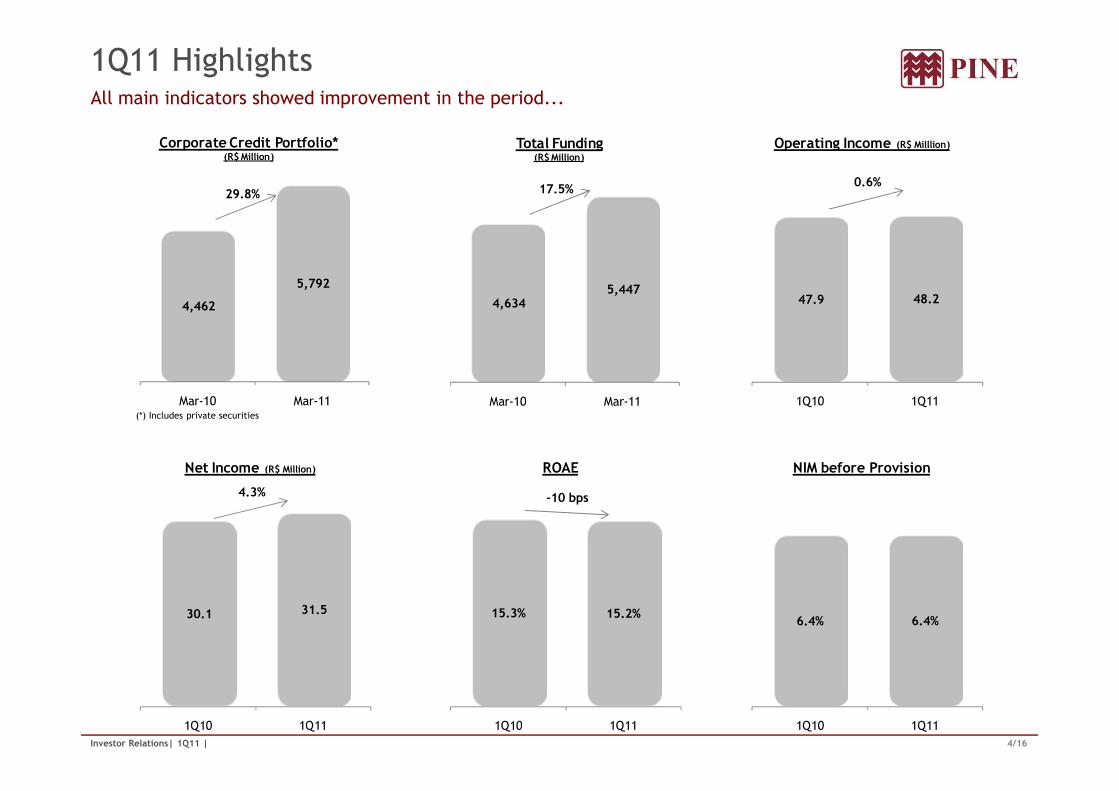

1Q11 HighlightsAll main indicators showed improvement in the period...

4,462

5,792

Mar-10 Mar-11

Corporate Credit Portfolio*(R$ Million)

29.8%

4,634 5,447

Mar-10 Mar-11

Total Funding(R$ Million)

17.5%

47.9 48.2

1Q10 1Q11

Operating Income (R$ Milllion)

0.6%

4/16Investor Relations| 1Q11 |

(*) Includes private securities

Mar-10 Mar-11 Mar-10 Mar-11 1Q10 1Q11

30.1 31.5

1Q10 1Q11

Net Income (R$ Million)

4.3%

15.3% 15.2%

1Q10 1Q11

ROAE

-10 bps

6.4% 6.4%

1Q10 1Q11

NIM before Provision

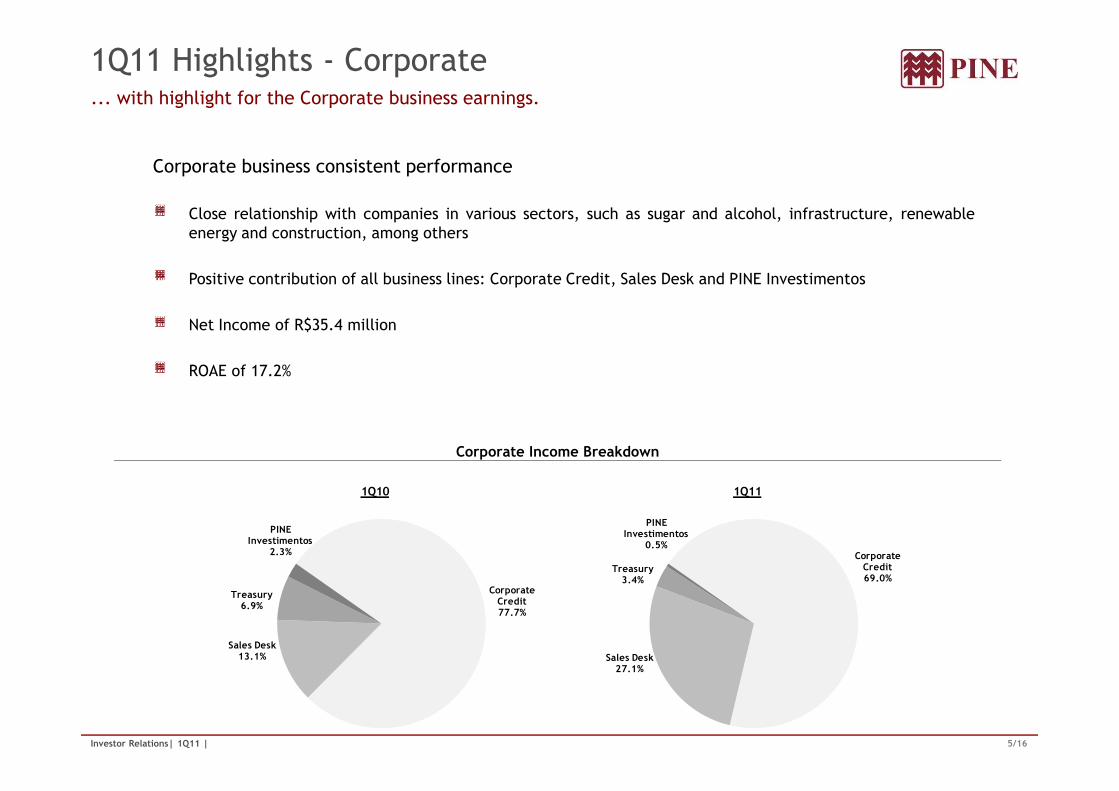

1Q11 Highlights - Corporate... with highlight for the Corporate business earnings.

Corporate business consistent performance

Close relationship with companies in various sectors, such as sugar and alcohol, infrastructure, renewableenergy and construction, among others

Positive contribution of all business lines: Corporate Credit, Sales Desk and PINE Investimentos

Net Income of R$35.4 million

ROAE of 17.2%

5/16Investor Relations| 1Q11 |

Corporate Income Breakdown

Corporate Credit77.7%

Sales Desk13.1%

Treasury6.9%

PINE Investimentos

2.3%

1Q10

Corporate Credit69.0%

Sales Desk27.1%

Treasury3.4%

PINE Investimentos

0.5%

1Q11

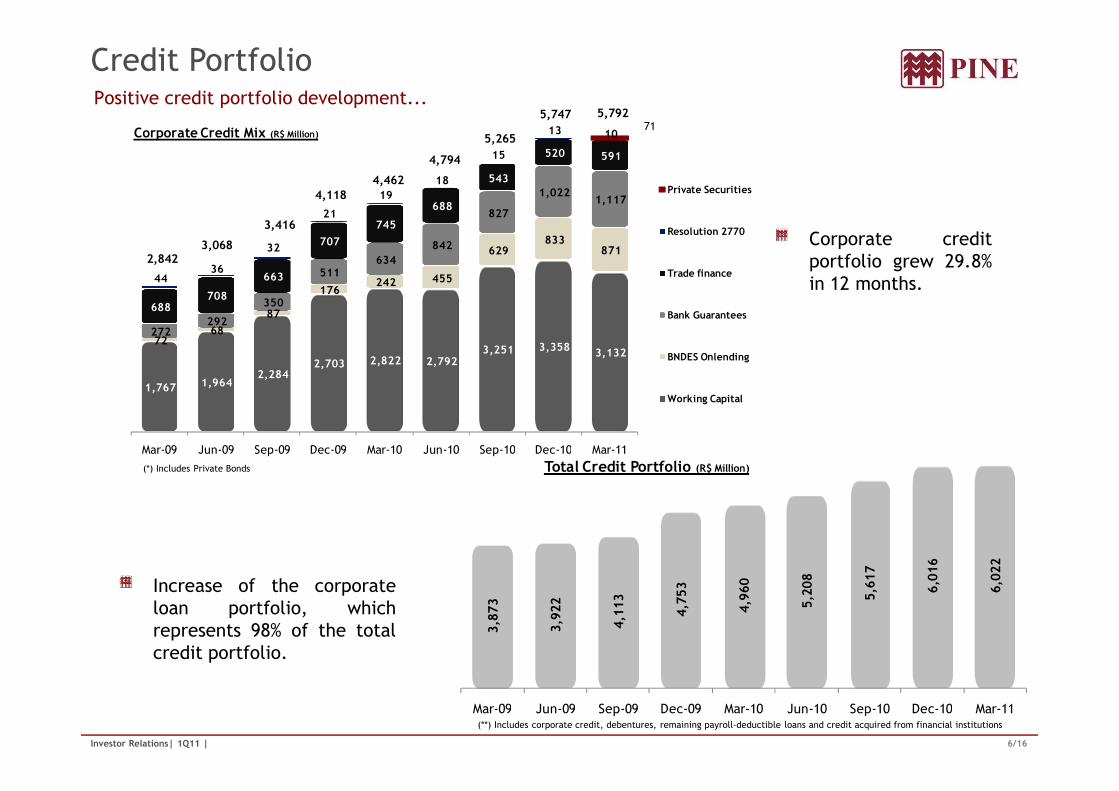

Credit PortfolioPositive credit portfolio development...

Corporate creditportfolio grew 29.8%in 12 months.

1,767 1,964 2,284

2,703 2,822 2,792 3,251 3,358

3,132 72

68

87

176 242 455

629 833

871

272 292

350

511 634

842

827

1,022 1,117

688 708

663

707

745

688

543

520 591

44 36

32

21

19

18

15

13 10 Corporate Credit Mix (R$ Million)

Private Securities

Resolution 2770

Trade finance

Bank Guarantees

BNDES Onlending

Working Capital

2,8423,068

3,416

4,1184,462

4,794

5,265

5,747 5,79271

6/16Investor Relations| 1Q11 |

Increase of the corporateloan portfolio, whichrepresents 98% of the totalcredit portfolio.

(*) Includes Private Bonds

(**) Includes corporate credit, debentures, remaining payroll-deductible loans and credit acquired from financial institutions

3,873

3,922

4,113

4,753

4,960

5,208

5,617

6,016

6,022

Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11

Total Credit Portfolio (R$ Million)Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11

Working Capital

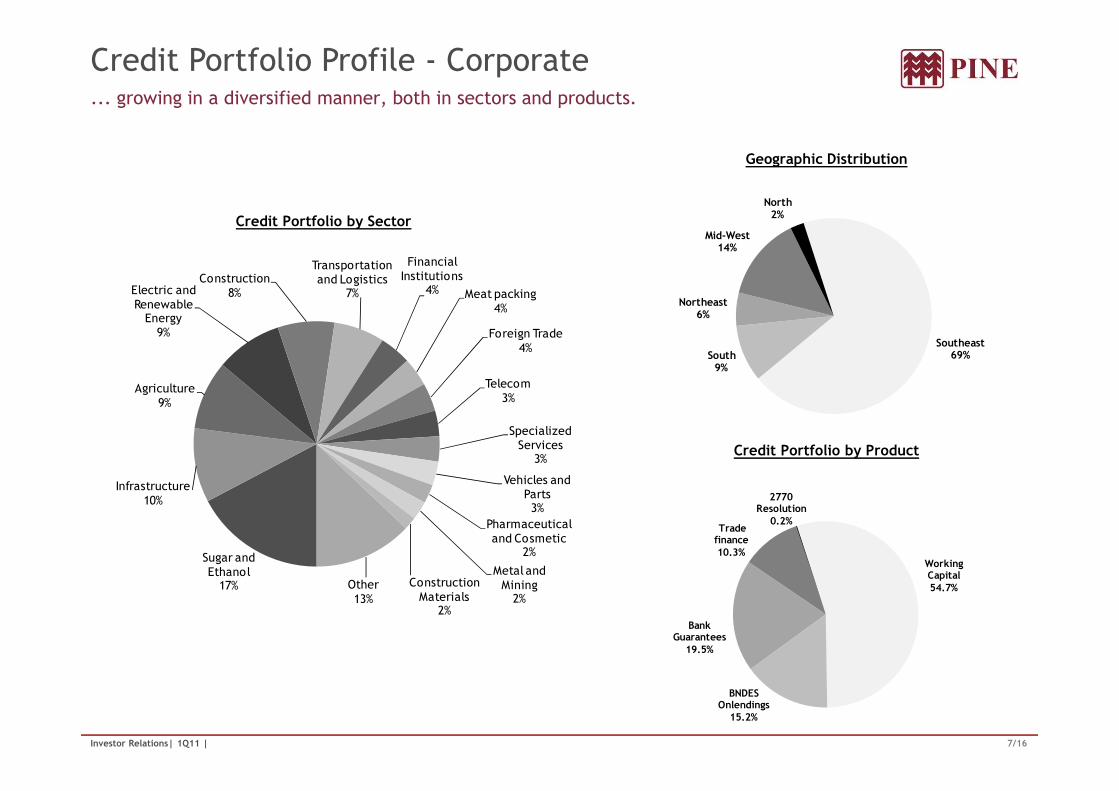

Credit Portfolio Profile - Corporate... growing in a diversified manner, both in sectors and products.

Credit Portfolio by Sector

Geographic Distribution

Agriculture9%

Electric and Renewable Energy9%

Construction8%

Transportation and Logistics

7%

Financial Institutions

4% Meat packing4%

Foreign Trade4%

Telecom3%

Southeast69%South

9%

Northeast6%

Mid-West14%

North2%

7/16Investor Relations| 1Q11 |

Credit Portfolio by Product

Sugar and Ethanol17%

Infrastructure10%

9% 3%

Specialized Services

3%

Vehicles and Parts3%

Pharmaceutical and Cosmetic

2%

Metal and Mining2%

Construction Materials

2%

Other13%

Working Capital54.7%

BNDES Onlendings

15.2%

Bank Guarantees

19.5%

Trade finance 10.3%

2770 Resolution

0.2%

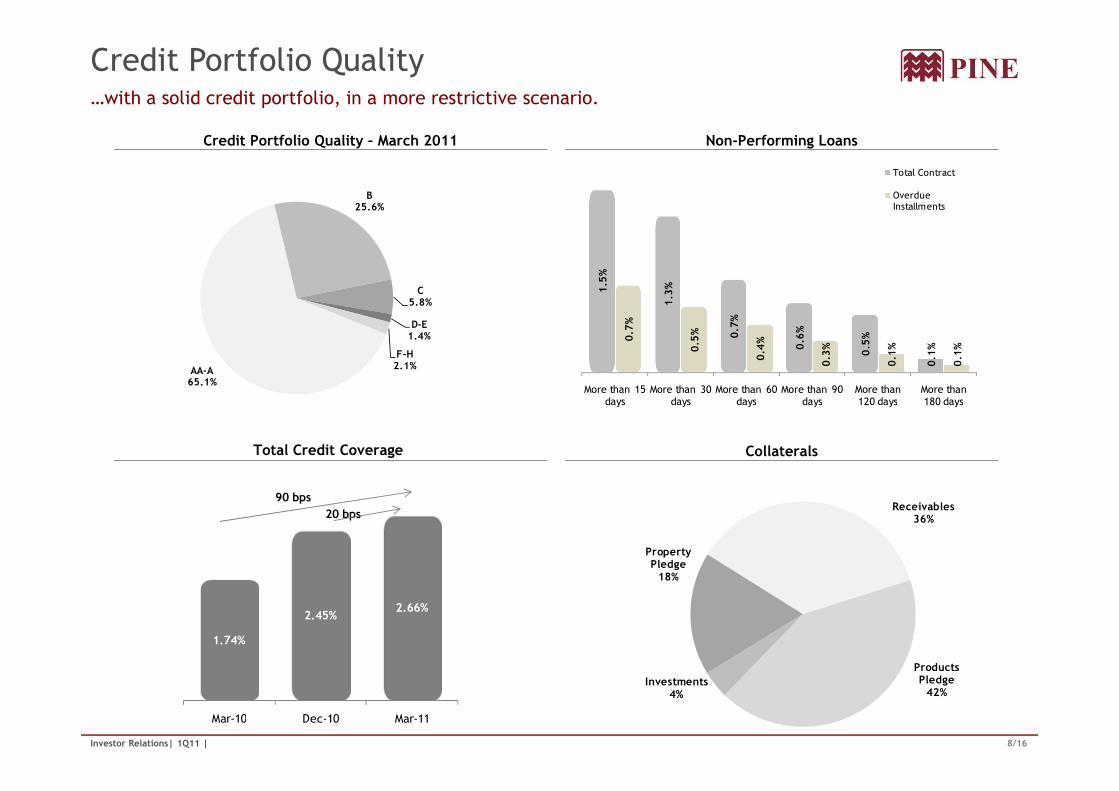

Credit Portfolio Quality

Credit Portfolio Quality – March 2011 Non-Performing Loans

…with a solid credit portfolio, in a more restrictive scenario.

1.5%

1.3%

0.7%

0.6%

0.5%

0.1%

0.7%

0.5%

0.4%

0.3%

0.1%

0.1%

More than 15 days

More than 30 days

More than 60 days

More than 90 days

More than 120 days

More than 180 days

Total Contract

Overdue Installments

AA-A65.1%

B25.6%

C5.8%

D-E1.4%

F-H2.1%

8/16Investor Relations| 1Q11 |

Total Credit Coverage Collaterals

More than 15 days

More than 30 days

More than 60 days

More than 90 days

More than 120 days

More than 180 days

1.74%

2.45%2.66%

Mar-10 Dec-10 Mar-11

90 bps

20 bpsReceivables

36%

Products Pledge42%

Investments4%

Property Pledge18%

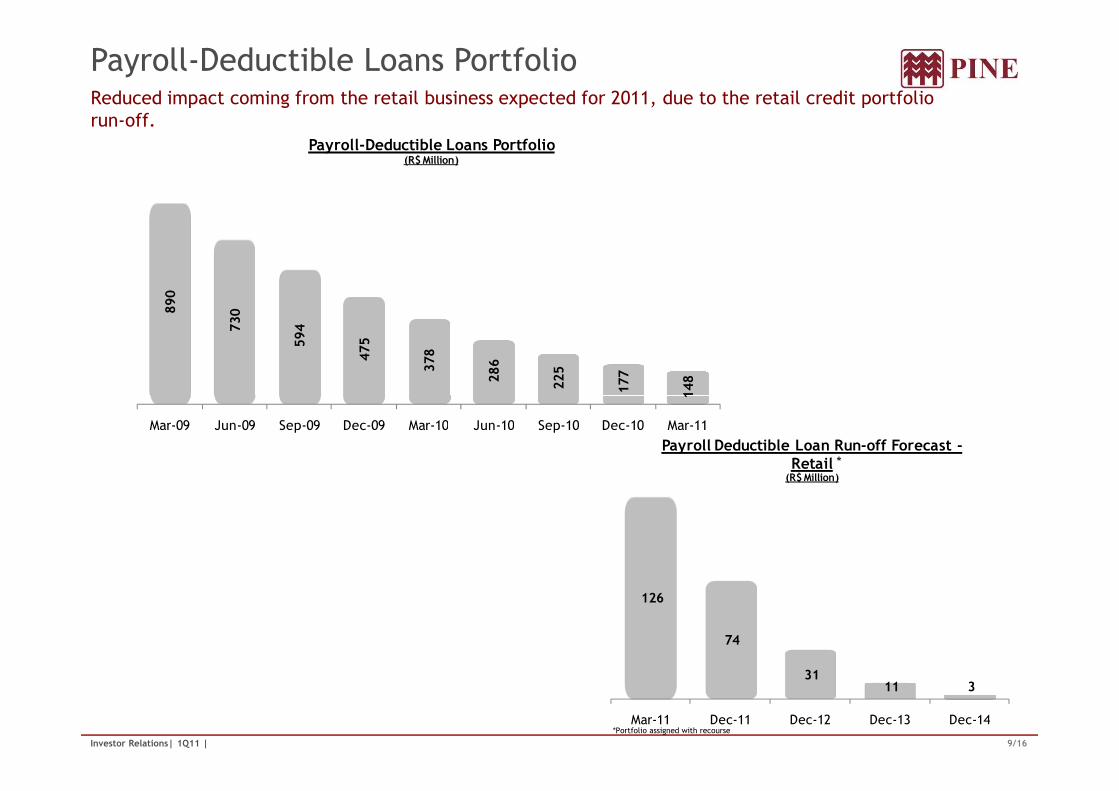

Payroll-Deductible Loans PortfolioReduced impact coming from the retail business expected for 2011, due to the retail credit portfolio run-off.

890

730

594

475

378

286

225

177

148

Payroll-Deductible Loans Portfolio(R$ Million)

9/16Investor Relations| 1Q11 |

148

Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11

126

74

31 11 3

Mar-11 Dec-11 Dec-12 Dec-13 Dec-14

Payroll Deductible Loan Run-off Forecast -Retail

(R$ Million)

*

*Portfolio assigned with recourse

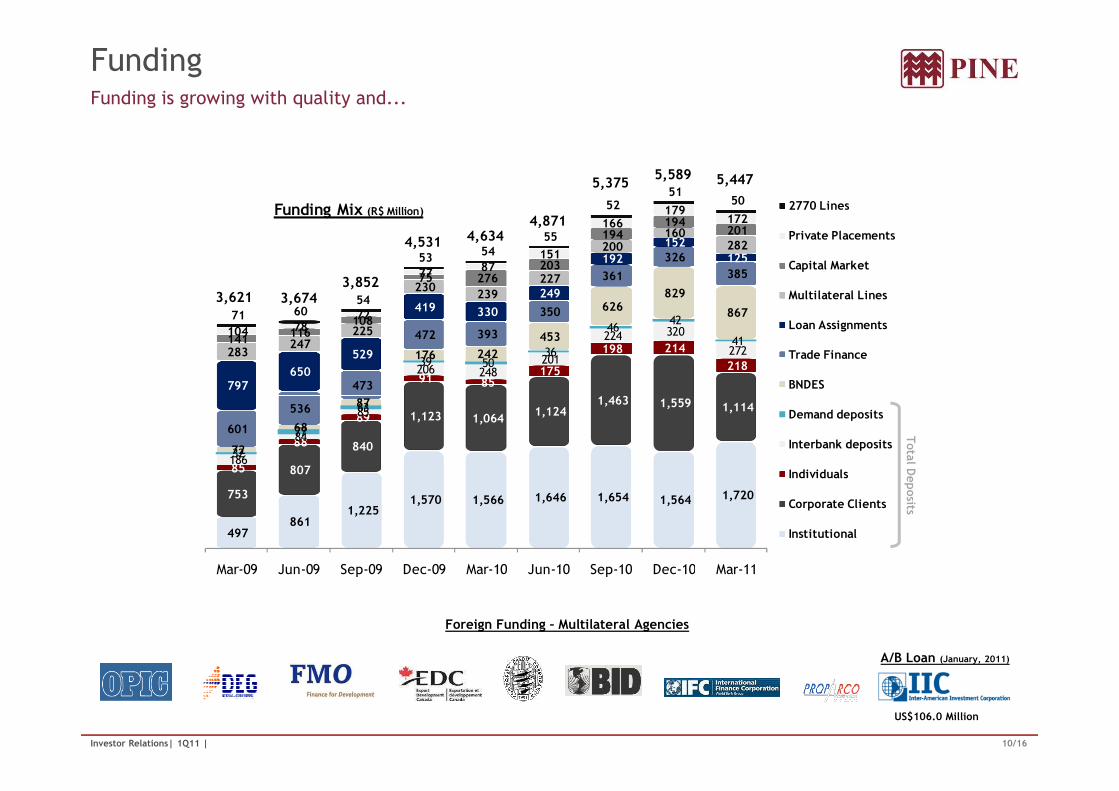

FundingFunding is growing with quality and...

1,463 1,559

91 85 175

198 214

218 206 248 201

224 320

272 39 50

36

46 42

41

87

176 242

453

626 829

867

473

472 393

350

361

326

385

797 650

529

419 330

249

192

152

125

283 247

225

230 239

227

200 160

282

141 116

108

75 276 203

194 194

201

104 78 72

77 87 151

166 179

172

71 60 54

53 54

55

52 51

50 Funding Mix (R$ Million) 2770 Lines

Private Placements

Capital Market

Multilateral Lines

Loan Assignments

Trade Finance

BNDES

5,375

4,8714,6344,531

3,8523,6743,621

5,589 5,447

10/16Investor Relations| 1Q11 |

Foreign Funding – Multilateral Agencies

US$106.0 Million

A/B Loan (January, 2011)

Total D

eposits

497 861

1,225 1,570 1,566 1,646 1,654 1,564 1,720 753

807

840

1,123 1,064 1,124

1,463 1,559 1,114

85

88

89

186

84

85

32

77

63

72

68

87

601

536

Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11

Demand deposits

Interbank deposits

Individuals

Corporate Clients

Institutional

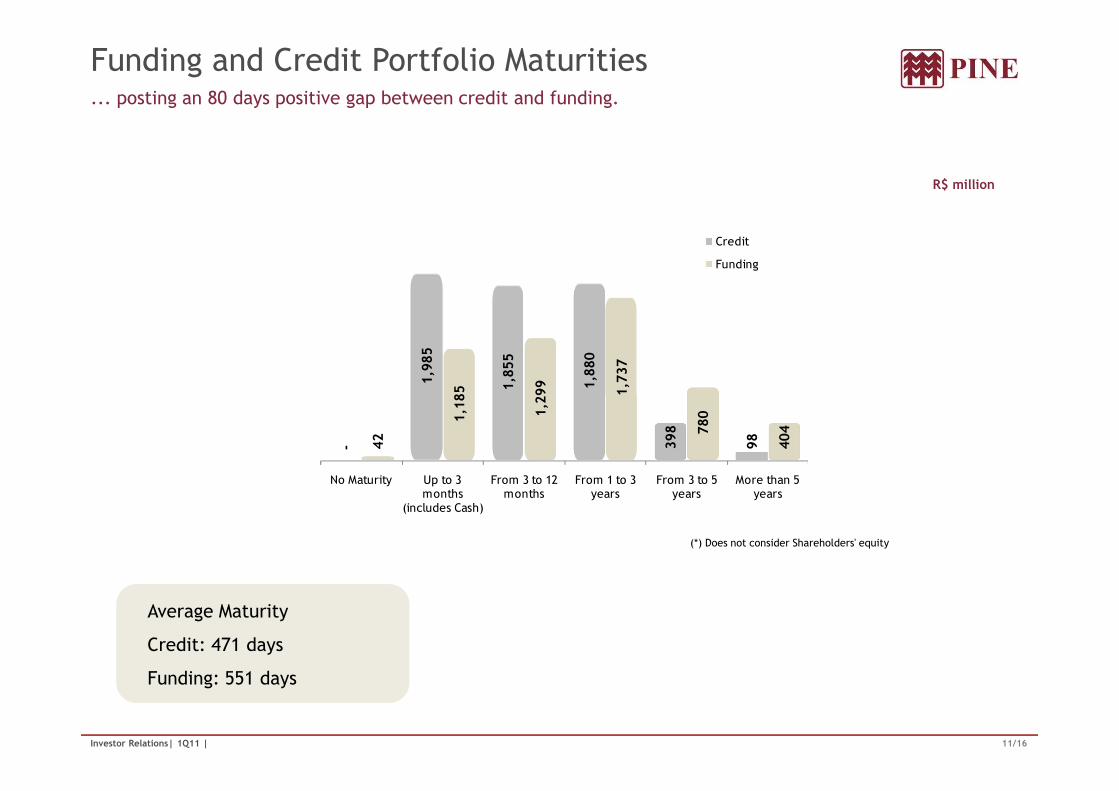

Funding and Credit Portfolio Maturities ... posting an 80 days positive gap between credit and funding.

R$ million

1,985

1,855

1,880

1,185

1,299

1,737

Credit

Funding

11/16Investor Relations| 1Q11 |

Average Maturity

Credit: 471 days

Funding: 551 days

(*) Does not consider Shareholders' equity

- 398

98

42

1,185

1,299

1,737

780

404

No Maturity Up to 3 months

(includes Cash)

From 3 to 12 months

From 1 to 3 years

From 3 to 5 years

More than 5 years

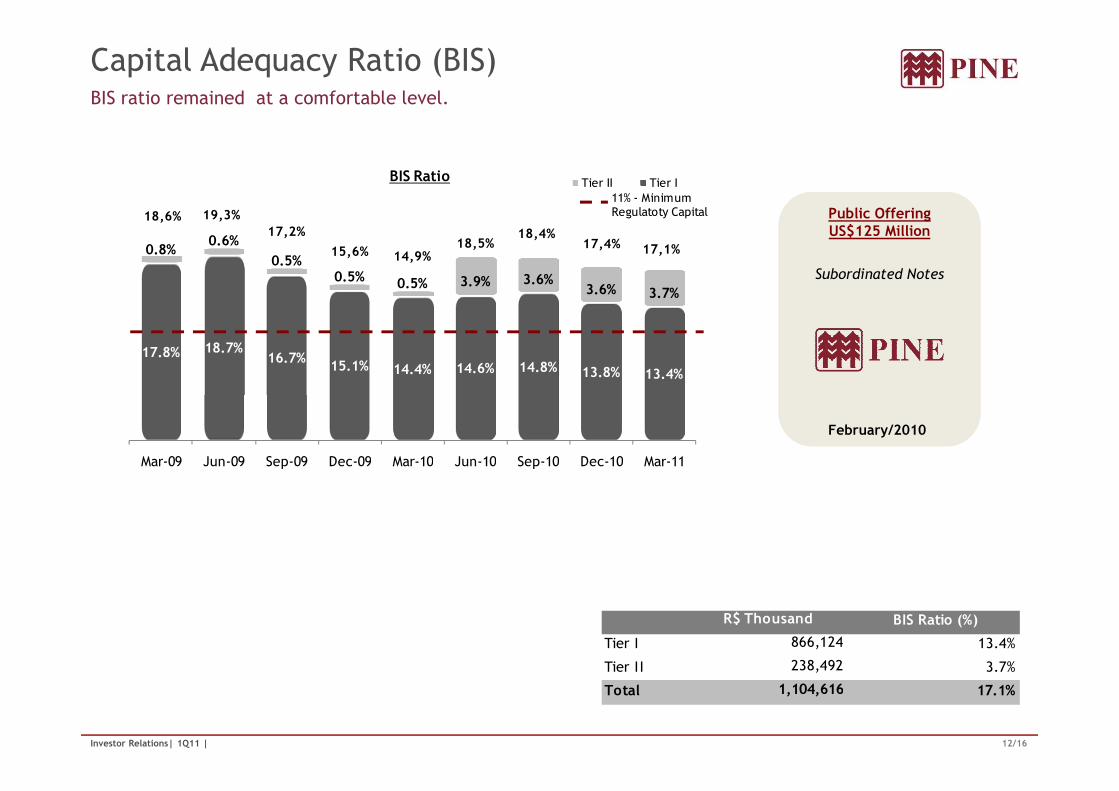

Capital Adequacy Ratio (BIS)BIS ratio remained at a comfortable level.

Subordinated Notes

Public OfferingUS$125 Million

17.8% 18.7%16.7%

15.1% 14.4% 14.6% 14.8% 13.8% 13.4%

0.8%0.6%

0.5%0.5% 0.5% 3.9% 3.6%

3.6% 3.7%

BIS Ratio Tier II Tier I

18,6% 19,3%17,2%

15,6% 14,9%18,5%

18,4%17,4%

11% - Minimum Regulatoty Capital

17,1%

12/16Investor Relations| 1Q11 |

February/2010

Tier I 13.4%

Tier II 3.7%

Total 17.1%

866,124

238,492

1,104,616

R$ Thousand BIS Ratio (%)

Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11

Other Highlights

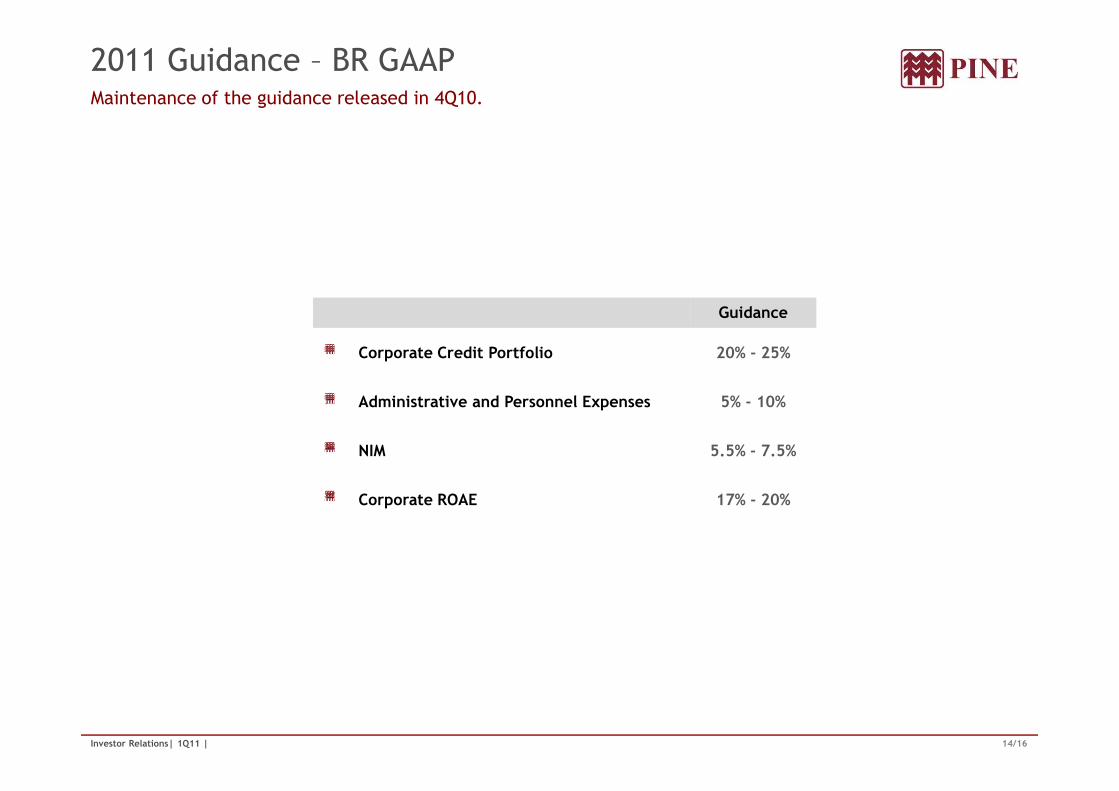

2011 Guidance – BR GAAPMaintenance of the guidance released in 4Q10.

Guidance

Corporate Credit Portfolio 20% - 25%

Administrative and Personnel Expenses 5% - 10%

14/16Investor Relations| 1Q11 |

Administrative and Personnel Expenses 5% - 10%

NIM 5.5% - 7.5%

Corporate ROAE 17% - 20%

1Q11 Events and HighlightsMarket Recognition.

PINE is ranked the 13th largest bank in Cetip’s overall derivatives ranking and the 3rd largest incommodities hedge for clients

On April 6th, PINE’s corporate credit FIDC transaction was successfully completed. The amountof the transaction was R$ 300 million, with a AA+ rating attributed by S&P

PINE was considered, for the second consecutive year, the best commercial bank in Brazil in theWorld Finance Banking Awards. The award was created by British magazine World Finance.Some of the most important criteria were: solutions for clients and optimization of

15/16Investor Relations| 1Q11 |

Some of the most important criteria were: solutions for clients and optimization ofrelationships, innovation and flexibility, and staying ahead of the competition

Investor Relations

Norberto Zaiet Junior

CFO

Nira Bessler

Head of Investor Relations

Alexandre Cavalcanti

16/16Investor Relations| 1Q11 |

This presentation contains forward-looking statements relating to the prospects of the business, estimates for operating and financial results, and those related to growth prospects of Banco Pine. These aremerely projections and, as such, are based exclusively on the expectations of Banco Pine’s management concerning the future of the business and its continued access to capital to fund the Company’sbusiness plan. Such forward-looking statements depend, substantially, on changes in market conditions, government regulations, competitive pressures, the performance of the Brazilian economy and theindustry, among other factors and risks disclosed in Banco Pine’s filed disclosure documents and are, therefore, subject to change without prior notice.

Investor Relations Manager

Alejandra Hidalgo

Investor Relations Analyst

Phone: +55-11-3372-5553 / 5552

www.bancopine.com.br/ir