1H FY2013 Financial Results Presentation · Restructuring & redundancy costs 2 3 Steel...

47

Paul O’Malley, Managing Director and Chief Executive Officer Charlie Elias, Chief Financial Officer 18 February 2013 1H FY2013 Financial Results Presentation BlueScope Steel Limited. ASX Code: BSL

Transcript of 1H FY2013 Financial Results Presentation · Restructuring & redundancy costs 2 3 Steel...

Paul O’Malley, Managing Director and Chief Executive OfficerCharlie Elias, Chief Financial Officer

18 February 2013

1H FY2013 Financial Results Presentation

BlueScope Steel Limited. ASX Code: BSL

Page 2

Important notice

THIS PRESENTATION IS NOT AND DOES NOT FORM PART OF ANY OFFER, INVITATION ORRECOMMENDATION IN RESPECT OF SECURITIES. ANY DECISION TO BUY OR SELL BLUESCOPE STEELLIMITED SECURITIES OR OTHER PRODUCTS SHOULD BE MADE ONLY AFTER SEEKING APPROPRIATEFINANCIAL ADVICE. RELIANCE SHOULD NOT BE PLACED ON INFORMATION OR OPINIONS CONTAINED INTHIS PRESENTATION AND, SUBJECT ONLY TO ANY LEGAL OBLIGATION TO DO SO, BLUESCOPE STEELDOES NOT ACCEPT ANY OBLIGATION TO CORRECT OR UPDATE THEM. THIS PRESENTATION DOES NOTTAKE INTO CONSIDERATION THE INVESTMENT OBJECTIVES, FINANCIAL SITUATION OR PARTICULARNEEDS OF ANY PARTICULAR INVESTOR.

THIS PRESENTATION CONTAINS CERTAIN FORWARD-LOOKING STATEMENTS, WHICH CAN BE IDENTIFIEDBY THE USE OF FORWARD-LOOKING TERMINOLOGY SUCH AS “MAY”, “WILL”, “SHOULD”, “EXPECT”,“INTEND”, “ANTICIPATE”, “ESTIMATE”, “CONTINUE”, “ASSUME” OR “FORECAST” OR THE NEGATIVETHEREOF OR COMPARABLE TERMINOLOGY. THESE FORWARD-LOOKING STATEMENTS INVOLVE KNOWNAND UNKNOWN RISKS, UNCERTAINTIES AND OTHER FACTORS WHICH MAY CAUSE OUR ACTUALRESULTS, PERFORMANCE AND ACHIEVEMENTS, OR INDUSTRY RESULTS, TO BE MATERIALLY DIFFERENTFROM ANY FUTURE RESULTS, PERFORMANCES OR ACHIEVEMENTS, OR INDUSTRY RESULTS,EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS.

TO THE FULLEST EXTENT PERMITTED BY LAW, BLUESCOPE STEEL AND ITS AFFILIATES AND THEIRRESPECTIVE OFFICERS, DIRECTORS, EMPLOYEES AND AGENTS, ACCEPT NO RESPONSIBILITY FOR ANYINFORMATION PROVIDED IN THIS PRESENTATION, INCLUDING ANY FORWARD LOOKING INFORMATION,AND DISCLAIM ANY LIABILITY WHATSOEVER (INCLUDING FOR NEGLIGENCE) FOR ANY LOSSHOWSOEVER ARISING FROM ANY USE OF THIS PRESENTATION OR RELIANCE ON ANYTHING CONTAINEDIN OR OMITTED FROM IT OR OTHERWISE ARISING IN CONNECTION WITH THIS.

Page 3

Introduction

Page 4

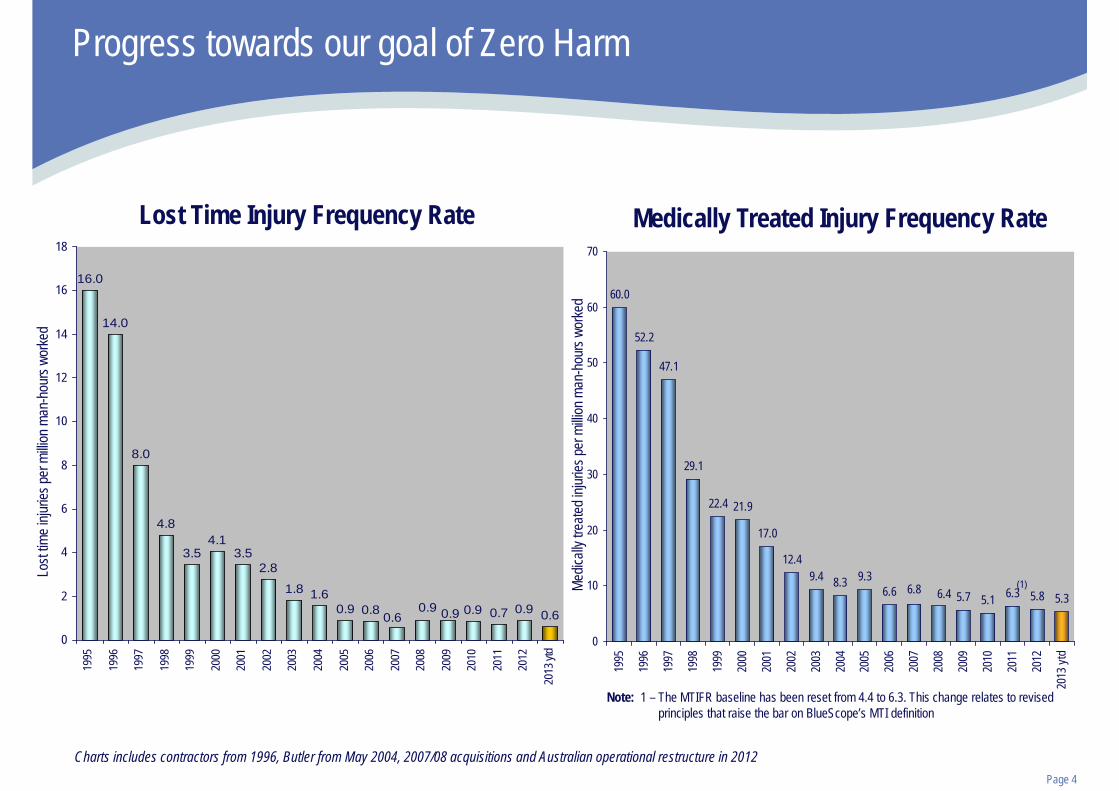

Progress towards our goal of Zero Harm

16.0

14.0

8.0

4.8

3.54.1

3.52.8

1.8 1.60.9 0.8 0.9 0.7 0.9 0.60.9

0.6 0.9

0

2

4

6

8

10

12

14

16

18

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

ytd

Lost

time i

njurie

s per

milli

on m

an-h

ours

worke

d

Medically Treated Injury Frequency RateLost Time Injury Frequency Rate

60.0

52.2

47.1

29.1

22.4 21.9

17.0

12.49.4 8.3 9.3

6.6 5.1 6.3 5.8 5.35.76.8 6.4

0

10

20

30

40

50

60

70

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

ytd

Medic

ally t

reate

d inju

ries p

er m

illion

man

-hou

rs wo

rked

Charts includes contractors from 1996, Butler from May 2004, 2007/08 acquisitions and Australian operational restructure in 2012

Note: 1 – The MTIFR baseline has been reset from 4.4 to 6.3. This change relates to revised principles that raise the bar on BlueScope’s MTI definition

(1)

Page 5

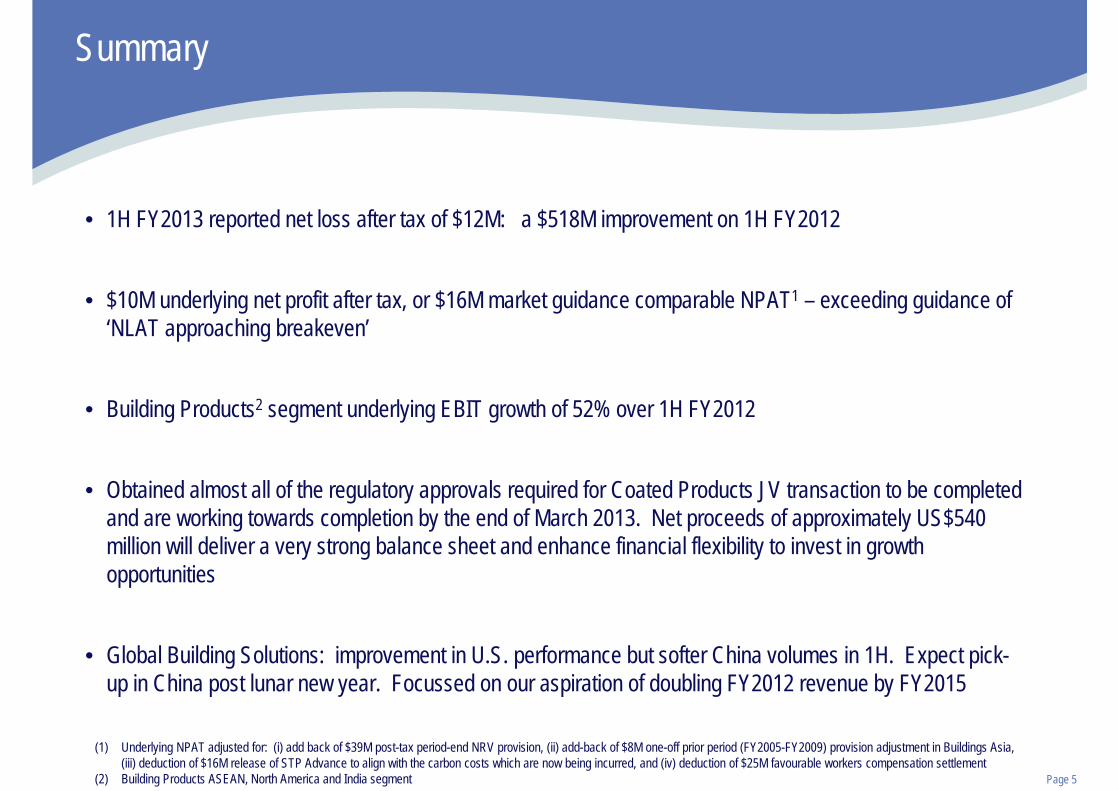

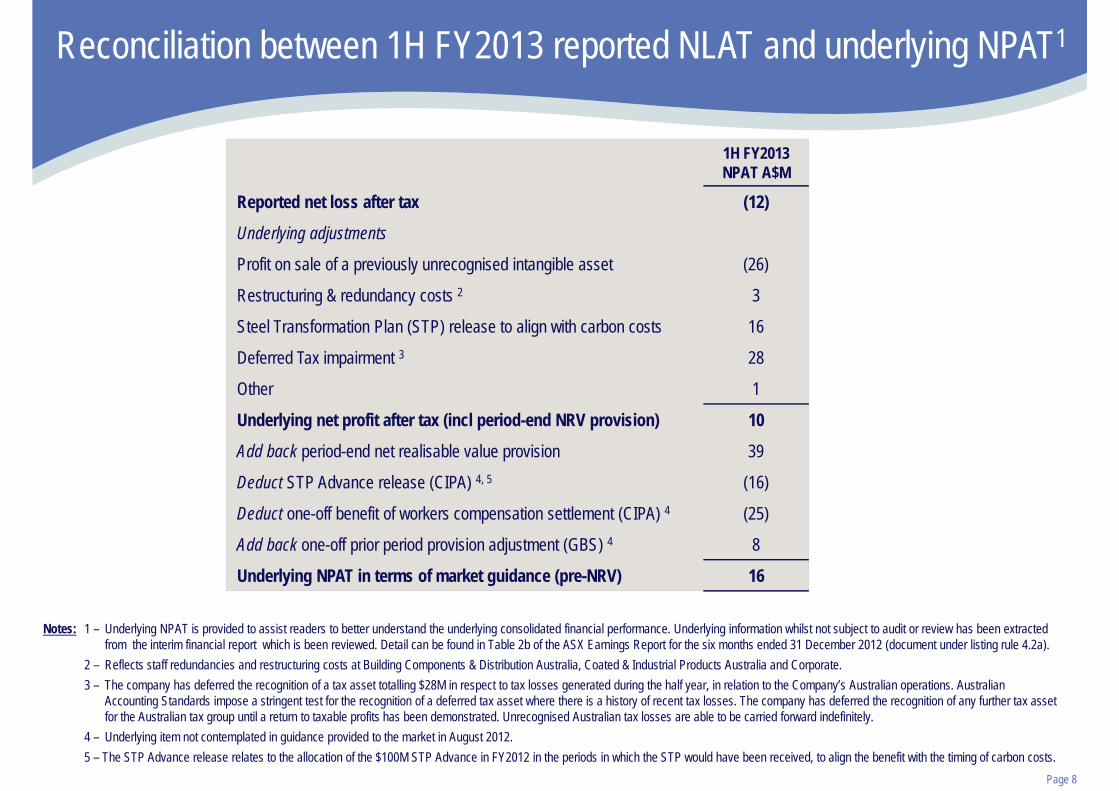

• 1H FY2013 reported net loss after tax of $12M: a $518M improvement on 1H FY2012

• $10M underlying net profit after tax, or $16M market guidance comparable NPAT1 – exceeding guidance of ‘NLAT approaching breakeven’

• Building Products2 segment underlying EBIT growth of 52% over 1H FY2012

• Obtained almost all of the regulatory approvals required for Coated Products JV transaction to be completed and are working towards completion by the end of March 2013. Net proceeds of approximately US$540 million will deliver a very strong balance sheet and enhance financial flexibility to invest in growth opportunities

• Global Building Solutions: improvement in U.S. performance but softer China volumes in 1H. Expect pick-up in China post lunar new year. Focussed on our aspiration of doubling FY2012 revenue by FY2015

Summary

(1) Underlying NPAT adjusted for: (i) add back of $39M post-tax period-end NRV provision, (ii) add-back of $8M one-off prior period (FY2005-FY2009) provision adjustment in Buildings Asia, (iii) deduction of $16M release of STP Advance to align with the carbon costs which are now being incurred, and (iv) deduction of $25M favourable workers compensation settlement

(2) Building Products ASEAN, North America and India segment

Page 6

• North Star 1H result 65% better on 1H FY2012. Continuing review of expansion opportunities

• CIPA underlying EBITDA improved to $79M profit1. Cost reduction performance strong; domestic HRC volumes softened. Expect positive underlying EBITDA in 2H FY2013 2

• Building Components & Distribution Australia delivered $2M underlying EBITDA, improved from $17M loss in 1H FY2012

• NZ Steel profit weaker on lower iron sands exports prices, lower steel prices and higher NZ$; however, significant improvement expected in 2H FY2013 and iron sands exports expansion to 2.7Mtpa on track for beginning of 2H FY2014

• Net debt of $499M at 31 Dec 2012; includes $132M benefit from sale of carbon units (equivalent amount of units to be purchased by 30 June 2013). Pro-forma net debt of $109M 3, assuming JV completion

Summary (ctd)

(1) CIPA is Coated and Industrial Products Australia segment. CIPA underlying EBITDA includes pre-tax benefits not contemplated in guidance: $23M release of STP Advance to align with the carbon costs which are now being incurred and $36M favourable one-off workers compensation settlement

(2) Subject to domestic demand and margins, spread and FX. Including benefit of partial release of $100M STP advance ($23M per half year, based on $183M over four years) – see footnote 5 on page 8(3) 31 December 2012 group net debt, pro-forma to reflect completion of Coated Products joint venture with Nippon Steel & Sumitomo Metal Corporation; see page 44 for further detail.

Pro-forma excludes $132M benefit from sale of carbon units, as an equivalent amount of units are expected to be purchased prior to 30 June 2013

Page 7

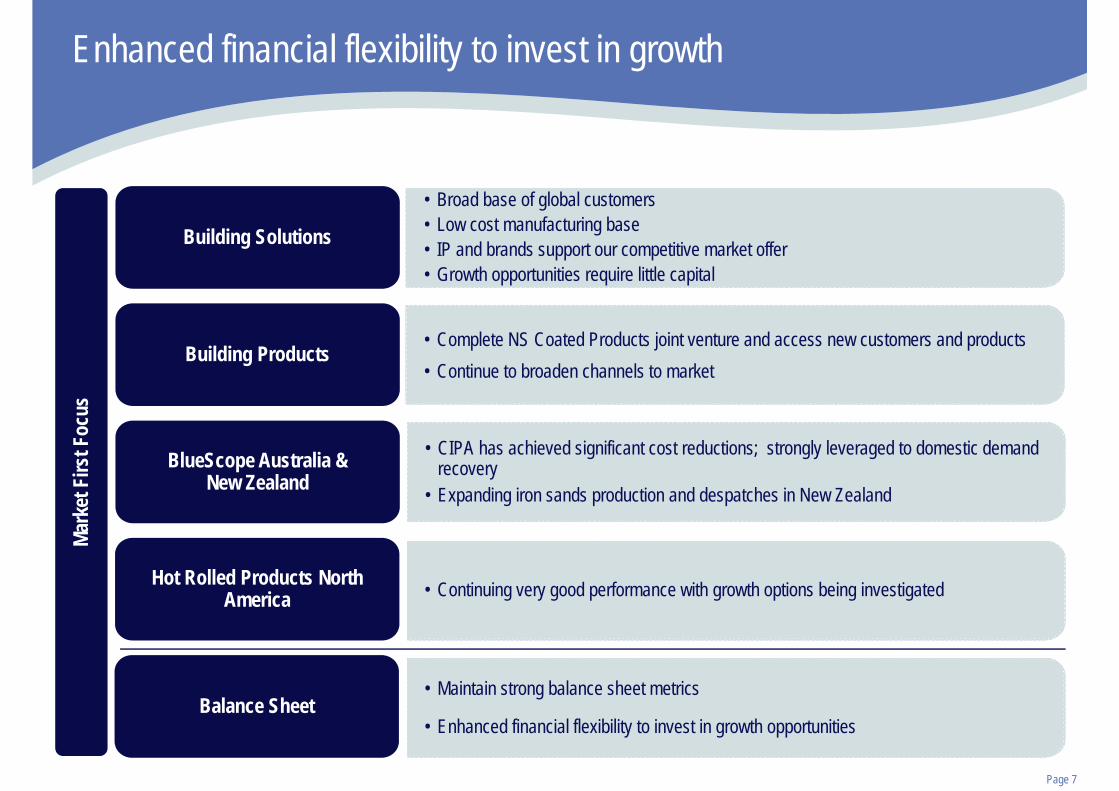

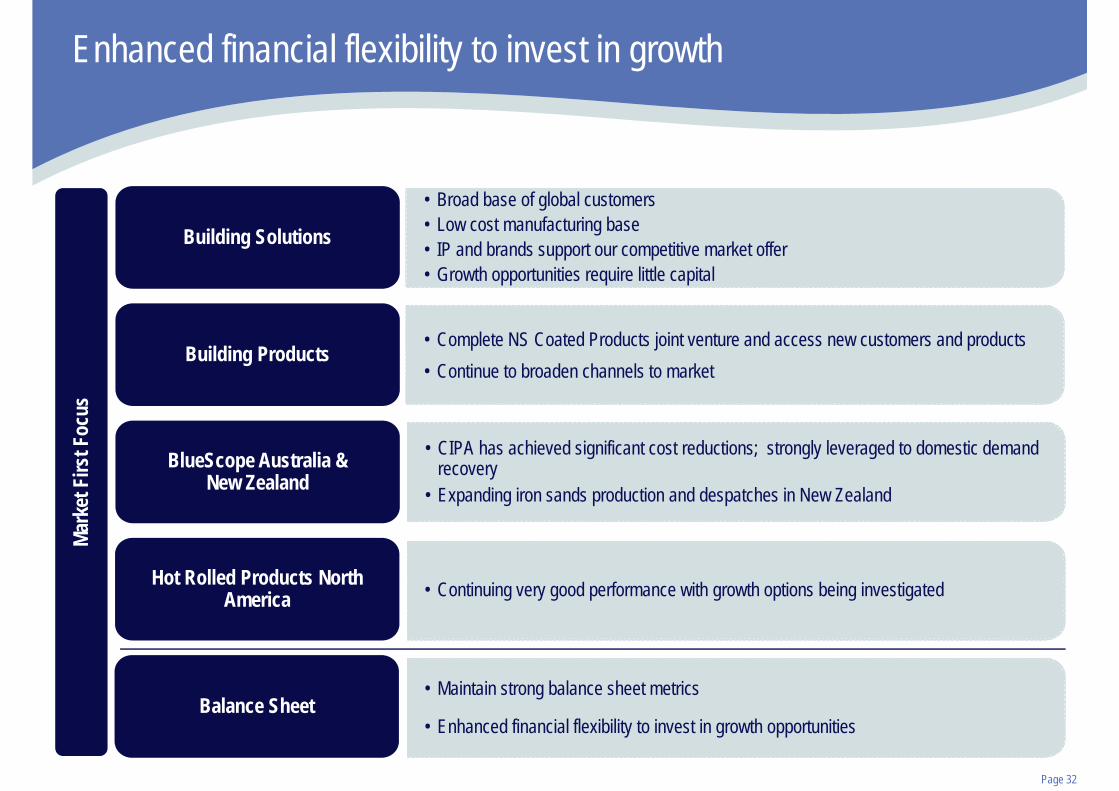

• Broad base of global customers• Low cost manufacturing base• IP and brands support our competitive market offer• Growth opportunities require little capital

Building Solutions

• Complete NS Coated Products joint venture and access new customers and products• Continue to broaden channels to market

Building Products

BlueScope Australia & New Zealand

Hot Rolled Products North America

Balance Sheet

Enhanced financial flexibility to invest in growthMa

rket

Firs

t Foc

us

• CIPA has achieved significant cost reductions; strongly leveraged to domestic demand recovery

• Expanding iron sands production and despatches in New Zealand

• Continuing very good performance with growth options being investigated

• Maintain strong balance sheet metrics

• Enhanced financial flexibility to invest in growth opportunities

Page 8

Reconciliation between 1H FY2013 reported NLAT and underlying NPAT1

1H FY2013NPAT A$M

Reported net loss after tax (12)

Underlying adjustments

Profit on sale of a previously unrecognised intangible asset (26)

Restructuring & redundancy costs 2 3

Steel Transformation Plan (STP) release to align with carbon costs 16

Deferred Tax impairment 3 28

Other 1

Underlying net profit after tax (incl period-end NRV provision) 10

Add back period-end net realisable value provision 39

Deduct STP Advance release (CIPA) 4, 5 (16)

Deduct one-off benefit of workers compensation settlement (CIPA) 4 (25)

Add back one-off prior period provision adjustment (GBS) 4 8

Underlying NPAT in terms of market guidance (pre-NRV) 16

Notes: 1 – Underlying NPAT is provided to assist readers to better understand the underlying consolidated financial performance. Underlying information whilst not subject to audit or review has been extracted from the interim financial report which is been reviewed. Detail can be found in Table 2b of the ASX Earnings Report for the six months ended 31 December 2012 (document under listing rule 4.2a).

2 – Reflects staff redundancies and restructuring costs at Building Components & Distribution Australia, Coated & Industrial Products Australia and Corporate.3 – The company has deferred the recognition of a tax asset totalling $28M in respect to tax losses generated during the half year, in relation to the Company’s Australian operations. Australian

Accounting Standards impose a stringent test for the recognition of a deferred tax asset where there is a history of recent tax losses. The company has deferred the recognition of any further tax asset for the Australian tax group until a return to taxable profits has been demonstrated. Unrecognised Australian tax losses are able to be carried forward indefinitely.

4 – Underlying item not contemplated in guidance provided to the market in August 2012. 5 – The STP Advance release relates to the allocation of the $100M STP Advance in FY2012 in the periods in which the STP would have been received, to align the benefit with the timing of carbon costs.

Page 9

Financial headlines 1H FY2013 vs. 1H FY2012

SIX MONTHS ENDED 1H FY2013 vs 1H FY2012

A$M (unless marked) 31 DEC 2011 31 DEC 2012 %Total revenue 4,539 3,704 Reduced 18%

External despatches 3,590Kt 2,831Kt Reduced 21%

EBITDA − Underlying 1 23 196 Improved

EBIT − Underlying 1 (137) 38 Improved

NPAT − Reported (530) (12) Improved

− Underlying 1 (136) 10 Improved

EPS − Reported (159.4) cps (2.2) cps Improved

− Underlying 1 (41.0) cps 1.8 cps Improved

Underlying EBIT Return on Invested Capital (5.1%) 1.8% Improved

Net Cashflow From Operating Activities (151) 44 Improved

- After capex / investments (256) (120) Improved

Dividend (fully franked) None None -

Net debt 796 499 Improved

Notes: 1 – Please refer to page 45 for a detailed reconciliation of reported to underlying results. Excludes Metl-Span operational earnings which have been re-categorised to discontinued operations.

Page 10

Segment Discussion

Page 11

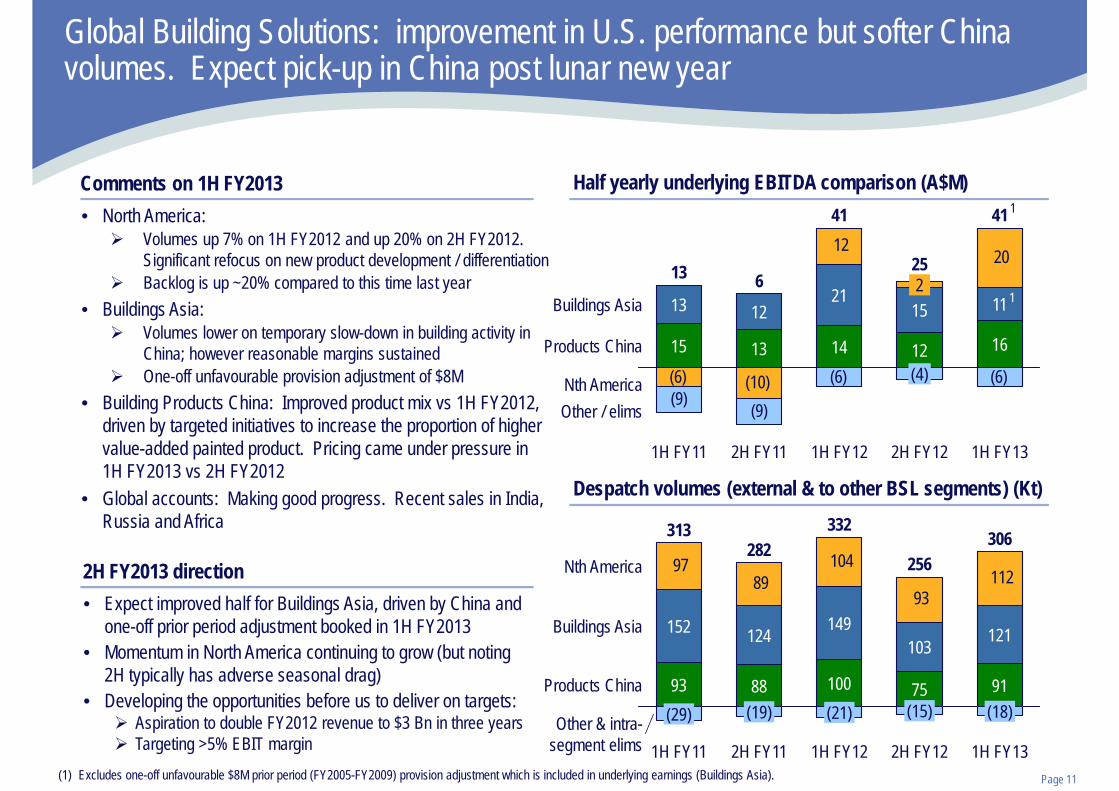

Global Building Solutions: improvement in U.S. performance but softer China volumes. Expect pick-up in China post lunar new year

Half yearly underlying EBITDA comparison (A$M) Comments on 1H FY2013• North America:

Volumes up 7% on 1H FY2012 and up 20% on 2H FY2012. Significant refocus on new product development / differentiationBacklog is up ~20% compared to this time last year

• Buildings Asia:Volumes lower on temporary slow-down in building activity in China; however reasonable margins sustainedOne-off unfavourable provision adjustment of $8M

• Building Products China: Improved product mix vs 1H FY2012, driven by targeted initiatives to increase the proportion of higher value-added painted product. Pricing came under pressure in 1H FY2013 vs 2H FY2012

• Global accounts: Making good progress. Recent sales in India, Russia and Africa

2H FY2013 direction• Expect improved half for Buildings Asia, driven by China and

one-off prior period adjustment booked in 1H FY2013• Momentum in North America continuing to grow (but noting

2H typically has adverse seasonal drag)• Developing the opportunities before us to deliver on targets:

Aspiration to double FY2012 revenue to $3 Bn in three yearsTargeting >5% EBIT margin

Despatch volumes (external & to other BSL segments) (Kt)

(6)(6)(10)(6)

(9)(9)

20 12

Other / elims

Products China

Buildings Asia

Nth America

1H FY13

41

16

11

2H FY12

25

(4)12

152

1H FY12

41

14

21

2H FY11

6

13

12

1H FY11

13

15

13

97 89

104

93 112

121

Other & intra-segment elims

Products China

Buildings Asia

Nth America

1H FY13

306

(18)91

2H FY12

256

(15)75

103

1H FY12

332

(21)100

149

2H FY11

282

(19)88

124

1H FY11

313

(29)93

152

(1) Excludes one-off unfavourable $8M prior period (FY2005-FY2009) provision adjustment which is included in underlying earnings (Buildings Asia).

1

1

Page 12

Building Products ASEAN, North America and India: underlying EBITDA growth of 25% in 1H FY2013 vs 1H FY2012

Half yearly underlying EBITDA comparison (A$M) Comments on 1H FY2013

• Thailand: Strong performance despite competitive environment. Recovery from floods in 1H FY2012, and successful roll-out of sales-focussed initiatives

• Indonesia: Improving sales channels• Malaysia: Lower volumes due to lower market activity in

advance of the election• Vietnam: Ongoing focus on sales initiatives saw

continued improvement in performance• North America: Making good headway on cost reduction

program• India: Improved on 2H, but still need to further ramp-up

volumes to improve performance

2H FY2013 direction

• Continued improvement in base business expected (esp in Indonesian and North America), with risks around imports and tariff/dumping regimes, especially in Thailand and Indonesia

• Commence Coated Products joint venture and develop opportunities

Despatch volumes (external & to other BSL segments) (Kt)

7

8

12

22

17

23 27

(8)(10)(2)(3)

(2)

7

OtherIndia

Nth AmericaVietnam

MalaysiaIndonesiaThailand

1H FY13

55

(2)

8

14

2H FY12

54

4

18

815

1H FY12

44

(2) (5)7

6156

2H FY11

80

(3)

21

20

15

1H FY11

47

(3) 6615

13

657 649 607 592 529

1H FY11 2H FY11 1H FY12 2H FY12 1H FY13

Page 13

• Obtained almost all of the regulatory approvals required for Coated Products JV transaction to be completed and are working towards completion by the end of March 2013. Net proceeds of approximately US$540 million will deliver a very strong balance sheet and enhance financial flexibility to invest in growth opportunities

• Joint feasibility study with NSSMC on manufacturing of products for home appliance market is well progressed Production of SuperDyma® coated steel for home appliances focussed on MCL2 in Maptaphut, ThailandAlso considering launch of a SuperDyma® branded product for the building & construction marketCommercial production of SuperDyma® for both home appliance and building & construction markets are planned for FY2015

• Received enquiries from potential Japanese customers and JV is being considered as a supplier to a number of key Japanese contractors in the region

Coated Products JV with Nippon Steel & Sumitomo Metal Corporation (NSSMC) –working towards completion by end of March 2013. Accelerating work on value opportunities

Page 14

Coated & Industrial Products Australia: underlying EBITDA improved to $79M profit; cost reduction performance strong; domestic HRC volumes softened. Expect positive underlying EBITDA for 2H FY20131

Half yearly underlying EBITDA comparison (A$M) Comments on 1H FY2013 79

(57)

(94)

(59)

3

1H FY132H FY121H FY122H FY111H FY11

• $79M underlying EBITDA, or $43M excluding one-off workers compensation settlement. $20M on earnings guidance comparable basis2 (exceeded guidance of neutral to negative EBITDA)

• Spread improved and cost reduction performance very strong• Domestic volumes weaker due to softer HRC sales (weak

conditions in the pipe & tube market) vs 2H FY2012. HRC, plate and galvanised volumes weaker vs 1H FY2012

• Domestic pricing environment weak – strong import competition• Anti-dumping: some success on HRC with duties imposed and

preliminary duties announced on metal coated products; anticipate findings on metal coated countervailing review by mid-March, and plate by early May

2H FY2013 direction• Launching Next Generation ZINCALUME® and COLORBOND®• Key end-user segment activity levels fairly steady; potential for

modest improvement in volumes• Expect positive underlying EBITDA in 2H FY20131

• Restructuring cash payments $30M in 1H FY2013; expect $41M in 2H FY2013 (including Western Port reconfiguration)

• 2H FY2013 capex of $90M expected ($140M for FY2013), of which, one third for growth projects

Includes pre-tax benefits: • $23M release of

STP Advance• $36M favourable

workers compensation settlement

Total despatches (external & to other BSL segments, Mt)

1.38 1.421.11

0.44 0.35

1.43

0.99

2H FY12

1.25

0.90

1H FY12

2.38

0.99

2H FY111H FY11 1H FY13

1.001.03

2.112.45

Export Domestic

(1) Subject to domestic demand and margins, spread and FX. Including benefit of partial release of $100M STP Advance ($23M per half year, based on $183M over four years) – see footnote 5 on page 8(2) Excludes partial release of Steel Transformation Plan Advance to align with carbon costs which are now being incurred ($23M) and one-off favourable workers compensation settlement ($36M)

Page 15

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Auto & transportAgri & miningManufacturingEngineeringDwelling

Non-dwelling

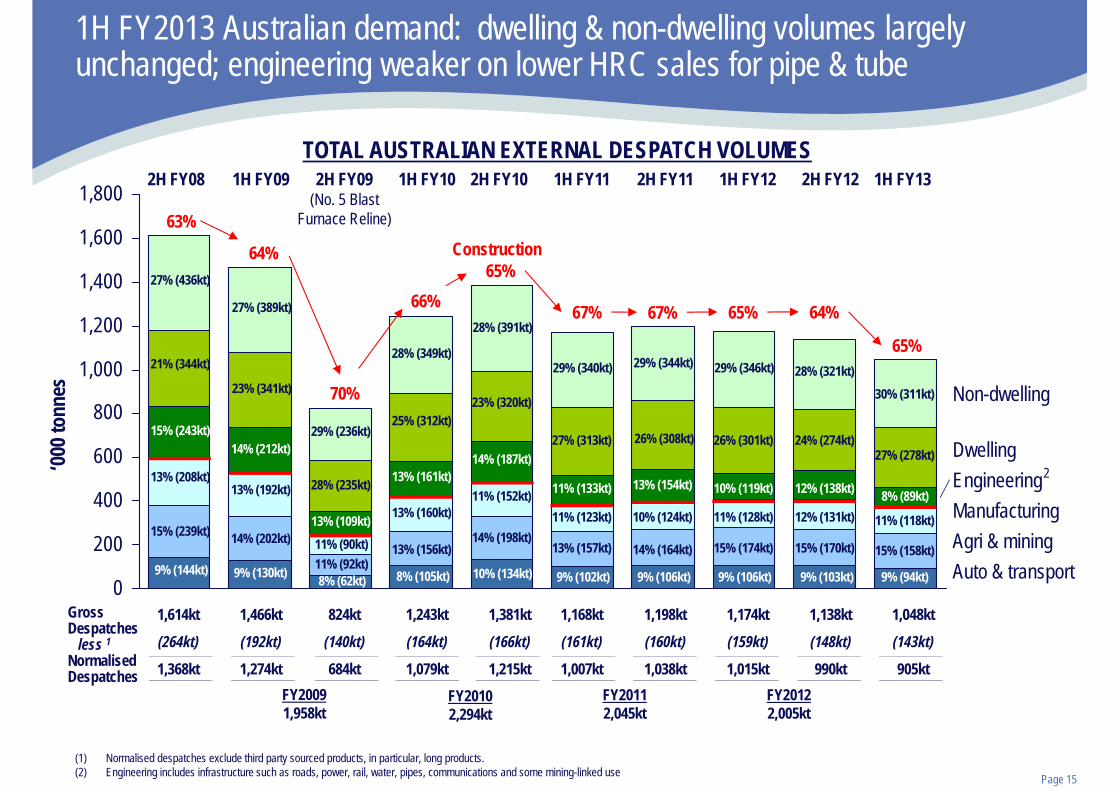

1H FY2013 Australian demand: dwelling & non-dwelling volumes largely unchanged; engineering weaker on lower HRC sales for pipe & tube

(1) Normalised despatches exclude third party sourced products, in particular, long products.(2) Engineering includes infrastructure such as roads, power, rail, water, pipes, communications and some mining-linked use

‘000 t

onne

s

2H FY08 1H FY09 2H FY09 1H FY10 2H FY10 1H FY11 2H FY11 1H FY12 2H FY12 1H FY13(No. 5 Blast

Furnace Reline)

TOTAL AUSTRALIAN EXTERNAL DESPATCH VOLUMES

63%

13% (208kt)

15% (239kt)

9% (144kt)

14% (212kt)

13% (192kt)

14% (202kt)

9% (130kt)

29% (236kt)

28% (235kt)

13% (109kt)11% (90kt)11% (92kt)8% (62kt)

13% (161kt)

13% (160kt)

13% (156kt)

8% (105kt)

14% (187kt)

11% (152kt)

14% (198kt)

10% (134kt)

Construction65%

66%

70%

64%27% (436kt)

21% (344kt)

15% (243kt)

27% (389kt)

23% (341kt)

28% (349kt)

25% (312kt)

28% (391kt)

23% (320kt)

211% (133kt)

11% (123kt)

13% (157kt)

9% (102kt)

67%

29% (340kt)

27% (313kt)

13% (154kt)

10% (124kt)

14% (164kt)

9% (106kt)

67%

29% (344kt)

26% (308kt)

65% 64%

10% (119kt)

11% (128kt)

15% (174kt)

9% (106kt)

29% (346kt)

26% (301kt)

1,614kt 1,466kt 824kt 1,243kt 1,381kt 1,168kt 1,198kt 1,174kt 1,138kt 1,048kt(264kt) (192kt) (140kt) (164kt) (166kt) (161kt) (160kt) (159kt) (148kt) (143kt)

1,368kt 1,274kt 684kt 1,079kt 1,215kt 1,007kt 1,038kt 1,015kt 990kt 905ktFY20091,958kt

FY20112,045kt

FY20102,294kt

FY20122,005kt

GrossDespatches

less 1NormalisedDespatches

12% (138kt)

12% (131kt)

15% (170kt)

9% (103kt)

28% (321kt)

24% (274kt)

65%

8% (89kt)

11% (118kt)

15% (158kt)

9% (94kt)

30% (311kt)

27% (278kt)

Page 16

Australian residential construction starts (total new houses) slowly improving from near lowest point of last three decades

Quarterly number of Australian residential construction starts (total new houses) to September 2012 1

Source: Australian Bureau of Statistics. Series ID: 8752.0 Building Activity, Australia. Table 33: Number of Dwelling Unit Commencements by Sector, Australia.

(1) Based on total number of dwelling units – total houses, on seasonally adjusted basis. Excludes multi-dwelling commencementsHouse definition: A detached building primarily used for long term residential purposes consisting of one dwelling unit. Includes detached residences associated with a non-residential building, and kit and transportable homesDwelling: A dwelling unit is a self-contained suite of rooms, including cooking and bathing facilities and intended for long-term residential use. Units (whether self-contained or not) within buildings offering institutional care, such as hospitals, or temporary accommodation such as motels, hostels and holiday apartments, are not defined as dwelling units. The value of units of this type is included in non-residential building.

(Number per quarter)

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Jun-

85

Jun-

86

Jun-

87

Jun-

88

Jun-

89

Jun-

90

Jun-

91

Jun-

92

Jun-

93

Jun-

94

Jun-

95

Jun-

96

Jun-

97

Jun-

98

Jun-

99

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12

Page 17Source: ABS, BIS Shrapnel, HIA. Charts show change in value of work done / forecast

Residential ConstructionAnnual % Change(Fin Yrs)

-3.4-2.1

7.6

3.5

9.18.4

12.8

-0.5

-2.8

-5

0

5

10

15

201420132012201120102009200820072006

Non Residential ConstructionAnnual % Change(Fin Yrs)

Engineering ConstructionAnnual % Change(Fin Yrs)

2.9

19.1

9.68.5

25.8

33.8

-505

10152025303540

2014

-2.9

2013

9.7

2012201120102009200820072006

External forecasters’ outlook for our key construction exposures

-5.2

1.2

3.2

-1.5

1.31.2

-3.4

3.6

-6.0

-4.5

-3.0

-1.5

0.0

1.5

3.0

4.5

6.0

20142013

-0.7

2012201120102009200820072006

7 Yr AverageHIA F’casts (Jan 13)

7 Yr AverageBIS Shrapnel F’casts (Nov 12)

7 Yr AverageBIS Shrapnel F’casts (Oct 12)

Page 18

• Production of next generation ZINCALUME® steel with Activate™ technology commences in 2H FY2013 following development and testing over a number of years, and recently completed modifications to Springhill production facilities

The introduction of magnesium into the aluminium-zinc alloy coating achieves a step change in corrosion resistance. Outcome: Improved performance with less total coating mass (125 g/m2 vs 150g/m2 for superseded ZINCALUME® steel)

• Customers will benefit from:Improved product lifespan and longer warranties

– Galvanic ‘healing’ mechanism improves protection of cut edges and scratches – Better protection of rain-free/unwashed surfaces exposed to air pollution

Reduced environmental footprint compared with previous generation ZINCALUME® steel in all LCA environmental impact categories for roofing applications due to reduced coating metals and increased lifespan

• BlueScope will benefit from:Sales into new areas and applications including perforated construction productsAn ‘exclusive’ offering of leading technology for roofing, walling and rainwater applicationsProtected by 21 product and manufacturing patents held between BSL and co-developer, NSSMC

• Market familiarisation program – very positive response from construction industry professionalsLow risk implementation: a better performing product, longer warranty, readily available with no change to fixing techniques will be and fully compliant with relevant Australian Standards for roofing and walling, and Building Code of Australia (BCA) requirements

• Next generation ZINCALUME® steel with Activate™ technology will become the substrate of next generation of COLORBOND® steel products which will be released late 2013

Launching next generation ZINCALUME® – reinforcing status as market leader

Page 19

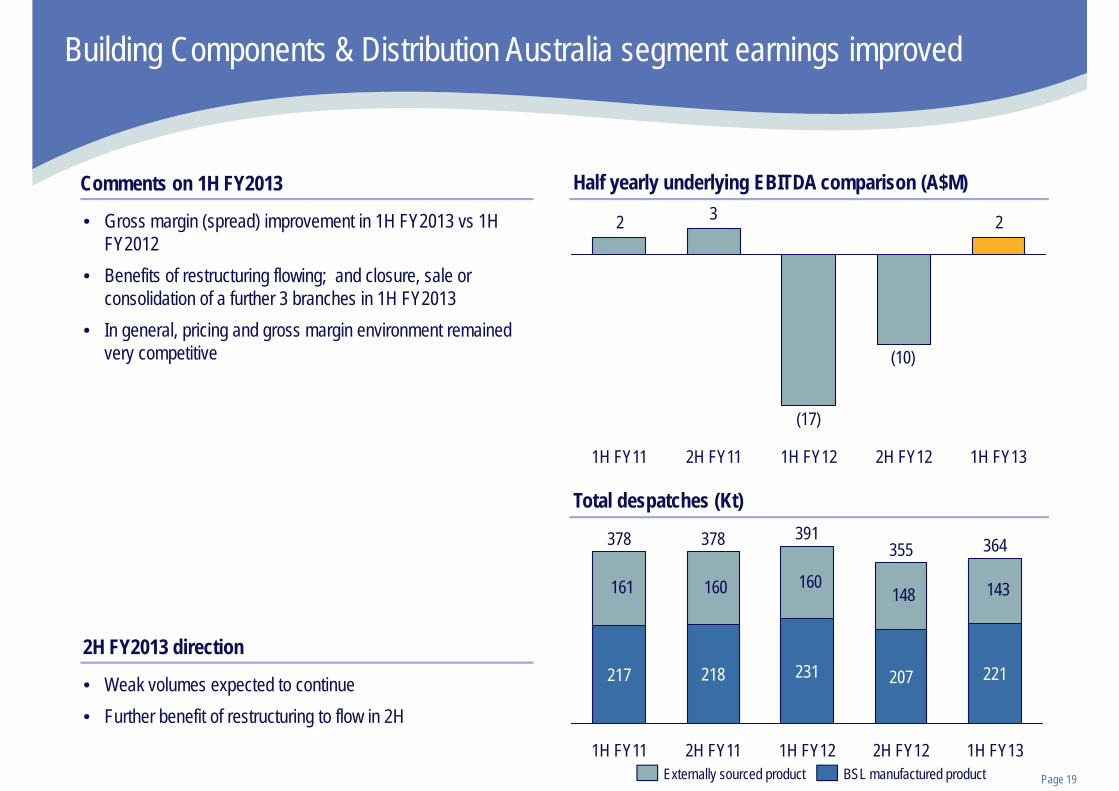

Building Components & Distribution Australia segment earnings improved

Comments on 1H FY2013

• Gross margin (spread) improvement in 1H FY2013 vs 1H FY2012

• Benefits of restructuring flowing; and closure, sale or consolidation of a further 3 branches in 1H FY2013

• In general, pricing and gross margin environment remained very competitive

2H FY2013 direction

• Weak volumes expected to continue• Further benefit of restructuring to flow in 2H

Half yearly underlying EBITDA comparison (A$M)

2

(10)

(17)

3 2

1H FY132H FY122H FY11 1H FY121H FY11

Total despatches (Kt)

? 161 160 160 148 143

1H FY11

217 218

378

2H FY12

355

207

1H FY12

391

231

2H FY11

378

221

364

1H FY13BSL manufactured productExternally sourced product

Page 20

New Zealand and Pacific Steel Products: profit lower on weaker iron sands export prices, lower steel prices and higher NZ$; however significant improvement expected in 2H FY2013 and iron sands expansion to 2.7Mtpa run-rate on track for Jan 2014

Comments on 1H FY2013• Lower iron sand prices given fall in iron ore prices in 1H• Benefit of higher iron sands volumes (up 78% on

1H FY2012)• Lower steel prices due to soft regional steel prices and

exchange rate• Steel export sales volumes slightly weaker due to

bi-annual hot strip mill shut• Higher conversion and maintenance costs due to several

scheduled plant shuts• Lower scrap and vanadium credits

2H FY2013 direction• Iron ore prices started the half stronger – positive for iron

sands pricing• Iron sands expansion to 2.7Mtpa run-rate on track for

beginning of CY2014: customer making good progress on vessel commissioning

• Market for steel is starting to improve with residential construction consent levels increasing from a year ago, albeit off a low base

• Expect significant improvement in earnings in 2H (stronger iron sands prices and lower conversion costs)

Half yearly underlying EBITDA comparison (A$M)

27

58 55 55

67

1H FY132H FY121H FY122H FY111H FY11

Steel despatches (Kt)

164 169 136

1H FY13

261

125

2H FY12

294

125

1H FY12

286

122

DomesticExport

Iron sands despatches (Kt)

831 674

466

2H FY14

1,350

1H FY132H FY121H FY12

Targ

et

Page 21

Monthly number of New Zealand residential construction approvals to November 20121

(Number per month)

Source: Statistics New Zealand. Series ID: SSC11AS.

(1) Based on total number of new dwellings consented on an unadjusted basis. Data includes apartments. Figures for new apartments are compiled from consents that have 10 or more attached new dwellings. Consent definition: A building consent is the formal approval issued by a Building Consent Authority (BCA) to ensure certain works meet the requirements of the Building Act 2004, Building Regulations and New Zealand Building Code

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Feb-

03

Aug-

03

Feb-

04

Aug-

04

Feb-

05

Aug-

05

Feb-

06

Aug-

06

Feb-

07

Aug-

07

Feb-

08

Aug-

08

Feb-

09

Aug-

09

Feb-

10

Aug-

10

Feb-

11

Aug-

11

Feb-

12

Aug-

12

New Zealand residential construction approvals trending higher

Page 22

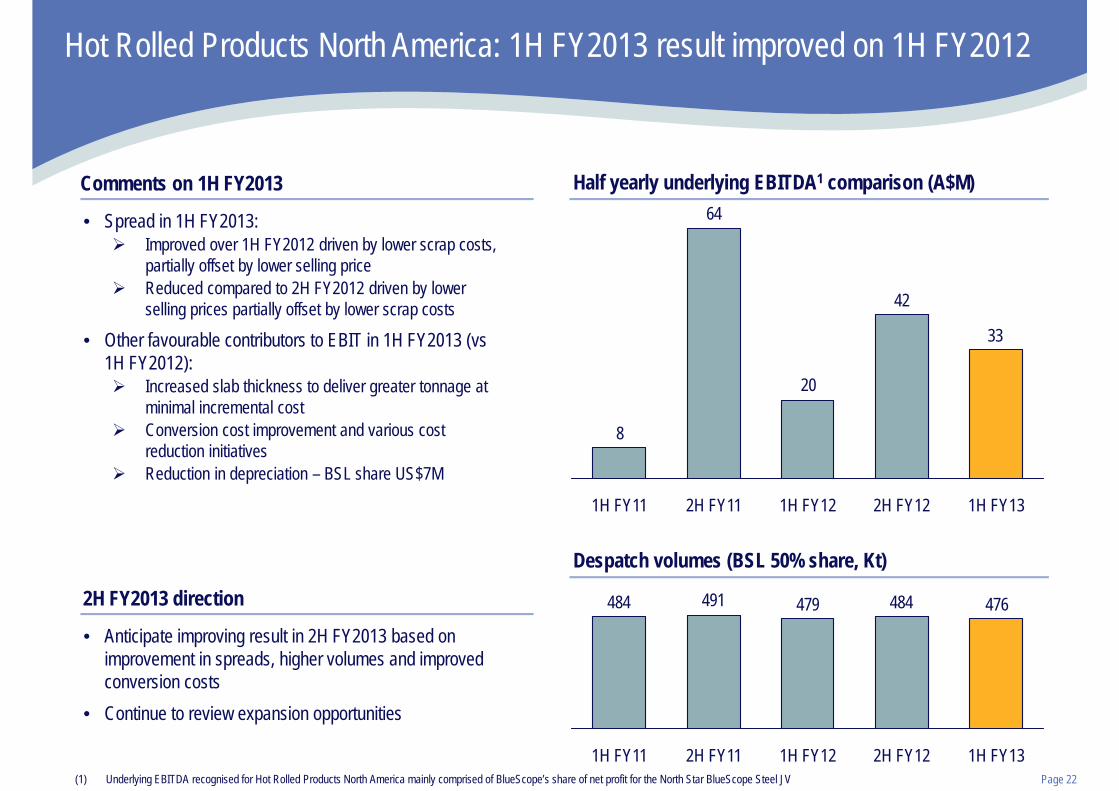

Hot Rolled Products North America: 1H FY2013 result improved on 1H FY2012

Half yearly underlying EBITDA1 comparison (A$M) Comments on 1H FY2013

33

42

20

64

8

1H FY12 1H FY132H FY121H FY11 2H FY11

• Spread in 1H FY2013:Improved over 1H FY2012 driven by lower scrap costs, partially offset by lower selling priceReduced compared to 2H FY2012 driven by lower selling prices partially offset by lower scrap costs

• Other favourable contributors to EBIT in 1H FY2013 (vs 1H FY2012):

Increased slab thickness to deliver greater tonnage at minimal incremental costConversion cost improvement and various cost reduction initiativesReduction in depreciation – BSL share US$7M

2H FY2013 direction

• Anticipate improving result in 2H FY2013 based on improvement in spreads, higher volumes and improved conversion costs

• Continue to review expansion opportunities

Despatch volumes (BSL 50% share, Kt)

476 484 479 491 484

1H FY121H FY11 2H FY122H FY11 1H FY13(1) Underlying EBITDA recognised for Hot Rolled Products North America mainly comprised of BlueScope’s share of net profit for the North Star BlueScope Steel JV

Page 23

Financials

Page 24

Cash flow – solid core earnings improvement

A$M 1H FY12 2H FY12 1H FY13Reported EBITDA (270) (219) 204Adjust for other cash profit items 5 322 (32)

Cash from operations (265) 103 172Working capital movement (inc provisions) 235 382 (16)

Gross operating cash flow (30) 485 156Financing costs (66) (43) (36)Interest received 1 2 2

(Payment) / refund of income tax1 (56) (25) (78)Net operating cash flow (151) 419 44Capex: payments for P, P & E and intangibles (110) (120) (129)Other investing cash flow 5 145 (35)

Net cash flow before financing (256) 444 (120)Equity issues 577 (1) -

Dividends (1) (4) (2)Net drawing / (repayment) of borrowings (309) (410) 103

Net increase/(decrease) in cash held 11 29 (19)

(1) The BlueScope Steel Australian tax consolidated group is estimated to have carried forward tax losses, as at 31 December 2012, in excess of $2.2Bn. There will be no Australian income tax payments until these losses are recovered.

Working capital movement includes $132M benefit from sale of carbon units (equivalent amount of units to be purchased by 30 June 2013) and $28M of CIPA

cash restructuring payments

Predominantly purchase cost of ASEAN minorities, partly offset by proceeds of sale of previously

unrecognised intangible asset

Cash capex of $129M (of which $102M of new capital commitments in 1H FY2013 and $27M of payment of

existing commitments)

Predominantly due to classification of proceeds of sale of previously unrecognised intangible asset as an

investing cash flow (see ‘Other investing cash flow’ below) – reversed from operating cash flow

Includes ~$35M tax paid following Metl-Span sale

Page 25

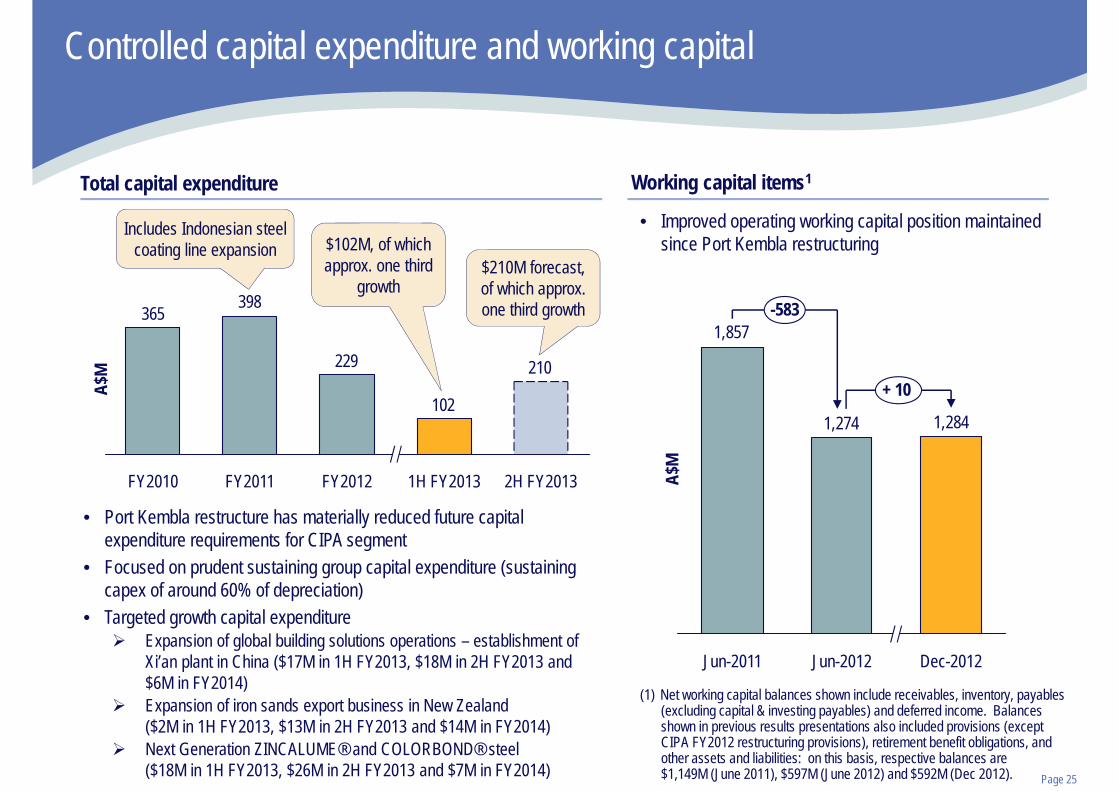

Controlled capital expenditure and working capital

Total capital expenditure

• Port Kembla restructure has materially reduced future capital expenditure requirements for CIPA segment

• Focused on prudent sustaining group capital expenditure (sustaining capex of around 60% of depreciation)

• Targeted growth capital expenditureExpansion of global building solutions operations – establishment of Xi’an plant in China ($17M in 1H FY2013, $18M in 2H FY2013 and $6M in FY2014)Expansion of iron sands export business in New Zealand($2M in 1H FY2013, $13M in 2H FY2013 and $14M in FY2014)Next Generation ZINCALUME® and COLORBOND® steel ($18M in 1H FY2013, $26M in 2H FY2013 and $7M in FY2014)

Working capital items1

210

102

229

398 365

FY2012 2H FY20131H FY2013FY2011FY2010

$210M forecast, of which approx. one third growth

Includes Indonesian steel coating line expansion $102M, of which

approx. one thirdgrowth

• Improved operating working capital position maintained since Port Kembla restructuring

A$M

1,284 1,274

1,857

+ 10

-583

Dec-2012Jun-2012Jun-2011A$

M(1) Net working capital balances shown include receivables, inventory, payables

(excluding capital & investing payables) and deferred income. Balances shown in previous results presentations also included provisions (except CIPA FY2012 restructuring provisions), retirement benefit obligations, and other assets and liabilities: on this basis, respective balances are$1,149M (June 2011), $597M (June 2012) and $592M (Dec 2012).

Page 26

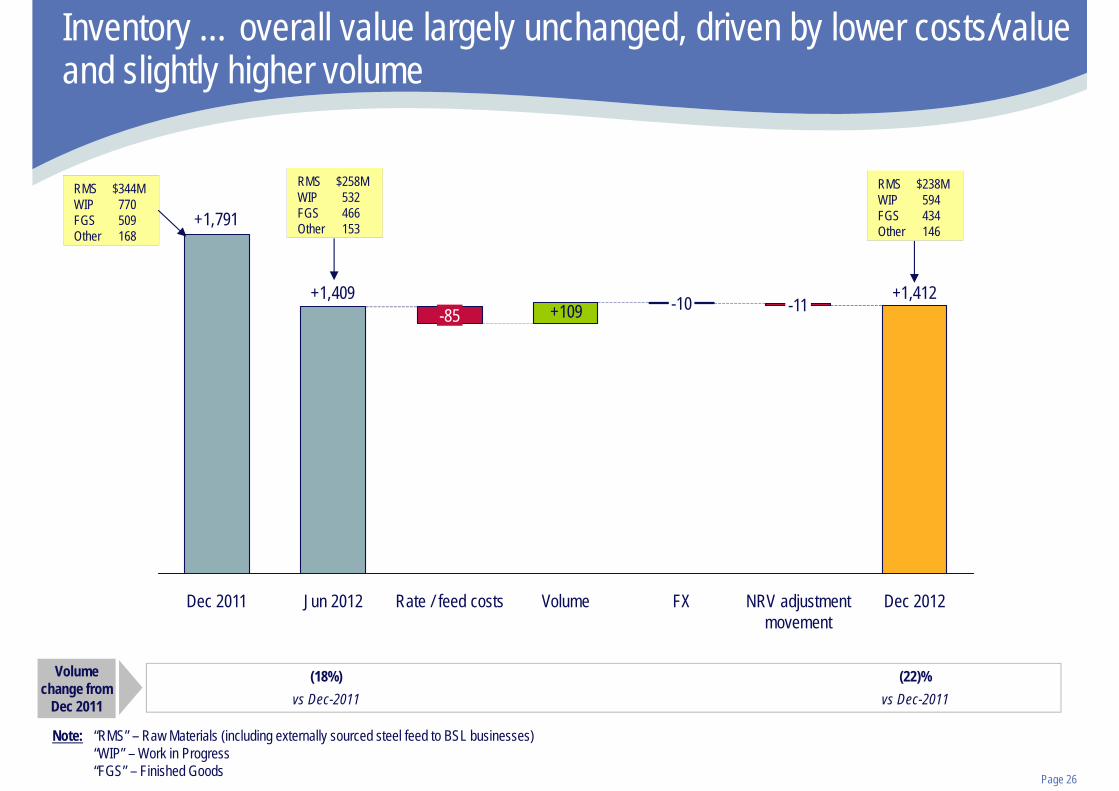

Inventory … overall value largely unchanged, driven by lower costs/value and slightly higher volume

Volume change from

Dec 2011

+109+1,409

+1,791

Dec 2012

+1,412

NRV adjustment movement

-11

FX

-10

VolumeRate / feed costs

-85

Jun 2012Dec 2011

Note: “RMS” – Raw Materials (including externally sourced steel feed to BSL businesses)“WIP” – Work in Progress“FGS” – Finished Goods

RMS $258MWIP 532FGS 466Other 153

(18%)vs Dec-2011

RMS $344MWIP 770FGS 509Other 168

(22)%vs Dec-2011

RMS $238MWIP 594FGS 434Other 146

Page 27

Strengthened balance sheet supports our strategy

• Completion of Coated Products JV transaction will deliver a further strengthened balance sheet

Net debt ($M) Net debt / EBITDA1 Gearing (ND/ND+E)

109

499 384

1,068

743

Pro-forma1H FY2013FY2012FY2011FY2010

Significant debt reduction largely driven by:• $600m equity raising• Working capital release from CIPA

restructureAlso benefited from favourable timing of year end cash flows of ~$200m (expected to unwind in FY2013)

Pro-forma at Dec 2012, as though Coated Products JV completed on 31 Dec 2012 and excludes $132M benefit from sale of carbon units

1,349 1,571

1,137

1,620

1H FY2013FY2012FY2011FY2010

Liquidity (undrawn facilities and cash, $M)

1H FY2013 annualised

1.3x

1H FY2013

11.8%

FY2012

9.2%

FY2011

19.5%Includes $132M benefit from sale of carbon units; equivalent amount of units to be purchased by 30 June 2013

(1) 31 Dec 2012 net debt to annualised 1H FY2013 underlying EBITDA

Page 28

Debt facilities maturity profile at 31 December 2012

Note: assumes AUD/USD at 1.0374

Current estimated cost of facilities:

Approximately 6% interest cost on gross drawn debt; plus

commitment fee on undrawn part of Syndicated Bank Facility of 1.1%; plus

other costs of $6m pa;

less: interest on cash.

97911 30571

675

2H FY16+

1H FY16

2H FY15

1H FY15

2H FY14

1H FY14

754

675

2H FY13

1H FY13

OtherUS Private Placement NotesSyndicated Bank Facility

In re-sizing our finance facilities and to reduce costs, upon completion of the Coated Products JV the A$675M December 2013 Syndicated Bank Facility tranche commitment will be reduced by A$450M to A$225M

Receivables securitisation program:

In addition to debt facilities, BSL has a receivables securitisation program

$150M maturing September 2014

$350M drawn of $675M committed

Nil drawn of $675M committed

Page 29

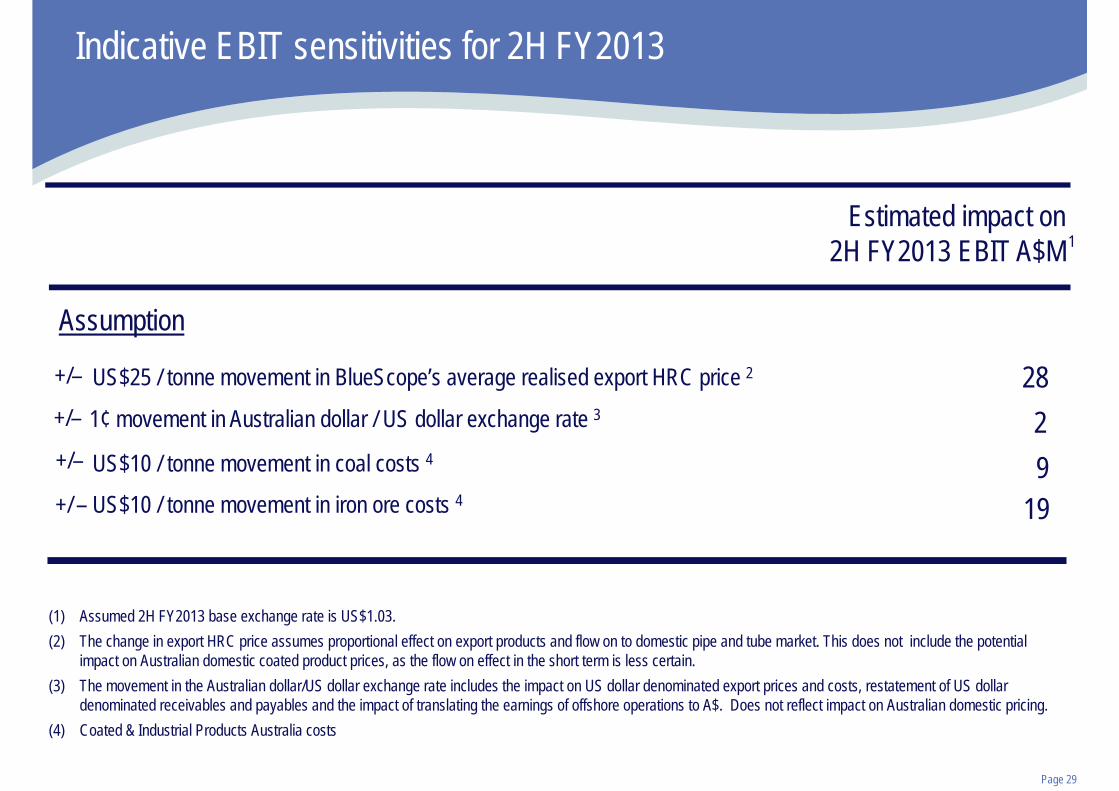

Indicative EBIT sensitivities for 2H FY2013

Estimated impact on2H FY2013 EBIT A$M

Assumption

+/– US$25 / tonne movement in BlueScope’s average realised export HRC price 2

1¢ movement in Australian dollar / US dollar exchange rate 3

US$10 / tonne movement in coal costs 4

+/ – US$10 / tonne movement in iron ore costs 4

+/–

+/–

2829

19

1

(1) Assumed 2H FY2013 base exchange rate is US$1.03.(2) The change in export HRC price assumes proportional effect on export products and flow on to domestic pipe and tube market. This does not include the potential

impact on Australian domestic coated product prices, as the flow on effect in the short term is less certain. (3) The movement in the Australian dollar/US dollar exchange rate includes the impact on US dollar denominated export prices and costs, restatement of US dollar

denominated receivables and payables and the impact of translating the earnings of offshore operations to A$. Does not reflect impact on Australian domestic pricing.(4) Coated & Industrial Products Australia costs

Page 30

Outlook & Summary

Page 31

2H FY2013 outlook

• In 2H FY2013, we expect a continued improvement in financial performance with a small net profit after tax (before period-end net realisable value adjustments, and subject to domestic demand and margins, spread and FX)

Page 32

• Broad base of global customers• Low cost manufacturing base• IP and brands support our competitive market offer• Growth opportunities require little capital

Building Solutions

• Complete NS Coated Products joint venture and access new customers and products• Continue to broaden channels to market

Building Products

BlueScope Australia & New Zealand

Hot Rolled Products North America

Balance Sheet

Enhanced financial flexibility to invest in growthMa

rket

Firs

t Foc

us

• CIPA has achieved significant cost reductions; strongly leveraged to domestic demand recovery

• Expanding iron sands production and despatches in New Zealand

• Continuing very good performance with growth options being investigated

• Maintain strong balance sheet metrics

• Enhanced financial flexibility to invest in growth opportunities

Page 33

Questions & Answers

Page 34

Additional Information

Page 35

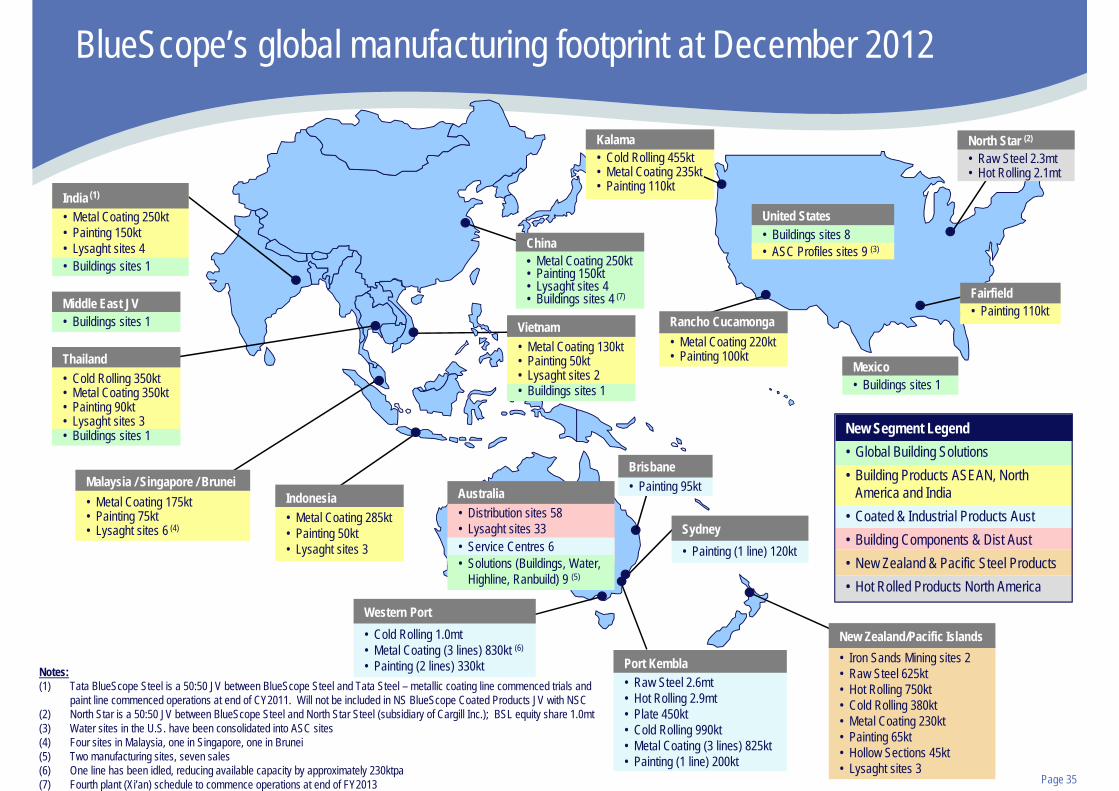

BlueScope’s global manufacturing footprint at December 2012

• Cold Rolling 1.0mt• Metal Coating (3 lines) 830kt (6)

• Painting (2 lines) 330kt Notes: (1) Tata BlueScope Steel is a 50:50 JV between BlueScope Steel and Tata Steel – metallic coating line commenced trials and

paint line commenced operations at end of CY2011. Will not be included in NS BlueScope Coated Products JV with NSC(2) North Star is a 50:50 JV between BlueScope Steel and North Star Steel (subsidiary of Cargill Inc.); BSL equity share 1.0mt(3) Water sites in the U.S. have been consolidated into ASC sites(4) Four sites in Malaysia, one in Singapore, one in Brunei(5) Two manufacturing sites, seven sales(6) One line has been idled, reducing available capacity by approximately 230ktpa(7) Fourth plant (Xi’an) schedule to commence operations at end of FY2013

Fairfield• Painting 110kt

• Metal Coating 220kt• Painting 100kt

Kalama• Cold Rolling 455kt• Metal Coating 235kt• Painting 110kt

India (1)

• Metal Coating 250kt• Painting 150kt• Lysaght sites 4

New Segment Legend• Global Building Solutions• Building Products ASEAN, North

America and India• Coated & Industrial Products Aust• Building Components & Dist Aust• New Zealand & Pacific Steel Products• Hot Rolled Products North America

Kalama North Star (2)

• Raw Steel 2.3mt • Hot Rolling 2.1mt

North Star (2)

Rancho Cucamonga

Fairfield

India (1)

• Metal Coating 175kt• Painting 75kt• Lysaght sites 6 (4)

Malaysia / Singapore / Brunei

• Metal Coating 285kt• Painting 50kt • Lysaght sites 3

Indonesia

Western Port

• Metal Coating 130kt• Painting 50kt• Lysaght sites 2

Vietnam

• Distribution sites 58• Lysaght sites 33

• Painting 95kt

• Painting (1 line) 120ktSydney

• Raw Steel 2.6mt• Hot Rolling 2.9mt • Plate 450kt• Cold Rolling 990kt• Metal Coating (3 lines) 825kt • Painting (1 line) 200kt

Port Kembla • Iron Sands Mining sites 2• Raw Steel 625kt• Hot Rolling 750kt• Cold Rolling 380kt• Metal Coating 230kt • Painting 65kt• Hollow Sections 45kt• Lysaght sites 3

New Zealand/Pacific Islands

• Buildings sites 1• Cold Rolling 350kt• Metal Coating 350kt• Painting 90kt• Lysaght sites 3

Thailand

• Buildings sites 1

• Metal Coating 250kt• Painting 150kt• Lysaght sites 4• Buildings sites 4 (7)

• Buildings sites 8United States

• ASC Profiles sites 9 (3)

Brisbane

China

• Buildings sites 1Middle East JV

Fairfield• Buildings sites 1Mexico

• Buildings sites 1

Australia

• Service Centres 6• Solutions (Buildings, Water,

Highline, Ranbuild) 9 (5)

Page 36

Business segments and strategy

External operating segment reporting structure1

Coated & Industrial Products Australia

(CIPA)

Building Components &

Distribution Australia

Global Building Solutions

Building Products ASEAN, North

America and India

New Zealand and Pacific Steel

Products

Hot Rolled Products North America

Largest supplier and only manufacturer of HRC, plate, metal coated and painted steel in AustraliaAustralian finished-product capacity of ~2.5Mtpa; domestic market 1.9Mt in CY2012

Major steel product supplier / distributor to the Australian building and construction, automotive, white goods manufacturing and general manufacturing industries

Only fully integrated flat steel maker in New ZealandLeading domestic market share of flat productsIncludes iron sands mines (own consumption and export sales)

2.1Mtpa mini-mill in Ohio50/50 JV with Cargill Inc.Voted no. 1 flat rolled steel supplier in North America (Jacobsen Survey) for ten consecutive years

Operates metallic coating and painting lines and roll-forming in Indonesia, Malaysia, Thailand, Vietnam, India and North AmericaIncludes NS BlueScope Coated Products JV

Leading global designer and manufacturer of pre-engineered buildings2

Key markets in China & Nth America; plants in ASEAN, India, Mid. EastSupplying buildings to global customersChina coating & painting

Managed as four primary businesses with distinct strategies

BlueScope Australia & New ZealandBuilding ProductsBuilding Solutions Hot Rolled ProductsNorth America

Maintain leading market positions; reducing cost baseLevered to domestic volume/mix, A$/US$ and steel & commodity pricesMaking progress on unfair trade (anti-dumping & countervailing actions)Continue to develop innovative products and services and enhanced customer relationships. Next generation ZINCALUME® and COLORBOND® in CY2013Expect CIPA to deliver positive underlying EBITDA in 2H FY2013 3

Continue to improve performance of Building Components & Distribution Australia. On track to nearly double NZ iron sands export capacity (2.7Mtpa, or greater, rate) from beginning of 2H FY2014

Maintain profitability with low cost, highly flexible operationsMaintain strong focus on customer relationsExploring brownfield expansion opportunities (DRI feed and caster expansion)

Grow leading position and enhance profitability in metal coated and painted steel building products in high growth and high value marketsCommence Coated Products joint ventureBase business growth, plus US$30-75M JV value opportunities expected by FY2017

Accelerate growth in EBS2 salesExpand global sales and supply chain networkExpand manufacturing footprint in ChinaDevelop new productsAspiration to double FY2012 segment revenue by FY2015. Target 5% EBIT margin

Stra

tegy

/ Gr

owth

(1) BlueScope also has a Corporate segment which is not shown; (2) engineering and component building systems; (3) Including STP Advance release of $23M and subject to domestic demand and margins, steel spreads and foreign exchange movements

Page 37

27%

37%

4%

21%

3%5% 3%

24%

36%4%

18%

4%

8%6%

22%

33%3%

16%

7%

12%

7%

Exports26%

(939Kt)

3,590Kt 3,164Kt

To the Americas

To Asia

To Europe, Middle East, Africa & IndiaAustralia

North America (including North Star) New Zealand/Pacific

Asia

KeyDomestic sales (produced and sold within country)

1H FY2012 2H FY2012Exports

18%(572Kt)

2,831Kt 12% decrease 11% decrease

Note: Percentages have been rounded.

1H FY2013Exports

11%(300Kt)

Total External Sales

Total BlueScope Group External Despatches

Origin of 1H FY13 External Export VolumeAustralia 132KtNZ 127Asia 29NA (incl Metl-Span) 12

300 Kt

Global despatch mix

Exports

Page 38

Products and end markets

BlueScope Water tanks and fittings

Roll-formed LYSAGHT® products

Slab

Plate

Hot rolled coil

Cold rolled coil

Galvanised (including GALVASPAN® steel) and special zinc finishes

Zinc/aluminium alloy-coated ZINCALUME® steel

Painted (including pre-painted COLORBOND® steel)

BlueScope Buildings, including BUTLER® and VARCO PRUDEN® engineered building solutions

• Steel manufacturing • Hot rolled coil and plate

• Manufacturing, building and construction and mining

• Infrastructure projects, mining equipment and structural applications

• Building and construction, mining, automotive and transport, manufacturing

• Mining equipment, racking, guard rails, building and construction products, structural tubing, water pipelines, oil/gas pipelines and automotive components

• Automotive and transport, manufacturing • Automotive, packaging (drums) and storage systems

• Building and construction, manufacturing, automotive and transport

• General manufacturing, automotive, structural sections for commercial and industrial buildings and structural decking

• Building and construction • Commercial and industrial construction including roofing, walling, rain water goods and residential framing

• Building and construction • Residential, commercial and industrial construction including roofing, walling, fencing, rain water goods, architectural panels, sheds and garages

• Building and construction • High strength and lightweight roofing and walling, industrial / commercial roofing and cladding support systems, premium residential products

• Building and construction• Industrial and resources

• Industrial building and construction (buildings for manufacturing, warehouses, mining and retail and Residential buildings for domestic application)

• Building and construction, infrastructure, agricultural and resources

• Water tanks for commercial, industrial, rural mining and agricultural applications

Product Primary end use markets ApplicationsIron sands • Internal and export steel manufacturers • Crude steel manufacturing

Page 39

2,600 2,600 2,600 2,600 2,600 2,600

5,307 5,285

3,517

4,724

5,173

0

1,000

2,000

3,000

4,000

5,000

6,000

FY07 FY08 FY09 FY10 FY11 Restructure

His torical Australian domestic steel despatches (excludingthird party sourced products)

Overview of the CIPA / Port Kembla Steel Works Restructuring

Shutting down one blast furnace involved:

• Reduction in capacity from 5.3Mtpa to 2.6Mtpa

• A$360-380M in cash costs funded by release of working capital

$301M incurred to 31 Dec 2012

• A$594M release of working capital across the Group: Oct 2011 to June 2012

Key benefits of the restructure:

• Improved alignment between BlueScope’s Australian steelmaking production capacity and Australian demand

• Reduction in significant losses on excess export volumes in the current environment

• Reduce long-term capital investment requirements at Port Kembla

• Potential to reduce volatility of earnings

Improved balance between domestic production and demandActions undertaken and rationale

BlueScope’s historical raw steel production with two blast furnaces

Port Kembla raw steel production capacity of 2.6mtpa following restructuring to one blast furnace (typical yield adjusted despatch mix is lower)

Excess production from second blast furnace

(‘000 tonnes)

Page 40

Background to the CIPA / Port Kembla Restructuring

• PKSW (part of the CIPA division), commenced operations in the 1920s and from 1999 to 2012 operated two blast furnaces50%-60% of production was typically sold into the domestic Australian market where BlueScope had ~70-80% market share of flat steel productsThe remaining 40%-50% was sold into export markets, in particular to Asia and North America

• From FY2009 to FY2012 steel spreads in A$ terms decreased from ~$327/t to $238/t (~27%) due to:Steel prices (set in US$ or import parity pricing) decreasedA$ rose significantly against US$ (FY2012 average rate of A$1.04/US$ vs FY09 average rate of A$0.74/US$)Raw material prices increased significantly

• As a result, in October 2011 BlueScope shut down one blast furnace at the Port Kembla Steel Works to substantially exit the export market

Segment 2005 2006 2007 2008 2009 2010 2011 2012 05-12 avg 09-12 avg 1H FY13^Global Building Solutions 14 39 58 103 61 19 19 66 47 41 33Building Products ASEAN, Nth Am, India 92 70 100 151 (6) 155 127 98 98 94 55Building Components & Distribution Aust 21 32 13 117 49 35 5 (27) 31 16 2New Zealand and Pacific Steel Products 216 132 119 115 117 107 122 113 130 115 27Hot Rolled Products North America 193 167 155 105 (58) 61 72 62 95 34 33Corporate & Group (53) (84) (41) (62) (121) (66) (66) (67) (70) (80) (29)Inter-segment, discontinued and other (54) 15 1 (118) 127 (22) 17 5 (4) 32 (4)Underlying EBITDA pre-CIPA 429 371 405 411 169 289 296 250 328 251 117Coated & Industrial Products Australia 1,427 756 969 1,207 337 305 (56) (151) 599 109 79Total Underlying EBITDA 1,856 1,127 1,374 1,618 506 594 240 99 927 360 196

• Long track record of positive underlying EBITDA in key business segments until CIPA impacted in FY2011 and FY212

CIPA impacted by export losses:FY2011: $152mFY2012: $106m

Substantial long term positive Underlying EBITDA excluding CIPA

(A$ in millions, years ended 30 June)

Note: ^ six month period only

Page 41

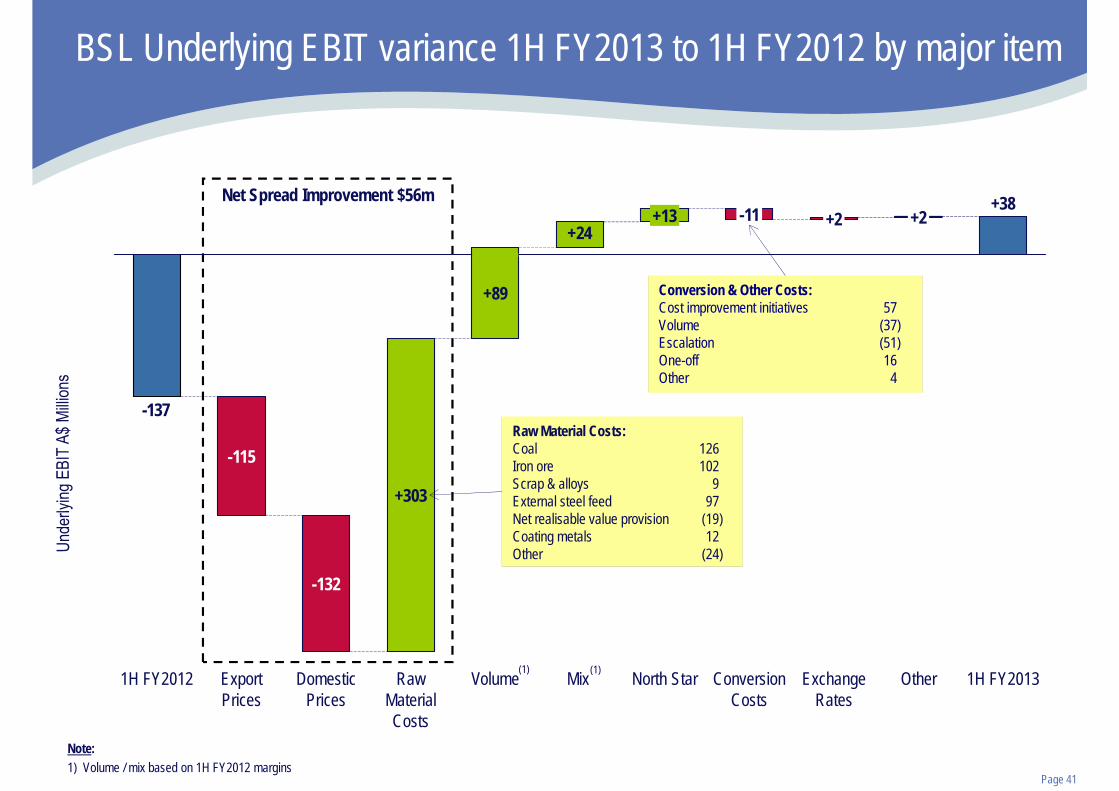

Net Spread Improvement $56m

BSL Underlying EBIT variance 1H FY2013 to 1H FY2012 by major item

+24

-137

1H FY2013

+38

Other

+2

Volume

+89

Raw Material Costs

+303

Domestic Prices

-132

Export Prices

-115

1H FY2012

+13

North Star

-11

Conversion Costs

+2

Exchange Rates

Mix

Raw Material Costs:Coal 126Iron ore 102Scrap & alloys 9External steel feed 97Net realisable value provision (19)Coating metals 12Other (24)

Conversion & Other Costs:Cost improvement initiatives 57Volume (37)Escalation (51)One-off 16Other 4

Note: 1) Volume / mix based on 1H FY2012 margins

(1) (1)

Page 42

Net Spread Reduction $22m

BSL Underlying EBIT variance 1H FY2013 to 2H FY2012 by major item

-87

Conversion Costs

+63

North Star

-9

Mix

+29

Volume

+59

Raw Material Costs

+118

Domestic Prices

-78

Export Prices

-62

2H FY2012 1H FY2013

+38

Other

0

Exchange Rates

+5

Conversion & Other Costs:Cost improvement initiatives 59Volume 22Escalation (47)One-off 18Other 11

(1) (1)

Note: 1) Volume / mix based on 2H FY2012 margins

Raw Material Costs:Coal 70Iron ore 49Scrap & alloys 6 External steel feed 39Net realisable value provision (45) Opening stock adjustments (4)Coating metals 3

Page 43

Balance Sheet

A$M 31 Dec 2011 30 Jun 2012 31 Dec 2012

Assets Cash 186 214 193Receivables * 1,059 995 971Inventory * 1,791 1,409 1,412Property, Plant & Equipment 3,466 3,296 3,225Intangible Assets 686 454 436Other Assets 413 366 376Total Assets 7,601 6,734 6,613

Liabilities Trade & Sundry Creditors * 968 1,008 842Capital & Investing Creditors 20 49 17Borrowings 982 598 692Deferred Income * 166 122 257Retirement Benefit Obligations 409 432 367Provisions & Other Liabilities 779 746 708Total Liabilities 3,324 2,955 2,883Net Assets 4,277 3,779 3,730

Note *: Net Working Capital 1,716 1,274 1,284

Page 44

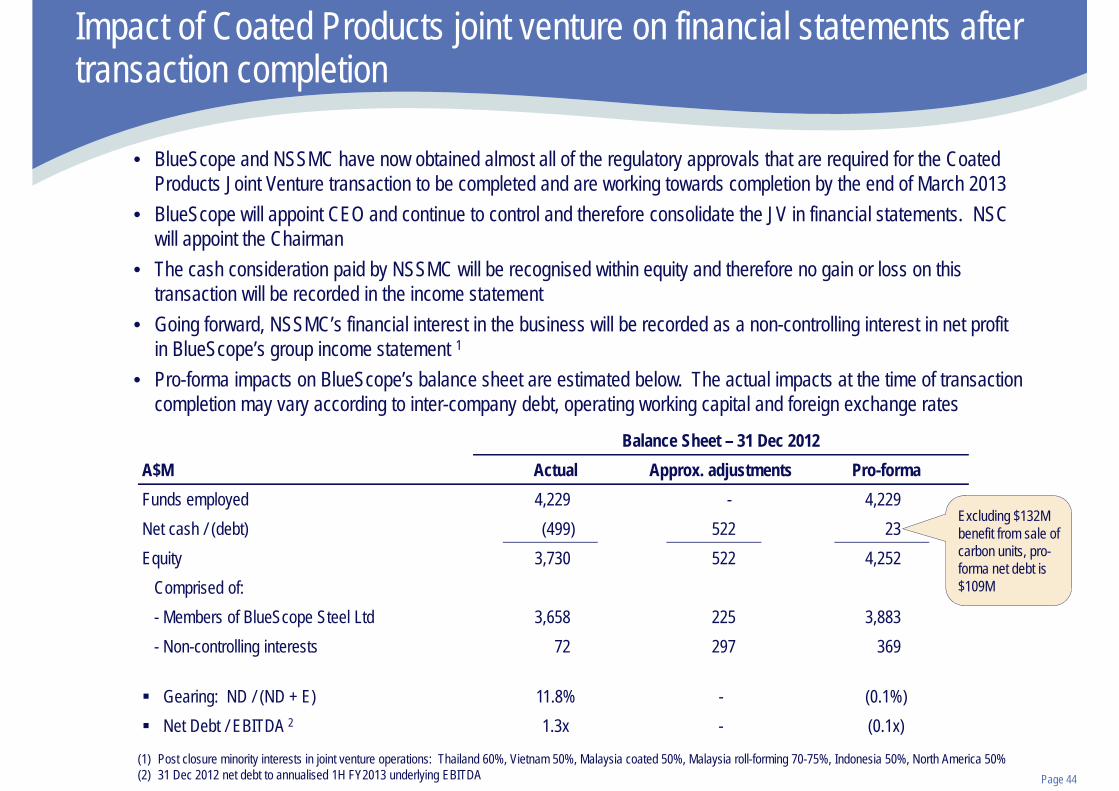

Impact of Coated Products joint venture on financial statements after transaction completion

Balance Sheet – 31 Dec 2012A$M Actual Approx. adjustments Pro-formaFunds employed 4,229 - 4,229Net cash / (debt) (499) 522 23Equity 3,730 522 4,252

Comprised of:- Members of BlueScope Steel Ltd 3,658 225 3,883- Non-controlling interests 72 297 369

Gearing: ND / (ND + E) 11.8% - (0.1%)Net Debt / EBITDA 2 1.3x - (0.1x)

(1) Post closure minority interests in joint venture operations: Thailand 60%, Vietnam 50%, Malaysia coated 50%, Malaysia roll-forming 70-75%, Indonesia 50%, North America 50%(2) 31 Dec 2012 net debt to annualised 1H FY2013 underlying EBITDA

• BlueScope and NSSMC have now obtained almost all of the regulatory approvals that are required for the Coated Products Joint Venture transaction to be completed and are working towards completion by the end of March 2013

• BlueScope will appoint CEO and continue to control and therefore consolidate the JV in financial statements. NSC will appoint the Chairman

• The cash consideration paid by NSSMC will be recognised within equity and therefore no gain or loss on this transaction will be recorded in the income statement

• Going forward, NSSMC’s financial interest in the business will be recorded as a non-controlling interest in net profit in BlueScope’s group income statement 1

• Pro-forma impacts on BlueScope’s balance sheet are estimated below. The actual impacts at the time of transaction completion may vary according to inter-company debt, operating working capital and foreign exchange rates

Excluding $132M benefit from sale of carbon units, pro-forma net debt is $109M

Page 45

Historical Earnings Performance – Reconciliation of Reported to Underlying (A$M)

FY2011 FY2012 1H FY2012 2H FY2012 1H FY2013Reconciliation of EBITDA and EBITEBITDA 2 Reported (687) (489) (270) (219) 204EBIT 2 Reported (1,043) (820) (435) (385) 47

Discontinued Business (gains)/losses (16)5 / (7)6 (47)5 / (39)6 (9)5 / (5)6 (38)5 / (34)6 -Business Development 7 7 - 7 1Restructure / redundancies 14 412 363 49 6Asset sales - 319 5 314 -Asset Impairments 922 (3) - (3) -Sale of previously unrecognised intangible asset - - - - (38)Steel Transformation Plan Advance - (100) (66) (34) 23

EBITDA 3 Underlying 1 240 99 23 76 196EBIT 3 Underlying 1 (107) (224) (137) (87) 38

Reconciliation of NPAT / (NLAT)NPAT / (NLAT) Reported (1,054) (1,044) (530) (514) (12)

Discontinued Business (gains)/losses (10) (4) (6) (2) -Business Development 5 5 - 5 1Restructure / redundancies 10 288 254 34 4Asset sales - 315 - 312 -Asset Impairments 922 (2) 3 (2) -Sale of previously unrecognised intangible asset - - - - (26)Steel Transformation Plan - (70) (46) (24) 16Borrowing Amendment Fees - 6 6 - -Deferred Tax Asset Impairments - 268 184 84 28

NPAT / (NLAT) Underlying 1 (127) (238) (136) (102) 10

EPS (¢) 4 Reported (291.3) (234.6) (159.4) (2.2)EPS (¢) 4 Underlying 1 (32.5) (53.4) (41.0) 1.8

Notes1. Management have provided an analysis of unusual items included in the reported IFRS financial information. These items have been considered in relation to their size and

nature, and have been adjusted from the reported information to assist readers to better understand the financial performance of the underlying business in each reporting period. These adjustments are assessed on a consistent basis from period to period and include both favourable and unfavourable items. Non-IFRS financial information whilst not subject to audit or review has been extracted from the interim financial report which has been subject to review by our external auditors.

2. EBIT = EBITDA - Depreciation & Amortisation 3. Underlying adjustments are the same for both EBITDA & EBIT 4. Earnings per share (EPS) reflects reported and underlying NPAT / (NLAT) divided by average shares on issue for the period

5. EBITDA adjustment6. EBIT adjustment

Page 46

EBIT Segment Summary – Reconciliation of Reported to Underlying (A$M)

FY2011 FY2012 1H FY2012 2H FY2012 1H FY2013Coated & Industrial Products Australia

Reported EBIT (1,063) (726) (463) (263) 7Restructure / redundancies 8 363 347 16 3Asset Impairments 797 136 - 136 -Sale of previously unrecognised intangible asset - - - - (38)Steel Transformation Plan Advance 0 (100) (66) (34) 23Underlying EBIT 1 (258) (327) (182) (145) (6)

Building Components & Distribution AustraliaReported EBIT (201) (227) (30) (197) (10)Restructure / redundancies 2 14 3 11 3Asset Impairments 177 167 - 167 -Profit on sale & leaseback of properties - - - - -Underlying EBIT 1 (22) (46) (27) (19) (7)

New Zealand Steel & Pacific Steel ProductsReported EBIT 82 65 34 31 2Restructure / redundancies - 4 - 4 -Underlying EBIT 1 82 69 34 35 2

Global Building SolutionsReported EBIT 50 (6) 11 (17) 17Asset impairment / (write back) (68) 11 - 11 -Restructure / redundancies 5 29 13 15 -Underlying EBIT 1 (14) 33 24 9 17

Building Products ASEAN, North America & IndiaReported EBIT 66 51 17 34 31Restructure / redundancies - 3 3 - -Asset sales - (3) - (3) -Asset Impairments 16 - - - -Underlying EBIT 1 82 51 21 31 31

Hot Rolled Products North AmericaReported & Underlying EBIT 1 72 62 20 42 33

Corporate & intersegmentReported EBIT (58) (78) (29) (49) (35)Restructure / redundancies - 5 1 3 2Business Development Costs 7 7 - 7 0Underlying EBIT 1 (51) (66) (27) (39) (33)

Discontinued BusinessesReported EBIT 8 39 5 33 -Restructure / redundancies (8) (39) (5) (33) -Underlying EBIT 1 - - - - -

Total GroupReported EBIT (1,043) (820) (435) (385) 47Underlying EBIT 1 (107) (224) (137) (87) 38

Note:1. Management have provided an

analysis of unusual items included in the reported IFRS financial information. These items have been considered in relation to their size and nature, and have been adjusted from the reported information to assist readers to better understand the financial performance of the underlying business in each reporting period. These adjustments are assessed on a consistent basis from period to period and include both favourable and unfavourable items. Non-IFRS financial information whilst not subject to audit or review has been extracted from the interim financial report which has been subject to review by our external auditors.

Paul O’Malley, Managing Director and Chief Executive OfficerCharlie Elias, Chief Financial Officer

18 February 2013

1H FY2013 Financial Results Presentation

BlueScope Steel Limited. ASX Code: BSL