1H 2006 Results Announcement 23 May 2006

44

1H 2006 Results Announcement 23 May 2006

Transcript of 1H 2006 Results Announcement 23 May 2006

1H 2006 ResultsAnnouncement

23 May 2006

2

1H 2006 presentation outline

Graeme Liebelt

Noel Meehan

Graeme Liebelt

• Overview of Results • Strategy

• Business Performance• Cashflow• Balance Sheet• A-IFRS

• IPL Divestment• Chemnet Restructure• Dyno Acquisition• Outlook

3

Sales Revenue +9%

EBIT +13%

NPAT +14%

EPS +6%

Record Result in Mining Services & Chemical Services

Improving Cashflow Performance

Successful Capital Raisings to Fund Dyno Acquisition

Continued growth in shareholder value

Half year ended 31 March 2006

Highlights

4A solid result

Half year ended 31March 2006

Financial summary2006 2005 % Change

NPAT (excluding significant items)

Underlying Results:Sales Revenue A$M 2,599 2,384 9EBIT (excluding significant items) A$M 276 245 13

A$M 146 128 14

Coverage Ratios:Gearing (book) % 35.2 49.0

Interest cover x 5.0 5.2

Results including significant items:

Significant items after tax A$M (23) (3) NPAT including significant items A$M 123 125 (1)

Gearing (adjusted)* % 41.3 49.0

* Hybrid shares notionally reclassified as 50% equity and 50% debt

5

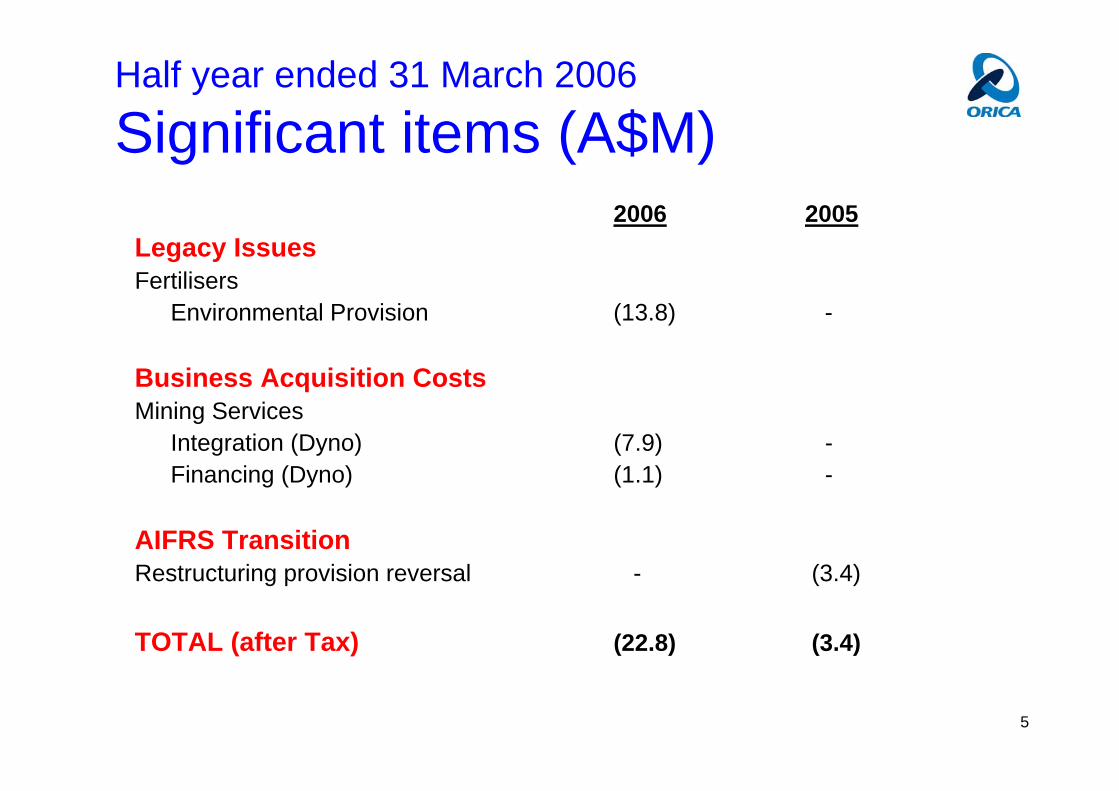

Half year ended 31 March 2006

Significant items (A$M)2006 2005

Legacy IssuesFertilisers

Environmental Provision (13.8) -

Business Acquisition CostsMining Services

Integration (Dyno) (7.9) -Financing (Dyno) (1.1) -

AIFRS TransitionRestructuring provision reversal - (3.4)

TOTAL (after Tax) (22.8) (3.4)

6

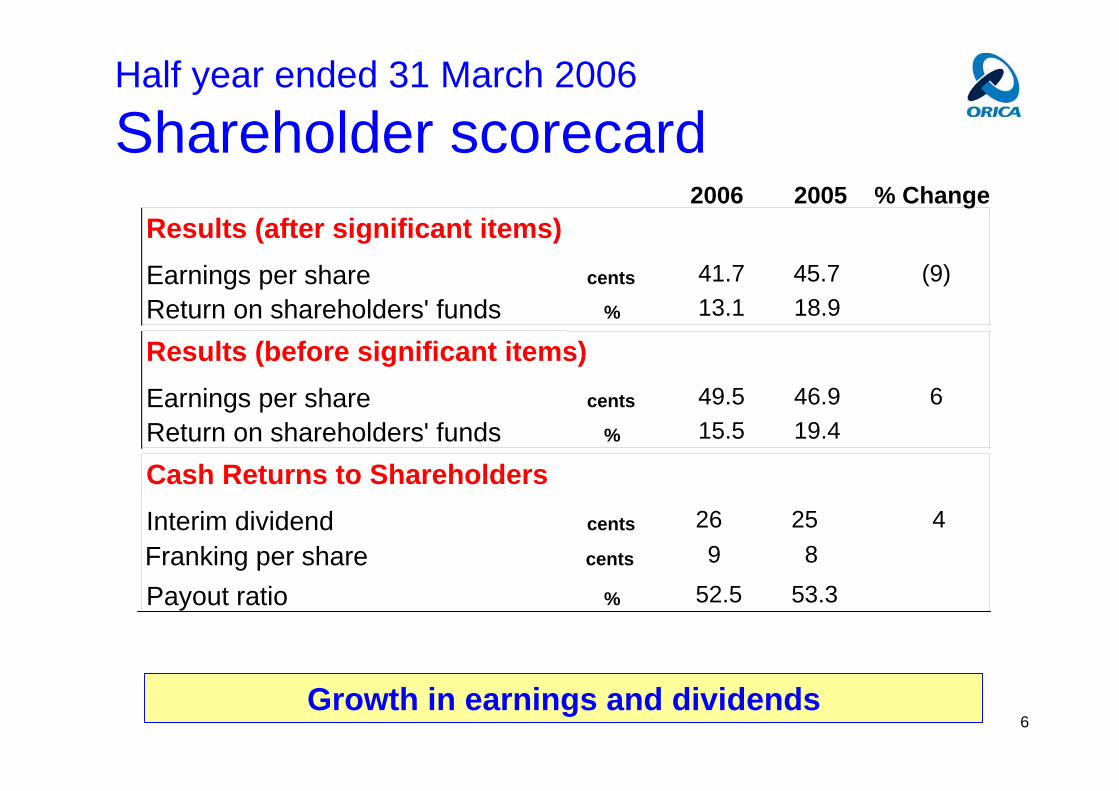

Half year ended 31 March 2006

Shareholder scorecard

Growth in earnings and dividends

Results (after significant items)Earnings per share cents 41.7 45.7 (9)Return on shareholders' funds % 13.1 18.9

Results (before significant items)Earnings per share cents 49.5 46.9 6Return on shareholders' funds % 15.5 19.4

Cash Returns to ShareholdersInterim dividend cents 26 25 4

Payout ratio % 52.5 53.3

2006 2005 % Change

Franking per share cents 9 8

7

Orica’s approach – value drivers

8

Half year ended 31 March 2006

Cost productivity

More work to do on productivity

2006 2005 Increase$M $M $M %

Sales revenue 2,599 2,384 215 9

Variable costs 1,589 1,442 147 10

Gross margin 1,010 942 68 7Gross margin/sales 38.9% 39.5%

Cash fixed costs 692 644 48 7

Depn and amortisation 74 68 7 10

Whole of cost bar 2,355 2,154 201 9WOCB/sales 90.6% 90.3%

Cash fixed costs/gross margin 68.5% 68.4%

9

Half year ended 31 March 2006

Capital productivity

290

50

275

128

FY 2004FY 20051H 2006

Yarwun AN

Major Plant Capacity - ktpa

Yarwun Sodium Cyanide

Kooragang Island

295

60

430 * 400

60

295

Share Buy-Back

Active Capital Management - $MN/A 54

Expansion Capex - $M 178 207 53Sustenance Capex - $M 103 147 146

* As of June 2006

10

Orica’s strategy

Three Key Principles:

Market leadership

Earning the “right to grow”

Growing “close to the core”

No change to existing strategy

11

SH&E

Commercial Ownership- Group Procurement- Supply chain improvement- Manufacturing efficiency

Creative Customer Solutions- Customer driven- Technology

Working Together

‘Deliver the Promise’

Orica – our culture

12

Business PerformanceCash Flow

Balance SheetA-IFRS

13• pre significant items

• pre 2005 not AIFRS adjusted

Expanded capital base impacted ROSHF

Half year ended 31 March 2006

Financial results

128

146

8097

122

300

20

40

60

80

100

120

140

160

01 02 03 04 05 06

NPA

T (A

$M)

0%

5%

10%

15%

20%

25%

RO

SHF

14

Half year ended 31 March

NPAT analysis

EBIT up 13%

Record result for Mining Services and Chemical Services

Fertilisers EBIT up significantly

OCP down marginally

Chemnet down 25%

Sale and Leaseback

Contribution from acquisitions

Sale of QGC shares

Higher interest on higher debt levels

Insurance costs

Elders Rebate & Botany Ground Water

1H05NPATBSI

ExistingBusinesses

SLB Acquisitions QGC Interest Insurance Elders case Other 1H06NPATBSI

128

18

73

4

-6

-4-4 -1

146

120

130

140

150

160A

$M

15

Mining ServicesSales $1,134M, EBIT $151M, Net Assets $1,387M

EBIT

A$M

0

50100

150

200

250

300

350

400

2003 2004 2005 200611

12

13

14

15

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin

Record half year result

Robust Australia/Asia & North American markets

Strong earnings from Joint Ventures

Recovering cost increases through price

Volume growth across all regions

Sale & Leaseback

Rapidly rising gas, ammonia and AN input costs impact margins

Higher fixed costs

Kooragang Island shutdown impact

1H05EBIT

Price/ Mix

NetVolume

SLB VariableCosts

FixedCosts

KI Shut Other 1H06EBIT

131

77

207

-72 -6 -5 -1

151

100

120

140

160

180

200

220

240

260A$M

16

Mining Services by geographyAustralia/Asia

EBIT

A$M

0

50

100

150

200

250

2003 2004 2005 200616

17

18

19

20

21

22

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin

Europe

EBIT

A$M

0

5

10

15

20

25

30

35

2003 2004 2005 20060

2

4

6

8

10

12

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin

Latin America

EBIT

A$M

05

1015202530354045

2003 2004 2005 200602468101214161820

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin

North America

01020304050607080

2003 2004 2005 20060

2

4

6

8

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin

EBIT

A$M

17

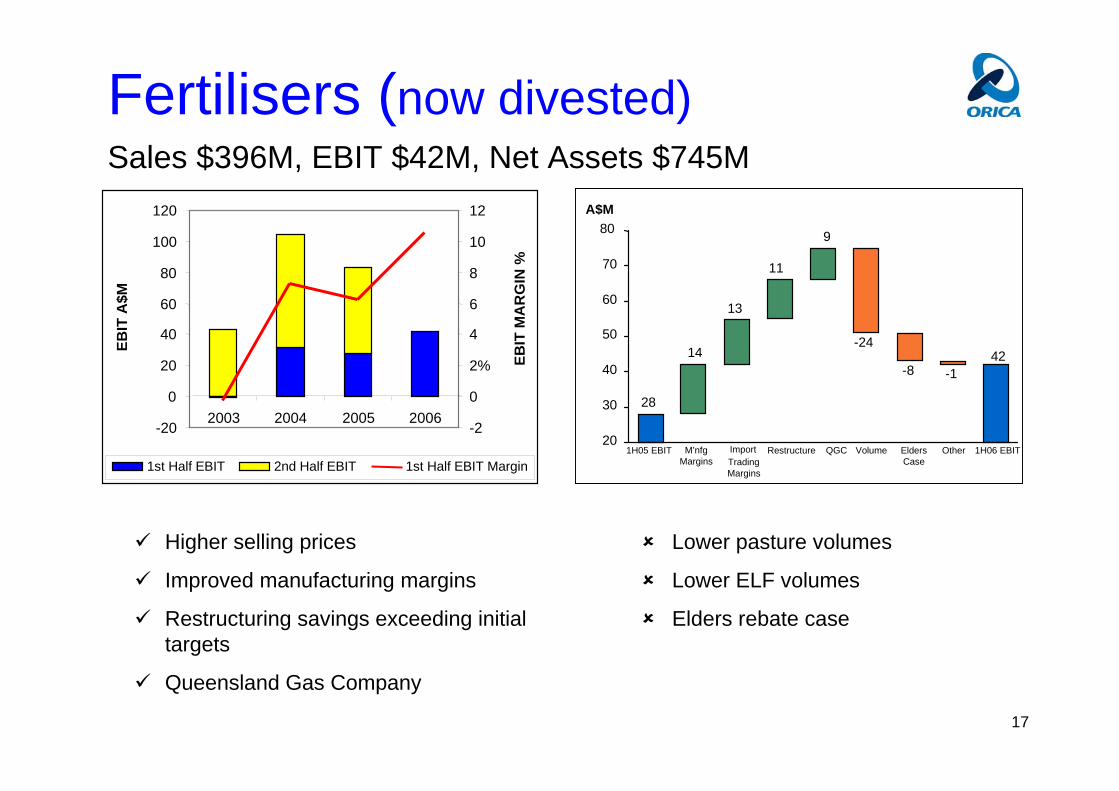

Fertilisers (now divested)Sales $396M, EBIT $42M, Net Assets $745M

Higher selling prices

Improved manufacturing margins

Restructuring savings exceeding initial targets

Queensland Gas Company

Lower pasture volumes

Lower ELF volumes

Elders rebate case

-20

0

20

40

60

80

100

120

2003 2004 2005 2006

EBIT

A$M

-2

0

2%

4

6

8

10

12

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin1H05 EBIT Import

TradingMargins

Restructure QGC Volume EldersCase

Other 1H06 EBIT

28

14

13

11

9

-24

-8 -142

20

30

40

50

60

70

80

M’nfgMargins

A$M

18

Consumer ProductsSales $402M, EBIT $48M, Net Assets $236M

Market share increase

Australian retail market soft

Woodcare, protective coatings, texture coatings and trade

Powder Coatings

Yates improvement

Raw material cost increases not fully passed on

Efficiency improvement

WA plant closure

Higher depreciation

EBIT

A$M

0

20

40

60

80

100

120

2003 2004 2005 20060

2

4

6

8

10

12

14

16

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin1H05 EBIT Yates Net Price Efficiency W.A.

ClosureDepreciation 1H06 EBIT

49

2

-3

2

-1-1

48

40

42

44

46

48

50

52

A$M

19

ChemnetSales $505M; EBIT $29M; Net Assets $425M

Pass through of input costs

Improved product mix

Volumes down (inc. Marplex)

Cash fixed costs up

B&J integration issues

Restructure costs up

1H05 EBIT Price / Mix Volume CashFixed Costs

RestructureCosts

Other 1H06 EBIT

38

4

-7

-2

-3 -1

29

20

25

30

35

40

45

A$M

EBIT

A$M

0102030405060708090

2003 2004 2005 20060

2

4

6

8

10

12

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin

20

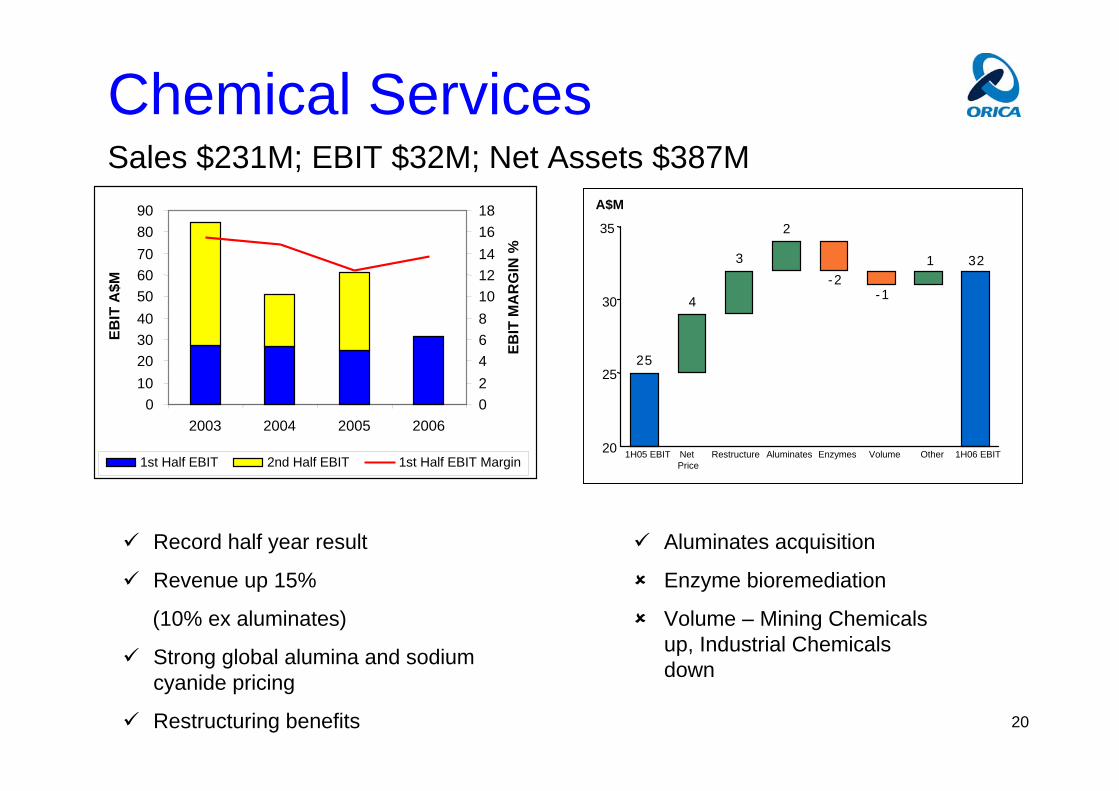

Chemical ServicesSales $231M; EBIT $32M; Net Assets $387M

1H05 EBIT Net Price

Restructure Aluminates Enzymes Volume Other 1H06 EBIT

25

4

3

2

-2-1

1 32

20

25

30

35

A$M

Record half year result

Revenue up 15%

(10% ex aluminates)

Strong global alumina and sodium cyanide pricing

Restructuring benefits

Aluminates acquisition

Enzyme bioremediation

Volume – Mining Chemicals up, Industrial Chemicals down

EBIT

A$M

0102030405060708090

2003 2004 2005 2006024681012141618

EBIT

MA

RG

IN %

1st Half EBIT 2nd Half EBIT 1st Half EBIT Margin

21

Corporate centre and other support services (A$M)

Corporate CentreLower head count

Other Support ServicesHigher insurance costsLower corporate initiative spend

2006 2005 $ ChangeCorporate Centre (17.7) (19.9) 2.2

Other Support Costs (6.8) (6.7) (0.1)

(24.5) (26.6) 2.2

22

Half year ended 31 March 2006

Cashflow A$M2006 2005 Change

EBITDA 350 312 38 Net interest paid (49) (44) (5)Net tax paid (52) (154) 102Trade working capital (223) (170) (53) Non-trade working capital (44) (76) 32

Net operating cash flows (17) (133) 116

Net investing cash flows (1,151) (166) (985)

Net financing cash flows 1,112 322 790 (56) 23 (79)

23

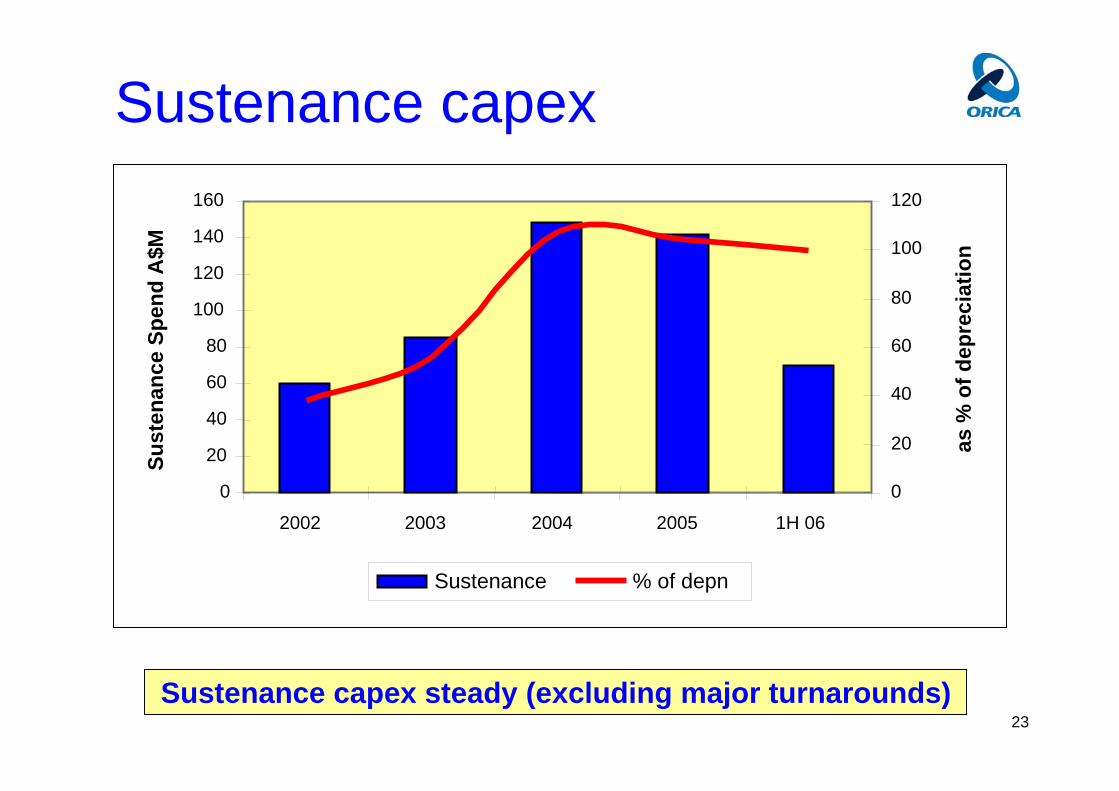

Sustenance capex

Sustenance capex steady (excluding major turnarounds)

Sust

enan

ce S

pend

A$M

0

20

40

60

80

100

120

140

160

2002 2003 2004 2005 1H 06

0

20

40

60

80

100

120

as %

of d

epre

ciat

ion

Sustenance % of depn

24

March Sept March2006 2005 2005

Trade working capital 875 604 949

Net property, plant & equipment 1,774 1,606 1,560

Net other assets 1,392 422 433

Net debt (1,423) (1,112) (1,441)

Net Assets 2,618 1,520 1,501

Orica shareholders' equity 2,432 1,328 1,306

Outside equity interests 187 192 195

Equity 2,618 1,520 1,501

Half year ended 31 March 2006

Balance sheet (A$M)

25

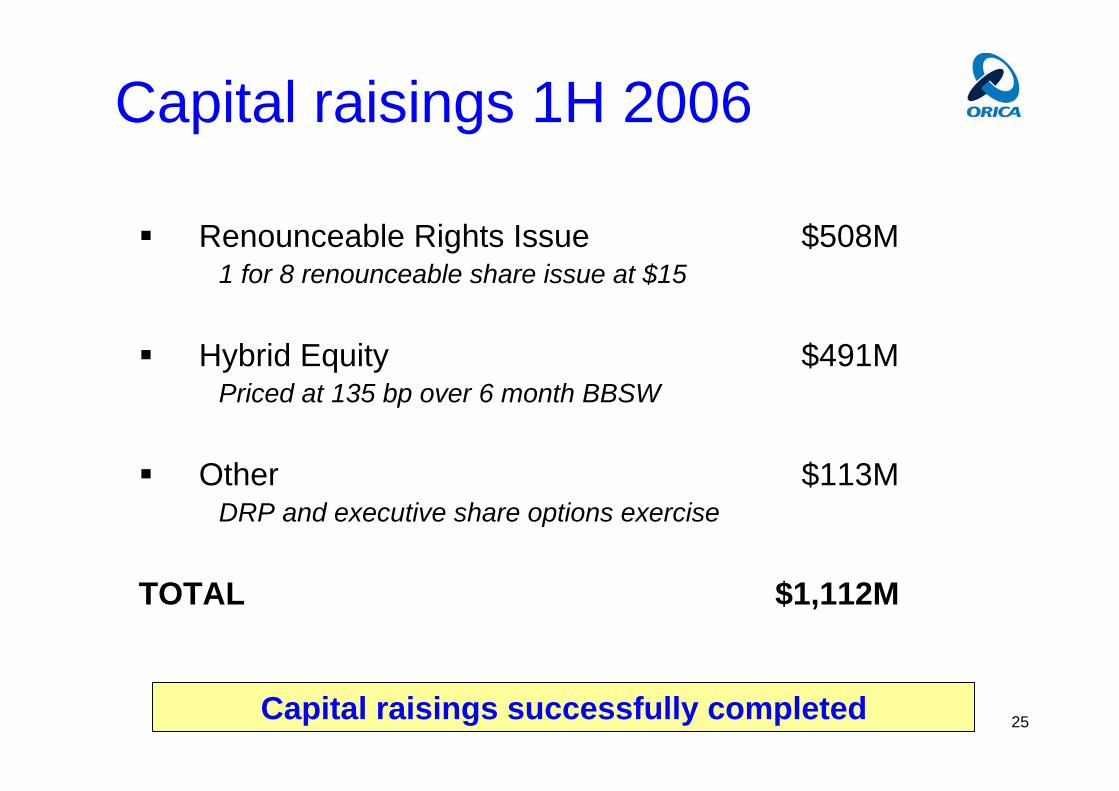

Renounceable Rights Issue $508M1 for 8 renounceable share issue at $15

Hybrid Equity $491MPriced at 135 bp over 6 month BBSW

Other $113MDRP and executive share options exercise

TOTAL $1,112M

Capital raisings 1H 2006

Capital raisings successfully completed

26

Book Gearing 35.2%

Adjusted Gearing 41.3% (hybrids notionally 50/50 debt & equity split)

Interest cover 5.0 times

Net debt and gearing

600

700

800

900

1000

1100

1200

1300

1400

1500

HY02 FY02 HY03 FY03 HY04 FY04 HY05 FY05 HY06

Net

deb

t (A

$M)

0

10

20

30

40

50

60

Gea

ring

%

Target gearing range shaded

27

Carrying amount 30 September 2005 $186M

Provisions made 1H 2006 $31M- Cockle Creek $28M- Botany Ground Water $3M

Cash Payments made 1H 2006 $24M- Botany Ground Water $16M- HCB Management $3M- Other $5M

Carrying amount 31 March 2006 $193M

Environmental provisions update

$48M of $193M carrying value relates to IPL

28

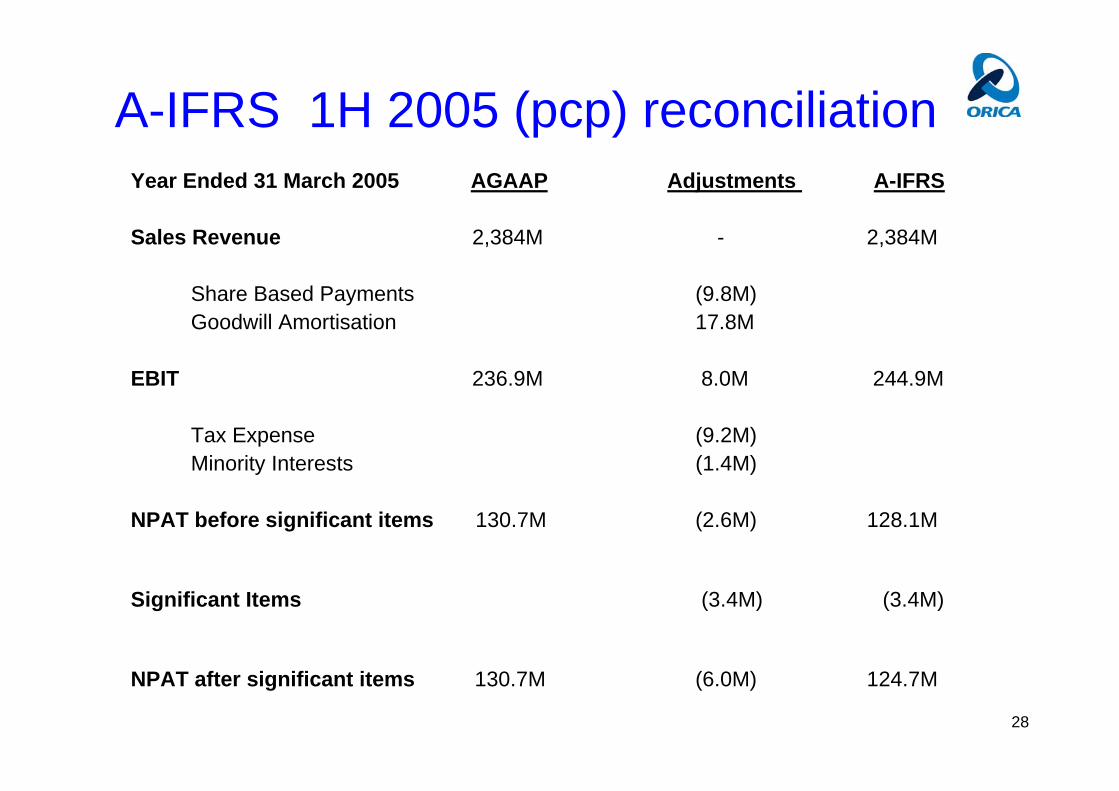

Year Ended 31 March 2005 AGAAP Adjustments A-IFRS

Sales Revenue 2,384M - 2,384M

Share Based Payments (9.8M)Goodwill Amortisation 17.8M

EBIT 236.9M 8.0M 244.9M

Tax Expense (9.2M)Minority Interests (1.4M)

NPAT before significant items 130.7M (2.6M) 128.1M

Significant Items (3.4M) (3.4M)

NPAT after significant items 130.7M (6.0M) 124.7M

A-IFRS 1H 2005 (pcp) reconciliation

29

Strong half year result despite weakness in some business platforms

Record Mining Services and Chemical Services result

Resilience to cost increases

Financial discipline and improved cashflow performance

Strong balance sheet capable of funding future growth

Summary

A disciplined and consistent approach to growing shareholder value

30

IPL DivestmentChemnet Restructure

Dyno AcqusitionOutlook

31

IPL divestment

Orica’s earnings will be less volatile post IPL

Rationale - less earnings volatility going forward- allows each entity to pursue an independent strategy

Orica capital management- Capital projects relating to existing businesses- M&A across remaining businesses

Gross proceeds from sale $857M

After tax gain $399M (to be booked as a significant item in FY2006 results)

32

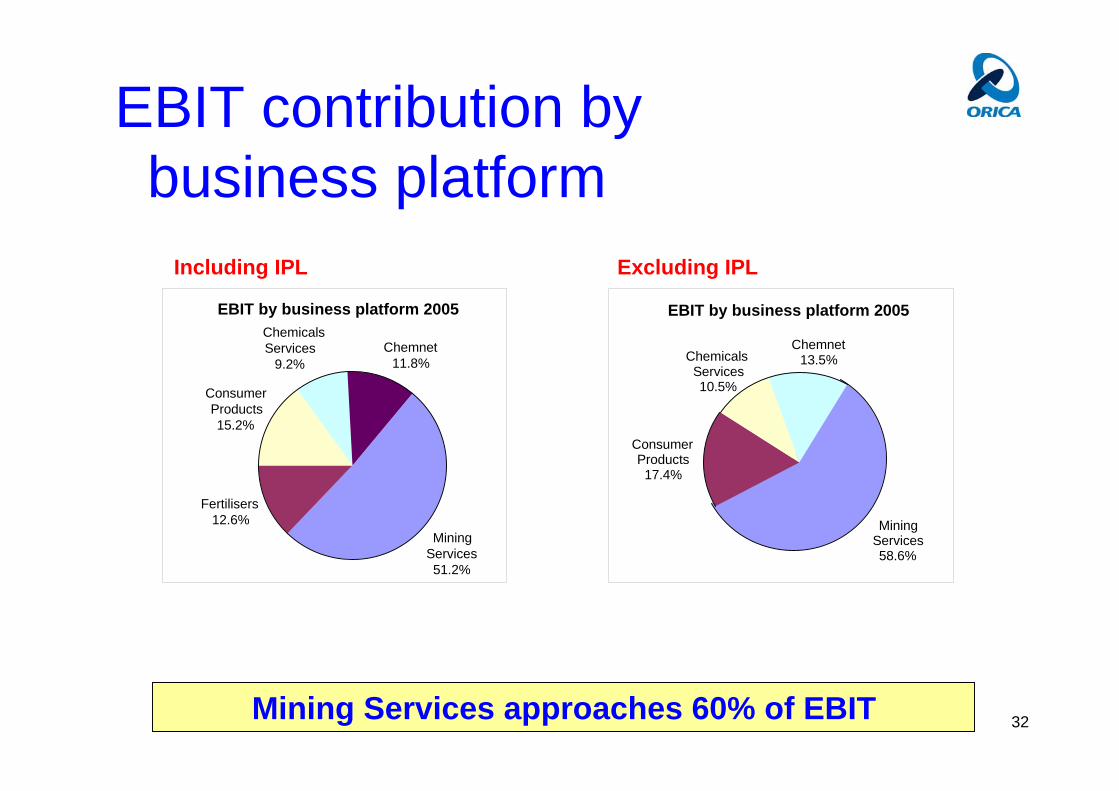

EBIT contribution by business platform

Mining Services approaches 60% of EBIT

EBIT by business platform 2005

Mining Services51.2%

Fertilisers12.6%

Consumer Products15.2%

Chemicals Services

9.2%Chemnet

11.8%

Including IPL

EBIT by business platform 2005

Mining Services58.6%

Consumer Products

17.4%

Chemicals Services10.5%

Chemnet13.5%

Excluding IPL

33

Gross sales by geography

Continuing the “internationalisation” of Orica

Gross sales by geographic area 2005

Australia61.3%

New Zealand9.4%

Americas17.9%

Other11.4%

Including IPL

Gross sales by geographic area 2005

Australia51.5%

New Zealand 11.8%

Americas22.4%

Other14.3%

Excluding IPL

34

EBIT* performance (exc. IPL)

Earnings less cyclical going forward* excluding corporate costs

Past Performance Orica Today

0

50100

150

200250

300350

400

450500

550

600650

700

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

EBIT

$A

M

Current Business EBIT EBIT as reported

35

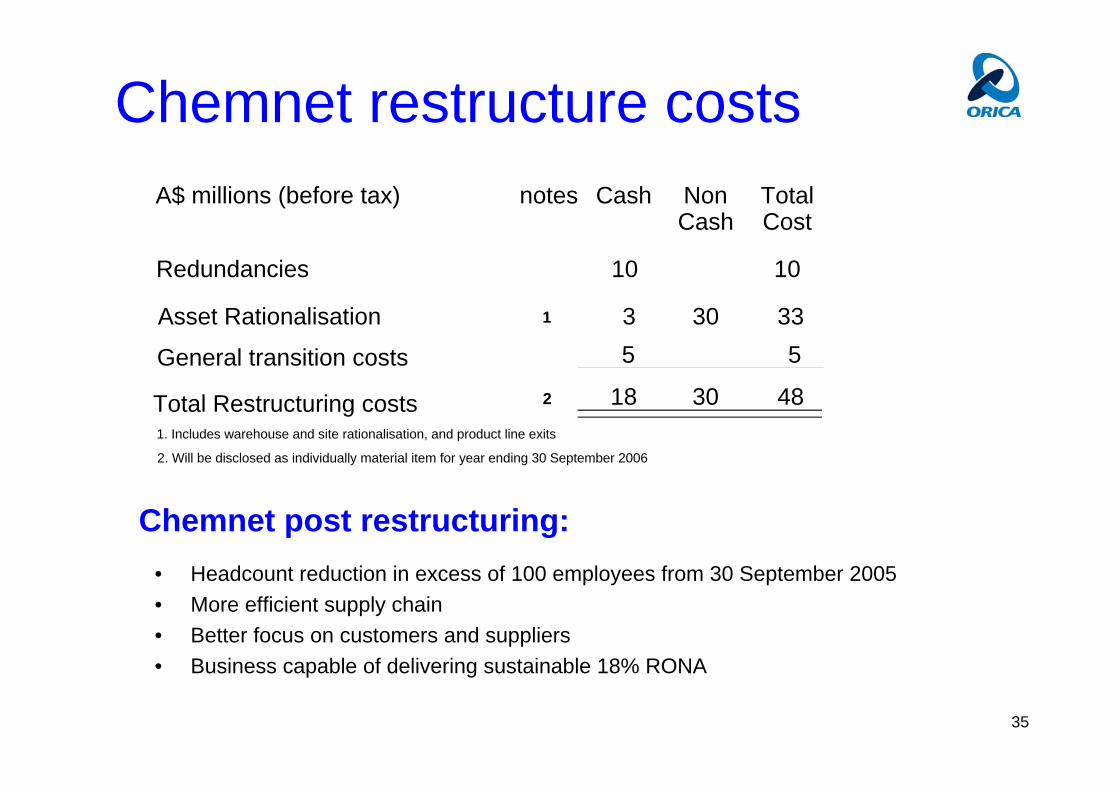

Chemnet restructure costs

1. Includes warehouse and site rationalisation, and product line exits

2. Will be disclosed as individually material item for year ending 30 September 2006

A$ millions (before tax) notes Cash Non TotalCash Cost

Redundancies 10 10

Asset Rationalisation 1 3 30 33

General transition costs 5 5

Total Restructuring costs 2 18 30 48

• Headcount reduction in excess of 100 employees from 30 September 2005• More efficient supply chain• Better focus on customers and suppliers• Business capable of delivering sustainable 18% RONA

Chemnet post restructuring:

36

Dyno businesses already transferred to Orica:VenezuelaThailandSlovakiaSwitzerlandPhilippinesPapua New GuineaIndonesiaChile

Transferred businesses represent 16% of Dynorevenue

Dyno acquisition - update

We remain confident of achieving synergy targets

37

Integration Progress to Date:

– 10 person integration team based in London

– Appointed MD’s of EMEA & Latin America

– No loss of customers from Dyno businesses

– Safety performance maintained

Dyno acquisition - update

We remain confident of achieving synergy targets

38

After the divestment of Incitec Pivot Limited, and excluding earnings from newly acquired Dyno Nobel businesses, earning growth in 2006 compared with 2005, influenced by general economic conditions.

Outlook

1H 2006 ResultsAnnouncement

23 May 2006

40

Supplementary Information

41

Half year ended 31 March 2006

Balance sheet – excluding IPL*

*Estimate subject to final accounting adjustments

March2006

Trade working capital 875M

Net property, plant & equipment 1,774M

Net other assets 1,392M

Net debt (1,423M)

Net Assets 2,618M

Orica shareholders' equity 2,431M

Outside equity interests 187M

Equity 2,618M

Gearing

Sale of IPL Orica excl IPL

35.2%

(263M)

(312M)

15M

0

(560M)

(399M)

(161M)

(560M)

17.9%

Proceeds

799M

799M

799M

612M

1,462M

1,407M

(624M)

2,857M

2,830M

27M

2,857M

42

Half year ended 31 March 2006

Profit & loss – excluding IPL*

*Estimate subject to final accounting adjustments

March2006

Sales Revenue 2,599M

Underlying Results

EBIT 276M

Net Interest (56M)

Tax (61M)

Minority interests (13M)

NPAT and minority interests

Results incl significant items

(23M)Significant items after tax

Sale of IPLOrica excl IPLMarch 2006

123M

(396M)

(42M)

4M

8M

(21M)

14M

116M

2,203M

234M

(51M)

(53M)

125M

(9M)

NPAT and minority interests

146M

(7M)

9M (5M)

Orica excl IPLMarch 2005

111M

1,945M

215M

(44M)

(54M)

114M

(3M)

(4M)

% change

4.5

13.3

8.8

15.9

(2)

9.6

(25)

43

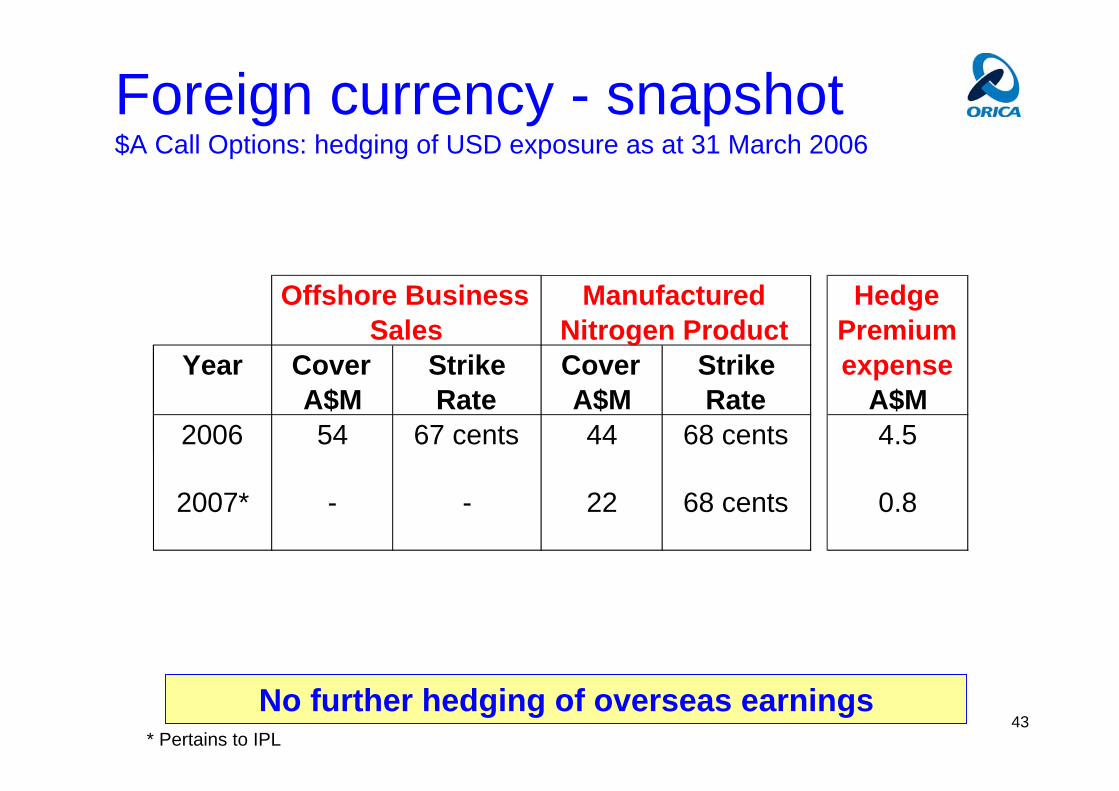

Offshore Business Manufactured HedgeSales Nitrogen Product Premium

Year Cover Strike Cover Strike expenseA$M Rate A$M Rate A$M

2006 54 67 cents 44 68 cents 4.5

2007* - - 22 68 cents 0.8

Foreign currency - snapshot$A Call Options: hedging of USD exposure as at 31 March 2006

No further hedging of overseas earnings* Pertains to IPL

44

50% of Orica’s AUD/USD exposure came from IPL

Every one cent movement in the USD/AUD exchange rate will impact EBIT:

2006 +/- $0.5M 2007 +/- $1.0M

Foreign currency - sensitivity(excluding IPL)

![Wimm-Bill-Dann Foods OJSC [NYSE: WBD] · 5 1H 2006 Operational Highlights • Profitable growth continues in 1H 2006 • New CEO Tony Maher appointed • Beverage segment turnaround](https://static.fdocuments.in/doc/165x107/5f0f51037e708231d4438ee9/wimm-bill-dann-foods-ojsc-nyse-wbd-5-1h-2006-operational-highlights-a-profitable.jpg)