19 - 1 ©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber...

49

19 - Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harriso Introduction to Management Accounting Chapter 19

-

Upload

brendan-glenn -

Category

Documents

-

view

238 -

download

4

Transcript of 19 - 1 ©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber...

19 - 1©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Introduction toManagement Accounting

Chapter 19

19 - 2©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Planning Acting

Feedback

Controlling

The Functions of Management

19 - 3©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Distinguish between financial

accounting and managementaccounting.

Objective 1

19 - 4©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Management Accounting and Financial Accounting

Internal managers of the businessInternal managers of the business

Investors, Creditors,Government authorities (IRS, SEC, etc.)

Investors, Creditors,Government authorities (IRS, SEC, etc.)

Primary Users

19 - 5©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Management Accounting and Financial Accounting

Help managers plan andcontrol business operations

Help managers plan andcontrol business operations

Help investors, creditors, and others makeinvestment, credit, and other decisions

Help investors, creditors, and others makeinvestment, credit, and other decisions

Purpose of Information

19 - 6©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Management Accounting and Financial Accounting

RelevanceRelevance

Reliability, objectivity, and focus on the pastReliability, objectivity, and focus on the past

Focus and Time Dimension

19 - 7©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Management Accounting and Financial Accounting

Internal reports not restricted by GAAPInternal reports not restricted by GAAP

Financial statements restricted by GAAPFinancial statements restricted by GAAP

Type of Report

19 - 8©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Management Accounting and Financial Accounting

No independent auditNo independent audit

Annual independent audit by CPAsAnnual independent audit by CPAs

Verification

19 - 9©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Management Accounting and Financial Accounting

Detailed reports onparts of the company

Detailed reports onparts of the company

Summary reports primarilyon the company as a wholeSummary reports primarilyon the company as a whole

Scope of Information

19 - 10©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Management Accounting and Financial Accounting

Concern about how reportswill affect employees behavior

Concern about how reportswill affect employees behavior

Concern about adequacy of disclosureConcern about adequacy of disclosure

Behavioral Implications

19 - 11©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

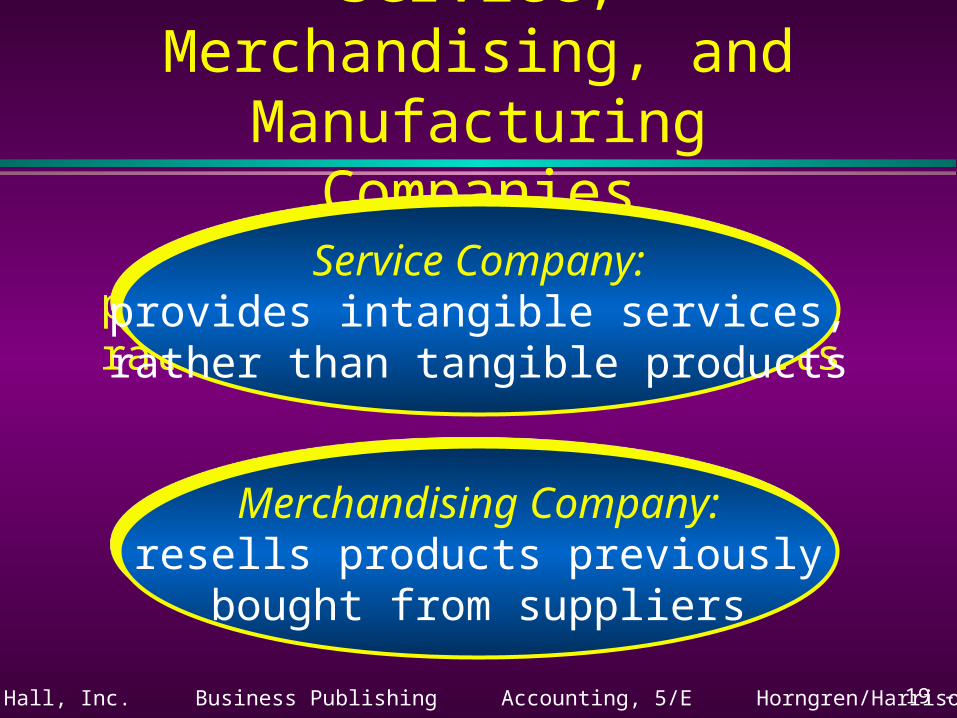

Service, Merchandising, and Manufacturing Companies

Service Company:provides intangible services,rather than tangible products

Service Company:provides intangible services,rather than tangible products

Merchandising Company:resells products previously

bought from suppliers

Merchandising Company:resells products previously

bought from suppliers

19 - 12©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Service, Merchandising, and Manufacturing Companies

Manufacturing Company:uses labor, plant, and equipment to convert

raw materials into finished products

Manufacturing Company:uses labor, plant, and equipment to convert

raw materials into finished products

Materials inventoryWork in process inventoryFinished goods inventory

Materials inventoryWork in process inventoryFinished goods inventory

19 - 13©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Describe the value chain

and classify costs byvalue-chain functions.

Objective 2

19 - 14©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Value Chain

Research andDevelopment

DesignProduction or

Purchases

Marketing Distribution CustomerServices

19 - 15©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Distinguish direct costs

from indirect costs.

Objective 3

19 - 16©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Cost Objects, Direct Costs,and Indirect Costs

Cost objects are anything for which a separate measurement of costs is desired.

Cost drivers are any factors that affect cost.

19 - 17©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Cost Objects, Direct Costs,and Indirect Costs

What are examples of cost objects?– individual products– alternative marketing strategies– geographic segments of the business– departments

19 - 18©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Cost Objects, Direct Costs,and Indirect Costs

What are direct costs? Direct costs are those costs that can be

specifically traced to the cost object. What are indirect costs? Indirect costs are costs that cannot be

specifically traced to the cost object.

19 - 19©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Distinguish among full product

costs, inventoriable productcosts, and period costs.

Objective 4

19 - 20©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Inventoriableproduct

costs

Inventoriableproduct

costs

Fullproduct

costs

Fullproduct

costs

Product Costs

What are product costs? They are the costs to produce (or purchase)

tangible products intended for sale. There are two types of product costs:

19 - 21©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

External Reporting

Inventoriableproduct

costs

Inventoriableproduct

costs

PeriodcostsPeriodcosts

19 - 22©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Inventoriable Product Costs

For external reporting, merchandisers’ inventoriable product costs include only costs that are incurred in the purchase of goods.

Inventoriable costs are an asset. Period costs flow as expenses directly to the

income statement.

19 - 23©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Inventoriable Product Costs

For external reporting, manufacturers’ inventoriable product costs include raw materials plus all other costs incurred in the manufacturing process.

Inventoriable product costs are incurred only in the third element of the value chain.

Costs incurred in other elements of the value chain are period costs.

19 - 24©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

DirectMaterials

DirectLabor

IndirectLabor

IndirectMaterials

Other

Manufacturing Overhead

Inventoriable Product Costs

19 - 25©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Inventoriable Product Costs

DirectMaterials

DirectLabor

Prime Costs = Direct Materials + Direct Labor

19 - 26©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Inventoriable Product Costs

Conversion Costs = Direct Labor + Manufacturing Overhead

DirectLabor

IndirectLabor

IndirectMaterials

Other

19 - 27©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Prepare the financial statements

of a manufacturing company.

Objective 5

19 - 28©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

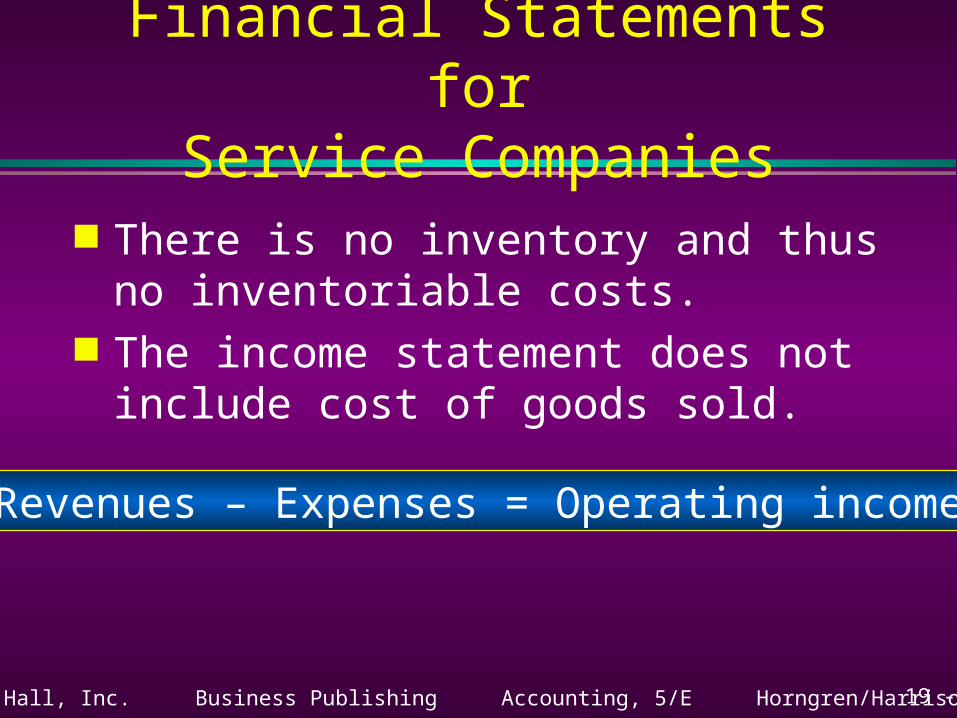

Revenues – Expenses = Operating income

Financial Statements forService Companies

There is no inventory and thus no inventoriable costs.

The income statement does not include cost of goods sold.

19 - 29©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Financial Statements for Merchandising Companies

Purchases ofInventory plus

Freight-In Inventory

Sales Revenue

Cost ofGoods Sold

INCOME STATEMENT

Operating Expenses

InventoriableCosts

BALANCE SHEET

equals Operating Income

whensalesoccur

deduct

equals Gross Margindeduct

PeriodCosts

19 - 30©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Financial Statements forManufacturing Companies

MaterialsInventory

FinishedGoods

Inventory

Sales Revenue

Cost ofGoods Sold

INCOME STATEMENT

Operating Expenses

InventoriableCosts

BALANCE SHEET

equals Operating Income

whensalesoccur

deduct

equals Gross Margindeduct

Work inProcess

Inventory

PeriodCosts

19 - 31©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Company Example

Kendall Manufacturing Company: Beginning and ending work-in-process

inventories were $20,000 and $18,000. Direct materials used were $70,000. Direct labor was $100,000. Manufacturing overhead incurred was

$150,000.

19 - 32©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Company Example

What is the cost of goods manufactured?

Beginning work in process $ 20,000Direct labor $100,000Direct materials 70,000Mfg. overhead 150,000 320,000Ending work in process 18,000Cost of goods manufactured $322,000

19 - 33©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Company Example

Kendall Manufacturing Company’s beginning finished goods inventory was $60,000 and its ending finished goods inventory was $55,000.

How much is the cost of goods sold?

19 - 34©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Company Example

Beg. finished goods inventory $ 60,000+ Cost of goods manufactured 322,000= Cost of goods available for sale $382,000– Ending finished goods 55,000= Cost of goods sold $327,000

19 - 35©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Company Example

Kendall Manufacturing Company had sales of $627,000 for the period.

How much is the gross margin?

Sales $627,000– Cost of goods sold 327,000= Gross margin $300,000

19 - 36©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Company Example

Kendall Manufacturing Company had operating expenses as follows:

Sales salaries and commissions $ 80,000 Delivery expense 10,000 Administrative expenses 30,000 Total$120,000

What is Kendall’s operating income?

19 - 37©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Manufacturing Company Example

Gross margin $300,000– Operating expenses 120,000= Operating income $180,000

19 - 38©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Flow of Costs through a Manufacturer’s Accounts

Direct Materials Inventory Beginning inventory+ Purchases and freight-in

= Direct materials availablefor use

– Ending inventory= Direct materials used

Work in Process Inventory Beginning inventory+ Direct materials used+ Direct labor+ Manufacturing overhead= Total manufacturing costs

to account for– Ending inventory= Cost of goods manufactured

19 - 39©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Flow of Costs through a Manufacturer’s Accounts

Finished Goods Inventory Beginning inventory+ Cost of goods manufactured= Cost of goods available for sale– Ending inventory= Cost of goods sold

19 - 40©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Identify major trends in thebusiness environment, and

usecost-benefit analysis to make

business decisions.

Objective 6

19 - 41©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Shift to a Service Economy

In the U.S., 55% of the workforceis employed in service companies.

Service Industries Other

19 - 42©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Competing in the Global Marketplace

Foreign Operations Other

Foreign operations accountfor over 30% of GE’s revenues.

19 - 43©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Just-in-Time

JIT philosophy means that the company schedules production just in time to satisfy needs.

Speeding up of the production process reduces throughput time.

Throughput time is the time between buying raw materials and selling the finished products.

19 - 44©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Total Quality Management

The goal of total quality management (TQM) is to please customers by providing them with superior products and services.

TQM emphasizes educating, training, and cross-training employees.

Quality improvement programs cost money today.

The benefits usually do not occur until later.

19 - 45©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Total Quality Management

Initial benefits and costs $170 million $200 million

Additionalexpected benefits 68 million

Total $238 million $200 million

Total Benefits Total Cost

19 - 46©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Use reasonable standards to

make ethical judgments.

Objective 7

19 - 47©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

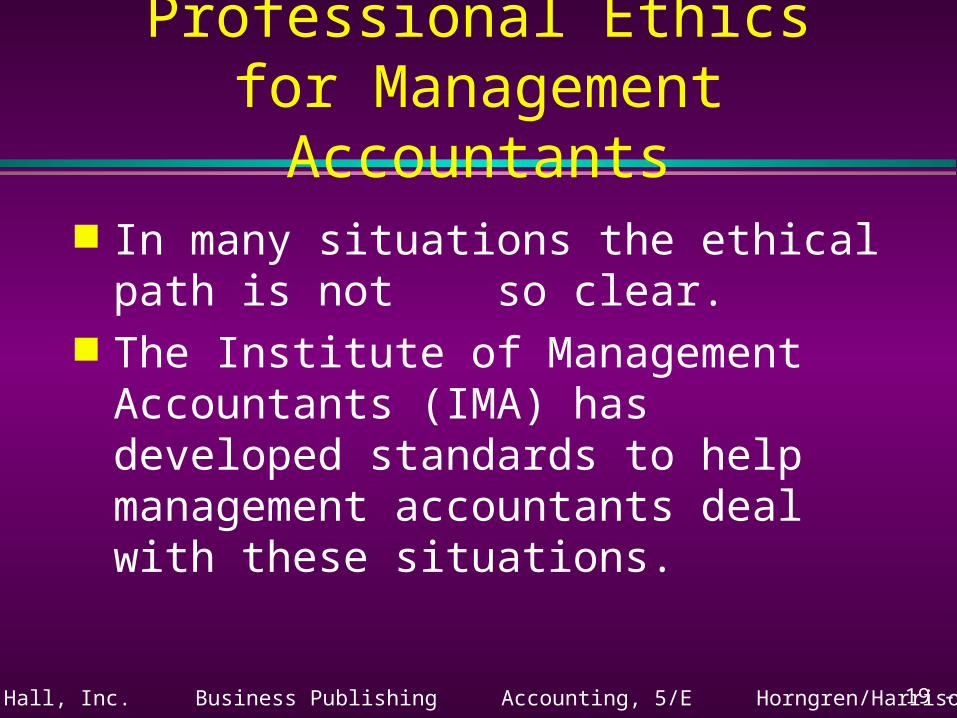

Professional Ethics for Management Accountants

In many situations the ethical path is not so clear.

The Institute of Management Accountants (IMA) has developed standards to help management accountants deal with these situations.

19 - 48©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

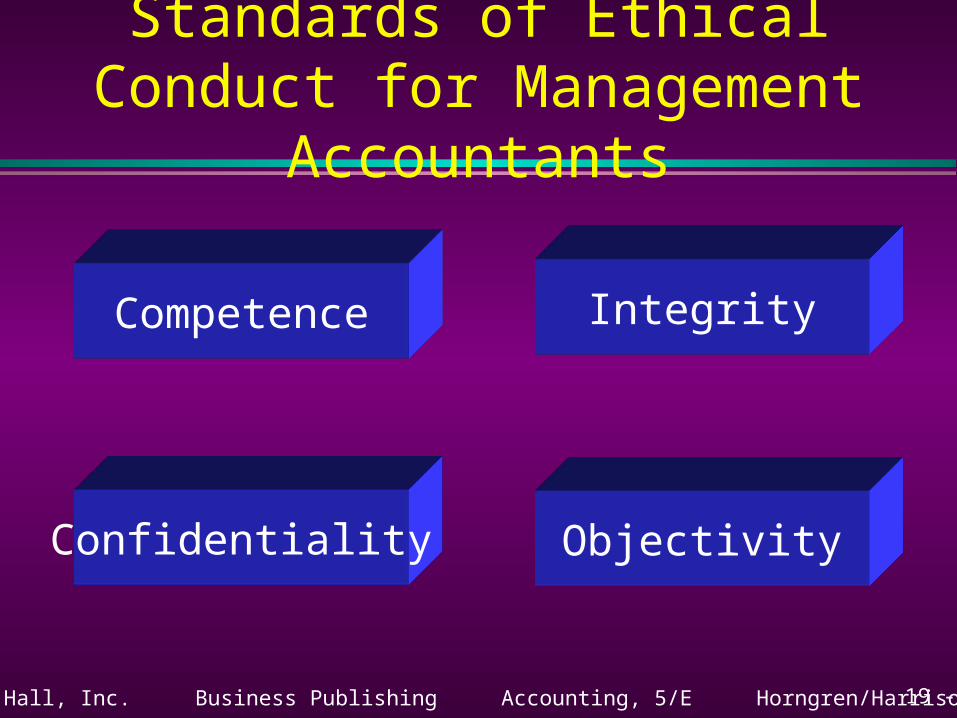

Standards of Ethical Conduct for Management Accountants

Confidentiality

Integrity

Objectivity

Competence

19 - 49©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

End of Chapter 19