18 September 20091 Health Plan Actuarial Value Variation Among Employers Actuarial Research...

39

18 September 2009 1 Health Plan Actuarial Value Variation Among Employers Actuarial Research Corporation Sarah Yi Jim Mays Middle Atlantic Actuarial Club 2009 Annual Meeting Session 6A

-

Upload

gwendolyn-maxwell -

Category

Documents

-

view

217 -

download

0

Transcript of 18 September 20091 Health Plan Actuarial Value Variation Among Employers Actuarial Research...

18 September 2009 1

Health Plan Actuarial Value Variation Among Employers

Actuarial Research CorporationSarah Yi

Jim Mays

Middle Atlantic Actuarial Club2009 Annual Meeting

Session 6A

18 September 2009 2

Outline of Presentation

• Background• EBSA Project• Data• Methodology• Results• Policy Applications• Questions and Comments

18 September 2009 3

Background

EBSA Project

• Research was funded by the Employee Benefits Security Administration (DoL/EBSA)

• The views and opinions contained in this report are solely those of the authors and do not necessarily reflect the official policy or position of the Department of Labor or the Employee Benefits Security Administration.

18 September 2009 4

18 September 2009 5

Background

• Context– Health finance reform design– Minimum coverage rules – Modification of tax exclusion

18 September 2009 6

Background

• Definition of Actuarial Value:the fraction of average recognized medical charges which a health plan would have paid, had it been covering a standardized population with standardized medical spending levels

• Actuarial Value is a single statistic that captures the effect of deductibles, copayments/coinsurance, and out-of-pocket maximums

18 September 2009 7

EBSA Project

18 September 2009 8

Research Questions/ Hypotheses

• How dispersed are employer-sponsored health insurance average actuarial values?

• To what degree does actuarial value predict plan cost?

18 September 2009 9

Goals

• Actuarial values for each health insurance plan in the NCS

• Percentile distributions of actuarial value• Summary distributions of plan costs within

actuarial value deciles

18 September 2009 10

Data

National Compensation Survey

• Produced by Bureau of Labor Statistics• Data not available for public use• Three stage survey design– Selection of areas– Selection of establishments (from private

industry)– Selection of occupations within establishments

• Plans remain in sample for 5 years

18 September 2009 11

18 September 2009 12

Uniqueness of NCS Data

• Definitive source for information on ESI parameters

• Well-established process• Detailed specifications• Large sample• More reliable than other datasets

18 September 2009 13

Use of NCS Data: Overview

• Plan provisions• Premiums• Plan characteristics• Worker characteristics• Establishment characteristics

18 September 2009 14

Use of NCS Data: Plan Provisions

• From Summary Plan Description documents abstracted by BLS analysts

• Consistent with National Compensation Survey: Employee Benefits in Private Industry in the United States, 2005

18 September 2009 15

Use of NCS Data: Plan Provisions

• Covered services (inpatient hospital, outpatient hospital, physician visits, mental health, prescription drugs)

• Cost-sharing parameters– Deductibles– Copayments– Coinsurance– Out-of-pocket maximums– Presence of benefit maximums

18 September 2009 16

Use of NCS Data: Premiums

• Collected in person or on phone by field economists

• Potential mismatch in plan types (medical, prescription, dental, vision) between provision and premium data

18 September 2009 17

Use of NCS Data: Premiums

• Premiums– Total premiums– Employer premiums– Employee premiums

18 September 2009 18

Use of NCS Data: Plan Characteristics

• Plan characteristics– Plan type (FFS, PPO/POS, HMO) – Financing (insured, self-insured or combined)

18 September 2009 19

Use of NCS Data: Worker and Establishment Characteristics

• Worker characteristics– Average wages– Union status

• Establishment size

18 September 2009 20

Use of NCS Data

• Kept plans with medical and drug provisions• Kept plans with a known plan type

18 September 2009 21

Methodology

18 September 2009 22

Methodology

• Run a claims payment program on each plan to calculate actuarial value

• Sort plans into deciles of actuarial value• Sort plans into deciles of premium• Make two-way tables

18 September 2009 23

Standardized Population Data for Claims Program

• Based on the MEPS public use files• Controlled to National Health Accounts totals• Adjusted to 2005 levels• Over 16,000 individual records• Representative of under 65 active ESI

enrollees

18 September 2009 24

Simplified Cost-Sharing Provisions for Plan A

• $20 copay for each physician visit• $450 deductible for each hospital

confinement

18 September 2009 25

Person 1’s Utilization and Covered Charges

• Total covered charges = $5,000

• Physician office visits = 5• Physician office visit covered charges = $1,000

• Hospital confinements = 2• Inpatient hospital covered charges = $4,000

18 September 2009 26

Person 1’s Cost-Sharing for Plan A

• Physician ($1,000, 5 visits, subject to $20 copay per visit)

Cost-sharing collected is 5*$20 = $100• Hospital (2 confinements at $2,000 each,

subject to $450 deductible per confinement)Cost-sharing collected is 2*$450 = $900

• Total cost-sharing = physician cost-sharing + hospital cost-sharing = $100 + $900 = $1000

18 September 2009 27

Plan Share for Plan A with Person 1’s Utilization and Covered Charges

• Plan payment = total covered charges – cost-sharing

• For Person 1, plan payment = $5,000 - $1,000 = $4,000

• Plan share = plan payment/ total covered charges• Plan share for Plan A for Person 1 =

$4,000/$5,000 = .8

18 September 2009 28

Actuarial Value for Plan A

• Weighted average plan shares for each of the 16,000 people

18 September 2009 29

Summary of Methodology

• Run a claims payment program on each plan to calculate actuarial value

• Sort plans into deciles of actuarial value• Sort plans into deciles of premium• Make two-way tables

18 September 2009 30

Results

18 September 2009 31

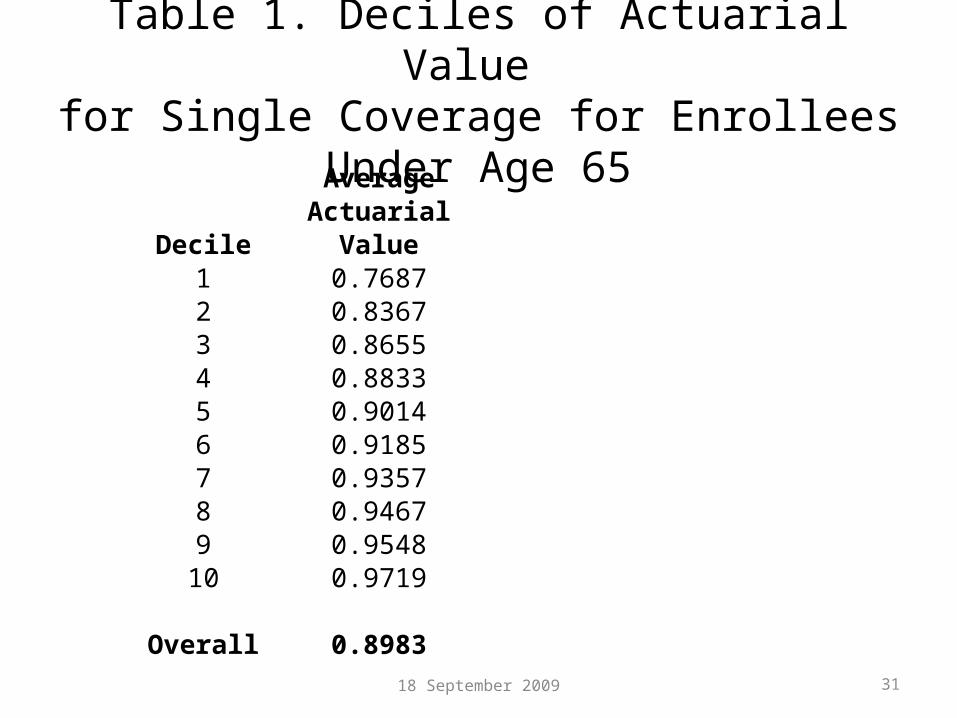

Table 1. Deciles of Actuarial Value for Single Coverage for Enrollees Under Age 65

AverageActuarial

Decile Value1 0.76872 0.83673 0.86554 0.88335 0.90146 0.91857 0.93578 0.94679 0.9548

10 0.9719

Overall 0.8983

18 September 2009 32

Table 2. Average Total Premium within Each Decile of Actuarial Value for Single Coverage for Enrollees Under Age 65

Average AverageActuarial Total

Decile Value Premium1 0.7687 344.752 0.8367 308.043 0.8655 311.484 0.8833 324.915 0.9014 324.266 0.9185 318.597 0.9357 333.088 0.9467 322.289 0.9548 332.49

10 0.9719 348.15

Overall 0.8983 326.81

Table 3. Average Actuarial Value within Each Decile of Total Premium for Single Coverage for Enrollees Under Age 65

18 September 2009 33

Average AverageTotal Actuarial

Decile Premium Value1 155.93 0.89602 228.03 0.89643 259.23 0.89514 284.93 0.89025 303.71 0.90396 328.55 0.90657 353.53 0.89568 377.27 0.90339 421.59 0.8951

10 555.87 0.9011

Overall 326.81 0.8983

18 September 2009 34

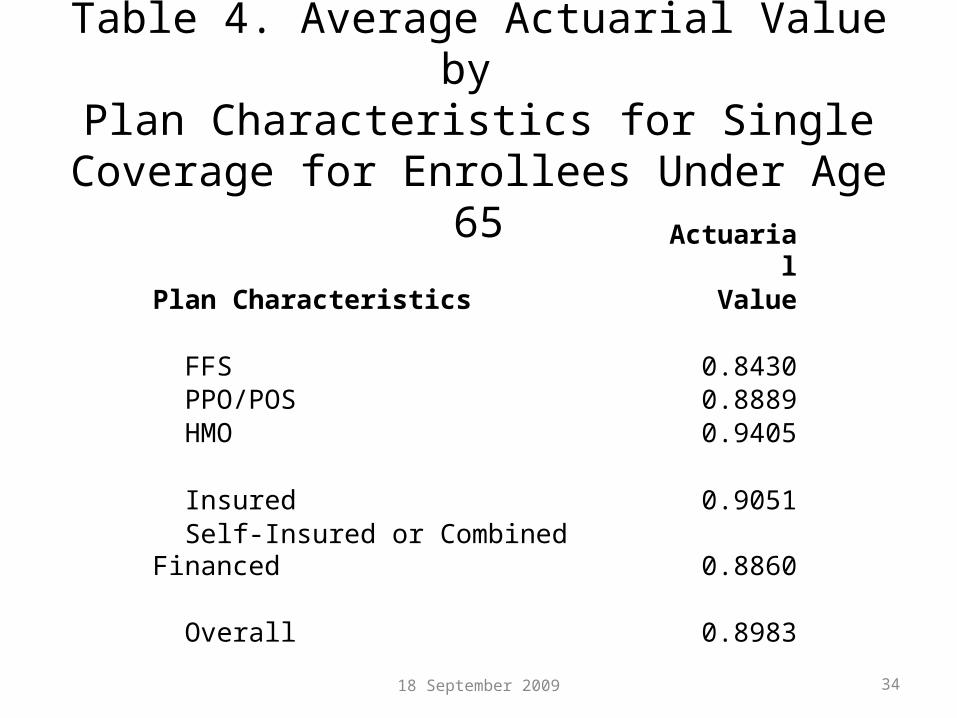

Table 4. Average Actuarial Value by Plan Characteristics for Single Coverage for

Enrollees Under Age 65

ActuarialPlan Characteristics Value

FFS 0.8430 PPO/POS 0.8889 HMO 0.9405

Insured 0.9051

Self-Insured or Combined Financed 0.8860

Overall 0.8983

18 September 2009 35

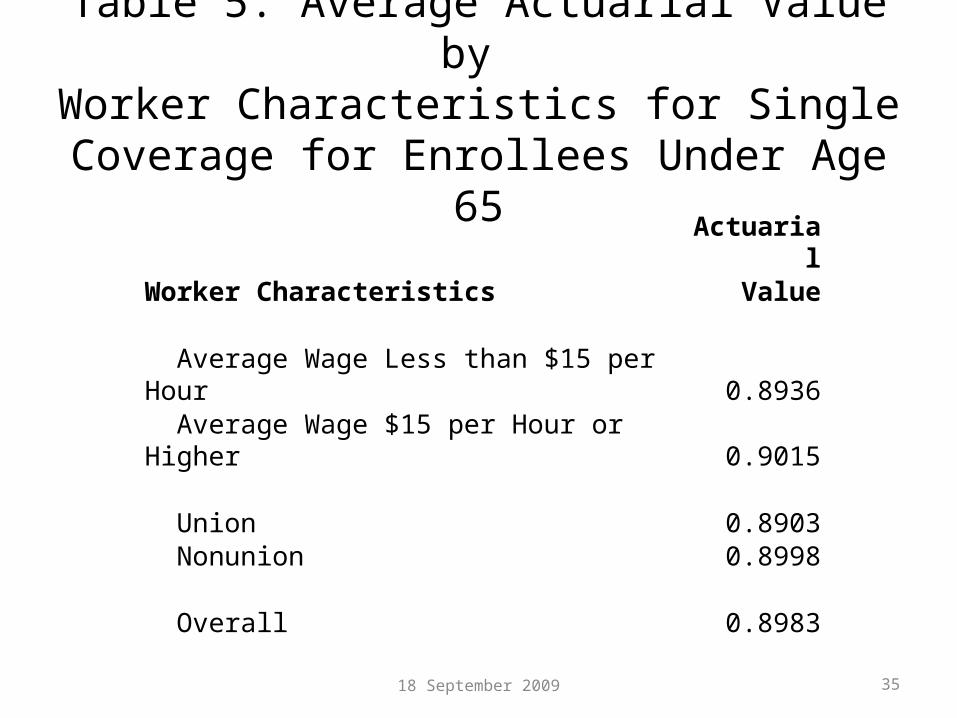

Table 5. Average Actuarial Value by Worker Characteristics for Single Coverage for

Enrollees Under Age 65

ActuarialWorker Characteristics Value

Average Wage Less than $15 per Hour 0.8936

Average Wage $15 per Hour or Higher 0.9015

Union 0.8903 Nonunion 0.8998

Overall 0.8983

18 September 2009 36

Table 6. Average Actuarial Value by Establishment Characteristics for Single Coverage

for Enrollees Under Age 65Actuarial

Establishment Characteristics Value

Fewer than 10 Workers 0.8687 10 to 24 Workers 0.9037 25 to 49 Workers 0.9036 50 to 99 Workers 0.8848 100 to 499 Workers 0.9000 500 to 999 Workers 0.8990

1000 Workers or More 0.9082

Overall 0.8983

18 September 2009 37

Policy Applications

18 September 2009 38

Policy Applications

• Minimum standards design

• Actuarial Value-based changes to tax exclusion (e.g., taxing of “Cadillac Plans”)

18 September 2009 39

Questions and Comments