17195344 Project Done ByRicha Vohra in Life Insurance Policy

32

A RESEARCH REPORT ON “CUSTOMER’S PERCEPTION TOWARDS LIFE INSURANCE POLICIES IN BHILAI-DURG” Submitted in partial fulfillment for the award of the degree Master of Business Administration Chhattisgarh Swami Vivekanand Technical University, Bhilai Submitted by, Richa Vohra MBA – Semester II (Section – B) (Session 2008-2009) Approved By, Dr. Sumita Dave HOD Guided By, Mr.Souren Sarkar Reader Shri Shankaracharya Institute of Management and Technology Junwani, Bhilai (C.G.) – 490020

-

Upload

anish-vyas -

Category

Documents

-

view

220 -

download

0

Transcript of 17195344 Project Done ByRicha Vohra in Life Insurance Policy

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 1/32

A

RESEARCH REPORT

ON

“CUSTOMER’S PERCEPTION TOWARDS LIFE INSURANCE

POLICIES IN BHILAI-DURG”

Submitted in partial fulfillment for the award of the degree

Master of Business Administration

Chhattisgarh Swami Vivekanand Technical University, Bhilai

Submitted by, Richa Vohra

MBA – Semester II (Section – B)

(Session 2008-2009)

Approved By,

Dr. Sumita Dave

HOD

Guided By,

Mr.Souren Sarkar

Reader

Shri Shankaracharya Institute of Management and Technology

Junwani, Bhilai (C.G.) – 490020

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 2/32

CERTIFICATE

This is to certify that the project “Customer’s perception towards life insurance policies in

Bhilai-Durg” submitted to Shri Shankaracharya Institute of Management & Technology,

Bhilai in partial fulfillment of the requirement for the award of Master of Business

Administration (MBA) is a bona fide work carried out by Richa Vohra (Session B), a student

of MBA II Sem, under my supervision and guidance.

Souren Sarkar

Reader,

SSIMT, Bhilai

Shri Shankaracharya Institute of Management and Technology

Junwani, Bhilai (C.G.) – 490020

[ii]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 3/32

DECLARATION

I Richa Vohra, a student of MBA II Semester 2008, at Shri Shankaracharya Institute of

Management & Technology hereby declare that this Project Report under the title

“Customer’s perception towards life insurance policies in Bhilai-Durg” is the record of

my original work under the guidance of Mr. Souren Sarkar. This report has never been

submitted to anywhere else for award of any degree/diploma.

Place: Bhilai Richa Vohra

Date : 30.03.2009 MBA – Semester II

[iii]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 4/32

ACKNOWLEDGEMENT

I would like to express our gratitude to all those who gave us the possibility to complete this

Research Work. I want to thank Shri Shankaracharya Institute of Management and

Technology for giving me the opportunity to carry out this Research Work in the first

instance, to do the necessary research work. I have furthermore to thank our Project Guide

Mr.Souren Sarkar who gave and confirmed us this Research and encouraged me to go

ahead with the Project and also for those valuable guidelines and support.

I would also like to thank all the faculty of the institute from whom I get lot of inputs and

help and support. It was a great experience and learns many

things which will help me in future.

Place: Bhilai Richa Vohra

Date : 30.03.2009 MBA – Semester II

[iv]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 5/32

TABLE OF CONTENTS

i. CERTIFICATE ii

ii. DECLARATION iii

iii. ACKNOWLEDGEMENT iv

iv. TABLE OF CONTENTS v

v. EXECUTIVE SUMMARY vi

1. INTRODUCTION Page No 1

2. LITERATURE REVIEW Page No 2-7

3. RESEARCH METHODOLOGY Page No 8

4. DATA ANALYSIS AND RESULTS Page No 9-18

5. INTERPRETATION OF FINDINGS Page No 19

6. RECOMMENDATIONS Page No 20

7. LIMITATIONS Page No 21

8. CONCLUSION Page No 22

vi. REFERENCES Page NO 23

vii. APPENDICES Page No 24

[v]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 6/32

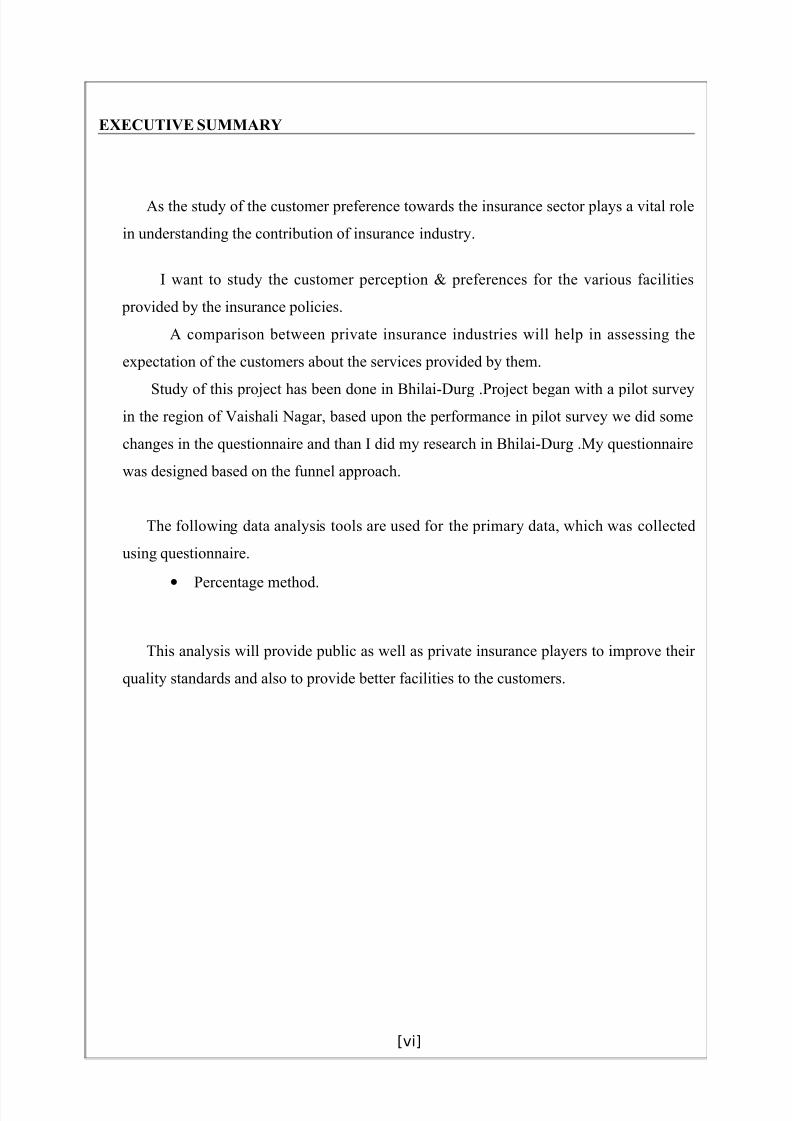

EXECUTIVE SUMMARY

As the study of the customer preference towards the insurance sector plays a vital role

in understanding the contribution of insurance industry.

I want to study the customer perception & preferences for the various facilities

provided by the insurance policies.

A comparison between private insurance industries will help in assessing the

expectation of the customers about the services provided by them.

Study of this project has been done in Bhilai-Durg .Project began with a pilot surveyin the region of Vaishali Nagar, based upon the performance in pilot survey we did some

changes in the questionnaire and than I did my research in Bhilai-Durg .My questionnaire

was designed based on the funnel approach.

The following data analysis tools are used for the primary data, which was collected

using questionnaire.

•

Percentage method.

This analysis will provide public as well as private insurance players to improve their

quality standards and also to provide better facilities to the customers.

[vi]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 7/32

INTRODUCTION

CUSTOMER PERCEPTION

Customer perceptions are dynamic. First of all, with the developing relationship between

customer and company, his perceptions of the company and its products or services will

change. The more experience the customer accumulates, the more his perceptions will shift

from fact-based judgments to a more general meaning the whole relationship gains for him.

Over time, he puts a stronger focus on the consequence of the product or service

consumption. Moreover, if the customers’ circumstances change, their needs and preferences

often change too. In the external environment, the offerings of competitors, with which a

customer compares a product or service will change, thus altering his perception of the best

offer around. Another point is that the public opinion towards certain issues can change. This

effect can reach from fashion trends to the public expectation of good corporate citizenship.

Shells intention to dump its Brent Spar platform into the ocean significantly altered many

customers perception of which company was worth buying fuel from. Research has been

donning on the impact of market share on the perceived quality of a product Depending on

the nature of the product and the customers’ preferences, increasing market share can have

positive or negative effects on how the customer perceives the product. In these days

customer perception is very important .When compared to customer perception of the

insurance company to other insurance company. The customer perception is showing the

problems of company. One company to other company will be show the difference of the

customer services like high quality, low price, offering door delivery service and sometimes

company offering free demo class regarding some electronic products. That’s why many

people are attracted to private organization.

Customer perception is an important component of our relationship with our customers.

[1]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 8/32

LITERATURE REVIEW

Brief History of the Insurance Sector in India

Insurance sector in India is one of the booming sectors of the economy and is growing at the

rate of 15-20 per cent annum. Together with banking services, it contributes to about 7 per

cent to the country's GDP. Insurance is a federal subject in India and Insurance industry in

India is governed by Insurance Act, 1938, the Life Insurance Corporation Act, 1956 and

General Insurance Business (Nationalization) Act, 1972, Insurance Regulatory and

Development Authority (IRDA) Act, 1999 and other related Acts.

The origin of life insurance in India can be traced back to 1818 with the establishment of the

Oriental Life Insurance Company in Calcutta. It was conceived as a means to provide for

English Widows. In those days a higher premium was charged for Indian lives than the non-

Indian lives as Indian lives were considered riskier for coverage. The Bombay Mutual Life

Insurance Society that started its business in 1870 was the first company to charge same

premium for both Indian and non-Indian lives. In 1912, insurance regulation formally began

with the passing of Life Insurance Companies Act and the Provident Fund Act.

By 1938, there were 176 insurance companies in India. But a number of frauds during 1920s

and 1930s tainted the image of insurance industry in India. In 1938, the first comprehensive

legislation regarding insurance was introduced with the passing of Insurance Act of 1938 that

provided strict State Control over insurance business.

Insurance sector in India grew at a faster pace after independence. In 1956, Government of

India brought together 245 Indian and foreign insurers and provident societies under one

nationalized monopoly corporation and formed Life Insurance Corporation (LIC) by an Act

of Parliament, viz. LIC Act, 1956, with a capital contribution of Rs.5 crore.

The (non-life) insurance business/general insurance remained with the private sector till

1972. There were 107 private companies involved in the business of general operations and

their operations were restricted to organized trade and industry in large cities. The General

Insurance Business (Nationalization) Act, 1972 nationalized the general insurance business in

India with effect from January 1, 1973. The 107 private insurance companies were

[2]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 9/32

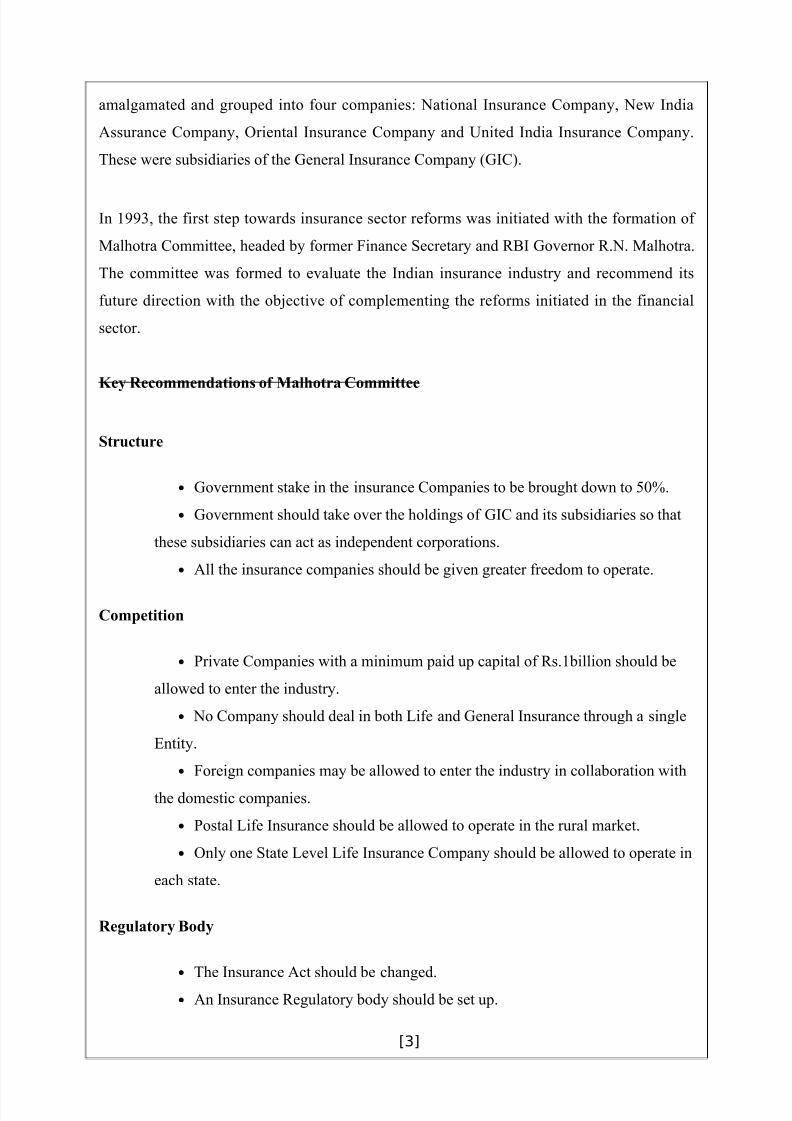

amalgamated and grouped into four companies: National Insurance Company, New India

Assurance Company, Oriental Insurance Company and United India Insurance Company.

These were subsidiaries of the General Insurance Company (GIC).

In 1993, the first step towards insurance sector reforms was initiated with the formation of

Malhotra Committee, headed by former Finance Secretary and RBI Governor R.N. Malhotra.

The committee was formed to evaluate the Indian insurance industry and recommend its

future direction with the objective of complementing the reforms initiated in the financial

sector.

Key Recommendations of Malhotra Committee

Structure

• Government stake in the insurance Companies to be brought down to 50%.

• Government should take over the holdings of GIC and its subsidiaries so that

these subsidiaries can act as independent corporations.

• All the insurance companies should be given greater freedom to operate.

Competition

• Private Companies with a minimum paid up capital of Rs.1billion should be

allowed to enter the industry.

• No Company should deal in both Life and General Insurance through a single

Entity.

• Foreign companies may be allowed to enter the industry in collaboration with

the domestic companies.

• Postal Life Insurance should be allowed to operate in the rural market.

• Only one State Level Life Insurance Company should be allowed to operate in

each state.

Regulatory Body

• The Insurance Act should be changed.

• An Insurance Regulatory body should be set up.

[3]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 10/32

• Controller of Insurance should be made independent.

Investments

• Mandatory Investments of LIC Life Fund in government securities to be

reduced from 75% to 50%.

• GIC and its subsidiaries are not to hold more than 5% in any company.

Customer Service

•

LIC should pay interest on delays in payments beyond 30 days• Insurance companies must be encouraged to set up unit linked pension plans.

• Computerization of operations and updating of technology to be carried out in

the insurance industry.

Malhotra Committee also proposed setting up an independent regulatory body - The

Insurance Regulatory and Development Authority (IRDA) to provide greater autonomy to

insurance companies in order to improve their performance and enable them to act as

independent companies with economic motives.

Insurance sector in India was liberalized in March 2000 with the passage of the Insurance

Regulatory and Development Authority (IRDA) Bill, lifting all entry restrictions for private

players and allowing foreign players to enter the market with some limits on direct foreign

ownership. There is a 26 percent equity cap for foreign partners in an insurance company.

There is a proposal to increase this limit to 49 percent. The opening up of the insurance sector

has led to rapid growth of the sector. Presently, there are 16 life insurance companies and 15

non-life insurance companies in the market. The potential for growth of insurance industry in

India is immense as nearly 80 per cent of Indian population is without life insurance cover

while health insurance and non-life insurance continues to be well below international

standards.

[4]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 11/32

Some of the important milestones in the life insurance business in India are:

185o – Non life insurance debuts with triton insurance company

1870 – Bombay mutual life assurance society is the first Indian owned Life insurer

1912 - The Indian Life Assurance Companies Act enacted as the first statute to regulate

the life insurance business.

1928 - The Indian Insurance Companies Act enacted to enable the government to collect

statistical information about both life and non-life insurance businesses.

1938 - Earlier legislation consolidated and amended to by the Insurance Act with the

objective of protecting the interests of the insuring public.

1956 - 245 Indian and foreign insurers and provident societies taken over by the central

government and nationalized. LIC formed by an Act of Parliament, viz. LIC Act, 1956, with

a capital contribution of Rs. 5 crore from the Government of India.

The General insurance business in India, on the other hand, can trace its roots to the Triton

Insurance Company Ltd., the first general insurance company established in the year 1850 in

Calcutta by the British.

Some of the important milestones in the general insurance business in India are:

1907 - The Indian Mercantile Insurance Ltd. set up, the first company to transact all classes

of general insurance business.

1957 - General Insurance Council, a wing of the Insurance Association of India, frames a

code of conduct for ensuring fair conduct and sound business practices.

[5]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 12/32

1968 - The Insurance Act amended to regulate investments and set minimum solvency

margins and the Tariff Advisory Committee set up.

1972 - The General Insurance Business (Nationalization) Act, 1972 nationalized the

general insurance business in India with effect from 1st Jan.

1973- insurers amalgamated and grouped into four company’s viz. the National Insurance

Company Ltd., the New India Assurance Company Ltd., the Oriental Insurance Company

Ltd. and the United India Insurance Company Ltd. GIC incorporated as a company.

[6]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 13/32

PRESENT SCENARIO - LIFE INSURANCE INDUSTRY IN INDIA

The life insurance industry in India grew by an impressive 47.38%, with premium income

at Rs. 1560.41 billion during the fiscal year 2006-2007.

Though the total volume of LIC's business increased in the last fiscal year (2006-2007)

compared to the previous one, its market share came down from 85.75% to 81.91%.

The 17 private insurers increased their market share from about 15% to about 19% in a

year's time. The figures for the first two months of the fiscal year 2007-08 also speak of the

growing share of the private insurers. The share of LIC for this period has further come down

to 75 percent, while the private players have grabbed over 24 percent.

With the opening up of the insurance industry in India many foreign players have entered

the market. The restriction on these companies is that they are not allowed to have more than

a 26% stake in a company’s ownership.

Since the opening up of the insurance sector in 1999, foreign investments of Rs. 8.7

billion have poured into the Indian market and 19 private life insurance companies have been

granted licenses.

Innovative products, smart marketing, and aggressive distribution have enabled fledgling

private insurance companies to sign up Indian customers faster than anyone expected.

Indians, who had always seen life insurance as a tax saving device, are now suddenly turning

to the private sector and snapping up the new innovative products on offer. Some of these

products include investment plans with insurance and good returns (unit. inked plans),multi-

purpose insurance plans, pension plans, child plans and money back plans.

.

[7]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 14/32

RESEARCH METHODOLOGY

Research Objectives :-

1 . To find out the customer’s reason towards investment in life insurance policies.

2. To identify major attributes which effects the decision making process of purchase of life

insurance policies.

3 .To identify major market players offering life insurance policies.

Data collection

There are two types of data collection method use in my project work report.

-Primary data

-Secondary data.

For my project, I decided on primary data collection method for observing customer

perception towards insurance and approaching customers directly in the field, comparing and

references to know their preference on insurance policies for my project throughquestionnaire.

I decided on secondary data collection method was used by referring to various websites,

books, magazines, journals and daily newspapers for collection information regarding project

under study

In my project, I decided primary data collection method because my study nature does not

permit to apply observational method. In survey approach .I selected a questionnaire method

for taking a customer view because it is feasible from the point of view of my subject &

survey purpose. I conducted 150 sample of survey in my project.

SAMPLE SIZE: - The sample size is 150

SAMPLING METHOD: - I used simple random sampling to collect the data.

[8]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 15/32

DATA ANALYSIS AND RESULTS

1. Number of life insurance policies customer holds:

Figure-1

.

NUMBER OF LIFE INSURANCE POLICIES OF POLICY HOLDER

7259

1550

10

20

30

40

50

60

70

80

0 to 1 2 to 3 4 to 5 5 and above

Series1

Interpretation :-

[9]

Option Number of respondents Percentage

0-1 72 48%

2-3 59 39%

4-5 15 10%

5&above 5 3%

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 16/32

Figure 1 shows that among 150 respondents, 48% are having 0-1 policies, 39% are having

2-3 policies, 10% are having 4-5 policies and 3% are having 5 or more policies. So, major

respondents are 0-1 policy holder.

2. Rationale behind holding the Life insurance policies:-

options Number of respondents Percentage

Tax saving instrument 111 7%

Necessity of life 9 6%

Both of the above 11 74%

Safety for loan 19 13%

Figure-2

RATIONALE BEHIND HOLDING THE LIFE INSURANCE P

7%6%

74%

13% TAX SA VING INSTRUME

NECESSITY OF LIFE FOR

SAFETY AND SECURITY

BOTH OF AB OVE

AS A SAF ETY FOR LOAN

Interpretation :-

Figure 2 shows that among 150 respondents, 111 i.e. (74%) consider insurance as tax

saving, safety and Security instrument and 19 i.e. (13%) consider it as for safety for a loan

and 11 i.e. (7%) consider it for tax saving and 9 i.e. (6%) consider it as a necessity of life for

[10]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 17/32

safety and security. So, most of the respondents consider it both as tax saving instrument and

as necessity of life for safety and security as rationale behind holding a life insurance policy.

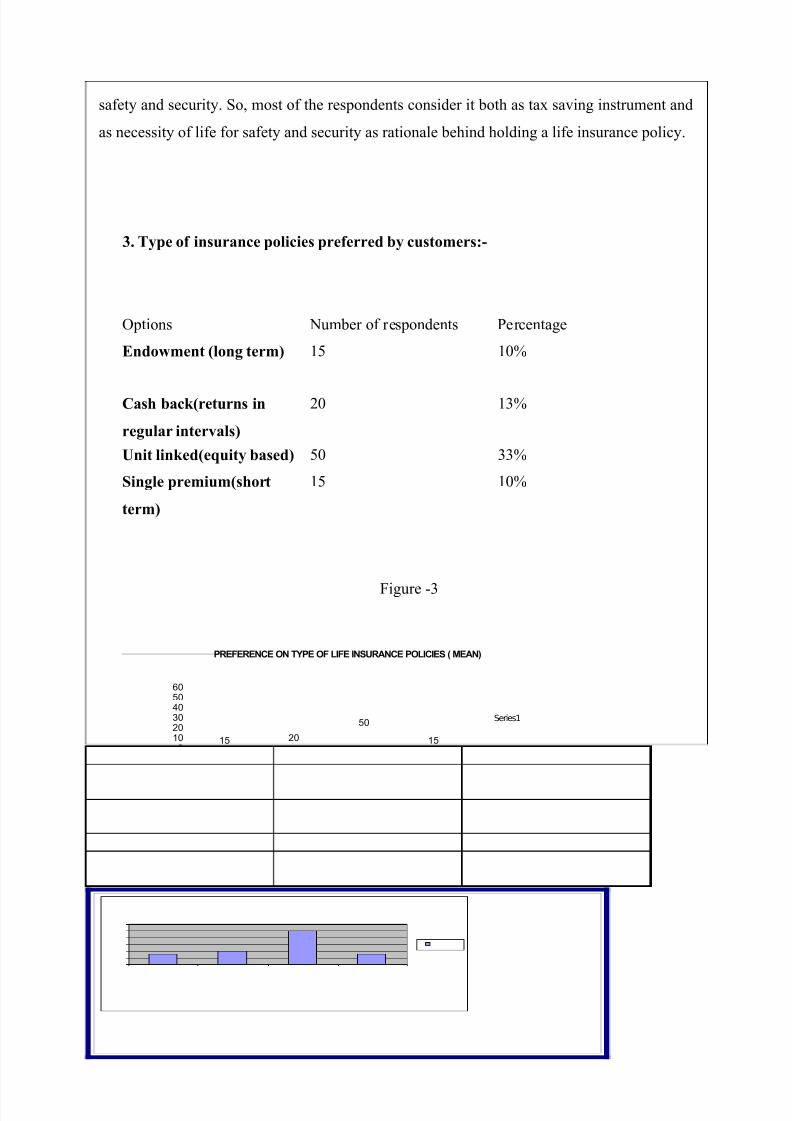

3. Type of insurance policies preferred by customers:-

Options Number of respondents Percentage

Endowment (long term) 15 10%

Cash back(returns in

regular intervals)

20 13%

Unit linked(equity based) 50 33%

Single premium(short

term)

15 10%

Figure -3

PREFERENCE ON TYPE OF LIFE INSURANCE POLICIES ( MEAN)

15 20

50

150

102030405060

ENDOWMENT

(LONG TERM)

CASH BACK(

RETURNS IN

REGULARINTERVALS)

UNIT LINKED(

EQUITY

BASED)

SINGLE

PREMIUM

Series1

Interpretation :-

[11]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 18/32

Figure 3 Figure 3 shows that among 150 respondents according to Mean taken most

preferred life insurance policy is Unit linked (Mean-50)

4. According to customer, what should be the moderate return from the investment

in the life insurance policies?

Option Number of respondents Percentage

Less than 5% 19 13%

5-8% 21 14%8-11% 43 29%

11&above 67 45%

Figure-4

RETURN FROM THE INVESTMENTS IN THE LIFE INSURA

POLICIES

19

21

43

67LESS THAN 5%

5-8%

8-11%

11% AND ABOVE

Interpretation :-

Figure 4 shows that among 150 respondents, 45% preferred a return of 11% and above,

29% liked to have a return of 8-11% while 14% and 13% respondents preferred it to be 5-8%

and less than 5% respectively. So, most preferred return from the investment in the life

insurance policies is 11% and above.

[12]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 19/32

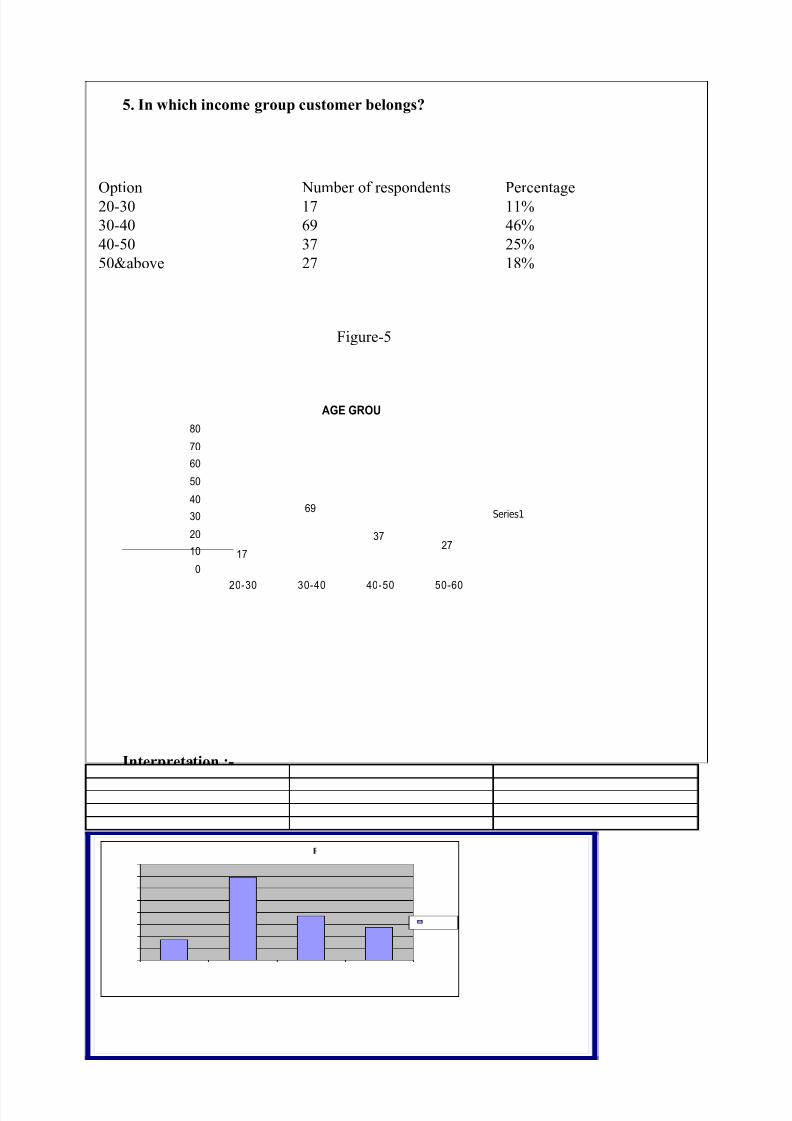

5. In which income group customer belongs?

Option Number of respondents Percentage

20-30 17 11%

30-40 69 46%

40-50 37 25%

50&above 27 18%

Figure-5

AGE GROU

17

69

3727

0

10

20

30

40

50

60

70

80

20-30 30-40 40-50 50-60

Series1

Interpretation :-

Figure 5, shows that among 150 respondents, 46% respondents are of the age group 30-40

years while 25% and 18% of respondents are of age group 40-50 and 50-60 years

respectively and only 11% belong to age group 20-30 years. So, maximum number of

respondents belongs to age group 30-40 years.

6. In which income group customer belongs?

[13]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 20/32

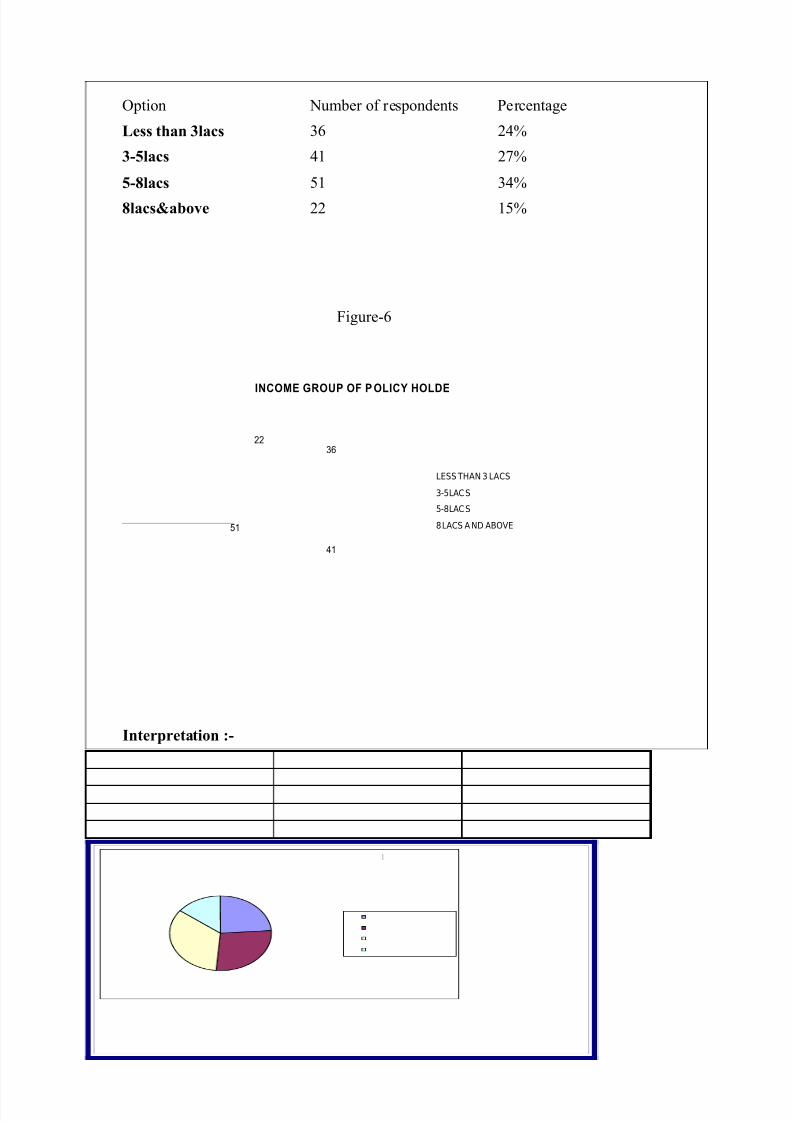

Option Number of respondents Percentage

Less than 3lacs 36 24%

3-5lacs 41 27%

5-8lacs 51 34%

8lacs&above 22 15%

Figure-6

INCOME GROUP OF P OLICY HOLDE

36

41

51

22

LESS THAN 3 LACS

3-5 LACS

5-8 LACS

8 LACS A ND ABOVE

Interpretation :-

Figure 6 shows that among 150 respondents, 34% belong to income group of 5-8 lacs

while 27% and 24% respondents are from income group 3-5 lacs and less than 3 lacs resp.

and only 15% respondents belong to income group 8 lacs and above. So, maximum no. of

respondents belongs to income group of 5-8 lacs

7. Sum total of insurance policies customer holds:

[14]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 21/32

option Number of respondents Percentage

Less than 50000 13 9%

50000-1lacs 77 51%

1-1.5lacs 29 19%

1.5&above 31 21%

Figure-7

SUM TOTAL OF INSURANCE POLICIES OF

POLICY HOLDERS

13

77

29 31

0

10

20

30

40

50

60

70

80

90

LESS THAN

50000

50000-100000 100000-

150000

150000 AND

ABOVE

Series1

.

Interpretation :-

. Figure 7 shows that among 150 respondents sum total of amount of insurance policy

premium of 51% policy holders is between 50,000-1 lac while for 21% and 19% policy

holders sum total of amount of insurance policy premium is 1.5 lacs and more and between 1

lac-1.5 lacs resp. and only 9% policy holders sum total of amount of insurance policy

premium is less than 50,000. So, maximum no. of policy holders are having sum total of

amount of insurance policy premium as 50,000-1 lac.

8. Type of life insurance policy customer prefers is recommended by.

Option Number of respondents PercentageFamily 80 53%

[15]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 22/32

Friends 40 27%

Advisor 20 13%

Others 10 7%

Figure-8

Interpretation :-

Figure -8 shows that among 150 respondents 53% respondents have taken life insurance

policies by the recommendation of family, 27% have taken by the recommendation of

friends, 13% & 7% by the recommendation of advisor &others, so maximum no. of life

insurance policies is recommended by family.

9. The customer have taken the life insurance policy through:

Option Number of respondents Percentage

Agent 96 64%

Online 14 9%

Self 23 15%Others 17 11%

[16]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 23/32

Figure-9

Interpretation:-

Figure-9 shows that among 150 respondents, 64% respondents have taken life insurance

policies through agent, 9% have taken through online, 15% & 11% have taken through self &

other means. So , maximum no. of respondents have taken through agent.

10 .Which companies provide better facility in the life insurance policy:

Option Number of respondents Percentage

LIC 34 23%

SBI LIFE 21 14%

HDFC 24 16%

HSBC 12 8%ICICI 54 36%

[17]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 24/32

OTHERS 5 3%

Figure-10

Interpretation :-

Figure-10 shows that among 150 respondents, 23% respondents thinks that LIC provides

better facilities, 14% & 16% thinks that SBI & HDFC provides better facilities, 8% & 3%

thinks that HDFC & others provides better facilities. So maximum no. of respondents

preferred ICICI for providing better facilities.

INTERPRETATION OF FINDINGS

• The buying of Life insurance policies is dependent on income.

• There is no impact of age on the rationale behind holding life insurance policy.

• Unit linked life insurance policy is preferred the most.

• Among 150 respondents maximum no. of policy holders are having sum total of

amount of insurance policy premium as 50,000-1 lac.

[18]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 25/32

• Among 150 respondents maximum no. of respondents belongs to income group of 5-

8 lacs.

• Most of the life insurance policies is recommended by the family of respondents.

•Among 150 respondents maximum number of respondents belongs to age group 30-40 years.

• Among 150 respondents most of the respondents consider life insurance both as tax

saving instrument and as necessity of life for safety and security as rationale behind

holding a life insurance policy.

• Among 150 respondents most preferred return from the investment in the life

insurance policies is 11% and above.

•According, to the customer major market player who offer better facilities in the lifeinsurance policies is ICICI .

• Most of the respondents have taken life insurance policies through agents.

[19]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 26/32

RECOMMENDATIONS

• Life insurance companies should be more reliable and stable towards their investors

by providing better facilities.

• Life insurance companies should give emphasis on their after-sale-service.

• The promotional activities of insurance companies should be good.

• Life insurance companies should provide the necessary information and the

importance of life insurance to the customers.

• They should adopt better marketing techniques to increase awareness among the

customers.

[20]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 27/32

LIMITATIONS

Some of the difficulties and limitations faced by me during my research work, which are as

follows:

• Lack of awareness among the people

• Bad image of the people towards Insurance sector

• Lack of awareness about the earning opportunity in the Insurance sector

• The sample size chosen for the questionnaire was only 150 and that may not

represent the true picture of the consumer perception about the Life Insurance sector.

• Customers do not like their money locked up for many years.

• Many people do not agree to fill the questionnaire because of lack of time

[21]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 28/32

CONCLUSIONS

I have come to know about the customer perception about the insurance sector and

how it varies with their age group and income.

The buying of Life insurance policies is dependent on income.

There is no impact of age on the rationale behind holding life insurance policy.

Unit linked life insurance policy is preferred the most.

• All the insurance company must advertise more in the market because not all

people know more about life insurance policy.

• Most number of people wants guaranteed returns so company must focus on this

for the customer investment.

The unit linked concept must be specifically promoted.

• People should not be afraid to invest money in insurance and must use it as an

effective tool for tax planning and long term.

[22]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 29/32

REFERENCES

TEXT BOOKS

1. PHILIP KOTLER (2001) ‘Marketing Management’, Prentice Hall

Pvt.Ltd., New Delhi, Millennium edition.

2. KOTHARI C.R. (1999) ‘Research Methodology’, Wishwa Prakashan,

New Delhi, 2nd edition.

3.LEON G. SCHFFMAN and LESLIE LAZAR KANUK (2007)

‘Consumer Behavior’, Prentice Hall Pvt.Ltd., New Delhi, 9th edition.

[23]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 30/32

APPENDICES

Questionnaire

Dear respondents,

I am a student of Shri Shankracharya institute of management & technology. As a part of

my curriculum I am conducting a study on “ CUSTOMER’S PERCEPTION TOWARDS

LIFE INSURANCE POLICIES IN BHILAI/DURG” It would be a great help if you please

spare some of your time to fill this questionnaire. The responses would be kept strictly

confidential & use to data analysis.

Q .1 Please tick the appropriate option.

Age 20-30 30-40 40-50 50&above

Annual income >3lacs 3-5lacs 5-8lacs 8&above

Q .2 Number of Life insurance policies you hold?

0-1 2-3

4-5 5& above

Q.3 According to you, what is the rationale behind holding the Life insurance policy?

(Please tick one)

As a tax instrument.

As a necessity of life for safety and security.

Both of the above.

[24]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 31/32

As a safety for loan.

Q .4 According to you, what should be the moderate return from the investment of the

life insurance policies?

Less than 5% 3-5%

8-11% 11%&above

Q .5 which type of life insurance policies do you prefer?

Endowment (long term)

Cash back(returns in regular intervals)

Unit linked(equity based)

Single premium(short term)

Q .6 what is the sum total of all life insurance policies you hold?

Less than 50,000 50,000-1lacs

1-1.5lacs 1.5&above

Q .7 How have you taken your life insurance policies?

Agent Online Self Others

Q .8 The life insurance policies you have taken is recommended by:

Family Friends Adviser Others

[25]

8/3/2019 17195344 Project Done ByRicha Vohra in Life Insurance Policy

http://slidepdf.com/reader/full/17195344-project-done-byricha-vohra-in-life-insurance-policy 32/32

Q .9 according to you which company provides better facilities in their life insurance

policies?

Please tick any one on the scale given below.

S.NO NAME OF BANKS

1. LIC

2. HDFC

3. HSBC

4. SBI LIFE

5. ICICI

6. OTHERS