160428 Gränges Q1 2016 Presentation · 2016 2015 Change Mar2016 Dec2015 Change...

14

First Quarter 2016 Earnings Conference 28 April, 2016

Transcript of 160428 Gränges Q1 2016 Presentation · 2016 2015 Change Mar2016 Dec2015 Change...

First Quarter 2016 Earnings Conference

28 April, 2016

2

Today’s presenters

JOHAN MENCKEL

CEO

Since: 2012Gränges since: 2004

OSKAR HELLSTRÖM

CFO

Since: 2011

2

3

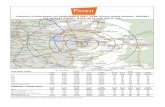

Gränges is the global leader with a market share of 20%

Sales and Technical support

Sales destinations

Percentage of sales volume FY 2015

FINSPÅNG,SWEDEN

SHANGHAI, CHINA

38%16% New York

Sao Paolo

Pune

Seoul

Tokyo

46%

4

� Sales volume increased by 5.7%

� Adjusted operating profit was unchanged at SEK 155 million

� Tailwind from favorable exchange rates was offset by negative price and mix effects and the aluminium premium price lag

� Earnings per share of SEK 1.25

� Cash flow before financingactivities of SEK -22 million

� Strong financial position

Summary Q1 2016 – Volume growth and stable profit

5

Source: IHS Automotive, April 11, 2016

Market growth of 3% expected for full year 2016

Light vehicle production growth (YoY)

Region

Asia

Europe

Americas

Global

Q1 2016 Q2 2016 outlook FY 2016 outlook

+1%

+2%

+1%

0%

+4%

+4%

+6%

+2%

+3%

+2%

+4%

+2%

6

Europe and North America show good growth whereas sales volume in Asia remained flat in the first quarter

Asia Europe Americas

� Increased sales to domestic heat exchanger producers in China

� Lower sales to costumers in other Asian markets

� Continued growth for heat exchanger materials

� Increased sales of scrap based products

� Higher contracted volumes with several customers

20.7 19.6 17.6 17.520.8

Q1 Q2 Q3 Q4 Q1

16.0 16.4 14.9 15.4 16.6

Q1 Q2 Q3 Q4 Q1

5.9 7.4 6.5 6.0 7.8

Q1 Q2 Q3 Q4 Q1

20162015

Gränges sales volume (ktonnes)

+0% +3%

+32%

20162015 20162015

7

2020 goal and strategy

� Grow significantly above the market rate

� Become the market leader in all geographical regions

� Maintain good and sustainable profitability

Drive growth throughinnovation

• Lead the development of heat exchanger materials

• Offer the most advanced solutions

• Be the preferred partner for our customers

Create value from sustainability

• Zero accident target• Reduce waste• Increase recycling• Ensure diversity• Be an attractive employer

Increase efficiencythrough continuous improvements

• Improve process stability• Increase productivity• Increase energy efficiency• Improve metal management

Grow presencethrough structural

expansion

• Add production capacity in North America

• Increase production capacity in Asia

• Expand into adjacent market segments

8

Volume growth and stable profit in first quarter

Rolling 12 months sales volume and adjusted operating profit

160 160 160 160 161 163 163 164 166

152 154 155159158

147 149 148

362 374348

372 371401

437 444463

521 528 541 541494

245199

286

100

120

140

160

180

200

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q150

150

250

350

450

550 Adjusted operating profit (SEK million)

Sales volume (ktonnes)

Sales Volume Adjusted Operating Profit

2012 2013 2014 2015 2016

9

1. Adjusted for items affecting comparability.2. Basic, historical earnings per share has been calculated on the same number of shares as of today.

Volume growth and stable profit in first quarter

SEK million Q1

Financial overview

Rolling 12 months

2016 2015 Change Mar 2016 Dec 2015 Change

Sales volume (ktonnes) 45.1 42.7 5.7% 166.4 163.9 1.5%

Net sales 1,360 1,456 -6.6% 5,398 5,494 -1.7%

Adjusted operating profit1 155 155 0.3% 541 541 0.1%

Adjusted operating margin (%) 11.4 10.6 0.8 ppt 10.0 9.8 0.2 ppt

Adjusted operating profit per tonne (kSEK) 3.4 3.6 -0.2 3.3 3.3 -

Operating profit 155 155 0.3% 539 538 0.1%

Profit for the period 94 111 -15.9% 361 379 -4.7%

Earnings per share2 (SEK) 1.25 1.49 -0.24 4.84 5.07 -0.24

Cash flow before financing activities -22 -1 n/a 579 600 -3.5%

Return on capital employed, R12 (%) 18.2 18.1 0.1 ppt

Net debt / adjusted EBITDA, R12 0.4 0.4 -

10

206

-154

-60-19

-14-316

-275

-400

-300

-200

-100

0

Cash flow before financing -22

Net debt was SEK 316 million at the end of the first quarter

Change in net debt

Net debt position (SEK million)

Net debtQ4 2015

Adjusted EBITDA

Change in working capital

Other operating items

Investments & divestments of fixed assets

FX & other Net debtQ1 2016

0.4 0.4

Net debt over adjusted EBITDA (rolling 12 months)

11

� Global Light Vehicle Production is expected to grow 4.2%1 in Q2 2016

� Gränges’ sales volume is expected to develop in line with the market during Q2 2016

� The aluminium premium has stabilised and is not expected to have any substantial effect on profitability for the remainder of 2016

� For full year 2016 global Light Vehicle Production is expected to grow 3.0%1

with growth expected in all geographical regions

� Positive outlook for 2016 – more stableconditions in China

� Price competition in Asia is expected to have some impact this year

Outlook

1Source: HIS Automotive, April 11, 2016

12

� A solid quarter with good sales growth and stable earnings

� Sales volume increased by 5.7%

� Adjusted operating profitstable at SEK 155 million

� Solid financial position

� Well positioned for profitable growth

Summary of first quarter

Q&AJohan Menckel, CEO

Oskar Hellström, CFO