16 April 2021 4QFY21 Results Preview Autos & Logistics

11

16 April 2021 4QFY21 Results Preview Autos & Logistics HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters Diverging growth outlook After the initial outperformance by the auto stocks, the sector returns are converging with those of the broader market due to moderating domestic growth trends across 2Ws and commodity-based inflation. OEMs expect an impact of ~300bps due to the rising base metal prices, which will limit the extent of margin expansion from improving leverage (as demand normalises over FY22-23E). Amidst this backdrop, we prefer stocks that have a diversified revenue model such as Tata Motors, Bharat Forge, and Bajaj Auto. We also have a BUY rating on Maruti Suzuki due to the sustained demand for PVs, given the shift towards personal mobility. Commodity inflation to impact 4QFY21 profitability: The commodity prices over the past six months are up sharply - aluminum (+26%), copper (+32%), crude (+55%), steel (+55%). In our discussion with Bajaj Auto, the company highlighted that the impact on margins will be 300-400bps. Most OEMs are highlighting similar views, with margin impact varying between 200-400bps due to the above. While OEMs will benefit from improved operating leverage as volumes normalise over FY22-23E, the extent of margin improvement will be contained due to the above. Demand revival – differing trends are emerging: Sales recovery trends have been mixed in 4Q, with PV and tractor demand remaining resilient while 2W sales have been tepid, particularly at the entry level (refer to our note: Divergent Trends in PVs and 2Ws). We believe the recovery in autos is a ‘K’ shaped one, where the COVID impact (closure of education institutes and dine-ins, weak SME activity, etc.) is affecting the lower end consumer segment. CV sales are recovering, though the expected benefit from the scrappage scheme will now be spread over FY22-24. Sector returns are converging with the broader market: The NIFTY Auto index returns in 4Q (+7% QoQ) has performed largely in line with the broader index (+5% QoQ) as commodity cost inflation and moderating growth trends across 2Ws have tempered stock price returns, after strong outperformance in 1HFY21. We believe that returns will be stock specific, going ahead, as the recovery is getting factored in (valuations are elevated) and growth rates are now diverging across segments. After several quarters, we have lowered estimates for FY22/23E due to the above factors. Key recommendations: We are positive on Bajaj Auto, Tata Motors, and Maruti amongst the OEMs. We have recently downgraded Hero to an ADD due to the moderating growth outlook. Amongst auto ancillaries, we have initiated on Bharat Forge with a BUY rating due to an improving outlook for global CVs as well as diversification initiatives (particularly in the defence segment). We continue to prefer Subros amongst domestic auto ancillaries due to its dominant presence in the car AC segment as well as expansion in the home and railway AC segment. Logistic companies: The rail-based logistic companies expect the benefits from the DFC to reflect from 2HFY22 as the 650km stretch from Rewari (Haryana) to Palanpur (Gujarat) will be commissioned by Apr-May. We reiterate our preference for Gateway Distriparks (BUY) as CONCOR (ADD) will have to contend with higher LLF charges levied by the Indian railways. CMP (INR/sh) * Reco Ashok Leyland 112 REDUCE Bajaj Auto 3,601 BUY Eicher 2,412 REDUCE Escorts 1,218 ADD Hero Moto 2,863 ADD Mahindra 805 ADD Maruti 6,652 BUY Tata Motors 304 BUY Amara Raja 802 ADD Bharat Forge 574 BUY Endurance 1,295 BUY Gulf Oil 706 BUY Subros 301 BUY Sundram 700 ADD CONCOR 565 ADD Gateway 176 BUY *CMP as of 15 th Apr-21 NIFTY Auto index Source: Bloomberg, HSIE Research; indexes rebased to 100 Aditya Makharia [email protected] +91-22-6171-7316 Mansi Lall [email protected] +91-22-6171-7357 80 100 120 140 160 180 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 NIFTY NIFTY AUTO

Transcript of 16 April 2021 4QFY21 Results Preview Autos & Logistics

16 April 2021 4QFY21 Results Preview

Autos & Logistics

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

Diverging growth outlook After the initial outperformance by the auto stocks, the sector returns are

converging with those of the broader market due to moderating domestic

growth trends across 2Ws and commodity-based inflation. OEMs expect an

impact of ~300bps due to the rising base metal prices, which will limit the

extent of margin expansion from improving leverage (as demand normalises

over FY22-23E). Amidst this backdrop, we prefer stocks that have a diversified

revenue model such as Tata Motors, Bharat Forge, and Bajaj Auto. We also

have a BUY rating on Maruti Suzuki due to the sustained demand for PVs,

given the shift towards personal mobility.

Commodity inflation to impact 4QFY21 profitability: The commodity

prices over the past six months are up sharply - aluminum (+26%), copper

(+32%), crude (+55%), steel (+55%). In our discussion with Bajaj Auto, the

company highlighted that the impact on margins will be 300-400bps. Most

OEMs are highlighting similar views, with margin impact varying between

200-400bps due to the above. While OEMs will benefit from improved

operating leverage as volumes normalise over FY22-23E, the extent of

margin improvement will be contained due to the above.

Demand revival – differing trends are emerging: Sales recovery trends

have been mixed in 4Q, with PV and tractor demand remaining resilient

while 2W sales have been tepid, particularly at the entry level (refer to our

note: Divergent Trends in PVs and 2Ws). We believe the recovery in autos

is a ‘K’ shaped one, where the COVID impact (closure of education institutes

and dine-ins, weak SME activity, etc.) is affecting the lower end consumer

segment. CV sales are recovering, though the expected benefit from the

scrappage scheme will now be spread over FY22-24.

Sector returns are converging with the broader market: The NIFTY Auto

index returns in 4Q (+7% QoQ) has performed largely in line with the

broader index (+5% QoQ) as commodity cost inflation and moderating

growth trends across 2Ws have tempered stock price returns, after strong

outperformance in 1HFY21. We believe that returns will be stock specific,

going ahead, as the recovery is getting factored in (valuations are elevated)

and growth rates are now diverging across segments. After several quarters,

we have lowered estimates for FY22/23E due to the above factors.

Key recommendations: We are positive on Bajaj Auto, Tata Motors, and

Maruti amongst the OEMs. We have recently downgraded Hero to an ADD

due to the moderating growth outlook. Amongst auto ancillaries, we have

initiated on Bharat Forge with a BUY rating due to an improving outlook for

global CVs as well as diversification initiatives (particularly in the defence

segment). We continue to prefer Subros amongst domestic auto ancillaries

due to its dominant presence in the car AC segment as well as expansion in

the home and railway AC segment.

Logistic companies: The rail-based logistic companies expect the benefits

from the DFC to reflect from 2HFY22 as the 650km stretch from Rewari

(Haryana) to Palanpur (Gujarat) will be commissioned by Apr-May. We

reiterate our preference for Gateway Distriparks (BUY) as CONCOR (ADD)

will have to contend with higher LLF charges levied by the Indian railways.

CMP

(INR/sh) * Reco

Ashok Leyland 112 REDUCE

Bajaj Auto 3,601 BUY

Eicher 2,412 REDUCE

Escorts 1,218 ADD

Hero Moto 2,863 ADD

Mahindra 805 ADD

Maruti 6,652 BUY

Tata Motors 304 BUY

Amara Raja 802 ADD

Bharat Forge 574 BUY

Endurance 1,295 BUY

Gulf Oil 706 BUY

Subros 301 BUY

Sundram 700 ADD

CONCOR 565 ADD

Gateway 176 BUY

*CMP as of 15th Apr-21

NIFTY Auto index

Source: Bloomberg, HSIE Research;

indexes rebased to 100

Aditya Makharia

+91-22-6171-7316

Mansi Lall

+91-22-6171-7357

80

100

120

140

160

180A

pr-

20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar-

21

Ap

r-21

NIFTY NIFTY AUTO

Page | 2

Autos & Logistics: 4QFY21E Results Preview

4QFY21E earnings preview

Volume (in units '000) NET SALES (INR bn) EBITDA margin (%) APAT (INR bn) Adj. EPS (INR)

4Q

FY21E

QoQ

(%)

YoY

(%)

4Q

FY21E

QoQ

(%)

YoY

(%)

4Q

FY21E

QoQ

(bps)

YoY

(bps)

4Q

FY21E

QoQ

(%)

YoY

(%)

4Q

FY21E

3Q

FY21

4Q

FY20

AUTOS

Ashok

Leyland 44 32 73 63.8 32 66 10.3 507 558 4.2 1,475 3,577 1.4 0.1 0.0

Bajaj Auto 1,170 (10) 18 79.6 (11) 17 18.0 (140) (37) 15.1 (3) 15 52.3 53.8 45.3

Eicher 205 2 25 28.7 2 30 23.7 (3) 416 6.0 12 96 21.8 19.5 11.2

Escorts 33 3 62 20.3 0 47 16.9 (117) 279 2.6 (7) 86 25.9 27.8 13.9

Hero Moto 1,568 (15) 18 79.3 (19) 27 12.7 (173) 215 8.5 (22) 36 42.3 54.3 31.1

Mahindra 202 (10) 33 124.6 (11) 38 15.9 (112) 222 13.9 (21) 330 11.6 14.6 2.7

Maruti 492 (1) 28 231.3 (1) 27 9.8 28 127 17.2 (11) 33 56.9 64.3 42.8

Tata Motors 192 21 89 181.5 24 87 7.6 16 NA 0.0 (0) (0) 0.0 (1.6) (5.8)

Aggregate 3,905 (9) 23 809.0 1 41 12.0 (55) 320 67.4 2 251

Source: Company, HSIE Research

NET SALES (INR mn) EBITDA margin (%) APAT (INR mn) Adj. EPS (INR)

4Q

FY21E

QoQ

(%)

YoY

(%)

4Q

FY21E

QoQ

(bps)

YoY

(bps)

4Q

FY21E

QoQ

(%)

YoY

(%)

4Q

FY21E

3Q

FY21

4Q

FY20

AUTO ANCS

Amara Raja 18,390 (6) 16 15.3 (30) (4) 1,612 (17) 18 9.4 11.3 8.0

Bharat Forge 10,832 5 23 22.3 156 978 1,282 31 522 2.8 2.1 0.4

Endurance 19,967 (2) 25 16.3 (97) 139 1,666 (17) 56 11.8 14.3 7.6

Gulf Oil 4,941 3 37 16.8 (54) 135 579 (10) 61 11.6 12.9 7.2

Subros 6,426 6 40 10.6 (34) 156 271 (1) 68 4.2 4.2 2.5

Sundram Fasteners 11,113 0 34 19.5 (127) 473 1,304 (9) 139 6.2 6.8 2.6

Source: Company, HSIE Research

NET SALES (INR mn) EBITDA margin (%) APAT (INR mn) Adj. EPS (INR)

4Q

FY21E

QoQ

(%)

YoY

(%)

4Q

FY21E

QoQ

(bps)

YoY

(bps)

4Q

FY21E

QoQ

(%)

YoY

(%)

4Q

FY21E

3Q

FY21

4Q

FY20

LOGISTICS

CONCOR 19,225 10 23 20.5 (70) (975) 2,617 10 (15) 4.3 3.9 5.1

Gateway Distriparks 3,358 7 12 22.7 (362) 116 175 (47) 56 1.6 3.0 1.0

Source: Company, HSIE Research

Page | 3

Autos & Logistics: 4QFY21E Results Preview

Autos and Auto ancillaries

COMPANY 4QFY21

OUTLOOK WHAT’S LIKELY KEY MONITORABLES

Ashok Leyland GOOD

Volumes for the quarter came in at 44k units,

+32% QoQ (+73% YoY due to lower base).

This was led by demand recovery in the

MHCV segment.

Revenue is expected to grow 32/66%

QoQ/YoY, from a low base.

EBITDA margin is expected at 10.3%

(+500bps QoQ) owing to improved operating

leverage. We expect the company to report a

profit of INR 4bn vs INR 267/114mn

QoQ/YoY.

Market share gains in the LCV segment –

new product response

Recovery trends in MHCVs

Impact of scrappage scheme on CVs

Bajaj Auto AVERAGE

Volumes in the quarter are up 18% YoY due

to a lower base. However, it declined 10%

QoQ.

Operating margins are expected at 18% (-

140/35bps QoQ/YoY) due to increased

commodity costs.

PAT at INR 15bn to decline 3% QoQ.

Outlook on exports, particularly to the

African continent

Three-wheeler outlook in the Indian market

Updates on PLI scheme and benefits for

Bajaj Auto

Eicher Motors AVERAGE

RE volumes grew 2.5% QoQ to 205k units

(163k units YoY).

We expect revenue at INR 28.7bn (+2%

QoQ).

EBITDA margin at 23.7%, (similar to QoQ).

PAT growth of 12% QoQ to INR 5.9bn.

Progress on the production ramp-up

Demand trends for the new product-Meteor

Escorts GOOD

Volumes grew by 3% QoQ to 32.6k units

(20k units YoY).

We expect revenue to be flat QoQ. EBITDA

margins to contract by 120bps QoQ to 16.9%

owing to commodity cost led pressure.

PAT at INR 2.6bn to decline by 7% QoQ

(INR 1.4mn YoY).

Progress/plans of the recently

commissioned plant with Kubota

Impact of Agri reforms on the farm

segment

Hero

MotoCorp AVERAGE

Volumes for Hero declined 15% QoQ (+18%

YoY) to 1.5mn units.

We expect a revenue decline of 19% QoQ.

EBITDA margin at 12.7% (-175bps QoQ due

to cost pressures).

PAT at INR 8.5bn to decline 22% QoQ, +36%

YoY.

Market share trends in the premium

segment – response to Xtreme 160cc

Inventory levels

Mahindra AVERAGE

Total volumes (including tractors) declined

10% QoQ. Revenue is expected to have a

similar decline.

EBITDA margin at 15.9% to contract by

110bps QoQ.

PAT decline of 21% QoQ to INR 13.9bn.

Outlook for demand in tractors

Amidst rising competition in the SUV

segment, timelines on the launch of XUV

500

Further update on the impact of exit from

Ford JV / SsangYong stake sale

Source: HSIE Research

Page | 4

Autos & Logistics: 4QFY21E Results Preview

COMPANY 4QFY21

OUTLOOK WHAT’S LIKELY KEY MONITORABLES

Maruti Suzuki AVERAGE

We expect a revenue decline of 1% QoQ

owing to a similar decline in volumes.

EBITDA margin at 9.8% to expand 30bps

QoQ.

PAT to decline by 12% QoQ to INR 17bn

(vs12.9bn YoY).

Demand trends – particularly that of

entry-level cars

Status of model availability and waiting

periods thereof

Capacity utilization post the 3rd phase of

Gujarat plant getting commissioned

Tata Motors GOOD

Standalone: Volumes grew by 22/89%

QoQ/YoY. We expect standalone revenues to

grow by 24% QoQ to INR 181bn. EBITDA

margin of 7.6% (+20bps QoQ, EBITDA loss

YoY).

We expect JLR to report an EBITDA margin

at 13.5% (vs 15.8/4.8% QoQ/YoY)

Progress on the EV platforms, especially in

terms of hybrids.

Impact of lockdown on the near term on

volumes

Impact of scrappage scheme on CVs

Amara Raja

Batteries AVERAGE

We expect a revenue decline of 6% QoQ to

INR 18bn (vs INR 15.8bn YoY).

EBITDA margin at 15.3% to contract by

30bps QoQ.

PAT decline of 17% QoQ to INR 1.6bn (vs

INR 1.3bn YoY).

Impact of tightening pollution norms

(draft Battery Waste Management rules,

2020)

Initiatives to expand beyond conventional

LAB segment

Bharat Forge GOOD

We expect revenue to grow by 5% QoQ due

to improved CV sales.

EBITDA margin at 22.3% to expand 160bps

QoQ.

PAT at INR 1.28bn to expand by 31% QoQ.

US class 8 truck trends

Any update on defence sector orders

Endurance

Technologies AVERAGE

We expect consolidated revenue to decline

by 2% QoQ to Rs 19.9bn.

EBITDA margin at 16.3% to contract by

100bps QoQ owing to cost pressure.

PAT at INR 1.66bn to decline by 17% QoQ.

Market share gains by Endurance – update

on new order wins

Outlook on industry growth trends

Gulf Oil AVERAGE

We expect revenue to grow by 2.5% QoQ.

Operating margin at 16.8% to contract by

50bps QoQ.

We expect PAT decline of 10% QoQ to INR

579mn (vs INR 359mn YoY).

Volume outlook in the DEO segment

RM price trends as oil prices are now

firming up

Subros GOOD

We expect revenues to grow by 6% QoQ.

Operating margin to contract by 30bps QoQ

to 10.6%.

We expect PAT to decline by 1% QoQ to INR

271mn.

Expectations for demand pick up in the

passenger vehicle segment

The demand outlook for the home AC

business and any benefits from the PLI

scheme

Page | 5

Autos & Logistics: 4QFY21E Results Preview

COMPANY 4QFY21

OUTLOOK WHAT’S LIKELY KEY MONITORABLES

Sundram

Fasteners GOOD

We expect consolidated revenue to be flat

QoQ.

Operating margin at 19.5% to contract by

125bps QoQ.

We expect PAT decline of 9% QoQ.

Demand outlook in both India as well as

overseas markets

Any possible impact of separation from

the TVS group

Source: HSIE Research

Logistics

COMPANY 4QFY21

OUTLOOK WHAT’S LIKELY KEY MONITORABLES

Container

Corporation AVERAGE

We expect revenue to grow by 10% QoQ due

to similar growth in volumes. Volumes were

supported by a revival in domestic traffic.

EBITDA margin is expected at 20.5% (-70bps

QoQ)

We expect PAT to grow by 7/15% QoQ/YoY

to INR 2bn.

Impact of higher LLF payout to the Indian

Government on profitability.

Gateway

Distriparks GOOD

We expect consolidated revenues to grow by

7/12% QoQ/YoY.

Operating margin at 22.7% to contract by

360bps QoQ, +115bps YoY.

We expect PAT at INR 175mn (-47% QoQ,

+56% YoY).

Update on commissioning of the DFC

Margin/Volume gains as CONCOR raises

its charges due to the revised LLF

Source: HSIE Research

Change in estimates and target price

Coverage

companies

Old

Rating

New

Rating

Old

TP

(INR)

New

TP ^

(INR)

Old target

multiple

New target

multiple

Old EPS (INR) New EPS (INR) % change

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

Ashok Leyland # REDUCE REDUCE 97 108 11x

EV/EBITDA

11x

EV/EBITDA 0.1 3.8 5.2 -0.3 4.0 5.7 NA 6 8

Bajaj Auto BUY BUY 4,250 4,145 20x 20x 162.5 179.5 211.6 163.6 180.5 207.2 1 1 -2

Eicher REDUCE REDUCE 2,600 2,400

23x core

business

16x VECV

23x core

business

16x VECV

56.8 87.4 115.2 54.8 81.7 109.5 -4 -7 -5

Hero Motocorp ADD ADD 3,350 3,350 17.5x 17.5x 147.7 172.0 192.1 147.3 171.2 191.0 -0 -0 -1

M&M ADD ADD 880 880 14x core

business

15x core

business 40.5 42.7 50.7 37.6 39.2 47.4 -7 -8 -7

Maruti Suzuki BUY BUY 9,000 8,440 27x 27x 156.7 260.6 332.6 158.4 245.0 312.5 1 -6 -6

Tata Motors # BUY BUY 315 360

11x

EV/EBITDA

Standalone

11x

EV/EBITDA

Standalone

-13.3 3.3 14.0 -13.2 4.2 16.6 -1 27 19

Amara Raja ADD ADD 1,000 910 19x 19x 36.2 44.0 52.5 36.2 40.4 47.8 0 -8 -9

Bharat Forge BUY BUY 720 700 32x 32x 5.2 12.5 22.5 5.2 12.5 21.8 - - -3

Endurance BUY BUY 1,680 1,565 30x 30x 36.3 45.8 55.9 36.3 44.0 52.2 -0 -4 -7

Gulf Oil BUY BUY 880 870 20x 20x 37.8 40.7 44.0 39.6 41.2 43.5 5 1 -1

Subros BUY BUY 410 405 22x 22x 5.4 13.2 18.6 7.4 13.4 18.4 37 2 -1

Gateway

Distriparks # BUY BUY 165 200

9x

EV/EBITDA

Rail

business

10x

EV/EBITDA

Rail

business

4.1 5.2 7.4 5.2 6.3 8.4 28 20 13

Source: Company, HSIE Research, #valued on EV/EBITDA, ^FY23E TP

Page | 6

Autos & Logistics: 4QFY21E Results Preview

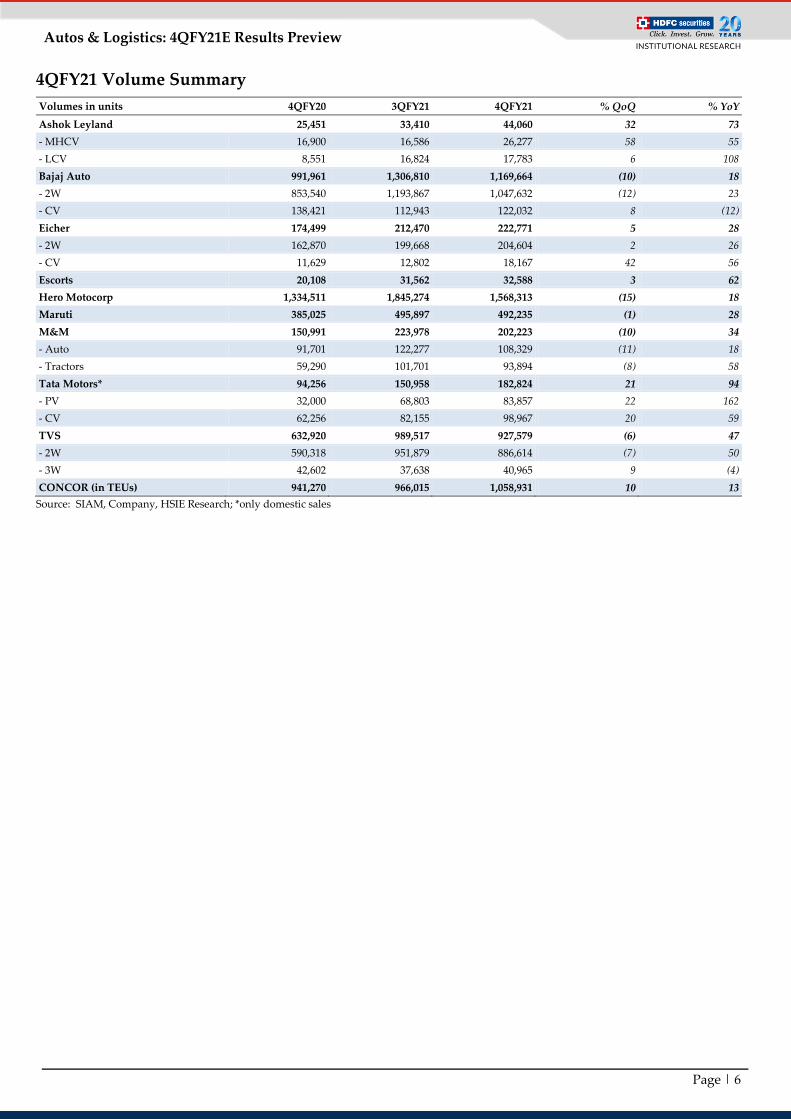

4QFY21 Volume Summary

Volumes in units 4QFY20 3QFY21 4QFY21 % QoQ % YoY

Ashok Leyland 25,451 33,410 44,060 32 73

- MHCV 16,900 16,586 26,277 58 55

- LCV 8,551 16,824 17,783 6 108

Bajaj Auto 991,961 1,306,810 1,169,664 (10) 18

- 2W 853,540 1,193,867 1,047,632 (12) 23

- CV 138,421 112,943 122,032 8 (12)

Eicher 174,499 212,470 222,771 5 28

- 2W 162,870 199,668 204,604 2 26

- CV 11,629 12,802 18,167 42 56

Escorts 20,108 31,562 32,588 3 62

Hero Motocorp 1,334,511 1,845,274 1,568,313 (15) 18

Maruti 385,025 495,897 492,235 (1) 28

M&M 150,991 223,978 202,223 (10) 34

- Auto 91,701 122,277 108,329 (11) 18

- Tractors 59,290 101,701 93,894 (8) 58

Tata Motors* 94,256 150,958 182,824 21 94

- PV 32,000 68,803 83,857 22 162

- CV 62,256 82,155 98,967 20 59

TVS 632,920 989,517 927,579 (6) 47

- 2W 590,318 951,879 886,614 (7) 50

- 3W 42,602 37,638 40,965 9 (4)

CONCOR (in TEUs) 941,270 966,015 1,058,931 10 13

Source: SIAM, Company, HSIE Research; *only domestic sales

Page | 7

Autos & Logistics: 4QFY21E Results Preview

Monthly volumes (in units)

Ashok Leyland: Demand is supported by recovery in

MHCV volumes

Bajaj Auto: Volume momentum sustaining due to

demand from the exports markets (54% of vols in 4Q)

Source: SIAM, Company, HSIE Research Source: SIAM, Company, HSIE Research

Royal Enfield: Volumes sustaining at 66k+ levels per

month

Hero: Volume growth has moderated over the past few

months

Source: SIAM, Company, HSIE Research Source: SIAM, Company, HSIE Research

Escorts: Tractor sales continue to witness healthy

momentum

Maruti Suzuki: Company is expanding capacity

Source: SIAM, Company, HSIE Research Source: SIAM, Company, HSIE Research

-

3,000

6,000

9,000

12,000

15,000

18,000

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

-

50,000

100,000

150,000

200,000

250,000

300,000

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

-

20,000

40,000

60,000

80,000

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

-

150,000

300,000

450,000

600,000

750,000

900,000

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

-

3,000

6,000

9,000

12,000

15,000

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

-

50,000

100,000

150,000

200,000

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Page | 8

Autos & Logistics: 4QFY21E Results Preview

Commodity prices forming up

Brent crude Lead

Source: Bloomberg, HSIE Research Source: Bloomberg, HSIE Research

Copper Aluminium

Source: Bloomberg, HSIE Research Source: Bloomberg, HSIE Research

Steel prices

Source: Steelmint, HSIE Research

10

30

50

70

90

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

Mar

-21

Brent price ($/bbl)

1,600

1,800

2,000

2,200

2,400

2,600

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

Mar

-21

Lead Price ($)

4,000

6,000

8,000

10,000

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

Mar

-21

Copper Price ($)

1,200

1,600

2,000

2,400M

ar-1

6

Mar

-17

Mar

-18

Mar

-19

Mar

-20

Mar

-21

Aluminium Price ($)

Page | 9

Autos & Logistics: 4QFY21E Results Preview

Index and stock price performance

Index/Stock Market price as of

31st Mar-21

% return

3M 6M 1Y

NIFTY 14,691 5% 31% 71%

NIFTY Auto 9,862 7% 25% 108%

Ashok Leyland 114 19% 53% 164%

Bajaj Auto 3,671 7% 27% 82%

Eicher 2,604 3% 18% 99%

Escorts 1,288 2% -2% 94%

Hero Motocorp 2,914 -6% -7% 83%

Mahindra 795 10% 31% 179%

Maruti Suzuki 6,859 -10% 2% 60%

Tata Motors 302 64% 126% 325%

Source: Bloomberg, HSIE Research

Ashok Leyland 1-yr forward

EV/EBITDA

Bajaj Auto 1-yr forward P/E band Eicher Motors 1-yr forward P/E

band

Source: Bloomberg, Company, HSIE Research

Escorts 1-yr forward P/E band Hero Motocorp 1-yr forward P/E

band

M&M 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

0

5

10

15

20

25

30

35

Ma

r-1

4

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

EV/EBITDA Mean

8

12

16

20

24

Ma

r-1

0

Ma

r-1

1

Ma

r-1

2

Ma

r-1

3

Ma

r-1

4

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

PE Mean

+1 SD -1 SD

20

25

30

35

40

Ma

r-1

5

Sep

-15

Ma

r-1

6

Sep

-16

Ma

r-1

7

Sep

-17

Ma

r-1

8

Sep

-18

Ma

r-1

9

Sep

-19

Ma

r-2

0

Sep

-20

Ma

r-2

1

P/E Mean

+1 SD -1 SD

5

10

15

20

Ma

r-1

6

Sep

-16

Ma

r-1

7

Sep

-17

Ma

r-1

8

Sep

-18

Ma

r-1

9

Sep

-19

Ma

r-2

0

Sep

-20

Ma

r-2

1

P/E Mean

+1 SD -1 SD

6

12

18

24

Ma

r-0

7M

ar-

08

Ma

r-0

9M

ar-

10

Ma

r-1

1M

ar-

12

Ma

r-1

3M

ar-

14

Ma

r-1

5M

ar-

16

Ma

r-1

7M

ar-

18

Ma

r-1

9M

ar-

20

Ma

r-2

1

PE Mean

+1 SD -1 SD

0

5

10

15

20

25

30

Ma

r-0

7M

ar-

08

Ma

r-0

9M

ar-

10

Ma

r-1

1M

ar-

12

Ma

r-1

3M

ar-

14

Ma

r-1

5M

ar-

16

Ma

r-1

7M

ar-

18

Ma

r-1

9M

ar-

20

Ma

r-2

1P/E Mean

+1 SD -1 SD

Page | 10

Autos & Logistics: 4QFY21E Results Preview

Maruti Suzuki 1-yr forward P/E

band

Amara Raja 1-yr forward P/E band Bharat Forge 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

Endurance 1-yr forward P/E band Gulf Oil 1-yr forward P/E band Subros 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

Sundram Fasteners 1-yr forward P/E

band

CONCOR 1-yr forward P/E band

Source: Bloomberg, Company, HSIE Research

5

15

25

35

45

Ma

r-0

7M

ar-

08

Ma

r-0

9M

ar-

10

Ma

r-1

1M

ar-

12

Ma

r-1

3M

ar-

14

Ma

r-1

5M

ar-

16

Ma

r-1

7M

ar-

18

Ma

r-1

9M

ar-

20

Ma

r-2

1

P/E Mean+1 SD -1 SD

0

10

20

30

40

Ma

r-0

9

Ma

r-1

0

Ma

r-1

1

Ma

r-1

2

Ma

r-1

3

Ma

r-1

4

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

P/E Mean+1 SD -1 SD

0

20

40

60

80

Ma

r-1

1

Ma

r-1

2

Ma

r-1

3

Ma

r-1

4

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

P/E Mean+1 SD -1 SD

15

20

25

30

35

40

Ma

r-1

7

Sep

-17

Ma

r-1

8

Sep

-18

Ma

r-1

9

Sep

-19

Ma

r-2

0

Sep

-20

Ma

r-2

1

P/E Mean

+1 SD -1 SD

10

15

20

25

30

Ma

r-1

5

Sep

-15

Ma

r-1

6

Sep

-16

Ma

r-1

7

Sep

-17

Ma

r-1

8

Sep

-18

Ma

r-1

9

Sep

-19

Ma

r-2

0

Sep

-20

Ma

r-2

1

PE Mean

+1 SD -1 SD

5

15

25

35

Ma

r-1

3

Ma

r-1

4

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

P/E Mean

+1 SD -1 SD

0

10

20

30

40

50

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

P/E Mean

+1 SD -1 SD

10

20

30

40

50

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Mar-

17

Mar-

18

Mar-

19

Mar-

20

Mar-

21

P/E Mean

+1 SD -1 SD

Page | 11

Autos & Logistics: 4QFY21E Results Preview

HDFC securities

Institutional Equities

Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park,

Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Board: +91-22-6171-7330 www.hdfcsec.com

Disclosure:

We, Aditya Makharia, CA & Mansi Lall, MBA, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report

accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also

certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC

Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication

of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest.

Any holding in stock –YES

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is solely for information of the recipient only. The report must not be used as a singular basis of any investment

decision. The views herein are of a general nature and do not consider the risk appetite or the particular circumstances of an individual investor; readers are requested to

take professional advice before investing. Nothing in this document should be construed as investment advice. Each recipient of this document should make such

investigations as they deem necessary to arrive at an independent evaluation of an investment in securities of the companies referred to in this document (including merits

and risks) and should consult their own advisors to determine merits and risks of such investment. The information and opinions contained herein have been compiled or

arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty,

representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without

notice. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete. HSL is not obliged to update this report for such

changes. HSL has the right to make changes and modifications at any time.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident

or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation

or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to the attention

of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or indirectly, for any purposes or in any manner.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or

the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk.

It should not be considered to be taken as an offer to sell or a solicitation to buy any security.

This document is not, and should not, be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report should not

be construed as an invitation or solicitation to do business with HSL. HSL may from time to time solicit from, or perform broking, or other services for, any company

mentioned in this mail and/or its attachments.

HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the

company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in

the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of

interests with respect to any recommendation and other related information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any

action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates , diminution in the NAVs,

reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the

report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this

report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for

any other assignment in the past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this

report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other

advisory service in a merger or specific transaction in the normal course of business.

HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the

research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our

Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may have issued other reports that are

inconsistent with and reach different conclusion from the information presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject

company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East),

Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066 Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600 HDFC

Securities Limited, SEBI Reg. No.: NSE, BSE, MSEI, MCX: INZ000186937; AMFI Reg. No. ARN: 13549; PFRDA Reg. No. POP: 11092018; IRDA Corporate Agent

License No.: CA0062; SEBI Research Analyst Reg. No.: INH000002475; SEBI Investment Adviser Reg. No.: INA000011538; CIN - U67120MH2000PLC152193

Rating Criteria

BUY: >+15% return potential

ADD: +5% to +15% return potential

REDUCE: -10% to +5% return potential

SELL: > 10% Downside return potential