15.905 Technology (&) Strategy - MIT SDM – System Design...

45

15.905 Technology (&) Strategy 15.905 Technology (&) Strategy SDM UltraLite for 2007 System Design & Management Conference: Cogitate, (re) Connect & Collaborate Michael A M Davies Broad Institute (via WebEx) Thursday 18 October 2007

Transcript of 15.905 Technology (&) Strategy - MIT SDM – System Design...

15.905 Technology (&) Strategy

15.905 Technology (&) StrategySDM UltraLite for 2007 System Design & ManagementConference: Cogitate, (re) Connect & CollaborateMichael A M DaviesBroad Institute (via WebEx)Thursday 18 October 2007

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 2

15.905 Technology (&) Strategy

Agenda for today

• A (very) brief introductionto the course

– introductions– objectives– overview

• A couple of key takeaways– Ten sessions in

ten minutes?– 142 slides…

• Hot topics– my perspective– your feedback

• The “state of the art” intechnology (&) strategy

• Acknowledgements• Follow up, contact

information andOpenCourseware

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 3

15.905 Technology (&) Strategy

Michael A M Davies

• From New Zealand,educated in the UK, livedin US >10 years

• 2 Masters in Engineering

• ~20 years ago, got veryinterested in howhigh-tech businessesmake strategic decisions

• …did an MBA at LondonBusiness School

• Worked in industry• Founded (and sold)

consulting business thatworks for tech businesses

• Recently working closelywith faculty from MITSloan (and elsewhere)

• …and teach NewTechnology Ventures,consult, and start-up CTO

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 4

15.905 Technology (&) Strategy

This course provides a framework for thestrategic management of technology businesses

• Complex• Dynamic - and unstable• Uncertain

• Co-evolution oftechnological innovation,demand opportunities andbusiness ecosystems

• Value creation andvalue capture

• Ways of thinking• Mental models

• Bring clarity tocomplexity

• Insights and anticipation• Better decisions

• Improve (significantly)the odds of success

Technology businesses This course

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 5

15.905 Technology (&) Strategy

It uses both cases and presentations, focusedon domains in which systems are important

• Products part of larger andmore complex systems

• Computing• Communications

– mobile– IP

• Consumer electronics• Industrial networking• Automotive• Aerospace

• not so much biotechor pharmaceuticals• Products are comprised

of multiple (sub-)systems

Apple iPod

iTunes

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 6

15.905 Technology (&) Strategy

What is business strategy?

• Pursuing choices amongst competing options– a different system of activities that creates unique

value and captures it– not operational effectiveness or improvement

• Planned and intended, pursued and realized– deliberate– emergent

• Pattern recognition– building the prepared mind– capable of making sound decisions

Michael Porter, “What is Strategy”, Harvard Business Review, November-December 1996, pages 61-78Henry Mintzberg, “Crafting Strategy”, July-August 1987, pages 66-74

Sarah Kaplan, “The Real Value of Strategic Planning”, MIT Sloan Management Review, Winter 2003, pages 71-76

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 7

15.905 Technology (&) Strategy

Why is technology (really, really) important?

• Technologicalinnovation driveseconomic growth

– why we can be heretoday

– why we no longerlive in caves

– escaping theMalthusian trap

– explaining howeconomies grow

• Get it wrong - waste alot of money andpeople’s lives

• Get it right - create(a lot of) wealth,capture (some of) it -and have fun

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 8

15.905 Technology (&) Strategy

Economic growth accelerated dramatically byIndustrial Revolution - 50x to 150x time faster

Brad de Long, “Estimates of World GDP, One Million BC - Present”Robin Hanson, “Long-Term Growth As a Sequence of Exponential Modes”

Gunnar Eliason, “The Role of Knowledge in Economic Growth”

Swedish Manufacturing Output(1875 = 100) World Average GDP per Capita

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 9

15.905 Technology (&) Strategy

Knowledge and technological innovation nowrecognized as engines driving economic growth

• “Output per hour worked in the United States [in 1990] is 10times a valuable as output per hour worked 100 years ago.”

• “Technological change - improvement in the instructions formixing together raw materials - lies at the heart of economicgrowth”

• “Technological change arises in large part because ofintentional actions taken by people who respond to marketincentives.”

• “[I]nstructions for working with raw materials are inherentlydifferent from other economic goods. Once the cost of creatinga new set of instructions has been incurred, the instructionscan be used over and over again at no additional cost.”

Paul Romer, “Endogenous Technological Change”, The Journal of Political Economy, October 1990, pages S71-S102Paul Romer, “Increasing Returns and Long-Run-Growth”, The Journal of Political Economy, 1986, pages 1002-1037

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 10

15.905 Technology (&) Strategy

Technology strategy (very often)determines who survives and thrives

• IBM (mainframecomputers)

• Sun Microsystems

• Matsushita, and manyothers (VHS)

• Sony (transistor radios)• Nikon (in semiconductor

capital equipment)• Canon (in photocopiers)• Canon, Nikon and others• Nokia

• DEC, Wang, Unisys andmany others

• Apollo Computer andothers

• Sony (Betamax)

• RCA• Cobilt, Canon,

Perkin-Elmer and GCA• Xerox• Polaroid and Kodak• Motorola

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 11

15.905 Technology (&) Strategy

A roadmap for the course

Technologicalinfrastructure

Demandopportunity

Co-evolution,life-cycles,epochs andtransitions

Businessecosystems,niches andco-opetition

Value creation,value capture

andinimitability

DDeciding

and Delivering

Ambiguity andscenarios,uncertainty

and realoptions

BPatterns of

change

CCapturing

Value

AIntroduction

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 12

15.905 Technology (&) Strategy

DemandOpportunity

BusinessEcosystem

TechnologicalInfrastructure

Time

Customers

Applications orOutcomes

Markets

Offer Partners

Technology Partners

t

Turning Points

t

Step changes

x

Trajectory shifts(disruption)

y

OperationsMarketingInnovationManagement

ArchitecturalShifts

Value Creationversus

Value Capture

Underlying drivers of time behaviour (dynamics)• customers and applications (vs products)• activities and processes (vs organization)

Connections or linkages, feedback loops (+ and -)

Framework

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 13

15.905 Technology (&) Strategy

Technological innovations and their diffusionresult in a characteristic life-cycle

DemandOpportunity

BusinessEcosystem

TechnologicalInfrastructure

Earlyferment

Dominantdesign

emerges

Eclipseor

renewal

Make it work -innovate on

performance,diverse

integrativedesigns

MaturityIncrementalinnovation

Figure out theoptimal

architecture,drive down

costs, make iteasy to use

Broaden theoffer, rationalize

the portfolio,build up

complementaryassets

Develop broadportfolio, build

platforms,search for new

options

Many entrants- diversebusinessmodels

Decisivebattles forleadership

Intensifyingcompetition,

earlyconsolidation

Fiercecompetition,consolidationaround majors

and minors

Lead users,early adopters- high payoff,low switching

costs

Earlymainstream -usability, cost

more important

Mainstreamcustomers -soft factors,aesthetics

Saturation,segmentation,customization

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 14

15.905 Technology (&) Strategy

Radicalinnovation

Technological innovation and the diffusion ofinnovations cause transitions

Time

Performance

Ferment

FermentDominant

design

Incrementalinnovation

Incrementalinnovation

• Incrementalinnovationinvolvesrelativelyminor changes

• Radicalinnovation isbased ondifferentengineeringand scientificprinciples

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 15

15.905 Technology (&) Strategy

How can you make good decisions, whenconflict is likely?

Common goals• collaborativeproblem solving• inquiry rather

than advocacy

Balanced power• value diversity

• cultivateminority views• fair process

• leverage expertcounsel

Focus on issues• not a slow

regular (annual)cycle

• not byorganizational(business) unit

Debate anddecide

• not review andapprove

• facts, optionsand choices

• More, rather thanless, objective and

timelyinformation, focus

on the facts

• Consider several(>2 ➔ ~4-5)

options together

• Make surestrategic decisions

consistent withone another andwith execution

• Make it fun!• inject humorinto the process

Resolutionwithout

consensus• collectiveownership

• dissent andrevisit

Context Agenda Outcome

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 16

15.905 Technology (&) Strategy

Three basic types of decision, with increasingrisks and levels of commitment

No-regretsmoves

• worth doing anyway• positive payoffs in

most scenarios

(Real) options

• positive payoffin some outcomes

• otherwise,small cost to play

• parallel or sequential

Big bets

• work in somescenarios

• high cost, negativeeffects in other cases

A

B

A1

A2B

✓✓

✓✓

✓

✓✓✓

X Y

A

B

A1

A2B $£€¥

Increasing risk

Increasing investment and commitment

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 17

15.905 Technology (&) Strategy

It’s not just big decisions - the tough part ismiddle ground - neither strategic nor tactical

Important decisions,many and growing innumber, too many for

top-level, not yethandled well

Strategic

TacticalFew Many

A few major strategicchallenges, top-levelsponsorship, one-offinitiatives, teams madeof up of best people

Many tactical decisionscan (and should) be

delegated for fast localdecision-making and

execution in local units

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 18

15.905 Technology (&) Strategy

So, what are hot topics in technology (&)strategy, presenting decision-making challenges

• Open innovation and open source– modularity– Linux– architecture and platform competition

• Aesthetics and usability– elegance– ease of use

• Portfolio, product and pipeline management– overload– the tyranny of choice– feature fatigue

• Decision-making in R&D– Toyota– real options– evidence-based decision-making and experimentation

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 19

15.905 Technology (&) Strategy

Let’s begin being clear about what we mean byportfolio management

• “How should the business most effectively invest its researchand development (R&D) and new product resources? That’swhat portfolio management is all about: resource allocation toachieve the business’s new product and technology objectives.”

– a dynamic decision process whereby a business’s list of activenew product (and R&D) projects is constantly updated andrevised

– new projects are evaluated, selected and prioritized– existing projects may be accelerated, killed or deprioritized– resources are allocated and reallocated to active projects– includes

• periodic reviews of the total portfolio of all projects• making go/kill decisions on individual projects on an

ongoing basis• developing a new product strategy for the business

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 20

15.905 Technology (&) Strategy

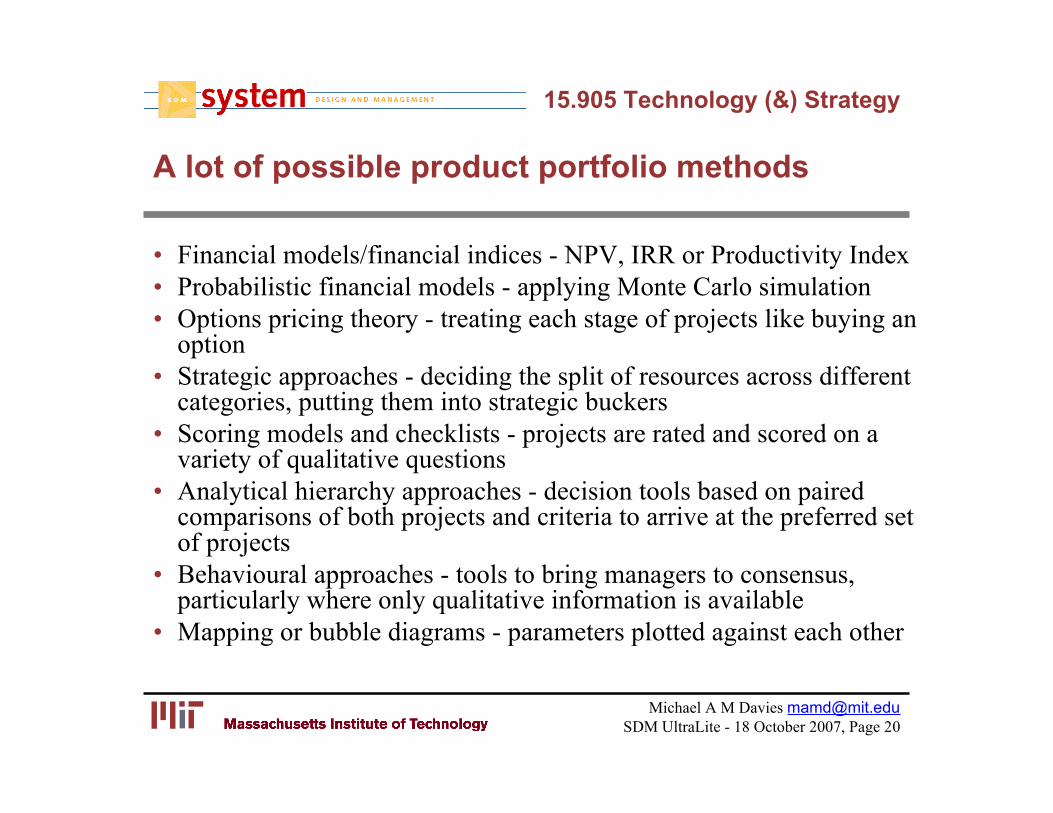

A lot of possible product portfolio methods

• Financial models/financial indices - NPV, IRR or Productivity Index• Probabilistic financial models - applying Monte Carlo simulation• Options pricing theory - treating each stage of projects like buying an

option• Strategic approaches - deciding the split of resources across different

categories, putting them into strategic buckers• Scoring models and checklists - projects are rated and scored on a

variety of qualitative questions• Analytical hierarchy approaches - decision tools based on paired

comparisons of both projects and criteria to arrive at the preferred setof projects

• Behavioural approaches - tools to bring managers to consensus,particularly where only qualitative information is available

• Mapping or bubble diagrams - parameters plotted against each other

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 21

15.905 Technology (&) Strategy

So, what actually gets used…

2.7%20.9%Checklists

13.3%37.9%Scoring models

5.3%40.6%Bubble diagrams

26.6%64.8%Business strategymethods

40.4%77.3%Financial methods

DominantUsedMethod

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 22

15.905 Technology (&) Strategy

Real - and growing - unhappiness, anddemonstrated success with alternative approaches

• Too many projects– wasted resources– overload

• Poor balance of projects– too much “momentum”– not enough real

innovation• Late or lacking deliverables

– schedule slippage– scope creep

• Confusing portfolios• Over-complex products

• Some real successes withmuch more limitedportfolios

• New approaches tomanaging pipeline

– Samsung– Toyota

• Simpler products withfewer features beating morecomplex products

– Apple iPod– SlingBox– TiVo

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 23

15.905 Technology (&) Strategy

So, how should we think about product, portfolioand pipeline management for high-tech products

Let’s go shopping!

How does thisproduct compare

to what I’vealready got?

And how do Inow feel aboutmy purchase,now that I’m

using it?

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 24

15.905 Technology (&) Strategy

Customers have two (very different) approachesto shopping behaviour - making choices

“Maximizers”– always aim to make the

best possible choices– more product comparisons,

before and after makingdecisions

– take longer to decide what tobuy

– spend more time comparingtheir decisions with others

– but greatest maximizers areleast happy with their efforts– unfortunately, get little

pleasure from knowing theydid better

– very unhappy if they didworse

“Satisficers”– aim for “good enough”

– even if there might still bebetter choices out there

Barry Schwartz and others,“Maximizing Versus Satis!cing:

Happiness Is a Matter of Choice”,Journal of Personality and Social PsychologyVolume 83, No. 5, pages 1178–1197 (2002)

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 25

15.905 Technology (&) Strategy

How do you know if you are a “maximizer”

1 Whenever I’m faced with a choice, I try to imagine what all the otherpossibilities are, even ones that aren’t present at the moment

2 No matter how satisfied I am with my job, it’s only right for me to be onthe lookout for better opportunities

3 When I’m listening to the radio, I often check other stations to see ifsomething better is playing, even if I’m satisfied with what’s playing

4 When I watch TV, I channel surf, often scanning though the availableoptions even while attempting to watch one program

5 I treat(ed) relationships like clothing; I {expect to try|tried} a lot onbefore finding the perfect fit

6 I often find it difficult to shop for a gift for a friend7 Renting videos is really difficult; I’m always struggling to pick the best8 When shopping, I have a hard time finding clothing that I really love9 I find that writing is very difficult, because it’s so hard to word things just

right; I often do several drafts of even simple things10 I’m a big fan of Top 10 lists

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 26

15.905 Technology (&) Strategy

Several psychological challenges arise fromhaving too much choice

• Quality of a choice cannot be assessed in isolation from alternatives– one of the costs of more choice is losing the opportunities of

other options - more options = greater opportunity cost– the more alternatives there are, deeper the sense of loss– worse for a maximizer than for a satisficer

• People may also suffer regret about the option that they settle on– depends on how much one feels personal responsibility– also depends on how easy it is to imagine a better alternative

(in particular, such as a subsequent successor product)• And…adaptation dulls joy, so very little in life turns as good as

we expect it to be– enthusiasm about positive experience does not sustain itself– costs associated with choice get amortized over the life of the

decision

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 27

15.905 Technology (&) Strategy

Too many choices can make people feel worsethan no choices at all

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 28

15.905 Technology (&) Strategy

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 29

15.905 Technology (&) Strategy

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 30

15.905 Technology (&) Strategy

John Gourville, “Eager Sellers and Stony Buyers”, Harvard Business Review, June 2006, pages 98-106

So, why do customers fail to buy innovativeproducts even when they’re better?

• First, newproducts requirebehaviourchanges

– transactioncosts

– learning costs– obsolescence

costs• This is what

Everett Rogerscharacterised ascompatibility andcomplexity

• And, more importantly,they imposepsychological costs

– evaluate attractiveness of alternativebased not on objective value but onsubjective, perceived value

– consumers evaluate products relative toa reference point, usually a product thatthey already own

– people value relative improvement as again, and treat all shortcomings relativeto reference point as losses

– losses have a far greater impact thansimilarly sized gains - “loss aversion”

– people value things they have,much more than those they don’t

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 31

15.905 Technology (&) Strategy

Loss aversion - people value things they havemore than (new) things that they don’t (yet) have

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 32

15.905 Technology (&) Strategy

John Gourville, “Eager Sellers and Stony Buyers”, Harvard Business Review, June 2006, pages 98-106

Customers value what they own, but may have togive up, much more than what they don’t own

• First, give coffee mugs to agroup of people

• Then, ask those who ownthem - Sellers - at whatprice point ($0.25 - $9.00)they would be willing topart with their mugs

• At the same time, askanother group - Choosers -who have not been giveneither coffee mugs ormoney, whether they wouldchoose the mug or themoney at each price point

• For both groups - “Sellers and“Choosers” - it’s the samechoice:

– coffee mug | money• However, they value the

coffee mugs very differently:– Sellers @ $7.00-$7.12– Choosers @ $3.12-$3.50

• Typically, people demandtwo to four times (2-4x) asmuch compensation to giveup products they alreadypossess as they are willing topay to own them

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 33

15.905 Technology (&) Strategy

John Gourville, “Eager Sellers and Stony Buyers”, Harvard Business Review, June 2006, pages 98-106

“Status quo bias” - why people tend to stick withwhat they have, even if better alternative exists

• Ask a first group to choosebetween a large bar of Swisschocolate and an attractivecoffee mug

• Give a second group the mug,and a short time later givethem the opportunity toexchange the mug for thechocolate bar

• Give chocolate bars to a thirdgroup and much later alloweach student to exchange hisor her chocolate bar for a mug

• And it intensifies over time…

• 56% chose the mug, 44%chose the chocolate bar - anear even split

• Only 11% wanted to change

• Only 10% wanted to change

• …other researchers found thatthe bias rises over time to afactor of approximately four

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 34

15.905 Technology (&) Strategy

There is also a trade-off amongst number offeatures, usability and behaviour change

Mercedes-Benz had packed its cars with electronic features, causingimportant parts to malfunction and making testing …more expensive.Many features were also unnecessary or annoying to drivers. For instance,the ability to store …preferred seat position in the car key frustrated driverswho borrowed their spouse’s key, … triggered the spouse’s preferredsettings, and could no longer access their own seat position.[F]rustrated product owners, …spread the word of their dissatisfaction...BMW[‘s] 7 Series cars feature the complicated iDrive system, which…offers about 700 capabilities requiring multifunction displays andmultistep operations— even for functions that formerly required the twistof a knob or the !ick of a switch. …sales of the 7 Series in the UnitedStates in the "rst half of 2005 were downabout 10% relative to the sameperiod in 2004.The Bosch Benvenuto B30 espresso and coffee machine, for instance,doesn’t stop at delivering a demitasse; its digital screen asks the user toselect from 12 drink options and to make myriad decisions about energy-saving modes, timer programming, and water hardness settings.

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 35

15.905 Technology (&) Strategy

Roland Rust,Debora Viana Thompson and Rebecca Hamilton,

“Defeating Feature Fatigure”,Harvard Business Review, February 2006, pages 98-106

Challenges even when and where features bothdeliver additional functionality and are familiar

• Businesses find themselves“tacking features ontoproducts that make themharder to use”

– perception incrementalcost of each feature is low

– may be cheaper to do fewfeature-rich products thantargeted products withfewer features

– lead users notrepresentative

– economic assumption thateach positive attributeincreases utility,and hencelikely market share

• Recent research sheds light– customers understand this

trade-off– but when it’s time to

choose, value capabilitymore highly than usability

– both when choosingamongst extant products,and when customizing

– however, once customershave used a product, theirpreferences change andusability matters verymuch

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 36

15.905 Technology (&) Strategy

We are our own worst enemies….

• Present participants with threemodels of a digital videoplayer or audio player

– rate their own expertise– rate each of 3 models (7,

14 or 21 features) oncapabilities and usability

– 62.3% chosehigh-feature models

• Ask them to choose featuresfrom a list of 25 possibilities

– 19.6 features on average– more than 50% took

more than 80% (21 ormore) of possiblefeatures

• Ask participants to evaluatethe product after use

– ask them to evaluatecapability and usability,and to provide an overallevaluation

– after use, only 44% whohad used the high-featuremodel chose it, even oncethey had invested inlearning how to use it

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 37

15.905 Technology (&) Strategy

Adding features improves initial attractivenessbut decreases customers’ satisfaction

• What looks attractive in prospect does not necessarily look good inpractice

– many will require service support, and return the product, ifthey can

– and customers will take their business elsewhere in future– and will not drive widespread diffusion

• We can do something about this– consider long-term customer equity and not just initial choices– where products have too many features in a bid to address

heterogeneity, tailor products with limited feature sets ofcapabilities for various targets

– design products that do one thing very well• Change the way we do and use market research

– use prototypes and other low-cost experiments– do much more product-in-use research

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 38

15.905 Technology (&) Strategy

It is possible to optimize the features for initialsales, word of mouth or lifetime value

• Highest number of featuresmaximises initial sales, ascustomers value capability morehighly than usability

• These products do not maximisetheir long-term satisfaction,propensity for repeat purchase andword-of-mouth to drive epidemicadoption

• Customers’ lifetime value isoptimized when we get the balanceright between more features to driveinitial sales and fewer features todrive long-term satisfaction

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 39

15.905 Technology (&) Strategy

Portfolio transformation

• (Too) manymainstreamproducts

• Unclear choices• (Too) few

explorative orexperimentalproducts

• Too many features

• Offer fewer mainstreamproducts - do one thingvery well, or clear long-term leaders

• Make choices amongstmainstream productsclear

• Tailor products to targetcustomer groups

• Make behaviourallycompatible products

• Strive for 10ximprovements inperformance

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 40

15.905 Technology (&) Strategy

$

Form/Function

Portfolio transformation - fewer mainstreammajors, many low-cost experiments

$

Form/Function

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 41

15.905 Technology (&) Strategy

Should we (also, more broadly) be re-thinkinghow we think about decision-making in R&D?

• Embrace uncertainty andambiguity

– Toyota has already doneso when it comes totechnical risk - albeit forproducts without muchmarket risk

– people like DuncanSimester and StefanThomke are (quiteseparately) advocatingdoing this on the marketside as well

• Discovery rather than delivery

• Discover more, earlier• Low-cost experiments with

rapid feedback and verydisciplined lessons learned

– digital simulation– prototypes and “concept”

products• Do things in parallel• Postpone decisions where

information not yet available• Re-map the portfolio

– few clear long-livedsimple core products

– many edgy products forexploration andexperimentation

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 42

15.905 Technology (&) Strategy

What is the “state-of-the-art” intechnology (&) strategy?

• Less is more– less R&D to get more out– open innovation +

open source– use architecture/platforms

as strategic weapons– focus on locus of value -

bottleneck constrainingperformance - and builddistinctive competence

• Fewer is better– number of projects– product portfolio– features– size of units– issues on agenda

• Focus on customers– market failure– get real evidence, where

available– experiment– elegance and ease of use

• Embrace uncertainty– recognize the reality– postpone decisions– use real options– explore and experiment

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 43

15.905 Technology (&) Strategy

Acknowledgements

• You guys… without whom there would be no 15.905• Every member of 15.905 Spring ‘07• Pat Hale and Bill Foley• Sloan School of Management Professors: Rebecca Henderson;

Nelson Repenning; and Duncan Simester• SDM Thesis supervisees: Charles Ufongene - (business models);

Alyson Scherer (decision-making/truth-telling); Arthur Mak -(industrial design); Julie Mitchell - open source

• Nokia: Jorma Ollila; Olli-Pekka Kallasvuo; Pertti Korhonen;Ahti Vaisanen; Joe Coles; Mike Butler; Jarkko Sairanen; BobIannucci; Frank Nuovo; Sebastian Nyström; and Jarmo Rintamaki

• Clients: Kouji Kodera; Björn Kilburn; Matt Williams; Eric Brown;Dave Illingworth; Helmut Angst; Steve Donald; Johann-GeorgGross; Paul Stoddart; John O’Donohue

• Endeavour Partners: Pad Kinsella; Sunny Ahn; Moe Kelley

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 44

15.905 Technology (&) Strategy

Contact information and OpenCourseware

• Keen to get guidance from alumni about what yourissues are in technology and strategy

• Michael A M Davies– [email protected]– +1 (617) 818-0818

• http://ocw.mit.edu/OcwWeb/Sloan-School-of-Management/15-905Spring-2007/CourseHome/index.htm

Michael A M Davies [email protected] SDM UltraLite - 18 October 2007, Page 45

15.905 Technology (&) Strategy

Questions and quotations

• OK, it’s cool technology, but will it really be any betterin customers perception, when we finally get it to work?

• Why on earth should I bother with the hassle andanxiety of trying to figure this &*!% out?

• “Show me the money!”• “Any sufficiently advanced technology is

indistinguishable from magic”• How do I get to be Switzerland, rather than Belgium?• Where’s the bottleneck - and what can we do that

customers care about, better than the other guys, thatthey can’t copy?

1: Jerry Maguire (Tom Cruise) to Rod Tidwell (Cuba Gooding, Jr.) in “Jerry Maguire”, directed by Cameron Crowe, 19962: Arthur C Clarke in “Profiles of the Future”, 2nd Edition, 1973