14 C H A P T E R Prepared by: Fernando Quijano and Yvonn Quijano And Modified by Gabriel Martinez...

36

14 14 C H A P T E C H A P T E R R Prepared by: Fernando Quijano and Yvonn Quijano And Modified by Gabriel Martinez Expectations: Expectations: The Basic Tools The Basic Tools

-

Upload

dylan-cobb -

Category

Documents

-

view

215 -

download

1

Transcript of 14 C H A P T E R Prepared by: Fernando Quijano and Yvonn Quijano And Modified by Gabriel Martinez...

1414C H A P T E RC H A P T E R

Prepared by:

Fernando Quijano and Yvonn Quijano

And Modified by Gabriel Martinez

Expectations:Expectations:The Basic ToolsThe Basic Tools

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal Versus RealNominal Versus RealInterest RatesInterest Rates

14-1

Nominal interestNominal interest ratesrates are interest rates are interest rates expressed in terms of expressed in terms of dollars.dollars.

Real interest ratesReal interest rates are are interest rates expressed in interest rates expressed in terms of a basket of terms of a basket of goods.goods.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal Versus RealNominal Versus RealInterest RatesInterest Rates

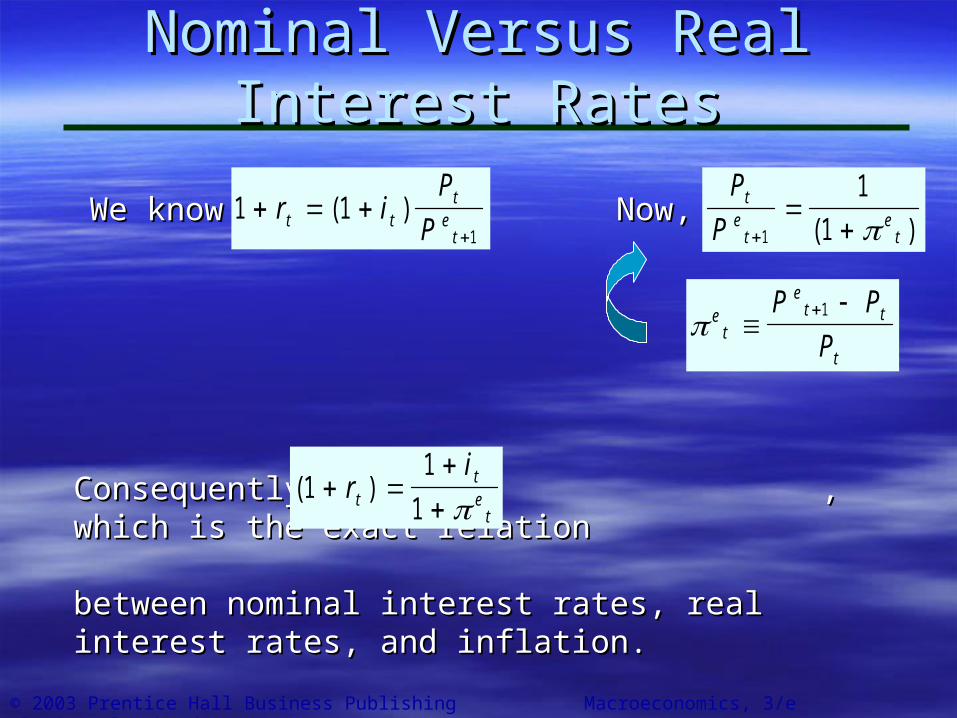

Definition and Definition and Derivation of the Real Derivation of the Real Interest RateInterest Rateiitt = nominal interest rate for year = nominal interest rate for year tt..

rrtt = real interest rate for year = real interest rate for year tt..

(1+ (1+ iitt): Lending one dollar this ): Lending one dollar this

year yields (1+ year yields (1+ iitt) dollars next ) dollars next

year. Alternatively, borrowing one year. Alternatively, borrowing one dollar this year implies paying dollar this year implies paying back (1+ back (1+ iitt) dollars next year.) dollars next year.

PPtt = price this year. = price this year.

PPeet+1t+1= expected price next year.= expected price next year.

Derivation

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal Versus RealNominal Versus RealInterest RatesInterest Rates

Consequently, , which is the exact relation Consequently, , which is the exact relation

between nominal interest rates, real interest rates, and between nominal interest rates, real interest rates, and inflation.inflation.

1 11

r iP

Pt tt

et

( )

et

et t

t

P P

P

1

( )11

1

ri

tte

t

We knowWe know Now,Now,P

Pt

et

et

1

1

1( )

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal Versus RealNominal Versus RealInterest RatesInterest Rates

If the nominal interest rate and the expected rate of If the nominal interest rate and the expected rate of inflation are not too large, a simpler expression is:inflation are not too large, a simpler expression is:

r it te

t

The real interest rate is (approximately) equal to the The real interest rate is (approximately) equal to the nominal interest rate minus the expected rate of inflation.nominal interest rate minus the expected rate of inflation.

Notice that higher rates of expected inflation reduce the Notice that higher rates of expected inflation reduce the real interest rate, given the nominal interest rate.real interest rate, given the nominal interest rate.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal and Real Interest Rates Nominal and Real Interest Rates in the United States Since 1978in the United States Since 1978

Nominal and Real Nominal and Real One-Year T-bill One-Year T-bill Rates in the United Rates in the United States, 1978-2001States, 1978-2001

While the nominal interest rate has declined considerably since the early 1980s, the real interest rate is actually higher in 2001 than it was then.

Despite the large decline in nominal interest rates, Despite the large decline in nominal interest rates, borrowing is actually more expensive in 2001 than it borrowing is actually more expensive in 2001 than it was in 1981.was in 1981.

Nominal

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal Versus RealNominal Versus RealInterest RatesInterest Rates

Expected and actual inflation may differ.Expected and actual inflation may differ.

r = i – r = i – is called the is called the ex-postex-post real interest real interest rate.rate.

r = i – r = i – ee is called the is called the ex-anteex-ante real interest real interest rate.rate.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Expected PresentExpected PresentDiscounted ValuesDiscounted Values

Computing Present Computing Present Discounted ValuesDiscounted Values

14-2

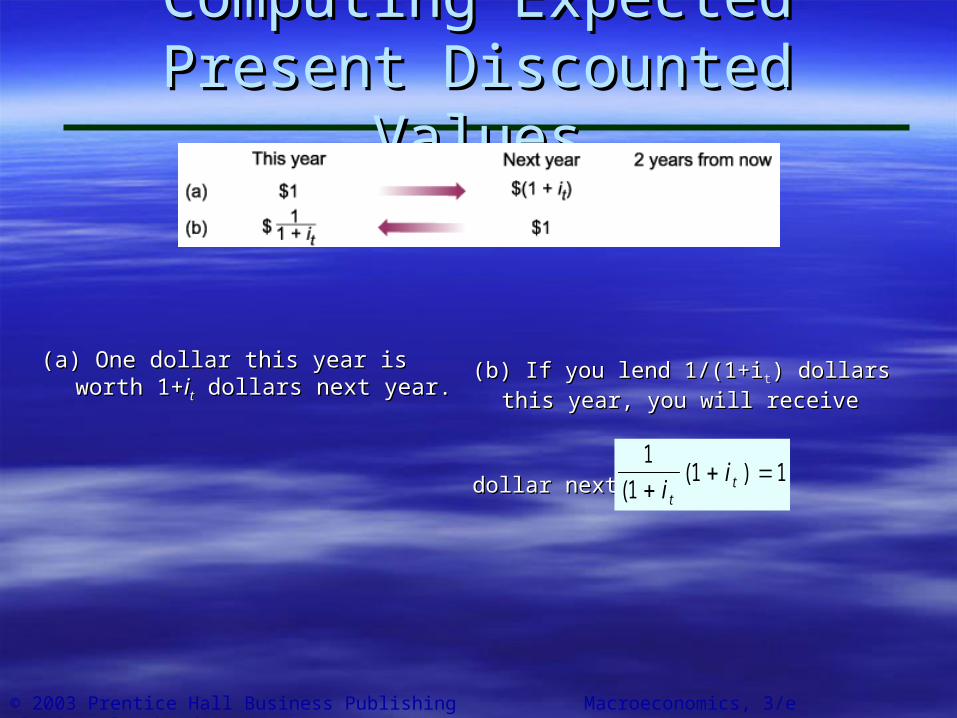

The expected present discounted value of a The expected present discounted value of a sequence of future payments is sequence of future payments is today’s today’s value value of this expected sequence of of this expected sequence of payments.payments.

The term 1/(1+The term 1/(1+iitt) is called the ) is called the discount discount

factorfactor, and the one-year nominal interest , and the one-year nominal interest rate, rate, iitt, it is often called the , it is often called the discount ratediscount rate..

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Computing Expected Present Computing Expected Present Discounted ValuesDiscounted Values

(a) One dollar this year is worth (a) One dollar this year is worth 1+1+iitt dollars next year. dollars next year.

(b) If you lend 1/(1+i(b) If you lend 1/(1+itt) dollars this ) dollars this

year, you will receiveyear, you will receive

dollar next year.dollar next year.

1

11 1

(( )

ii

tt

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Computing Expected Present Computing Expected Present Discounted ValuesDiscounted Values

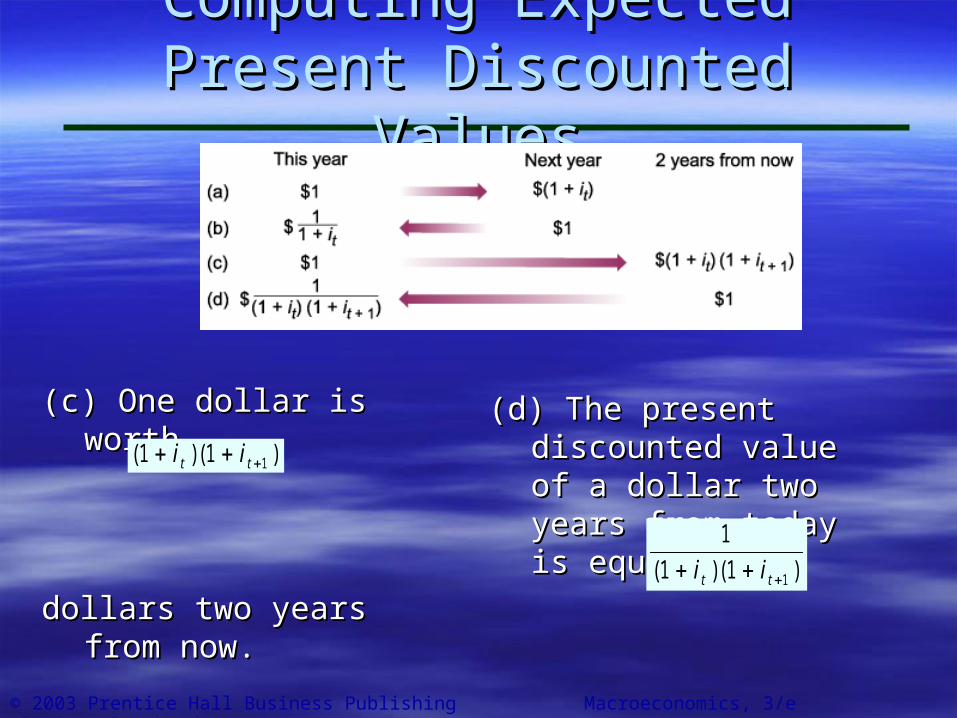

(c) One dollar is worth(c) One dollar is worth

dollars two years from dollars two years from now.now.

( )( )1 1 1 i it t

(d) The present discounted (d) The present discounted value of a dollar two value of a dollar two years from today is equal years from today is equal toto 1

1 1 1( )( ) i it t

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

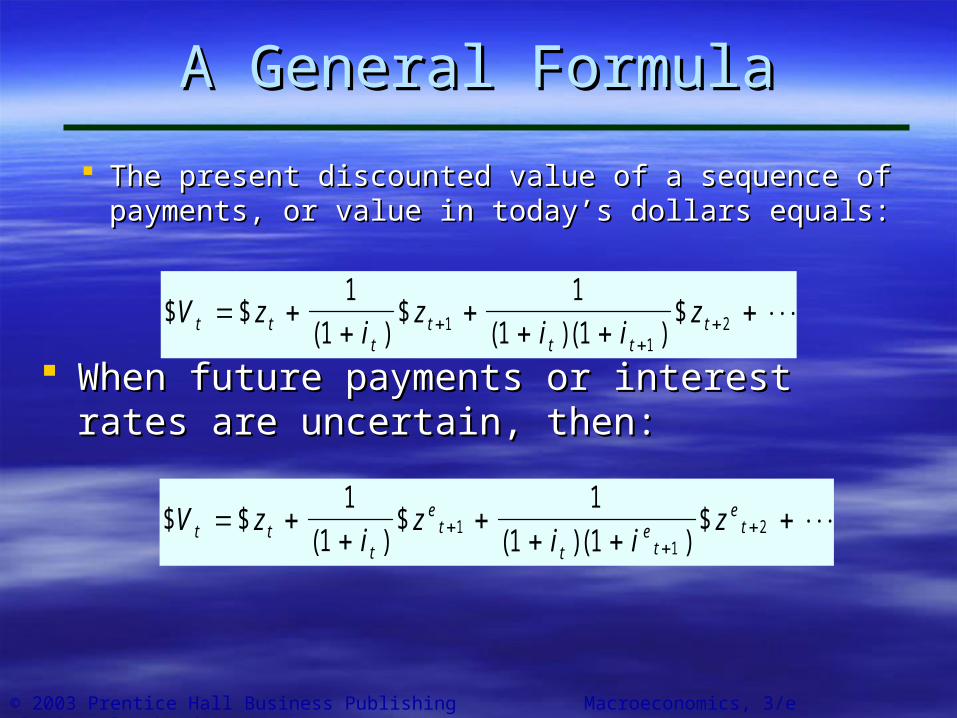

A General FormulaA General Formula

The present discounted value of a sequence of The present discounted value of a sequence of payments, or value in today’s dollars equals:payments, or value in today’s dollars equals:

When future payments or interest rates are When future payments or interest rates are uncertain, then:uncertain, then:

$ $( )

$( )( )

$V zi

zi i

zt tt

tt t

t

1

1

1

1 111

2

$ $( )

$( )( )

$V zi

zi i

zt tt

et

te

t

et

1

1

1

1 11

12

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

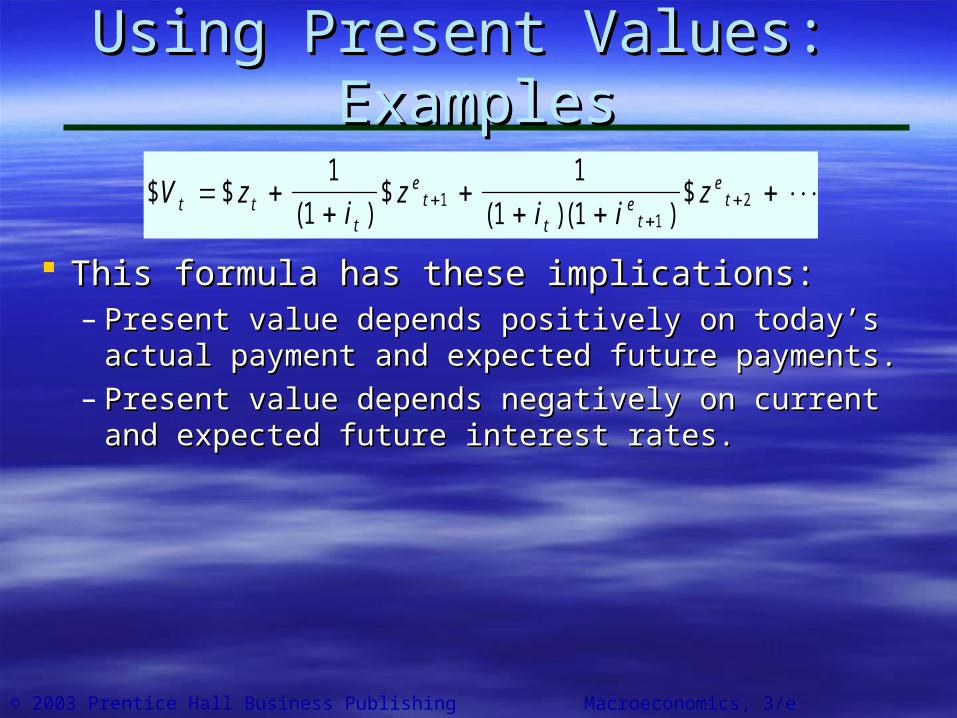

Using Present Values: ExamplesUsing Present Values: Examples

This formula has these implications:This formula has these implications:– Present value depends positively on today’s Present value depends positively on today’s

actual payment and expected future payments.actual payment and expected future payments.– Present value depends negatively on current and Present value depends negatively on current and

expected future interest rates.expected future interest rates.

$ $( )

$( )( )

$V zi

zi i

zt tt

et

te

t

et

1

1

1

1 11

12

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Constant Interest RatesConstant Interest Rates

To focus on the effects of the sequence of To focus on the effects of the sequence of payments on the present value, assume that payments on the present value, assume that interest rates are expected to be constant interest rates are expected to be constant over time, then:over time, then:

– PDV is a weighted sum of the payments.PDV is a weighted sum of the payments.– The weight of future payments declines The weight of future payments declines

geometrically over time.geometrically over time.

$ $( )

$( )

$V zi

zi

zt te

te

t

1

1

1

11 2 2

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Constant Interest RatesConstant Interest Ratesand Paymentsand Payments

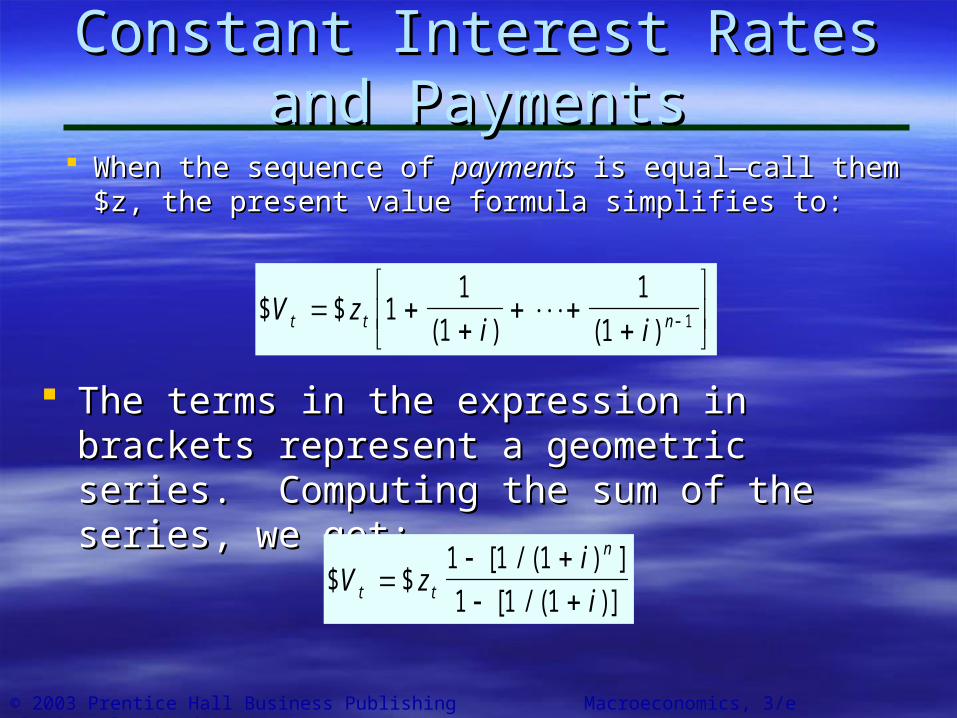

When the sequence of When the sequence of paymentspayments is equal—call is equal—call them $z, the present value formula simplifies to:them $z, the present value formula simplifies to:

The terms in the expression in brackets represent The terms in the expression in brackets represent a geometric series. Computing the sum of the a geometric series. Computing the sum of the series, we get:series, we get:

$ $( ) ( )

V zi it t n

1

1

1

1

1 1

$ $[ / ( ) ]

[ / ( )]V z

i

it t

n

1 1 1

1 1 1

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

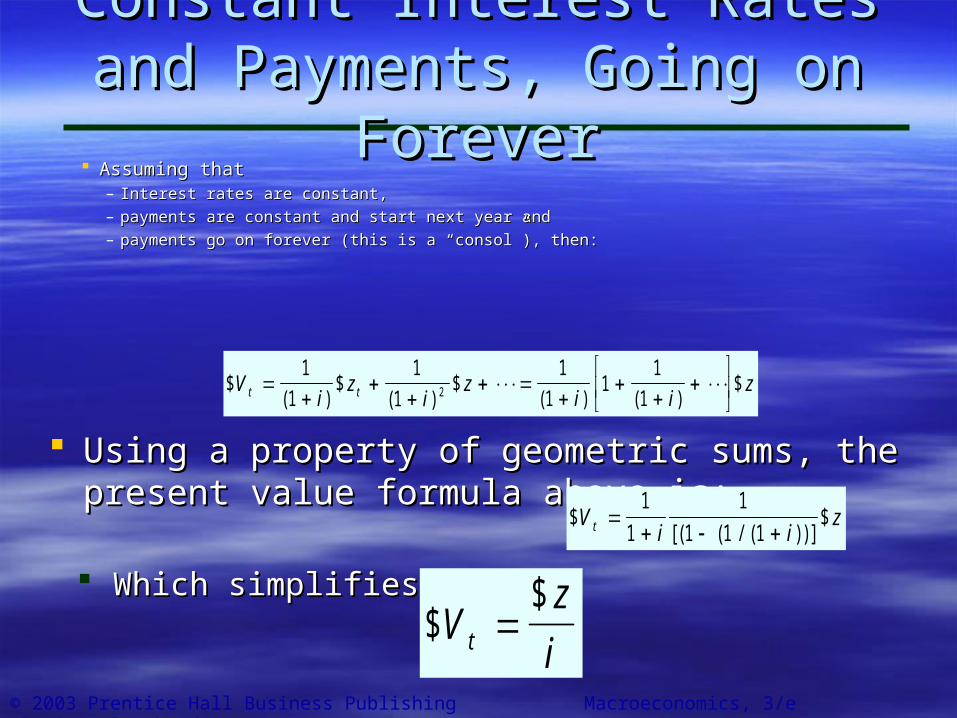

Constant Interest Rates and Constant Interest Rates and Payments, Going on ForeverPayments, Going on Forever

Assuming that Assuming that – Interest rates are constant,Interest rates are constant,– payments are constant and start next year andpayments are constant and start next year and– payments go on forever (this is a “consol”), then:payments go on forever (this is a “consol”), then:

Using a property of geometric sums, the present Using a property of geometric sums, the present value formula above is:value formula above is:

$( )

$( )

$( ) ( )

$Vi

zi

zi i

zt t

1

1

1

1

1

11

1

12

$[( ( / ( ))]

$Vi i

zt 1

1

1

1 1 1

Which simplifies to:Which simplifies to:$

$V

z

it

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Constant Interest Rates and Constant Interest Rates and Payments, Going on ForeverPayments, Going on Forever

It’s quite clear from this formula thatIt’s quite clear from this formula that– Higher payments increase the value of the Higher payments increase the value of the

security.security.– Higher interest rates reduce the value of the Higher interest rates reduce the value of the

security.security.

$$

Vz

it

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

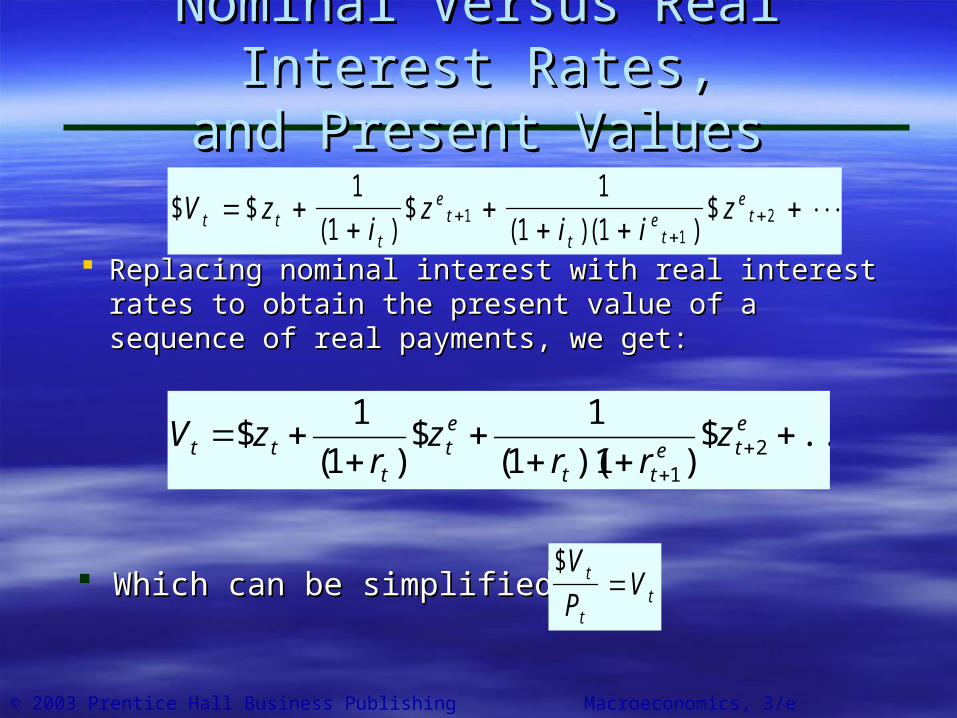

Nominal Versus Real Interest Rates,Nominal Versus Real Interest Rates,and Present Valuesand Present Values

Replacing nominal interest with real interest Replacing nominal interest with real interest rates to obtain the present value of a sequence rates to obtain the present value of a sequence of real payments, we get:of real payments, we get:

Which can be simplified to:Which can be simplified to:

$ $( )

$( )( )

$V zi

zi i

zt tt

et

te

t

et

1

1

1

1 11

12

$V

PVt

tt

...$))((

$)(

$

ete

tt

et

ttt z

rrz

rzV 2

111

1

1

1

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal Versus Real Interest Rates,Nominal Versus Real Interest Rates,and Present Valuesand Present Values

Why have two formulae?Why have two formulae?– Bonds, for example, promise a Bonds, for example, promise a nominalnominal

payment, so we need the payment, so we need the nominal PDVnominal PDV equation.equation.

– Expectations about Income, and Consumption Expectations about Income, and Consumption and Investment decisions, depend on and Investment decisions, depend on realreal variables (why bother with the extra uncertainty variables (why bother with the extra uncertainty about inflation). So we use the about inflation). So we use the real PDVreal PDV equation.equation.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Interest Rates and InvestmentInterest Rates and Investment

Investment is the purchase of a capital Investment is the purchase of a capital good.good.

If If VVtt is the value of a capital good, the is the value of a capital good, the amount of investment will depend amount of investment will depend

… … positively on positively on zztt – I.e., the expected income from investment, I.e., the expected income from investment,

determined by sales and determined by sales and YYtt..

… … and negatively on and negatively on rrtt

...$))((

$)(

$

ete

tt

et

ttt z

rrz

rzV 2

111

1

1

1

+ –

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal and Real InterestNominal and Real InterestRates, and the Rates, and the IS-LMIS-LM Model Model

When deciding how much investment to When deciding how much investment to undertake, firms care about real interest undertake, firms care about real interest rates.rates.

They compare the (real) marginal product of They compare the (real) marginal product of capital with the real interest rate.capital with the real interest rate.

Then, the Then, the ISIS relation must read: relation must read:

14-3

Y C Y T I Y r G ( ) ( , )

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal and Real InterestNominal and Real InterestRates, and the Rates, and the IS-LMIS-LM Model Model

The interest rate directly affected by monetary The interest rate directly affected by monetary policy—the one that enters the policy—the one that enters the LMLM relation—is relation—is the nominal interest rate, then:the nominal interest rate, then:

Recall Md is affected by the opportunity cost Recall Md is affected by the opportunity cost of holding money, which of holding money, which includesincludes inflation. inflation.

M

PY L i ( )

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal and Real InterestNominal and Real InterestRates, and the Rates, and the IS-LMIS-LM Model Model

Y C Y T I Y r G ( ) ( , )

M

PY L i ( )

eir

GiYITYCY e ),()(

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Money Growth, Inflation, andMoney Growth, Inflation, andNominal and Real Interest RatesNominal and Real Interest Rates

This section explains the following This section explains the following assertions:assertions:

14-4

After a Monetary ExpansionAfter a Monetary Expansion

Nominal interest Nominal interest rates, irates, i

Lower in the Lower in the short runshort run

Higher in the Higher in the medium runmedium run

Real Interest Real Interest Rates, rRates, r

Lower in the Lower in the short runshort run

Unchanged in Unchanged in the medium runthe medium run

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Revisiting the IS-LM ModelRevisiting the IS-LM Model

Equilibrium Output Equilibrium Output and Interest Ratesand Interest Rates

The equilibrium level of output and the equilibrium nominal interest rate are given by the intersection of the IS curve and the LM curve. The real interest rate equals the nominal interest rate minus expected inflation.

ir constantis If

irir Ifee

ee

0 If i falls, r falls, I rises, and

equilibrium output rises in the goods market: the IS curve slopes down.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

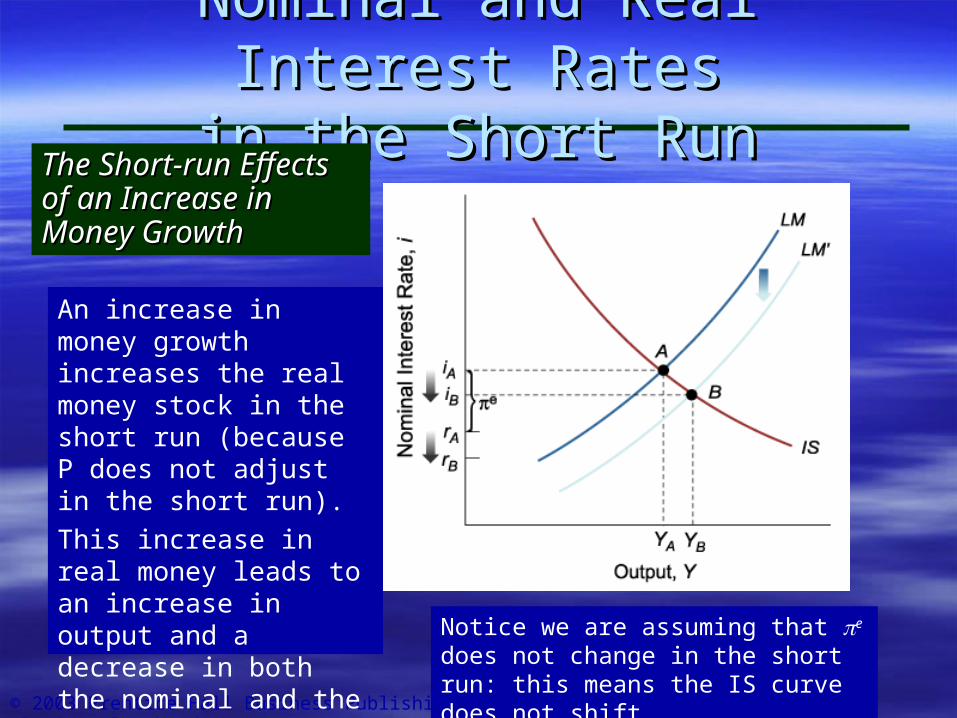

Nominal and Real Interest RatesNominal and Real Interest Ratesin the Short Runin the Short Run

The Short-run Effects The Short-run Effects of an Increase in of an Increase in Money GrowthMoney Growth

An increase in money growth increases the real money stock in the short run (because P does not adjust in the short run).

This increase in real money leads to an increase in output and a decrease in both the nominal and the real interest rate. Notice we are assuming that e does not

change in the short run: this means the IS curve does not shift.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

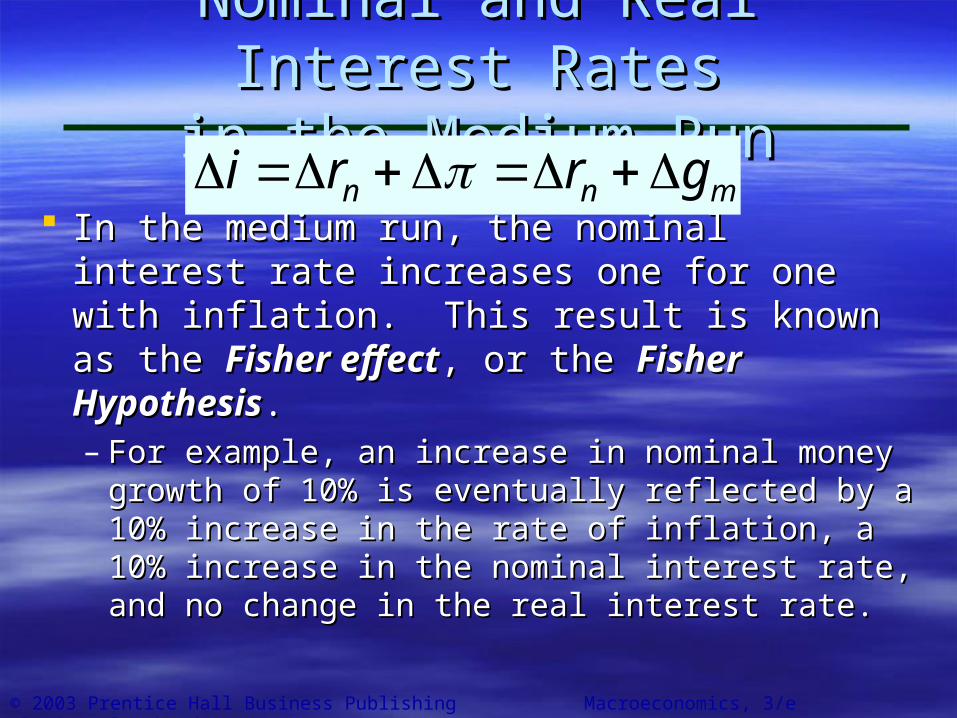

Nominal and Real Interest RatesNominal and Real Interest Ratesin the Medium Runin the Medium Run

In the medium run, , then IS becomes:In the medium run, , then IS becomes:Y Yn

Y C Y T I Y r Gn n n ( ) ( , )

The relation between the nominal interest rate The relation between the nominal interest rate and the real interest rate is:and the real interest rate is:

i r e

i rne

In the medium run, the real interest rate In the medium run, the real interest rate equals the natural interest rate, equals the natural interest rate, rrnn, then:, then:

rn is the interest rate that will make spending equal to the natural level of output.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal and Real Interest RatesNominal and Real Interest Ratesin the Medium Runin the Medium Run

In the medium run, In the medium run, ee==, expected inflation is , expected inflation is equal to actual inflation, soequal to actual inflation, so

i rn

Recall Recall =g=gmm-g-gyy

Higher output growth leads to more money Higher output growth leads to more money demand. If gdemand. If gmm>g>gyy, there must be inflation., there must be inflation.

This implies that This implies that ==ggmm..

Hence, in the medium run:Hence, in the medium run:

mn gri

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Nominal and Real Interest RatesNominal and Real Interest Ratesin the Medium Runin the Medium Run

In the medium run, the nominal interest rate In the medium run, the nominal interest rate increases one for one with inflation. This increases one for one with inflation. This result is known as the result is known as the Fisher effectFisher effect, or the , or the Fisher HypothesisFisher Hypothesis..– For example, an increase in nominal money For example, an increase in nominal money

growth of 10% is eventually reflected by a 10% growth of 10% is eventually reflected by a 10% increase in the rate of inflation, a 10% increase increase in the rate of inflation, a 10% increase in the nominal interest rate, and no change in in the nominal interest rate, and no change in the real interest rate.the real interest rate.

mnn grri

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

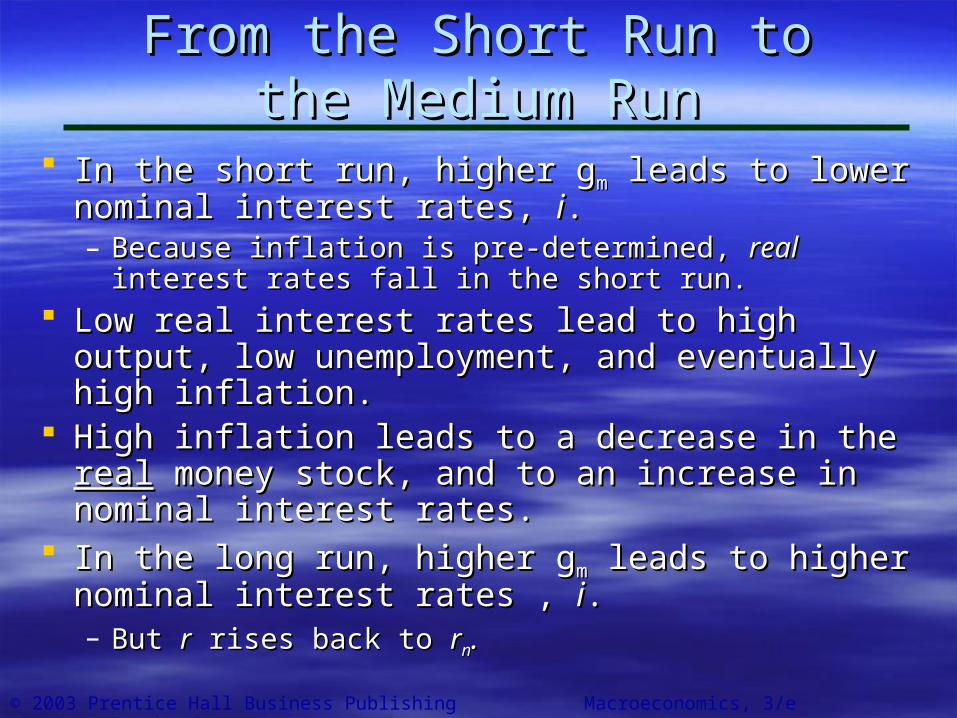

From the Short Run toFrom the Short Run tothe Medium Runthe Medium Run

In the short run, higher gIn the short run, higher gmm leads to lower nominal leads to lower nominal interest rates, interest rates, ii..– Because inflation is pre-determined, Because inflation is pre-determined, realreal interest rates interest rates

fall in the short run.fall in the short run. Low real interest rates lead to high output, low Low real interest rates lead to high output, low

unemployment, and eventually high inflation. unemployment, and eventually high inflation. High inflation leads to a decrease in the High inflation leads to a decrease in the realreal

money stock, and to an increase in nominal money stock, and to an increase in nominal interest rates.interest rates.

In the long run, higher gIn the long run, higher gmm leads to higher nominal leads to higher nominal interest rates , interest rates , ii..– But But rr rises back to rises back to rrnn..

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

From the Short Run toFrom the Short Run tothe Medium Runthe Medium Run

Suppose Suppose ggmm’>’>ggmm. Using the Phillips Curve,. Using the Phillips Curve,

Over time, inflation keeps increasing, and Over time, inflation keeps increasing, and keeps increasing…keeps increasing…

When When > g> gmm, real money growth turns , real money growth turns

negative, which raises nominal interest negative, which raises nominal interest rates.rates.

r r Y Y u un n n

E ven tua lly g g im m' ( ' ) 0

mn gri

M

P

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

From the Short Run toFrom the Short Run tothe Medium Runthe Medium Run

What happens to What happens to rr? We know two things:? We know two things:– Initially, Initially, rr fell. fell.

Immediately after the monetary expansion, nominal rates fell Immediately after the monetary expansion, nominal rates fell while inflation was predetermined.while inflation was predetermined.

– In the medium run, r = rIn the medium run, r = rnn..

So we know that So we know that rr must must riserise back to back to rrnn..

How? When How? When > g> gmm, real money growth turns , real money growth turns

negative, which raises nominal interest rates … negative, which raises nominal interest rates … and, at a given level of and, at a given level of , it raises , it raises realreal interest interest rates.rates.

As As rr rises back to rises back to rrnn, , II and and YY fall back to fall back to YYnn..

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

From the Short Run toFrom the Short Run tothe Medium Runthe Medium Run

– Notice inflation Notice inflation mustmust overshoot for r to overshoot for r to riserise to r to rnn..

So we know that r goes back So we know that r goes back upup to to rrnn. What . What

happens to happens to ii??– It must be equal to It must be equal to rrnn plus the new, higher level plus the new, higher level

of inflation.of inflation.

In the medium run, In the medium run, r rn

Y Yn

u u n

g m

i r gn m

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

From the Short Run toFrom the Short Run tothe Medium Runthe Medium Run

The Adjustment of the Real The Adjustment of the Real and the Nominal Interest Rate and the Nominal Interest Rate to an Increase in Money to an Increase in Money GrowthGrowth

An increase in money growth leads initially to a decrease in both the real and the nominal interest rate. Over time, the real interest rate returns to its initial value. The nominal interest rate converges to a new higher value, equal to the initial value plus the increase in money growth.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Evidence on the Fisher Evidence on the Fisher HypothesisHypothesis

To see if increases in inflation lead to one-To see if increases in inflation lead to one-for-one increases in nominal interest rates, for-one increases in nominal interest rates, economists look at:economists look at:– Nominal interest rates and inflation across Nominal interest rates and inflation across

countries. The evidence of the early 1990s finds countries. The evidence of the early 1990s finds substantial support for the Fisher hypothesis.substantial support for the Fisher hypothesis.

– Swings in inflation, which should eventually be Swings in inflation, which should eventually be reflected in similar swings in the nominal interest reflected in similar swings in the nominal interest rate. Again, the data appears to fit the rate. Again, the data appears to fit the hypothesis quite well.hypothesis quite well.

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Evidence on the Fisher Evidence on the Fisher HypothesisHypothesis

Nominal Interest Rates Nominal Interest Rates and Inflation Across Latin and Inflation Across Latin America in the Early America in the Early 1990s1990s

Roughly half of the points are above the line, the other half below. This is evidence that a 1% increase in inflation should be reflected in a 1% increase in the nominal interest rate.

Nom

ina

l

© 2003 Prentice Hall Business Publishing Macroeconomics, 3/e Olivier Blanchard

Evidence on the Fisher Evidence on the Fisher HypothesisHypothesis

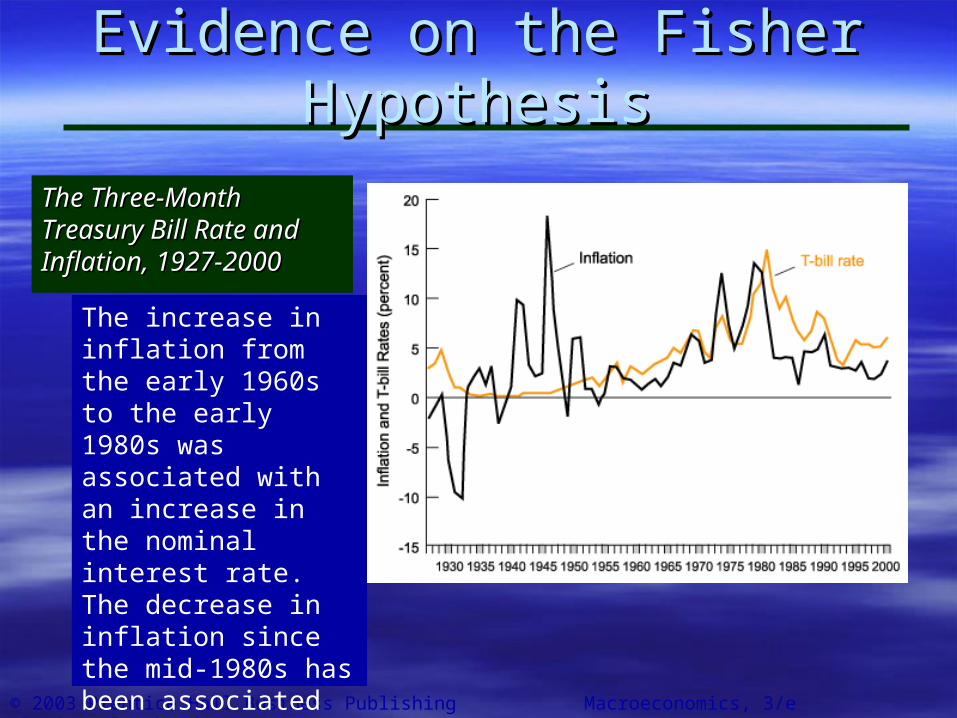

The Three-Month The Three-Month Treasury Bill Rate and Treasury Bill Rate and Inflation, 1927-2000Inflation, 1927-2000

The increase in inflation from the early 1960s to the early 1980s was associated with an increase in the nominal interest rate. The decrease in inflation since the mid-1980s has been associated with a decrease in the nominal interest rate.