13.1 Introduction - Skadden, Arps, Slate, Meagher & Flom · PDF filesubordinated lender from...

48

Chapter 13 Debt Mark Darley Partner Skadden, Arps, Slate, Meagher & Flom LLP 13.1 Introduction This chapter gives an overview of the use of debt in the funding of private equity transactions, the roles of the main participants and the types of debt instruments that are used. It also explores how the debt package is put together – the order of events and the key agreements – and considers some of the more frequently debated provisions. The objective is to provide a better understanding of how the debt piece of a transaction fits into the overall structure and to explain some of the basic structures and issues. With the credit markets in their current turmoil it is exceptionally difficult to be specific as to structures and terms – many of the trans- actions that are funded are bespoke with atypical terms. Rather than try to describe such features, this chapter concentrates on the charac- teristics of funding in an orderly market. 13.2 Why is debt necessary in a private equity transaction? There are a host of reasons why debt is used in a private equity trans- action, but two principal reasons are described below. 13.2.1 Spreading the risk In recent years private equity houses have raised many billions of dollars to fund acquisitions, but even these funds are dwarfed by the size of the business that has been put up for sale. Without debt to 225

Transcript of 13.1 Introduction - Skadden, Arps, Slate, Meagher & Flom · PDF filesubordinated lender from...

Chapter 13

DebtMark DarleyPartnerSkadden, Arps, Slate, Meagher & Flom LLP

13.1 Introduction

This chapter gives an overview of the use of debt in the funding ofprivate equity transactions, the roles of the main participants and thetypes of debt instruments that are used. It also explores how the debtpackage is put together – the order of events and the key agreements– and considers some of the more frequently debated provisions. Theobjective is to provide a better understanding of how the debt pieceof a transaction fits into the overall structure and to explain some ofthe basic structures and issues.

With the credit markets in their current turmoil it is exceptionallydifficult to be specific as to structures and terms – many of the trans-actions that are funded are bespoke with atypical terms. Rather thantry to describe such features, this chapter concentrates on the charac-teristics of funding in an orderly market.

13.2 Why is debt necessary in a private equitytransaction?

There are a host of reasons why debt is used in a private equity trans-action, but two principal reasons are described below.

13.2.1 Spreading the risk

In recent years private equity houses have raised many billions ofdollars to fund acquisitions, but even these funds are dwarfed by thesize of the business that has been put up for sale. Without debt to

225

supplement their own funds the PE houses would be unable to fund thelarger acquisitions or would find that the number of investments theycould make would be much smaller and the risk more concentrated.

The ability of the PE houses to borrow on a limited recourse basis hasgiven them the opportunity to absorb much larger transactions and tospread their exposure. In crude terms, without debt, a £billion PEfund would have a purchasing power of just £1 billion, whereas withdebt, the same fund would have a purchasing power of potentially£2.5 billion (assuming it invests 40 per cent of its funds and borrows60 per cent for each purchase). Assuming the same investment strat-egy, this allows a theoretical 2.5 times greater diversification in invest-ments and exposure.

That is not to say that using bank debt is the only approach PE houseshave to bidding for large, multi-billion pound acquisitions or todiversification. Increasingly, PE houses have clubbed together so thata consortium of two or more PE houses might make a joint acquisi-tion. Inevitably, at the peak of the market, larger private equity acqui-sitions were a combination of multi-house consortia, lower equityinvestments and higher bank borrowings.

13.2.2 Debt is cheaper than equity

Equity share capital is commonly referred to as “risk capital”. Itcarries with it no guarantee of any return, whether in the form ofregular income (dividends), in final pay-out (e.g. through a secondarysale or liquidity on an initial public offering (“IPO”)) or in recovery ofamount invested (if the investment fails). To compensate, sharehold-ers expect a higher return over the life of their investment than some-one with less risk.

Lenders, on the other hand, will typically say they are not in the busi-ness of taking risks, just providing funding. They expect regularcompensation (interest) for the money they provide and completerepayment of the loan no later than the end of its term. As a creditor,they will rank ahead of the shareholders and, as most private equitydebt is fully secured, they will also rank ahead of most trade andother creditors. In brief, lenders will do all they can to minimise theirrisk, and as their risk reduces so should their return.

A Practitioner’s Guide to Private Equity

226

13.3 The cast

13.3.1 PE house/borrower side

13.3.1.1 The PE houseThe PE house, as architect of the acquisition, will take responsibilityfor coordinating the borrower’s financing. At an early stage in theacquisition it will call on the lenders with whom it has worked closelyin the past (and whose affiliates may have invested in the PE house’sfunds) (“relationship banks”) to offer financing terms. The PE houseexpects that the relationship banks’ familiarity with the PE house’sbusiness strategy, risk management procedures and typical financingterms will lead to the cheapest terms and fastest execution of thetransaction.

In many ways the interests of the PE house and its lenders arealigned:

(a) both will want to diligence the investment (or “Target”) to iden-tify inherent risks (and areas of potential efficiency) beforecommitting to acquire or fund the asset;

(b) both are interested in ensuring the acquisition is structured inthe most tax-efficient manner; and

(c) both are interested in ensuring that the business will be prof-itable over its life (albeit for different reasons).

However, although aligned in many respects, the PE house will notwant to be party to any agreement with the banks: unlimited expo-sure could lead to disastrous losses for the PE house, its managersand its funds.

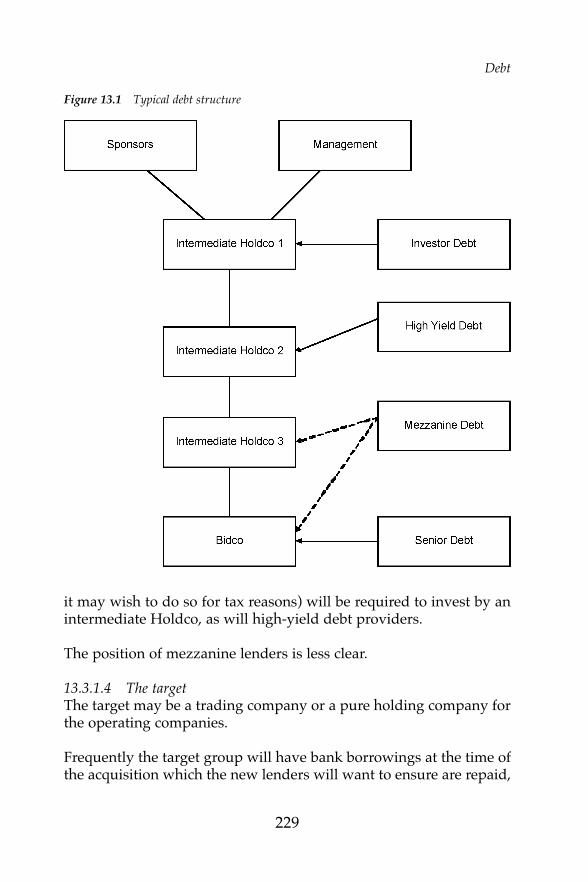

13.3.1.2 BidcoBidco is the structural name commonly given to the vehicle used bythe PE house to make the acquisition. This entity (normally a limitedliability company) will borrow all or a large majority of the debtrequired for the acquisition. It will most probably be a specialpurpose vehicle (“SPV”; i.e. a newly created entity that has no previ-ous trade, assets or (importantly) liabilities) established in a jurisdic-tion that gives tax efficiency and maximises the collateralopportunities for the lenders. Its ultimate shareholders will be the PE

Debt

227

house funds, (commonly) Target management and potentially otherstrategic investors (collectively, the “investors”), all of whom will bekeen to ensure that they have no exposure to the investment otherthan their shareholding (and so will shy away from any contractualobligations to the lenders). Bidco’s assets will be quite limited, oftenjust the shares in Target, contractual rights under the acquisitionagreement and claims against report providers (see below) – no truehard assets such as real property or machinery – but yet it is the prin-cipal borrower. Therefore, the lenders will be extremely keen toensure that they can get full security over such limited assets as it hasand to limit its ability to carry on trade (and so incur competingliabilities).

13.3.1.3 Intermediate HoldcosAside from tax reasons, intermediate Holdcos (i.e. companies placedbetween the investors and the Bidco) are used principally to achievesubordination between competing classes of lenders. Subordination –the means of ensuring one class of creditor is paid in priority toanother class when there are insufficient funds to pay all out in full –can be achieved in three principal ways:

(a) by granting security to one class but not another;(b) by contractual arrangements between the different classes of

lenders; and(c) by structural subordination.

The use of an intermediate Holdco helps to achieve structuralsubordination: the subordinated lenders are required to lend to thisentity whilst the senior lenders lend direct to the Bidco or evenTarget and its subsidiaries. As the intermediate Holdco’s only assetis the equity in Bidco, it will only ever receive a return on a failureof the investment (and so its creditors, the subordinated lenders,will only ever receive repayment) if Bidco has any value/assetsafter the repayment in full of all Bidco’s creditors (e.g. the seniorlenders).

Which class of lender will be required to fund via an intermediateHoldco will depend on negotiating strength, independence of thesubordinated lender from the senior lender and marketability of theclass of debt. Invariably, the investor, if it advances money by debt (as

A Practitioner’s Guide to Private Equity

228

it may wish to do so for tax reasons) will be required to invest by anintermediate Holdco, as will high-yield debt providers.

The position of mezzanine lenders is less clear.

13.3.1.4 The targetThe target may be a trading company or a pure holding company forthe operating companies.

Frequently the target group will have bank borrowings at the time ofthe acquisition which the new lenders will want to ensure are repaid,

Debt

229

Figure 13.1 Typical debt structure

both to avoid competing creditors and because the existing banks areunlikely to allow Target to give collateral to the new lenders.

It is commonplace for acquisitions to be made with existing Targetdebt still in place (and an appropriate reduction in the purchase price)and for that debt to be refinanced out of the new lender loans. Thetotal amount (of debt and purchase price) that the investors pay (andthe lenders advance) is no greater and there is one key advantage tothe lenders in structuring the transaction in this way: as will be seenbelow, most jurisdictions restrict the ability of companies to givecollateral for debt used to fund the acquisition of their own or theirparent’s shares, but there is no such restriction on giving collateral fora company’s own borrowings. If the new lenders are able to structuretheir financing so that part is borrowed by (or “pushed down” to) theoperating companies in the target group (i.e. to enable them to repayexisting debt), the lenders will then have a direct claim against theoperating companies for which they can take security and so rankahead of unsecured creditors (e.g. trade creditors).

13.3.1.5 Report providersReport providers are the professionals who carry out diligence orresearch or who provide advice (such as on matters of tax, keycontract terms, insurance or environmental hazards) to the PEhouses.

The nature of the reports required for an acquisition vary accordingto the target business but would typically include tax, business andfinancial, pensions, environmental, insurance and legal. The reportsare provided to the Bidco who may “rely” on them (i.e. claim againstthe report providers if they are negligently incorrect) and also the PEhouses. In the European market, the practice has developed that thelenders too may have these reports addressed to them and “rely” onthem to avoid the cost of the lenders duplicating the work by havingseparate reports provided to them. The practice in the US ismarkedly different and typically such reports would not beaddressed to the lenders although they may be allowed to see themon a “non-reliance” basis. Indirectly, the lenders benefit from thereports addressed to the Bidco as they take security over all of itsassets (one of which may be the right to claim against the reportproviders).

A Practitioner’s Guide to Private Equity

230

The extent to which lenders can rely on reports can be hotly debatedbetween them and the report providers, and it is always best to startresolution of this issue early in a transaction, although most majorprofessionals will have terms they have agreed in previous transac-tions with the same or similar lenders as well as (in some instances)industry guidelines. Hot topics usually include:

(a) a financial liability limit;(b) a long-stop date for claims; and(c) who can claim (arrangers will want all lenders to be able to

claim, whether they are initial lenders or join in syndication orsubsequent transfer, whilst report providers will want only theinitial lenders to have that right).

In view of the potential limitation on liability, lenders will want torestrict the ability of the PE houses to claim against a report providerin competition with them. How this plays out is a matter for debate,but solutions can include an agreement that no PE house claim can bemade whilst the lenders have outstanding debt or that any monies thePE houses recover will be invested in the Bidco.

13.3.2 Lender side – bank debt

13.3.2.1 The arrangersPutting together a loan package that the investors can be confidentwill be sufficiently attractive for banks to be willing to fund the acqui-sition is a specialist task. Whilst, in a normal credit environment, theinvestors may have a good feel for what is “market”, they will takecomfort from having an “independent” person with whom to negoti-ate terms and who has daily exposure to what is and is not acceptableto banks. The person to whom the investors turn is called an“arranger”.

Typically, the investors are likely to approach a number of their rela-tionship banks to be arranger and ask them to submit their best termsfor their engagement and the financing. One or more arrangers willthen be appointed from this competitive process.

The arrangers’ functions can be summarised as:

Debt

231

(a) structuring the debt package;(b) diligencing or reviewing the diligence provided by the report

providers;(c) reviewing and stress testing the PE houses’ financial model;(d) negotiating the legal documentation;(e) pricing (at least initially and subject to any right to flex) the

loans; and(f) attempting to market/sell the loan to the funding banks.

In return for their services, the arrangers are paid a fee (the “arrange-ment fee”), typically a certain percentage of the amount of the loansthey arrange.

The more sizeable and complex transactions are likely to have anumber of arrangers who will divide the various tasks amongstthemselves. Engaging a number of arrangers not only helps in thedivision of labour but also indicates that more than one financier isconfident that the financing is marketable on the terms presented tothe bank market and this can be persuasive in syndicating the loan.Amongst a group of arrangers, one or more may be appointed “leadarranger(s)” or “mandated lead arranger(s)” (i.e. first among equals):this role is prestigious and important for the bank’s industry leaguetable ranking. The mandated lead arranger (“MLA”) acts as a coordi-nator and bears the principal role of arranging the loan. Its appoint-ment will be driven by a number of factors including relationships,track record in selling loans, terms it believes can be sold and, impor-tantly, the amount of the loan that it (or its affiliates) commit to takeup itself.

Although a lender, in its capacity as arranger, has no obligation tolend, typically it will commit to provide (or “underwrite”) all or partof the loan (in this capacity it is an “underwriter”). The nature of thatcommitment needs to be carefully examined by the borrower as oftenit is conditional upon a number of matters such as “acceptable dili-gence and documentation”, other lenders joining the syndicate (i.e. itis just a partial commitment not for the whole amount of the loan) orthe absence of any material adverse change (“MAC”) in the financialmarkets or the target business. The acceptability of such conditionsdepends on whether these matters can be resolved before Bidco signsa binding acquisition agreement or whether that agreement has a

A Practitioner’s Guide to Private Equity

232

“financing out”. A fee is payable for the underwriting commitment,though this is usually included as part of the arrangement fee.

The legal relationship between the arranger and Bidco is contained ina “mandate letter” and will provide that the arranger has little liabil-ity to Bidco (other than in its capacity as underwriter). The extent towhich the arranger has duties to the lenders to whom it sells the loanhas been the subject of debate and litigation. The credit agreementwill try to exclude all liability, but this contractual arrangement willonly be binding once the lenders have signed the agreement – it willnot avoid the risk of potential liability if the arranger has mademisrepresentations that induced the lenders to sign the credit agree-ment. The arranger will market the loan using an information memo-randum put together by it but at Bidco’s request and for which Bidcoassumes responsibility. This document will contain carefully craftedwording making it clear that the arranger assumes no responsibilityfor the content of the information memorandum, no responsibility toupdate the information and no duty of care to the potential lenders.The efficacy of this language has been tested in court and, on the factsof that case, found to be effective1.

13.3.2.2 The facility agentThe role of the facility agent (also called the administrative agent) isadministrative in nature, acting as an intermediary between theborrowers and the lenders for which it is paid an annual agency fee.Its principal functions are to:

(a) collate and pass on to the lenders information provided by theborrowers (as required by the credit agreement), which in somecredit agreements can be very extensive;

(b) pass communications between lenders and borrowers;(c) process requests from the borrowers for loans, letters of credit or

new interest periods;(d) set interest rates (based on the appropriate interbank rates or base

rates plus the margin (see Section 13.4.1.3 ”Interest payments”);(e) act as a conduit for the flow of payments and receipts between

the lenders and the borrowers;

Debt

233

1 See IFE Fund SA v Goldman Sachs International [2007] 2 Lloyd’s Rep 449.

(f) process transfers of loans between lenders; and(g) comply with instructions given by the requisite majority of the

lenders in taking any action permitted by the credit agreementbut for which no specific provision is made in the documents.

Importantly, the facility agent owes no duty to the lenders to ensurethat the legal documents are enforceable or to advise or monitor theperformance of the borrowers or their compliance with the docu-ments, although it will be required to tell the lenders if it has actualknowledge of an event of default. Furthermore, unless it is specifi-cally required to take action by the credit agreement, the facility agentmay refuse to act, and even when required to act, may refuse to do sountil appropriately indemnified by the lenders.

13.3.2.3 The security trusteeThe security trustee (also called the security agent or the collateralagent) again has only an administrative function for which it is paidan annual security trustee fee. It is commonplace for the roles of secu-rity trustee and facility agent to be performed by the same institutionand for the fees to be combined.

As the title implies, its primary role is to:

(a) act as the holder of the security granted for the loans;(b) take whatever action it is legally entitled to take as directed by

the lenders (subject to an appropriate indemnity) on enforce-ment of the security following a default under the credit agree-ment; and

(c) distribute the proceeds of enforcement in accordance with theorder of priority set out in the credit agreement or the intercred-itor agreement.

In the absence of a security trustee, lenders might only get the bene-fit of security if it was granted to each of them individually. Thiswould be prohibitively burdensome and costly in all but the smallestloans as any transfer of a loan from one lender to a new lender wouldrequire new security to be executed (which might start new harden-ing periods running) and registered and, in some jurisdictions,notarised and taxed.

A Practitioner’s Guide to Private Equity

234

Not all jurisdictions recognise the effectiveness of a security trust oragency arrangement. However, and in those jurisdictions a paralleldebt approach is needed under which all sums owed to the lendersare deemed to be owed also to the security trustee so that the securitygranted to the security trustee covers the totality of the debt. Theborrower is not exposed to “double dipping”, as provision is madethat discharge of the debt owed to the lenders discharges an equalamount of debt notionally owed to the security trustee under theparallel debt arrangement. The complexity of taking security in vari-ous jurisdictions is a fascinating topic, but it is beyond the scope ofthis Guide.

13.3.2.4 The lendersThe arranger will want to sell down (or syndicate) its underwritingparticipation in the loan to reduce its exposure and free up its capitalto participate in further loans. The borrower will also benefit if theloan is successfully sold, but it will also be keen to ensure that it hasa group of “friendly” lenders who will be sympathetic if it needswaivers.

A regular debate between PE houses and arrangers surrounds thetopic of what control the borrower has over the composition of itssyndicate: the borrower wanting consent rights and the arranger typi-cally being willing only to grant consultation rights at most. There isno correct answer to this debate and much depends on the opennessof the credit markets and the size and structure of the loan. At thepeak of the borrower-dominant market, the borrower could expect toachieve consent control for small to mid-sized loans, but with thecontraction of the credit markets, this position has changed markedlyand it is now rare for borrowers to have a say in the identity of thelenders in any but the smallest loans.

13.3.2.5 Defaulting lendersWith the collapse of several significant international banks there hasbeen considerable debate about what protection borrowers shouldseek against one of their syndicate banks not being able or willing tofund loans (especially working capital loans). Should they be disen-franchised on voting? Should they continue to receive commitmentfees? Should the borrower be able to draw additional sums fromperforming banks to make whole the shortfall etc.? This debate is

Debt

235

ongoing and it is being actively promoted by the Loan MarketAssociation (“LMA”). The New York market is far more developed inits approach to these matters. The debate is of course much moreacute when the defaulting lender is also the agent through whom allpayments should flow.

13.3.3 Lender side – bonds

Part of the debt funding for large PE transactions (especially acquisi-tions in the US) may take the form of bonds or notes issued by theborrower or an affiliate (the “issuer”) under an indenture or TrustDeed (the equivalent of the credit agreement). These are often (struc-turally) subordinated to the bank debt and the additional risk iscompensated by a higher interest rate or yield (so-called “high-yielddebt”). In broad terms, the bonds are arranged by managers (roughlythe equivalent of the arrangers) and sold to noteholders (the equiva-lent of the lenders), who are mainly large institutional investors.

Noteholders are not usually concerned with building a long-termrelationship with the issuer; indeed often the issuer may not know theidentity of the noteholders and this leads to difficulty in coordinatinga group of sympathetic creditors if the issuer’s credit takes a turn forthe worse.

However, the noteholders are keen to ensure a liquid market for thebonds so that they can be traded as necessary to meet the notehold-ers’ investment policy – there are generally no contractual constraintson the ability of the noteholders to transfer the notes. Liquidity comesthrough arranging for the notes to be traded on the public marketsand credit rated by one or more of the internationally recognisedrating agencies. The public nature of the notes creates additionalresponsibilities and potential liability for the issuer, its managementand the managers as the marketing of the notes is by way of a publicdocument (the offering memorandum), and periodically the issuerwill be required to make further filings reflecting its financial positionand to notify the market of material developments to its business. Ahigh standard of accuracy and disclosure is expected from thesefilings which, if not met, can lead to significant liability for the issuer,its officers and advisers.

A Practitioner’s Guide to Private Equity

236

Noteholders have little contact with the issuer unless the credit turnssour. Whilst noteholders monitor the public announcements, theyrarely interface with the issuer as the bank lenders might.

The absence of any relationship and detailed knowledge of the busi-ness, together with the nature of the noteholders’ business models,results in a high probability that the issuer will need to pay a fee tothe noteholders for any amendment to, or waiver of, the issuer’sobligations, so it is important that the terms of the notes are suffi-ciently flexible to allow the issuer and its affiliates to carry out what-ever activity it anticipates over the (potentially lengthy) term of thenotes. Consequently, the notes are typically far more flexible than thebank debt.

The trustee is in some ways similar to the agent in a bank lending inthat it interfaces with the issuer. The trustee can approve changes tothe notes, but unless they are of a minor or technical nature, they mayonly do so with the approval of the noteholders. In view of the poten-tial liability for a trustee and the fact that noteholders are not aimingto build a long-term relationship with the issuer, it is rare for a trusteeto exercise its discretion without getting directions. The trustee can, ofcourse, also accelerate and enforce the notes at the behest of the note-holders. If the notes are secured, the security will be held by a secu-rity trustee, usually the same entity as the bank security trustee, andthe noteholders and bank lenders will organise their prioritiesthrough the intercreditor agreement.

13.3.4 Lender side – bridge financing

Whilst it is possible for a note issuance to be synchronised withcompletion and funding of an acquisition, there is a degree of uncer-tainty in this approach (as the offering memorandum needs tocontain detailed (and current) financial statements that may not beavailable at the time the notes need to be marketed and there needs tobe a market for notes (of the type that all but disappeared in thesecond half of 2007)). The gap between the need for funds at comple-tion of the acquisition and the uncertainty of when the note proceedswill be available, can be closed through the use of a short-term bridgefacility provided, for a fee, by the managers. It is important to bear inmind that the managers will not want the bridge facility to be in place

Debt

237

for long and will expect the issuer to do all it can to replace it withnotes as soon as possible – the issuer can expect a high financialinducement to do so!

13.3.5 Stapled financing

In passing, it is worth mentioning a product or service that wascommon at the height of the borrower-dominant market. As themarkets became increasingly hot, PE houses increasingly competitiveand deals increasingly speedy, a product called stapled financingemerged. This was an offer to each bidder made by an affiliate of thefinancial adviser structuring the sale to arrange and underwrite theacquisition financing to each bidder on certain common terms.

Its promoters argued that because it had already looked at the Targetwhen the financial adviser affiliate began working on the sale, it wasfamiliar with Target’s business, had assessed the risk and was able topackage the financing quicker than any external lender. This wouldmean that any investor who took up the offer of stapled financingwould be ahead of the game and would not have to worry about thesource or terms of its funding.

The reality was somewhat different to the theory and few stapledfinancings were ever concluded. Investors found that their relation-ship banks were able to act just as quickly and that the terms theycould obtain there were more in line with their expectations(frequently, the terms provided by the staple bank were little morethan indicative or untailored standard forms). The provision ofstapled financing in the US also caused issues of conflict that threat-ened liability.

13.4 The props (the types of debt fundingcommonly seen in a PE acquisition)

As a general rule, the larger and more leveraged an acquisition, themore layers of different types of debt there are likely to be.

Traditionally, most private equity transactions were funded withsenior debt and mezzanine debt, supplemented occasionally by

A Practitioner’s Guide to Private Equity

238

investor debt (as a substitute for PE house equity) and vendor debtand, for the larger transactions, high-yield debt. However, as the sizeof acquisitions grew and the availability of lender funding increasedin the early 2000s, institutions started marketing ever more innova-tive debt products, such as second lien debt, PIK debt and PIK toggledebt. These new products had different security or payment rankingsand were priced accordingly (so appealing to different investorgroups). The remainder of this section highlights some of the keyfeatures of each of these products.

13.4.1 Senior debt

13.4.1.1 General descriptionSenior debt is a feature of almost all transactions and is provided byspecialist acquisition finance banks.

Senior debt is so called because it is structured to have the greatestlikelihood of full repayment on default by the borrower. It is alsopriced accordingly, being the cheapest institutional debt in the struc-ture. Senior debt priority comes in a number of ways:

(a) Guaranteed by all companies in the Bidco (and Target) groupand secured over all of their assets to the extent that this islegally possible (and not prohibitively expensive) ahead of allother lenders. Typically, guarantees will only be provided by the“material subsidiaries”, that is, those subsidiaries that accountfor a certain percentage (2.5 per cent to 5 per cent) of consoli-dated EBITDA, gross assets or turnover of the group.Ranking will be reinforced by an intercreditor agreement, towhich all institutions providing debt for the acquisition (andpotentially all significant members of the Bidco and Target groupsproviding intra-group debt) will be party. The intercreditor agree-ment will provide that the senior lenders can enforce first (andthat all other parties will defer enforcing until the senior lendershave had a suitable opportunity to consider their position andwhat action they want to take) and that all recoveries on enforce-ment are applied first to the discharge of the senior debt.

(b) A shorter maturity to the other debt pieces, typically six or sevenyears after being advanced.

Debt

239

(c) Amortising (at least in part), leading to increased security cover-age (and a reduction in risk) as the amount of debt secured byTarget assets reduces over its term. The reduction of the seniordebt by amortisation is supplemented by various mandatoryprepayment events.

13.4.1.2 Core terms

GeneralThe terms of the senior credit agreement are likely to be less flexiblethan other parts of the debt structure as the senior lenders want toensure that:

(a) the borrower runs the business in the way they were told itwould when deciding whether (and at what price) to providefinancing;

(b) the assets over which they expect to have security are not dissi-pated (including by moving assets from one group companyfrom whom they have collateral to another from whom they donot); and

(c) their debt is repaid at least as quickly as they expected.

The senior lenders will expect extensive information rights concern-ing the business, its past performance, its future budgets and strat-egy: information flow and dialogue is key at this level of debt.

FacilitiesThe senior facilities agreement will provide at the very least a “termfacility” (which is used to fund the acquisition), almost invariably a“revolving credit facility” (“RCF”; which is used for the working capi-tal needs of the Target business) and, depending on the nature of theTarget business, it may provide one or more of the following as well:

(a) a “capital expenditure facility” (or “capex facility”);(b) an “acquisition facility”; and(c) a “bank guarantee facility”.

The “term facility”The term facility is the main part of the facility and provides thefunding for the acquisition of the Target and the repayment of any

A Practitioner’s Guide to Private Equity

240

long-term debt in the Target group. It will typically be available at thetime of closing the acquisition and for a short period afterwards tofund any repayments that cannot be made at closing (although this israre).

The borrower in respect of that part of the term facility used for theacquisition will be Bidco. There may be more than one Bidco depend-ing on the structure of the acquisition, but if so, each will be expectedto be jointly and severally liable (as guarantors) for the borrowings ofthe others.

The ultimate borrower in respect of the part of the term facility usedto refinance long-term debt of the Target group may be Bidco or moretypically the Target group members whose debt is being refinanced.There are a number of structural, tax and legal matters to be consid-ered in deciding upon the best course, but to the extent possible, thelenders will prefer that the loan is at the level of the companies whosedebt is being refinanced (especially if they are operating companies orcompanies with substantial assets) as this means there is less chancethat they will be structurally subordinated to trade creditors and alsohelps to minimise limitations in certain jurisdictions on the giving ofguarantees by Target group companies for debt of their parent.However, often Target group companies are unwilling to participatein the loan arrangements until after the acquisition has beencompleted whereas lenders will expect existing debt to be repaidimmediately upon the acquisition being effective. This tension isresolved by Bidco borrowing to repay existing Target group debt, butwith the relevant Target group borrowers assuming this part of thedebt from Bidco as soon as possible after the acquisition is effective.This mechanic is known as “debt pushdown”.

The revolving credit facility (“RCF”)The RCF is used to fund the group’s working capital requirements. Inthe context of an acquisition, the lenders may also allow the RCF tobe used to fund working capital adjustments to the purchase price.

BorrowersIt is usually in the interests of both the Target group and the lendersfor all operating companies in the group to be borrowers under theRCF. However, whether this is appropriate in all cases depends on the

Debt

241

ease with which lenders can lend into the required jurisdiction andwhether interest can be paid free from withholding or similar taxesfor which the banks would expect to be compensated. Where it isimpractical to lend direct to an operating company, the borrowingwill have to be made by another company in the group and on-lentintra-group.

The facilitiesAn RCF typically comprises two main facilities: a loan facility and abank guarantee facility. It is common for the bank guarantee facilityto be a sub-limit of the RCF amount (i.e. the full amount of the RCFcould not be used just for bank guarantees), but this need not neces-sarily be the case if the business needs of the Target group dictateotherwise.

RCF loan facilityUnlike a loan under the term facility, an RCF loan is short-term (typi-cally one, three or six months in duration), but can be reborrowedthroughout the availability period for the RCF (typically the sameperiod as the term facility).

RCF bank guarantee facilityMany businesses require bank guarantees, and the lenders agree thatthey will provide them under the RCF. Only one bank actuallyprovides the bank guarantee, but each bank agrees to share in anylosses that the Letter of Credit Bank (“L/c Bank”) suffers if the bankguarantee is called and not reimbursed by the borrower. Each bankreceives a fee for this service equal to the margin and the L/c Bankalso receives a fronting fee of (typically) 12.5 bps on the amount of theL/c in respect of the exposure it has should the other banks not reim-burse it on default by the borrower.

Ancillary facilitiesAncillary facilities are used where a borrower needs a credit line thatcannot easily be provided on a syndicated basis, for example a hedg-ing line (such as for foreign exchange (“FX”) exposure), a BACS facil-ity or a small bank guarantee or loan or an overdraft facility. Anancillary facility is a bilateral arrangement between the relevant RCFborrower and an RCF lender who agrees to provide the line (there isno obligation on the lender to provide the line of credit, but it is

A Practitioner’s Guide to Private Equity

242

usually provided by the bank with whom the Target group has mostof its operating accounts) and the fees it receives are determined bythose bilateral negotiations. If the borrower defaults under the ancil-lary facility, there is an adjustment to each lender’s exposure to theborrower so that each shares in the ancillary facility lender’s loss.

Other facilitiesA number of other specific facilities might be provided depending onthe nature of the business being acquired. So, for example, a targetgroup with a sizeable capital expenditure requirement would typi-cally expect to receive a capex facility available to be drawn forspecific, budgeted capital expenditure investments that could not beeasily funded from its revenue. Similarly, a business whose develop-ment plans involved making complimentary acquisitions that mightnot be capable of being funded from its own revenue would seek anacquisition facility. The terms and nature of such facilities, whilst verycommon, are outside the scope of this Guide.

13.4.1.3 Common termsThis section deals with terms of the credit agreement that arecommon to more than one of the facilities.

RepaymentIn addition to any term amortisation repayments and RCF repayments,provision is also made for voluntary and mandatory prepayment.

(a) Voluntary prepayment: borrowers are typically permitted toprepay all or (subject to an agreed minimum amount) part of theterm facility at any time after a nominal amount of notice to thefacility agent. Voluntary prepayment is allowed without thepayment of any penalty or premium but is subject to thepayment of break costs.Lenders typically do not fund their loans off their own balancesheets but instead borrow the money they need from the inter-bank market. If the lender is repaid before the end of the inter-est period, it will still be required to pay interest in the interbankmarket on the amount it borrowed for the full period and, whilstit should be able to recoup part of the foregone interest by rein-vesting the principal repayment it received in the interbank

Debt

243

market, there remains the risk that this will not compensate itfully. Break costs reimburse the banks for this loss (but not theloss of margin).

Voluntary prepayments ordinarily reduce the debt owed to eachlender under the relevant term facility on a pro-rata basis.

(b) Mandatory prepayment: lenders require a borrower to prepaytheir debt not just in accordance with an agreed amortisationschedule or at the end of a term, but also (subject to certainexceptions and de minimis thresholds) where the business onwhich they based their credit assessment changes or where theborrower has more revenue than is needed for its business (i.e.revenues that, if there was no debt, might be returned to the PEfund as dividends).

The main examples of this are as follows.

(i) Business change:

– Bidco has a claim against the seller of the target businessunder the acquisition agreement as a result of a breachof representation or warranty under that agreement;

– Bidco has a claim against a report provider;– there is a change of control of Bidco;– Target group makes a material disposal; and– Target group suffers a loss resulting in a receipt of

insurance proceeds.(ii) Surplus revenue:

– excess cash flow sweep (where, at the end of eachfinancial year, the business has surplus revenue); and

– An IPO of the Target group.

The borrower should bear in mind that frequently the funds to beprepaid will not be held by the borrower but by a subsidiary or sistercompany and to make the mandatory prepayment at the borrowerlevel it will be necessary to move the moneys to the borrower. In manyjurisdictions it will not be possible to transfer the funds to a parent orsister company other than by way of dividend because of legal orfiscal constraints: the borrower needs to be mindful not to agree tosomething that it cannot perform. There are various compromises that

A Practitioner’s Guide to Private Equity

244

can be reached here and different lenders have different stancesdepending on the circumstances.

Cancellation and commitment feesThe borrower can cancel any part of the facilities that it no longerneeds on nominal notice to the facility agent and without payment ofany fee. The incentive for doing this is that the borrowers are chargeda commitment fee of a certain percentage of the facilities that areavailable to it but unused and uncancelled; the fee reduces as thefacilities are cancelled.

Interest paymentsInterest payments comprise three elements:

(a) the rate incurred by the banks when they borrow the amount oftheir loan in the interbank markets (being LIBOR or, in the caseof euro loans, EURIBOR);

(b) a percentage to reflect the regulatory costs incurred by bankswhen lending, known as “mandatory costs”; and

(c) the margin, being the lenders’ “profit” based on their risk assess-ment of the loan.

In US syndicated financings, borrowers may also elect to pay intereston US dollar loans calculated by reference to Federal Reserve rates(base rate loans) instead of LIBOR.

LIBOR and EURIBOR rates vary according to the length of the inter-est period chosen by the borrower. Interest periods are typically one,three or six months. LIBOR/EURIBOR is generally calculated by thefacility agent by reference to screen rates and there is provision for thescreen rate not being available (the facility agent then asks three“reference banks”) or if no rates are available at all or they do notreflect the true cost of borrowing.

The margin is fixed at signing of the credit agreement. It is nowcommon for the margin for certain facilities to step down (and backup) according to the leverage of the group. The leverage of the groupwill be calculated quarterly and the margin adjusted a few businessdays after delivery to the facility agent of the quarterly accounts thatare used to calculate the leverage. If the accounts are not delivered or

Debt

245

if there is an outstanding default, the margin will usually automati-cally increase to the highest level until the accounts are delivered orthe default rectified.

HedgingThe borrower’s exposure to changes in LIBOR and EURIBOR interestrates is typically mitigated by entering into an arrangement to hedgeits interest rate exposure on a certain percentage of the floating ratedebt. The hedging is ordinarily provided by one of the lenders andwill rank pari passu with the senior debt for security purposes.Because the hedging can be lucrative, arrangers frequently ask for aright to match any proposal by a third-party bank. This is resisted onthe basis that if it becomes known in the market, it may result ininsufficient banks bidding to give fair competition on terms.

Representations and warrantiesThe credit agreement will contain extensive representations andwarranties designed to ensure the business is as anticipated by thelenders and to allocate the risk of certain occurrences to the borrower.A breach of the representations is considered serious and can lead tothe lenders being entitled to refuse to lend or even demanding repay-ment of the debt. The representations will cover:

(a) the ability of the borrowers and guarantors to enter into thefinance documents and the acquisition agreements;

(b) the validity and enforceability of those documents;(c) the payment of related taxes;(d) the absence of significant litigation, environmental and tax

liability;(e) the absence of unauthorised borrowings and collateral;(f) ownership of assets needed to run the business and over which

the lenders intend to take security;(g) accuracy of information on which the lenders based their deci-

sion to lend (including the reports);(h) accuracy and fullness of disclosure in the information memo-

randum used for syndication;(i) accuracy of the financial statements;(j) absence of significant pension exposure; and(k) group structure and other representations specific to the

transaction.

A Practitioner’s Guide to Private Equity

246

The representations and warranties are made when the credit agree-ment is signed and selected elements are repeated on each drawdownand possibly also at the start of each interest period and on each inter-est payment date. Those representations relating to the informationmemorandum will be repeated only on initial drawdown, when theinformation memorandum is circulated and when syndicationoccurs. A point of contention between borrower and lenders is whichof the representations and warranties are to be repeated. This is amatter for negotiation, but generally those that are also addressed bythe covenants need not be repeated.

Covenants or undertakingsThe covenants require the borrower group to do or refrain from doingcertain acts. Whilst the representations establish (hopefully) that thetarget business is as anticipated by the lenders, the covenants aredesigned to ensure the business is conducted as the lenders expect.They can be divided into the following categories:

(a) Information covenants. There are two elements to these: finan-cial information and general business information covenants.They are designed to ensure the lenders receive the informationthey need to monitor the group’s business and provide notice ofdifficulties in the business.The financial information covenants will require the borrowergroup to provide monthly, quarterly and semi-annual unau-dited accounts, audited annual accounts, annual budgets (allprepared consistently and in line with the appropriate account-ing standards) and compliance certificates (certifying compli-ance with the financial covenants (see below), calculation of anyadjustment to the margin and the guarantor coverage ratio (seebelow)). To the extent that the compliance certificate calculatesmatters from the audited accounts, the auditors may be requiredto confirm the calculations (or the figures from which the calcu-lations are derived).The general information covenants are intended to keep thebanks appraised as to significant business developments andwill include all information that as a matter of law is to bepassed to shareholders or creditors generally, details of materiallitigation or other claims (e.g. under the acquisition agreement)and notice of any defaults under the finance documents. There

Debt

247

is also a general provision requiring the borrowers to give thefacility agent such other information as it reasonably requires.It is also common for the borrower group to be required to giveannual presentations to the lenders and for the facility agent tohave inspection rights and access to the auditors of the group(though the borrower will normally only allow this if there is adefault or event of default).

(b) Business covenants. The business covenants – both positive(requiring the group to take certain actions) and negative(requiring them to refrain from actions) – are intended to ensurethe business is operated as the lenders were told it would be, toprotect their collateral package and to ensure that there is nounexpected dissipation of the group’s assets. There are a numberof ways in which the business covenants can be categorised;below is just one example.

Authorisations and compliance with laws: requiring the group to comply with alllaws and obtain all authorisations necessary for the enforceability of thefinance documents and the conduct of the group’s business; comply with envi-ronmental and pensions laws; and pay all taxes when due.

Restrictions on business focus: restricting mergers and acquisitions of othercompanies and businesses; prohibiting a change from the general nature of thebusiness as it was at the time of the financing; restricting Bidco from carryingout any activity other than a holding company; maintenance of IP rights; andrequiring the group to maintain its assets in good order.

Restrictions on dealing with assets and security: requiring the group to ensure thatthe lenders’ claims rank at least pari passu with the claims of other unsecuredcreditors; a negative pledge prohibiting the group from having other securityinterests (NB: security interest may be defined very broadly to include reten-tion of title and set-off arrangements as well as any other arrangement that hasthe effect of conferring preferential access to assets to a third party); and restric-tions on the disposal of assets.

Restrictions on movements of cash: restrictions on group companies makingloans, giving guarantees and paying dividends (except within the group itselfof course) and other sums and fees to the investors and intermediate holdingcompanies; restrictions on incurring additional financial indebtedness; andprohibiting hedging for speculative purposes.

Miscellaneous restrictions: ensuring that transactions with affiliates are on arm’s-length terms and for fair market value; maintaining insurance; and not makingamendments to the acquisition agreements.

A Practitioner’s Guide to Private Equity

248

Of necessity the above are only illustrative and in practice thebusiness covenants will be more extensive and tailored for theparticular business. Management commentary on what is neces-sary should be sought as early as possible.

(c) Financial covenants. The financial covenants are intended tomonitor the financial performance of the group and to measurethat performance against projections made to the lenders at thetime they were considering lending. They are intended to act asearly warning signals to the lenders that the business is notperforming as well as was expected and so give the lenders anopportunity to talk to the borrower about the reasons for thisand what might be done to get the business back on track beforeit is too late. However, most financial covenants are historic (i.e.they calculate the past performance of the group) being based onthe most recently delivered quarterly, semi-annual and annualaccounts. As such, there is the risk that by the time the problemcomes to light, the source of the difficulty is embedded. Thefinancial covenant thresholds are set at a level that is intended totake this into account. A detailed analysis of the financialcovenants is outside the scope of this Guide.A common debate around the financial covenants is theborrower’s entitlement to an “equity cure”. Typically a breach ofa financial covenant is considered to be so serious by the lendersthat it results in an immediate event of default. In recent years ithas become common for borrowers to be allowed to “cure” abreach of a financial covenant by the PE fund injecting equity ordeeply subordinated debt. This right to cure is not unlimitedand typically can only be exercised a few times during the life ofthe loan and not on consecutive testing dates.

Events of defaultThe occurrence of an event of default entitles the lenders to acceleratethe loan, demand repayment and enforce the guarantees and securitythey have. These events are clearly very serious and include:

(a) non-payment under the finance documents;(b) breach of the financial covenants;(c) breach of other obligations in the finance documents (in some

cases, where capable of being remedied, a short “grace

Debt

249

period” will be given before the breach becomes an event ofdefault);

(d) breach of representations (again, possibly with a grace period);(e) cross-default subject to a de minimis exception;(f) insolvency related matters;(g) unlawfulness or unenforceability of the finance documents;(h) cessation of business;(i) material adverse audit qualification;(j) repudiation of the finance documents; and(k) MAC clause (i.e. if there is a material adverse change in the busi-

ness of the group taken as a whole).

Clean upAlthough the PE house will have conducted a thorough due diligenceexercise and have spoken to Target management before committing tomake the acquisition, it will not have full exposure to the businessuntil the acquisition is completed and it is able to send its own officersin to examine the business from the inside. This is even more truewhere Target is a publicly listed company, as the extent to which infor-mation concerning the business can be disclosed to a bidder whilst thecompany is listed and it’s shares traded is very constrained.

Consequently, the borrower usually negotiates a short period (around90 days) after closing where a breach of a representation or covenantinsofar as it is caused by the Target does not trigger an event ofdefault or a drawstop. There will be conditions to this relaxation,including that it will not apply to certain events, that the breach mustbe capable of being remedied, that steps are being taken to remedythe breach and that it does not have a material adverse effect on thegroup as a whole.

Conditions precedentConditions precedent fall into two general categories: documentaryconditions precedent and event conditions precedent. The documen-tary conditions precedent need to be satisfied before the first drawingis made, whilst the event conditions precedent need to be satisfiedbefore each drawing.

Documentary conditions precedent include the facility agent beingsatisfied with:

A Practitioner’s Guide to Private Equity

250

(a) corporate resolutions of the borrower;(b) the acquisition documents;(c) the due diligence reports;(d) the group structure;(e) the tax structure paper (setting out how the acquisition will be

effected and the tax consequences);(f) agreed base case model;(g) latest financial reports;(h) “know your customer” checks; and(i) legal opinions.

Event conditions precedent include the accuracy of the representa-tions and warranties and the absence of any default.

Conditions subsequentIt will not always be practicable for guarantors to accede to thefinance documents before closing (as they will comprise Target groupcompanies who will be unwilling to commit until they have beenacquired on completion) and consequently there will be a series ofconditions subsequent relating to the participation of these compa-nies in the finance documents. There will be a grace period for thesesteps to happen (typically 90 days but possibly longer depending onthe nature of the group and the jurisdictions involved).

13.4.2 Mezzanine debt

Mezzanine debt ranks behind senior debt on enforcement, both interms of repayment and in terms of security. As a result, it attracts ahigher rate of interest. The terms of the mezzanine facility agreementare very similar to the terms of the senior credit agreement and thesecurity is identical (typically contained in the same document andheld on behalf of the mezzanine lenders by the same security trustee).The subordination of the mezzanine debt is contained in the inter-creditor deed (see 13.5 below). The main differences between the termsof the senior debt and the mezzanine debt are as described below.

13.4.2.1 PurposeThe mezzanine debt is purely term debt provided for the purposeof the acquisition. It is drawn in one instalment at closing of theacquisition.

Debt

251

13.4.2.2 BorrowerTypically there is just one borrower, Bidco. The senior lenders wouldbe reluctant to allow the mezzanine banks to lend direct to operatingcompanies (even if part of the mezzanine debt is to be used to refi-nance existing debt in the Target group) as this would mean that themezzanine banks would be structurally on a par (or ahead of) thesenior lenders.

13.4.2.3 TermReflecting its subordinated status, the mezzanine debt matures laterthan the last tranche of the senior debt (generally 6–12 months later).It is repayable in one bullet instalment (i.e. no amortisation).

13.4.2.4 InterestThe margin commonly comprises two elements: a cash pay elementand a PIK element (roughly equal in amounts). The cash pay elementis paid at the end of each interest period whereas the PIK element isrolled up and added to the principal amount of the loan (and soattracts interest itself). The PIK element is only finally paid out whenthe loan is repaid.

13.4.2.5 PrepaymentPrepayment of all or any part of the mezzanine debt within a certainperiod from signing will result in the payment of a prepaymentpremium. How much depends on market conditions, but it willgenerally be a higher percentage if prepayment occurs earlier in theterm of the facility.

Prepayment premia would not normally be required on mandatoryprepayments (apart from for change of control or on an IPO) or avoluntary prepayment of just one bank (e.g. on yank the bank; ifprepayment rather than transfer is allowed in this instance).

13.4.2.6 Financial covenantsWith the exception of the cash-flow covenant, there is usually extraheadroom under the financial covenants in the mezzanine facilityagreement to ensure that the senior debt covenants are tripped first(and so to avoid the mezzanine being able to hold the senior lendersto ransom).

A Practitioner’s Guide to Private Equity

252

13.4.2.7 Board observer rightsMezzanine lenders occasionally ask for board observer rights thatwould give them the right to have one of their officers sit in on boardmeetings but without the right to speak or vote. Borrowers areagainst this for the reason that they do not necessarily want to airtheir problems to the mezzanine lenders before discussing themamongst themselves. It is not common for such observer rights to begiven.

13.4.2.8 WarrantsIn broad terms as part of the cost of obtaining mezzanine debt, aborrower might be required to give warrants to the mezzaninelenders. These allow the mezzanine lenders to subscribe for shares inthe borrower at a predetermined price upon certain trigger eventsoccurring (such as a change of control, a sale or an IPO). The warrantinstrument would contain tag-along rights, which would providethat if the investors are selling the shares in the borrower to a thirdparty, the mezzanine lenders have the right to have their sharespurchased at the same price. In summary, warrants give the mezza-nine lenders the opportunity to participate in the equity of theborrower and in the equity returns of the investors. The percentage ofshares in which they could invest would be set at the time of signingthe agreement and might contain elaborate adjustment mechanics tocater for additional issues of shares to the investors or the creation ofnew classes of shares with different voting or economic rights.

Inevitably, this potential dilution of the equity interests of theinvestors is not attractive to them and is resisted.

13.4.3 Investor debt

As mentioned above, often there are tax advantages for investors ifthey advance their part of the acquisition funds in the form ofinvestor debt. As also mentioned above, the investor debt will beadvances to an intermediate Holdco.

The investor debt will provide that it is long term in nature and thatinterest payments can be capitalised and added to the principalamount of the loan rather than cash paid (for the reason that thesenior and mezzanine lenders will restrict the ability of the Bidco to

Debt

253

pay dividends or make payments to the intermediate Holdco as longas they are outstanding and, consequently, there will be no funds tomeet any cash payments to the investors). What rate of interestaccrues on the investor debt will be a factor of the return ultimatelyrequired and the tax effect on both the intermediate Holdco and theinvestors.

Provided neither senior lenders not mezzanine lenders have anycredit exposure to the intermediate Holdco, it should not be necessaryfor the investors to be party to any intercreditor agreement with thelenders subordinating their claims.

13.4.4 Vendor debt

Occasionally the seller of the Target group may agree to reinvest partof the sale proceeds or to leave some of the purchase price outstand-ing in the form of vendor debt.

This will usually be treated as akin to investor debt by the commer-cial lenders, that is, it will be subordinated (structurally and, if neces-sary, contractually) to their debt. However, on occasions, the vendormay insist on being treated as an arm’s-length third-party lender.How this debate concludes depends on the market and respectivenegotiating powers, but it will in all but the most exceptional cases besubordinated to the lender debt.

As between the investors and the seller, the terms of the vendor debtwill be a matter for negotiation though the vendor debt is likely torank ahead of and be repayable before any investor debt and beforepayment of any dividends to the investors. The vendor debt will mostprobably be unsecured (but if secured, it will not be secured at thesame level as the commercial lenders) and interest payments will rollup in the same way as (and for the same reasons as) for investor debt.

13.4.5 High-yield debt

Although high-yield debt (“HYD”) has fallen out of favour since thecredit crunch, this is likely to be only a temporary phenomenon andit is anticipated that it will re-establish itself as an important part ofthe funding structure for larger acquisitions.

A Practitioner’s Guide to Private Equity

254

HYD emerged from the US where it was a common feature of mostsizeable acquisitions. In Europe, however, HYD was really only seenin the larger acquisitions. This difference probably reflects the differ-ent maturity and depth of the two markets.

HYD has two significant attractions for the funds by whom it isprovided: it is long term in nature (typically more than 10 years) andit attracts a higher interest rate than can be earned on most other debtinstruments. The instrument is typically listed and is rated, so intheory (and in an orderly market) it is easily tradeable. These factorscombined to make HYD extremely popular with large institutionalfunds who were keen to allocate significant amounts of capital toHYD. In turn, this means that, in normal market conditions, HYD isan easily accessible source of funding for borrowers.

The key features of HYD are:

(a) Subordinated: HYD is subordinated to senior and mezzaninedebt, usually both structurally and contractually. In the structureconsidered here, it would be lent in at an intermediate Holdcolevel and on-lent by the intermediate Holdco to the Bidco.

(b) Collateral: HYD traditionally has limited collateral rights.Typically, it might have first-ranking security over the shares inthe borrower of the HYD and second-ranking security (behindthe senior and mezzanine lenders) in the on-loan to the Bidco ofthe HYD proceeds but no more. Recently, however, it hasbecome more common for the holders of the HYD to benefitfrom at least part of the guarantees and security given to thesenior and mezzanine lenders. Where this happens, it will beclear that the rights of the HYD holders (both to enforce and onrecovery following enforcement) rank behind those of the seniorlenders.

(c) Repayment and prepayment: repayment is in a bullet at the endof the term of the HYD. Prepayment is allowed but subject to amake-whole payment in respect of future interest payments.

(d) Interest payments: the interest periods are set at the time of theissue of the HYD and are generally quarterly. Interest isexpected to be kept current and provision will need to be madefor payments to be made by Bidco to the intermediate Holdcoto service the HYD. There will be a prohibition in the HYD

Debt

255

documents on any “burdensome covenant” under any otheragreement that restricts the payment of dividends or upstreamloans such that the HYD interest payments might be threatened.Interest is generally charged at a fixed rate.

(e) Covenants: HYD covenants will be more relaxed than covenantscontained in the senior debt for a combination of the followingreasons.The rate of return received by HYD holders is higher than thelenders of the senior debt, so it is appropriate that they takegreater risk and have less control.Whilst HYD holders are keen to receive information about thecredit and to ensure that the rating (and value) of their invest-ment is not under threat, they do not play as active a role in theday-to-day monitoring of the business of the borrower as thesenior lenders. Their function is one of investor, and they do notnecessarily have the same interest as the senior lenders in build-ing a long-term relationship with the borrower. Consequently,should it be necessary for the borrower to seek a waiver oramendment from the HYD holders, it is likely that they will seethis as an opportunity to get more return by requiring a “consentfee”. Naturally, the borrower wants to limit the occasions itmight need to approach the HYD holders and for this reasonsseeks less-restrictive terms. This is not reflected in the fact thatthere are few pure negative covenants (absolutely prohibitingactions) but instead a series of “incurrence” covenants thatallow, for example, the incurrence of new financial indebtednessor security provided certain financial covenant tests can be metboth before and after the new financial indebtedness or securityis incurred.

(f) Rated and listed: the pricing of HYD and its attraction to themarket will depend on what long-term debt rating is given to itby the institutional rating agencies. The rating agencies continueto monitor the debt throughout its life and this will affect themarketability of the investment.Listing the HYD adds to its marketability and attraction (andhence may result in cheaper rates). However, to maintain a list-ing a high degree of information must be published on a regularbasis and this can add considerably to the cost and burden of

A Practitioner’s Guide to Private Equity

256

HYD (especially as the reporting may extend to guarantors) andpotential liability for the issuer, its management and advisers.

13.4.6 Bridge financing

As explained above, bridge financing covers the period betweenwhen funding is needed to complete the acquisition and when it ispossible to effect an HYD issue (the proceeds of the HYD issue wouldbe used to repay the bridge financing).

The borrower under the bridge financing is likely to be the sameperson as the ultimate issuer of the HYD, whilst the lenders will bethe banks who agree to arrange and underwrite the HYD issue. Thebridge financing is likely to benefit from the same level of collateralas is proposed for the HYD.

The borrower will be incentivised to take out the bridge with theHYD at the earliest opportunity by periodic increases in the margincharged under the bridge: the longer it remains outstanding, the moreexpensive it gets, up to a capped amount. Fees are paid for arrangingthe bridge. Fees are also payable to the arrangers of the HYD, butthese are offset against the fees paid under the bridge. Again, toencourage the borrower to take out the bridge as soon as possible, therebate on the HYD arrangement fees reduces as time passes. In theevent that the bridge is not replaced by HYD after a period of time,the arrangers can call for the replacement of the bridge with HYDand, if they do not call within a certain period of the bridge beingdrawn (generally 12 months), the bridge financing will convert topermanent financing at the higher margin.

The bridge financing terms may be more relaxed than the senior facil-ities (and the borrower will want them to be akin to those for theHYD), but it is not unusual for de minimis carve-outs for the covenantsto be tighter, given the shorter-term nature of the borrowing.

13.5 The intercreditor deed

The various rankings of the different creditors of the group areaddressed by structural subordination in some instances but also byeach creditor signing up to an “intercreditor deed”.

Debt

257

The parties to this contractual arrangement will include eachborrower as well as each creditor. As it is likely that there will beintra-group loans, each member of the group will also participate inthe intercreditor arrangement by agreeing that, on acceleration of theinstitutional debt, their claims against their fellow group companieswill be subordinated to the claims of the institutional lenders and thatthey will not take any steps to accelerate or enforce any of their intra-group debt as long as the prior ranking debt remains outstanding.

The intercreditor deed is structured as a series of double protectioncovenants: the most junior creditor will covenant that, for example, itwill not take any security and will not demand repayment of its debtas long as the more senior debt is outstanding, and the relevantborrower will covenant that it will not give such security or makesuch payment. This is repeated in respect of each creditor.

There are a few provisions of interest, including:

(a) There will be a limit on the amount of additional senior debt thatcan be incurred by the borrower without the consent of the juniorlenders: the more senior debt is incurred, the less likely it is thatthe junior creditors will be paid out in full on an insolvency.

(b) The junior creditors agree certain “standstill periods” duringwhich, even if there is an event of default under their owninstrument, they cannot enforce if more senior debt is stilloutstanding. However, the lenders under the senior debt cannotsimply stand by and take no action, so prejudicing the juniorcreditors. To protect against this risk, it is agreed that after theexpiry of the standstill period, the junior creditors cancommence enforcement. This provision is often called “fish orcut bait”.

(c) Frequently, senior creditors can require junior creditors torelease any collateral they have or claims they have against theborrower group (though their debt remains to be settled) as thismay be the only way that the senior creditors can maximise thevalue of the borrower group on enforcement (the value wouldbe much less if the borrower group were to be sold subject tothat debt and security remaining in place). This can becontentious and it is not unusual for junior creditors to agree tothis only if an investment bank has certified that fair value is

A Practitioner’s Guide to Private Equity

258

being obtained and it is necessary to realise the full value of thegroup. One additional point to note here is that if the juniorcreditors have actual claims outstanding against the companybeing sold on enforcement by the senior creditors, the release ofthose claims may crystallise a tax gain in the released company(which again may depress its price).

(d) On enforcement, the security trustee need have regard only tothe instructions of the senior lenders until they are paid out infull, then the trustee has regard to the directions of the next mostsenior creditor, and so on.

(e) The intercreditor deed will contain various protections for thesecurity trustee and will also contain the provisions constitutingthe security trust.

(f) “Turnover trust” terms will be included such that if a juniorcreditor receives a payment that it should not have received, itagrees to hold that receipt on trust for and pay it over to thesenior creditors.

13.6 Guarantees and security

Lenders of senior debt expect to get the greatest possible level ofguarantees and security from the borrower group. In practice theremay be a number of companies in the group that are just too small tomerit the cost of taking guarantees or security and consequently thelenders usually agree that they may be excluded: a test of 2.5 per centto 5.0 per cent of the group’s EBITDA, revenue or gross assets is acommon threshold for this purpose, provided the banks get in aggre-gate from all such companies at least 75–85 per cent of the group’sEBITDA, revenue and gross assets. Compliance with these ratios isgenerally tested annually.

However, there are significant legal and fiscal constraints in a numberof jurisdictions on the giving of “upstream” and “cross guarantees”(i.e. guarantees by subsidiaries of their parent’s debt and guaranteesby one company of its sister company’s debt) and security supportingthose guarantees. Such constraints include:

(a) Financial assistance for the acquisition of a company’s ownshares or those of its parent. For example, if the Target was to

Debt

259

give a guarantee or security for the debt incurred by Bidco tobuy shares in the Target. In most European countries this isprohibited (sometimes it is illegal) or subject to limitations onthe amount that can be guaranteed. The effect of a breach canvary: it will almost invariably result in civil liability for the direc-tors of the company giving the guarantee/security, but it mayalso be unlawful (i.e. a criminal offence) for the directors and thecompany giving the guarantee. Importantly for the lendingbanks, the guarantee and security may be unenforceable.

(b) Corporate benefit. Typically in European jurisdictions guaran-tees and security can only be given if there is real corporatebenefit for the company giving the collateral. In establishingwhether there is corporate benefit, the interests of the individualcompany are often considered in isolation from the interests ofthe group as a whole. Corporate interest could be demonstrated,for example, in respect of the guarantee given for the debt of theBidco to the extent that such debt is intended to be on-lent to theguaranteeing company (e.g. to refinance existing debt on betterterms or to fund working capital needs). In the absence of corpo-rate benefit, the amount that can be guaranteed is typicallylimited to the amount of distributable reserves or such amountas would mean the company would be able to pay all of its othercreditors and avoid insolvency.

(c) Tax. Giving collateral can result in adverse tax treatment incertain jurisdictions and this should be considered early on inthe negotiations.

(d) General. It is important to agree, at an early stage in the negoti-ations, the principles on which security is to be taken.

In some jurisdictions the cost of taking security can almost outweighany advantage to the lenders, leaving the professionals that put it inplace or the local tax authorities as the only true beneficiaries. By wayof example, in some countries security attracts a tax based on thevalue of the asset or even the amount of debt that is being secured. Inmany jurisdictions the security needs to be notarised and in somecountries this can be very expensive.

Equally, whilst effecting the security may in itself be relatively cheap,the costs of perfecting it by registration can be costly (e.g. if it is neces-sary to register the IP security around the world).

A Practitioner’s Guide to Private Equity

260

Commercially, the steps needed to perfect security may not be accept-able. For example, to perfect a security assignment of a contract itmay be necessary to give notice to the borrower’s counterparty. If thecontract is sensitive, or if there are a series of contracts with customerswho may not understand the reason for the notice, this could be detri-mental to the business. In some instances, assignment or giving secu-rity over the contract may be prohibited by the terms of the contractor could lead to a breach, so jeopardising the existence of a valuablearrangement.

Bank accounts are particularly tricky, as the only way to obtain thebest form of security over them is to ensure that monies cannot bepaid out of them without the express approval of the security trusteeon a case-by-case basis. This is clearly impractical if the account is anoperating account.

All of these matters need to be negotiated and resolved ahead of sign-ing the loan document.

One final observation on security is that in most jurisdictions it issubject to “hardening periods”. This means that if the grantor of thesecurity becomes insolvent within a certain period of granting thesecurity (a period that can vary from months to years depending onthe jurisdiction), there is a risk that the security can be set aside. Thecircumstances in which this may happen and the possible defencesare beyond the scope of this chapter.

13.7 Upstream and cross-company loans

The main borrower, Bidco, will be a special purpose vehicle with noindependent revenue generating business. How, then, is it able tomeet its interest and principal payment obligations?

A proportion of its debt service requirements may be met by theTarget companies paying dividends to Bidco. However, this is not asecure arrangement as it depends on each company in the chainthrough which the dividends flow having distributable reserves. Ifone company has a significant realised loss, that may act as a “divi-dend block” and prevent the funds moving further to Bidco.

Debt

261

To cater for Bidco’s debt service requirements, it is common for the cash-generative operating companies to lend money up to Bidco as andwhen required. The arrangement is usually documented in a shortintra-group loan agreement. There are a few points to bear in mind here:

(a) this arrangement may amount to financial assistance (see above);(b) it may be necessary to demonstrate real corporate benefit for the