Interpreting Inner Mongolia’s Cultural Heritage: A Study ...

Upload

the-business-council-of-mongoliaCategory

view

174download

1

3rd Annual Mongolia – Trade and Commodity Finance Conference

Mongolia’s promise of mineral wealth

2

Contents

1. Global Mining – Macro

2. Near Term Outlook for Mongolia

3. Medium Term Outlook for Met Coal and Copper

4. Capital Markets

5. Attracting more investment

6. What ING can offer

Global Mining – MacroWeakening as demand remains sluggish and supply catches up

4

China’s growth has slowed...

Source: EMED data service, ING Bank

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1992

CN

Y bi

llion

s

Actual

1Q94-4Q01 Trend (8.7% growth)

1Q02-3Q08 Trend (11.5% growth)

1Q11-1Q14 Trend (7.7% growth)

China – Real GDP – Seasonally Adjusted

8

16

32

64

128

256

512

1024

2048

Post-WWII tofirst oil shock(9.2% growth)

Source: Bloomberg, ING Bank

Global Trade, US$ billions, 3 mma, log scale

Oil Shocks

Volc

ker

Rec

essi

on

Reagan Boom to Asian Crisis (9.5% growth)

China joins WTO(17%)

GFC and QE

911

SARS

Tech boom bust

SARS

5

0% 20% 40% 60% 80%

Iron Ore(seaborne)

Iron Ore(total)

Met Coal(seaborne)

Met Coal(total)

Lead

Aluminium

Copper

Nickel

Crude Oil

LNG

2006

2009

2012

2015

but expansion plans seem to have overshot

Source: UBS

China drives demand for commodities Supply has finally caught up (global supply growth since 2006)

-0.1 0.1 0.3 0.5 0.7 0.9 1.1

Iron Ore (seaborne)

Iron Ore (total)

Met Coal (seaborne)

Met Coal (total)

Lead

Aluminium

Copper

Nickel

Crude Oil

LNG

'06-'09

'06-'12

'06-'15

Source: IEA, CRU, UBS

Near term outlookExports and FDI remain under pressure

7

with prices are falling into the cost curve

Source: Bloomberg, GS, UBS

Copper Price relative to cost curve in USD / ton Seaborne Metallurgical Coal Price relative to cost curve in USD / ton

0

2,000

4,000

6,000

8,000

10,000

12,000

2006 2008 2009 2010 2012 2013 2014

C1 Cash Cost 75th percentile

C1 Cash Cost 90th percentile

90th percentile Sustaining Costs

0

50

100

150

200

250

300

350

2006 2008 2009 2010 2012 2013 2014

C1 Cash Cost 75th percentile

C1 Cash Cost 90th percentile

Sustaining Cash Costs

Source: WoodMackenzie, Bloomberg

8

-30

-20

-10

0

10

20

30

40

2010 2011 2012 2013

ConsumptionInvestmentNet Exports

Weaker prices and exports, and lower FDI

Source: EMED data service, ING Bank

Mongolia – Sources of GDP Growth – in %

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2008 2009 2010 2011 2012 2013 20140%

10%

20%

30%

40%

50%

60%

70%

80%

2008 2009 2010 2011 2012 2013

Mongolia - Reserve Money Growth - in % Mongolia – International Reserves – in USDm

OutlookCopper and Metallurgical Coal – medium term

10

Met Coal – limited structural upside

0

50

100

150

200

250

300

350

-5

0

5

10

15

20

2011 2012 2013 2014 2015 2016 2017

Surplus/Deficit Benchmark Forecast

0

1

2

3

4

5

6

7

8

9

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0%

10%

20%

30%

40%

50%

60%

70%

Jan/11 Jun/12 Oct/13 Mar/15 Jul/16

Chinese Imports - in million tons per month Will this further displace Mongolian Metallurgical Coal?

Market Position Seaborne Coking Coal– million tons per annum

Source: Chinese Customs

Source: AME, Analyst Concensus Source: Anglo American Mongolia, Analyst Concensus

11

Copper – ST downside, structural support

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

-

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014

CCFD SHFE Comex

LME Copper Price

Copper Inventories – high but reducing – in days of production

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014F 2015F 2016F

Capex Spend

Supply Growth

Copper Production – Significant Expansion Growth

0 5,000 10,000 15,000

-5,000

-3,000

-1,000

1,000

3,000

5,000

7,000

9,000

But Supported by the cash cost curve

Capital MarketsStrong Bank Liquidity – weak equity markets

13

Drop in prices is hurting valuations

Source: ING, Bloomberg

Equity Valuations by Commodity Class - in % from 2010 peak

-80%

-60%

-40%

-20%

0%

20%

40%

60%

2010 2011 2012 2012 2013 2013 2014 2014

BBG World Coal Equity Index

Gold Equities

Copper Equities

Iron Ore Equities

2007 2008 2008 2009 2009 2010 2010

14

0

200

400

600

800

1,000

1,200

1,400

4/1/

2008

7/1/

2008

10/1

/200

8

1/1/

2009

4/1/

2009

7/1/

2009

10/1

/200

9

1/1/

2010

4/1/

2010

7/1/

2010

10/1

/201

0

1/1/

2011

4/1/

2011

7/1/

2011

10/1

/201

1

1/1/

2012

4/1/

2012

7/1/

2012

10/1

/201

2

1/1/

2013

4/1/

2013

7/1/

2013

10/1

/201

3

1/1/

2014

putting the exploration sector on life support

Source: SNL Metal Strategies 2014

Total Equity Raised for the mining sector – in USD million (TSX, ASX) Global Exploration Spending - in USD billion

0.0

5.0

10.0

15.0

20.0

25.0

Source: SNL Metal Strategies

Equity market effectively closed

15

-500

-300

-100

100

300

500

700

900

1,100

1,300

1,500Mines Closed Pre-Feasibility on Hold Feasibility Cancelled New Mines Pre Feasibility Feasibility Studies

and halting new mine development studies

Source: SNL Metal Strategies 2014

Newly added in situ resources by value - in USD million

Hardly any feasibility work

16

but Bank market liquidity remains strong

Source: Dealogic

Total Metals & Mining Bank Debt Volumes, USD million

0

20

40

60

80

100

120

140

160

180

200

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

EMEA Asia Americas Deals

Preparing for the next cycleMarket perception and sentiment will be key

18

Mongolia – lost the hype?

19

Obvious potential for mineral wealth...Plenty of Potential – Geological Potential

Mongolia

Source: 2012/2013 Fraser Institute Ranking of Potential

Mongolia

Held back by regulatory environment – Policy Perception

20

...but realising that requires a reliable partnerMine development nowadays takes in excess of 10 years from discovery

81st37th 49th36th52nd

Purported Erdenet Default on SB loan

SEFIL / Southgobi

Chalco Dispute On TT prepay

New Mining Law

Suspension of exploration licenses

Desire to renegotiate the OT investment agreement

Khan / ARMZ sage – in arbitration

OT Investment Agreement

AwardedTT IPO Process, partner search

2009 2010 2011 2012 2013 2014

??

OT Financing Agreed OT Financing Delayed

Suspended

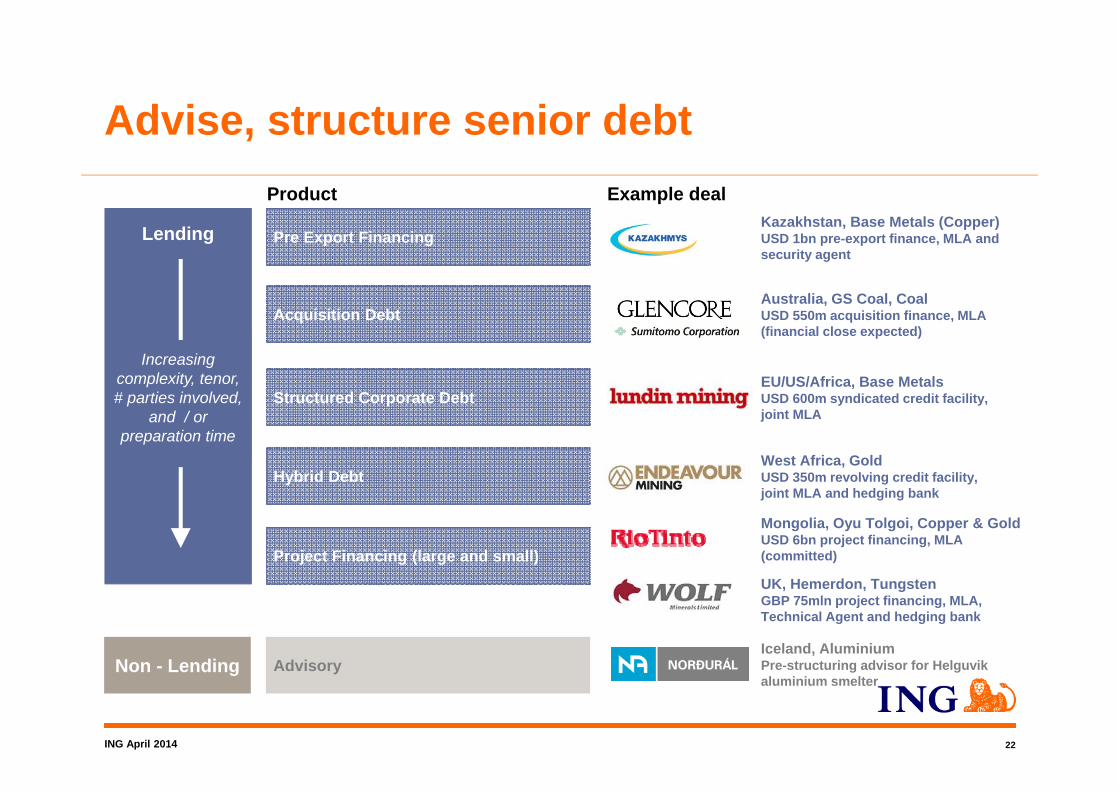

What ING can do and can provide Senior Debt across the spectrum for mining companies

ING April 2014 22

Lending

Advise, structure senior debt

Non - Lending AdvisoryIceland, Aluminium Pre-structuring advisor for Helguvikaluminium smelter

Project Financing (large and small)UK, Hemerdon, TungstenGBP 75mln project financing, MLA, Technical Agent and hedging bank

Hybrid DebtWest Africa, Gold USD 350m revolving credit facility, joint MLA and hedging bank

Pre Export Financing

EU/US/Africa, Base MetalsUSD 600m syndicated credit facility, joint MLA

Acquisition DebtAustralia, GS Coal, CoalUSD 550m acquisition finance, MLA (financial close expected)

Kazakhstan, Base Metals (Copper)USD 1bn pre-export finance, MLA and security agent

Example dealProduct

Increasing complexity, tenor, # parties involved,

and / or preparation time

Structured Corporate Debt

Mongolia, Oyu Tolgoi, Copper & GoldUSD 6bn project financing, MLA (committed)

ING April 2014 23

Advise, structure senior debt

Development FundingMine in Production

Technical Due Diligence Mine Plan, operating costs, sustaining capex

Environmental Plans, reviewed by ESR consultantEnvironmental Due Diligence Equator Principles, ESIA, and Action Plans

Class I Feasibility Study, capital costing, equipment strategy

Offtake Agreements Clear Volume and Pricing Basis

Repayment Offshore, withheld from exports Offshore flowing into a controlled waterfall,

Clear Volume / Pricing Basis, tenor exceeding loan

Tenor Up to 3 years Up to 12 years, depending on ECA cover eligibility

Debt Sizing Full payout, Leverage not to exceed 2.0x EBITDA Full payout, Leverage not to exceed 2.0x EBITDA

Price Assumptions Low minus 10% Base Case – based on Market DD

Providers Banks and Traders Banks, ECAs, Multilaterals

Questions?