1.3 Reliability

15

1.3 RELIABILITY

-

Upload

vce-accounting-michael-allison -

Category

Education

-

view

61 -

download

2

Transcript of 1.3 Reliability

1.3 RELIABILITY

Videos of this presentation at…

YouTube Channel for VCE Accounting

© Michael Allison. Author’s permission required for external use.

1.3 RELIABILITY

The Rules of Accounting

Relevance

Reliability

Comparability

Understandability

Entity

Historical cost

Going concern

Reporting period

Monetary unit

Conservatism

Consistency

Qualitative Characteristics

Accounting Principles

© Michael Allison. Author’s permission required for external use.

ReliabilityOnly information that is reliable should be included in the

firm’s accounting reports

So what is reliable information?

1.3 RELIABILITY

Definition:

Information is reliable if it:

• Is free from error, personal opinions and estimates

• Is based on data that can be checked or verified

• Has a source document to verify it

© Michael Allison. Author’s permission required for external use.

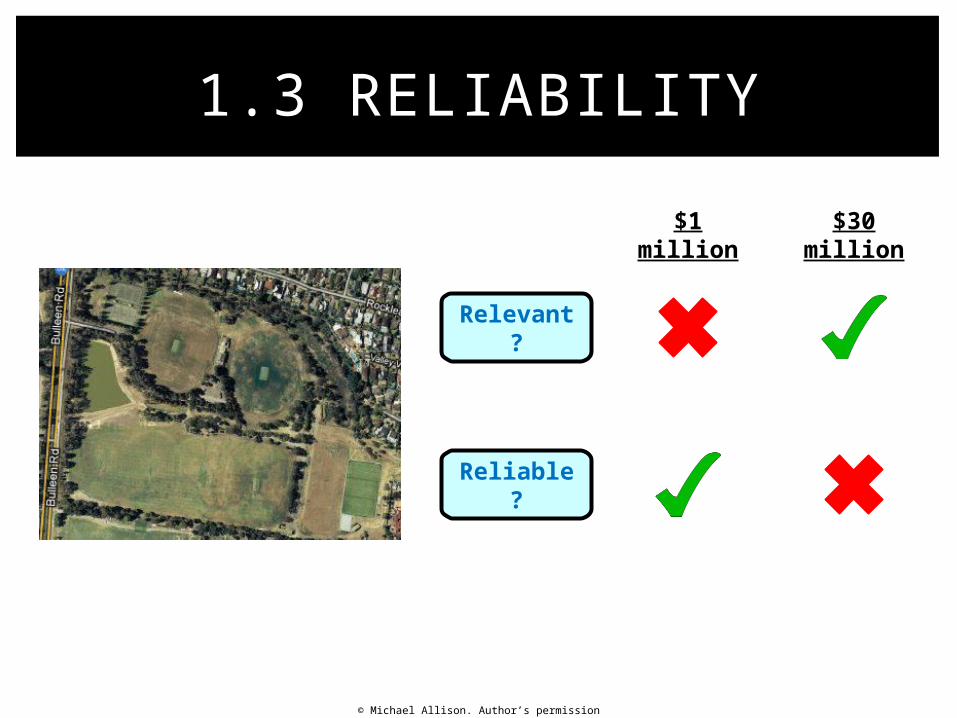

Relevance vs. Reliability In 1985 Trinity bought the

land at Bulleen for $1m

30 years later it is estimated that the land is now valued at $30m

Which amount should Trinity show in its Balance Sheet?

1.3 RELIABILITY

© Michael Allison. Author’s permission required for external use.

1.3 RELIABILITY

Relevant?

Reliable?

$1 million

$30 million

© Michael Allison. Author’s permission required for external use.

TASK

In-class Homework

Cambridge Revision Question 1.5 – Reliability X

SQ21 X

© Michael Allison. Author’s permission required for external use.

Internal control involves the practices involved to ensure that:

• Accounting records and reports are accurate and reliable

• The firm’s Assets are protected from theft, fraud and misrepresentation

1.3 RELIABILITY

© Michael Allison. Author’s permission required for external use.

Example: ensuring the firm’s accounting records and reports are accurate and reliable

A supplier called Lana’s Landscapes sends us (Playgrounds Galore) a statement showing our account with their firm…

1.3 RELIABILITY

How can we check this is

accurate and reliable?

According to Lana’s Landscapes, we owe them

$7,040

© Michael Allison. Author’s permission required for external use.

1.3 RELIABILITY

Playgrounds Galore

• We should have a ledger showing the balance that we have

• We should have copies and originals of each of the documents that have been issued during the month

Creditor – Lana’s Landscapes8/5 Cash 2043 1/5 Balance 2150

8/5 Discount exp

107 7/5 Sales/GST 5500

18/5 Stock 660 23/5 Sales/GST 2200

31/5

Balance 7040

9850 9850

1/6 Balance 7040Credit Note

© Michael Allison. Author’s permission required for external use.

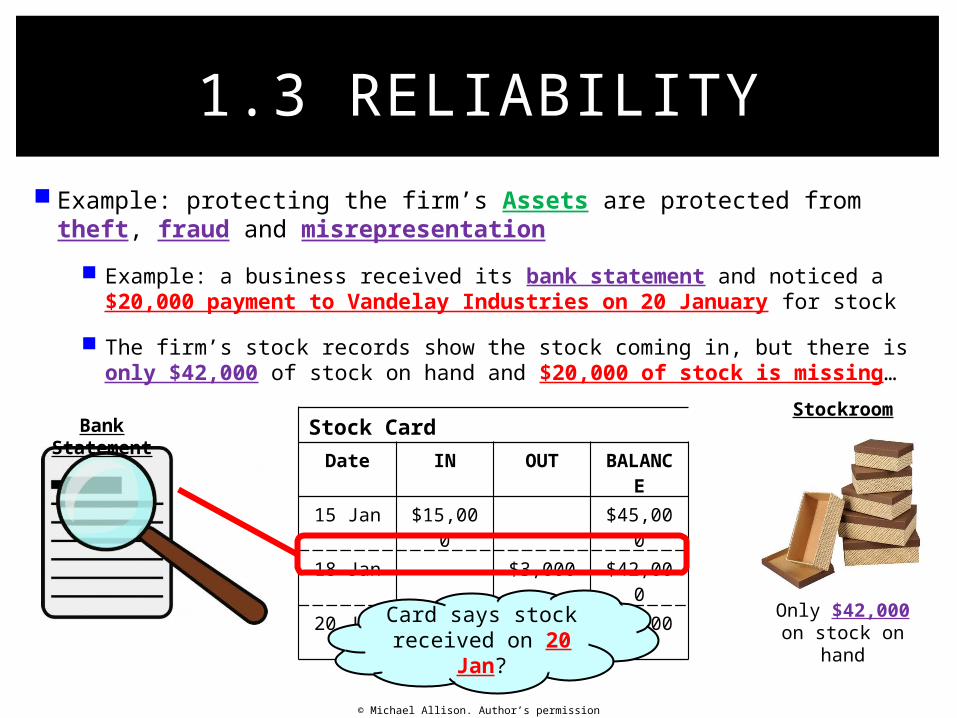

Example: protecting the firm’s Assets are protected from theft, fraud and misrepresentation

Example: a business received its bank statement and noticed a $20,000 payment to Vandelay Industries on 20 January for stock

The firm’s stock records show the stock coming in, but there is only $42,000 of stock on hand and $20,000 of stock is missing…

1.3 RELIABILITY

Bank Statement

Stock Card

Date IN OUT BALANCE

15 Jan $15,000 $45,000

18 Jan $3,000 $42,000

20 Jan $20,000 $62,000

Card says stock received on 20

Jan?

Stockroom

Only $42,000 on stock on

hand

© Michael Allison. Author’s permission required for external use.

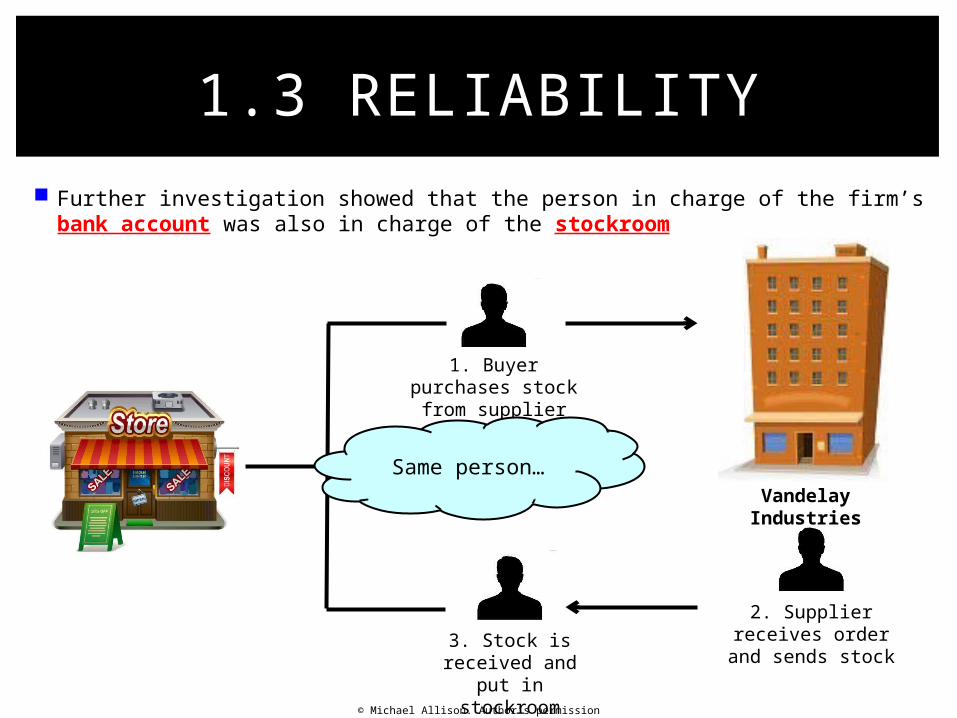

Further investigation showed that the person in charge of the firm’s bank account was also in charge of the stockroom

1.3 RELIABILITY

1. Buyer purchases stock

from supplier

2. Supplier receives order and

sends stock

Vandelay Industries

3. Stock is received and put

in stockroom

Same person…

© Michael Allison. Author’s permission required for external use.

What can be done to ensure internal control?

• Well-defined responsibilities for staff – clear who is in charge of what

• Separation of duties – tasks are broken up between several staff rather than one person in charge of an entire process

• Rotation of duties – staff are rotated between tasks over time rather than doing the same task for a long time

• Authorisation rules enforced – staff must get required approval for all tasks

• Document control – the accounting system must accurately record and store all documents (receipts, invoices, statements etc.)

• Physical safeguards and checks – for protection of cash and stock, e.g. safes, security tags

1.3 RELIABILITY

© Michael Allison. Author’s permission required for external use.

Internal control helps fulfil Reliability as it requires:

• Source documents must be kept

• These can be used to verify transactions that have taken place (or not taken place)

• This ensures accounting information is accurate and reliable

• And this minimises the chance of theft and fraud

1.3 RELIABILITY

© Michael Allison. Author’s permission required for external use.

TASK

In-class Homework

SQ27 X