12 Chapter 10 - Treasurycomparativetaxation.treasury.gov.au/.../downloads/12_Chapter_10.pdf · •...

32

Chapter 10 International taxation arrangements

-

Upload

truongthuan -

Category

Documents

-

view

215 -

download

0

Transcript of 12 Chapter 10 - Treasurycomparativetaxation.treasury.gov.au/.../downloads/12_Chapter_10.pdf · •...

Chapter 10International taxation arrangements

Contents

Summary 301

10.1 Introduction 301

10.2 Residence 302

10.3 Treatment of foreign source income 30510.3.1 Treatment of an individual’s foreign source income 30510.3.2 Treatment of a company’s foreign source income 31210.3.3 Foreign tax credit (FTC) systems 315

10.4 Treatment of income of non-residents 31910.4.1 Treatment of conduit income 324

10.5 Attribution and other international tax integrity rules 325

10.6 Tax treaties 327

Page 301

10. INTERNATIONAL TAXATION ARRANGEMENTS

SUMMARY

Australia’s international taxation arrangements are consistent with OECD practice and the other OECD-10 countries in the following areas:

• the application of its domestic taxation system to cross-border investment and transactions (inbound and outbound);

• the taxation of temporary residents1; and

• the taxation of dividends, interest and royalties paid to non-residents, although some countries have zero withholding tax rates on these payments, while others have extended withholding taxes to a broader range of non-resident income.

In some areas, Australia’s international taxation arrangements differ, for example:

• Australia’s treatment of the capital gains of non-residents and foreign losses2; and

• Australia has an extensive foreign business income exemption for its companies and does not tax foreign business income flowing through Australian companies to foreign shareholders.

The extent of Australia’s attribution rules, which prevent residents accumulating passive income (such as dividends and interest) in non-resident entities in low-tax countries to defer Australian tax, is broadly similar to those in other OECD-10 countries. Australia also has other international tax integrity rules, as do the rest of the OECD-10.

10.1 INTRODUCTION

International tax arrangements involve modifications to the normal rules of a country’s domestic income tax system where they interact with the tax system of another country as a result of cross-border investments or transactions. They form part of the personal and corporate tax bases and seek to enhance the economic benefits derived from cross-border activities (or limit the economic costs of them). The balance between the costs and benefits of cross-border activities and the consequent international tax rules may vary depending on the circumstances of a particular country.

1 The Australian Government announced in the 2005-06 Budget (and has recently introduced legislation to Parliament) measures to align more closely its tax treatment of temporary residents to that of other countries.

2 Reforms announced in the 2005-06 Budget will address these areas and bring Australia into line with other OECD-10 countries.

International comparison of Australia’s taxes

Page 302

• For example, inbound foreign direct investment may be valued more highly by a net capital-importing country than by a net capital-exporting country. As a result, the capital-importing country may decide to modify its domestic tax law to a larger degree to accommodate this type of activity (for example, reduce the non-resident withholding tax rate or base). Conversely, if it is in need of more revenue and it perceives its inbound investments as being sufficiently profitable, then it may choose to increase the source taxation on those inbound investments (for example, increase the non-resident withholding tax rate or base).

To compare international tax arrangements, it is necessary to consider the basis on which tax is levied — the residence of the taxpayer or the source of the income. This chapter considers ‘residence’ and ‘source’ for international tax purposes (to tax foreign source income), and compares tax residence rules for both natural and legal persons across the OECD-10. It goes on to look at the tax treatment of foreign source income, firstly for individuals (including for temporary residents) and then for companies. It then compares the foreign tax credit (FTC) systems (with a company focus) across the OECD-10.

The tax treatment of the income of non-residents, including conduit income (for example, foreign business income earned by a resident company and distributed to non-resident shareholders), is then considered, followed by commonly used international tax integrity rules. The chapter concludes with a comparison of tax treaty networks and features across the OECD-10.

Box 10.1: Australia and the Review of International Taxation Arrangements (RITA) Australia recently reviewed many of its international tax arrangements (and continues to implement recommendations/commitments from the review, including the changes announced in the 2005-06 Budget). The review focused on ensuring that, in an increasingly integrated global business environment, Australia’s tax system was not hindering its attractiveness as a place for multinational business and investment. One of the key outcomes was the reduction in, and streamlining of, Australia’s taxation of inbound, outbound and conduit investment. By doing so, it will potentially raise the attractiveness of outbound investment and regional headquarter activity from Australia, increase its attractiveness to inbound foreign investment and help reduce its cost of capital.

Ensuring that international tax arrangements are not discouraging these cross-border investments is a key focus for many countries, including Australia.

10.2 RESIDENCE

Generally, countries tax both residents and non-residents on domestic source income. Tax residence rules usually extend the taxation of residents to their foreign source income.

• Residence is an international tax law construct used to tax the legal and natural persons of a country on their foreign source income. Without such a construct, a country would only be able to tax these persons on their domestic source income (see Box 10.2).

As a result, only resident taxpayers tend to be taxed on their worldwide income whereas non-resident taxpayers are generally only taxed on their domestic source income

Chapter 10: International taxation arrangements

Page 303

(see Box 10.3). Some countries have a territorial tax system which only taxes income arising within their own borders, irrespective of the residence of the taxpayer. Key reasons for taxing the foreign source income of residents are to achieve horizontal and vertical equity goals, and to improve the tax neutrality of investment decisions (efficiency).

Box 10.2: Residency rules All countries have residence tests for both natural persons (individuals) and legal persons (companies). These tests can be based on legal form and/or economic form (substance).

The tax residence of individuals is usually based on either: physical presence in the country (legal form, such as citizenship); facts and circumstances that prove residence in a country (economic substance, such as the country where the person has a fiscal presence); or a combination of the two. In many cases, this may be satisfied simply by being present in a country for a set period of time, such as 183 days.

The tax residence of companies (that is, where companies are established or carry on business) is usually based on either place of incorporation (legal seat), location of management (real seat) or a combination of the two.

Residency rules have an important role to play in tax treaties as they clarify the right to tax and assist in the avoidance of double taxation.

Box 10.3: Source rules Broadly, source rules operate to identify income arising within a country’s geographical boundaries.

The term ‘source’ is not defined in Australia’s tax legislation. Australia’s source rules are derived from a combination of common law, statutory provisions and Australia’s tax treaties. For example, Australia has statutory source rules which identify profits arising from certain import and export sales as having an Australian source.

The common law has developed a range of principles which operate in the absence of statutory provisions. Whether or not the income will be seen to be sourced in Australia under the common law principles is a question of fact in the circumstances of the particular case.

In addition, Australia is largely unique in the world in that its tax treaties contain source rules that empower Australia to exercise taxing rights that are allocated to it by the treaty even when domestic law may not otherwise provide source country taxing rights.

International practice varies as to the nature and extent of the source rules. Generally, countries use geographical boundaries, types of income, or a mixture of both to determine the extent to which they will seek to tax income sourced in their jurisdiction.

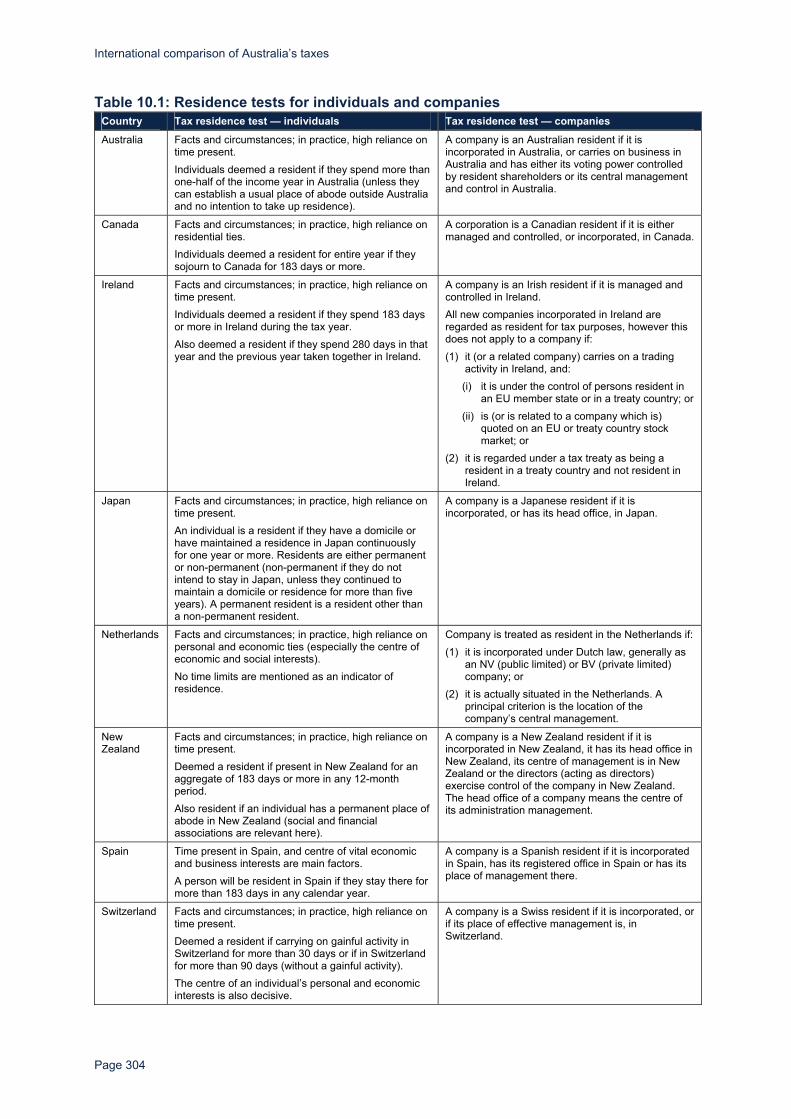

Table 10.1 shows for the OECD-10 the basis of the residence test for both individuals and companies.

International comparison of Australia’s taxes

Page 304

Table 10.1: Residence tests for individuals and companies Country Tax residence test — individuals Tax residence test — companies

Australia Facts and circumstances; in practice, high reliance on time present. Individuals deemed a resident if they spend more than one-half of the income year in Australia (unless they can establish a usual place of abode outside Australia and no intention to take up residence).

A company is an Australian resident if it is incorporated in Australia, or carries on business in Australia and has either its voting power controlled by resident shareholders or its central management and control in Australia.

Canada Facts and circumstances; in practice, high reliance on residential ties. Individuals deemed a resident for entire year if they sojourn to Canada for 183 days or more.

A corporation is a Canadian resident if it is either managed and controlled, or incorporated, in Canada.

Ireland Facts and circumstances; in practice, high reliance on time present. Individuals deemed a resident if they spend 183 days or more in Ireland during the tax year. Also deemed a resident if they spend 280 days in that year and the previous year taken together in Ireland.

A company is an Irish resident if it is managed and controlled in Ireland. All new companies incorporated in Ireland are regarded as resident for tax purposes, however this does not apply to a company if: (1) it (or a related company) carries on a trading

activity in Ireland, and: (i) it is under the control of persons resident in

an EU member state or in a treaty country; or (ii) is (or is related to a company which is)

quoted on an EU or treaty country stock market; or

(2) it is regarded under a tax treaty as being a resident in a treaty country and not resident in Ireland.

Japan Facts and circumstances; in practice, high reliance on time present. An individual is a resident if they have a domicile or have maintained a residence in Japan continuously for one year or more. Residents are either permanent or non-permanent (non-permanent if they do not intend to stay in Japan, unless they continued to maintain a domicile or residence for more than five years). A permanent resident is a resident other than a non-permanent resident.

A company is a Japanese resident if it is incorporated, or has its head office, in Japan.

Netherlands Facts and circumstances; in practice, high reliance on personal and economic ties (especially the centre of economic and social interests). No time limits are mentioned as an indicator of residence.

Company is treated as resident in the Netherlands if: (1) it is incorporated under Dutch law, generally as

an NV (public limited) or BV (private limited) company; or

(2) it is actually situated in the Netherlands. A principal criterion is the location of the company’s central management.

New Zealand

Facts and circumstances; in practice, high reliance on time present. Deemed a resident if present in New Zealand for an aggregate of 183 days or more in any 12-month period. Also resident if an individual has a permanent place of abode in New Zealand (social and financial associations are relevant here).

A company is a New Zealand resident if it is incorporated in New Zealand, it has its head office in New Zealand, its centre of management is in New Zealand or the directors (acting as directors) exercise control of the company in New Zealand. The head office of a company means the centre of its administration management.

Spain Time present in Spain, and centre of vital economic and business interests are main factors. A person will be resident in Spain if they stay there for more than 183 days in any calendar year.

A company is a Spanish resident if it is incorporated in Spain, has its registered office in Spain or has its place of management there.

Switzerland Facts and circumstances; in practice, high reliance on time present. Deemed a resident if carrying on gainful activity in Switzerland for more than 30 days or if in Switzerland for more than 90 days (without a gainful activity). The centre of an individual’s personal and economic interests is also decisive.

A company is a Swiss resident if it is incorporated, or if its place of effective management is, in Switzerland.

Chapter 10: International taxation arrangements

Page 305

Table 10.1: Residence tests for individuals and companies (continued) Country Tax residence test — individuals Tax residence test — companies

United Kingdom

Facts and circumstances; in practice, high reliance on time present. Individual regarded as a resident for an income tax year if they spend an aggregate of 183 days in the United Kingdom for that tax year, or if habitually visiting the United Kingdom for more than 91 days or more in four consecutive years (residence from the fifth year). There is also strong reliance on the maintenance of a permanent home in the United Kingdom.

A company is a United Kingdom resident if its central management and control is in the United Kingdom, or it is incorporated in the United Kingdom.

United States

Time present in the United States, lawful permanent residence and citizenship. An individual is treated as a resident of the United States under the substantial presence test for a calendar year if: they spend 31 days or more in the United States; or if the sum of the days present in the United States during the current year, plus one-third the number of days present in the first preceding calendar year, plus one-sixth the number of days present in the second preceding year, equals 183 days or more.

A company is a United States resident if it is incorporated under the laws of any State in the United States.

Source: Various, see Chapter 1 (1.4.1). Most of the OECD-10, including Australia, supplement their residence tests for both individuals and companies with substance-based tests. Without these tests, individuals and companies may be able quite easily to reduce or avoid worldwide income taxation by migrating (in legal form) to a low-tax country without their underlying economic circumstances changing.

For individuals, the majority of the OECD-10, including Australia, have a residence test based upon the facts and circumstances of the case. The most common factor appears to be time present in the country. Most countries consider that around six months (183 days) is sufficient to establish residency unless there are other facts to suggest otherwise regardless of time spent.

For companies, only the United States relies solely on the incorporation test to establish residence.3 All other countries in the OECD-10, including Australia, have some form of management or control test as a part of their company residence test.

10.3 TREATMENT OF FOREIGN SOURCE INCOME

10.3.1 Treatment of an individual’s foreign source income

As noted, resident individuals are generally taxed on their worldwide income while non-resident individuals are generally only taxed on their domestic source income. But some individuals have features of both residents and non-residents. A common example is foreign long-stay individuals, often referred to as ‘temporary residents’ or ‘expatriates’, who may work in a country for more than half a year (when they might ordinarily become residents)

3 The United States has experienced some difficulties in recent times with resident companies migrating in legal form to low-tax countries in part because of such a black and white test.

International comparison of Australia’s taxes

Page 306

but are not permanent (for example are on work visas — quasi-non-resident). Many countries specifically cater for these individuals by not taxing them on their worldwide income unless their temporary nature becomes permanent (however determined). These rules are intended to improve the attractiveness of countries to internationally mobile labour.

Table 10.2 shows for the OECD-10 what constitutes temporary residence and compares the tax treatment of their income with that of ordinary resident and non-resident individuals.

Page 307

Chapter 10: International taxation arrangements

Page 307

Tabl

e 10

.2: C

ompa

ring

tax

trea

tmen

t of t

empo

rary

resi

dent

s (e

xpat

riate

s) w

ith re

side

nt a

nd n

on-r

esid

ent i

ndiv

idua

ls

Cou

ntry

K

ey te

mpo

rary

re

side

nce

rule

s (e

xpat

riate

s)

Liab

ility

to ta

x Ta

x ra

tes

Tax

base

(inc

ludi

ng s

ocia

l sec

urity

con

trib

utio

ns/o

blig

atio

ns o

f em

ploy

ees

and

empl

oyer

s)

Aus

tralia

(a)

No

spec

ific

rule

s ex

ist f

or te

mpo

rary

re

side

nts.

Th

ere

are

som

e ex

empt

ions

for

shor

t-ter

m a

nd

‘exe

mpt

’ vis

itors

.

Res

iden

ts: w

orld

wid

e in

com

e.

Exp

atria

tes:

ther

e is

no

sepa

rate

cat

egor

y of

te

mpo

rary

resi

dent

s, s

o lia

bilit

y to

tax

depe

nds

on s

tatu

s as

resi

dent

or

non-

resi

dent

. The

re is

a

limite

d ex

empt

ion

for

‘exe

mpt

vis

itors

’ fro

m

the

fore

ign

inve

stm

ent

fund

rule

s fo

r fou

r yea

rs

prov

ided

they

are

ho

lder

s of

a te

mpo

rary

vi

sa. A

lso

an e

xem

ptio

n fro

m th

e C

GT

deem

ed

disp

osal

rule

(whi

ch

appl

ies

whe

n re

side

nts

beco

me

non-

resi

dent

s)

for s

hort-

term

resi

dent

s (th

at is

, ind

ivid

uals

who

ha

ve o

nly

been

re

side

nts

for l

ess

than

5

of th

e pa

st 1

0 ye

ars)

on

pre-

resi

denc

e or

be

quea

thed

ass

ets.

N

on-r

esid

ents

: A

ustra

lian

sour

ce

inco

me.

Inco

me:

resi

dent

s ar

e ta

xed

at

redu

ced

rate

s, c

ompa

red

with

no

n-re

side

nts,

at i

ncom

es le

ss

than

A$2

1,60

0.

Cap

ital g

ains

: oth

er th

an

diffe

renc

e in

rate

s re

ferr

ed to

ab

ove,

no

diffe

renc

e be

twee

n no

n-re

side

nts

and

resi

dent

s (c

apita

l gai

ns a

re a

ggre

gate

d w

ith in

com

e).

Inco

me:

min

or re

lief f

or s

uppo

rt of

dep

enda

nts

avai

labl

e to

resi

dent

s. M

edic

are

(com

puls

ory

med

ical

insu

ranc

e sy

stem

) rig

hts

and

oblig

atio

ns a

re n

ot a

pplic

able

to n

on-r

esid

ents

. C

apita

l gai

ns: c

ompr

ehen

sive

(res

iden

ts) A

ustra

lian

land

, bus

ines

s as

sets

and

dire

ct in

tere

sts

in A

ustra

lian

entit

ies

(non

-res

iden

ts).

Exp

atria

te tr

eatm

ent o

f cap

ital g

ains

will

dep

end

on

whe

ther

they

are

con

side

red

a re

side

nt o

r non

-res

iden

t. G

ains

are

incl

uded

in ta

xabl

e in

com

e, a

nd th

eref

ore

pote

ntia

lly s

ubje

ct to

diff

eren

t rat

es a

s be

twee

n re

side

nts

and

non-

resi

dent

s.

International comparison of Australia’s taxes

Page 308

Tabl

e 10

.2: C

ompa

ring

tax

trea

tmen

t of t

empo

rary

resi

dent

s (e

xpat

riate

s) w

ith re

side

nt a

nd n

on-r

esid

ent i

ndiv

idua

ls (c

ontin

ued)

C

ount

ry

Key

tem

pora

ry

resi

denc

e ru

les

(exp

atria

tes)

Liab

ility

to ta

x Ta

x ra

tes

Tax

base

(inc

ludi

ng s

ocia

l sec

urity

con

trib

utio

ns/o

blig

atio

ns o

f em

ploy

ees

and

empl

oyer

s)

Can

ada

Non

e R

esid

ents

: wor

ldw

ide

inco

me.

E

xpat

riate

s: n

/a.

Non

-res

iden

ts:

Can

adia

n so

urce

in

com

e.

Inco

me:

no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Cap

ital g

ains

: no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Inco

me:

min

or re

lief f

or s

uppo

rt of

dep

enda

nts

avai

labl

e to

resi

dent

s. C

anad

a ha

s a

prov

inci

al

med

ical

insu

ranc

e sy

stem

. The

met

hod

of fu

ndin

g va

ries

from

pro

vinc

e to

pro

vinc

e.

Com

puls

ory

med

ical

insu

ranc

e sy

stem

righ

ts a

nd o

blig

atio

ns a

re n

ot a

pplic

able

to

non-

resi

dent

s.

Em

ploy

ees

and

empl

oyer

s m

ust c

ontri

bute

to th

e em

ploy

men

t ins

uran

ce fu

nd. T

he m

axim

um

cont

ribut

ion

for a

n em

ploy

ee is

C$7

29 a

nd fo

r em

ploy

ers

C$1

,021

(em

ploy

ee c

ontri

butio

ns a

re

C$1

.87

and

empl

oyer

con

tribu

tions

are

C$2

.62

per C

$100

of I

nsur

able

ear

ning

s); m

axim

um

Insu

ranc

e ea

rnin

gs is

C$3

9,00

0. A

cces

s to

mos

t soc

ial p

rogr

amm

es is

rest

ricte

d to

resi

dent

s.

Can

adia

n pe

nsio

n pl

an c

ontri

butio

ns a

re re

quire

d on

ann

ual e

arni

ngs

(as

at 2

005)

exc

eedi

ng

C$3

,500

(to

max

of C

$41,

100)

; con

tribu

tion

rate

is 4

.95

per c

ent o

f suc

h ea

rnin

gs (s

plit

betw

een

empl

oyer

and

em

ploy

ee).

Som

e ju

risdi

ctio

ns in

Can

ada

impo

se a

form

al p

ayro

ll ta

x (N

ewfo

undl

and,

Man

itoba

, Que

bec,

O

ntar

io, t

he N

orth

wes

t ter

ritor

ies

and

Nun

avut

). C

apita

l gai

ns: c

ompr

ehen

sive

(res

iden

ts) C

anad

ian

land

, Can

adia

n bu

sine

ss a

sset

s an

d di

rect

in

tere

sts

in C

anad

ian

com

pani

es a

nd tr

usts

(non

-res

iden

ts).

Irela

nd

Res

iden

t, bu

t not

or

dina

rily

dom

icile

d in

Ire

land

.

Res

iden

ts: w

orld

wid

e in

com

e.

Exp

atria

tes:

inco

me

from

an

Irish

sou

rce

and

Uni

ted

Kin

gdom

em

ploy

men

t and

oth

er

fore

ign

sour

ce in

com

e re

mitt

ed to

Irel

and.

N

on-r

esid

ents

: Iris

h so

urce

inco

me.

Inco

me:

non

-res

iden

ts a

re n

ot

entit

led

to p

oten

tially

low

er ra

tes

asso

ciat

ed w

ith jo

int

asse

ssm

ent.

Cap

ital g

ains

: no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Inco

me:

non

-res

iden

ts a

re n

ot ta

xed

on in

tere

st fr

om g

over

nmen

t sec

uriti

es. R

esid

ents

are

ab

le to

cla

im in

tere

st d

educ

tions

(cap

ped)

on

hom

e lo

ans

used

for a

prin

cipa

l res

iden

ce;

non-

resi

dent

s un

likel

y to

hav

e Iri

sh p

rinci

ple

resi

denc

e.

All

Irish

resi

dent

s ar

e en

title

d to

cer

tain

bas

ic h

ealth

car

e se

rvic

es. A

ll em

ploy

ees

and

self-

empl

oyed

indi

vidu

als

othe

r tha

n m

edic

al c

ard

hold

ers

mus

t pay

a h

ealth

con

tribu

tion

levy

of

2 p

er c

ent o

f the

ir gr

oss

earn

ings

(if a

nnua

l inc

ome

is a

t lea

st €

22,8

80).

In

term

s of

soc

ial s

ecur

ity, a

ll em

ploy

ed a

nd s

elf-e

mpl

oyed

indi

vidu

als

and

empl

oyer

s co

ntrib

ute

to th

e so

cial

wel

fare

fund

(em

ploy

ers

10.7

5 pe

r cen

t on

all i

ncom

e; e

mpl

oyee

s 4

per c

ent o

n in

com

e up

to €

46,6

00 (f

rom

200

6); s

elf-e

mpl

oyed

app

roxi

mat

ely

3 pe

r cen

t on

all

inco

me)

. Soc

ial s

ecur

ity c

ontri

butio

ns a

re n

ot d

educ

tible

aga

inst

inco

me.

The

se b

enef

its a

re

larg

ely

limite

d to

resi

dent

s.

Cap

ital g

ains

: com

preh

ensi

ve (r

esid

ents

). C

ompr

ehen

sive

, but

fore

ign

gain

s on

ly ta

xed

on

rem

ittan

ce b

asis

(exp

atria

tes)

. Iris

h la

nd, I

rish

busi

ness

ass

ets

and

shar

es in

Iris

h la

nd o

r bu

sine

ss a

sset

rich

non

-list

ed c

ompa

nies

(non

-res

iden

ts).

Japa

n R

esid

ents

who

do

not i

nten

d to

live

pe

rman

ently

in

Japa

n, a

nd d

o no

t st

ay fo

r mor

e th

an

five

year

s in

any

10

-yea

r per

iod.

Res

iden

ts: w

orld

wid

e in

com

e.

Exp

atria

tes:

Jap

anes

e so

urce

inco

me

and

fore

ign

sour

ce in

com

e re

mitt

ed to

Jap

an.

Non

-res

iden

ts:

Japa

nese

sou

rce

inco

me.

Inco

me:

resi

dent

s ar

e ta

xed

at

prog

ress

ive

rate

s up

to

37 p

er c

ent (

if no

t a p

erm

anen

t re

side

nt, 5

0 pe

r cen

t).

Non

-res

iden

ts a

re ta

xed

at a

flat

ra

te o

f 20

per c

ent.

Cap

ital g

ains

: res

iden

ts ta

xed

at

14-3

9 pe

r cen

t (de

pend

s on

type

of

gai

n). N

on-r

esid

ents

usu

ally

ta

xed

at fl

at ra

te o

f 10

per c

ent.

Inco

me:

non

-res

iden

ts a

re n

ot e

ntitl

ed to

a b

asic

ded

uctio

n of

¥38

0,00

0. E

xpat

riate

s ar

e en

title

d to

tax

free

relo

catio

n an

d an

nual

hom

e le

ave

allo

wan

ces.

It

is c

ompu

lsor

y fo

r an

empl

oyee

or s

elf-e

mpl

oyed

indi

vidu

al in

Jap

an to

join

the

thre

e so

cial

in

sura

nce

sche

mes

: hea

lth, p

ensi

on, a

nd e

mpl

oyee

s in

sura

nce.

Hea

lth a

nd p

ensi

on in

sura

nce

sche

mes

are

pay

able

mon

thly

by

the

empl

oyee

and

em

ploy

er in

equ

al a

mou

nts.

Any

co

ntrib

utio

ns m

ade

by a

n in

divi

dual

will

be

dedu

ctib

le fo

r inc

ome

tax

purp

oses

. For

exp

atria

tes,

on

ly J

apan

sou

rced

pay

men

ts a

re c

harg

eabl

e an

d on

ly if

pay

roll

oper

ated

in J

apan

. C

apita

l gai

ns: c

ompr

ehen

sive

(res

iden

ts a

nd e

xpat

riate

s); J

apan

ese

right

s/lic

ence

s, d

irect

in

tere

sts

in J

apan

ese

com

pani

es, J

apan

ese

busi

ness

es a

nd c

erta

in s

ecur

ities

(non

-res

iden

ts).

Chapter 10: International taxation arrangements

Page 309

Tabl

e 10

.2: C

ompa

ring

tax

trea

tmen

t of t

empo

rary

resi

dent

s (e

xpat

riate

s) w

ith re

side

nt a

nd n

on re

side

nt in

divi

dual

s (c

ontin

ued)

C

ount

ry

Key

tem

pora

ry

resi

denc

e ru

les

(exp

atria

tes)

Liab

ility

to ta

x Ta

x ra

tes

Tax

base

(inc

ludi

ng s

ocia

l sec

urity

con

trib

utio

ns/o

blig

atio

ns o

f em

ploy

ees

and

empl

oyer

s)

Net

herla

nds

Exp

atria

tes

wor

king

in th

e N

ethe

rland

s w

ith a

D

utch

com

pany

w

ith s

carc

e sp

ecifi

c ex

perti

se.

A ti

me

limit

of u

p to

10

year

s ap

plie

s (a

lthou

gh a

fter f

ive

year

s th

e ta

x ad

min

istra

tion

may

re

quire

pro

of th

at

expa

triat

e st

ill h

as

the

spec

ific

know

-how

).

Res

iden

ts: w

orld

wid

e in

com

e.

Exp

atria

tes:

eith

er

resi

dent

or n

on-r

esid

ent

treat

men

t, at

exp

atria

te’s

el

ectio

n.

Non

-res

iden

ts: D

utch

so

urce

inco

me.

Inco

me:

no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Cap

ital g

ains

: no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Inco

me:

exp

atria

tes

can

rece

ive

30 p

er c

ent o

f the

ir sa

lary

and

wag

es ta

x fre

e fo

r a m

axim

um

of 1

0 ye

ars.

Cer

tain

per

sona

l allo

wan

ces,

min

or re

lief f

or s

uppo

rt of

dep

enda

nts

and

inco

me-

split

ting

are

not a

vaila

ble

for n

on-r

esid

ents

. B

oth

empl

oyee

s an

d ot

her r

esid

ents

are

obl

iged

to p

ay s

ocia

l sec

urity

pre

miu

ms

unde

r the

na

tiona

l soc

ial s

ecur

ity s

chem

e (a

ppro

xim

atel

y 32

per

cen

t of t

axab

le in

com

e up

to €

30,3

57;

peop

le o

ver 6

5 pa

y ap

prox

imat

ely

14 p

er c

ent).

The

re is

als

o an

add

ition

al o

blig

ator

y so

cial

se

curit

y sc

hem

e w

hich

cov

ers

empl

oyee

s on

ly (p

rem

ium

s ap

porti

oned

to b

oth

empl

oyer

s an

d em

ploy

ees)

. Non

-res

iden

ts: E

U n

atio

nals

who

com

e to

the

Net

herla

nds

to w

ork

on a

tem

pora

ry

basi

s ca

n ap

ply

for a

one

or t

wo

year

exe

mpt

ion

from

pay

ing

natio

nal s

ocia

l sec

urity

pre

miu

ms

on th

e ba

sis

of E

U le

gisl

atio

n. T

his

exem

ptio

n is

ava

ilabl

e fo

r oth

er n

on-r

esid

ents

as

wel

l if

Net

herla

nds

has

a so

cial

sec

urity

trea

ty w

ith th

eir h

ome

coun

try.

As

of 2

006

a ne

w h

ealth

car

e in

sura

nce

syst

em e

xist

s (to

repl

ace

the

old

dual

sch

eme)

. The

pr

emiu

m w

ill b

e 6.

5 pe

r cen

t of s

alar

y w

ith a

max

imum

of €

1,95

1. T

he s

ame

treat

men

t exi

sts

for r

esid

ents

and

non

-res

iden

ts.

An

unem

ploy

men

t ins

uran

ce c

ontri

butio

n is

levi

ed a

t a ra

te o

f app

roxi

mat

ely

5.2

per c

ent o

n an

nual

inco

me

betw

een

€15,

138

and

€43,

848

(the

cont

ribut

ion

is d

educ

tible

). C

apita

l gai

ns: n

o di

ffere

nce

betw

een

resi

dent

s an

d no

n-re

side

nts.

New

Ze

alan

d N

ew Z

eala

nd is

in

the

proc

ess

of

amen

ding

its

law

s so

that

firs

t-tim

e (o

r firs

t tim

e in

10

year

s) re

side

nts

who

com

e to

New

Ze

alan

d fo

r wor

k w

ill b

e ex

empt

on

fore

ign

inco

me

othe

r tha

n di

vide

nds,

inte

rest

, em

ploy

men

t in

com

e an

d se

rvic

e bu

sine

ss

inco

me.

Lim

it of

fiv

e ye

ars

(or t

hree

if

not e

mpl

oyed

on

arriv

al).

Res

iden

ts: w

orld

wid

e in

com

e.

Exp

atria

tes:

if

amen

dmen

ts a

re p

asse

d,

fore

ign

sour

ce in

com

e ot

her t

han

divi

dend

s,

inte

rest

, em

ploy

men

t in

com

e an

d se

rvic

e bu

sine

ss in

com

e w

ill b

e ex

empt

. N

on-r

esid

ents

: New

Ze

alan

d so

urce

inco

me.

Inco

me:

no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Cap

ital g

ains

: no

capi

tal g

ains

ta

x.

Inco

me:

min

or re

lief f

or s

uppo

rt of

dep

ende

nt c

hild

ren

avai

labl

e to

resi

dent

s.

Ther

e is

no

com

puls

ory

heal

th o

r soc

ial s

ecur

ity in

sura

nce.

The

re is

a c

ompr

ehen

sive

acc

iden

t co

mpe

nsat

ion

sche

me

adm

inis

tere

d by

Acc

iden

t Com

pens

atio

n C

orpo

ratio

n, fu

nded

by

levi

es

on e

mpl

oyer

s an

d em

ploy

ees,

and

sel

f-em

ploy

ed in

divi

dual

s. L

evie

s pa

yabl

e ar

e ba

sed

on

earn

ings

and

col

lect

ed th

roug

h th

e P

AYE

sys

tem

. The

fund

pay

s ou

t for

‘acc

iden

t-rel

ated

’ m

edic

al s

ervi

ces

and

for l

oss

of e

arni

ngs.

C

apita

l gai

ns: n

o ca

pita

l gai

ns ta

x.

International comparison of Australia’s taxes

Page 310

Tabl

e 10

.2: C

ompa

ring

tax

trea

tmen

t of t

empo

rary

resi

dent

s (e

xpat

riate

s) w

ith re

side

nt a

nd n

on re

side

nt in

divi

dual

s (c

ontin

ued)

C

ount

ry

Key

tem

pora

ry

resi

denc

e ru

les

(exp

atria

tes)

Liab

ility

to ta

x Ta

x ra

tes

Tax

base

(inc

ludi

ng s

ocia

l sec

urity

con

trib

utio

ns/o

blig

atio

ns o

f em

ploy

ees

and

empl

oyer

s)

Spa

in

Indi

vidu

als

(exp

atria

tes)

who

m

ove

thei

r re

side

nce

to S

pain

to

wor

k m

ay o

pt to

be

taxe

d un

der t

he

Spa

nish

inco

me

tax

as

non-

resi

dent

s.

Res

iden

ts: w

orld

wid

e in

com

e.

Non

-res

iden

ts: S

pani

sh

sour

ce in

com

e.

Inco

me:

resi

dent

s ar

e ta

xed

at

prog

ress

ive

rate

s up

to

45 p

er c

ent.

Non

-res

iden

ts a

re

taxe

d at

flat

rate

of 2

5 pe

r cen

t w

ithou

t ded

uctio

ns o

r al

low

ance

s (te

mpo

rary

wor

k is

on

ly ta

xed

at 2

per

cen

t).

Exp

atria

tes:

may

ele

ct to

be

taxe

d as

resi

dent

s (th

at is

, the

pr

ogre

ssiv

e ra

tes

abov

e w

ith

certa

in e

xpen

ses

dedu

ctib

le)

or a

s no

n-re

side

nts

(flat

rate

of

25 p

er c

ent,

but n

o de

duct

ions

) in

the

tax

year

th

ey m

ove

to S

pain

and

for t

he

next

five

yea

rs.

Cap

ital g

ains

: res

iden

ts a

re

taxe

d at

15

per c

ent f

lat r

ate.

N

on-r

esid

ents

are

taxe

d on

lo

ng-te

rm g

ains

(ass

ets

held

fo

r mor

e th

an o

ne y

ear)

gene

rally

at a

rate

of

35 p

er c

ent.

Inco

me:

exe

mpt

inco

me

for r

esid

ents

incl

udes

: ind

emni

ties

for p

hysi

cal/m

enta

l dam

ages

; m

anda

tory

com

pens

atio

n fo

r ter

min

atio

n of

em

ploy

men

t; di

sabi

lity

pens

ions

; chi

ld s

uppo

rt pa

ymen

ts. D

educ

tions

allo

wab

le fo

r soc

ial s

ecur

ity c

ontri

butio

ns a

nd c

ontri

butio

ns to

priv

ate

pens

ion

sche

mes

(non

-res

iden

ts n

ot e

ntitl

ed to

thes

e).

All resident

em

ploy

ed a

nd s

elf-e

mpl

oyed

indi

vidu

als

mus

t pay

mon

thly

con

tribu

tions

to th

e so

cial

sec

urity

sys

tem

, whi

ch c

onsi

sts

of a

gen

eral

con

tribu

tion

syst

em a

nd a

spe

cial

co

ntrib

utio

n sc

hem

e. T

he g

ener

al s

yste

m d

ivid

es e

mpl

oyee

s in

to p

rofe

ssio

nal c

ateg

orie

s to

de

term

ine

thei

r soc

ial s

ecur

ity c

ontri

butio

n. T

he g

ener

al c

ontri

butio

n sy

stem

has

a m

inim

um

and

max

imum

con

tribu

tion

base

that

is a

djus

ted

annu

ally

. For

200

6, th

e m

axim

um m

onth

ly

base

is a

ppro

xim

atel

y €2

,897

.70.

Com

puls

ory

soci

al s

ecur

ity c

ontri

butio

ns a

re d

educ

tible

for

indi

vidu

al in

com

e ta

x pu

rpos

es.

Cap

ital g

ains

: the

re a

re s

hort-

term

gai

ns (a

sset

s he

ld fo

r one

yea

r or l

ess)

whi

ch a

re ta

xed

as

inco

me,

and

long

-term

gai

ns w

hich

are

sub

ject

to a

sep

arat

e ca

pita

l gai

ns ta

x (1

5 pe

r cen

t).

Exe

mpt

ions

exi

st fo

r ind

ivid

uals

’ prim

ary

resi

denc

e.

Sw

itzer

land

E

xpat

riate

s ar

e en

title

d to

cer

tain

de

duct

ions

. E

xpat

riate

s ar

e ex

ecut

ives

or

spec

ialis

t who

are

as

sign

ed to

S

witz

erla

nd fo

r a

perio

d no

t ex

ceed

ing

five

year

s (a

s so

on a

s in

tent

ion

to s

tay

for l

ess

than

five

ye

ars

chan

ges

the

dedu

ctio

ns a

re n

o lo

nger

ava

ilabl

e.

They

are

not

de

nied

re

troac

tivel

y).

Res

iden

ts: ‘

inla

nd in

com

e’

(gen

eral

ly in

clud

es a

ll w

orld

wid

e so

urce

s of

re

venu

e fro

m m

ovea

ble

prop

erty

). N

on-r

esid

ents

: Sw

iss

sour

ced

inco

me.

Inco

me:

the

sam

e ta

x ra

tes

are

appl

icab

le fo

r no

n-re

side

nts

as fo

r res

iden

ts.

Res

iden

t im

mig

rant

s: s

peci

al

rate

s ap

ply

on p

assi

ve in

com

e fo

r a li

mite

d pe

riod

from

im

mig

ratio

n.

Cap

ital g

ains

: no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s (S

wis

s bu

sine

ss

capi

tal g

ains

are

trea

ted

as

inco

me)

.

Inco

me:

no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s. E

xpat

riate

s m

ay c

laim

spe

cific

de

duct

ions

acc

ordi

ng to

’sub

-nat

iona

l and

nat

iona

l’ la

w (f

or e

xam

ple

cost

s fo

r hou

sing

, mov

ing,

an

d tra

velli

ng).

Hea

lth in

sura

nce

is m

anda

tory

, but

is a

lso

the

resp

onsi

bilit

y of

the

indi

vidu

al (p

rem

ium

s va

ry

depe

ndin

g on

the

insu

ranc

e co

mpa

ny a

nd a

ge o

f the

indi

vidu

al).

Non

-res

iden

ts a

re n

ot s

ubje

ct

to th

e m

inim

um m

edic

al in

sura

nce.

In

term

s of

soc

ial s

ecur

ity, e

mpl

oyer

s w

ithho

ld e

mpl

oyee

s’ c

ontri

butio

ns (o

ld-a

ge s

urvi

vors

in

sura

nce

4.2

per c

ent;

disa

bilit

y 0.

7 pe

r cen

t; m

ilita

ry c

ompe

nsat

ion

0.15

per

cen

t; un

empl

oym

ent i

nsur

ance

1 p

er c

ent).

No

cont

ribut

ion

is le

vied

on

inco

me

in e

xces

s of

C

HF1

06,8

00.

Em

ploy

ees

with

ann

ual w

age

exce

edin

g C

HF1

9,35

0 m

ust c

ontri

bute

to c

ompa

ny’s

pen

sion

sc

hem

e; c

ontri

butio

ns v

ary

depe

ndin

g on

sch

eme

(the

sche

me

mus

t mee

t cer

tain

sta

ndar

ds).

Em

ploy

er h

as to

bea

r at l

east

one

-hal

f of o

vera

ll co

ntrib

utio

ns o

f the

em

ploy

ee.

Cap

ital g

ains

: res

iden

ts n

ot s

ubje

ct to

CG

T on

gai

ns fr

om m

ovab

le p

rope

rty o

r whe

re re

al

esta

te is

hel

d fo

r priv

ate

inve

stm

ent p

urpo

ses.

N

on-r

esid

ents

: sub

ject

to C

GT

on g

ains

from

land

/bui

ldin

g st

ruct

ures

in S

witz

erla

nd a

nd a

sset

s us

ed in

car

ryin

g on

a tr

ade/

busi

ness

from

a p

erm

anen

t est

ablis

hmen

t in

Sw

itzer

land

.

Chapter 10: International taxation arrangements

Page 311

Tabl

e 10

.2: C

ompa

ring

tax

trea

tmen

t of t

empo

rary

resi

dent

s (e

xpat

riate

s) w

ith re

side

nt a

nd n

on re

side

nt in

divi

dual

s (c

ontin

ued)

C

ount

ry

Key

tem

pora

ry

resi

denc

e ru

les

(exp

atria

tes)

Liab

ility

to ta

x Ta

x ra

tes

Tax

base

(inc

ludi

ng s

ocia

l sec

urity

con

trib

utio

ns/o

blig

atio

ns o

f em

ploy

ees

and

empl

oyer

s)

Uni

ted

Kin

gdom

R

esid

ent,

but n

ot

ordi

naril

y re

side

nt

in th

e U

nite

d K

ingd

om (t

hat i

s,

inte

nd to

rem

ain

for l

ess

than

thre

e ye

ars)

or w

ho a

re

dom

icile

d ou

tsid

e th

e U

nite

d K

ingd

om.

Res

iden

ts: w

orld

wid

e in

com

e.

Exp

atria

tes:

ear

ning

s fro

m U

nite

d K

ingd

om

empl

oym

ent a

nd

othe

r for

eign

sou

rce

inco

me

rem

itted

to

the

Uni

ted

Kin

gdom

. N

on-r

esid

ents

: U

nite

d K

ingd

om

sour

ce in

com

e.

Inco

me:

no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Cap

ital g

ains

: no

diffe

renc

e be

twee

n re

side

nts

and

non-

resi

dent

s.

Inco

me:

non

-res

iden

ts g

ener

ally

do

not g

et a

cces

s to

the

stan

dard

ded

uctio

n.

All

indi

vidu

als

resi

dent

in th

e U

nite

d K

ingd

om fo

r 12

mon

ths

or m

ore

are

entit

led

to fr

ee m

edic

al tr

eatm

ent

unde

r the

Nat

iona

l Hea

lth S

ervi

ce. T

his

is fi

nanc

ed o

ut o

f gen

eral

taxa

tion

(ther

e ar

e no

add

ition

al s

peci

fic

cont

ribut

ions

or t

axes

). S

ocia

l sec

urity

ben

efits

: ben

efits

are

div

ided

bet

wee

n co

ntrib

utor

y be

nefit

s an

d no

n-co

ntrib

utor

y be

nefit

s.

Con

tribu

tory

ben

efits

(une

mpl

oym

ent,

pens

ions

) are

thos

e w

hich

are

pai

d to

indi

vidu

als

who

hav

e th

e re

quis

ite

cont

ribut

ions

reco

rd. T

he c

ontri

butio

ns re

ferr

ed to

are

nat

iona

l ins

uran

ce c

ontri

butio

ns (t

hat i

s, c

ontri

butio

ns to

th

e N

atio

nal I

nsur

ance

Fun

d) o

ut o

f whi

ch c

ontri

buto

ry b

enef

its a

re p

aid.

Non

-con

tribu

tory

ben

efits

(for

ex

ampl

e ch

ild b

enef

it) d

o no

t req

uire

a c

ontri

butio

ns re

cord

and

are

fund

ed o

ut o

f gen

eral

taxa

tion.

A

ll in

divi

dual

s pr

esen

t in

the

Uni

ted

Kin

gdom

are

liab

le to

pay

nat

iona

l ins

uran

ce c

ontri

butio

ns, w

hate

ver t

heir

leve

l of i

ncom

e, o

nce

it ex

ceed

s a

basi

c th

resh

old.

A lo

wer

rate

of c

ontri

butio

ns is

pay

able

by

thos

e em

ploy

ees

who

are

mem

bers

of a

con

tract

ed-o

ut o

ccup

atio

nal o

r per

sona

l pen

sion

sch

eme.

Em

ploy

ers

are

also

liab

le to

pay

nat

iona

l ins

uran

ce c

ontri

butio

ns in

resp

ect o

f the

ir em

ploy

ees.

The

em

ploy

ers’

con

tribu

tions

fu

nctio

n as

a p

ayro

ll ta

x.

Exp

atria

tes:

fore

ign

natio

nals

com

ing

to th

e U

nite

d K

ingd

om d

o no

t hav

e to

pay

nat

iona

l ins

uran

ce

cont

ribut

ions

for t

he fi

rst 5

2 w

eeks

afte

r arr

ival

pro

vide

d th

eir s

tay

in th

e U

nite

d K

ingd

om is

tem

pora

ry, t

hey

are

empl

oyed

by

a fo

reig

n em

ploy

er a

nd th

eir n

orm

al p

lace

of a

bode

bef

ore

arriv

al w

as n

ot th

e U

nite

d K

ingd

om (o

ther

wis

e lia

bilit

y ge

nera

lly a

rises

imm

edia

tely

upo

n ar

rival

). M

ost s

ocia

l sec

urity

trea

ties

prov

ide

that

fore

ign

natio

nals

will

be

exem

pt fr

om li

abili

ty to

nat

iona

l ins

uran

ce c

ontri

butio

ns fo

r a fi

xed

perio

d af

ter

arriv

al, p

rovi

ded

they

hav

e a

certi

ficat

e fro

m th

eir h

ome

coun

try a

ttest

ing

to th

eir c

ontin

ued

liabi

lity

to th

e eq

uiva

lent

tax

ther

e.

Cap

ital g

ains

: com

preh

ensi

ve (r

esid

ents

). C

ompr

ehen

sive

, but

fore

ign

gain

s on

ly w

hen

rem

itted

to th

e U

nite

d K

ingd

om (e

xpat

riate

s). U

nite

d K

ingd

om la

nd a

nd b

usin

ess

asse

ts (n

on-r

esid

ents

).

Uni

ted

Sta

tes

Non

e R

esid

ents

: wor

ldw

ide

inco

me.

N

on-r

esid

ents

: U

nite

d S

tate

s so

urce

in

com

e.

Inco

me:

no

n-re

side

nts

taxe

d as

per

resi

dent

s bu

t ar

e ta

xed

flat

30 p

er c

ent o

n in

vest

men

t inc

ome.

C

apita

l gai

ns: n

o di

ffere

nce

betw

een

resi

dent

s an

d no

n-re

side

nts.

Inco

me:

non

-res

iden

ts c

anno

t use

mar

ried

filin

g or

hea

d of

hou

seho

ld re

turn

s. A

lso,

can

not c

laim

dep

ende

nts

exem

ptio

ns. R

esid

ents

are

abl

e to

cla

im in

tere

st d

educ

tions

on

hom

e lo

ans

used

for a

prin

cipa

l res

iden

ce;

non-

resi

dent

s un

likel

y to

hav

e U

nite

d S

tate

s pr

inci

ple

resi

denc

e.

Res

iden

ts a

nd n

on-r

esid

ents

are

sub

ject

to s

ocia

l sec

urity

(ie

old-

age,

sur

vivo

rs a

nd d

isab

ility

insu

ranc

e) a

nd

Med

icar

e ta

x on

rem

uner

atio

n pa

id fo

r ser

vice

s pe

rform

ed w

ithin

the

Uni

ted

Sta

tes

rega

rdle

ss o

f whe

ther

the

empl

oyee

will

be

elig

ible

for b

enef

its. N

atio

nal l

aw re

quire

s em

ploy

ers

to w

ithho

ld s

ocia

l sec

urity

and

Med

icar

e ta

xes

from

rem

uner

atio

n. F

or 2

005

the

first

US

$90,

000

of re

mun

erat

ion

paid

to e

ach

empl

oyee

is s

ubje

ct to

so

cial

sec

urity

tax

at a

rate

of 1

2.4

per c

ent (

empl

oyer

pay

s 6.

2 pe

r cen

t and

with

hold

s 6.

2 pe

r cen

t fro

m th

e em

ploy

ee’s

rem

uner

atio

n). T

he M

edic

are

tax

is im

pose

d on

the

empl

oyee

’s e

ntire

rem

uner

atio

n at

a ra

te o

f 2.

9 pe

r cen

t (em

ploy

er p

ays

1.45

per

cen

t and

with

hold

s 1.

45 p

er c

ent f

rom

the

empl

oyee

’s re

mun

erat

ion)

. C

erta

in e

xem

ptio

ns a

vaila

ble

to n

on-r

esid

ent a

liens

und

er s

ocia

l sec

urity

tota

lisat

ion

agre

emen

ts, i

f tho

se

non-

resi

dent

s co

ntin

ue to

pay

soc

ial s

ecur

ity ta

xes

in h

ome

coun

try.

Cap

ital g

ains

: com

preh

ensi

ve (r

esid

ents

). G

ener

ally

exe

mpt

, but

Uni

ted

Sta

tes

real

pro

perty

gai

ns a

re ta

xed

at m

argi

nal t

ax ra

tes

(non

-res

iden

ts).

(a)

Tax

Law

s A

men

dmen

t (20

06 M

easu

res

No.

1) B

ill 2

006,

whi

ch in

clud

es m

easu

res

affe

ctin

g th

e ta

x tre

atm

ent o

f tem

pora

ry re

side

nts,

is c

urre

ntly

bef

ore

the

Aus

tralia

n P

arlia

men

t. If

enac

ted

as

intro

duce

d, th

ese

mea

sure

s w

ill a

lign

mor

e cl

osel

y A

ustra

lia’s

tax

treat

men

t of t

empo

rary

resi

dent

s to

that

of o

ther

cou

ntrie

s, in

par

t by

gene

rally

exe

mpt

ing

thei

r for

eign

non

-em

ploy

men

t inc

ome.

S

ourc

e: V

ario

us, s

ee C

hapt

er 1

(1.4

.1).

International comparison of Australia’s taxes

Page 312

Table 10.2 shows that temporary residence rules generally limit the tax base to employment income and domestic source investment income. Among the countries that have special taxation rules for these individuals, however, there is a general trend to limit these rules. Limitations can relate to: exempting non-employment foreign income only if it is not remitted to the country; providing that the exemption only applies for a maximum period of time; and providing that the exemption is only available to individuals with scarce specific expertise (that are not generally available in the particular country concerned).4

Table 10.2 also shows that most countries apply the same tax rates to residents and non-residents. Where differences in treatment apply, the general trend seems to be for non-residents to be subject to a slightly higher effective tax rate. Australia’s approach is consistent with this general trend.

In terms of income, most countries treat residents similarly by taxing worldwide income; they also treat non-residents similarly by taxing domestic source income only. As between residents and non-residents, some countries will often allow residents to claim some deductions and relief not available to non-residents. For countries that have a compulsory medical insurance system, non-residents are usually not covered and therefore not required to contribute.

In terms of capital gains tax, most countries comprehensively tax residents, but limit the taxation of the gains of non-residents to land or real property situated in the country concerned. Australia does not currently have such a limitation.5

Countries that levy social security contributions taxes often apply them equally to their residents, temporary residents and non-residents alike. Some countries deny temporary and non-resident individuals entitlement to the related benefits (for example, the United States).

10.3.2 Treatment of a company’s foreign source income

As with individuals, resident companies are generally taxed on their worldwide income while non-resident companies are generally only taxed on their domestic source income. Temporary residence tests are not necessary for companies.

Typically, all residents are taxed on their foreign source income unless the income is expressly carved out of the tax base by a foreign income exemption, either unilaterally (in the domestic law) or by a tax treaty with another country. Table 10.2 showed that resident individuals across the OECD-10 are generally comprehensively taxed (with relatively few exemptions) on their worldwide employment, business and investment income. Key reasons for this may be to achieve horizontal and vertical equity goals, and to improve the tax neutrality of investment decisions (efficiency).

4 The Australian Government announced in the 2005-06 Budget (and has recently introduced legislation to Parliament) measures to align more closely our tax treatment of temporary residents to that of other countries. Once enacted, Australia will have few restrictions in its temporary residence rules. The main limitation will be simply that the individual hold a temporary visa and not be an Australian resident for social security purposes (whether directly or via their spouse).

5 The reforms announced in the 2005-06 Budget to the capital gains tax treatment of non-residents will bring Australia into line with international practice.

Chapter 10: International taxation arrangements

Page 313

By contrast, resident companies typically receive greater exemptions, particularly on their foreign business income. A key reason for this may be because such exemptions interfere less with goals of horizontal and vertical equity, given the withholding aspect of corporate taxation, and the existence of a subsequent taxing point on company income (when the dividends are distributed to resident shareholders).

Foreign income exemptions for resident companies can be based on:

• the type of income earned (for example business, investment income);

• the type of country the income is sourced from (for example comparable tax, treaty or non-tax-haven countries);

• the type of non-resident entity that earns the foreign income on behalf of the resident company (for example company, superannuation fund, managed fund);

• the degree to which it has been taxed (for example subject to tax, taxed at 75 per cent of the resident company tax rate, taxed by a listed country); or

• a combination of the above.

Table 10.3 shows for the OECD-10 the extent to which resident companies are taxed on their foreign source income, and in particular, the foreign income exemptions they receive.

Table 10.3: Treatment of foreign source income of corporate residents Country Taxation of resident companies Key foreign income

exemptions from worldwide income taxation

Australia Corporate residents subject to tax on worldwide income and capital gains. Foreign income exemptions are extensive (based on active income and active business tests), with FTC system unilaterally covering the rest. Non-exempt foreign losses are quarantined from domestic income on a per-class (of income) basis and can be carried forward indefinitely (and set off against future foreign income of the same class).(a) Foreign affiliate: foreign company in respect of which a resident company owns directly at least 10 per cent of the voting stock (a ‘non-portfolio’ interest). A foreign affiliate effectively also has a (foreign) affiliate if it owns a non-portfolio interest in another foreign company.(b)

Foreign branch business profits (active income) are exempt. Non-portfolio dividends are exempt, including when paid through a chain of foreign companies. Capital gains on shares in foreign affiliates carrying on an active business are exempt. (Full participation exemption.)

Canada Corporate residents subject to tax on worldwide income and capital gains. Foreign income exemptions are narrow, with FTC system unilaterally covering the rest. All foreign branch income is assessable with unilateral credit, as are most types of foreign dividends and all other foreign income. Foreign losses are deductible against domestic income without recapture against, or recharacterisation of, future foreign income. Foreign affiliate: foreign company in respect of which a resident company owns (directly or indirectly) at least 10 per cent of the shares of any class.

No unilateral exemptions. Generally, only dividends from foreign affiliates in treaty countries paid out of ‘exempt surplus’ (active or business income and certain capital gains) are exempt.

Ireland Corporate residents subject to tax on worldwide income and capital gains. Essentially, there are no foreign income exemptions, and FTC system only partially covers the rest (mainly by treaties). All foreign branch income assessable, with foreign tax generally deducted as business expense (unless treaty applies). Foreign losses are quarantined from domestic income on a per-source basis and can be carried forward indefinitely. Foreign affiliate: foreign company in respect of which a resident company owns (directly or indirectly) at least 5 per cent of the ordinary share capital.

None

International comparison of Australia’s taxes

Page 314

Table 10.3: Treatment of foreign source income of corporate residents (continued) Country Taxation of resident companies Key foreign income

exemptions from worldwide income taxation