1/16 LECTURE INTRODUCTION TO MICROFINANCE May 6th, 2009 Emilie Levy, Executive Director.

16

1/16 /16 LECTURE INTRODUCTION TO MICROFINANCE May 6th, 2009 Emilie Levy, Executive Director

-

Upload

prudence-davis -

Category

Documents

-

view

215 -

download

0

Transcript of 1/16 LECTURE INTRODUCTION TO MICROFINANCE May 6th, 2009 Emilie Levy, Executive Director.

11/16/16

LECTURE

INTRODUCTION TO MICROFINANCE

May 6th, 2009

Emilie Levy, Executive Director

22/16/16

DEFINITION OF MICROFINANCEDEFINITION OF MICROFINANCE

STAKEHOLDERSSTAKEHOLDERS

MICROFINANCE BEST PRACTICESMICROFINANCE BEST PRACTICES

SUSTAINABILITY AND RISKSSUSTAINABILITY AND RISKS

SNAPSHOT OF MICROFINANCE TODAYSNAPSHOT OF MICROFINANCE TODAY

Agenda

33/16/16

Mrs. Israel, 48 years old

• Unemployed husband • 4 children• No savings• Good cook

• Mrs. Israel decides to start a small catering service at home

• Mrs. Israel goes to the bank and makes a demand for a loan at her bank

MRS. ISRAEL’S DEMAND IS REJECTED

Case study

44/16/16

Why are people excluded from certain financial services?

Justification and definition of microfinance

• Lack collateral or guarantors

• A bad credit history

• Gap in the communication / lack of confidence in the Banks

• Doubt of the bank of the repayment capacity

• Lack of access to financial infrastructure and services in remoted areas

WHAT IS THE ALTERNATIVE?

MICROFINANCE

55/16/16

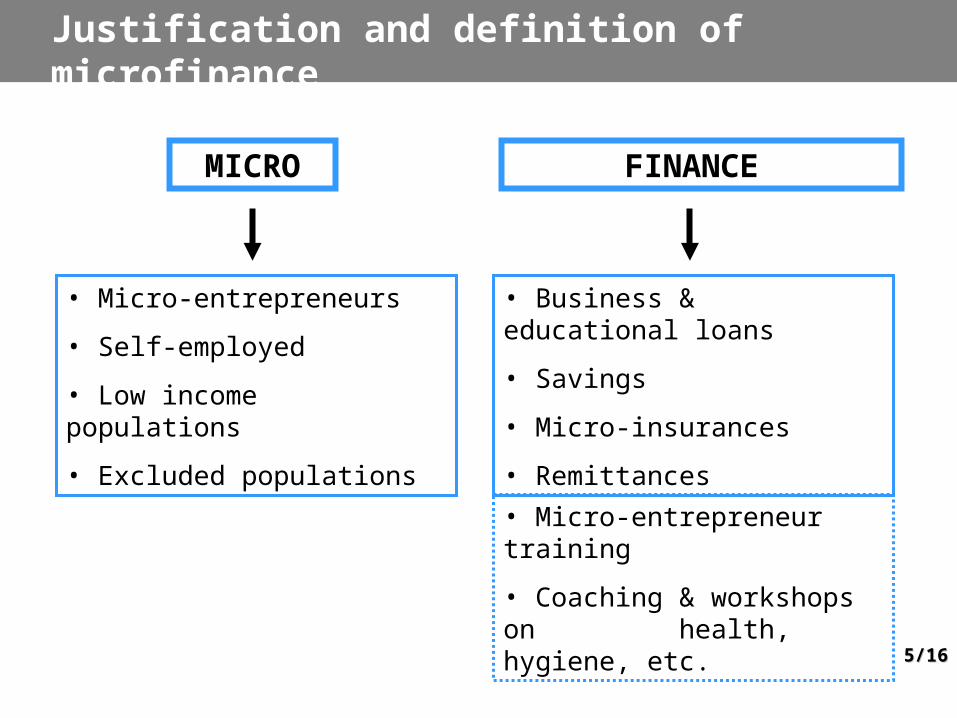

Justification and definition of microfinance

FINANCE MICRO

• Micro-entrepreneurs

• Self-employed

• Low income populations

• Excluded populations

• Business & educational loans

• Savings

• Micro-insurances

• Remittances

• Micro-entrepreneur training

• Coaching & workshops on health, hygiene, etc.

66/16/16

Microfinance is a tool against poverty by enabling the beneficiaries to :

• Create sustainable activities to increase their incomes

• Reduce external shocks

• Improve the living conditions of entrepreneurs and of their families

• Empower people and mainly the women

Definition

Microfinance is the offer of financial & non-financial services to people excluded from the traditional banking system.

The services are adapted to the needs of the target populations

77/16/16

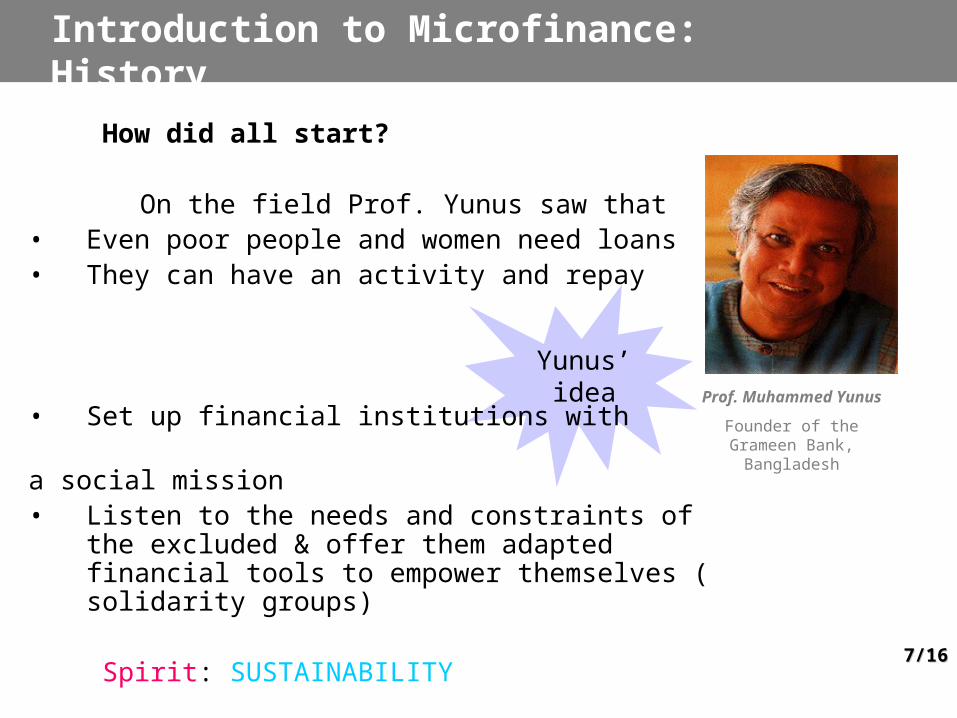

Yunus’ idea Prof. Muhammed Yunus

Founder of the Grameen Bank, Bangladesh

Introduction to Microfinance: History

How did all start?

On the field Prof. Yunus saw that• Even poor people and women need loans• They can have an activity and repay

• Set up financial institutions with a social mission• Listen to the needs and constraints of the

excluded & offer them adapted financial tools to empower themselves ( solidarity groups)

Spirit: SUSTAINABILITY

88/16/16

MICROFINANCE MICROFINANCE INSTITUTIONS (MFIs)INSTITUTIONS (MFIs)(NGO, ASSOCIATIONS & BANKS)

Commercial Banks

COMMERCIAL BANKS & INVESTMENT FUNDS

FOUNDATIONS & DONORS (incl.

enterprises)

GOVERNMENT & LOCAL BODIES SUPPORT

ORANIZATIONS (e.g. PF)

BENEFICIARIESBENEFICIARIES

Actors & Mechanisms

99/16/16

44 Final Repayment 12 weeks later

Demand for a 2nd loan over

NIS 1500 to buy a fridge)

22 Purchase of the ingredients

Start of cooking & sale

(Daily benefits amount NIS 100)

11 Visit of Mrs. Israel to the MFI

Meeting wit the Loan Officer

Convinced, reception of a loan of

NIS 1,000 (+ NIS 30 interest rate)

33 Weekly Repayment ( 86 NIS)

Remaining money is used to buy food

Regular contact and Regular contact and follow up between the follow up between the

MFI and the clientMFI and the client

Micro-credit Best practices (1/4 ): microcredit

Mrs. Israel needs NIS 1,000Mrs. Israel needs NIS 1,000

1010/16/16

Microfinance is not philanthropy!• Clients need to pay for the services• Microcredit clients need to repay the loans• Interest rate to cover the costs

Why is repayment important?

• Offer new loans and extend the client base• Ensure correct functioning and growth of the institution • Cover office & operational costs • Cover for non-payments when they occur• Avoid financial loss and loss of credibility for the institution

REPAYMENT ON TIME GUARANTEES THE SUSTAINABILITY OF THE PROGRAM

Microcredit Best Practice (2/4 ) Repayment

1111/16/16

Prejudices

• The social mission should consist in a free loan

• Interest Rate, perceived as a burden to the client

Reality

• Micro-credits allow for the creation or expansion of an income generating activity and the generation of profit

• Interest rates are no burden if the business plan is solid and good evaluation has been done

Micro-credit Best practices (3/4 ): Interest Rate

1212/16/16

Methodology

• Regular follow up

• Requirement of good repayment for future access to a bigger loan

• Local loan officers familiar with local culture

Adapted products and procedures

• Small and short term credits

• Repayment capacity assessment

• Adapted collaterals / group solidarity guarantee

Business Development Services

• Compensation for lack of education of loan beneficiaries

Microcredit Best practices (4/4): Key success factors

1313/16/16

Sustainability: the conceptual framework

OUTREACH

IMPACT

How do we measure the impact?

SUSTAINABILITY

Why few MFIs are sustainable?

• Need to make trade-off sometimes

• Need to reduce the internal and external risks to maximize the success

1414/16/16

• 10,000 MFIs manage a global portfolio of US$30 Billions

• In a range from 150 US$ to 7,000 US$, the average loan size is US$ 450

• 150 Mio micro-credit active clients

• 300 Mio micro-saving active clients

• 50 Mio micro-insurance active clients

Sources : CGAP, BIT, Microcredit Summit, PlaNet Finance

Microfinance in the world today

1515/16/16

• Development of MF in industrialized countries (e.g. Israel, France, USA) thanks to the adaptation of the tools and methodologies

• Commercialization of the stakeholders

• Use of new technologies as a new development tool

New trends

1616/16/16

Thank you!Thank you!

www.planetfinancegroup.orgwww.planetfinancegroup.orgelevy@[email protected]