11 - SAGE Publications Inc€¦ · 11 STRATEGIC LEADERSHIP NATALIE SLAWINSKI The University of...

38

11 STRATEGIC LEADERSHIP NATALIE SLAWINSKI The University of Western Ontario 297 There are three categories of people—the person who goes into his office, puts his feet up on his desk, and dreams for twelve hours; the person who arrives at 5:00 am and works for sixteen hours, never once stopping to dream; and the one who puts his feet up, dreams for one hour, then does something about those dreams. —Steven J. Ross 1 I n the past 20 years, researchers have begun to pay more attention to the study of strate- gic leadership, which has come to be viewed by many as a critical aspect of firm success (Daft, 2005). Broadly speaking, strategic leadership refers to the study of executives who have overall responsibility for the firm and how their decisions affect organi- zational outcomes (Finkelstein & Hambrick, 1996). The focus is on top managers because they usually have decision-making responsibilities that affect the whole organization— including the other organizational members—and its overall performance (Daft, 2005). Strategic leaders create a sense of purpose and direction, which guides strategy formula- tion and implementation within the firm (Daft, 2005; Hosmer, 1982; Shrivastava & Nachman, 1989). They also interact with key stakeholders, such as customers, government agencies, and unions, especially when these relationships are critical to firm performance (House & Aditya, 1997). Organizations and the environments in which they operate are increasingly complex and ambiguous. Therefore, strategic leaders must navigate through these complexities and develop strategies that will allow their organizations to be successful, whether they are for- profit or nonprofit. Another perspective of strategic leadership focuses on the specific activities and behav- iors of strategic leaders that can improve the success of the firm (Ireland & Hitt, 1999; Rowe, 2001). This perspective argues that in an ever-changing complex business environment, 11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 297

Transcript of 11 - SAGE Publications Inc€¦ · 11 STRATEGIC LEADERSHIP NATALIE SLAWINSKI The University of...

11STRATEGIC LEADERSHIP

NATALIE SLAWINSKI

The University of Western Ontario

297

There are three categories of people—the person who goes into his office,puts his feet up on his desk, and dreams for twelve hours; the person whoarrives at 5:00 am and works for sixteen hours, never once stopping todream; and the one who puts his feet up, dreams for one hour, then doessomething about those dreams.

—Steven J. Ross1

I n the past 20 years, researchers have begun to pay more attention to the study of strate-gic leadership, which has come to be viewed by many as a critical aspect of firmsuccess (Daft, 2005). Broadly speaking, strategic leadership refers to the study of

executives who have overall responsibility for the firm and how their decisions affect organi-zational outcomes (Finkelstein & Hambrick, 1996). The focus is on top managers becausethey usually have decision-making responsibilities that affect the whole organization—including the other organizational members—and its overall performance (Daft, 2005).

Strategic leaders create a sense of purpose and direction, which guides strategy formula-tion and implementation within the firm (Daft, 2005; Hosmer, 1982; Shrivastava & Nachman,1989). They also interact with key stakeholders, such as customers, government agencies, andunions, especially when these relationships are critical to firm performance (House & Aditya,1997). Organizations and the environments in which they operate are increasingly complexand ambiguous. Therefore, strategic leaders must navigate through these complexities anddevelop strategies that will allow their organizations to be successful, whether they are for-profit or nonprofit.

Another perspective of strategic leadership focuses on the specific activities and behav-iors of strategic leaders that can improve the success of the firm (Ireland & Hitt, 1999; Rowe,2001). This perspective argues that in an ever-changing complex business environment,

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 297

strategic leaders may be a source of competitive advantage. Ireland and Hitt (1999) definestrategic leadership as the “ability to anticipate, envision, maintain flexibility, think strategi-cally, and work with others to initiate changes that will create a viable future for the orga-nization” (p. 43). Given the challenges that firms face in an often turbulent and unpredictableglobal environment, Ireland and Hitt have identified six components of strategic leadershipthat will lead to enhanced organizational performance: determining the firm’s purpose orvision, exploiting and maintaining core competencies, developing human capital, sustain-ing an effective organizational culture, emphasizing ethical practices, and establishing bal-anced organizational controls.

DETERMINING THE FIRM’S PURPOSE OR VISION

The first component of strategic leadership consists of determining the firm’s purpose orvision. This means that strategic leaders must articulate a clear and realistic statementabout why the firm exists and what is distinctive about it. This statement will thenempower members of the organization to develop and execute strategies that are in linewith the vision of the firm.

EXPLOITING AND MAINTAINING CORE COMPETENCIES

Strategic leaders exploit and maintain core competencies. Core competencies are resourcesand capabilities that give firms an edge over their rivals. Strategic leaders need to under-stand which combinations of resources and capabilities are valuable, rare, costly to imitate,and difficult to substitute for, as these will allow the firm to gain a competitive advantage.

DEVELOPING HUMAN CAPITAL

Strategic leaders are effective at developing human capital. Human capital refers to the knowl-edge, skills, and abilities of the firm’s employees. Because these employees are critical to thesuccess of the organization, strategic leaders invest in them through training and mentoring.

SUSTAINING AN EFFECTIVE ORGANIZATIONAL CULTURE

Strategic leaders sustain an effective organizational culture. An organization’s culture is acomplex combination of ideologies, symbols, and values that are shared by employees ofthe firm. Strategic leaders learn how to shape a firm’s shared values and symbols in waysthat allow the firm to be more competitive.

EMPHASIZING ETHICAL PRACTICES

Strategic leadership involves the emphasis of ethical practices. Top managers who usehonesty, trust, and integrity in their decision making are able to inspire their employeesand create an organizational culture that encourages the use of ethical practices in day-to-day organizational activities.

298 • CASES IN LEADERSHIP

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 298

ESTABLISHING BALANCED ORGANIZATIONAL CONTROLS

Organizational controls refer to the formal procedures that are used in organizations toinfluence and guide work. These controls act as limits on what employees can and can-not do. There are two types of internal controls: strategic and financial. Strategic con-trols are accomplished through information exchanges that help to develop strategies,whereas financial controls are accomplished through setting objective criteria such asperformance targets. Strategic controls emphasize actions, whereas financial controlsemphasize outcomes. Financial controls can be especially constraining and can stiflecreativity in organizations. Strategic leaders must establish balanced organizationalcontrols by incorporating the two types in order to allow employees to remain flexibleand innovative.

In addition to accomplishing the above activities, strategic leaders must balance theshort-term needs of their organizations while ensuring a future competitive position.Rowe (2001) defines strategic leadership as “the ability to influence others to voluntarilymake day-to-day decisions that enhance the long-term viability of the organization, whileat the same time maintaining its short-term financial stability” (pp. 82–83). This type ofleadership is a synergistic combination of visionary leadership, which emphasizes invest-ing in the future, and managerial leadership, which emphasizes preserving the existingorder. Strategic leaders focus on both the day-to-day operations and the long-term strategic orientation of the firm, recognizing that neither can be ignored if a firm is to besuccessful.

Importantly, strategic leaders have strong positive expectations of the performance theyexpect from their superiors, peers, subordinates, and themselves (Rowe, 2001). Theseexpectations encourage organizational members to voluntarily make decisions that con-tribute to short-term stability and long-term viability of the organization. As such, strate-gic leaders do not have to expend as much effort on monitoring and controlling employees.It is also important that those leaders who already exhibit strategic leadership abilitiesencourage their development in other organizational members. In this way, strategic lead-ership can exist at all levels of the organization. Strategic leaders also select the next gen-eration of leaders to ensure that the organization will continue to have strategic leadershipin the long term (Boal & Hooijberg, 2000).

STRATEGIC LEADERSHIP VERSUS LEADERSHIP

In Chapter 1 of this casebook, leadership was defined as the process of influencing othersin order to accomplish a goal. The focus was on the relationship between the leader andfollower in a group context and on the process of leading in order to achieve a goal. Sohow is strategic leadership different from leadership? The main difference is that leader-ship can be accomplished at any level of the organization and can have an impact on dif-ferent types of organizational goals, such as increasing the sales of a particular product lineor reducing the turnover of employees.

Strategic leadership, on the other hand, is mainly concerned with, but not necessarilyrestricted to, the higher levels of the organization, given that executives are in a uniqueposition to influence the direction and vision of the organization (Finkelstein & Hambrick,1996). Strategic leadership has an impact on organization-wide outcomes, such as thefinancial performance of a small manufacturing company or the strategic change of a large

Strategic Leadership • 299

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 299

multinational company. The difference can also be thought of as leadership “in” organiza-tions versus leadership “of” organizations (Boal & Hooijberg, 2001). The leadershipapproaches discussed throughout this book are mainly concerned with how leaders affectfollowers “in” the organization, whereas strategic leadership is primarily concerned with the leadership “of” organization by top managers. But as we saw earlier, leaders atall levels of the organization can have an impact on organizational performance. The focusof strategic leadership is often on top-level executives such as CEOs because they tend tohave more power and are given responsibility for the overall performance of the firm. Theyare also held accountable by shareholders for the success of the firm, and poor perfor-mance can lead to their dismissal.

POSITIONAL VERSUS BEHAVIORAL

In contrast to some of the other theories within the realm of leadership, such as the traitapproach and the skills approach, the strategic leadership perspective is not as well devel-oped. Furthermore, there is a lack of agreement regarding what strategic leadership is. Aswe have seen, strategic leadership has come to have several different, but often comple-mentary, meanings. Some (e.g., Finkerstein & Hambrick, 1996) view it as having to dowith one’s position in a company, while others (e.g., Ireland & Hitt, 1999) view it as a setof behaviors that lead to superior performance.

The positional view argues that anyone holding the position of CEO or another topexecutive position is a strategic leader because of his or her decision-making power andlevel of responsibility. This perspective looks at the differences in psychological charac-teristics of strategic leaders to examine how these differences affect their organizations(Finkelstein & Hambrick, 1996). Others view strategic leadership as a set of activities thatleaders must perform if they are to enhance organizational performance. For example,strategic leaders are those who sustain an effective corporate culture (Ireland & Hitt,1999). A related perspective (Rowe, 2001) on strategic leadership views it as a leadershipstyle that individuals may possess at any level of the organization. Rowe (2001) arguesthat organizations that have CEOs who are strategic leaders will create more value thanthose who have visionary or managerial leaders.

As we saw in the definitions above, there is no consensus on exactly what strategic leader-ship is, but certain themes do emerge. For instance, most of the definitions or conceptualiza-tions of strategic leadership mention the importance of studying CEOs and other top managersto better understand why some firms outperform others. Whether it is viewed as a style of lead-ership, a set of activities, or a broad area of study, strategic leadership is viewed by many ascritical to firm success, especially given our complex, global business environment.

Several themes emerge in the literature concerning what strategic leaders do to increasefirm performance. They look after both the short-term operational side of their organi-zation and the long-term directional aspects, such as defining the firm’s purpose (Phillips& Hunt, 1992; Rowe, 2001). Strategic leaders select and develop other organizationalmembers to ensure that these successful strategic leader abilities will exist throughout theorganization, not just at the top. They influence others by behaving ethically and transpar-ently. Strategic leaders who have overall responsibility for the firm (such as a CEO) artic-ulate a vision that will provide the organization’s members with meaning and guidance.They are also in a position to influence external constituents, such as suppliers, unions,

300 • CASES IN LEADERSHIP

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 300

and government agencies. Strategic leaders who incorporate these important activities canhelp ensure the future competitiveness of the firm.

NOTE

1. Steven J. Ross is the former chairman and co-CEO of Time Warner.

REFERENCES

Boal, K. B., & Hooijberg, R. (2001). Strategic leadership research: Moving on. The LeadershipQuarterly, 11, 515–549.

Daft, R. L. (2005). The leadership experience (3rd ed.). Mason, OH: Thomson, South-Western.Finkelstein, S., & Hambrick, D. C. (1996). Strategic leadership: Top executives and their effects on

organizations. St. Paul, MN: West.Hosmer, L. T. (1982). The importance of strategic leadership. Journal of Business Strategy, 3, 47–57.House, R. J., & Aditya, R. N. (1997). The social scientific study of leadership: Quo vadis? Journal

of Management, 2(23), 409–473.Ireland, R. D., & Hitt, M. A. (1999). Achieving and maintaining strategic competitiveness in the 21st

century: The role of strategic leadership. Academy of Management Executive, 13, 43–57.Loeb, M. (1993, January 24). Steven J. Ross, 1927–1992. Fortune, p. 4.Phillips, R. L., & Hunt, J. G. (1992). Strategic leadership: A multi-organizational-level perspective.

London: Quorum Books.Rowe, W. G. (2001). Creating wealth in organizations: The role of strategic leadership. Academy of

Management Executive, 15, 81–94.Shrivastava, P., & Nachman, S. A. (1989). Strategic leadership patterns. Strategic Management

Journal, 10, 51–66.

THE CASES

Vic Young and Fishery Products International (A)

Fishery Products International Ltd. is one of the largest seafood companies in NorthAmerica. In January 2000, Vic Young marked his 15th anniversary as the only chief exec-utive officer of the company. Under his leadership, the company overcame the collapse ofthe North Atlantic fishery to become an international seafood company and an importantcontributor to the Newfoundland and Labrador economy. However, its share price has lan-guished, and the company was recently the target of a hostile takeover bid. The bid wasunsuccessful, due partly to government regulation on the company’s stock ownership, butYoung realizes another attempt is possible and wonders how to maintain shareholder con-fidence in Fishery Products’ current board and management team.

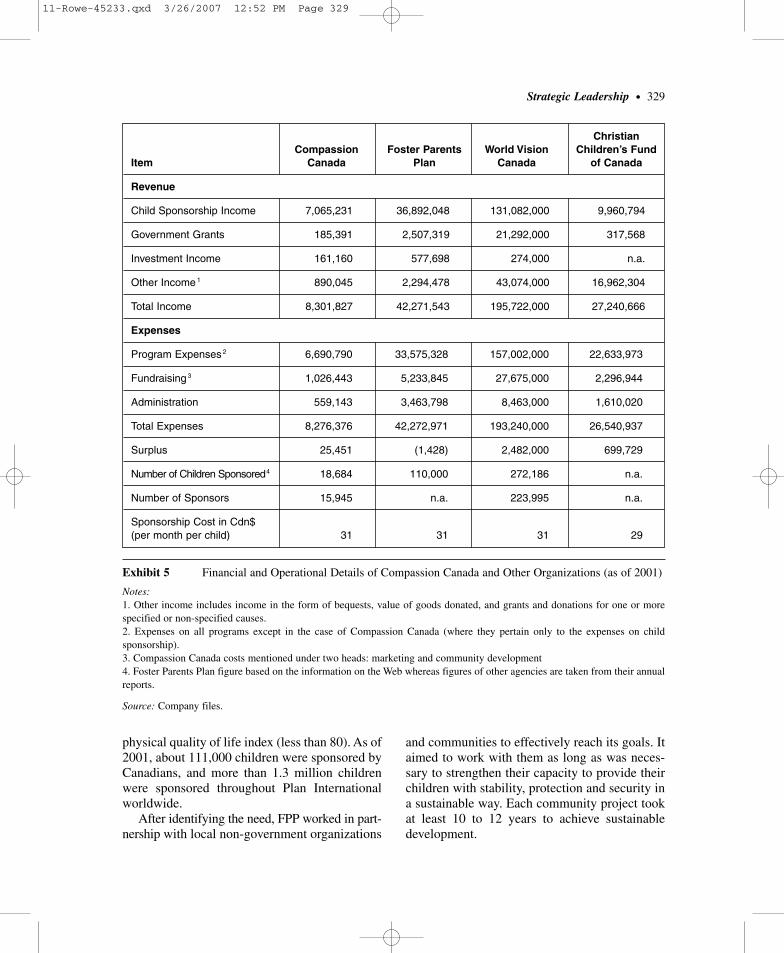

Compassion Canada

Compassion Canada is a nonprofit ministry focusing on the holistic development ofpoor children in developing countries. Over the past 10 years, the organization has onlydoubled its sponsorships. The chief executive officer must analyze the organization’s

Strategic Leadership • 301

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 301

performance and develop a strategic plan that will enable Compassion Canada to reach itsgoal of fivefold growth over the next 10 years.

THE READING

You’re an Entrepreneur: But Do You Exercise Strategic Leadership?

This brief article describes the differences among the concepts of strategic leadership,visionary leadership, and managerial leadership. In addition, it defines strategic leader-ship. It describes two entrepreneurs who developed large organizations that created wealthfor their owners.

302 • CASES IN LEADERSHIP

VIC YOUNG AND FISHERYPRODUCTS INTERNATIONAL (A)1

Prepared by John Melnyk, Tami L. Hynes and W. Glenn RoweCopyright © 2003, Ivey Management Services Version: (A) 2004–02–03

In January 2000, Vic Young marked his 15thanniversary as the chief executive officer (CEO)of Fishery Products International Ltd. (FPI).

As the only CEO of FPI since its inceptionin December 1984, Young had led the companythrough a host of challenges—labor unrest, theloss of a crucial source of supply, internationalexpansion, economic recession and a recent hos-tile takeover bid by competitors.

In the process, FPI had grown to become one ofthe largest seafood companies in North America,producing and selling a wide range of seafoodproducts around the world. Its important role in itshome province’s economy was recognized with aNewfoundland and Labrador Export Award in1998. Young was named Financial Times CEO ofthe Year in 1994, and made an Officer of the Orderof Canada in 1996 as “a model of corporate respon-sibility for industry leaders.”2

FPI’s earnings per share (EPS) from opera-tions for 1999 were $0.72,3 up from $0.55 in1998, a fourth consecutive annual increase.Despite this, the company’s stock had languishedin thin trading on the Toronto Stock Exchange

(TSE), and the company had been the target ofan unsolicited takeover bid in November 1999.Although that bid had been unsuccessful, Youngrealized that another attempt was very possibleand wondered how he could convince sharehold-ers to remain confident in FPI’s current board ofdirectors and management team.

HISTORY

The North Atlantic fishery had a long history.Early explorers returned from voyages to theNew World with stories of fish so numerous “theyimpeded the progress of the ships” and “could bescooped up from the side of the boat in a basket.”

This seemingly inexhaustible resource drewEuropean settlers to the region as early as the1500s. They built a fishery based on hard workand simple technology—small wooden boats,nets handled by hand and family operations—that continued almost unchanged for hundreds ofyears, becoming the basis for a regional eco-nomy and way of life. However fish stocks

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 302

migrated away from the coastline during winter,so it was a seasonal industry, and thus supportedonly a meager living for most.

The advent of large steam-powered fishingvessels in the mid-1900s held promise to breakthe cycle of seasonal employment and govern-ment support that had become prevalent in the region that by then had become “AtlanticCanada.”4 These large trawlers could follow thefish out to sea in winter and use huge mecha-nized nets to harvest year-round, storing catchesat sea for up to 10 days at a time. This mass-production fishery carried on by company-owned trawlers far out at sea became known asthe “offshore” fishery, and the smaller closer-to-shore operations of independent fisherman as the“inshore” fishery.

The prospect of large catches on a year-roundbasis led to significant investment in new pro-cessing capacity throughout the region, oftengenerously encouraged by government in thehope of generating permanent employment; thenumber of fish processing plants jumped from 89in 1971 to 249 in 1982. These developments ledto widespread economic optimism that drownedout concerns of some fishermen and scientistswho had begun to notice that the fish were not asplentiful as in the past.

By the early 1980s, declining catches, highinterest rates and changing consumer tastestowards higher quality products caused severalfishing companies to fail, despite escalating government loan guarantees and direct subsidiesintended to preserve employment in the region.

In response to this situation, the governmentof Canada and the affected provincial govern-ments stepped in to restructure the Atlantic fish-ery. Two of the largest independent companies,National Sea Products (based in Nova Scotia) andFishery Products Ltd. (based in Newfoundland),were chosen as the vehicles to create an econom-ically viable and competitive industry.

Fishery Products International—A Fresh Start

In December 1984, Fishery Products Ltd.,two other corporate entities and assets from

several other seafood companies were amalga-mated to form Fishery Products InternationalLtd. Through a $150-million package of cashand conversion of debt to equity, the federal gov-ernment ended up holding 63 percent of the newcompany; the Newfoundland and Labrador government, 26 percent and the Bank of NovaScotia, 11 percent.

Vic Young, then chairman and CEO ofNewfoundland Hydro Group, a provincialCrown corporation,5 was jointly appointed by theprovincial and federal governments to lead thenewly formed company. Young had started hiscareer with the provincial government in 1968and had risen to deputy minister of the TreasuryBoard at age 27, from which position he laterserved as special advisor to the Premier ofNewfoundland and Labrador.

At the time of Young’s appointment, FPI wasstill operating under bankruptcy protection andembroiled in a major strike. Young was able toresolve these issues and under his leadership, thecompany quickly embarked on a modernizationprogram, closing or selling marginal assets andinvesting in the 19 processing plants, 58 fishingvessels and eight port facilities it continued tooperate.

FPI operated as a Crown corporation for itsfirst three years, suffering losses in 1984 and1985, but achieving profitability by 1986. As hadbeen planned at the time of the government inter-vention, FPI was then returned to the private sector, albeit with some conditions.

An Act Respecting the Return of the Businessof Fishery Products International Limited toPrivate Investors (the FPI Act), passed by theNewfoundland government to privatize FPI, stip-ulated that no single shareholder could own morethan 15 percent of FPI’s common voting shares;that shareholders could not act in concert to circumvent this provision; that a majority of themembers of the board of directors be residents of Newfoundland; that the company could notapply to continue under another jurisdiction; thatthe company could not exit the business of har-vesting, processing and marketing seafood; andthat only one member of management could be a member of the board of directors. The limit of

Strategic Leadership • 303

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 303

304

* to

nn

es (

1 to

nn

e ==

2,20

5 p

ou

nd

s)19

9919

9819

9719

9619

9519

9419

9319

9219

9119

9019

8919

8819

87

Land

ings

1*

Gro

undf

ish

21,4

0016

,400

7,80

09,

900

5,20

010

,800

45,0

0069

,000

111,

100

123,

400

139,

300

164,

000

172,

700

She

llfis

h10

,200

8,50

06,

600

5,40

03,

600

4,00

0S

hrim

p16

,100

16,3

009,

400

6,40

06,

400

5,10

0O

ther

1,50

02,

800

3,30

03,

300

300

300

11,4

009,

800

11,8

0012

,400

12,0

0013

,600

8,90

0To

tal

49,2

0044

,000

27,1

0025

,000

15,5

0020

,200

56,4

0078

,800

122,

900

135,

800

151,

300

177,

600

181,

600

Pro

cure

men

t2*

Gro

undf

ish

fille

ts15

,500

15,3

0015

,700

14,5

0016

,100

14,9

0011

,900

8,20

04,

500

4,20

04,

100

2,10

01,

900

Sem

i-pro

cess

ed

3,00

06,

300

8,90

07,

400

7,90

010

,500

4,90

02,

300

——

——

—gr

ound

fish

Raw

shr

imp

2,30

02,

700

2,80

01,

800

1,60

01,

400

n/a

——

——

——

Tota

l20

,800

24,3

0027

,400

23,7

0025

,600

26,8

0016

,800

10,5

004,

500

4,20

04,

100

2,10

01,

900

Val

ue-a

dded

pro

duct

ion

*29

,300

28,7

0029

,300

25,1

0024

,400

25,7

0021

,500

18,9

0019

,300

20,8

0016

,300

17,2

0016

,300

Act

ive

vess

els

1815

1314

1213

3147

5151

6166

66(d

urin

g ye

ar)3

Act

ive

plan

ts

1111

1010

99

1017

1919

1919

19(d

urin

g ye

ar)3

Tota

l em

ploy

ees

3,40

03,

400

3,20

03,

000

2,60

02,

600

3,90

07,

200

8,40

08,

400

8,60

08,

600

8,60

0(d

urin

g ye

ar)3

She

llfis

h in

clud

ed in

Oth

er u

ntil

1994

Shr

imp

incl

uded

in O

ther

unt

il 19

94

Exh

ibit

1Se

lect

ed O

pera

ting

Stat

istic

s

Sour

ce:

FPI A

nnua

l Rep

orts

. Whe

re f

igur

es h

ave

been

res

tate

d in

late

r re

port

s,th

e m

ost r

ecen

t fig

ure

has

been

use

d.

1. L

andi

ngs

wer

e ha

rves

ted

by F

PI it

self

or

purc

hase

d fr

om in

depe

nden

t New

foun

dlan

d fi

sher

men

.2.

Pro

cure

men

t qua

ntiti

es w

ere

obta

ined

oth

er th

an b

y “l

andi

ng,”

prim

arily

fro

m in

tern

atio

nal s

ourc

es.

3. S

ome

of th

e ve

ssel

s,pl

ants

and

em

ploy

ees

show

n as

act

ive

duri

ng th

e ye

ar m

ay n

ot n

eces

sari

ly h

ave

been

act

ive

by y

ear

end.

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 304

15 percent ownership per shareholder was alsoenshrined in the FPI bylaws.6

Despite these conditions, FPI’s initial publicoffering (IPO), April 15, 1987, was successful,raising $177 million that was used to buy out the governments’ positions. Pension fundsand financial institutions took the bulk of the stock, but 560,000 shares were granted to eligi-ble employees, not including executives.

On its first trading day FPI stock closed up $3from its issue price of $12.50, and within a fewmonths had risen to $21.25. The shares paid divi-dends at an annual rate of $0.48, raised to $0.56 inDecember 1987. That year FPI also distributed $6.6million in profit-sharing to its employees, plus aspecial $1 million “Award for Excellence” for theircontribution to the company’s turnaround; it alsopaid a bonus to its inshore fishery suppliers for their “demonstration of loyalty.” The company’sachievements were recognized with a Gold Medalfor Productivity at the 1987 Canada Awards forBusiness Excellence, and a Canada Export Award.

Even before privatization, Young had setabout to make the company more market-drivenand diversified, investing heavily in technologyand its workforce, in order to be able to meetconsumer demands for higher quality products.

In June 1987, FPI completed the conversionof an old primary-processing7 plant in Burin,Newfoundland, into a world-class secondary-processing7 facility, tripling its capacity to 7,000tonnes per year, well above demand at the time. That same month, FPI entered into a joint-venture agreement to market FPI secondary-processed products in Japan with with NichiroGyogyo Kaisha (Nichiro), the third largestJapanese seafood trading company.

FPI had been exporting raw materials to Japan for years, but the Japanese consumer mar-ket posed very different challenges, including amaze of government regulations, culturally spe-cific business customs and exacting demands forunusual quality and packaging standards.

Nevertheless, FPI persisted, and with the helpof three quality control specialists from Nichiroworking in the Burin plant alongside FPIemployees for a time, eventually achieved the

capability to produce to rigorous Japanese specifications. A successful launch in February1988, made FPI the first North American seafoodcompany to have its value-added products onJapanese retail shelves.

Crises and Changes

In January 1989, the Government of Canadaannounced the first of what was to become aseries of reductions in fishing quotas for theAtlantic Canada fishery, in response to mountingconcerns about the state of the fish stock. Each of these reductions was a hotly debated compro-mise between environmental pressure to protectthe dwindling fish stocks and political pressureto maintain employment in Atlantic Canada bykeeping the fishery open. Before long, the roomfor compromise, like the fish stock itself, wasexhausted, and a complete moratorium on har-vesting several groundfish species,8 includingcod, was imposed on September 6, 1993.

Groundfish, of which cod was the most com-mon and valuable, had been the basis for 85 percent of FPI sales in the late 1980s—in 1987,FP had “landed” (either harvested itself orpurchased from independent Newfoundland fishermen) 172,700 metric tonnes of groundfish,primarily cod; in 1995, it would land just 5,200tonnes, none of which was cod. As a result, 6,000FPI employees eventually lost their jobs, astrawlers were deactivated and plants were closed(see Exhibit 1); even then, capacity utilization inthe remaining plants was only 65 percent.Surplus assets were sold or leased to the extentpossible, but often for only nominal amounts.Newfoundland-based assets had to be writtendown by $85 million, and the company sufferedlosses in the early 1990s (see Exhibits 2 and 3).

During this period, the company did its best tocushion the blow for its employees and theircommunities by spreading what work there wasamong its plants to allow as many workers aspossible to qualify for Employment Insurance9

(EI) payments from the federal government.Nevertheless, labor unrest and angry publicdemonstrations were widespread.

Strategic Leadership • 305

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 305

306

All

fig

ure

s ’0

00s

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

1987

Ass

ets

Cur

rent

Ass

ets

Cas

h$

916

933

5,60

94,

981

5,46

01,

659

7,25

63,

595

3,77

66,

190

5,82

834

,102

36,0

48A

ccou

nts

Rec

eiva

ble

80,6

4490

,424

84,1

5578

,178

71,7

4767

,521

58,3

7969

,517

61,9

0567

,945

57,2

4542

,305

38,9

92In

vent

orie

s11

9,47

112

3,86

615

0,01

211

1,37

412

2,00

212

4,15

111

2,12

613

0,44

997

,360

87,5

8887

,909

68,6

3265

,448

Pre

-pai

d E

xpen

ses

5,63

74,

429

3,89

63,

024

2,87

41,

832

1,96

72,

475

2,78

12,

825

2,52

02,

210

2,08

4To

tal C

urre

nt A

sset

s20

6,66

821

9,65

224

3,67

219

7,55

720

2,08

319

5,16

317

9,72

820

6,03

616

5,82

216

4,54

815

3,50

214

7,24

914

2,57

2P

rope

rty,

Pla

nt a

nd

93,6

7789

,318

71,1

6567

,501

66,1

4074

,585

76,6

9495

,907

152,

403

158,

522

159,

334

154,

123

134,

610

Equ

ipm

ent

(P,P

&E

)O

ther

Ass

ets

14,0

5716

,782

11,6

8110

,353

14,8

3912

,985

11,5

0810

,829

6,95

46,

348

16,3

967,

777

1,07

4

Tota

l Ass

ets

$314

,402

325,

752

326,

518

275,

411

283,

062

282,

733

267,

930

312,

772

325,

179

329,

418

329,

232

309,

149

278,

256

Lia

bili

ties

an

d S

har

eho

lder

s’E

qu

ity

Cur

rent

Lia

bilit

ies

Ban

k In

debt

edne

ss$4

3,12

470

,373

65,8

8042

,101

68,4

3051

,410

49,2

6456

,928

21,9

7419

,171

13,8

18—

—A

ccou

nts

Pay

able

&

37,2

5231

,739

41,6

5438

,211

35,0

8445

,488

49,0

7364

,045

48,6

1547

,782

56,7

8241

,853

45,3

63A

ccru

ed L

iabi

litie

sC

urre

nt P

ortio

n of

8,

351

8,26

26,

488

8,54

66,

077

6,35

75,

671

7,36

36,

398

7,55

77,

856

5,92

93,

174

Long

-ter

m L

iabi

litie

sTo

tal C

urre

nt L

iabi

litie

s88

,727

110,

374

114,

022

88,8

5810

9,59

110

3,25

510

4,00

812

8,33

676

,987

74,5

1078

,456

47,7

8248

,537

Long

-ter

m L

iabi

litie

s62

,323

57,4

7158

,351

37,0

4230

,314

32,2

4432

,415

37,4

1434

,230

40,6

1547

,785

38,5

9317

,487

Tota

l Lia

bili

ties

151,

050

167,

845

172,

373

125,

900

139,

905

135,

499

136,

423

165,

750

111,

217

115,

125

126,

241

86,3

7566

,024

Sha

re C

apita

l48

,044

48,4

3949

,148

52,1

1752

,023

51,9

7351

,942

51,9

2616

0,55

816

0,52

416

1,09

915

8,62

115

8,43

0C

ontr

ibut

ed S

urpl

us75

,083

75,3

8375

,836

79,4

1379

,413

79,4

1379

,413

108,

645

Ret

aine

d E

arni

ngs*

41,5

3533

,331

24,9

0516

,712

10,6

0213

,881

—(1

3,86

5)53

,434

53,7

2241

,951

64,1

5353

,802

For

eign

Cur

renc

y (1

,310

)75

44,

256

1,26

91,

119

1,96

715

231

6(3

0)47

(59)

Tran

slat

ion

Adj

ustm

ent

Tota

l Sh

areh

old

ers’

163,

352

157,

907

154,

145

149,

511

143,

157

147,

234

131,

507

147,

022

213,

962

214,

293

202,

991

222,

774

212,

232

Eq

uit

y

Tota

l Lia

bili

ties

an

d

$314

,402

325,

752

326,

518

275,

411

283,

062

282,

733

267,

930

312,

772

325,

179

329,

418

329,

232

309,

149

278,

256

Sh

areh

old

ers’

Eq

uit

y

Exh

ibit

2C

onso

lidat

ed B

alan

ce S

heet

s fo

r Yea

rs E

ndin

g D

ecem

ber

31

* A

ccum

ulat

ed D

efic

it ca

ncel

led

by a

tran

sfer

fro

m C

ontr

ibut

ed S

urpl

us in

199

3.

Sour

ce:

FPI A

nnua

l Rep

orts

. Whe

re f

igur

es h

ave

been

res

tate

d in

late

r re

port

s,th

e m

ost r

ecen

t fig

ure

has

been

use

d.

Con

trib

uted

Sur

plus

incl

uded

in S

hare

Cap

ital a

bove

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 306

307

All

fig

ure

s $0

00's

exce

pt

per

sh

are

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

1987

Sal

es$

708,

911

681,

563

675,

945

664,

598

643,

009

665,

596

601,

179

590,

351

542,

937

535,

044

349,

791

366,

611

395,

705

Cos

t of

Goo

ds S

old

633,

124

614,

467

613,

617

606,

473

593,

096

598,

250

549,

844

536,

373

483,

046

468,

924

314,

347

302,

808

285,

671

Gro

ss P

rofit

75,7

8767

,096

62,3

2858

,125

49,9

1367

,346

51,3

3553

,978

59,8

9166

,120

35,4

4463

,803

110,

034

Com

mis

sion

Inc

ome

3,32

72,

382

2,96

83,

665

3,39

44,

645

2,78

96,

502

7,28

18,

437

1,15

6

Gro

ss P

rofit

plu

s 79

,114

69,4

7865

,296

61,7

9053

,307

71,9

9154

,124

60,4

8067

,172

74,5

5736

,600

63,8

0311

0,03

4C

omm

issi

on

Adm

inis

trat

ion

and

45,4

5642

,152

39,9

6339

,865

39,7

1140

,718

32,9

7544

,945

44,9

8847

,335

33,6

8729

,444

27,9

66M

arke

ting

Dep

reci

atio

n an

d 9,

883

8,96

78,

656

7,87

28,

484

8,38

010

,040

12,4

4115

,005

16,6

9414

,849

13,3

6013

,763

Am

ortiz

atio

nP

rofit

Sha

ring

1,54

11,

088

1,06

384

0—

1,68

4—

—11

058

6—

1,83

77,

599

Inte

rest

7,14

67,

467

5,89

05,

669

8,24

26,

786

6,66

76,

210

5,07

44,

566

665

159

46

Ope

ratin

g E

xpen

ses

64,0

2659

,674

55,5

7254

,246

56,4

3757

,568

49,6

8263

,596

65,1

7769

,181

49,2

0144

,800

49,3

74

Ope

ratin

g In

com

e15

,088

9,80

49,

724

7,54

4(3

,130

)14

,423

4,44

2(3

,116

)1,

995

5,37

6(1

2,60

1)19

,003

60,6

60

Gai

n (lo

ss)

on

715

1,00

53,

202

(998

)(1

04)

(1,3

34)

(1,8

08)

(2,2

70)

For

eign

Exc

hang

eG

ain

(loss

) on

21

438

182

959

203

Dis

posa

l of

P,P

&E

Sha

re in

gai

n (lo

ss)

(1,0

27)

(1,6

75)

of jo

int

vent

ure

Ext

raor

dina

ry I

tem

(s)

(965

)(2

0,00

0)(6

5,00

0)(1

85)

7,96

2(7

,500

)26

,959

Inco

me

befo

re

14,1

239,

804

9,72

47,

565

(2,6

92)

15,3

20(1

4,62

1)(6

6,38

6)81

213

,234

(21,

435)

17,1

9585

,349

Inco

me

Taxe

s

Inco

me

Taxe

s4,

097

1,37

81,

531

1,45

558

71,

439

746

913

1,10

01,

463

767

440

27,3

86

Net

Inc

ome

10,0

268,

426

8,19

36,

110

(3,2

79)

13,8

81(1

5,36

7)(6

7,29

9)(2

88)

11,7

71(2

2,20

2)16

,755

57,9

63

Net

Inc

ome

per

shar

e$

0.66

0.55

0.51

0.37

(0.2

0)0.

85(0

.94)

(4.1

0)(0

.02)

0.72

(1.3

8)1.

053.

62

Exh

ibit

3C

onso

lidat

ed S

tate

men

ts o

f In

com

e fo

r Yea

rs E

ndin

g D

ecem

ber

31

Sour

ce:

FPI A

nnua

l Rep

orts

. Whe

re f

igur

es h

ave

been

res

tate

d in

late

r re

port

s,th

e m

ost r

ecen

t fig

ure

has

been

use

d..

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 307

Over time, FPI was able to compensate somewhat by developing an international procure-ment network to source cod and other groundfish(from Alaska, Iceland, Norway and Russia) forprocessing in Newfoundland and by developinguses for other groundfish species for which the stock in Canadian waters was more plentiful.However, even by 1999, the company’s ground-fish processing was still limited to three plantsoperating on a seasonal basis.

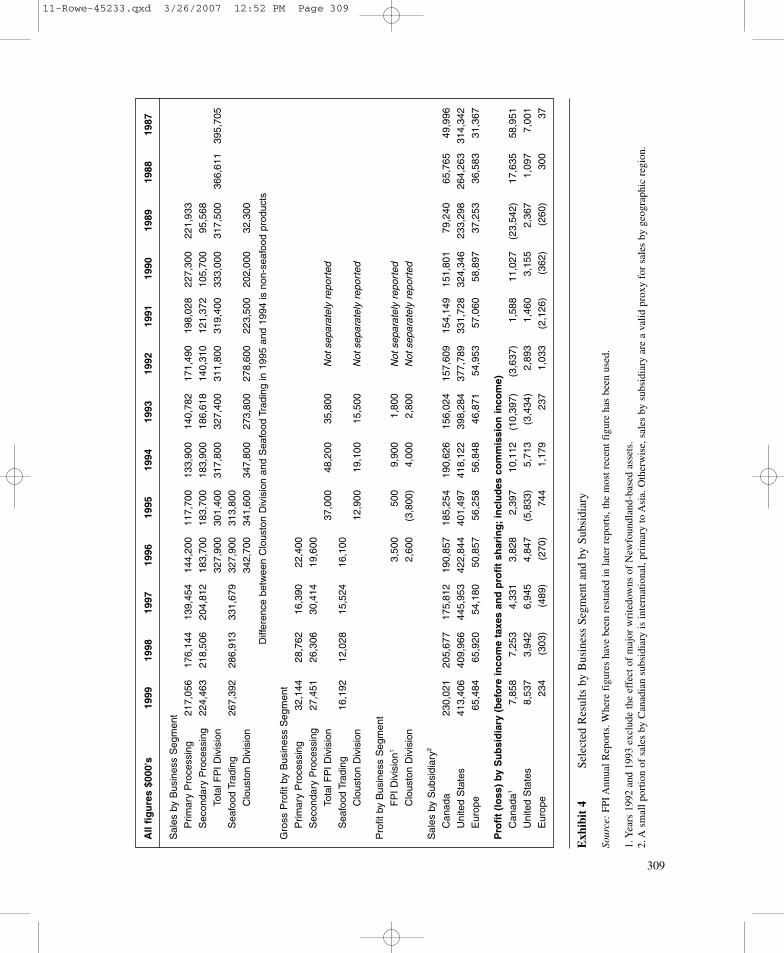

The effect on FPI’s revenue was mitigated by the October 1989 acquisition—FPI’s first—ofClouston Foods of Montreal, an internationalseafood trading, marketing and brokerage opera-tion with a substantial presence in the Canadianmarket. The acquisition operated as a separatedivision for a time, buying and selling seafood,primarily shrimp, throughout the world. Thesenew activities added $202 million to FPI 1990sales (see Exhibit 4), albeit at a lower marginthan the production activities. The Clouston division also came to act as FPI’s marketing armin Canada and Europe, as FPI placed new empha-sis on producing and marketing secondary-processed products.

In September 1992, FPI acquired the U.S.foodservice business of National Sea Products.This strengthened the company’s position in theAmerican market and brought the establishedvalue-added shrimp brand “Treasure Isle” to itsproduct portfolio. At first, FPI had to contract outproduction for this new line, but soon brought itin-house at its Boston plant, as shrimp and othershellfish10 became an important new product cat-egory for the company.

Shrimp was the largest species component of per capita seafood consumption in NorthAmerica on a dollar basis, and demand wasgrowing. In 1990, FPI commissioned a newshrimp freezer trawler to take fuller advantage of the cold-water shrimp resources offNewfoundland and Labrador that were still in ahealthy state. In the following years, it twiceupgraded its shrimp processing facility in Port au Choix and also converted an idle groundfishplant at Port Union to shrimp. By the late 1990s,the company had become dominant in the

Newfoundland cold-water shrimp industry,even introducing a new branding strategy, “FPIIce Shrimp, from the Icy Cold Waters ofNewfoundland.”

By 1995, these adjustments in progress hadstabilized the company’s situation, but there wasa significant downturn in the seafood market thatyear. In response, FPI consolidated its two U.S.processing plants into one (realizing $5 millionfrom sale of the redundant plant), and subse-quently consolidated U.S. warehousing opera-tions around the remaining plant in Danvers,Massachusetts. These changes resulted in annualoperating savings of $2.5 million and superiordistribution capabilities for the U.S. market.

Seafood trading continued to make up a sig-nificant portion of FPI sales. However, towardsthe end of the decade, the company chose tofocus on core product lines and eliminate anycategories in which FPI could not differentiate.

THE SEAFOOD INDUSTRY

Seafood was a global commodity, sourced,processed, sold and consumed worldwide. TheFood and Agriculture Organization of the UnitedNations (FAO) estimated that 30 million peopleworldwide derived a living from the fishingindustry in 1997, and that 95 percent of fisherswere from developing countries.

After increasing steadily for more than 30years, annual world harvest of fish from naturalhabitat had dropped sharply in 1990, stabiliz-ing between 90 million and 95 million tonnesthrough the mid-1990s. The FAO estimated that70 percent of marine species were then beingharvested at, or beyond, sustainable levels. As aresult, aquaculture (fish farming) was becom-ing more important, producing 28 million tonnesworldwide in 1997, more than double the 1990quantity.

Human consumption of seafood grew steadilythroughout the 1990s, but growth was slowingdue to supply constraints. Seafood was generallywell regarded as a healthy and nutritious food,but had to compete with other protein sources

308 • CASES IN LEADERSHIP

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 308

309

All

fig

ure

s $0

00's

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

1987

Sal

es b

y B

usin

ess

Seg

men

t

Prim

ary

Pro

cess

ing

217,

056

176,

144

139,

454

144,

200

117,

700

133,

900

140,

782

171,

490

198,

028

227,

300

221,

933

Sec

onda

ry P

roce

ssin

g22

4,46

321

8,50

620

4,81

218

3,70

018

3,70

018

3,90

018

6,61

814

0,31

012

1,37

210

5,70

095

,568

Tota

l FP

I D

ivis

ion

327,

900

301,

400

317,

800

327,

400

311,

800

319,

400

333,

000

317,

500

366,

611

395,

705

Sea

food

Tra

ding

267,

392

286,

913

331,

679

327,

900

313,

800

Clo

usto

n D

ivis

ion

342,

700

341,

600

347,

800

273,

800

278,

600

223,

500

202,

000

32,3

00

Gro

ss P

rofit

by

Bus

ines

s S

egm

ent

Prim

ary

Pro

cess

ing

32,1

4428

,762

16,3

9022

,400

Sec

onda

ry P

roce

ssin

g27

,451

26,3

0630

,414

19,6

00

Tota

l FP

I D

ivis

ion

37,0

0048

,200

35,8

00

Sea

food

Tra

ding

16,1

9212

,028

15,5

2416

,100

Clo

usto

n D

ivis

ion

12,9

0019

,100

15,5

00

Pro

fit b

y B

usin

ess

Seg

men

t

FP

I D

ivis

ion1

3,50

050

09,

900

1,80

0

Clo

usto

n D

ivis

ion

2,60

0(3

,800

)4,

000

2,80

0

Sal

es b

y S

ubsi

diar

y2

Can

ada

230,

021

205,

677

175,

812

190,

857

185,

254

190,

626

156,

024

157,

609

154,

149

151,

801

79,2

4065

,765

49,9

96

Uni

ted

Sta

tes

413,

406

409,

966

445,

953

422,

844

401,

497

418,

122

398,

284

377,

789

331,

728

324,

346

233,

298

264,

263

314,

342

Eur

ope

65,4

8465

,920

54,1

8050

,857

56,2

5856

,848

46,8

7154

,953

57,0

6058

,897

37,2

5336

,583

31,3

67

Pro

fit

(lo

ss)

by S

ub

sid

iary

(b

efo

re in

com

e ta

xes

and

pro

fit

shar

ing

;in

clu

des

co

mm

issi

on

inco

me)

Can

ada1

7,85

87,

253

4,33

13,

828

2,39

710

,112

(10,

397)

(3,6

37)

1,58

811

,027

(23,

542)

17,6

3558

,951

Uni

ted

Sta

tes

8,53

73,

942

6,94

54,

847

(5,8

33)

5,71

3(3

,434

)2,

893

1,46

03,

155

2,36

71,

097

7,00

1

Eur

ope

234

(303

)(4

89)

(270

)74

41,

179

237

1,03

3(2

,126

)(3

62)

(260

)30

037

Exh

ibit

4Se

lect

ed R

esul

ts b

y B

usin

ess

Segm

ent a

nd b

y Su

bsid

iary

Sour

ce:

FPI A

nnua

l Rep

orts

. Whe

re f

igur

es h

ave

been

res

tate

d in

late

r re

port

s,th

e m

ost r

ecen

t fig

ure

has

been

use

d.

1. Y

ears

199

2 an

d 19

93 e

xclu

de th

e ef

fect

of

maj

or w

rite

dow

ns o

f N

ewfo

undl

and-

base

d as

sets

.2.

A s

mal

l por

tion

of s

ales

by

Can

adia

n su

bsid

iary

is in

tern

atio

nal,

prim

ary

to A

sia.

Oth

erw

ise,

sale

s by

sub

sidi

ary

are

a va

lid p

roxy

for

sal

es b

y ge

ogra

phic

reg

ion.

Diff

eren

ce b

etw

een

Clo

usto

n D

ivis

ion

and

Sea

food

Tra

ding

in 1

995

and

1994

is n

on-s

eafo

od p

rodu

cts

Not

sep

arat

ely

repo

rted

Not

sep

arat

ely

repo

rted

Not

sep

arat

ely

repo

rted

Not

sep

arat

ely

repo

rted

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 309

such as poultry, pork and beef, as well as pasta,all of which were very cost-competitive.

Japan and the United States were traditionallythe top seafood importers by a wide margin.Canada ranked 11th in seafood imports and sixth in seafood exports in 1997. Most of Canada’sfish products were exported to the United States(see Exhibit 5) where American consumers spentalmost $50 billion per year on seafood products.Japan and the United Kingdom were Canada’ssecond and third most important export marketsrespectively.

In most countries, raw material was pur-chased through free market, auction and/or directsales mechanisms. Prices were thus driven byglobal supply and demand, reflecting a variety offactors: seasonal variations in yields, supplyinterruptions due to natural disasters, changes inthe cost of fishing inputs such as fuel oil, traderestrictions such as tariffs and foreign exchangerate fluctuations.

The market for seafood products was highlycompetitive, with buyers at all levels demandinghigh-quality product and service at competitiveprices. Processors purchased raw material (fish)from seafood harvesters and developed basic orvalue-added packaged seafood products to bemarketed through wholesale and/or retail chan-nels around the world. Generally, margins werehighest for the fish harvesters at the beginning ofthe supply chain, and for retailers and restaurantsselling to end-consumers.

Fishery Management

The sustainability of global fish stocks was a critical issue for the industry. Significant overfishing in many parts of the world had seri-ously depleted stocks of certain species, threat-ening the viability of both harvesters and fishprocessors.

Industry and government had joined efforts inmany countries to try to ensure a sustainableresource base, and the Northwest AtlanticFishing Organization (NAFO) attempted to pro-mote international consultation and co-operationfor “the optimum utilization, rational manage-ment and conservation of the northwest Atlanticfishery resources.”11 In Canada, the federalDepartment of Fisheries and Oceans (DFO)worked with provinces and territories to managefishery resources and balance quotas with pro-cessing capacity.

Under the Law of the Sea, Canada had eco-nomic jurisdiction over the 200-mile zone offthe coast of Atlantic Canada. This area wasdivided into three divisions and 16 zones. TheDFO established “total allowable catch”(TAC) quotas for each of these zones to limithow many fish could be harvested each year;this allocation also, in effect, divided theresource among the four Atlantic Canadaprovinces.

The TAC for each zone was split between theinshore and offshore fisheries, and the offshore

310 • CASES IN LEADERSHIP

Origin/Destination Jan-98 Jan-99 Jan-00

Canada to United States 649 807 1,106

Canada to All Countries 1,480 1,603 2,052

Canada to All Countries 909 964 1,215— shrimp, scallops, crab,

groundfish only

Exhibit 5 Canadian Fish Exports (Cdn$ millions)

Source: Industry Canada (2000).

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 310

quotas were then allocated to individual compa-nies by means of licences, giving them the rightto harvest certain amounts of specific fish. FPIregularly received the largest TAC allocation ofany company.

Fish processors also required licences foreach species; these were issued by provincial and territorial governments. Only Canadian-controlled companies were eligible for theselicences.

These regulations strictly limited foreignaccess to fish stocks off the Canadian coast,and as a consequence, many European nationsimposed high tariffs on Canadian seafoodimports. However, neither Canadian regulationsnor the voluntary NAFO guidelines could pre-vent foreign vessels from fishing just outside the

edge of Canada’s 200-mile economic zone. Thiswas a source of constant concern to the Canadianfishing industry.

Competition

Besides FPI, major publicly held competitorsin the international seafood industry includedSanford Limited, Icelandic Freezing PlantsCorporation Plc. and High Liner Foods Inc. (seeExhibit 6). There were also a number of signifi-cant privately held competitors. These includedClearwater Fine Foods Inc. and The Barry Groupof Companies.

Icelandic Freezing Plants Corporation Plc.(IFPC) employed nearly 1,400 people of whom1,300 were based outside of Iceland in subsidiaries

Strategic Leadership • 311

High LinerFirm FPI Ltd. Foods Inc. Sanford Limited IFPC Plc.

Headquartered Canada Canada New Zealand Iceland

Revenue $ 708,911 $ 302,392 $ 265,555 $ 760,125

Net Income $ 10,026 $ (4,067) $ 40,740 $ (3,731)

Total Assets $ 314,412 $ 219,901 $ 297,979 $ 381,425

Current Ratio 3.32 1.68 1.25 1.14

Cost of Goods Sold % 89% 74% Not Published 87%

ROE (After Taxes) 6.14% −0.06% 18.40% −6.28%

ROE (Before Taxes) 9.00% −0.05% 22.00% N/A

Earnings per Share $ 0.66 $ (0.56) $ 0.41 $ (0.12)

Number of Employees 3,000 1,500 13,005 1,300

Subsidiaries & Associates 4 3 18 6

Ownership/ Shareholders Maximum 15% No Restrictions; 2,547 shareholders; Information not per shareholder (two shareholders one shareholder available

own in aggregate holds 37%; no over 50%) maximum evident

Exhibit 6 Significant Publicly Held Competitors in the Seafood Industry

Note: All figures on consolidated basis for 1999, converted if necessary to Canadian dollars using nominal rate of January 1, 2000.

Source: Corporate Web sites and Annual Reports.

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 311

located in Europe, Russia, Norway, the UnitedKingdom and the United States. IFPC offeredover 40 species, primarily harvested near Iceland,and sold in over 30 countries including the FarEast. Its customers included large supermarkets,distributors, wholesalers, as well as restaurantsand food processors for its product line of wholefrozen fish, fillets and fillet portions, shellfish anda wide variety of convenience products.

Sanford Limited (Sanford) was New Zealand’slargest seafood company with 18 subsidiaries,associate companies in four countries and 1,500employees. Sanford produced a wide range ofseafood products, primarily for export to Europe(31 percent of sales) and to North and SouthAmerica (23 percent). Sanford was one of theoldest publicly listed companies in New Zealand.One shareholder owned 37 percent of the company.

There were approximately 1,000 seafoodcompanies operating in the United States, and150 in Canada. These varied widely in size andproduct line. Like IFPC and Sanford, many ofthese firms (including FPI) were vertically integrated, fishing from company-owned vessels,processing in company-owned plants, and distributing and marketing through in-houserepresentatives.

Canadian-based High Liner Foods Ltd. (HighLiner), formerly National Sea Products, was thelargest Atlantic Canada-based supplier of freshgroundfish to the U.S. market. It processed andmarketed seafood under High Liner and otherbrands and had a strong position in the retail frozen seafood market. The company operated inNova Scotia, Ontario and the United States andemployed 1,500 people. High Liner procured mostof its raw material internationally, although it alsoharvested approximately 11,000 tonnes of seafoodeach year from Nova Scotia to Labrador. Even so,the company’s advanced processing facilities oper-ated at just over 40 percent capacity. High Linerhad recently diversified into non-seafood productsby acquiring Italian Village, a pasta products oper-ation. Two corporate investors owned more than 50 percent of High Liner’s shares.

The Barry Group of Companies (The BarryGroup), based in Corner Brook, Newfoundland,

was a fourth-generation family business estab-lished in 1910. It owned and operated 17 plantsin Atlantic Canada employing more than 3,000people, and marketed its products under theOcean Leader and Seafreeze brands.

Clearwater Fine Foods Inc., (Clearwater)based in Halifax, Nova Scotia, specialized in lob-ster, sea scallops, surf clams and shrimp. Thecompany owned and operated eight shore-basedprocessing plants in Atlantic Canada as well as23 vessels with capacity to harvest more than20,000 tonnes of fish per year. Clearwateremployed more than 2,000 people, 1,100 ofwhom had been added since the cod moratoriumhad been announced.

FISHERY PRODUCTS

INTERNATIONAL LTD. IN 2000

FPI was headquartered in St. John’s, Newfoundlandand Labrador, Canada, and had subsidiaries inthe United States and Europe.

Company advertisements proclaimed “theFPI flag flies proudly in 42 countries.” FPI main-tained sales offices in Canada (St. John’s,Montreal, Toronto, Calgary and Vancouver),the United States (Danvers, Massachusetts and Seattle, Washington), Reading, England, andCuxhavin, Germany, as well as a brokerage anddistribution network throughout North Americaand Europe. The Canadian operation handledexports to Asia.

The company also had co-packing arrange-ments in shrimp-processing plants in Thailand,Ecuador, Indonesia and Mexico; at fish-process-ing facilities in Norway and Chile; and at aqua-culture farms and secondary-processing plants in China. Integrated information systems keptemployees around the world connected to suppli-ers, customers and each other in real time.

Products and Marketing

FPI produced and marketed primary- andsecondary-processed seafood products including

312 • CASES IN LEADERSHIP

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 312

cold-water shrimp, snow crab, sea scallops, cod,flounder, sole, redfish, pollock, Greenland hal-ibut, haddock and capelin.

FPI was a leading marketer of primary-processed cold-water shrimp and snow crab inEurope, North America and Asia. Three-quartersof FPI’s value-added sales were to the foodser-vice market (restaurant and hotel chains, airlinecaterers, hospitals, etc.) and wholesale clubstores in the United States. Most of the remain-ing 25 percent went to restaurant and retail markets in Canada, where FPI was the leadingsupplier to the private label market. Some wentto overseas markets, primarily Switzerland,which was the only tariff-free European countryfor Canadian seafood exports in 2000.

The company conducted product develop-ment through a full-time staff of food scientistsand food technologists. FPI’s development staff often worked closely with customer menu-development departments, to generate newprocess concepts and value-added products. Newproduct launches annually generated more than15 percent of FPI sales.

FPI had developed a strong brand and a repu-tation for quality. Buyers frequently requestedFPI products by brand name, and the companywas regularly recognized for its sales and marketing excellence by industry associationsand independent trade organizations. In 1999,FPI received “outstanding supplier” awards fromNorth America’s largest independent foodservicedistributor, largest retail chain, and severalnational restaurant chains.

These customers tended to be somewhat flexible regarding price if they were assured of astable and high-quality supply. However, largecustomers such as McDonald’s, Price Club andRed Lobster posed a special challenge for FPIand all seafood companies because of their pricesensitivity. These customers demanded top qual-ity and excellent service, but were quite preparedto switch suppliers or even change to substitutefoodstuffs at a certain price point.

The company’s seafood trading businessearned commission income by brokering interna-tionally sourced seafood products such as black

tiger and warm water shrimp (which made up 60 percent of trading sales), king crab, farmedscallops, North Atlantic lobster, salmon and seabass. These products, many originating fromaquaculture, were sourced from other producersin North America, Southeast Asia, SouthAmerica and Europe.

Operations

FPI reported its operations in three categories:primary processing, secondary processing andseafood trading (see Exhibit 4).

Primary processing turned fresh-caught fishinto ready-to-market basic products (such asloose fillets or shrimp) or into inputs for furthervalue-added processing. All primary processingwas done in Atlantic Canada through nineprocessing plants, many of which had beenupgraded to state-of-the-art technology.

Secondary processing increased the value ofprimary-processed products by adding non-seafood ingredients such as batter, stuffings andsauces to create finished products ready for con-sumers’ plates. FPI’s two secondary processingplants (Burin, Newfoundland, for the Canadianmarket and Danvers, Massachusetts, for the U.S.market) had recently been upgraded with newtechnologies such as automated weighing, pack-aging and freezing capabilities and now had acombined annual capacity of 43,000 tonnes ofvalue-added products.

All FPI plants were treated as cost centres. Asa result, plant management tended to be verycost-conscious and operated relatively indepen-dently of the marketing side of the company.

Raw material for the plants was partiallysourced by FPI’s own fleet of 18 fishingvessels—12 outfitted for catching groundfish,five for sea scallops and one for shrimp—thatoperated off Newfoundland and Nova Scotia andwere serviced from the company’s refit centre in Burin. This backward integration reducedvolatility in raw material costs and secured a cer-tain volume of supply. However, natural condi-tions and government quotas limited its totalcatch, so FPI also purchased raw material from

Strategic Leadership • 313

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 313

more than 3,000 independent Newfoundlandfishers, and sourced 25 seafood species fromover 30 countries. FPI technical personnelworked with suppliers at source around theworld to ensure quality and to build long-termsupplier relationships.

Quality Assurance and Environmental Awareness

All seafood companies were required to adhereto strict quality assurance standards. FPI’s qualityassurance practices and processing facilitiescontinually met or exceeded the Canadian FoodInspection Agency’s (CFIA) regulatory require-ments. FPI was periodically audited by the CFIA,the U.S. Food and Drug Administration, the U.S.Department of Commerce and customers.

FPI’s quality management programs werebased on the principles of Hazard AnalysisCritical Control Point (HACCP), originallydeveloped by the Pillsbury Company to providesafe food for American astronauts. An HACCPsystem involved inspection at different points of the production process, rather than simplyinspecting the end product. Many importers,including all U.S. companies, accepted seafoodproducts only from foreign suppliers using anHACCP system.

FPI was committed to maintaining a sustain-able fishery and regularly stated its support forthe DFO’s conservation measures, difficult asthose had been for the company. Manage-ment structure included a standing committeethat monitored operations to ensure regulatorycompliance and sound environmental policies.The company continually improved its fishing practices to avoid catching undersized fish or restricted species and fully supported indepen-dent-observer monitoring of its harvesting oper-ations.

FPI vessels and crew had participated in 25directed research surveys in co-operation withthe DFO to gather scientific data on which TACquotas were based. FPI also supported tworesearch chairs in oceanography and fish conser-vation at Memorial University in St. John’s withmore than $800,000 in grants.

Human Resources

Teamwork and innovation have beenthe heart and soul of our success. . . .While seafood is our business, peopleare our strength.

—Vic Young, FPI 1999 Annual Report

Of FPI’s 3,400 employees worldwide, 3,000worked in Atlantic Canada. The company’sannual reports consistently attributed its successto the commitment of its employees. Turnoverwas low among staff and executive management.

Trawler workers, plant workers and fisherswere unionized through the Fish, Food andAllied Workers (FFAW) affiliated with theCanadian Auto Workers (CAW). The company’srelationships with its employees and theirunions, as well as with the communities in whichit operated, were positive. Many people attrib-uted this to Young, whose negotiating abilitieswere recognized beyond the company; as aspecial mediator for a 1994 labor disputebetween Newfoundland and Labrador teachersand the provincial government, Young was cred-ited with preventing a bitter strike.

Collective agreements had provided for wage increases for FPI’s Newfoundland-basedemployees in eight of the last nine years, and thecompany considered the wages it paid to be“industry-leading.” As well, the company had adefined benefit pension plan and a profit-sharingplan that distributed 10 percent of pre-tax profitbefore extraordinary items to employees. FPI alsoreserved over 200,000 shares issuable at marketvalue for its employee share purchase plan.

In 1997, FPI appointed its first female plantmanager, Angela Bugden, at its Riverport, NovaScotia, scallop-harvesting operation. Bugdenwas also responsible for the five scallop trawlersand the refit yard for those vessels.

As part of its long-standing commitment tothe professional development of its employees,FPI had invested in teamwork training for themanagement teams at its two shrimp plants.Team building posed some special challenges inthe small, closely knit Newfoundland communi-ties, in which a single extended family might

314 • CASES IN LEADERSHIP

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 314

include a member of plant management, a unionrepresentative, as well as independent fishermenand plant employees. As a result, informationabout cost structure was closely held.

Leadership and Governance

CEO Young had led FPI for all of its 15-yearexistence to date, becoming a prominent figurein the process. During that period, he was namedFinancial Times’ 1994 CEO of the Year, inductedinto the Order of Canada in 1996 and, that sameyear, awarded an honorary doctorate by his almamater, Memorial University.

Young was very active in the businesscommunity, as a director of four other prominentCanadian corporations and a member of anumber of fishing industry associations andadvisory committees. He also regularly lent hissupport and stature to a variety of worthy causes.

As chairman, CEO and president, Young wasthe only member of management on FPI’s 12-member board of directors (see Exhibit 7). The11 other members were all unrelated, as definedby TSE guidelines. Seven members were fromthe province of Newfoundland and Labrador,three from Ontario and one from NewBrunswick. One position on the Board wasreserved for FFAW, a legacy of the agreementending the 1984 strike at FPI. In 1999, the boardof directors, as a group, owned less than one percent of FPI’s outstanding stock.

The chairperson of the board’s humanresources committee was designated the role ofdealing with matters of governance, includingoverseeing the relationship between the boardand senior management. It was not unusual forsenior management other than Young to attendboard meetings to present business information.However, at each meeting the board held somediscussions without the CEO or other manage-ment in attendance.

Finance

In the early 1990s, the company struggledwith severe industry supply shortages, andrecorded losses from 1991 through 1993 (see

Exhibit 3). Since then, with the exception of aloss in 1995, due to lower quotas and poor mar-ket conditions in the United States and Mexico,EPS had improved every year. In 1999, FPI paida dividend ($0.12 per share) on its common stockfor the first time in 11 years.

FPI practised conservative fiscal manage-ment, maintaining high liquidity and low debt,because “Fish and debt don’t mix,” as Young wasfond of saying. Like other local seafood compa-nies, FPI financed some independent harvestersthrough mortgages secured against their vessels;it had helped some inshore fishers convert theirboats to shrimp fishing in this way. Accountsreceivable credit risk was minimal as FPI’s 10largest customers made up less than 30 percentof sales and no single customer represented morethan six percent.

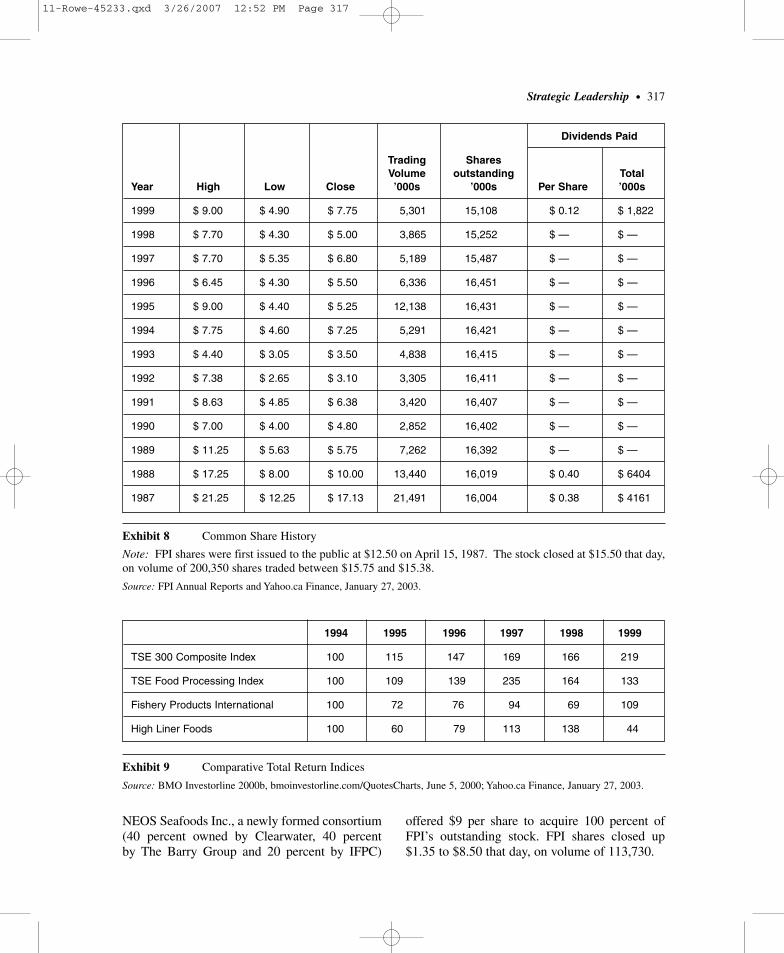

FPI stock traded on the TSE. Since 1987, itsshare price had declined to a range between $5 to$7 on comparatively low trading volume (seeExhibits 8 and 9). FPI had taken advantage ofthis situation to buy back one million commonshares at an average price of $6.75 during 1997,and continued to buy back shares in 1998(250,300) and 1999 (164,400). Nevertheless, a$100 investment in FPI’s IPO, including rein-vestment of all dividends, was worth only $59.50at the beginning of November 1999. The sameinvestment over that period in the TSE indexwould have been worth $192. However, if placedin High Liner Foods (the successor company to National Sea Products), $100 would havedeclined to less than $6!

During the summer of 1999, FPI initiated dis-cussions with the government of Newfoundlandand Labrador about dropping the 15 percentownership limit per shareholder on FPI stock,arguing that it restricted the company in its abil-ity to raise capital and enter into mergers orstrategic alliances. These discussions resulted inthe understanding that if FPI were to propose amajor initiative requiring large amounts ofcapital, the government would consider remov-ing the share ownership restriction, although theonus would be on FPI to convince shareholders,employees and the communities affected of thewisdom of doing so.

Strategic Leadership • 315

11-Rowe-45233.qxd 3/26/2007 12:52 PM Page 315

316 • CASES IN LEADERSHIP

Membersince

James C. Ballie 1992 Partner, Tory, Tory, DesLauriers and BinningtonToronto, Ontario

R. William Blake, PhD 1999 Dean, Faculty of Business Administration, Memorial University

Bruce C. Galloway 1999 Company DirectorOakville, Ontario

Janet C. Gardiner 1987 Treasurer, Chester Dawe, Ltd.St. John’s, Newfoundland and Labrador

Michael F. Harrington 1998 Senior Partner, Stewart McKelvey Stirling ScalesSt. John’s, Newfoundland and Labrador

Albert F. Hickman 1984 President, Hickman Motors Ltd.St. John’s, Newfoundland and Labrador

Thomas E. Kierans 1990 Chairman & CEO, Canadian Institute for Advanced ResearchToronto, Ontario

Rev. Desmond T. McGrath 1987 Education Officer, Fish, Food and Allied Workers,St. John’s, Newfoundland and Labrador

Frances M. Nichols, FCA 1991 Chartered AccountantGrand Falls-Windsor, Newfoundland and Labrador