100 · Key Issues and Best Practices GDPR for North American Insurers Digital FNOL: Key Issues and...

28

2018 INSURER IT BUDGETS AND PROJECTS 2019 INSURANCE TECHNOLOGY CASE STUDY COMPENDIUM 2018 BUSINESS AND TECH TRENDS IN INSURANCE 100 DATA, DIGITAL, AND CORE CAPABILITIES FOR INSURERS INSURETECH FOR INSURERS: 150 STARTUP PROFILES PROPERTY/CASUALTY & LIFE/HEALTH/ANNUITY POLICY ADMINISTRATION SYSTEMS VENDORS INSURANCE TECHNOLOGY CASE STUDY COMPENDIUM 2018 INSURETECH FOR INSURERS: 150 STARTUP PROFILES PROPERTY/CASUALTY & LIFE/HEALTH/ANNUITY POLICY ADMINISTRATION SYSTEMS VENDORS 2018

Transcript of 100 · Key Issues and Best Practices GDPR for North American Insurers Digital FNOL: Key Issues and...

2018

INSURER IT BUDGETS AND PROJECTS 2019

INSURANCE TECHNOLOGY

CASE STUDY COMPENDIUM 2018

BUSINESS AND TECH TRENDS IN INSURANCE

100DATA, DIGITAL, AND CORE CAPABILITIES

FOR INSURERS

INSURETECH FOR INSURERS:

150 STARTUP PROFILES

PROPERTY/CASUALTY & LIFE/HEALTH/ANNUITY

POLICY ADMINISTRATION SYSTEMS VENDORS

INSURANCE TECHNOLOGY

CASE STUDY COMPENDIUM 2018

INSURETECH FOR INSURERS:

150 STARTUP PROFILES

PROPERTY/CASUALTY & LIFE/HEALTH/ANNUITY

POLICY ADMINISTRATION SYSTEMS VENDORS

2018

2 Novarica Research Annual | 2018

Contents

Council Studies & SurveysEmerging Technology in Insurance: AI, Big Data, Chatbots, IoT, RPA, and More

IT Value Metrics: Six Common Measurements of Business Impact

Cloud Adoption in Insurance: Trends and Issues

Insurance IT Practices and Disciplines

2018 Council Meeting Report

Insurance Technology Case Study Compendium 2018

Novarica New Normal 100: Digital, Data, and Core Capabilities for Property/Casualty Insurers

Novarica New Normal 100: Digital, Data, and Core Capabilities for Life/Annuity Insurers

Policy Administration System Project Metrics

Unstructured Claims data Usage in Insurance

Insurer IT Budgets and Projects 2019

Digital Benchmarks for Insurers Across the Enterprise

3

Welcome to the Novarica Research Annual! This issue provides a summary of recently published reports, including studies of insurers’ technology experiences, capabilities, and plans from our Research Council; business and technology trends; CIO best practices; vendor information in our Novarica Market Navigators; and recent webinars and presentations. All of the research summarized here is available for download by our advisory clients at novarica.com. Research reports can also be purchased individually.

If you’d like to learn more or arrange a conversation to discuss any of these topics with our senior team, please contact us at [email protected] or 833-668-2742.

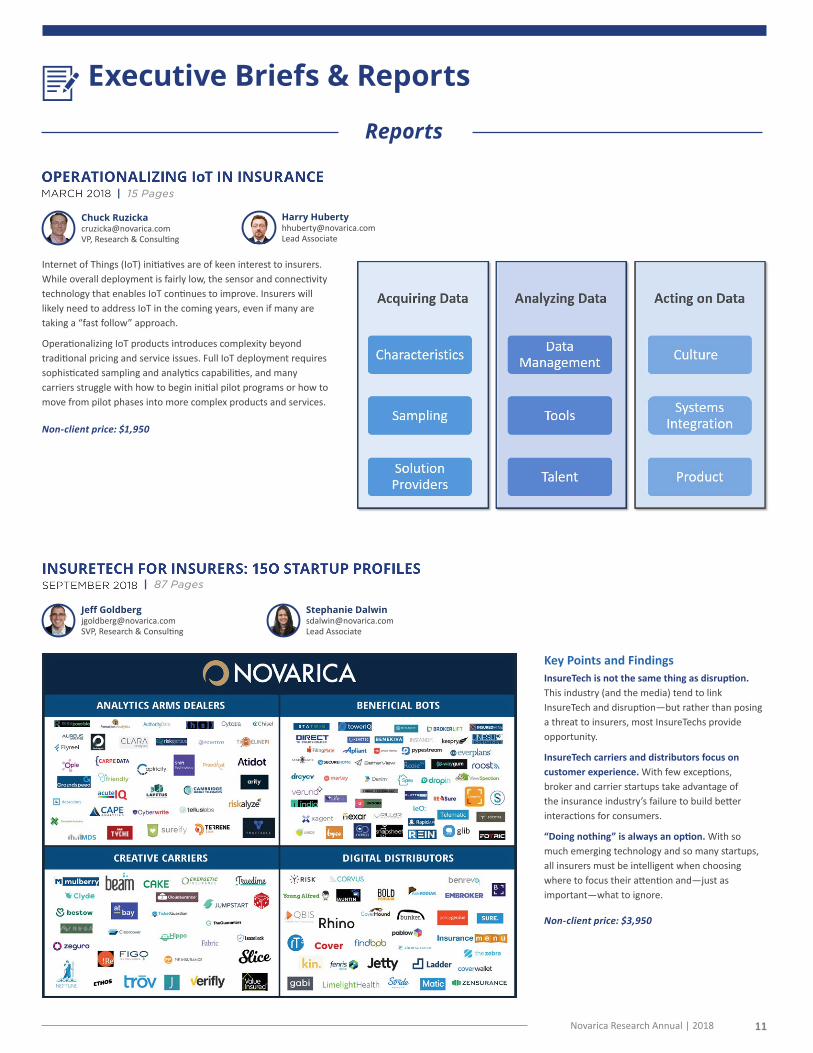

Executive Briefs & ReportsReportsOperationalizing IoT in Insurance

InsureTech for Insurers: 150 Startup Profiles

External Data in Insurance: Overview and Prominent Providers

Executive BriefsNovarica IT Financial Management Maturity Model

Quantum Computing and Insurance: Overview and Potential Players

Broker/Carrier Technology Trends and Challenges

Life Insurance Contact Centers: Key Issues and Trends

Enabling Innovation, Vol. 3: More Lessons from Silicon Valley

Purpose-Built AI Solutions for Insurers

Agile Adoption in Insurance: Approaches and Trends

Life Core Systems Conversion: Key Issues and Best Practices

Beyond UBI: Auto Telematics in Insurance

Insurance Digital Strategy: Key Issues and Best Practices

11

3Novarica Research Annual | 2018

Business & Tech Trends

Reinsurance

Group Life/Annuity/Voluntary Benefits

Large Commercial Brokers

Individual Life Insurance

Specialty Lines

Individual Annuity

Commercial Lines

Defined Contribution Retirement Plans

Personal Lines

Workers’ Compensation

18

CIO Checklists Best Practices for Evaluating SaaS Core Solutions

Core Systems Project Readiness

Maximizing the Value of Offshore Resources

17

Executive Briefs & Reports (Cont.)Aerial Imagery in Insurance: Overview and Prominent Providers

ITFM Platforms at Insurers: Overview and Prominent Providers

Data Strategy for Insurers: Key Issues and Best Practices

GDPR for North American Insurers

Digital FNOL: Key Issues and Prominent Providers

Enabling Innovation, Vol. 4: More Lessons from Silicon Valley

Cloud Migration Strategy: Key Issues and Best Practices

DevOps in Insurance: Lessons from Early Adopters

Microservices Architecture: The Future of SOA?

Broker-Carrier Automation: Overview and Prominent Providers

DXP and aPaaS for Insurers: Overview and Prominent Providers

InsureTech Impact on Life/Annuity Product and Distribution Strategies

Life Insurance Claims Systems: Overview and Prominent Providers

14

Novarica Market Navigators IT Services Providers for Insurers

Property/Casualty Policy Administration Systems

Life/Health/Annuity Policy Administration Systems

Document ECM/CCM Systems

Predictive Analytics Solutions for Insurers

Property/Casualty Agent Portals

BPO-BPaaS Providers for L/A Insurers

BPO-BPaaS Providers for P/C Insurers

Reinsurance Management

Business Intelligence Solutions for Insurers

Property/Casualty Billing Systems

23

4 Novarica Research Annual | 2018

Council Studies & Surveys

AI, AR/VR, big data, blockchain, chatbots, drones, robotic process automation, sensors and telematics, smart home automation, and wearables are not yet widely deployed in the insurance industry, but many of these areas are showing positive results and are poised for growth. Mobile and predictive analytics, often still classed by insurers as emerging technology, are approaching ubiquity.

This report analyzes the results of a study of 116 insurer CIO members of the Novarica Insurance Technology Research Council.

Insurer IT leaders benefit from using simple, meaningful metrics to communicate the value of technology investments to their business peers who are focused on the speed and efficiency of key business processes. This report presents a proposed framework of 21 KPIs tied to IT capabilities and an analysis of more than 100 case studies on impactful IT projects to determine which KPIs are used most commonly.

Key Points and FindingsThe most pilot activity is in digital and analytics areas like AI, big data, sensors, drones, RPA, and chatbots. Insurers are looking to these technologies to improve risk selection, claims, service, and operating efficiency.

P/C insurers are more likely to focus on underwriting and claims, L/A insurers on marketing and service when leveraging emerging technologies.

Areas with low consumer adoption aren’t generating much interest from insurers yet. Augmented and virtual reality, blockchain, smart home automation, and wearables are still over the horizon for most insurers.

Key Points and Findings Keep it simple and meaningful. Good IT value metrics are easy to track and meaningful to business executives’ operational challenges.

Value metrics may not be fully under IT’s control. Unlike engineering metrics or performance metrics, value metrics depend on business units’ use of technology to achieve a result. But value is measured in results, not capabilities, and IT leaders should operate accordingly.

Feel the need for speed. Five of the six most common KPIs have to do with accelerating cycle times, especially in the face of changing customer and distributor expectations and a highly competitive market.

Topics• Current deployment rates and planned pilot activity for 2018.

• Functional areas in which these technologies have been deployed.

• Return on investment for insurers who have already deployed these technologies.

Matthew [email protected]/CEO

Matthew [email protected]/CEO

| 23 Pages

| 9 Pages

Eric [email protected], Research & Consulting

Non-client price: $1,950

Non-client price: $1,950

Topics• The importance of value metrics.

• Proposed framework of 21 KPIs that are easy to track and understand.

• Six most commonly used KPIs with example case studies of successful insurer IT initiatives that used these KPIs to demonstrate value.

5Novarica Research Annual | 2018

Novarica estimates that use of cloud has more than tripled in the last few years, with most insurers incorporating it into their technology architectures. Insurers are realizing significant benefits in speed, flexibility, and capacity compared to traditional infrastructures. Security, long seen as a disadvantage of cloud usage, is now understood as an advantage, while cost benefits are more elusive than some anticipated.

This report presents data from a recent study of 89 insurer CIO members of the Novarica Insurance Technology Research Council.

This study defines cloud as Infrastructure as a Service (IaaS) or Platform as a Service (PaaS), not Software

as a Service.

Demand for IT capabilities continues to grow and diversify, while IT budgets remain relatively constant. In response, CIOs are working to shift dollars from running the business to growth and transformation initiatives by driving multi-faceted and multi-year IT practice process improvement programs. This report covers the adoption rate and degree of planned expansion of both well-known and newly emerging IT practices. The challenges encountered and lessons learned are also discussed.

Key Points and Findings Cloud computing is mainstream. More than 70% of insurers use some cloud, and those that do are planning to use more. About 10% of insurers run most of their infrastructure on cloud.

The conventional wisdom on security and cost has flipped. Security is now widely viewed as a benefit, while realizing cost advantages is understood to require careful management.

No magic bullets. As with any new beneficial technology, getting the most out of cloud requires careful planning, management, and upskilling.

Key Points and FindingsTalent and IT operations remain the two most pressing concerns for CIOs. Finding and retaining the right resources to manage legacy environments is top of mind.

Agile development practices have continued to expand and are now the top priority. Carriers have widely adopted Agile to ensure quick, responsive delivery of internal projects.

Enterprise architecture and UX initiatives are also expanding. Carriers are addressing the challenges of integrating new core systems or new technologies into their technical environments, as well as meeting internal and external expectations for usability.

No IT practice improvement efforts saw a decrease in activity. Carriers’ efforts held steady (when they weren’t expanding), indicating that activity from 2017 and earlier remains ongoing. Integrating IT practices isn’t an overnight process.

Topics• Agile Development

• QA/Testing

• Master Data Management/Data Stewardship

• Enterprise Architecture

• IT Governance

• User Experience (UX) or Human Factors Engineering

• Bimodal IT or FAST/CORE IT

Keith [email protected], Research & Consulting

Matthew [email protected]/CEO

Matthew [email protected]/CEO

Chuck [email protected], Research & Consulting

| 14 Pages

| 14 Pages

Non-client price: $750

Non-client price: $1,950

Topics• Current and planned adoption, including application areas and examples of

recent initiatives.

• Security, including shifting perception of security from a disadvantage to an advantage.

• Advice from CIOs, including the impact on architectures, team skills, and managing costs.

6 Novarica Research Annual | 2018

Matthew [email protected]/CEO

| 25 Pages

Non-client price: $1,950

The Novarica Insurance Technology Research Council is a knowledge-sharing community of more than 300 CIOs and insurer IT leaders with a mission to strengthen the industry’s ability to leverage technology effectively. The 11th annual Council Meeting brought together more than 80 members for a series of presentations, panels, workshops, and direct networking in support of this mission. This report contains a summary of each of the formal sessions and workshops.

Key Points and FindingsRealignment. The way that insurers deliver value to their customers and the way that IT leaders deliver value to their organizations are both being realigned due to changes in technology that enable speed and easier access to information and transactional capabilities.

Clarity. This world of rapid change requires clear understanding of and strategies in market, operating, technology, and talent management practices.

Community. No insurer CIO is an island. IT teams, business unit leaders, vendors, regulators, distribution partners, and other key stakeholders must be understood and respected in order for insurers to thrive.

Topics• Innovation and InsureTech. New entrants are more

of an educational opportunity than a threat to insurers.

• Data, Digital, and Core. Managing new capabilities and legacy systems.

• Communication and Alignment. Balancing Agile development and cloud deployment with legacy management practices.

7Novarica Research Annual | 2018

Matthew [email protected]/CEO

| 46 Pages

Non-client price: $2,950

Novarica’s seventh annual case study compendium includes more than 30 detailed examples of IT initiatives that delivered real business impact.

Each case details business goals, project sponsors, team structure, project timeline, tools and technology used, challenges faced, success factors, and business results delivered.

Novarica Impact Awards, voted on by more than 50 CIOs, recognized winners in four categories: digital, data/analytics, core, and IT practice or infrastructure.

Key Points and Findings Cloud, microservices, and AI are playing a bigger role in a wide variety of initiatives that are creating real, short-term business value in all four categories.

Core systems transformations may be challenging, complex, and in many cases lengthy projects, but they are leading to real advances in speed and efficiency and are supporting growth in measurable ways.

Innovation is being approached actively, with formal structures to drive programs and manage results.

2018 Winners • Allstate for use of drone imaging in claims (data and analytics)

• Ameritas for its cloud/API layer to enable external app (IT practice or infrastructure)

• AXIS Insurance for its enterprise transformation project (core)

• Chubb for its agent portal and STP capability built on microservices (digital)

• MetLife for its use of machine learning to optimize personal auto underwriting (data and analytics)

• Pekin Insurance for its enterprise transformation program (core)

• Penn Mutual for its digital life insurance experience (digital)

• XL Catlin for its digital innovation practice (IT practice or infrastructure)

DIGITAL CASES

Chubb

Penn Mutual

Acuity

American Equity

Cake

Erie Insurance

Everest Insurance

Jetty

Mitsui Sumitomo

NSM Insurance

ProSight

Saxon Motor & General

Unum

Zurich Accident and Health

DATA AND ANALYTICS CASES

Allstate

MetLife

Everest Insurance

ProSight

Tokio Marine HCC

CORE APPLICATIONS CASES

AXIS Insurance

Pekin

CM Vantage Specialty

Everest

Haven Life

Motorist

OneBeacon

Wayne Insurance

Westfield

Zurich Life

IT PRACTICE OR INFRASTRUCTURE CASES

Ameritas

XL Catlin

Allianz Life

Farm Bureau Financial

Northwestern Mutual

8 Novarica Research Annual | 2018

The Novarica New Normal 100 (3N100) is a list of 100 technology capabilities that represent the “new normal” for insurers, spanning product development, marketing, distribution, underwriting, customer engagement, billing, claims, and finance/operations functions. They are organized into digital, data, and core areas.

This report explains the 3N100 Framework and provides analysis of deployment and pilot data from a survey of 17 life/annuity insurers.

Matthew [email protected]/CEO

Key Points and FindingsDigital distribution capabilities are widespread, but maturity levels vary. Nearly all insurers have transactional agent portals, but only about a third consider their capabilities mature.

The analytics gap is closing but remains in claims. More than two-thirds of insurers use predictive analytics in underwriting. But only half as many midsize insurers use it in claims.

Midsize insurers are piloting today’s large company table stakes. The most commonly piloted capabilities for midsize insurers are in digital and predictive analytics, while large companies are exploring AI and other emerging technologies.

Topics• Using the Novarica New Normal 100 Framework to benchmark capabilities.

• Current deployment digital, data, and core capabilities.

• Emerging technologies and current and planned pilot activity. How fast will new capabilities become table stakes?

| 48 Pages

Non-client price: $1,950

The Novarica New Normal 100 (3N100) is a list of 100 technology capabilities that represent the “new normal” for insurers, spanning product development, marketing, distribution, underwriting, customer engagement, billing, claims, and finance/operations functions. They are organized into digital, data, and core areas.

This report explains the 3N100 Framework and provides analysis of deployment and pilot data from a survey of 41 property/casualty insurers.

Matthew [email protected]/CEO

Key Points and FindingsDigital distribution capabilities are widespread, but maturity levels vary. Nearly all insurers have transactional agent portals, but only about a third consider their capabilities mature.

The analytics gap is closing but remains in claims. More than two-thirds of insurers use predictive analytics in underwriting. But only half as many midsize insurers use it in claims.

Midsize insurers are piloting today’s large company table stakes. The most commonly piloted capabilities for midsize insurers are in digital and predictive analytics, while large companies are exploring AI and other emerging technologies.

Topics• Using the Novarica New Normal 100 Framework to benchmark capabilities.

• Current deployment digital, data, and core capabilities.

• Emerging technologies and current and planned pilot activity. How fast will new capabilities become table stakes?

| 48 Pages

Non-client price: $1,950

9Novarica Research Annual | 2018

Carriers retain vast amounts of unstructured claims data and create more each day. Technologies to unlock the value of this data are becoming a bigger part of insurers’ arsenals to address more effective claims management. While large carriers have led the way in unstructured claims data use, small and midsize carriers are catching up as the technology becomes more available.

This brief examines the uses and challenges of unstructured data in claims based on data from a recent study of 44 insurer CIO members of the Novarica Insurance Technology Research Council.

Key Points and FindingsUnstructured claims data usage is currently tactical. Insurers deploy it in areas like claims fraud and severity indication. Few deploy unstructured data for strategic needs like detecting underwriting weakness.

Most challenges to adoption of unstructured claims data are equal in weight. Challenges include funding, ROI, access to tools, data integrity, and business interest. Carriers do not find one challenge more daunting than the others.

Investment belts could be tightening, choking off opportunity. Hard ROI is of growing interest for funding—and is increasingly a requirement. This can stall efforts such as data mining.

Jim [email protected], Research & Consulting

Topics• Why PAS conversions? Novarica explores why P/C insurers are investing

in legacy system replacements.

• Project metrics. Metrics including cost, duration, and resourcing are broken down.

• Insurer considerations. Key priorities, success factors, and challenges are reviewed.

Key Points and FindingsSwitching to Agile methodology was both a major challenge and key success factor. Insurers that invested in Agile adoption attributed their successful PAS conversion to this transition.

Consolidation of multiple legacy systems was a common theme. Many multi-system conversions involved consolidating, centralizing, and streamlining various legacy systems.

Multi-system conversions did not necessarily take longer or cost more than single-system conversions. Several insurers implemented multi-system conversion projects with relatively short timelines and low cost.

Core conversions are shifting beyond the scope of policy administration systems. Insurers across the board are taking on multi-component core implementations with longer timelines and higher costs.

To help insurers benchmark their core system implementations, Novarica conducted an analysis of 35 case studies involving a policy administration system (PAS) implementation. This report highlights trends in this area and provides metrics around estimated project cost, duration, and resourcing.

| 12 Pages

Tiffany [email protected]

Martina [email protected], Research & Consulting

Non-client price: $1,950

| 10 Pages

Non-client price: $1,950

Topics• Current state, including adoption and challenges.

• Usage and insights derived among insurers.

• Benefits realized among insurers that leverage unstructured data for claims today.

10 Novarica Research Annual | 2018

This report provides benchmark data on deployment and pilot activity for digital capabilities that are commonly considered to be part of a comprehensive digital strategy. The capabilities included in this study span marketing, distribution, underwriting, customer engagement, billing, and claims. It also provides benchmark data on digital investments and summary case studies of successful initiatives.

Key Points and FindingsDigital distribution capabilities are widespread, but maturity levels vary. Nearly all insurers have transactional agent portals, but only about a third consider their capabilities mature.

Insurers are piloting customer engagement, claims, and billing capabilities at high rates. Large insurers are also exploring IoT data capture and other emerging technologies.

Proliferation of channels creates additional complexity. As insurers consider expanding from Web and mobile to new channels like voice, additional complexities in content management and cross-channel consistency of experience will arise.

Matthew [email protected]/CEO

Total spending levels and patterns are roughly consistent with prior years as insurers attempt to squeeze new digital, analytics, and security initiatives into essentially static budgets. Overall budget trends and spending patterns continue to hold in aggregate, but there are significant variations between companies. Small shifts away from core systems spending toward digital, data, and security are starting to be visible.

This report analyzes the results of the 11th annual survey of insurer CIO members of the Novarica Insurance Technology Research Council.

Key Points and Findings Historical norms govern budgets, with total IT spending at 3.7% of premium. OpEx/CapEx splits and IT staff ratios are all similar to those in previous years. Run/Grow/Transform spending breakdowns remain at roughly 55/25/20.

Life insurers are focused on digital, property/casualty insurers on analytics and speed to market. Both sectors increasingly see talent and improving IT operations as key IT challenges.

Core systems replacement volume is starting to wane. Projects are still common, but new replacement projects are down slightly from previous years as prior investments start to come online.

| 16 Pages

Non-client price: $1,950

Topics• Current deployment rate of digital capabilities.

• Current and planned pilot activity to help insurers understand how soon emerging digital capabilities will become table stakes.

• Digital spending ratios in insurer IT budgets.

Matthew [email protected]/CEO

| 27 Pages

Non-client price: $1,950

Topics• Budgets, including growth rates and breakdowns by spend type

and focus area.

• Priorities and challenges facing insurer CIOs.

• Current capabilities and replacement/enhancement plans across the Novarica Insurance Core Systems Map.

11Novarica Research Annual | 2018

Executive Briefs & Reports

Internet of Things (IoT) initiatives are of keen interest to insurers. While overall deployment is fairly low, the sensor and connectivity technology that enables IoT continues to improve. Insurers will likely need to address IoT in the coming years, even if many are taking a “fast follow” approach.

Operationalizing IoT products introduces complexity beyond traditional pricing and service issues. Full IoT deployment requires sophisticated sampling and analytics capabilities, and many carriers struggle with how to begin initial pilot programs or how to move from pilot phases into more complex products and services.

Key Points and FindingsInsureTech is not the same thing as disruption. This industry (and the media) tend to link InsureTech and disruption—but rather than posing a threat to insurers, most InsureTechs provide opportunity.

InsureTech carriers and distributors focus on customer experience. With few exceptions, broker and carrier startups take advantage of the insurance industry’s failure to build better interactions for consumers.

“Doing nothing” is always an option. With so much emerging technology and so many startups, all insurers must be intelligent when choosing where to focus their attention and—just as important—what to ignore.

| 87 Pages

Reports

| 15 Pages

Chuck [email protected], Research & Consulting

Harry [email protected] Associate

Non-client price: $1,950

Stephanie [email protected] Associate

Jeff [email protected], Research & Consulting

Non-client price: $3,950

12 Novarica Research Annual | 2018

Executive Briefs

IT is the largest single expense area for insurers besides claims and commissions. Given its intangible nature, it’s also the area whose value is questioned most often. IT financial management (ITFM) is the practice of managing, optimizing, and demonstrating the value of these costs. In many insurance organizations, the practice of ITFM is immature, which leads to internal management conflict and lack of agreement about IT value.

In this report, Novarica introduces a new framework, the Novarica IT Financial Management Maturity Model. This four-stage, seven-dimension model enables an organization to determine both its current and desired levels of maturity as it considers the evolution of its ITFM capabilities.

IT financial management is neither free nor easy. It requires dedicated resources, coordination across the enterprise, leadership, and commitment. But it also has the potential to lower costs, improve ROI, and demonstrate IT value.

Insurers are increasingly interested in leveraging third-party data for analytics augmentation, for predictive modeling, and for the validation/cleansing of existing data.

This report reviews multiple insurance industry use cases for third-party data and examples of insurers that are investing in this area. It also includes profiles of 29 data providers used by insurers.

Key Points and FindingsDigital distribution capabilities are widespread, but maturity levels vary. Nearly all insurers have transactional agent portals, but only about a third consider their capabilities mature.

Insurers are piloting customer engagement, claims, and billing capabilities at high rates. Large insurers are also exploring IoT data capture and other emerging technologies.

Proliferation of channels creates additional complexity. As insurers consider expanding from Web and mobile to new channels like voice, additional complexities in content management and cross-channel consistency of experience will arise.

While artificial intelligence is poised to have significant impact on the insurance industry, the technology is still limited by barriers imposed by classic binary computing. Quantum computing addresses these concerns but will also have a profound effect on the fundamentals underlying data usage and protection, risk modeling, and the nature of insurance core systems.

This report provides an overview of the definitions of quantum, potential areas of impact, and current players in the space. It begins with a comparative overview of classical binary and quantum qubit computing, moves on to address several potential areas of impact for insurers, and then culminates in a discussion of potential players actively developing solutions in the space.

Though not yet an immediate issue, insurers should begin incorporating the technology into five-year outlook plans. Given the increasing research and discovery in this field, insurers should understand how it will affect the way they do business.

At present, several large technology providers—among them Google, IBM, Microsoft, and Intel—and targeted startups are vying to be the first organization with a quantum computer that can achieve quantum supremacy: the point at which conventional supercomputers become obsolete against this new technology. And this point is drawing near.

Steven [email protected], Research

Jeff [email protected], Research & Consulting

| 33 Pages

Eric [email protected], Research & Consulting

Non-client price: $1,950

| 11 Pages

Eric [email protected], Research & Consulting

Non-client price: $750

| 7 Pages

Mitch [email protected], Research & Consulting

Non-client price: $750

13Novarica Research Annual | 2018

Silicon Valley is often championed as the leader of technology innovation. While the Valley seems to hold the optimal blend of talent, capital, and ideas, there is no single formula that produces innovation. As insurers are increasingly expected to bring innovation in-house, operationalizing innovation is becoming imperative. The insurance industry is ripe for the type of disruption that the Valley offers, and carriers can take away valuable lessons to prepare to lead their organizations into the future. This brief explores insights and best practices for insurers from Novarica’s Silicon Valley Innovation Tour in the third quarter of 2017.

Key Points and Findings R&D is often spelled M&A. Silicon Valley provides many opportunities for carriers to invest in and partner with startups producing innovative technologies.

Innovation starts at the top and trickles down. It’s not enough to confine innovation to a lab; successful innovation is driven by executive leadership and permeates enterprise-wide.

The talent landscape is shifting. Organizations throughout the Valley are looking for creative solutions to challenges in attracting and retaining talent, specifically women, in technology.

Insurance brokers and specialty/large commercial carriers are lagging behind other segments when it comes to automating communication. Email is still the dominant form of data exchange for new business and renewals, both because of the industry’s inability to standardize data models and business processes and a cultural belief that email is more personal. Looming cybersecurity issues further complicate automation efforts. Carrier CIOs are adopting new technologies in support of their digital strategies and operations, while broker CIOs tend to be more conservative in adopting new technologies.

Life insurers strive to achieve the same levels of customer satisfaction in their contact centers delivered by retailers and consumer finance, but they face numerous challenges that have hindered their progress over the years.

Some challenges can be overcome through transformation efforts including process redesign and systems integration. Other challenges should be solved by relying on new technologies reaching a level of maturity that supports deployment in production environments.

Understanding the issues, approaches, and technologies surrounding contact centers is a key step in enabling insurers to transform their current environments, achieving significant cost reductions and improving the customer experience.

| 9 Pages

Rob [email protected], Research & Consulting

Keith [email protected], Research & Consulting

Chuck [email protected], Research & Consulting

Non-client price: $750

| 8 Pages

Chuck [email protected], Research & Consulting

Non-client price: $750

| 7 Pages

Ken [email protected], Research & Consulting

Non-client price: $750

14 Novarica Research Annual | 2018

Several insurers have undergone pilots with general-purpose AI providers that offer platforms for machine learning or NLP. These solutions are leveraged by early adopters looking at emerging technology transformation projects, with innovation budgets dedicated to hiring experts and training AI systems against insurance data sets.

Despite the strategic potential, insurers are finding general solutions require an insurmountable investment of time, resources, and capital. Instead, AI offerings tailor-made for the insurance industry are emerging as solutions to internal inefficiencies across the insurance value chain.

This brief explores the potential value of purpose-built AI solutions, the difference between purpose-built AI and general-purpose AI, and some notable solution providers in the space.

Non-client price: $750

Telematics is growing, but overall participation remains modest: about a third of P/C carriers have telematics capabilities live or in pilot, and about a third of their policyholders participate in those programs.

At the same time, vendors and carriers are beginning to move beyond traditional UBI programs to target services that are enabled or closely aligned with telematics, especially around claims. New apps have started to leverage smartphones for data capture, which give insurers and OEMs a convenient platform to bundle these offerings.

This report summarizes the state of automotive telematics for the auto insurance industry, including recent trends and directions for future development. It also surveys major players in the vendor landscape.

Jeff [email protected], Research & Consulting

Harry [email protected] Associate

| 12 Pages

Non-client price: $750

Digital disruptors are entering the insurance market with business strategies based on leading-edge technological capabilities. Their presence challenges existing carriers to meet new levels of service, customer and agent expectations, and to keep pace with an accelerating rate of digital change. To remain competitive, carriers must develop digital strategies to re-align their organizations, focus their IT investments, and guide them through the numerous decisions required across digitalization efforts. This paper explores best practices digital leaders leverage to effectively shape their digital strategies.

Chuck [email protected], Research & Consulting

| 8 Pages

Agile is now widely accepted across the insurance industry. However, adopting the Agile methodology takes time and commitment. The iterative development with fast failure and fast recovery can be attractive, but there are implications to the business and its operations.

In turn, carriers are at various levels of adoption and maturity; full adoption requires changes to traditional budgeting and planning as well as the mindsets of various stakeholders. This brief explores approaches to adopting Agile, considerations for senior leadership, and some of the potential benefits.

Deb Culliton [email protected] VP, Research & Consulting

| 7 Pages

Non-client price: $750

Understanding the factors that contribute to conversion project complexity and developing a strategy to address each of them is critical to success. It is equally important to develop an approach that addresses all product blocks, accounts for the time sensitivity of financial transactions, and sets guardrails for what is an acceptable balance between automation and manual processes. Using best practice approaches, increasing the involvement of knowledgeable resources, and developing a multi-run approval process, carriers increase their chances of a successful conversion.

Non-client price: $750

| 8 Pages

Ken [email protected], Research & Consulting

| 8 Pages

Jeff [email protected], Research & Consulting

Stephanie [email protected] Associate

Non-client price: $750

Insurers are using aerial imagery and drones for post-catastrophe damage assessment, property inspection, and underwriting. Technology providers offer a range of solutions, including hardware, drone operators, software and analytics, as well as support and training.

The advent of the IoT, big data, and artificial intelligence (including machine vision) has only increased the amount—and the accuracy—of data available from aerial imagery. This brief discusses current insurance use cases for drones, regulation impacting this technology, and over 15 drone solution providers.

| 8 Pages

Martina [email protected], Research & Consulting

Emily [email protected] Associate

Non-client price: $750

15Novarica Research Annual | 2018

Insurers recognize the benefits of cloud adoption—elasticity, increased stability, and rapid deployments. However, the transition to cloud also changes an organization’s daily business and impacts its finances, architecture, and staff.

Many insurers acknowledge that cloud migration is not immediate. Carriers will likely support a hybrid approach as they prepare their operations and business for a cloud-enabled future.

This brief explores approaches and best practices for insurers looking to migrate their infrastructure and applications to the cloud.

Non-client price: $750

IT financial management, or ITFM, is still an emerging capability at insurers. Most organizations do not have a formal process to track costs associated with IT systems and services; those who do often maintain a high-level record. Now, insurers’ IT organizations are turning their attention to dedicated ITFM platforms that provide cost details by IT service. In turn, the use of these platforms can help to communicate and demonstrate the value of IT applications.

This brief explores the drivers of ITFM platform adoption at insurers; their challenges; and key platform providers like Apptio, Nicus, and Oracle.

Eric [email protected], Research & Consulting

Jim [email protected], Research & Consulting

| 7 Pages

Non-client price: $750

The insurance industry has embraced data analytics to drive business results. Using large warehouses of internal data, augmentation from third-party providers, and big data sources, data analysts are driving product R&D and predictive modeling as well as influencing strategy at all levels of the organization. However, many insurers are dealing with the challenges of diverse core systems, little data integration, and limited agreement on what data assets mean. Instead of mining for insights, many insurers are still struggling with basic data quality and completeness issues. To resolve this, carriers need to develop a comprehensive data strategy which looks across the entire organization: at people, process, and technology.

Mitch [email protected], Research & Consulting

| 9 Pages

The European Union’s General Data Protection Regulation (GDPR) aims to allow individuals to exercise control over their data and stipulates rules for anonymizing and purging data upon request. Each EU member will create a national supervisory authority to enforce compliance.

The law also applies to US firms that do business in the EU—and possibly to US firms that do business with EU citizens in the US. (The latter is subject to legal disagreement and will need to be tested in court.) US carriers must be aware of GDPR provisions and may need to take steps to comply. Further, the California Consumer Privacy Act of 2018 resembles GDPR, though the former is less stringent in some key areas.

Mitch [email protected], Research & Consulting

| 11 Pages

Non-client price: $750

First Notice of Loss (FNOL) capabilities can be a key differentiator for P/C insurers, as initiating a claim represents the critical “moment of truth” at the crux of the insurer/policyholder relationship. To meet enhanced policyholder expectations for digital experiences, insurers are leveraging data from sources such as telematics, smartphones, wearable devices, IoT sensors, and GPS. Carriers can ensure a positive experience and gain internal efficiencies by enhancing the digital capabilities that underpin this interaction.

This brief focuses on the impact of digital in P/C FNOL and provides CIOs and their business.

Keith [email protected], Research & Consulting

Harry [email protected] Associate

| 9 Pages

Non-client price: $750

Novarica recently concluded its fourth semi-annual Silicon Valley Innovation Tour, which included the opportunity to lead a delegation of senior leaders through a series of on-site visits to luminary companies in the Bay Area. These visits provide an “immersion” experience into the inner workings of one of the world’s preeminent centers for innovation; they explore incubators, accelerators, venture capital firms, early stage startups, and mature companies that have managed to retain innovation as a central element of their corporate DNA.

This report captures key themes that emerged from our discussions during the visit in the third quarter of 2018.

Deb Culliton [email protected] VP, Research & Consulting

| 8 Pages

Rob [email protected], Research & Consulting

Non-client price: $750

Jeff [email protected], Research & Consulting

Emerson [email protected] Associate

| 8 Pages

Non-client price: $750

16 Novarica Research Annual | 2018

Insurance brokers and carriers in the specialty/large commercial space have been largely unable to standardize data models and business processes. They have, however, addressed new business and renewal application processes by point-to-point integrations or, more often, simply emailing forms back and forth. Recent investment in InsureTech has led to startups offering more automated solutions and leveraging AI, analytics, and cloud computing.

This brief provides an overview of two solution categories, digital broker platforms (DBPs) and automated application intake solutions (AAIs), along with profiles of vendors in both categories.

Digital engagement with distributors and customers remains high-priority for insurers. While most portals today are either custom builds or vendor applications, insurers are exploring new classes of solution provider to help them deploy digital capabilities. Some carriers are looking to cross-industry solutions; others are investigating novel offerings from traditional insurance systems vendors.

This brief provides an overview of two solution categories—digital experience platforms (DXPs) and application Platform-as-a-Service solutions (aPaaS)—as well as profiles of vendors in both categories.

DevOps is the practice of unifying software development and operations, with the goal of improved speed and efficiency in application delivery. After a breakout year in 2017, most carriers are now engaged in DevOps pilot and rollout activities. Recent Novarica research suggests that 91% of carriers have some form of initiative underway.

This brief is based on research conducted with the industry’s early adopters in mid-2018. Most have observed efficiency gains due to their DevOps rollout—one was confident that his group would see 25% improvement in development speed. In most cases, however, rollout was slower and more complex than expected, with many carriers encountering barriers related to technology, skill sets, governance, and culture. This Executive Brief provides an introduction to DevOps and explores adoption strategies, barriers encountered, and lessons learned.

| 12 Pages

Martin [email protected], Research & Consulting

Non-client price: $750

| 10 Pages

Chuck [email protected], Research & Consulting

Tom [email protected], Research & Consulting

Non-client price: $950

Life insurers are increasingly willing to experiment with digital distribution, driven in part by the example set by InsureTechs and their customer-centric approach to products, marketing, and distribution. Unafraid to fail and retry, InsureTechs are searching for ways to optimize the digital buying process for life insurance and expand the market.

With InsureTech business models providing insurers with fresh new perspective, insurers are taking steps to restructure their new business and underwriting capabilities. Many traditional life carriers are developing D2C products while others are providing their agents, wholesalers, and broker-dealers with more effective digital capabilities.

| 7 Pages

Deb Culliton [email protected] VP, Research & Consulting

Non-client price: $750

Life insurers are seeking improved claims capabilities to increase efficiency for cost reduction and customer experience, along with supporting new product features to meet the needs of policyholders and plan sponsors.

While policy administration system suites generally provide integral claims processing, carriers are looking to stand-alone solutions for better integration and increased capabilities.

This report discusses trends, carrier needs, and key providers of stand-alone life claims solutions like ClaimVantage, DXC, FAST, FINEOS, Intellect SEEC, and Pega.

| 9 Pages

Non-client price: $750

Tom [email protected], Research & Consulting

Microservices architecture has become mainstream over the last couple of years, and it seems set to play a pivotal role in the future of insurance technology. Carriers and vendors are actively engaged in new builds as well as attempting to rework their existing systems along microservices lines.

Some have called microservices architecture “SOA done right.” The reality, however, is more nuanced. It’s true that SOA failed to deliver in many areas, but it’s also clear that software development underwent some radical changes over the same period. In many ways, SOA feels distinctly legacy in today’s world of Agile development and cloud deployments.

This brief discusses what microservices architecture is, where it came from, and how it differs from traditional SOA. It also covers the benefits and drawbacks and explains how adopting it in isolation is a recipe for disappointment.

| 10 Pages

Martin [email protected], Research & Consulting

Non-client price: $750

Steven [email protected], Research

| 8 Pages

Chuck [email protected], Research & Consulting

Non-client price: $750

17Novarica Research Annual | 2018

9 Consider the location of the solution’s servers

9 Determine a preference for multi-tenant or single-tenant architecture

9 Confirm the time involved with establishing the account

9 Plan for solution updates and clarify an update release process

9 Confirm the vendor’s fee schedule

9 Understand the vendor’s disaster and business continuity plan

9 Confirm the vendor’s policies around data

9 Understand the benefits of a software code escrow

Novarica predicts that, by 2020, more than 50% of new insurance core system licenses will be a SaaS engagement. Advantages of this approach include a better ongoing maintenance and upgrade path, infrastructure and security ownership by dedicated experts, more flexible pricing models, and an architecture that supports modern best practices.

Not all vendors, however, mean the same thing when they talk about SaaS. Insurers must plan not only for evaluating the system and technology of a vendor, but also for hosting, maintaining, and licensing the service in the cloud.

Insurance core systems projects require careful planning and an enterprise-wide understanding of the changes required to be successful.

This brief presents a framework of key assets and steps required during the planning phase. It covers three critical areas: business readiness, IT/technical readiness, and program readiness.

Collaborating with partners to plan a project before it starts will improve insurers’ chances of both a successful implementation and realization of the many business benefits modern solutions deliver.

Offshore outsourcing can create tremendous value for insurers. Many carriers have created value by moving parts of their IT and operations offshore. However, outsourcing is not a once-and-done process. Ensuring that these investments generate continuous value takes focus. Without it, carriers lose productivity, costs go up, and turnover creeps higher. When this happens, insurers often react by pulling back on offshoring.

Offshoring requires strong teams and hands-on management on both sides of the equation. This CIO Checklist can help to run effective offshore operations. No matter what level of support vendors offer, insurer leaders are accountable for the organization. Period. This includes the people, the success, and the setbacks.

9 Write down the strategy and share it

9 Establish a single leadership thread

9 Develop the global talent team

9 Devote resources to training

9 Focus on change management

9 Measure (almost) everything

9 Move the right work at the right time

9 Go on-site, in both directions

9 Transition ownership and decision-making when possible

CIO Checklists

| 7 Pages

| 8 Pages

| 6 Pages

Jeff [email protected], Research & Consulting

Martina [email protected], Research & Consulting

Paul Vancheri [email protected] VP, Research & Consulting

Non-client price: $1,950 Non-client price: $1,950

Non-client price: $1,950

18 Novarica Research Annual | 2018

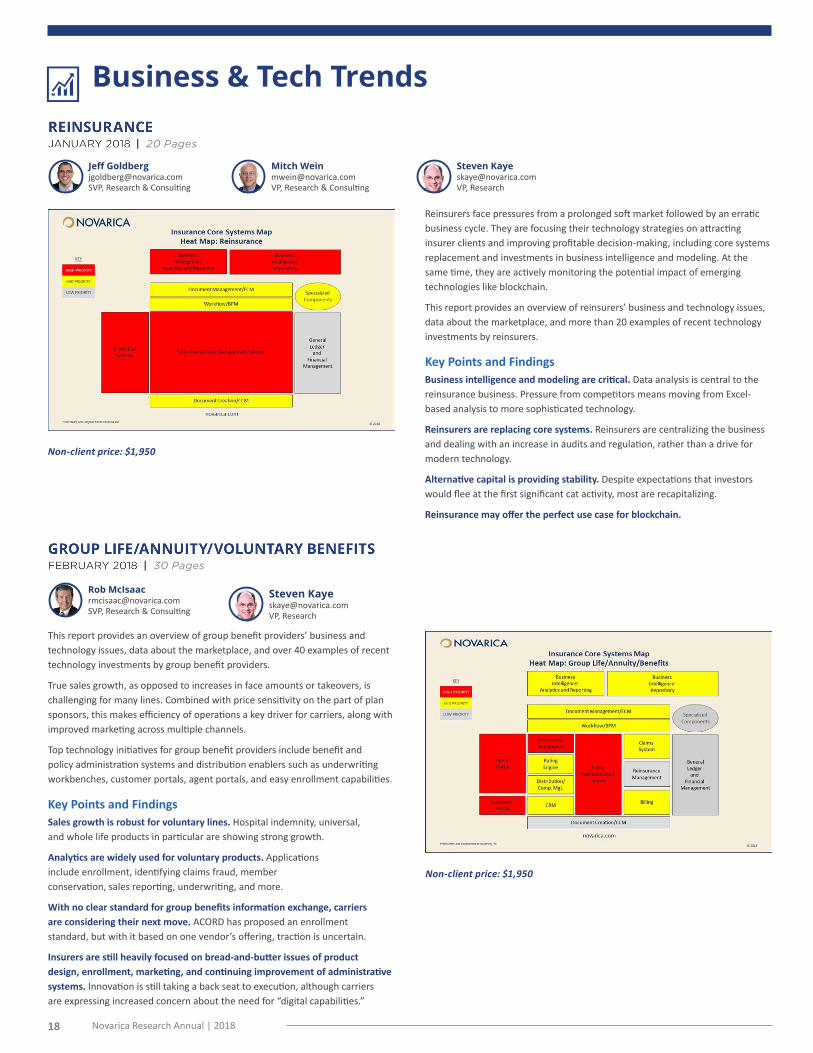

Reinsurers face pressures from a prolonged soft market followed by an erratic business cycle. They are focusing their technology strategies on attracting insurer clients and improving profitable decision-making, including core systems replacement and investments in business intelligence and modeling. At the same time, they are actively monitoring the potential impact of emerging technologies like blockchain.

This report provides an overview of reinsurers’ business and technology issues, data about the marketplace, and more than 20 examples of recent technology investments by reinsurers.

Key Points and Findings Business intelligence and modeling are critical. Data analysis is central to the reinsurance business. Pressure from competitors means moving from Excel-based analysis to more sophisticated technology.

Reinsurers are replacing core systems. Reinsurers are centralizing the business and dealing with an increase in audits and regulation, rather than a drive for modern technology.

Alternative capital is providing stability. Despite expectations that investors would flee at the first significant cat activity, most are recapitalizing.

Reinsurance may offer the perfect use case for blockchain.

This report provides an overview of group benefit providers’ business and technology issues, data about the marketplace, and over 40 examples of recent technology investments by group benefit providers.

True sales growth, as opposed to increases in face amounts or takeovers, is challenging for many lines. Combined with price sensitivity on the part of plan sponsors, this makes efficiency of operations a key driver for carriers, along with improved marketing across multiple channels.

Top technology initiatives for group benefit providers include benefit and policy administration systems and distribution enablers such as underwriting workbenches, customer portals, agent portals, and easy enrollment capabilities.

Key Points and FindingsSales growth is robust for voluntary lines. Hospital indemnity, universal, and whole life products in particular are showing strong growth.

Analytics are widely used for voluntary products. Applications include enrollment, identifying claims fraud, member conservation, sales reporting, underwriting, and more.

With no clear standard for group benefits information exchange, carriers are considering their next move. ACORD has proposed an enrollment standard, but with it based on one vendor’s offering, traction is uncertain.

Insurers are still heavily focused on bread-and-butter issues of product design, enrollment, marketing, and continuing improvement of administrative systems. Innovation is still taking a back seat to execution, although carriers are expressing increased concern about the need for “digital capabilities.”

Rob [email protected], Research & Consulting

Steven [email protected], Research

Jeff [email protected], Research & Consulting

| 30 Pages

| 20 Pages

Steven [email protected], Research

Mitch [email protected], Research & Consulting

Business & Tech Trends

Non-client price: $1,950

Non-client price: $1,950

19Novarica Research Annual | 2018

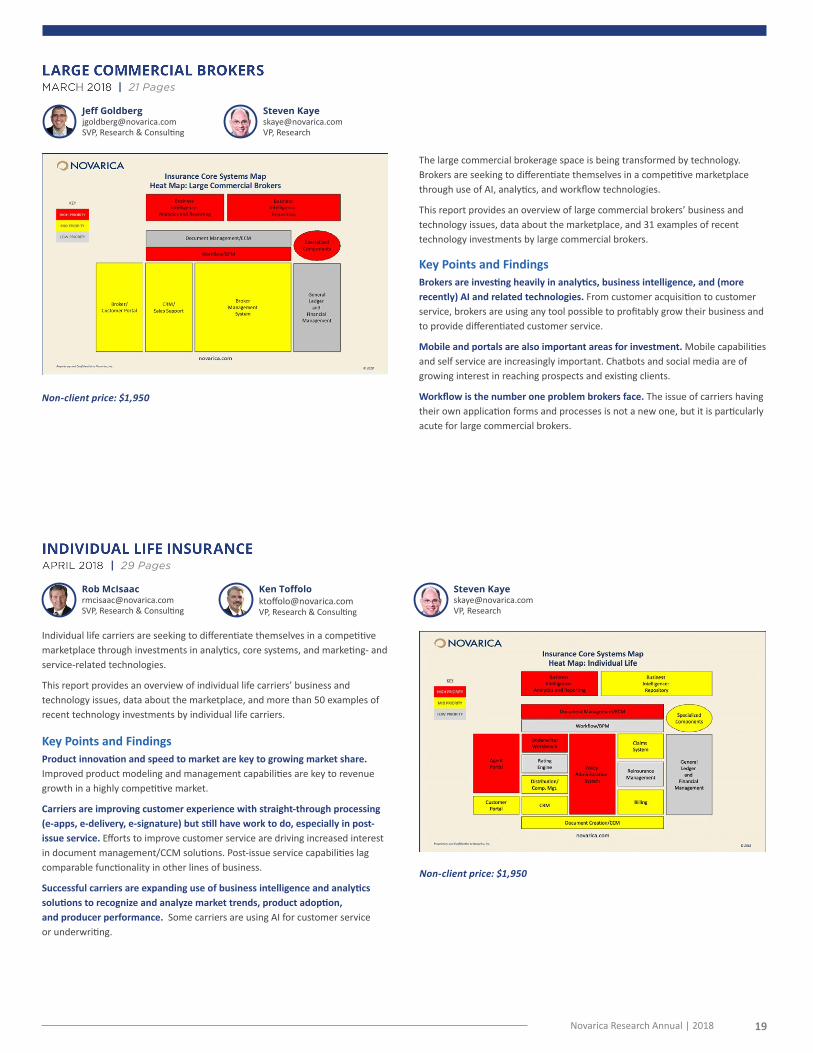

The large commercial brokerage space is being transformed by technology. Brokers are seeking to differentiate themselves in a competitive marketplace through use of AI, analytics, and workflow technologies.

This report provides an overview of large commercial brokers’ business and technology issues, data about the marketplace, and 31 examples of recent technology investments by large commercial brokers.

Key Points and FindingsBrokers are investing heavily in analytics, business intelligence, and (more recently) AI and related technologies. From customer acquisition to customer service, brokers are using any tool possible to profitably grow their business and to provide differentiated customer service.

Mobile and portals are also important areas for investment. Mobile capabilities and self service are increasingly important. Chatbots and social media are of growing interest in reaching prospects and existing clients.

Workflow is the number one problem brokers face. The issue of carriers having their own application forms and processes is not a new one, but it is particularly acute for large commercial brokers.

Jeff [email protected], Research & Consulting

| 21 Pages

| 29 Pages

Steven [email protected], Research

Steven [email protected], Research

Rob [email protected], Research & Consulting

Ken [email protected], Research & Consulting

Individual life carriers are seeking to differentiate themselves in a competitive marketplace through investments in analytics, core systems, and marketing- and service-related technologies.

This report provides an overview of individual life carriers’ business and technology issues, data about the marketplace, and more than 50 examples of recent technology investments by individual life carriers.

Key Points and Findings Product innovation and speed to market are key to growing market share. Improved product modeling and management capabilities are key to revenue growth in a highly competitive market.

Carriers are improving customer experience with straight-through processing (e-apps, e-delivery, e-signature) but still have work to do, especially in post-issue service. Efforts to improve customer service are driving increased interest in document management/CCM solutions. Post-issue service capabilities lag comparable functionality in other lines of business.

Successful carriers are expanding use of business intelligence and analytics solutions to recognize and analyze market trends, product adoption, and producer performance. Some carriers are using AI for customer service or underwriting.

Non-client price: $1,950

Non-client price: $1,950

20 Novarica Research Annual | 2018

| 27 Pages

Eric [email protected], Research & Consulting

Steven [email protected], Research

While specialty carriers have traditionally made less use of automation compared to other sectors, they are now seeking to differentiate themselves in a competitive marketplace through use of business intelligence, policy administration and rating, billing, and portals.

This report provides an overview of specialty carriers’ business and technology issues, data about the marketplace, and 57 examples of recent technology investments by specialty insurers.

Key Points and FindingsCarriers are pursuing long-term data strategies, starting with data quality initiatives and focusing on data warehouses, operational data stores, and appropriate data marts. Carriers are prioritizing reporting tools to allow the business to run ad hoc reports and obtain insights.

Improved underwriting and product development flexibility are key considerations. Carriers are continuing to upgrade to highly configurable policy administration systems to improve underwriting and enable product development flexibility to speed entry to profitable niches.

Billing efforts focus on handling both retail and wholesaler billing needs. Account billing is becoming a higher priority as part of a shift to a more customer-centric approach.

Specialty carriers are extending functionality to agents and policyholders.

New technologies such as IoT are already impacting specialty carriers.

| 29 Pages

Chris [email protected], Research & Consulting

Steven [email protected], Research

Key Points and FindingsSelf-service and transactional capabilities are required to manage expenses, but AI-related technologies are needed to build engagement and address projected increased producer workloads. With a push to lower fees, producers need to grow their client base to make up for lost income—but an increased compliance workload makes serving that base challenging.

Speed to market and product design are vital for sales growth. Business intelligence and core systems investments continue to be critical in improving time to market and product flexibility.

Carriers must be prepared for equity market shifts. Technology to support pricing, reserves, capital management, and statutory reserving are also key.

Regulatory changes will continue to impact the annuities market in the near term. While the DOL guidelines are all but gone, additional NAIC, SEC, and state regulations will replace them.

The individual annuity market faces declining volumes and rising competition from alternative wealth products. Carriers are looking to deepen existing distribution relationships, expand new channels, and improve transparency. Priorities include modernization of policy administration systems, as well as improvements to agent portals, business intelligence, and risk management.

This report provides an overview of individual annuity carriers’ business and technology issues, data about the marketplace, and more than 40 examples of recent technology investments by individual annuity insurers.

Non-client price: $1,950

Non-client price: $1,950

21Novarica Research Annual | 2018

Steven [email protected], Research

| 28 Pages

Martina [email protected], Research & Consulting

Commercial lines carriers are seeing some premium increases, are seeking growth through expanded jurisdictions and new products, and are adopting analytics more broadly. The commercial market is still fiercely competitive. Carriers are seeking to drive down the cost of service, refine pricing and underwriting, and pursue growth, especially in the small commercial space.

This report provides an overview of commercial lines carriers’ business and technology issues, data about the marketplace, and more than 40 examples of recent technology investments by commercial lines insurers.

Key Points and Findings Drones, IoT, robots, and autonomous vehicles are poised to transform the industry. These technologies are reducing the need for on-site adjusters and investigators while greatly improving underwriting and pricing, as well as lowering claims frequency.

Agent portals remain key to customer acquisition and retention, and direct sales capabilities will be increasingly important for more transactional products and program business. Agents and carriers should be spending their time solving client problems, not taking orders or pushing products.

Commercial lines carriers are increasingly adopting AI and analytics. Carriers are using AI and analytics in claims, customer services, and underwriting to better predict claims activity, improve customer satisfaction, and improve risk selection and pricing.

| 31 Pages

Steven [email protected], Research

Keith [email protected], Research & Consulting

In what remains a highly competitive business—where scale can have a significant impact on overall success—carriers are focused on driving down costs and attracting new clients, all while retaining existing clients and assets through improved insights and investment performance.

This report provides an overview of defined contribution retirement plan business and technology issues, data about the marketplace, and more than 35 examples of recent technology investments by defined contribution retirement plan insurers.

Key Points and FindingsPlan sponsors continue to be concerned about compliance. Lawsuits over excessive investment fees are growing, and ensuring employee financial wellness is of increasing concern to employers.

Automated advice continues to grow in the defined contribution space. Incumbents have scale and marketing, but new entrants are raising the bar for customer experience. Declining fees drive the need to serve a larger customer base more cost-effectively to remain profitable.

Portal initiatives and communications continue to be vital. A focus on participant financial wellness across the board requires effective communications as well as reporting and analytics.

Non-client price: $1,950

Non-client price: $1,950

22 Novarica Research Annual | 2018

Chuck [email protected], Research & Consulting

Steven [email protected], Research

| 31 Pages

The competitive pressures in personal lines have never been more intense. Traditional approaches to gain operational efficiency and to segment markets are no longer enough. Carriers are investing in InsureTechs to accelerate learning and diversify R&D efforts, using AI to speed the claims process, deepening their knowledge of the customer, reducing earnings volatility through analytics, and improving self-service capabilities. Core systems remain a high priority to establish a base for future capabilities.

This report provides an overview of business and technology issues, market trends, and more than 50 examples of recent technology investments.

Key Points and FindingsPersonal lines lead the way in industry experimentation with AI. A high transactional volume combined with relative simplicity makes personal lines a natural choice for AI usage, especially in claims.

Personal lines also lead in digitalization. Carriers are pushing the envelope in digital self service. Carriers are also designing products for digital processes and targeting digitally oriented consumers.

Insurers are preparing for a very different world. Carriers are hedging their bets against autonomous vehicles by providing a broader range of services to diversify income.

| 27 Pages

Steven [email protected], Research

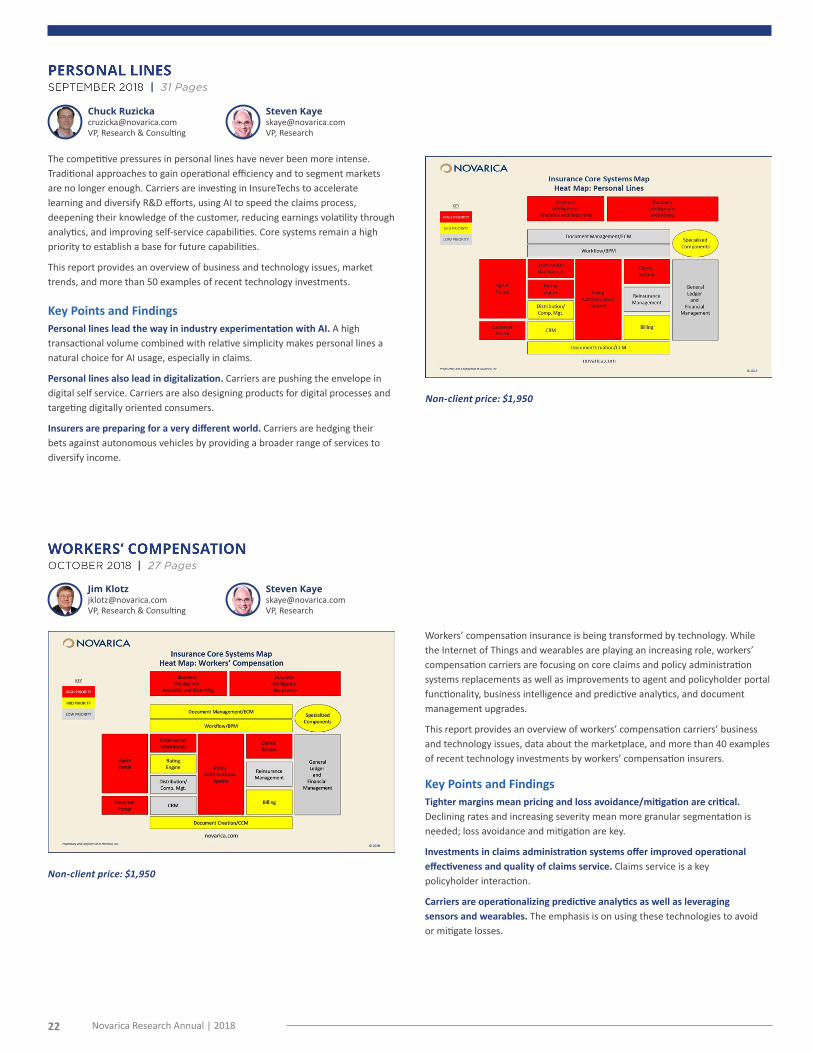

Key Points and FindingsTighter margins mean pricing and loss avoidance/mitigation are critical. Declining rates and increasing severity mean more granular segmentation is needed; loss avoidance and mitigation are key.

Investments in claims administration systems offer improved operational effectiveness and quality of claims service. Claims service is a key policyholder interaction.

Carriers are operationalizing predictive analytics as well as leveraging sensors and wearables. The emphasis is on using these technologies to avoid or mitigate losses.

Workers’ compensation insurance is being transformed by technology. While the Internet of Things and wearables are playing an increasing role, workers’ compensation carriers are focusing on core claims and policy administration systems replacements as well as improvements to agent and policyholder portal functionality, business intelligence and predictive analytics, and document management upgrades.

This report provides an overview of workers’ compensation carriers’ business and technology issues, data about the marketplace, and more than 40 examples of recent technology investments by workers’ compensation insurers.

Jim [email protected], Research & Consulting

Non-client price: $1,950

Non-client price: $1,950

23Novarica Research Annual | 2018

Novarica Market Navigators

This report provides an overview of 41 major IT services providers for North American insurers, with a focus on their experience levels in key functional areas. The report contains a brief profile of each vendor, including a chart detailing the provider’s experience levels in specific, targeted functions.

Providers include: Accenture, Birlasoft, Capgemini, The CastleBay Companies, CGI Group, Cognizant, Deloitte Consulting, DXC Technologies, Ebix Consulting, Edgewater Consulting, Equisoft, EY, Genpact, HCL Technologies, Hexaware Technologies, HITSS, HTC Global Services, IBM, Infosys Limited, Jarus Technologies, LTI, Majesco, MFXchange US, Mindtree, Mphasis, msg global solutions, NIIT Technologies, NTT Data, PwC, Red Hawk, Slalom, Synechron, Syntel, TCS, Trianz, UCT, ValueMomentum, Virtusa, Wipro Limited, Xceedance, and Zensar Technologies.

Tom [email protected], Research & Consulting

| 95 Pages

| 553 Pages

Keith [email protected], Research & Consulting

This report provides an overview of the available policy administration systems and suites for US P/C insurers. The report contains profiles of 42 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: 1insurer; Beyontec; BriteCore; CGI; CodeObjects; DAVID Corporation; Decision Research Corporation; Duck Creek Technologies; DXC; eBaoTech; Ebix; ECCA; Echo Ridge Partners; EIS Group; Finys; Focus on Innovation; Focus Technologies; Guidewire Software; Instec; Insurance Systems; Insuresoft; Insurity; JW Software; Majesco; MFX; Oceanwide; OneShield; Patriot Technology Solutions; PCIS; PCMS; Policy Administration Solutions; SAP SE; Sapiens; Solartis; Speedbuilder Systems; StoneRiver, a Sapiens Company; Sunlight Solutions; Tata Consultancy Services; and Tropics.

Martina [email protected], Research & Consulting

Jeff [email protected], Research & Consulting

Chuck [email protected], Research & Consulting

Non-client price: $2,950

Non-client price: $7,450

24 Novarica Research Annual | 2018

This report provides an overview of the available policy administration systems and suites for US property/casualty insurers. The report contains profiles of each of 42 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: 1insurer; Beyontec; BriteCore; CGI; CodeObjects; DAVID Corporation; Decision Research Corporation; Duck Creek Technologies; DXC; eBaoTech; Ebix; ECCA; Echo Ridge Partners; EIS Group; Finys; Focus on Innovation; Focus Technologies; Guidewire Software; Instec; Insurance Systems; Insuresoft; Insurity; JW Software; Majesco; MFX; Oceanwide; OneShield; Patriot Technology Solutions; PCIS; PCMS; Policy Administration Solutions; SAP SE; Sapiens; Solartis; Speedbuilder Systems; StoneRiver, a Sapiens Company; Sunlight Solutions; Tata Consultancy Services; and Tropics.

Chris [email protected], Research & Consulting

Rob [email protected], Research & Consulting

Tom [email protected], Research & Consulting

| 332 Pages

Chuck [email protected], Research & Consulting

Tom [email protected], Research & Consulting

| 146 Pages

This report provides an overview of the available stand-alone document management/enterprise content management (ECM) and document creation/customer communications management (CCM) systems currently available to US insurers. The report contains profiles of each of 20 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: CEDAR Document Technologies, Cincom Systems, Echo Ridge Partners, FIS, GhostDraft, Hyland, iPipeline, Messagepoint, Napersoft, OpenText, Optical Image Technology, Oracle, Pitney Bowes, Pyramid Solutions, Quadient, Smart Communications, Top Down Systems, Vertafore, and Xpertdoc Technologies.

Non-client price: $4,950

Non-client price: $2,950

25Novarica Research Annual | 2018

This report provides an overview of the available predictive analytics software solutions currently available to US insurers. The report contains profiles of each of 19 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: Angoss, Atidot, Carpe Data, Guidewire, Infogix, Infosys McCamish, Intellect SEEC, ISO, LexisNexis, LTI, MFX, Pegasystems, Saama Technologies, SAS, Valen Analytics, Willis Towers Watson, and Zensar Technologies.

This report provides an overview of the available agent portal systems and suites for US property/casualty insurers. The report contains profiles of each of 13 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: Appulate, Duck Creek, DXC, eBaoTech, Ebix, Guidewire, Majesco, NTT DATA, Outline Systems, Unqork, ValueMomentum, VUE, and Willis Towers Watson.

| 122 Pages

Jeff [email protected], Research & Consulting

Eric [email protected], Research & Consulting

Chuck [email protected], Research & Consulting

| 103 Pages

Chuck [email protected], Research & Consulting

Non-client price: $2,950

Non-client price: $2,950

26 Novarica Research Annual | 2018

This report provides an overview of 12 BPO-BPaaS providers to North American life/annuity insurers with a focus on their experience levels in key functional areas. The information in this report was collected directly from the providers using a proprietary Novarica RFI. The report contains a brief profile of each vendor, including a chart detailing the provider’s experience levels in specific, targeted functions.

Providers included: Capgemini, Cognizant, Concentrix, DXC, EXL, Genpact, Infosys BPM, NTT DATA, SE2, TCS, Wipro, and WNS.

This report provides an overview of 16 BPO-BPaaS providers to North American property/casualty insurers with a focus on their experience levels in key functional areas. The information in this report was collected directly from the providers using a proprietary Novarica RFI. The report contains a brief profile of each vendor, including a chart detailing the provider’s experience levels in specific, targeted functions.

Providers included: Blue Cod Technologies, Capgemini, CGI, Cognizant, Covenir, DXC, EXL, Genpact, Infosys BPM, Innovation Group, MFX, Seibels, Solartis, TCS, West Point Insurance, and WNS.

| 49 Pages | 53 Pages

Jim [email protected], Research & Consulting

Jim [email protected], Research & Consulting

Keith [email protected], Research & Consulting

Keith [email protected], Research & Consulting

| 93 Pages

Jeff [email protected], Research & Consulting

Eric [email protected], Research & Consulting

This report provides an overview of the available reinsurance management solutions currently available to US insurers. The report contains profiles of each of 15 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: AdvantageGo, DataCede, DXC, Effisoft, FIS, InsurIQ, NTT DATA, Policy Admin Solutions, Prevail, SAP, Sapiens, TAI Inc., and Tata Consultancy Services Ltd.

Non-client price: $2,950Non-client price: $2,950

Non-client price: $2,950

27Novarica Research Annual | 2018

| 102 Pages

Jeff [email protected], Research & Consulting

Eric [email protected], Research & Consulting

This report provides an overview of the business intelligence software solutions currently available to US insurers. The report contains profiles of 15 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: 4Sight Business Intelligence, AdvantageGo (NIIT Technologies), Cloverleaf, Duck Creek Technologies, Guidewire Software Inc., Infogix Inc., Information Builders Inc., Insight Decision Solutions, Insurity, Majesco, Policy Administration Solutions, SAP SE, Semantify, SpatialKey, and Zensar.

This report provides an overview of the available stand-alone billing systems for US property/casualty insurers. The report contains profiles of each of 15 vendor solutions, summarizing the vendor organization, technology used, differentiators, client base, lines of business supported, deployment options, implementation approaches, upgrades/enhancements, and key functionality.

Vendors included: Axiom, Billing Management Services, Decision Research Corporation, Duck Creek Technologies, DXC Technology, EIS Group, Guidewire, Input 1, Insuresoft, Majesco, OneShield, Policy Administration Solutions, Sapiens, SpeedBuilder Systems, and West Point Insurance Services.

| 118 Pages

Jim [email protected], Research & Consulting

Martina [email protected], Research & Consulting

Chuck [email protected], Research & Consulting

Martin [email protected], Research & Consulting

Non-client price: $2,950

Non-client price: $3,950

Novarica helps more than 100 insurers make better decisions about technology projects and strategy through research, advisory services, and consulting.

We serve clients in life/annuity/retirement, property/casualty, workers’ compensation, and reinsurance. Our clients range from Fortune 100 insurers to small regionals and specialty companies. Although most of our clients prefer us to keep their names confidential, a partial client roster includes Amica, AXA XL, GenRe, Penn Mutual, ProSight, SECURA, and SunLife.

Our senior team has direct experience as senior IT executives at firms including AIG, Arbella, AXA, Guardian, Liberty Mutual, MassMutual, Marsh, Progressive, Prudential, Voya, and others.

We publish frequent, independent, in-depth research on trends, best practices, and vendors. Our research projects are directed by our senior team and leverage the knowledge of more than 300 insurer CIO members of our Research Council. All reports are available to our clients without seat license restrictions.

Our Strategy-as-a-Service advisory services provide on-demand phone and email consultations on any topic in insurance or technology (as well as full access to our library). Our clients have told us it’s like having a team of experts down the hall—for a flat annual fee that is a small fraction of the cost of a single employee.

Our consulting services include vendor selection, benchmarking, project assurance, and IT strategy development. They are based on our deep knowledge base, extensive relationships, personal experience, and proven methodologies. Our clients get rapid, actionable insights and guidance delivered directly by our senior team.

© 2019, Novarica, Inc. All rights reserved.

linkedin.com/company/novarica

@novarica

novarica.com/podcast

280 Summer Street, 6th FloorBoston, MA [email protected]