10 years after: Implications of the current financial ... · of the current financial market...

28

10 years after: Implications of the current financial market turmoil 9th OECD-ADBI Roundtable on Capital Market Reform in Asia Tokyo, 26-27 February 2008 This report is solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organisation without prior written approval from McKinsey & Company. This material was used by McKinsey & Company during an oral presentation; it is not a complete record of the discussion.

-

Upload

truongkien -

Category

Documents

-

view

216 -

download

0

Transcript of 10 years after: Implications of the current financial ... · of the current financial market...

10 years after: Implications

of the current financial

market turmoil

9th OECD-ADBI Roundtable on Capital Market Reform

in Asia

Tokyo, 26-27 February 2008This report is solely for the use of client personnel. No part of it may be

circulated, quoted, or reproduced for distribution outside the client

organisation without prior written approval from McKinsey & Company.

This material was used by McKinsey & Company during an oral

presentation; it is not a complete record of the discussion.

1

AGENDA

• 10 years after: Positive diagnostic on Asia’s financial

markets health

• US subprime crisis: Visible but limited direct impact to date

• The next 10 years: Opportunities outweigh challenges

• The road ahead: Shift from hardware to software

2

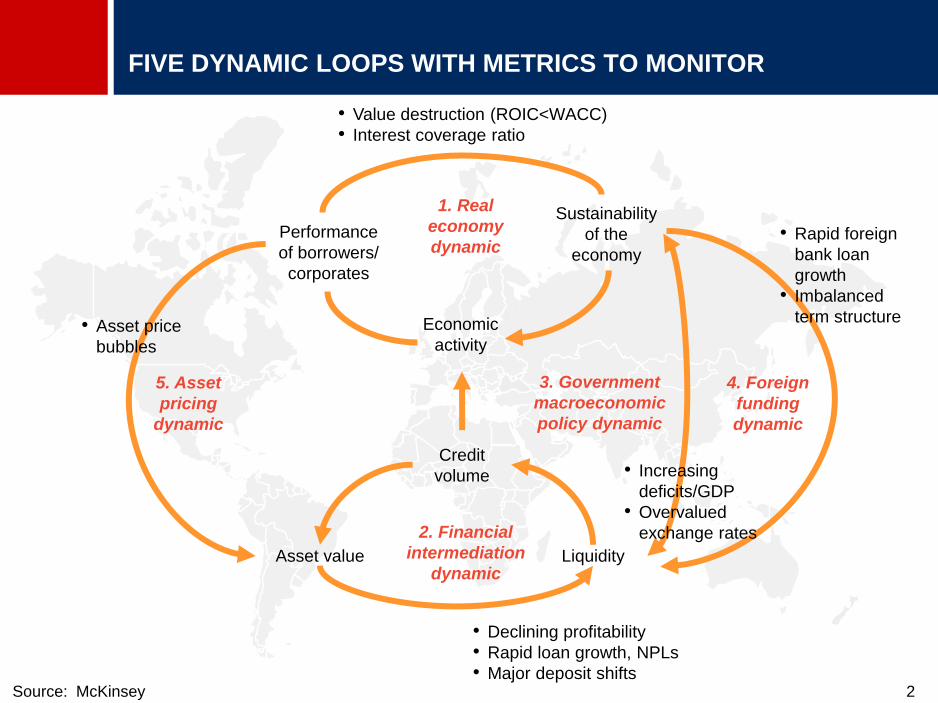

FIVE DYNAMIC LOOPS WITH METRICS TO MONITOR

Source: McKinsey

5. Asset

pricing

dynamic

4. Foreign

funding

dynamic

3. Government

macroeconomic

policy dynamic

2. Financial

intermediation

dynamicAsset value Liquidity

Credit

volume

1. Real

economy

dynamicPerformance

of borrowers/

corporates

Economic

activity

Sustainability

of the

economy

• Value destruction (ROIC<WACC)

• Interest coverage ratio

• Declining profitability

• Rapid loan growth, NPLs

• Major deposit shifts

• Rapid foreign

bank loan

growth

• Imbalanced

term structure

• Increasing

deficits/GDP

• Overvalued

exchange rates

• Asset price

bubbles

3

TWO MACRO FACTORS AND SEVEN MICRO FACTORS POINT TO

SIGNIFICANT IMPROVEMENTS

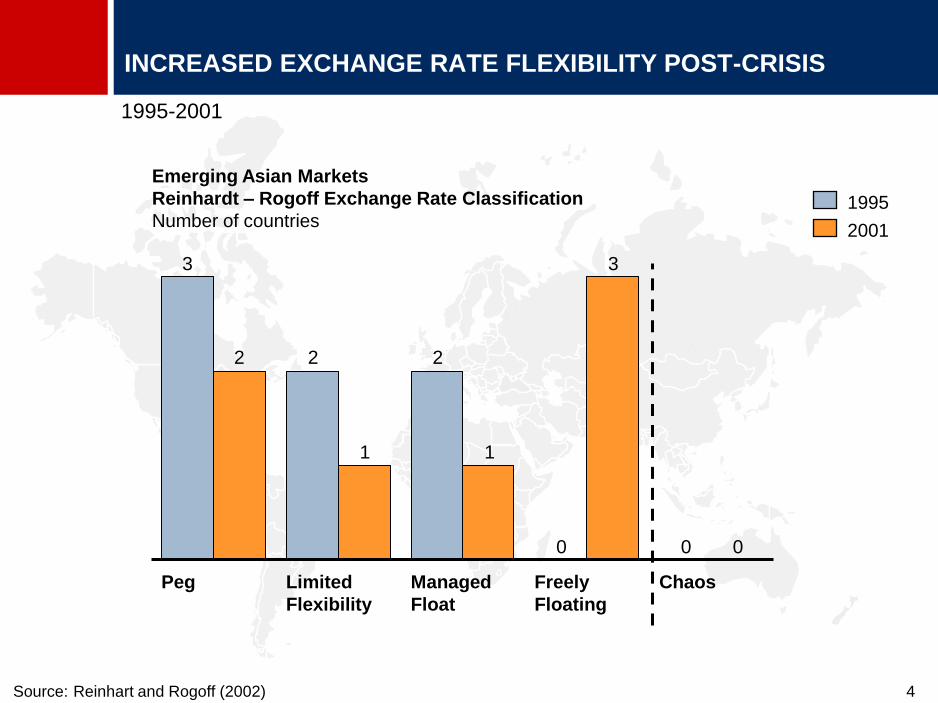

1. Foreign funding and exchange rates: Since

the late 1990s, most exchange rates in Asia

have moved from being fixed to flexible, and

even floating

2. Economic growth, government budget

deficits, inflation and unemployment: There

has been broad improvement in most

government macro indicators across Asia

2 macro factors: Clear improvements

1. Banking systems strength: Underlying strength

and capabilities of banks across Asia significantly

improved over last 10 years

2. Underlying credit and risk skills: Credit

capabilities improved, albeit from a relatively low

base

3. Strength and consistency of regulation and

supervisory approach: Efforts required but

supervisors’ capabilities substantially improved

4. Breadth and depth of financing options: Still

bank dominated but capital markets (particularly

equities) beginning to play a large role

5. Underlying infrastructure efficiency: Payments

systems (e.g., RTGS) improving; exchange

governance and operations overhauled

6. Corporate sector vitality: The majority of listed

Asian companies are now achieving ROIC greater

than their WACC

7. Asset bubbles: Strong contributors and triggers of

past crises (e.g., Thailand in 1997, Sweden in

1992), they remain a concern today

7 micro factors: Solid momentum

Source: McKinsey

4

INCREASED EXCHANGE RATE FLEXIBILITY POST-CRISIS

Source: Reinhart and Rogoff (2002)

00

22

3

0

3

11

2

Managed

Float

Limited

Flexibility

Peg ChaosFreely

Floating

Emerging Asian Markets

Reinhardt – Rogoff Exchange Rate Classification

Number of countries

1995-2001

1995

2001

5

420

774

854

951

1,0511,148

1,2501,354

1,458

284

331

330

320

298276

168355

2008E

1,687

1,105

4,238

2009E

1,812

1,189

4,527

2010E

242

1,921

1,2711,019

1,533

2007E

945

1,317

2006

3,126

3,543

1,066

2005

2,727

843 875

826121

2000

1,064

3,924

2011E

207

2,030

1,357

5,052

2012E

Other

Asia*

Other

major

Asia**

China

Japan

4,788

* Bangladesh, Cambodia, India, Indonesia, Lao PDR, Nepal, Pakistan, Philippines, Sri Lanka, Thailand, Vietnam.

** Hong Kong, Korea, Malaysia, Singapore, Taiwan.

Source: IMF; Ministry of Economic Affairs, Taiwan; Global Insight; UBS Asian Economic Monitor; MGI Cross-border

Holdings Database; McKinsey Global Institute analysis

53

21

32

50

20

41

618

Asian holdings of foreign reserve assets

$ billion

% of nominal GDP

2006 2012

ASIAN FOREIGN EXCHANGE RESERVES TO REACH $5.1

TRILLION

6

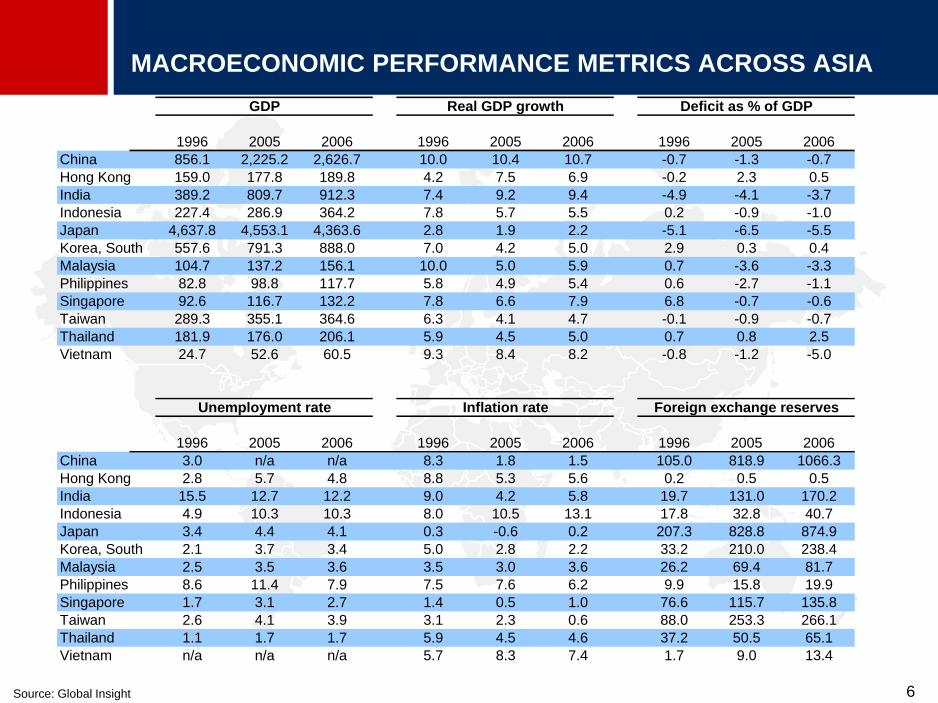

1996 2005 2006 1996 2005 2006 1996 2005 2006

China 856.1 2,225.2 2,626.7 10.0 10.4 10.7 -0.7 -1.3 -0.7

Hong Kong 159.0 177.8 189.8 4.2 7.5 6.9 -0.2 2.3 0.5

India 389.2 809.7 912.3 7.4 9.2 9.4 -4.9 -4.1 -3.7

Indonesia 227.4 286.9 364.2 7.8 5.7 5.5 0.2 -0.9 -1.0

Japan 4,637.8 4,553.1 4,363.6 2.8 1.9 2.2 -5.1 -6.5 -5.5

Korea, South 557.6 791.3 888.0 7.0 4.2 5.0 2.9 0.3 0.4

Malaysia 104.7 137.2 156.1 10.0 5.0 5.9 0.7 -3.6 -3.3

Philippines 82.8 98.8 117.7 5.8 4.9 5.4 0.6 -2.7 -1.1

Singapore 92.6 116.7 132.2 7.8 6.6 7.9 6.8 -0.7 -0.6

Taiwan 289.3 355.1 364.6 6.3 4.1 4.7 -0.1 -0.9 -0.7

Thailand 181.9 176.0 206.1 5.9 4.5 5.0 0.7 0.8 2.5

Vietnam 24.7 52.6 60.5 9.3 8.4 8.2 -0.8 -1.2 -5.0

1996 2005 2006 1996 2005 2006 1996 2005 2006

China 3.0 n/a n/a 8.3 1.8 1.5 105.0 818.9 1066.3

Hong Kong 2.8 5.7 4.8 8.8 5.3 5.6 0.2 0.5 0.5

India 15.5 12.7 12.2 9.0 4.2 5.8 19.7 131.0 170.2

Indonesia 4.9 10.3 10.3 8.0 10.5 13.1 17.8 32.8 40.7

Japan 3.4 4.4 4.1 0.3 -0.6 0.2 207.3 828.8 874.9

Korea, South 2.1 3.7 3.4 5.0 2.8 2.2 33.2 210.0 238.4

Malaysia 2.5 3.5 3.6 3.5 3.0 3.6 26.2 69.4 81.7

Philippines 8.6 11.4 7.9 7.5 7.6 6.2 9.9 15.8 19.9

Singapore 1.7 3.1 2.7 1.4 0.5 1.0 76.6 115.7 135.8

Taiwan 2.6 4.1 3.9 3.1 2.3 0.6 88.0 253.3 266.1

Thailand 1.1 1.7 1.7 5.9 4.5 4.6 37.2 50.5 65.1

Vietnam n/a n/a n/a 5.7 8.3 7.4 1.7 9.0 13.4

GDP Real GDP growth Deficit as % of GDP

Foreign exchange reservesInflation rateUnemployment rate

MACROECONOMIC PERFORMANCE METRICS ACROSS ASIA

Source: Global Insight

7

HIGH DEGREE OF DIRECT STATE INFLUENCE ON THE BANKING

SYSTEM

* Calculated by multiplying government’s equity share of SOE banks by assets under SOE banks

Source: Bankscope; annual reports; Central Banks; BI; team analysis

Banking assets under state-owned banks

Percent, 2005

Banking assets under direct government control*

Percent, 2005

0

0

8

20

22

25

31

47

49

62

Hong Kong

Czech Republic

Indonesia

Philippines

Poland

Taiwan

Thailand

Hungary

Malaysia

Korea

0

0

6

11

12

13

13

15

16

31

Hong Kong

Czech Republic

Malaysia

Thailand

Taiwan

Korea

Poland

Hungary

Indonesia

Philippines

• State-owned banks (i.e. banks in which the government

owns some % of equity) have a larger share of banking

assets in Malaysia and Taiwan, compared to Indonesia

• However, the government in Indonesia directly controls a

much higher share of banking assets

• This is because the Indonesian government owns a

relatively high % of equity in state-owned banks

Indicative sample of

Asian and Eastern

European countries

Indicative sample of

Asian and Eastern

European countries

8

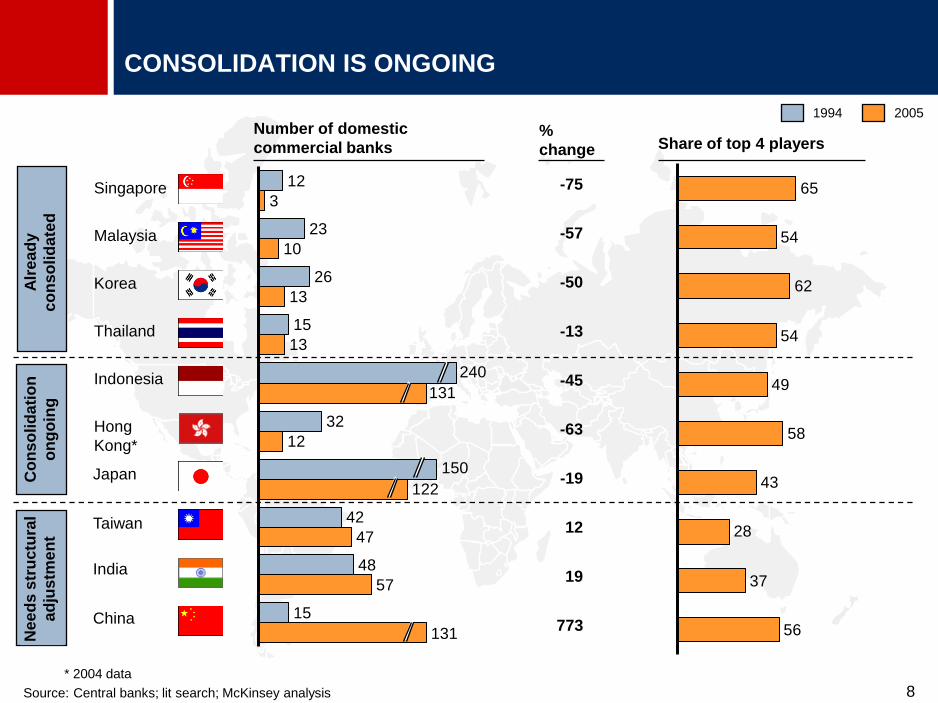

42

48

3

10

13

13

12

15

32

15

26

23

12

57

47

CONSOLIDATION IS ONGOING

Share of top 4 players%

change

Number of domestic

commercial banks

Alr

ea

dy

co

nso

lid

ate

d

Singapore

Korea

Thailand

* 2004 data

Source: Central banks; lit search; McKinsey analysis

Co

ns

olid

ati

on

on

go

ing

Indonesia

Malaysia

Hong

Kong*

China

Japan

Ne

ed

s s

tru

ctu

ral

ad

justm

en

t

India

-75

-57

-50

-13

-45

-63

-19

12

773

19

122

150

240

131

1994 2005

Taiwan

131

65

54

62

54

58

56

37

28

43

49

9

FINANCIAL SECTOR CONCENTRATION INCREASES FINANCIAL

SECTOR STABILITY

Source: Policy Research Working Paper #3041, World Bank, ―Bank concentration and crisis‖, Thorsten Beck, Aslh

Demirguc-Kunt, Ross Levine

Rationale for improved stability

A World Bank

report has found

empirical

evidence linking

concentration and

financial stability

Profit buffer• Concentrated banking systems enhance

profits and therefore lower bank fragility, which

provides a "buffer" against adverse shocks and

increase the franchise value of the bank,

reducing incentives for bank owners to take

excessive risk.

Better

supervision

• A few large banks are easier to monitor than

many small banks, so control of banks will be

more effective and the risks of contagion less

pronounced in a concentrated banking system

Diversification• There is some empirical evidence that large

banks can diversify better so banking systems

with a few large banks will be less fragile than

banking systems with many small banks

10Source: IMF; McKinsey analysis

CAPITAL MARKET DEPTH DECREASES THE

COST OF FINANCIAL CRISIS

0

5

10

15

20

25

30

35

40

0 50 100 150 200

South Korea 97–99

Thailand 97–00

Indonesia 98–00

Chile 82–85

Spain 77–85Mexico 95–97

Finland 90–93

Japan 98–03

US S&L 80–91Sweden 91–93

Brazil 95–96

Argentina 95–96Norway 88–92

Co

st

of

cri

sis

Depth of capital markets at time of crisis

(% of GDP)

Percent

of GDPArgentina 81–90

11

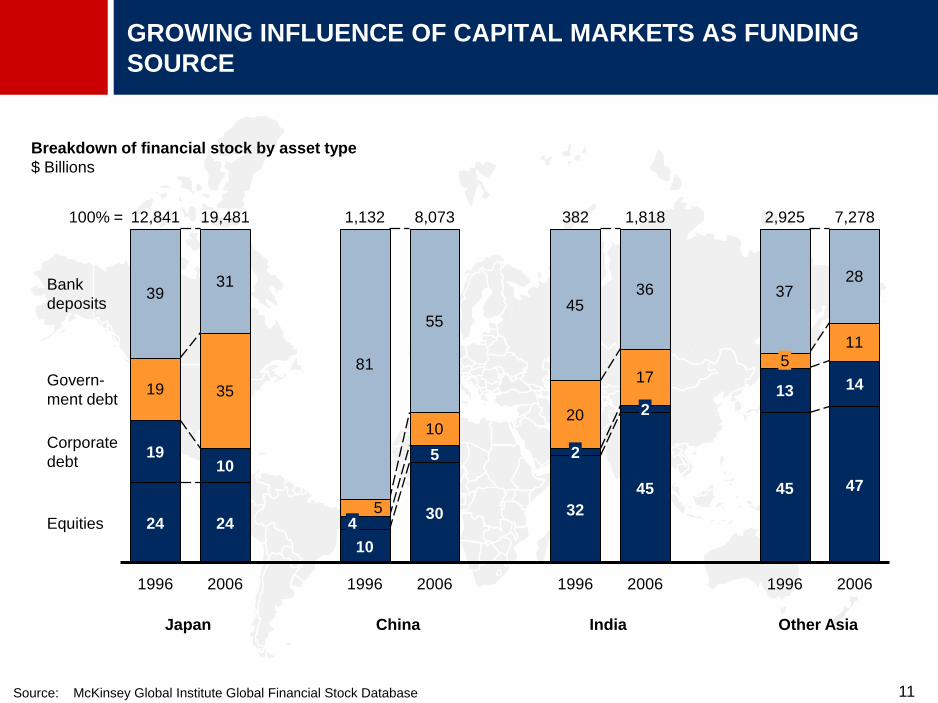

GROWING INFLUENCE OF CAPITAL MARKETS AS FUNDING

SOURCE

19 35

1020

17

11

3931

81

5545

36 3728

524

45

1,81812,841

1996 2006

10

24

19,481

2006

5

13

4

10

45

2,9251,132

1996 1996

5

30

8,073

2006

19 2

32

47

7,278382

1996

14

Bank

deposits

Govern-

ment debt

Corporate

debt

Equities

100% =

2

2006

Japan China India Other Asia

Breakdown of financial stock by asset type

$ Billions

Source: McKinsey Global Institute Global Financial Stock Database

12

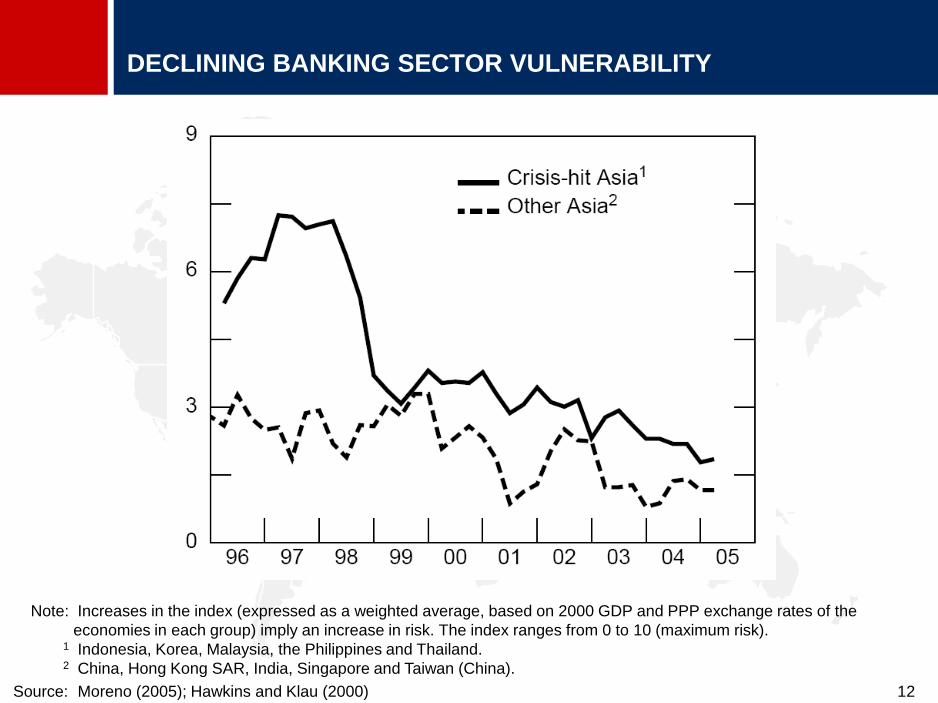

DECLINING BANKING SECTOR VULNERABILITY

Note: Increases in the index (expressed as a weighted average, based on 2000 GDP and PPP exchange rates of the

economies in each group) imply an increase in risk. The index ranges from 0 to 10 (maximum risk).1 Indonesia, Korea, Malaysia, the Philippines and Thailand. 2 China, Hong Kong SAR, India, Singapore and Taiwan (China).

Source: Moreno (2005); Hawkins and Klau (2000)

13

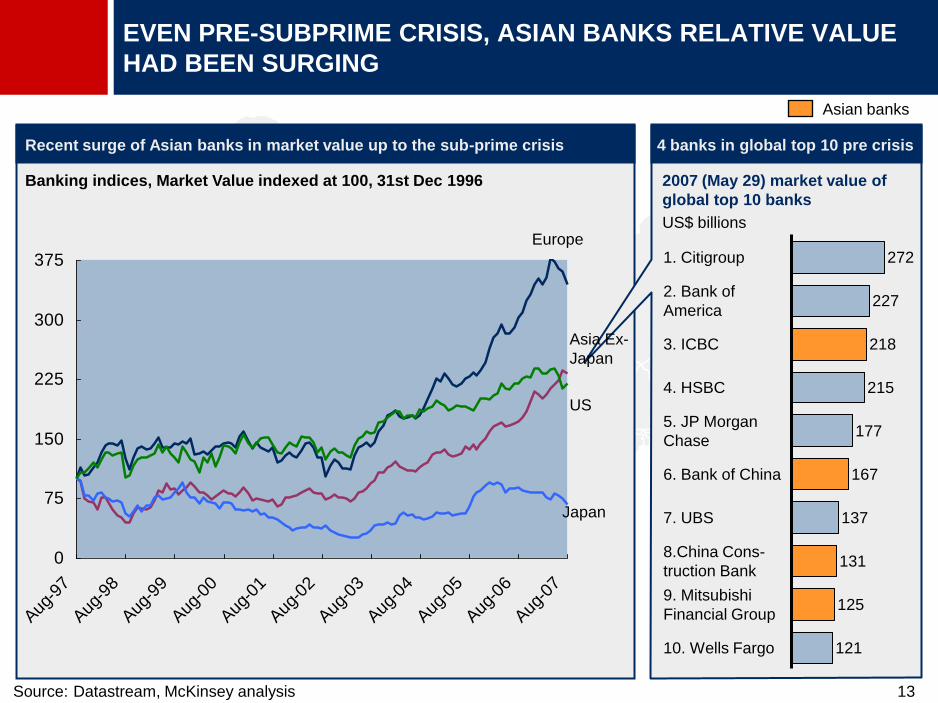

Banking indices, Market Value indexed at 100, 31st Dec 1996

Recent surge of Asian banks in market value up to the sub-prime crisis 4 banks in global top 10 pre crisis

EVEN PRE-SUBPRIME CRISIS, ASIAN BANKS RELATIVE VALUE

HAD BEEN SURGING

2007 (May 29) market value of

global top 10 banks

US$ billions

Asian banks

Source: Datastream, McKinsey analysis

0

75

150

225

300

375

Aug

-97

Aug

-98

Aug

-99

Aug

-00

Aug

-01

Aug

-02

Aug

-03

Aug

-04

Aug

-05

Aug

-06

Aug

-07

Asia Ex-

Japan

Japan

US

Europe 2721. Citigroup

2272. Bank of

America

2183. ICBC

2154. HSBC

1775. JP Morgan

Chase

1676. Bank of China

1377. UBS

1318.China Cons-

truction Bank

1259. Mitsubishi

Financial Group

12110. Wells Fargo

14

AGENDA

• 10 years after: Positive diagnostic on Asia’s financial

markets health

• US subprime crisis: Visible but limited direct impact to

date

• The next 10 years: Opportunities outweigh challenges

• The road ahead: Shift from hardware to software

15

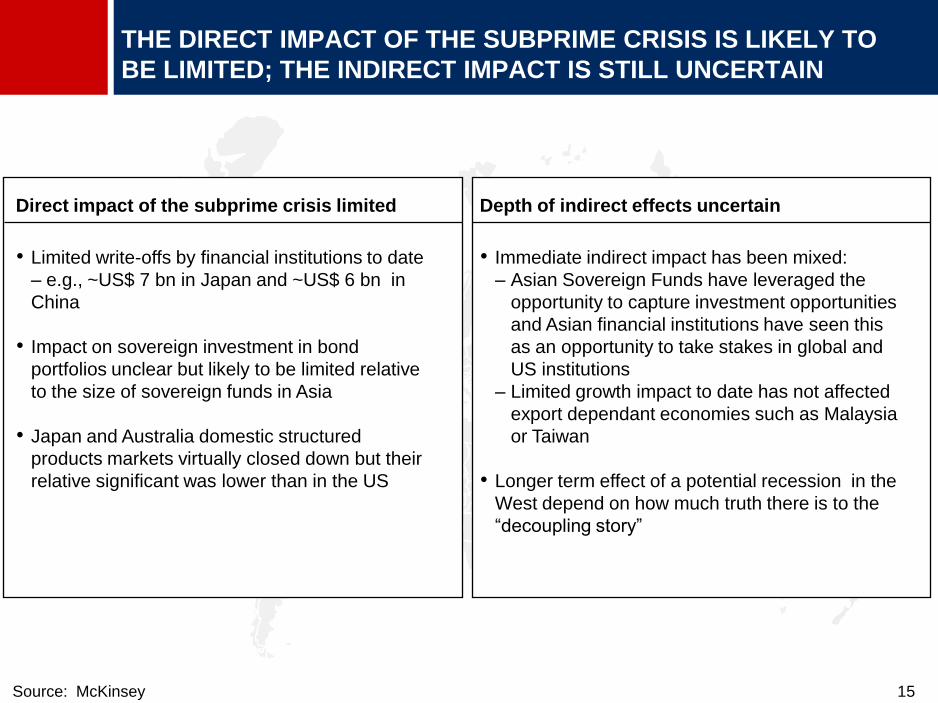

THE DIRECT IMPACT OF THE SUBPRIME CRISIS IS LIKELY TO

BE LIMITED; THE INDIRECT IMPACT IS STILL UNCERTAIN

Direct impact of the subprime crisis limited Depth of indirect effects uncertain

Source: McKinsey

• Limited write-offs by financial institutions to date

– e.g., ~US$ 7 bn in Japan and ~US$ 6 bn in

China

• Impact on sovereign investment in bond

portfolios unclear but likely to be limited relative

to the size of sovereign funds in Asia

• Japan and Australia domestic structured

products markets virtually closed down but their

relative significant was lower than in the US

• Immediate indirect impact has been mixed:

– Asian Sovereign Funds have leveraged the

opportunity to capture investment opportunities

and Asian financial institutions have seen this

as an opportunity to take stakes in global and

US institutions

– Limited growth impact to date has not affected

export dependant economies such as Malaysia

or Taiwan

• Longer term effect of a potential recession in the

West depend on how much truth there is to the

―decoupling story‖

16

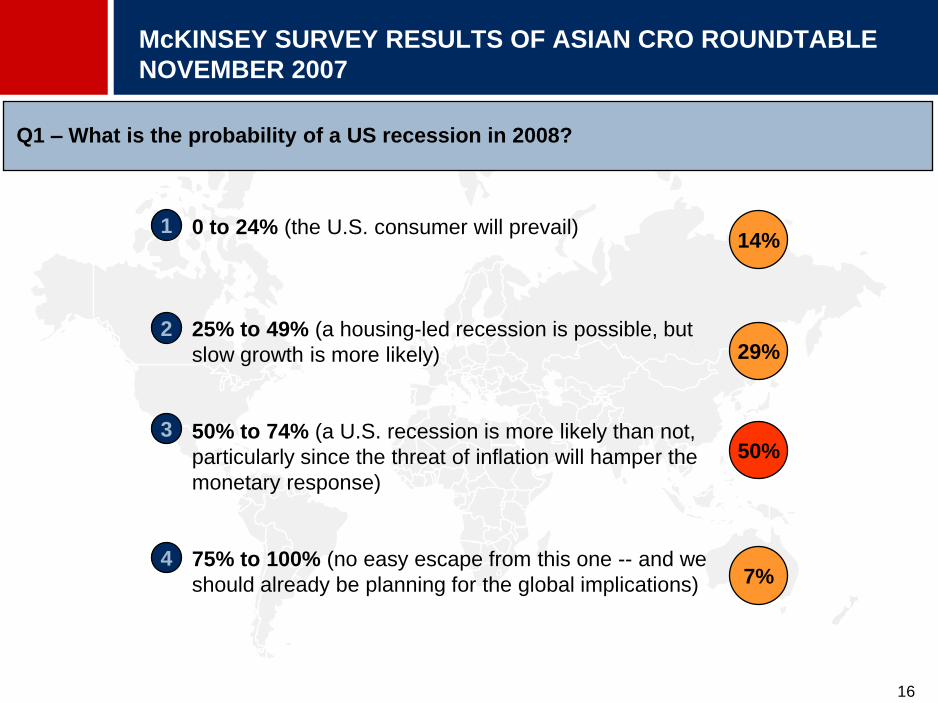

0 to 24% (the U.S. consumer will prevail)

25% to 49% (a housing-led recession is possible, but

slow growth is more likely)

50% to 74% (a U.S. recession is more likely than not,

particularly since the threat of inflation will hamper the

monetary response)

75% to 100% (no easy escape from this one -- and we

should already be planning for the global implications)

1

2

3

4

14%

29%

50%

7%

Q1 – What is the probability of a US recession in 2008?

McKINSEY SURVEY RESULTS OF ASIAN CRO ROUNDTABLE

NOVEMBER 2007

17

By January 2008, this will be behind us (we are 75% of

the way through this)

By mid 2008, credit and liquidity markets will return to

normal (e.g., with spreads returning to 2004 or 2005 levels)

Through late 2008 or early 2009 (we are only 25% through

this)

It will be years before markets fully return to the loose

credit conditions that prevailed over the past 5 years (in

particular, subprime lending, complex CDO structures and

business models heavily reliant on securitization will not

return for several years, if at all).

1

2

3

4

0%

36

%

36%

28%

Q2 – How much longer will the credit and liquidity events experienced since July

continue?

McKINSEY SURVEY RESULTS OF ASIAN CRO ROUNDTABLE

NOVEMBER 2007

18

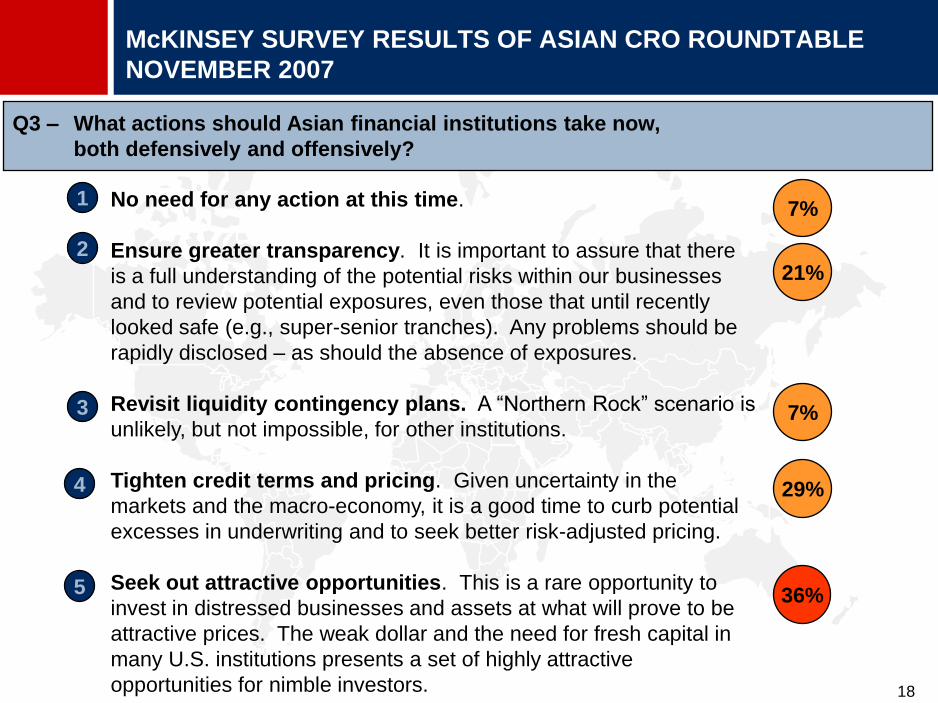

No need for any action at this time.

Ensure greater transparency. It is important to assure that there

is a full understanding of the potential risks within our businesses

and to review potential exposures, even those that until recently

looked safe (e.g., super-senior tranches). Any problems should be

rapidly disclosed – as should the absence of exposures.

Revisit liquidity contingency plans. A ―Northern Rock‖ scenario is

unlikely, but not impossible, for other institutions.

Tighten credit terms and pricing. Given uncertainty in the

markets and the macro-economy, it is a good time to curb potential

excesses in underwriting and to seek better risk-adjusted pricing.

Seek out attractive opportunities. This is a rare opportunity to

invest in distressed businesses and assets at what will prove to be

attractive prices. The weak dollar and the need for fresh capital in

many U.S. institutions presents a set of highly attractive

opportunities for nimble investors.

1

2

3

4

5

7%

21%

7%

29%

36%

Q3 – What actions should Asian financial institutions take now,

both defensively and offensively?

McKINSEY SURVEY RESULTS OF ASIAN CRO ROUNDTABLE

NOVEMBER 2007

19

AGENDA

• 10 years after: Positive diagnostic on Asia’s financial

markets health

• US subprime crisis: Visible but limited direct impact to date

• The next 10 years: Opportunities outweigh challenges

• The road ahead: Shift from hardware to software

20

OPPORTUNITIES AND CHALLENGES FOR THE NEXT 10 YEARS

1. India and China rise: By 2015, 800 million

people in China and India will join the middle

class

2. The return of Japan: Japan has been on the

sidelines for much of the past 16 years and is

emerging stronger from its long reform

3. Infrastructure spending: Annual infrastructure

spending from US$1.1 trillion today to US$2.1

trillion in 2010, increasingly from private sector

4. The rise of Asian champions: By 2010, Asia

could account for 30 percent of the top 1,000

from 18% in 2004

5. Intra-Asia trade: Trade among Asian countries

outgrowing that with the rest of the world with

China an increasingly important trading partner

6. Innovation: Asia becoming a major center of

innovation with need to serve large populations

with low-cost products a driving force

7. Asia’s growing financial power: Asia shifting

from investment destination to home of some of

the most powerful global markets investors

Opportunities

1. Ensure that compliance and risk-management

capabilities can keep up with extraordinary

growth, especially in China and India

2. Win “The War for Talent”: Most significant

constraint to sustained growth is insufficient

leadership and management talent

3. Build regulation, supervision capability: Rapid

changes in all aspects of the financial-services

industry; budgets inadequate in many cases

4. Improve information-sharing, regulatory

coordination: Limited availability, low consistency

(off-balance-sheet activities, int’l flows within Asia)

5. Asset bubbles: There are increasing concerns

about rapidly rising real-estate prices in several

Asian countries

6. Political disruptions or natural disasters:

Growing rich-poor divide fueling social and political

tensions; health care; natural resource constraints

7. Beware of arrogance: Arrogance or over-

confidence – behaviors directly linked to

extraordinary success – were evident in early 1997

Challenges

Source: McKinsey

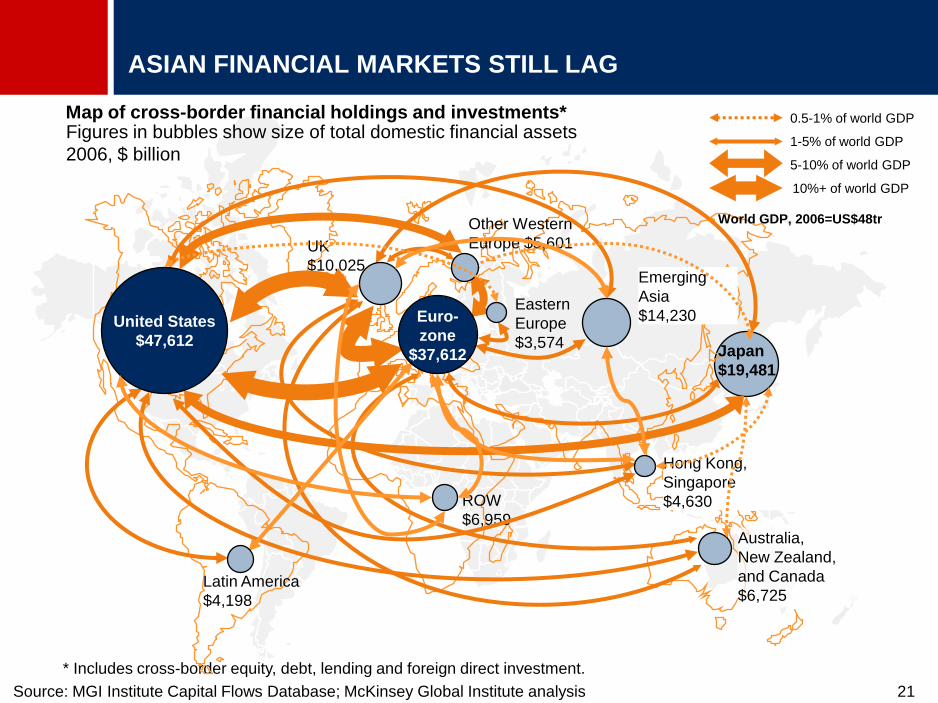

21

Map of cross-border financial holdings and investments*

* Includes cross-border equity, debt, lending and foreign direct investment.

Source: MGI Institute Capital Flows Database; McKinsey Global Institute analysis

Australia,

New Zealand,

and Canada

$6,725

Eastern

Europe

$3,574

ROW

$6,959

Latin America

$4,198

Other Western

Europe $5,601UK

$10,025

Hong Kong,

Singapore

$4,630

Emerging

Asia

$14,230

Japan

$19,481

Figures in bubbles show size of total domestic financial assets

2006, $ billion

0.5-1% of world GDP

1-5% of world GDP

5-10% of world GDP

10%+ of world GDP

ASIAN FINANCIAL MARKETS STILL LAG

World GDP, 2006=US$48tr

Euro-

zone

$37,612

United States

$47,612

22

* The figures reported for global capital inflows exceed outflows by $150 billion per year due to errors in reporting.

** Includes Russia

Source: McKinsey Global Institute Capital Flows Database

THE U.S., UK, AND EUROPE STILL ACCOUNT FOR 80% OF

CAPITAL FLOWS

Intra-Euro Area flows

Japan

Latin America

Rest of world

U.S.

India

4048

192 300

32 152

2223

82 154

China

106 103721 688

U.K.Eastern

Europe**

Average annual cross-border capital flows*, 2001-05

$ Billions

1,576 1,636

Euro Area

1,022

460

Inflows

Outflows

23

AGENDA

• 10 years after: Positive diagnostic on Asia’s financial

markets health

• US subprime crisis: Visible but limited direct impact to date

• The next 10 years: Opportunities outweigh challenges

• The road ahead: Shift from hardware to software

24

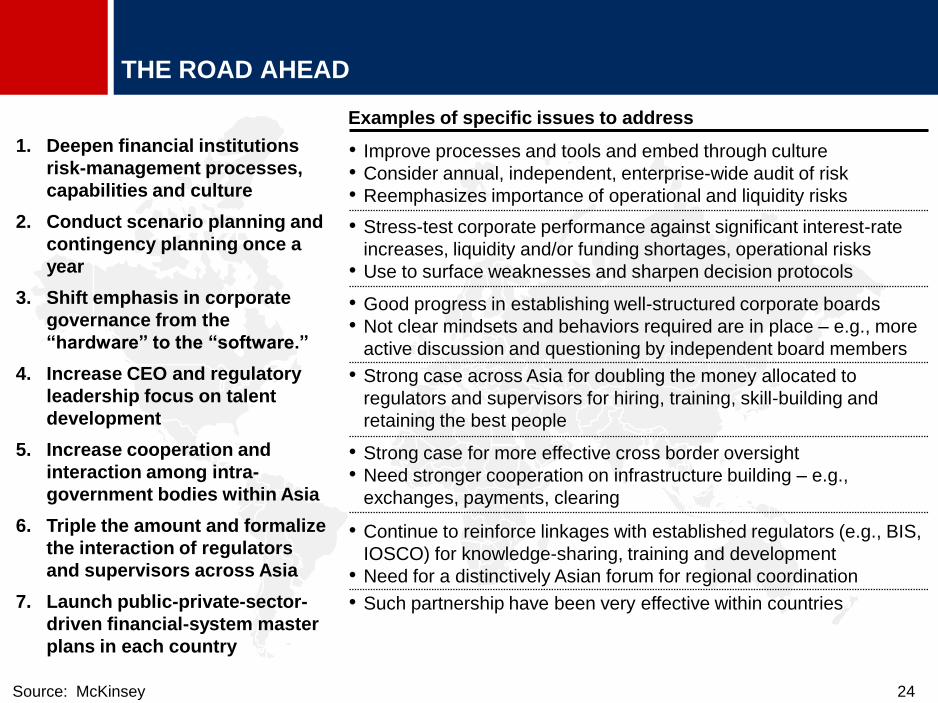

THE ROAD AHEAD

Source: McKinsey

1. Deepen financial institutions

risk-management processes,

capabilities and culture

2. Conduct scenario planning and

contingency planning once a

year

3. Shift emphasis in corporate

governance from the

“hardware” to the “software.”

4. Increase CEO and regulatory

leadership focus on talent

development

5. Increase cooperation and

interaction among intra-

government bodies within Asia

6. Triple the amount and formalize

the interaction of regulators

and supervisors across Asia

7. Launch public-private-sector-

driven financial-system master

plans in each country

• Improve processes and tools and embed through culture

• Consider annual, independent, enterprise-wide audit of risk

• Reemphasizes importance of operational and liquidity risks

Examples of specific issues to address

• Stress-test corporate performance against significant interest-rate

increases, liquidity and/or funding shortages, operational risks

• Use to surface weaknesses and sharpen decision protocols

• Good progress in establishing well-structured corporate boards

• Not clear mindsets and behaviors required are in place – e.g., more

active discussion and questioning by independent board members

• Strong case across Asia for doubling the money allocated to

regulators and supervisors for hiring, training, skill-building and

retaining the best people

• Strong case for more effective cross border oversight

• Need stronger cooperation on infrastructure building – e.g.,

exchanges, payments, clearing

• Continue to reinforce linkages with established regulators (e.g., BIS,

IOSCO) for knowledge-sharing, training and development

• Need for a distinctively Asian forum for regional coordination

• Such partnership have been very effective within countries

25

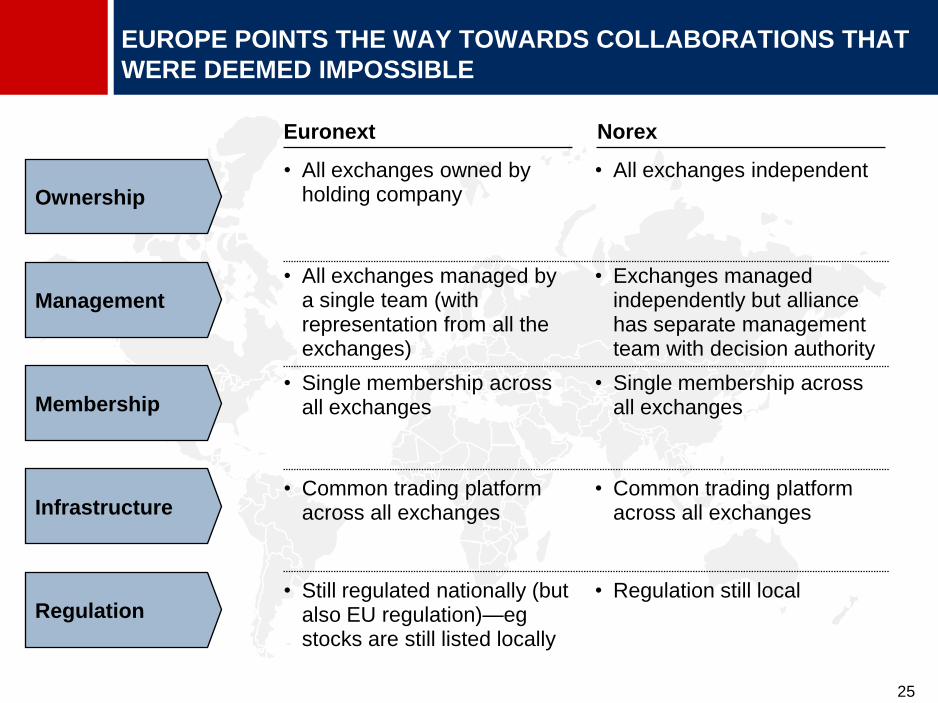

EUROPE POINTS THE WAY TOWARDS COLLABORATIONS THAT

WERE DEEMED IMPOSSIBLE

Euronext Norex

Ownership

Membership

Infrastructure

Regulation

Management

• All exchanges owned by holding company

• All exchanges managed by a single team (with representation from all the exchanges)

• Single membership across all exchanges

• Common trading platform across all exchanges

• Still regulated nationally (but also EU regulation)—eg stocks are still listed locally

• All exchanges independent

• Exchanges managed independently but alliance has separate management team with decision authority

• Single membership across all exchanges

• Common trading platform across all exchanges

• Regulation still local

26

IN CONCLUSION …

•10 years after: Positive diagnostic on

Asia’s financial markets health

•US subprime crisis: Visible but limited

direct impact to date

•The next 10 years: Opportunities

outweigh challenges

•The road ahead: Shift from hardware to

software

10 years after: Implications

of the current financial

market turmoil

9th OECD-ADBI Roundtable on Capital Market Reform

in Asia

Tokyo, 26-27 February 2008This report is solely for the use of client personnel. No part of it may be

circulated, quoted, or reproduced for distribution outside the client

organisation without prior written approval from McKinsey & Company.

This material was used by McKinsey & Company during an oral

presentation; it is not a complete record of the discussion.