1.0 Pharmaceutical Market

41

1.1 Pharmaceutical Sales

-

Upload

ilukicscribd -

Category

Documents

-

view

21 -

download

0

description

market

Transcript of 1.0 Pharmaceutical Market

1.1 Pharmaceutical Sales

1.1 Pharmaceutical Sales

3 Internal usage only

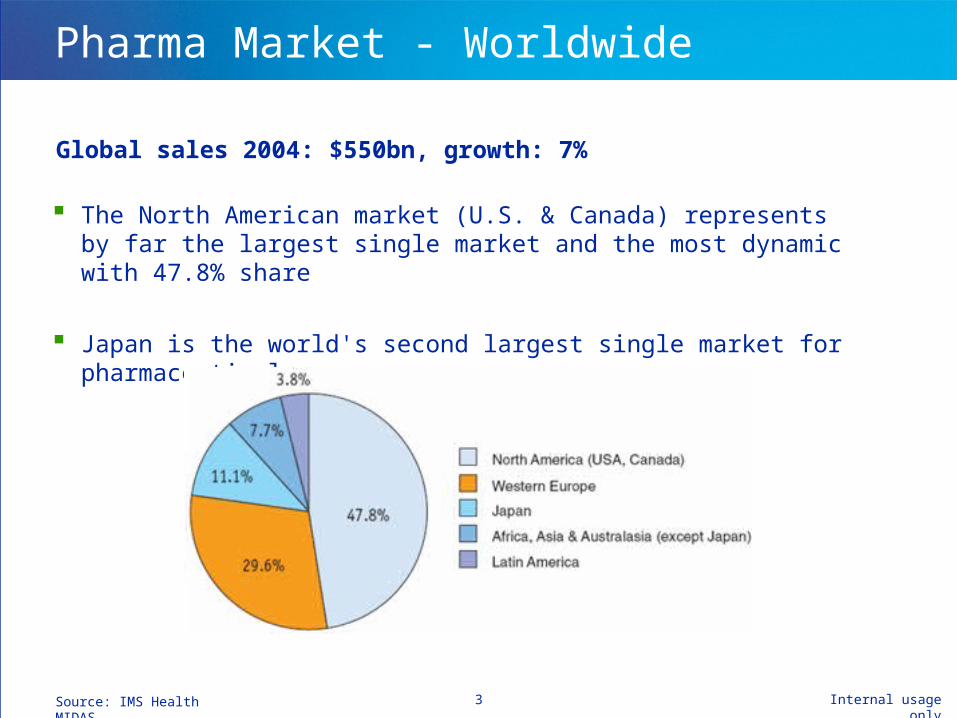

Pharma Market - Worldwide

Global sales 2004: $550bn, growth: 7%

The North American market (U.S. & Canada) represents by far the largest single market and the most dynamic with 47.8% share

Japan is the world's second largest single market for pharmaceuticals

Source: IMS Health MIDAS

Internal usage only4

Pharma Market - Typology

BIOGENERICS are foreseen to share soon the same market

Source: IMS Health

Presence of the different types of drugs on the pharma market

The pharmaceutical market includes three types of medicines:

In 2004, the market of biopharmaceuticals was worth $55bn, a growth of ~17% with respect to 2003

The global sales for generics reached $35bn in 2004, growing about 10%

Pharmaceuticals:

New drugs developed by using chemical synthesis

Biopharmaceuticals:

New drugs developed by using biotechnologies

Generics:

Unbranded version of off-patent drugs

5 Internal usage only

Pharma Market - Insight US

Growth in 2004

Source: Pharmaceutical Engineering, Jul/Aug 2005, 25 (4) 5 Internal usage only

Biopharmaceutical market grows faster

The new blockbusters are more and more bio products (13 out of 67 in total)

Biotech companies such as Amgen, Genentech, Serono and Genzyme are within the top 50 companies

Despite increasing sales in 2004, the US with 7% is experiencing the first drop below double-digit growth since 1995. However, the potential to grow for the market is still high and the growth is foreseen at 8-9% pace in 2006

Generics are promoted by the governmental policy to reduce healthcare costs

In 2004, generics accounted for more than 30% of volume consumption. However, due to low prices they account only for 8% of drug sales by value

Generics market is predicted to grow at rate of 14% annually

6 Internal usage only

Pharma Market - Insight Canada

A bright future in biotech

About 500 diversified companies leading in biotech research

50% of product approvals are expected to be biological products by 2010

A key role of generics

In 2004, 40% of annual prescriptions were generics, even if they accounted for only 15% of the annual expenses

6 Internal usage only

Stable growth of pharmaceuticals and Biotech on the upspring

Source: Pharmaceutical Engineering, Mar/Apr 2004, 25 (2)

7 Internal usage only

Pharma Market - Insight Japan

Japanese market will suffer with a limited 3% growth through 2008 due to the governmental policy to contain costs

In 2004 Japan’s market is worth $60bn - growth: 3%

Pharmaceutical market features particular large share of foreign companies of about 44 %

Dramatic increase in national medical costs forecast due to rising life expectancy and improved medical technology will trigger severe drop of pharmaceutical prize index

Source: Pharmaceutical Engineering, Mar/Apr 2003, 23 (2) 7 Internal usage only

8 Internal usage only

Pharma Market - Insight Western Europe

Source: EFPIA members associations

5 main protagonists:

Germany

France

UK

Italy

Spain

Sales 2004: ~ $163bn Growth rate: 4-5%

8 Internal usage only

In 2006 growth is expected to stay constant at a rate of 4-5%

Internal usage only9

Generics Market - Insight Western Europe

The recent politics of cost containment are promoting the use of generics in all the main European markets. An exceptions is France where the low penetration of generics is probably related to the low level of prices, also for branded medicines

9 Internal usage onlySource: EFPIA members associations

Share in % accounted for by generics in pharmacy market - sales value 2003

Internal usage only10

Pharma Market - Insight Latin America

Latin America (LA) pharma sales in 2003: $21.8bn

Source: IMS Health

Generics

Governmental policy of cost reduction is promoting the use of unbranded drugs

However, generics must fight with cheap copy products, which are not tested for bioequivalence

Latin America’s demand for pharmaceuticals is highly growing

Increasing demand of prescription drugs related to the increased welfare

Mexico and Brazil are the most stable markets in LA

Internal usage only11

Main Markets - Future Trends

The global market size will continue to grow, even if at a contained rate of 6-7%, reaching $640-650bn by 2006

However, there are new elements in the global pharmaceutical markets that need to be taken into consideration. These are:

Source: IMS Health

The presence of new markets such as CEE, China, and India

growing demand for pharmaceuticals

increasing outsourcing and partnerships with local companies

Higher profitability in niche markets

a number of companies move away from the blockbuster model to target at specific patients, i.e. therapies for rare cancer

12 Internal usage only

Audited drug sales in the 8 new members in 2004: $9.2bn - growth: 16%

Market is expected to be worth $13-14 billion by 2010

Generics

In 2002, generics accounted for about 70% of all prescriptions issued in Poland, Hungary and the Czech Republic. They also accounted for more than 40% of the value of the retail market in Poland and the Czech Republic, and about 35% of the value of the retail market in Slovakia and Slovenia

New Markets - Insight CEE

The EU expansion to the Central & Eastern European (CEE) countries with the free circulation of goods generated a new emerging market

Source: IMS Health 12 Internal usage only

Internal usage only13

New Markets - Insight China

Source: IMS MIDAS Quantum

China is world‘s industrial powerhouse - the increasing welfare of its population spurs the demand for pharmaceutical products

13 Internal usage only

China’s highest growth in 2004

China has been recording an impressive double-digit growth of 30% with a market size of ~ $8.5bn. In 2006 the Market will reach $13–14bn with growth of 17-18%. China is expected to become the fifth largest drug market in the world by 2010

Internal usage only14

New Markets - Insight India

Source: IMS MIDAS Quantum

India’s market worth in 2004: $4.6bn

India market ranks thirteenth world wide, but it is expected to have a 80% increase reaching $8.3bn by 2009

A competitive generics market

Ranbaxy or Dr. Reddy’s are top generics producers also outside India

India has enormous market potential due to the increasing welfare of a huge part of the population!

14 Internal usage only

Top 10 Pharma companies in India in 2004

1.2 Pharmaceutical Companies

Internal usage only16

Top 20 Pharmaceutical Companies

Source: http://www.contractpharma.com/top_comp.php#pharma

Rank Company Sales Country1 Pfizer $46.133 US2 GlaxoSmithKline $31.417 UK3 Sanofi-Aventis $29.596 France4 J&J $22.128 US5 Merck $21.494 US6 AstraZeneca $21.426 UK7 Novartis $18.497 CH8 Bristol-Myers Squibb $15.482 US9 Roche $13.840 CH

10 Lilly $13.059 US

11 Wyeth $13.021 US

12 Abbott $11.462 US

13 Takeda $8.538 Japan

14 Boehringer-Ingelheim $7.667 Ger

15 Schering-Plough $6.417 US

16 Bayer $5.529 Ger

17 Novo Nordisk $4.848 DK

18 Schering AG $4.171 Ger

19 Sankyo $4.152 Japan

20 Merck KgA $3.907 Ger

Based on pharmaceutical revenues in 2004 (in millions)

Internal usage only17

Top 10 Generics Companies

Generics sales - 2Q 2005 (in millions)

Source: www.leaddiscovery.co.uk/reports/The_World_Top_Ten_Generic_Companies.html

Rank Company Sales Country

1 Teva Pharmac. Industry $1,230 Israel

2 Sandoz $832 CH / Ger

3 Merck Generics $435 Ger

4 Watson Pharmaceuticals $313 US

5 Mylan Laboratories $253 US

6 Schwarz Pharma $238 Ger

7 Pliva $191 Croatia

8 Barr Pharmaceuticals $188 US

9 Alpharma $103 Norway

10 Actavis $90 Iceland

Internal usage only18

Top 10 Biopharmaceutical Companies

Based on biopharmaceutical revenues in 2004 (in millions)

Source: http://www.contractpharma.com/top_comp.php#pharma

Rank Company Sales Country

1 Amgen $9.977 US

2 Genentech $3.749 US

3 Serono $2.178 CH

4 Biogen Idec $2.112 CH/US

5 Genzyme $1.479 US

6 Gilead $1.242 US

7 MedImmune $1.124 US

8 Chiron $990 US

9 Millennium $349 US

10 Intermune $147 US

1.3 Pharmaceutical Drugs and Compounds

Internal usage only20

Top 10 Pharmaceutical Products

Source: IMS MIDAS Quantum

NOTE: Sales are in U.S. dollars for the 12 months ending June 2005. The figures cover pharmaceutical channel purchases from pharmaceutical wholesalers and manufacturers; they include prescription and certain over-the-counter data and current manufacturer prices.

Pfizer’s Lipitor is number-one drug with annual sales exceeding $10 billion

The top 10 therapies classes account for 30% of the total world market with global sales in excess of $50 billion

Internal usage only21

Forecast for the leading Therapy Classes

A market growth is expected as the population ages!

Source: IMS Health

By 2005 more than 20% of the developed countries population will be over 60 years old (source: UN)

Demand for treating conditions such as hypertension, diabetes, high cholesterol levels, osteoarthritis, menopause symptoms, and prostrate problems will increase

Oncology will have the highest global growth rate of 17–18% in 2006 with a market reaching more than $40 billion by 2008

This is due to better diagnostics, the introduction of further innovative products and the increased patient access to these innovative treatments. Moreover, cancer drugs cannot be impacted by over-the-counter switching

Internal usage only22

New Medicines Launch

70% of sales of new medicines* marketed since 1999 are generated on the US market

Source: IMS Health, 2004

* New medicines cover all new active ingredients marketed for the first time on the world market during the period 1999-2003

Between 1990-2004, R&D investment in US grew 4.5 vs. only the 2.7 times in Europe

Compared to the US, Europe is seen as a less attractive R&D investment location in terms of market conditions and incentives for the creation of new centers

Internal usage only23

Pharma R&D - The Drug Approval Process

Source: EFPIA members associations (official figures)

* Di Masi J., Tufts University, Centre for the Study of Drug Development, November 2001

Startinginvestigation:10,000 entities

Preclinical test: in vitro and in vivo tests

4-5 years

1 goes to commerciali-sation8 years

Phase II Phase III Phase IV

9 year 10 year

Phase I

Safety & tolerability testson 20-80 healthy

volunteers

N D A

FDA approval

12-13 year

Clinical efficacy on 100-300 volunteers

Definitive assessment on 1000-3000 volunteers

Safety surveillance

Clinical Trials on human beings

NDA: New Drug Application

Long: It takes an average of 12-13 years for a new drug from synthesis to medicines basket

Costly: R&D of a chemical or biological entity costs > $1bn*

Of a high risk nature: only 1 out of 10,000 synthesized substances becomes a marketable medicine

1.4 Pharmaceutical Production: Status & Trends

Internal usage only25

Insight US – I

The United States: biggest market and strong producer

Highlights:

National production:US pharmaceutical manufacturing is a dynamic industry answering global economic growth, demographics of an aging population and the production of newer, specialized therapeutics

Strong location:19 out of the top 50 global pharmaceutical companies have corporate headquarters in the US

Not only Blockbusters:Lower costs are needed to allow for better-targeted medicines aimed at smaller patient groups

Contract manufacturing is $30bn market and will grow to $48bn by 2008

Source: Pharmaceutical Engineering, Jul/Aug 2005, 25 (4) 25 Internal usage only

Internal usage only26

Insight US – II

Increase efficiency and reduce cost!

Challenges:

Government and public pressure to reduce overall healthcare costs

Regulatory agencies require compliance with tougher cGMP standards

Contract manufacturing shifts to countries with lower production costs but still complying with high manufacturing standards (e.g. India)

Strategies:

Larger companies seek to integrate previously separate functions, such as development and manufacturing operations

Large scale improvements of productivity and efficiency in pharmaceutical production (i.e. by introducing FormWeigh.Net)

Source: Pharmaceutical Engineering, Jul/Aug 2005, 25 (4) 26 Internal usage only

Internal usage only27

Insight Canada – I

Advantage on pharmaceutical production costs

Highlights:

Favorable environment:stable governments, diversified society and being US neighbor are major advantages for potential Canadian investments

Big economic factor:over 50 pharmaceutical companies employ more than 24 000 people all over Canada

Advantage Canada:KPMG estimated Canada’s pharmaceutical production to have lowest costs worldwide and a 6% cost advantage vs. the US in 2004

Continuous investments:several companies have upgraded plant facilities and installed new equipment to increase production efficiency

Source: Pharmaceutical Engineering, Mar/Apr 2004, 25 (2) 27 Internal usage only

Internal usage only28

Insight Canada – II

Challenges:

Governmental cost-cutting measures will impact on pharmaceutical companies and their production sites

Patent protection lags behind other major western countries

Strategies:

Maximize production by increasing manufacturing efficiency

Improvements to patent legislation and further tax incentives to stimulate future investments

Source: Pharmaceutical Engineering, Mar/Apr 2004, 25 (2)

Facing the future with higher production efficiency and improved legislation

28 Internal usage only

Internal usage only29

Insight Japan – I

Many players at high technological level

Highlights:

Big numbers:Japan’s pharmaceutical industry features a very large number of small national producers (~1400 in total)

Crossing the gap:Japanese chemical companies are developing their own pharmaceutical production technologies

High technological level in manufacturing:since the mid 1990‘s, export dominates the pharmaceutical trade, demonstrating Japan‘s cutting-edge production technology

Source: Pharmaceutical Engineering, Mar/Apr 2003, 23 (2) 29 Internal usage only

Internal usage only30

Insight Japan – II

New regulations are challenging for national producers

Challenges:

The Pharmaceutical Affairs Law (PAL) will encourage the presence of foreign pharmaceutical products, thus challenging local manufacturers

Little growth in pharmaceutical production due to biennial governmental drug price schedule

Strategies:

Higher industrial productivity and fast adoption of global unified rules and standards to increase competitiveness

Intensifying national Merger & Acquisitions to face international competitors

Source: IMS Health, Pharmaceutical Engineering, Mar/Apr 2003, 23 (2) 30 Internal usage only

Internal usage only31

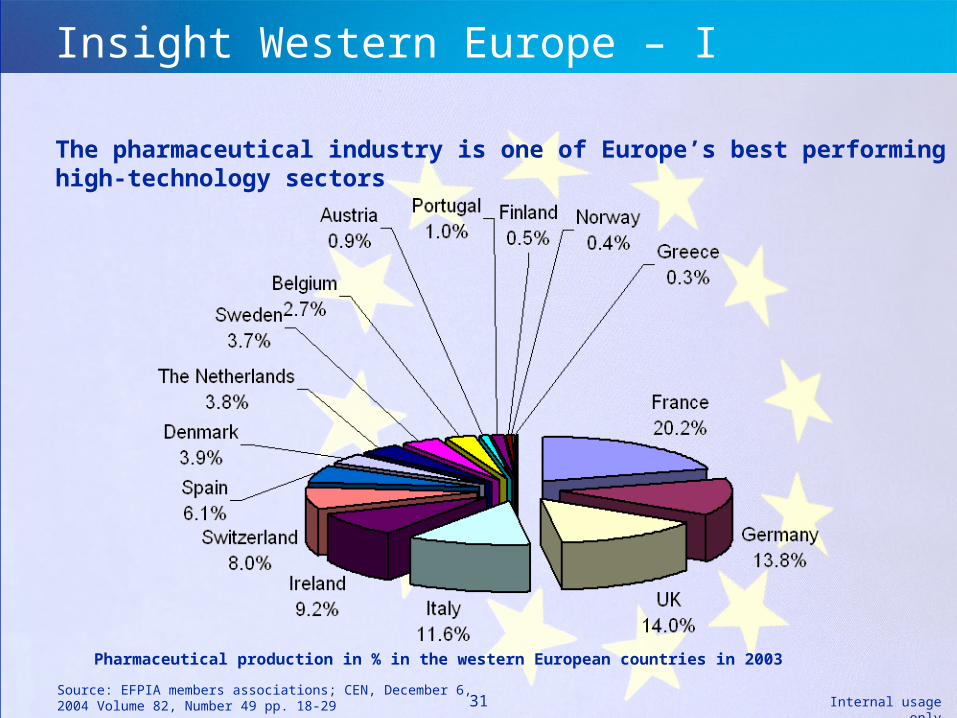

Insight Western Europe – I

The pharmaceutical industry is one of Europe’s best performing high-technology sectors

Source: EFPIA members associations; CEN, December 6, 2004 Volume 82, Number 49 pp. 18-29 31 Internal usage only

Pharmaceutical production in % in the western European countries in 2003

Internal usage only32

Insight Western Europe – II

A thriving pharmaceutical manufacturing with strong technical competence and expertise

Highlights:

Innovation, excellent education system and highly skilled workforce are the strong points to achieve exemplary compliance of facilities for top quality products

Switzerland is still a big protagonist within the world wide drugs manufacturers

Both, UK and France count more than 500 licenses to manufacture drugs

Germany is still one of the top manufacturers in Europe, even if the governmental cost containment politics in 2004 led to lower local investments by big pharma companies

Source: Pharmaceutical Engineering, Jan/Feb 2004, 24 (1) & Nov/Dec 2004, 24 (6); 32 Internal usage only

Internal usage only33

Insight Western Europe – III

The main producers have to face the global rationalization of manufacturing activities

Challenges

An increasingly competitive global marketplace for investment in manufacturing capability, e.g. CEE, China, and India

Strategies

Patient-specific drugs will dominate future markets requiring high flexibility concerning frequent changes in demand and capacity-planning The “make to order” manufacturing facility of the future will require high innovation and excellent engineering skills

Source: Pharmaceutical Engineering, Mar/Apr 2003, 23 (2) 33 Internal usage only

Internal usage only34

Insight CEE – I

Favorable tax regimes and incentives for foreign companies will encourage drug makers to invest in facilities in CEE

Highlights

350 pharmaceutical manufacturers only in the polish market registering more than 8,000 medicinal products

A big opportunity for generic drug manufacturers: profit from low labor, set-up, production costs, and raising demand

Top five pharmaceutical players are already present on the territory and many others start to expand

Source: Pharmaceutical Engineering, May/Jun 2004, 24 (3); PriceWaterHouseCoopers; IMS Health 34 Internal usage only

Internal usage only35

Insight CEE – II

However, the unstable and unpredictable legal environment can still limit investments and development

Challenges

Few experienced GMP professionals

Poor or absence of data exclusivity and protection of intellectual property

Strategies

Huge investment in the pharmaceutical sector to improve know-how and seek for external support or guidance

Reorganization of the local manufacturing: e.g. most of the Polish pharmaceuticals sector has already been privatized or sold to foreign investors

Source: Pharmaceutical Engineering, May/Jun 2004, 24 (3); PriceWaterHouseCoopers; IMS Health 35 Internal usage only

Internal usage only36

Insight China – I

Multinationals consider China as biggest potential future market

Highlights

According to IMS, there are already 1,700 Sino-foreign joint ventures

Roche, Novartis, GSK, and Pfizer rank among the top 10 companies which plan to set local manufacturing facilities

A great opportunity for biopharmaceutical manufacturing sites: low costs and high expertise in biology and biotechnology

Attractive tax incentive for foreign investors in the manufacturing

6,000 domestic producers with 97% of their production being copies of foreign products

Source: PriceWaterHouseCoopers & IMS Health 36 Internal usage only

Internal usage only37

Insight China – II

However, major regulatory improvements are still needed

Challenges

China’s poor record of protecting intellectual property can deter both indigenous and foreign companies from launching new products

Counterfeit drugs are supposed to kill 192,000 Chinese every year!

A complex regulatory processes to obtain drug recognition and start production

Strategies

A State Food & Drug administration (SFDA) has been specifically set up to streamline processes and ensuring compliance with GMP

Source: PriceWaterHouseCoopers & IMS Health 37 Internal usage only

Internal usage only38

Insight India – I

India is becoming a key manufacturing destination for the multinationals: costs to set-up and run a production facility are 80% lower than in the West

Highlights

70% of a total of 60,000 manufactured formulations are managed by 10,000 domestic firms

Multinational companies, such as Teva, Sandoz, and Ratiopharma, are starting production in India to increase market share

Tax break for foreign investors in the local manufacturing facilities

A thriving biopharmaceutical industry: six of the most important biopharmaceutical products are manufactured in India

Source: Pharmaceutical Engineering, Nov/Dec 2005 38 Internal usage only

Internal usage only39

Insight India – II

And the regulatory apparatus is evolving with the Industry

Challenges

Despite the Patents Act, ratified in April 2005, full intellectual protection is not yet reached

Counterfeit or substandard manufactured drugs are still an issue!

Partly poor infrastructure: shortages on water supply, electric power, paved roads and rail transportation continue to hamper growth

Strategies

Hi-tech industry and hi-GMP with 60% of the manufacturing sites already approved by US FDA

High quality ancillary industry: all needed equipment is locally produced (glass bottles, vials, capsules, blisters, packaging,…)

Source: Pharmaceutical Engineering, Nov/Dec 2005 39 Internal usage only

Internal usage only40

Insight Latin America – I

Strong multinational manufacturing presence

Source: Pharmaceutical Engineering, Jan/Feb 2005, 25 (1)

Highlights

Major multinationals, e.g. Pfizer, Novartis, Roche, GSK, Aventis, Bristol-Myers Squibb, Schering Plough, have local production facilities or partnership with local contractors

Huge investments in the production have been realized to increase scale and productivity of top products

The Bioindustry park: a very promising source of new medicines and genetic discovery which will attract new companies, enterprises and business

Internal usage only41

Insight Latin America – II

Still unfavorable tax regimes and no incentives for foreign investors

Source: Pharmaceutical Engineering, Jan/Feb 2005, 25 (1)

Challenges

FDA has identified several issues dealing with unmatched GMP requirements

Counterfeit medicines and lack of patent protection are still an issue

Strategies

Know-who rather than know-how: understanding the culture diversity!

Alliance and partnership with local manufacturers to outsource most of the activities

Establish a base in the most stable regions, i.e. Brasil, Mexico and then expand to the other LA countries