1 Wolfgang Modery Directorate Monetary Policy The ECB’s monetary policy at times of crisis Visit...

29

1 Wolfgang Modery Directorate Monetary Policy The ECB’s monetary policy The ECB’s monetary policy at times of crisis at times of crisis Visit of Representatives of the Swedish Industry Frankfurt am Main, 1 October 2009

-

Upload

ronald-webb -

Category

Documents

-

view

220 -

download

0

Transcript of 1 Wolfgang Modery Directorate Monetary Policy The ECB’s monetary policy at times of crisis Visit...

1

Wolfgang ModeryDirectorate Monetary Policy

The ECB’s monetary policy The ECB’s monetary policy at times of crisis at times of crisis

Visit of Representatives of the Swedish Industry

Frankfurt am Main, 1 October 2009

2

• Turmoil started in 2007 in US as sub-prime crisis

• Intensification in autumn 2008 (Lehman

Brothers)

• Functioning of money market seriously

hampered

• Spill-over of financial stress to real economy

severe downward impact on economic growth

The unfolding of the crisis

3

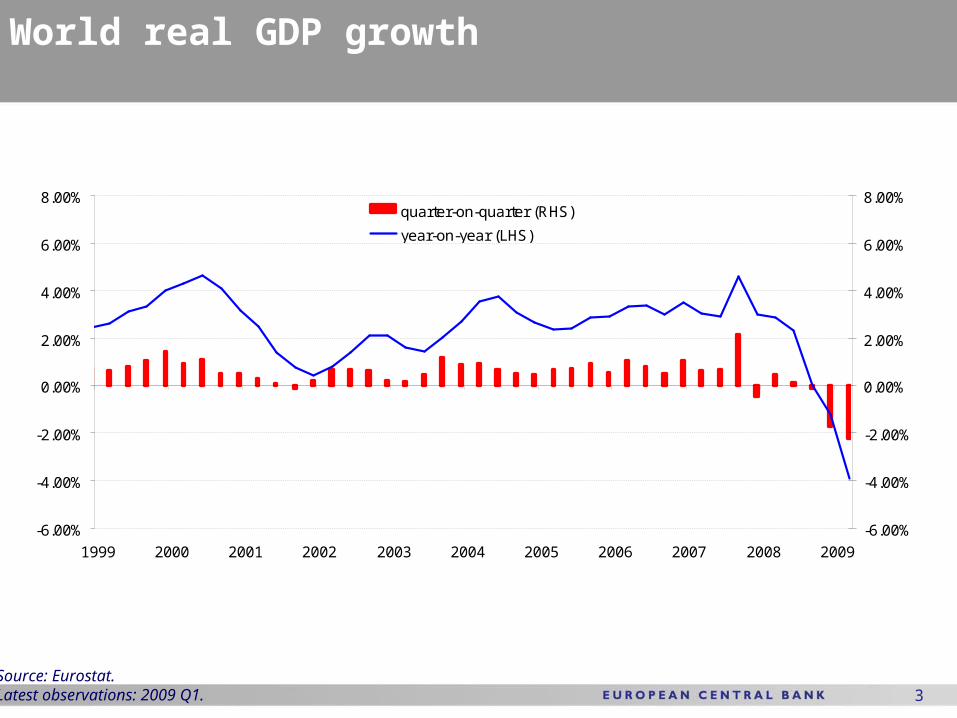

World real GDP growth

Source: Eurostat.Latest observations: 2009 Q1.

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%quarter-on-quarter (RHS)

year-on-year (LHS)

4Source: Eurostat.Latest observations: 2009 Q2.

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

-2.7

-2.4

-2.1

-1.8

-1.5

-1.2

-0.9

-0.6

-0.3

0.0

0.3

0.6

0.9

1.2

1.5quarter on quarter percentage changes (RHS)

annual percentage changes (LHS)

Euro area real GDP growth

5

Euro area real GDP growth: historical perspective

Source: Eurostat.Latest observation: 2009 Q2.

-6

-4

-2

0

2

4

6

8

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006

-6

-4

-2

0

2

4

6

8

quarter-on-quarter (LSH) year-on-year (RHS)

6

Euro area industrial production: historical perspectiveExcluding construction production

Source: Eurostat.Latest observation: 2009 Q2.

-20

-15

-10

-5

0

5

10

15

20

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

-20

-15

-10

-5

0

5

10

15

20

quarter-on-quarter (LHS) year-on-year (RHS)

7

Comparison of forecasts for euro area real GDP growth

(annual percentage changes)

Institution Date of release 2009 2010

ECB staff macroeconomic projections Sept. 2009 -4.4 - -3.8 -0.5 - 0.9

European Commission May 2009 -4.0 -0.1

IMF July 2009 -4.8 -0.3

OECD June 2009 -4.8 0.0

ECB Survey of Professional Forecasters 2009 Q3 -4.5 0.3

Consensus Economics August 2009 -4.3 0.6

Euro Zone Barometer August 2009 -4.3 0.7

GDP growth forecasts / projections

8

Eurosystem staff projections for euro area growth Real GDP growth between -4.4% and -3.8%

in 2009 and between -0.5% and 0.9% in 2010

Upwards revision of the range for both 2009 and 2010, reflecting the recent, more positive developments and information

GDP expected to continue to stabilise in second half of 2009, before gradually recovering during 2010

Projected improvement mainly supported by revival of exports and positive effects of fiscal impulse on domestic demand

9

Risks to the growth outlook

Risks are broadly balanced and result from Effects from the macroeconomic stimulus from various policy measures Confidence improvement Favourable developments in labour markets and foreign demand

On the other hand Stronger impact on the real economy from the turmoil in financial markets Increases in oil and other commodity prices Intensification of protectionist pressures Adverse developments in the world economy from disorderly correction of global imbalances

10

Inflation

Latest observation: August 2009. Sources: BIS, Eurostat and ECB calculations

HICP, (percentage change compared to the previous year)

-2

0

2

4

6

8

10

12

14

16

1970 1975 1980 1985 1990 1995 2000 2005

11

Source: Eurostat. Last observation: HICP August 2009.

(percentage points, annual percentage changes)

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

2004 2005 2006 2007 2008 2009

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

Contribution of food component to overall HICPContribution of energy component to overall HICPOverall HICPHICP excluding food and energy

HICP inflation and contributions from energy and foods

12

Background slides

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

2004 2005 2006 2007 2008 2009

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Const ruct ionManufacturingMarket servicesT otal economy

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1999Q1 2001Q1 2003Q1 2005Q1 2007Q1 2009Q1

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Nominal unit labour costsReal unit labour costs (GDP deflated)Compensation per employeeLabour productivity

Employment growth by sector (annual growth rates)

Labour cost indicators (annual growth rates)

Current labour market developments

Source: Eurostat and ECB.

13

Euro area unemployment ratePercent of labour force

Latest observation: July 2009.Source: Eurostat.

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

unemployment rate

14

Sources: Reuters, Consensus Economics and ECB. 1 ECB’s Survey of Professional Forecasters Gathers expectations for euro area inflation, economic activity and unemployment from experts affiliated to financial or non-financial institutions based in the European Union. Latest observations: 20 August 2009.

Inflation expectations

(annual percentage change)

1.0

2.0

3.0

4.0

1.0

2.0

3.0

4.0

Inflation expectations 5 to 10 years ahead (Consensus Economics Forecasts)

HICP Inflation expectations, 5 years ahead (SPF)

15

Survey based and market inflation expectations in the euro areaPercent per annum

Source: Reuters, Consensus, and ECB calculations.Latest observation: 15 September 2009.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2004 2005 2006 2007 2008 2009

5-year BEIR (seas. adj.)5-year forward 5 years ahead BEIR (seas. adj.)1-year forward 4 years ahead BEIR (seas. adj.)6 to 10 years ahead Consensus inflation forecastLong term inflation expectations from SPF

16

Comparison of forecasts for euro area consumer price inflation

(annual percentage changes)

Institution Date of release 2009 2010

ECB staff macroeconomic projections Sept. 2009 0.2 - 0.6 0.8 - 1.6

European Commission May 2009 0.4 1.2

IMF July 2009 0.3 0.6

OECD June 2009 0.5 0.7

ECB Survey of Professional Forecasters 2009 Q3 0.4 1.1

Consensus Economics August 2009 0.3 1.2

Euro Zone Barometer August 2009 0.3 1.1

HICP forecasts

17

Eurosystem staff projections for euro area inflation

Price and cost expected to remain dampened in the wake of ongoing sluggish demand in the euro area and elsewhere

Annual HICP inflation projected between 0.2% and 0.6% in 2009 and between 0.8% and 1.6% in 2010

Slight upward revision for both 2009 and 2010 compared with the June 2009 ECB staff projections, reflecting mainly upward revisions to energy prices

18

Risks to the inflation outlook

~ Outlook for economic activity

Higher than expected commodity prices Stronger than currently expected

increases in indirect taxation and administered prices due to the need for fiscal consolidation in the coming years

19

Since the intensification of the financial crisis in autumn of 2008

… and against the background of rapidly receding inflationary pressures …

… the ECB has taken a series of monetary policy and liquidity management measures …

… unprecedented in nature, scope and timing

Unprecedented response by the ECB to the crisis

20

ECB response: strong decline in ECB interest rates Percentages per annum; daily data

Source: ECBLast observations: 16 September 2009

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09 Feb-09Mar-09 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09

EONIA

main refinancing rate

deposit rate

marginal lending rate

21

ECB response to the crisis – enhanced credit support

Primarily bank-based measures to enhance

the flow of credit beyond the standard

interest rate channel

- Fixed-rate full allotment

- Expansion of collateral

- Longer-term liquidity provision

- Liquidity provision in foreign currencies

- Financial market support through purchases of

covered bonds

22

Note: Breakdown of the sources of external financing of non-financial corporations, in percent, average 2004 – 2008

Source: ECB Monthly Bulletin, April 2009

0

20

40

60

80

100

Euro Area United States

0

20

40

60

80

100

Banks

Non-Bank

Non-Bank

Banks

Different role played by banks in funding firms in the euro area and the US

23

Breakdown of the financing of non-financial businesses in the US (4-quarter moving sum of transactions, in USD bn)

Breakdown of the financing of non-financial corporations in the euro area (4-quarter moving sum of transactions, in EUR bn)

-1000

-500

0

500

1000

1500

2000

2500

3000

2000 2002 2004 2006 2008

-1000

-500

0

500

1000

1500

2000

2500

3000

bank loansloans from private ABS issuerstrade creditdebt securitiesshares and other equity other financingtotal financing

-400

-200

0

200

400

600

800

1000

2000 2002 2004 2006 2008

-400

-200

0

200

400

600

800

1000

MFI loansOFI loansother f inancingdebt securitiesshares and other equity (netted)total f inancing

Sources: Board of Governors of the Federal Reserve System and ECBLast observations: 2009 Q1

Different financial structures in euro area and the US

24

The Eurosystem’s balance sheetIn millions, euro

Source: ECBLast observations: End-of-August 2009

600

800

1,000

1,200

1,400

1,600

1,800

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09

Start of financial turmoil

25

Loans to the private sectorAnnual percentage changes; adjusted for seasonal and calendar effects

Source: ECB calculations.Latest observations: July 2009

-1

2

5

8

11

14

2004 2005 2006 2007 2008 2009

-1

2

5

8

11

14

non-financial corporations

households

26

MFI interest ratesAnnual percentage points

Short-term Long-term

Sources: ECB and Reuters.Latest observations: MFI interest rates: July 2009; money market rates: 9 September 2009 (average of daily data).

2

3

4

5

6

2003 2004 2005 2006 2007 2008 2009

2

3

4

5

6

loans for house purchase (over 5 and up to 10 years)loans for house purchase (over 10 years)small loans to non-financial corporations (over 5 years)large loans to non-financial corporations (over 1 and up to 5 years)large loans to non-financial corporations (over 5 years)

0

1

2

3

4

5

6

7

8

9

10

2003 2004 2005 2006 2007 2008 2009

0

1

2

3

4

5

6

7

8

9

10

consumer creditloans for house purchasesmall loans to non-financial corporationslarge loans to non-financial corporations3-months Euribor

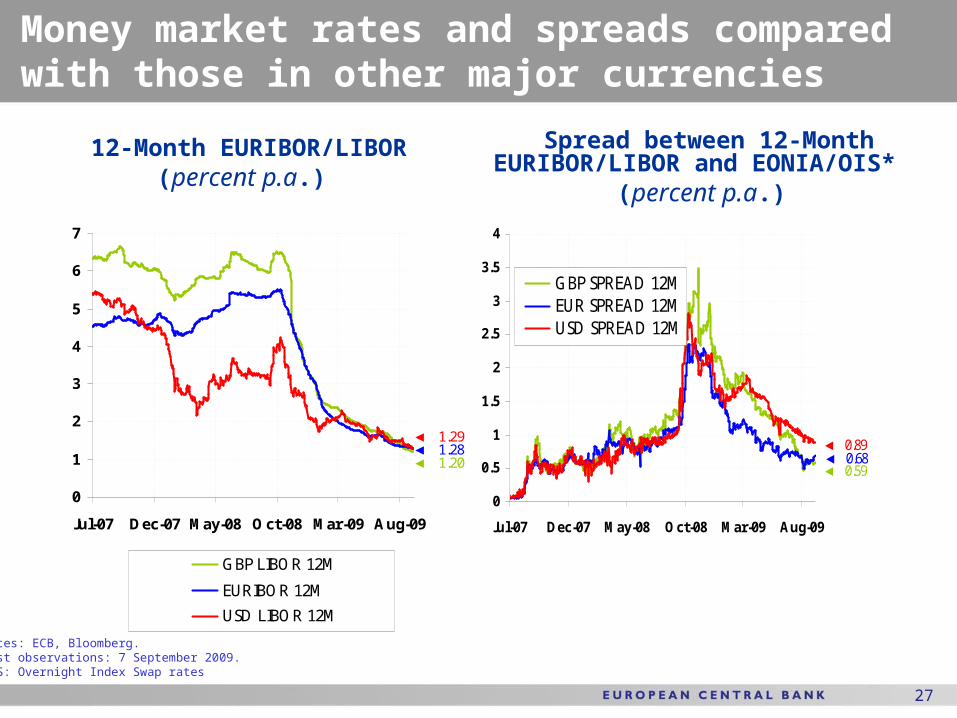

27

Spread between 12-Month EURIBOR/LIBOR and EONIA/OIS*

(percent p.a.)

12-Month EURIBOR/LIBOR(percent p.a.)

Sources: ECB, Bloomberg.Latest observations: 7 September 2009. * OIS: Overnight Index Swap rates

Money market rates and spreads compared with those in other major currencies

◄ 1.20◄ 1.28◄ 1.29

0

1

2

3

4

5

6

7

Jul-07 Dec-07 May-08 Oct-08 Mar-09 Aug-09

GBP LIBOR 12M

EURIBOR 12M

USD LIBOR 12M

◄ 0.89

◄ 0.59◄ 0.68

0

0.5

1

1.5

2

2.5

3

3.5

4

Jul-07 Dec-07 May-08 Oct-08 Mar-09 Aug-09

GBP SPREAD 12MEUR SPREAD 12MUSD SPREAD 12M

28

Lessons to be drawn? (1)

Make financial markets more effective by

• Stricter regulation of all financial market participants and

products

• More adequate capital requirements and accounting

rules

• Stronger international cooperation in financial oversight

• Appropriate time horizon for macro-economic policies

• Adjustment of banking models and remuneration

systems

• Global management of global risks ?

29

Lessons to be drawn? (II)

Moreover

• Strengthen incentives that improve disciplining

forces of competition

• Discourage “short-termism” and strengthen concept

of liability and responsibility

• The value added by having a monetary union was

particularly

proved helpful at times of financial distress