1 Welcome State Retirement Agency Presenter Patricia Fitzhugh February 24, 2009 Employers’...

81

1 Welcome Welcome State Retirement Agency Presenter Patricia Fitzhugh February 24, 2009 Employers’ Training Program Employers’ Training Program

-

Upload

warren-gordon -

Category

Documents

-

view

214 -

download

1

Transcript of 1 Welcome State Retirement Agency Presenter Patricia Fitzhugh February 24, 2009 Employers’...

1

WelcomeWelcome

State Retirement Agency

Presenter

Patricia FitzhughFebruary 24, 2009

Employers’ Training ProgramEmployers’ Training Program

2

Introductory RemarksIntroductory Remarks

This recorded presentation is a result of several live presentations held throughout the State of Maryland in 2008-2009. This presentation will cover the same topics covered at the live presentations and will also incorporate many of the common questions that were asked during those presentations. Our agenda includes the following topics:

- Membership - Enrollment - Purchase of Previous Service - Transfer of Service- Re-employment after Retirement - Withdrawals - Workers’ Compensation Offsets - Payment Options - SRPS Resources

3

Introductory RemarksIntroductory Remarks

SRA’s MissionSRA’s Mission

To administer the survivor, disability, and retirement benefits of the System’s participants, and to ensure that sufficient assets are available

to fund the benefits when due.

4

Introductory RemarksIntroductory Remarks

SRA’s GoalsSRA’s Goals

- Efficiently collect the required employer and employee contributions to fund the System

- Prudently invest assets to optimize returns while controlling risks

- Effectively communicate to participants the benefits provided by the System - Pay benefits accurately and on time

5

Introductory RemarksIntroductory Remarks

To best help you, we need…To best help you, we need…

Accurate, useable and timely member data and information

6

Introductory RemarksIntroductory Remarks

And, from us, you need…And, from us, you need…- Up-to-date instructions

- Clear expectations

- Our support when you have questions and issues (Manual/Web site (http://www.sra.state.md.us/employer.html),

Counselors, Telephone, Written Materials)

7

Introductory RemarksIntroductory Remarks

So that…So that…

Members receive accurate/timely information,and retirees are paid accurately and on time.

We have common goals.We have common goals.

8

Introductory RemarksIntroductory Remarks

Workshop GoalsWorkshop Goals- Assist you in fulfilling your day-to-day responsibilities as an employer-partner of the SRPS.

- Strengthen cooperation and communication.

9

Introductory RemarksIntroductory Remarks

SRA Administers Several Separate Plans:SRA Administers Several Separate Plans:

1. Teachers’ Retirement System 2. Employees’ Retirement System 3. Correctional Officers’ Retirement System 4. State Police Retirement System 5. Judges’ Retirement System 6. Legislative Retirement System 7. Law Enforcement Officers’ Pension System 8. Teachers’ Pension System 9. Employees’ Pension System10. Local Fire and Police Pension System

Each system has its own set of rules of eligibility and benefits.

10

Introductory RemarksIntroductory Remarks

State Retirement and Pension System of Maryland (SRPS)State Retirement and Pension System of Maryland (SRPS)[Defined Benefit Plan—Internal Revenue Code 401(a)]

Our Responsibilities

- Fiduciary responsibility for administering retirement and pension allowances and other benefits- Keep employer rates affordable- Maximize investment returns and minimize risks

11

MembershipMembership

TopicsTopics

- Who is eligible?

- Numbers

- Who must be enrolled?

- Who is not eligible?

- Membership termination

12

MembershipMembership

Members Include…Members Include…- State Employees- Employees of Participating Gov’t Units (PGU’s)- State Police- Teachers- Law Enforcement Officers- Correctional Officers - Fire Fighters- Legislators- Judges

13

MembershipMembership

By the Numbers...By the Numbers... Active members = 199,255

Retirees and Beneficiaries = 112,422

14

MembershipMembership

Membership is…Membership is…

Mandatory for all employees who meet the following eligibility criteria: - Regular, full-time employees - Regular, part-time employees who are budgeted to work at least 500 hours/year or who actually work 500 hours in a fiscal year (retroactive to the beginning of the FY)

- - - Employees who meet these criteria cannot reject

membership; they must be enrolled immediately upon employment.

15

MembershipMembership

Membership is Membership is NotNot Available to… Available to…

- Temporary employees - Contractual employees

- Seasonal or Emergency employees

A temporary or contractual employee cannot elect membership.

16

MembershipMembership

Membership terminates if the member…Membership terminates if the member…

- Is separated from employment for a certain period of time (depending on the system) - Terminates employment and withdraws accumulated contributions - Retires - Dies

17

Membership Q&A’sMembership Q&A’s

Common Questions - MembershipCommon Questions - Membership

1)1) Do all part-time employees qualify for membership?Do all part-time employees qualify for membership?

When a new part-time employee is hired you need to determine whether or not they are expected (budgeted) to work at least 500 hours in the fiscal year. If they are expected to work at least 500 hours then they must be enrolled. If they are expected to work less than 500 hours then they should not be enrolled, however, you should monitor their actual hours worked. If it becomes clear that they will work more than 500 hours in the fiscal year then they must be enrolled.

18

Membership Q&A’sMembership Q&A’s

Common Questions – MembershipCommon Questions – Membership2)2) What do I need to do if I have a new employee who was not What do I need to do if I have a new employee who was not enrolled when they began employment because they were not enrolled when they began employment because they were not expected to work at least 500 hours in the fiscal year, but they expected to work at least 500 hours in the fiscal year, but they do end up working at least 500 hours?do end up working at least 500 hours?

You must enroll the employee back to the beginning of the current fiscal year or their date of employment whichever is more recent. For example if we are in FY2009 and you have an employee who was hired November 1, 2008 then 11/1/08 would be their enrollment date. If you had an employee who had been hired February 1, 2008 (FY2008) you would make their enrollment date July 1, 2008 (the start of the current fiscal year). The employer must start reporting retirement payroll data for the employee and Prior Pay Period Adjustment Forms must be submitted on behalf of the employee. Once the employee is enrolled they are always a member and should have their retirement payroll data reported to the Agency even if in subsequent fiscal years their actual hours worked fall below 500 hours.

19

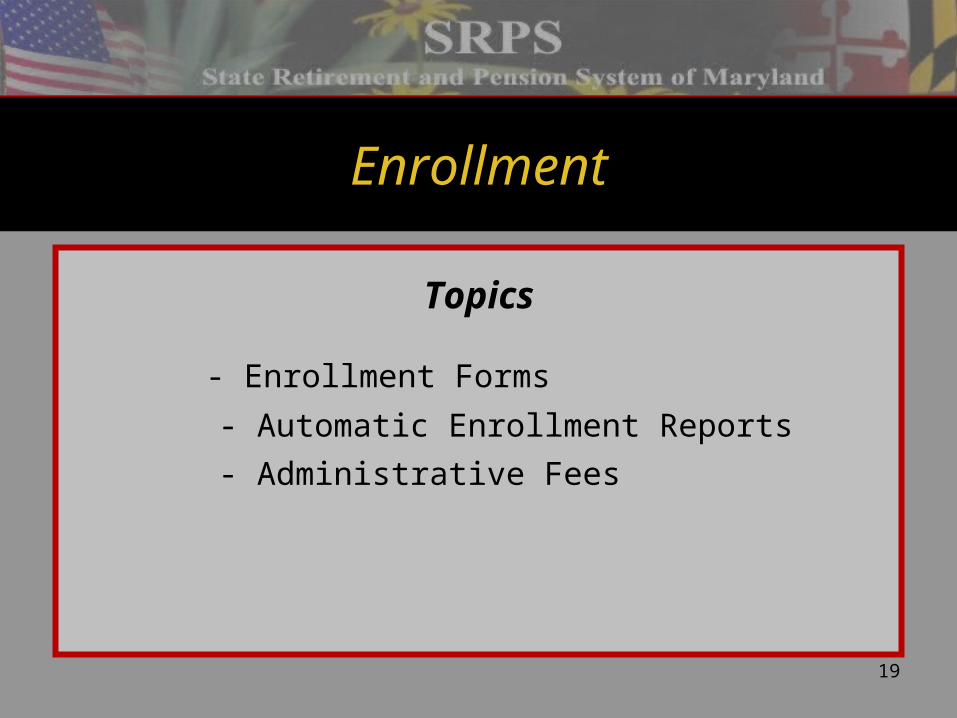

EnrollmentEnrollment

TopicsTopics

- Enrollment Forms

- Automatic Enrollment Reports

- Administrative Fees

20

EnrollmentEnrollment

Eligible members must accurately complete Eligible members must accurately complete and submit three documents:and submit three documents:

1) Application for Membership (#001) (separate form for Legislators and Judges) or Legislative Pension Plan Application for Membership (#002) or Judges Retirement System Application for Membership (#003), and

2) Valid Proof of Birth Date, and

3) Designation of Beneficiary Form (#004) (signed, dated and notarized).

Note: Enrollment is complete when Employer submits the proper forms accurately and completely. If not complete or accurate, the forms will be returned to the Retirement Coordinator for completion.

21

EnrollmentEnrollment

What is considered valid proof of birth date?What is considered valid proof of birth date? For US citizens, a copy of valid proof of birth date document includes any one of the following: - Unexpired driver’s license - Maryland identification card - Birth certificate - Adoption record - United States passport - Naturalization records - Census record from United States Bureau of the Census - Military documentation from any branch of the United States Armed Forces - Hospital birth record, certified by the custodian of record - Statement of Age card: county health dept. or US Bureau of Vital Statistics

For Non US citizens - Resident Alien Registration Receipt Card

Note: Please make sure that on any copy of valid proof of birth date document, that the date of birth is clearly visible and readable.

22

EnrollmentEnrollment

Automatic Enrollment (AE) ReportsAutomatic Enrollment (AE) Reports What is Automatic Enrollment? Employee is enrolled via automated payroll transaction data, but enrollment forms (Application, valid proof of birth and Beneficiary forms) were not received, or payroll information could be under an incorrect Social Security Number4

When are AE Reports prepared? Semi-annually, a listing of AE records (by location code) is submitted to the agency/PGU for review and correction.

What should an employer do with the AE Report? Submit the enrollment forms (Application, Proof of Birth Date, Designation of Beneficiary) to SRPS as soon as possible.

23

EnrollmentEnrollment

Administrative FeesAdministrative FeesFees to be imposed as a result of the 2008 Legislative Session.

Law provides for the imposition of an administrative fee ($100.00) for each employee that an employer fails to properly enroll.

How it works: - Nov. and Apr.— AE Reports are distributed. Employers have until June to correct AE records. - June— Fiscal year end AE Report (effective 6/30/XX) shows employees that began employment prior to 4/1/XX and are active after 5/31/XX and have not been properly enrolled. - Aug.— Invoices to employers based upon fiscal year-end AE Report - Sept.— Payment due 30 days after invoice date

24

Enrollment Q&A’sEnrollment Q&A’s

Common Questions - EnrollmentCommon Questions - Enrollment

1)1) Why is an administrative fee being imposed for each employee Why is an administrative fee being imposed for each employee that an employer fails to properly enroll?that an employer fails to properly enroll?

SRA uses the data in our records to effectively administer the Plan. When an employee is not properly enrolled, SRA must use incomplete information which can impact our operations. Additionally, the data in our records is used by our actuary to help determine the liabilities of the System and the annual employer contribution rate. Therefore, it is critical that our data be complete and accurate.

25

Purchase of Previous ServicePurchase of Previous Service(Buyback)(Buyback)

TopicsTopics

- Definition of Service Purchase (Buyback)- How Credit is Accrued

- Types of Buyback- Cost Formulas

26

Purchase of Previous ServicePurchase of Previous Service

What is a “Buyback”?What is a “Buyback”?

Acquisition of additional retirement credit through the employee’s direct payment to SRPS.

27

Purchase of Previous ServicePurchase of Previous Service

How Credit is AccruedHow Credit is Accrued

- Credit for active military duty - Credit for unused sick leave - Credit for service in a PGU before the PGU joined SRPS

28

Purchase of Previous ServicePurchase of Previous Service

““Buyback” is service purchased other than the above, and includes:Buyback” is service purchased other than the above, and includes:

- Paying for missed contributions while in an eligible position or for specific periods of employment that would not have qualified for credit except for legislative authority. - Regaining previous membership credit after withdrawing contributions and interest. - Transferring credit from another PGU (no service break; within one year of entering new system; must transfer required contributions within same period of time; forfeit benefits in former system). - Purchasing credit for qualifying leave such as: Personal Illness; Maternity/ Paternity; Adoption; Study; Gvt. Sponsored or Subsidized Work; Service as an Officer in an Officially Recognized Organization

29

Purchase of Previous ServicePurchase of Previous Service

Costs: Three FormulasCosts: Three Formulas

Normal: Contribution rate at time of service XX salary earned at time of service ++ statutory interest on the contributions to date of payment

Full Cost: An amount equal to the annuity reserve ++ pension reserve to fund the additional allowance

Half Cost: Same formula as “Full Cost” but cost is halved (because credit was lost through service break)

Note: Money to pay for previous service may be rolled from a voluntary retirement program.

30

Purchase of Service Q&A’sPurchase of Service Q&A’s

Common Questions – Purchase of ServiceCommon Questions – Purchase of Service

1)1) Can contractual service be purchased? How?Can contractual service be purchased? How?

Contractual service may be purchased by a member of the Pension System at “full cost” which is the amount equal to the reserves needed to fund the additional benefit as a result of the purchase. The difference between the reserves needed to pay the benefit, with and without the purchased service, is the cost to the member.

If the member is not an employee of a participating governmental unit or a former participating governmental unit that has withdrawn, and is purchasing service for periods of employment with the State, the cost is reduced by 50%.

This type of service may only be purchased in the 12 month period immediately preceding retirement, as this is when the benefit reserves will be known. A maximum of 10 years service may be purchased at “full cost”.

31

Purchase of Service Q&A’sPurchase of Service Q&A’s

Common Questions – Purchase of ServiceCommon Questions – Purchase of Service2)2) What is the process for purchasing service?What is the process for purchasing service?

The process starts with a member completing the top portion of the Form 26. If they are purchasing service that is only purchasable in the 12-month period preceding retirement (full cost), they should indicate their proposed retirement date, the amount of service they would like to purchase, and also submit a Form 9, “Application for an Estimate of Service Retirement Allowance.” The member then submits the Form 26 to their former employer for verification of employment.

The former employer will verify the necessary information and forward the Form 26 to our office.

Once we receive the Form 26 the verification is reviewed for purchase eligibility. If the service is not eligible for purchase, the Form 26 is returned to the member with a letter of explanation. If the service is eligible for purchase, a calculation is prepared, a bill is generated and mailed to the member.

All full cost bills prepared also generate an estimate of retirement benefits. Estimates with the purchase of service included and without the purchase (if eligible for retirement without the additional service included) are sent to the member shortly after the bill has been released.

32

Purchase of Service Q&A’sPurchase of Service Q&A’s

Common Questions – Purchase of ServiceCommon Questions – Purchase of Service

3)3) How does a member pay SRA to complete the purchase?How does a member pay SRA to complete the purchase?

A member may remit payment by returning the bill to our office along with a check or money order payable to the State Retirement and Pension System of Maryland. Payment may also be made by direct rollover from a Traditional IRA, or an Eligible Employer Plan which includes a plan qualified under section 401(a) of the Internal Revenue Code, including a 401(k) plan, profit sharing plan, defined benefit plan, stock bonus plan, and money purchase plan; a section 403(a) annuity plan; a section 403(b) tax sheltered annuity; and an eligible section 457(b) plan maintained by a governmental employer (governmental 457 plan). The rollover payment must be accompanied by a completed Form 192 “Trustee-to-Trustee Transfer Request for Purchase of Service.” A Form 192 is sent to the member for this purpose along with the bill.

33

Transfer of ServiceTransfer of Service

TopicsTopics

- Title 37- Eligibility to Transfer- Career Changes- Transfer of Service Credit Waivers

34

Transfer of ServiceTransfer of Service

Title 37 of Annotated Code of MD allows…Title 37 of Annotated Code of MD allows… …members of a state or local pension or retirement system to transfer to another state or local pension system under the following circumstances:

1) No break (30 days or more) in service, and 2) Application (for transfer is made within one year of becoming a member of the new system), and 3) Each system is operated on an actuarial basis

35

Transfer of ServiceTransfer of Service

Eligibility for TransferEligibility for Transfer(Change in job requiring participation in a different plan)

Guidelines: - Employee initiates the transfer (Employer should alert the employee of the criteria) within one year of new employment…otherwise, the service credit is maintained in separate plans.* - Employment must be continuous (no break in employment over 30 days).

*Exceptions: a) If the change is from Employees’ Contributory Pension System to the Teachers’ Contributory Pension System or vice versa, then there is no time limit to the transfer service credit. b) If the change is from Non-Contributory to Contributory Pension or Alternate Contributory Pension or from Contributory to Alternate Contributory Pension, accounts may be combined after completion of one year of service.

36

Transfer of ServiceTransfer of Service

Career ChangesCareer ChangesForm to transfer depends on previous plan

- Career changes within same pension system (with no break in service)— Member does not need to take any action.

- Career changes into a different SRPS (no break in service)—Within one year, member needs to complete form 37 (Election to Transfer) to have accounts combined.

- Career changes with a break in service—Does not qualify under Title 37

- Career change from an external system—Member should complete Form 26 (Request to Purchase Previous Service) and send it to the previous employer for salary and service certification.

37

Transfer of ServiceTransfer of Service

Transfer of Service Credit WaiversTransfer of Service Credit Waivers Guidelines

Who can request a waiver from the one year filing requirement?

A member who has: -Accumulated service credit in a pension or retirement system, and

-Accepted a new position requiring membership in the SRPS, and

-Did not make claim to transfer service within the one-year after becoming a member of one of the several SRPS systems.

38

Transfer of ServiceTransfer of Service

Requests for Waiver of One Year RequirementRequests for Waiver of One Year Requirement A member who fails to make claim for transfer of service credit within the one year may do the following…

- Submit a written request to the Executive Director along with supporting documents stating why member did not make the claim to transfer within one year.

- Provide written certification from prior/current employer that the sole reason was attributable to mishandling or misinformation by member’s employer.

- Requests for waiver must be within four years after joining the new system

- Members who became eligible to transfer service credit before 7/1/2007 must apply for the waiver on or before 6/30/2011.

39

Transfer of ServiceTransfer of Service

Review of Requests for Waiver by Executive DirectorReview of Requests for Waiver by Executive Director

Executive Director may accept a member’s request for a waiver if the member satisfactorily demonstrates that…

- Failure to make claim to transfer within one year was solely attributable to physical or mental incapacity during the filing period, or

- Failure to make claim was attributable solely to misinformation or mishandling by the member’s employer and member provides certification required from the reporting authority agency head.

40

Transfer of ServiceTransfer of Service

Automatic WaiverAutomatic WaiverAgency will grant an automatic waiver of the one year filing requirement, if…

– The member submits the completed form and all documentation within one year of becoming a member in the new system.

–The required deposit of member contributions, plus interest, does not occur within one year.

–The delay in the deposit of the member contributions is attributable solely to the failure of the previous employer to transfer the contributions.

41

Transfer of Service Q&A’sTransfer of Service Q&A’s

Common Questions – Transfer of ServiceCommon Questions – Transfer of Service

1)1) Why are all annual base salaries (not partial year earnings) and Why are all annual base salaries (not partial year earnings) and effective dates of salary changes required?effective dates of salary changes required?

The calculation of cost is the amount of contributions (plus interest) the member would have contributed based on their annual salary had they been a member of the State System for the period being transferred.

42

Transfer of Service Q&A’sTransfer of Service Q&A’s

Common Questions – Transfer of ServiceCommon Questions – Transfer of Service

2)2) In addition to the beginning and ending dates of the membership being In addition to the beginning and ending dates of the membership being transferred, why are the dates of any missing time and additional transferred, why are the dates of any missing time and additional service, such as military credit or a purchase, required?service, such as military credit or a purchase, required?

The exact dates of actual service are needed not only to calculate the contributions and interest correctly, but to ensure the member receives the proper benefit calculation at retirement (post-7/98 enhanced service vs. pre-7/98 non-enhanced service). These dates are also needed to ensure that the member will not be granted duplicate service credit such as military service or purchased service.

43

Transfer of Service Q&A’sTransfer of Service Q&A’s

Common Questions – Transfer of ServiceCommon Questions – Transfer of Service

3)3) When can a member transfer retirement service credit from another When can a member transfer retirement service credit from another employer?employer?

If an employee participated in another Maryland retirement plan immediately prior to this new enrollment, service credit may be transferred from the previous system/plan if certain criteria are met. While the employee must initiate any transfer request, the new employer is in an important position to alert the employee of the transfer criteria.

The application to transfer is irrevocable, so you should advise your employee to contact one of our Retirement Benefits Specialists, so the employee can make an informed decision.

44

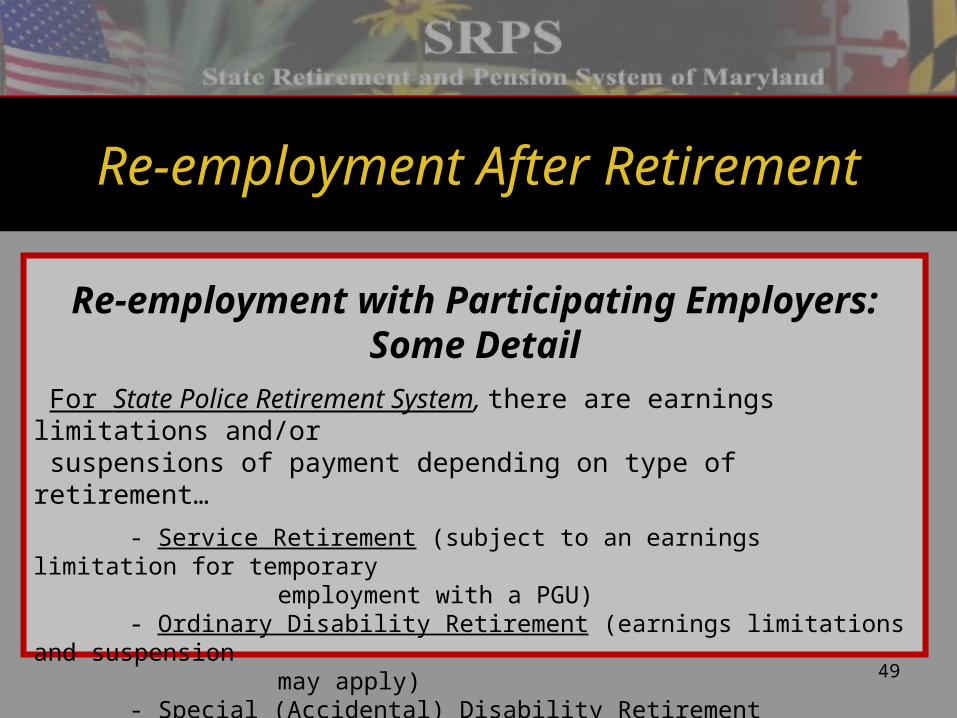

Re-employment After RetirementRe-employment After Retirement

TopicsTopics

- General Guidelines- Earnings Limitations Overview

- Some Detail for Different Pension and Retirement Systems

45

Re-employment After RetirementRe-employment After Retirement

IntroductionIntroductionIn general, retirees returning to work with a participating employer in SRPS may be subject to an earnings limitation and a reduction in monthly benefits.

Participating employers include: State agencies/colleges/ universities, public schools, libraries, participating counties, cities and towns.

46

Re-employment After RetirementRe-employment After Retirement

General GuidelinesGeneral Guidelines

Rules vary depending on the type of retirement (service or disability), retirement system and employer.

There must be a bona fide separation of employment.

MD Retirement Law requires a minimum of 45 day break between the member’s last day on payroll and the date rehired by the same employer.

47

Re-employment After RetirementRe-employment After Retirement

Earnings Limitation OverviewEarnings Limitation Overview An “earnings limitation” is the maximum annual income a SRPS retiree may earn through re-employment (after retiring), with the same participating employer without being subject to a reduction to the monthly retirement allowance.

Note: Significant IRS-related tax penalties can apply.

48

Re-employment After RetirementRe-employment After Retirement

Re-employment with Participating Employers:Re-employment with Participating Employers:Some DetailSome Detail

For Employees’ and Teachers’ Retirement & Pension Systems, Correctional Officers’ Retirement System and Local Fire & Police Pension Systems, there are earnings limitations and/or suspension of pension payment depending on type of retirement: - Service Retirement (earnings limitations apply)

- Early Service Retirement (earnings limitations apply)- Ordinary Disability Retirement (earnings limitations & suspensions apply)- Accidental Disability Retirement (suspensions apply)

Exceptions: If Annual Final Compensation is less than $10K; if retired more than nine calendar years.

49

Re-employment After RetirementRe-employment After Retirement

Re-employment with Participating Employers:Re-employment with Participating Employers:Some DetailSome Detail

For State Police Retirement System, there are earnings limitations and/or suspensions of payment depending on type of retirement…

- Service Retirement (subject to an earnings limitation for temporary employment with a PGU)

- Ordinary Disability Retirement (earnings limitations and suspension may apply)

- Special (Accidental) Disability Retirement (suspensions may apply)

50

Re-employment After RetirementRe-employment After Retirement

Re-employment with Participating Employers:Re-employment with Participating Employers:Some DetailSome Detail

For Law Enforcement Officers’ Pension System, there are earnings limitations and/or suspension of payment depending on type of retirement…

- Service Retirement (earnings limitations do not apply)- Ordinary Disability Retirement (earnings limitations and suspension could apply)- Special (Accidental) Disability Retirement (suspensions may apply)

51

Re-employment After RetirementRe-employment After Retirement

Re-employment with Participating Employers:Re-employment with Participating Employers:Some DetailSome Detail

For Judges’ Retirement System, there are earnings limitations and or suspension of payment depending on type of retirement… - Service Retirement (earnings limitations may apply) Exceptions

• Employed as a faculty member with a community college or public institution of higher learning.•Temporary Assignments to sit in a Court of the State.

52

Re-employment After RetirementRe-employment After Retirement

Re-employment with Participating Employers:Re-employment with Participating Employers:Some DetailSome Detail

For Legislative Pension System, earnings limitations do not apply.

53

Re-employment After Retirement FAQsRe-employment After Retirement FAQs

Common Questions – Re-employment After RetirementCommon Questions – Re-employment After Retirement

1)1) How does the Agency determine if someone has exceeded their How does the Agency determine if someone has exceeded their earnings limitation?earnings limitation?

Each year SRA requests a file containing the earnings of all employees from each employer. SRA compares the employees listed on this file against the retirees listed in our records. When we find a match we compare the wages for those people with their current employer against their earnings limitation that was calculated when they retired. Those people who have exceeded their earnings limitation are contacted by the SRA to arrange for repayment of their excess earnings.

54

WithdrawalsWithdrawals

TopicsTopics

- Termination of Membership - Vesting - Withdrawal Process - Tax Consequences

55

WithdrawalsWithdrawals

Membership terminates if the member…Membership terminates if the member…

- Is separated from employment for a certain period of time (depending on the system) - Terminates employment and withdraws accumulated contributions - Retires - Dies

56

WithdrawalsWithdrawals

Termination of MembershipTermination of Membership

Members who terminate state or municipal employment, may withdraw the balance of their contributions and end

their membership in the system.

By withdrawing their accumulated contributions, they forfeit all rights to a possible future benefit.

57

WithdrawalsWithdrawals

Vested MembersVested Members-Vesting is the accrued right to a retirement benefit, (based

upon the plan of membership) at a later date.

-Generally vesting requires five years of eligibility service.

- Vested members contributions continue to earn interest up to date of payment.

-Non-vested members who leave the balance of their contributions in the SRPS will continue to earn interest at 4% or 5% per annum on their balances until their membership period ends. At that time, no additional interest will be added.

58

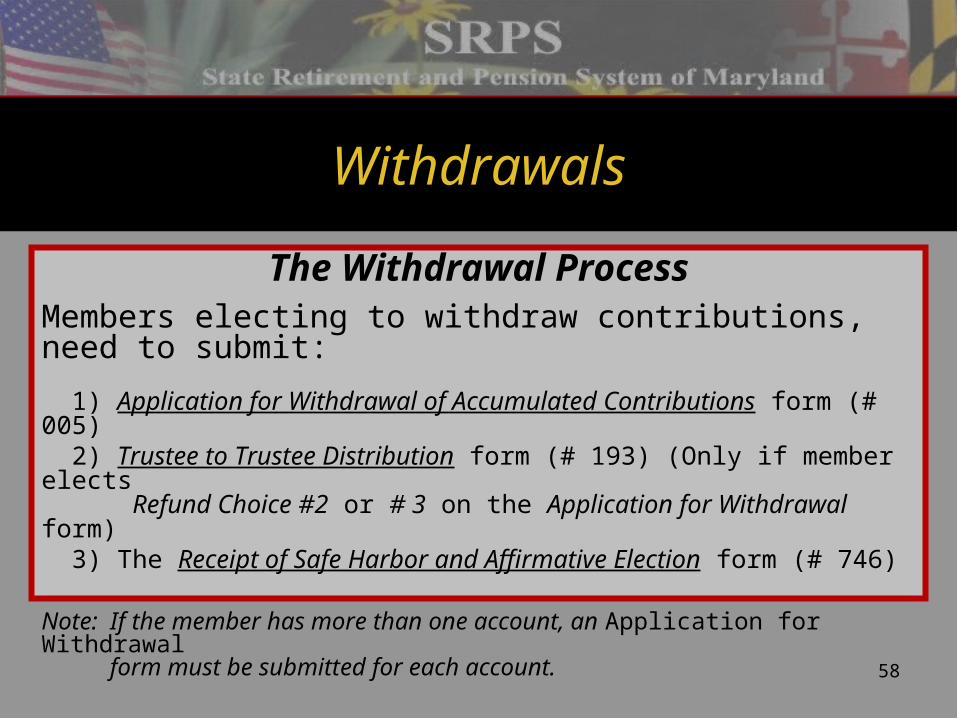

WithdrawalsWithdrawals

The Withdrawal ProcessThe Withdrawal ProcessMembers electing to withdraw contributions, need to submit:

1) Application for Withdrawal of Accumulated Contributions form (# 005) 2) Trustee to Trustee Distribution form (# 193) (Only if member elects Refund Choice #2 or # 3 on the Application for Withdrawal form) 3) The Receipt of Safe Harbor and Affirmative Election form (# 746)

Note: If the member has more than one account, an Application for Withdrawal form must be submitted for each account.

59

WithdrawalsWithdrawals

The Withdrawal ProcessThe Withdrawal Process

- Processing deadline is the 10th of the month.

- Checks will be dated and mailed on the last banking day of the month.

- No refunds may be processed in July.

- All applications received after June 10th will have a check date of Aug. 31st.

60

WithdrawalsWithdrawals

Tax ConsequencesTax Consequences

Before anyone withdraws contributions from SRPS, they should consult a tax advisor. Under some circumstances,

there could be costly mandatory tax consequences. - - - - - - - - - -

Members who receive a payment from SRA, will be mailed an IRS tax form 1099-R by January 31 of the year following the withdrawal for tax reporting

of the distribution.

61

Withdrawals Q&A’sWithdrawals Q&A’s

Common Questions – WithdrawalsCommon Questions – Withdrawals1)1) Who can withdraw their contributions and interest?Who can withdraw their contributions and interest?

Only employees who are terminating employment and membership. SRPS does not allow partial withdrawals or loans against contributions and interest.

2)2) When must the Retirement Coordinator complete the Coordinator When must the Retirement Coordinator complete the Coordinator section on the Form 5?section on the Form 5?

The Retirement Coordinator must complete the Coordinator section by clearly noting the date of termination/resignation date of the applicant if the date is within three months of the date of application for the refund.

62

Workers’ Compensation OffsetsWorkers’ Compensation Offsets

TopicsTopics

- Offset Provisions- Administration of Offsets

63

Workers’ Compensation OffsetsWorkers’ Compensation Offsets

OffsetsOffsets Law requires that SRPS reduce accidental or special disability retirement benefits by Workers’ Compensation benefits paid or payable after the date of retirement for the same accident.

This offset applies to retirees who were State employees. It also applies to retirees who were teachers and members of the Teachers’ Retirement or Pension Systems.

64

Workers’ Compensation OffsetsWorkers’ Compensation Offsets

Offset ProvisionsOffset Provisions

SRPS does not offset the portion of an accidental or special disability benefit attributable to employee contributions…only to the employer funded portion.

SRPS must leave sufficient payment to cover the cost of health insurance premiums and may not offset for

Workers’ Compensation benefits that are reimbursements for various fees paid to third parties.

65

Workers’ Compensation OffsetsWorkers’ Compensation Offsets

Administration of OffsetsAdministration of Offsets To prevent any overlap of Workers’ Compensation benefits and retirement benefits paid, SRPS will review each accidental or special disability allowance prior to payment of any retroactive pension benefit payment.

If an offset is required, SRPS will offset any retroactive benefits to the extent allowed by law.

If the retroactive benefits are not sufficient to satisfy the offset, SRPS will initiate a monthly recovery in accordance with the Board of Trustees’ policy.

66

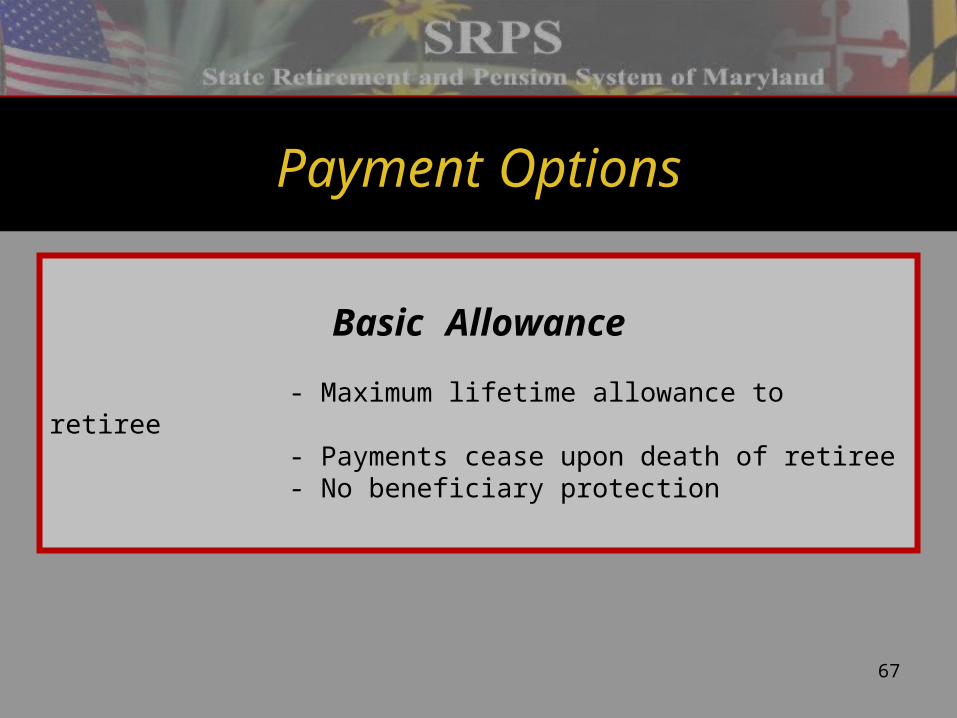

PaymentPayment OptionsOptions

TopicsTopics

- Basic Allowance - Single-life Annuities - Dual-life Annuities - Beneficiary Limitations - Option Selection Changes

67

PaymentPayment OptionsOptions

BasicBasic AllowanceAllowance - Maximum lifetime allowance to retiree - Payments cease upon death of retiree - No beneficiary protection

68

PaymentPayment OptionsOptions

Single-lifeSingle-life AnnuitiesAnnuities

- Pay benefits over retiree’s lifetime- Upon death of retiree, reserves, if any, are distributed as a lump sum to one or more designated beneficiary(ies). (Beneficiary can be changed at anytime during retirement.)- No recalculation of benefits

69

Payment OptionsPayment Options

Single-life Annuity OptionsSingle-life Annuity Options Option 1 Full Return of Present Value of Retiree’s Basic Allowance - Lower monthly benefit than Basic Allowance.

- Guarantees monthly payments that equal the total of the retirement benefit’s present value, if any, remaining at time of retiree’s death.

Option 4 Full Return of Employee Accumulated Contributions - Provides lower monthly benefit than Basic Allowance - Guarantees the return of the remaining balance in accumulated contributions and interest as established at time of retirement, if any balance remains at the time of the retiree’s death.

70

Payment OptionsPayment Options

Dual-life AnnuitiesDual-life Annuities

Four options pay benefits over two lifetimes (retiree’s and sole surviving beneficiary’s lifetimes).

- Benefit amount based on retiree’s age and age of beneficiary at time of member’s retirement. - Only one beneficiary can be designated.- Beneficiary can be changed (but causes a recalculation of retiree’s benefit based on current ages).

71

Payment OptionsPayment Options

Dual-life Annuity OptionsDual-life Annuity Options

Option 2 100% Survivor’s Benefit

- Lower monthly benefit than Basic Allowance- Guarantees same benefit to survivor after retiree’s death - Benefit ends after death of retiree and beneficiary

72

Payment OptionsPayment Options

Dual-life Annuity OptionsDual-life Annuity Options

Option 3 50% Survivor’s Benefit

- Lower monthly benefit than Basic Allowance

- Guarantees 50% of the benefit to survivor after retiree’s death

- Benefit ends after death of retiree and beneficiary

73

Payment OptionsPayment Options

Dual-life Annuity OptionsDual-life Annuity Options Option 5 100% Survivor’s Benefit with “Pop-Up” Provision

- Lower monthly benefit than Basic Allowance - Guarantees same benefit to survivor for life after retiree’s death - Guarantees that the monthly benefit will “pop-up” to the Basic Allowance for the retiree if the beneficiary predeceases the retiree. - If the original beneficiary predeceases the retiree and the retiree is collecting the Basic Allowance amount and names a new beneficiary, the benefit will be recalculated based on the new beneficiary’s designation and current age.

74

Payment OptionsPayment Options

Dual-life Annuity OptionsDual-life Annuity Options

Option 6 50% Survivor’s Benefit with “Pop-Up” Provision

- Lower monthly benefit than Basic Allowance - Guarantees 50% of the benefit to survivor for life after retiree’s death - Guarantees that the monthly benefit will “pop-up” to the Basic Allowance for the retiree if the beneficiary predeceases the retiree. - If the original beneficiary predeceases the retiree and the retiree is collecting the Basic Allowance amount and names a new beneficiary, the benefit will be recalculated based on the new beneficiary’s designation and

current age.

75

Payment OptionsPayment Options

Special Limitation of Beneficiary SelectionSpecial Limitation of Beneficiary Selection

Beginning 1/1/06, pension law prohibits certain beneficiary designations for these options:

- 100% Survivor’s Benefit (Option 2) - 100% Survivor Benefit with “Pop-Up” Provision (Option 5)

Retirees who select either of these two options cannot name a beneficiary who is 10 or more years younger than the retiree unless the beneficiary is a spouse or disabled child (as certified by physician).

76

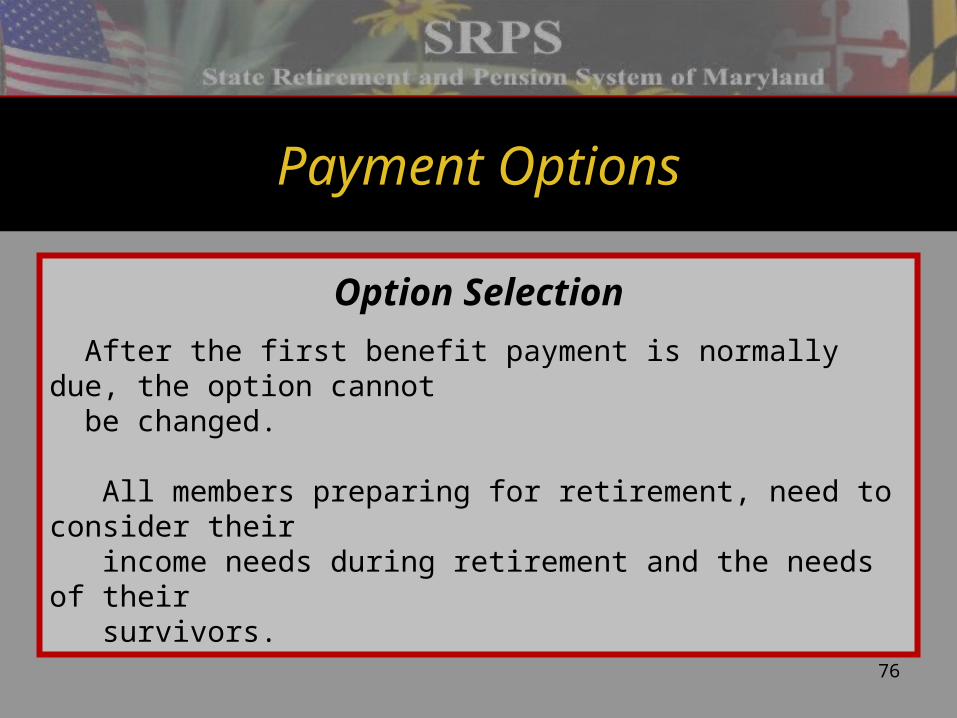

Payment OptionsPayment Options

Option SelectionOption Selection

After the first benefit payment is normally due, the option cannot be changed. All members preparing for retirement, need to consider their income needs during retirement and the needs of their survivors.

77

Payment Options Q&A’sPayment Options Q&A’s

Common Questions – Payment OptionsCommon Questions – Payment Options

1)1) Will the retiree’s beneficiary receive health insurance?Will the retiree’s beneficiary receive health insurance?

For state employees who retire and select option 2,3,5 or 6 and named their spouse as beneficiary, upon the retiree’s death, their spouse will receive a continuing monthly benefit and may elect to receive health insurance..

2) What does the beneficiary receive if the retiree selects the basic 2) What does the beneficiary receive if the retiree selects the basic allowance?allowance?

The basic allowance does not provide any beneficiary protection. If the retiree dies after the 15 th of the month the beneficiary or beneficiaries will receive the payment due to the retiree for that month. If the retiree dies on the 15th of the month or before the beneficiary or beneficiaries will not receive a payment from the SRA.

78

Payment Options Q&A’sPayment Options Q&A’s

Common Questions – Payment OptionsCommon Questions – Payment Options

3)3) Can a beneficiary be changed anytime during retirement?Can a beneficiary be changed anytime during retirement?

Yes. For retiree’s who selected the basic allowance or retirement options 1 or 4, a new beneficiary or beneficiaries can be designated at any time by submitting a notarized Form 4. There is no effect on the retiree’s monthly benefit.

For retirement options 2,3,5 or 6, a Form 66 and Form 67 must be completed to designate a new beneficiary with a proof of birth document for the new beneficiary. The retiree’s monthly benefit will be recalculated using the new beneficiary’s information.

79

SRPS ResourcesSRPS Resources

Web siteWeb site (http://www.sra.state.md.us/)

Information for Members, Employers, Retirees; Forms/Documents, Contact Information, FAQ’s, etc.

- - - -

Member CounselorsMember CounselorsBenefits/Account Information through

Retirement Counseling, Telephone Response and Correspondence Units- - - -

Published HandbooksPublished Handbooks

80

SRPS ResourcesSRPS Resources

Additional ResourcesAdditional ResourcesPersonal Statement of BenefitPersonal Statement of Benefit

(PSB—history and projections for active members)- - - -

Web Page for EmployersWeb Page for Employers (http://www.sra.state.md.us/employer.html)

Information on Employer Contribution Rates, Forms, FAQ’s.View and print Comprehensive Annual Financial Reports and individual

system benefit Handbooks

See Manual for more resources, contact information and plan detail.

81

ConclusionConclusion

Thank you!Thank you!

![Learning Dynamical Systems Requires Rethinking Generalization · 2020. 11. 16. · FitzHugh–Nagumo (FHN) [FitzHugh, 1961] and, independently, [Nagumo et al., 1962] derived the equations](https://static.fdocuments.in/doc/165x107/60d38b7ec48d57609971fbdd/learning-dynamical-systems-requires-rethinking-generalization-2020-11-16-fitzhughanagumo.jpg)

![Robustness of chimera statesfor coupled FitzHugh …arXiv:1411.5481v1 [nlin.AO] 20 Nov 2014 Robustness of chimera statesfor coupled FitzHugh-Nagumo oscillators Iryna Omelchenko,1,∗](https://static.fdocuments.in/doc/165x107/5e48bee18e88e43e47086681/robustness-of-chimera-statesfor-coupled-fitzhugh-arxiv14115481v1-nlinao-20.jpg)