1 Wealth Preservation Planning for Clients and their Families March 2009.

26

1 Wealth Preservation Wealth Preservation Planning for Planning for Clients Clients and their and their Families Families March 2009 March 2009

-

date post

21-Dec-2015 -

Category

Documents

-

view

221 -

download

0

Transcript of 1 Wealth Preservation Planning for Clients and their Families March 2009.

1

Wealth Preservation Wealth Preservation Planning for Clients Planning for Clients and their Families and their Families

March 2009March 2009

2

By: John P. DedonOdin, Feldman & Pittleman, P.C.9302 Lee Highway, Suite 1100

Fairfax, Virginia 22031(703) 218-2131

3

Personal Asset Personal Asset AccumulationAccumulation

WagesQualified PlansInvestment

Income

Inheritance

4

5

Proper Planning Will Allow You to . Proper Planning Will Allow You to . . .. .

Give what you have,Give what you have,To whom you want,To whom you want,

When you want, andWhen you want, andIn the way you wantIn the way you want

And Pay Less for:And Pay Less for: Court CostsCourt Costs

Attorney’s fees Attorney’s fees Estate TaxesEstate Taxes

6

We want to give our children enough . . .

but we don’t want them to blow it!

7

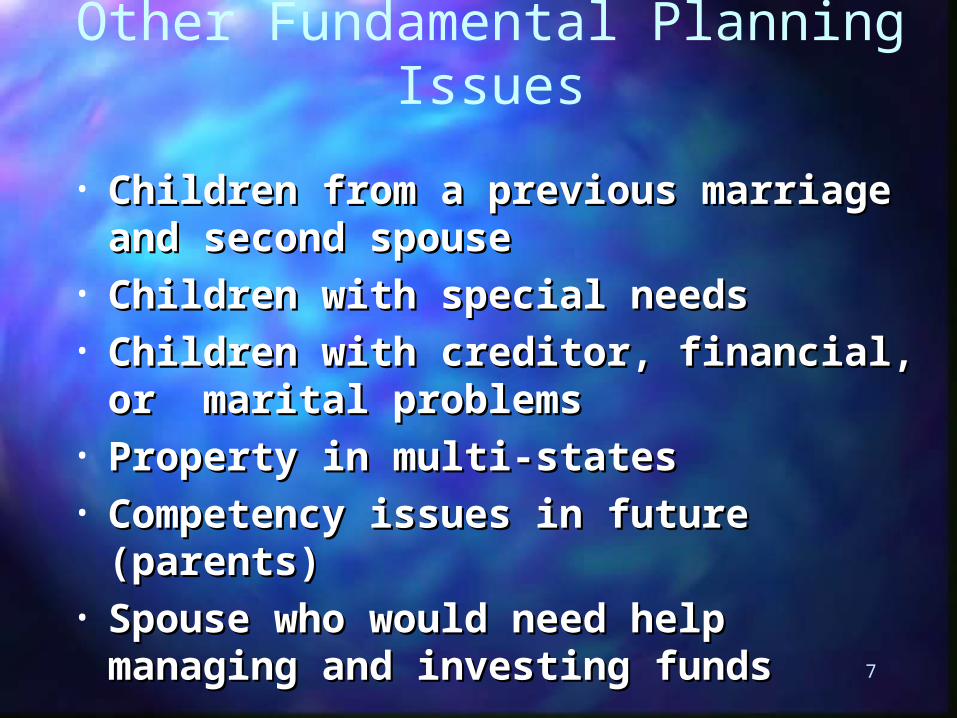

Other Fundamental Planning Issues

• Children from a previous marriage and Children from a previous marriage and second spousesecond spouse

• Children with special needsChildren with special needs• Children with creditor, financial, or Children with creditor, financial, or

marital problemsmarital problems• Property in multi-statesProperty in multi-states• Competency issues in future (parents)Competency issues in future (parents)• Spouse who would need help managing Spouse who would need help managing

and investing fundsand investing funds

8

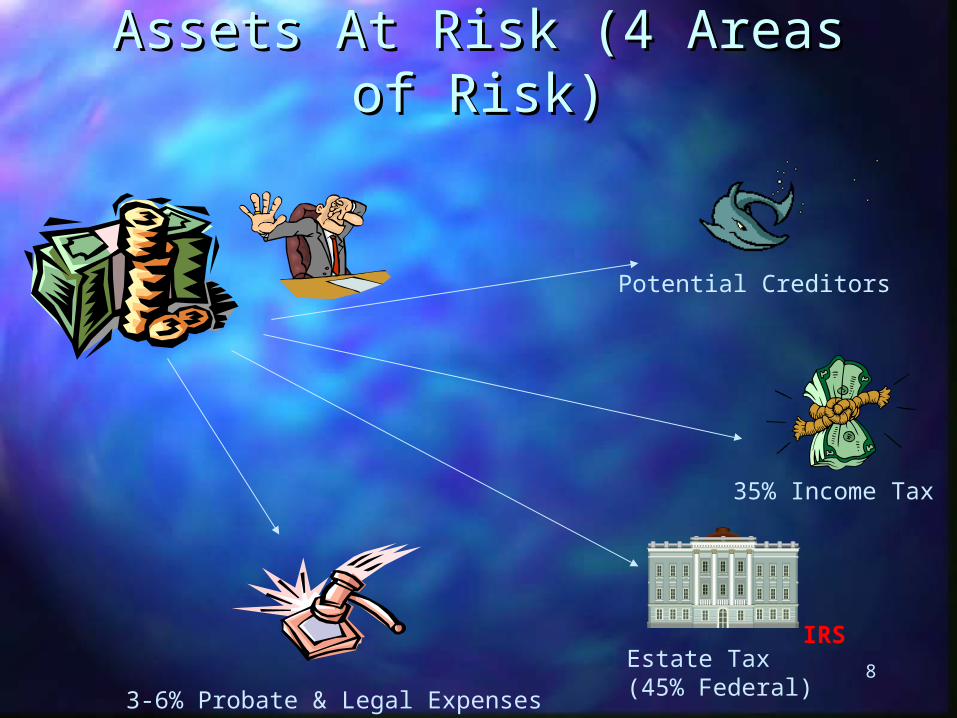

Assets At Risk (4 Areas of Assets At Risk (4 Areas of Risk)Risk)

Potential Creditors

3-6% Probate & Legal Expenses

Estate Tax(45% Federal)

35% Income Tax

IRS

9

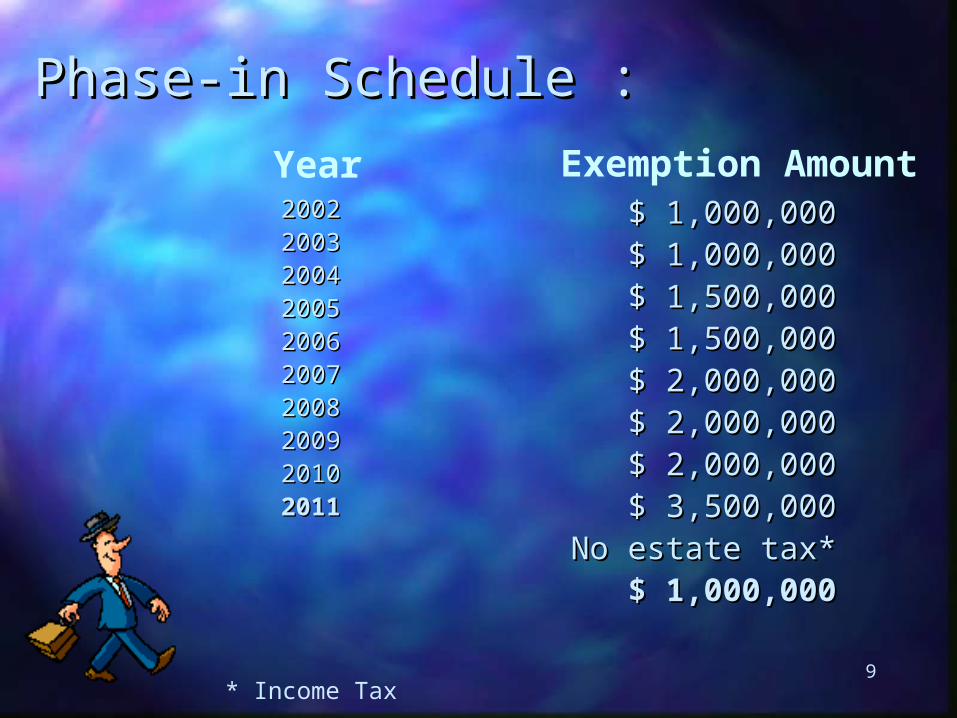

Phase-in SchedulePhase-in Schedule : :

20022002200320032004200420052005200620062007200720082008200920092010201020112011

$ 1,000,000$ 1,000,000$ 1,000,000$ 1,000,000$ 1,500,000$ 1,500,000$ 1,500,000$ 1,500,000$ 2,000,000$ 2,000,000$ 2,000,000$ 2,000,000$ 2,000,000$ 2,000,000$ 3,500,000$ 3,500,000

No estate tax*No estate tax*$ 1,000,000$ 1,000,000

Exemption AmountYear

* Income Tax

10

50%

50%

11

MONTH9

IRS

12

Death is Inevitable . . .

You have the option to plan your estate and avoid Death Taxes

Estate Tax is Not!IRS

13

Current Lifetime Gifting Current Lifetime Gifting RatesRates

$ 13,000 Annual $ 13,000 Annual ExclusionExclusion

$1,000,000 : Life Time Gift$1,000,000 : Life Time Gift

14

Probate Assets Pass Probate Assets Pass According to Will or According to Will or

Intestacy LawsIntestacy Laws

• Assets Passing Without a Will• Assets Passing With a Will

15

ProbateProbate

CostTime DelaysPublicityProperty In Multiple

States

16

Benefits of Revocable Living TrustsBenefits of Revocable Living Trusts

I. Avoids Probatea. Costb. Time Delaysc. Publicityd. Problems with property in multiple states

II. Incapacity PlanningIII. Estate Tax Planning

a. Bypass and Marital Trustsb. GST Planning

RevocableTrust

17

BASIC PLANNINGBASIC PLANNING

WillsWills Revocable Living TrustsRevocable Living Trusts Advanced Medical Directives Advanced Medical Directives

(Living Wills)(Living Wills) Powers of AttorneyPowers of Attorney

18

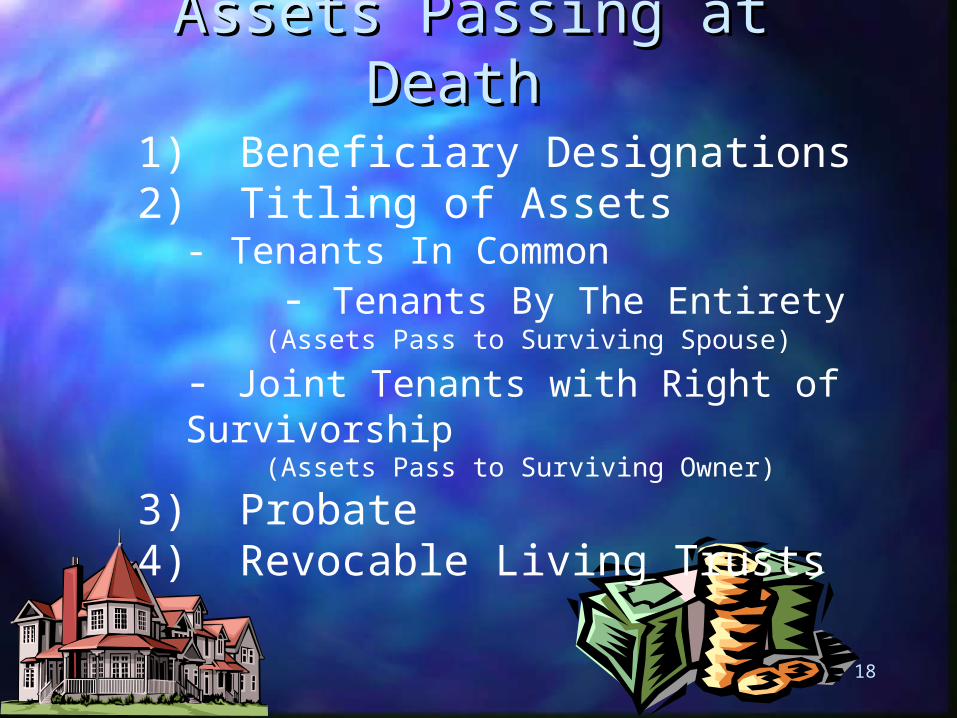

Assets Passing at Death Assets Passing at Death 1) Beneficiary Designations2) Titling of Assets

- Tenants In Common - Tenants By The Entirety

(Assets Pass to Surviving Spouse)

- Joint Tenants with Right of Survivorship (Assets Pass to Surviving Owner)

3) Probate4) Revocable Living Trusts

19

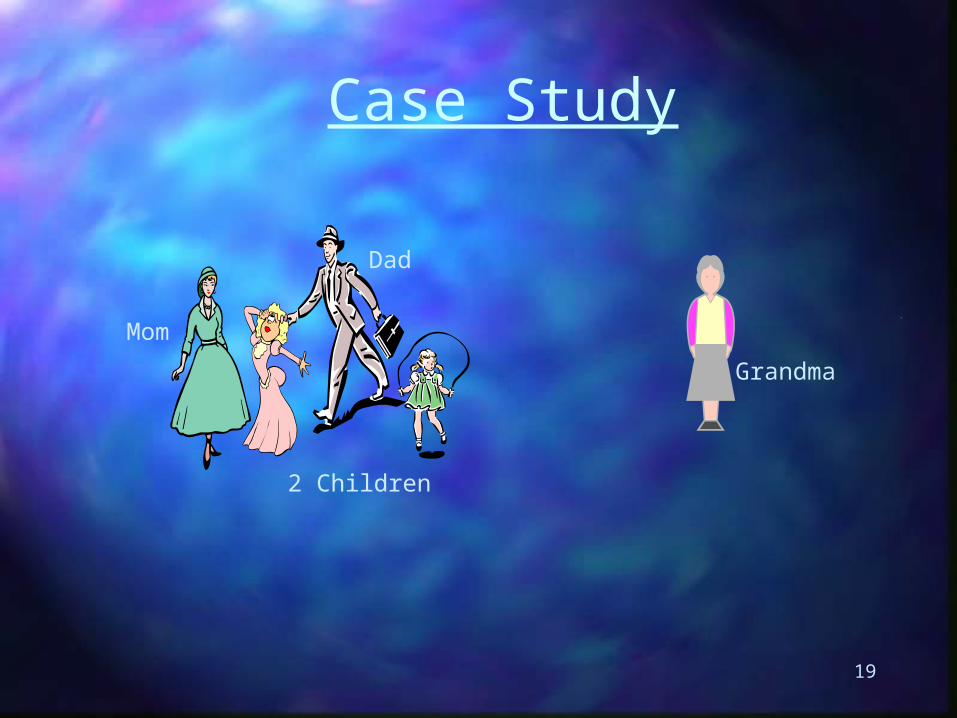

Case Study

Mom

Dad

2 Children

Grandma

20

ProfileProfile

• Married• $2 Million +• Equity in real estate, retirement

plans, other liquid assets, life insurance

21

Assets

$ 450,000 $100,000

$ 800,000

Retirement

$ 300,000

Liquid

Insurance

$ 900,000

$2,000,000 $250,000

Total $2,450,000 $350,000 $2,000,000

Grand Total = $4.8 million

22

Objectives

• Provide for surviving spouse• Eliminate or avoid estate tax• Eliminate probate• Provide for children at second

death• Provide for Mom

23

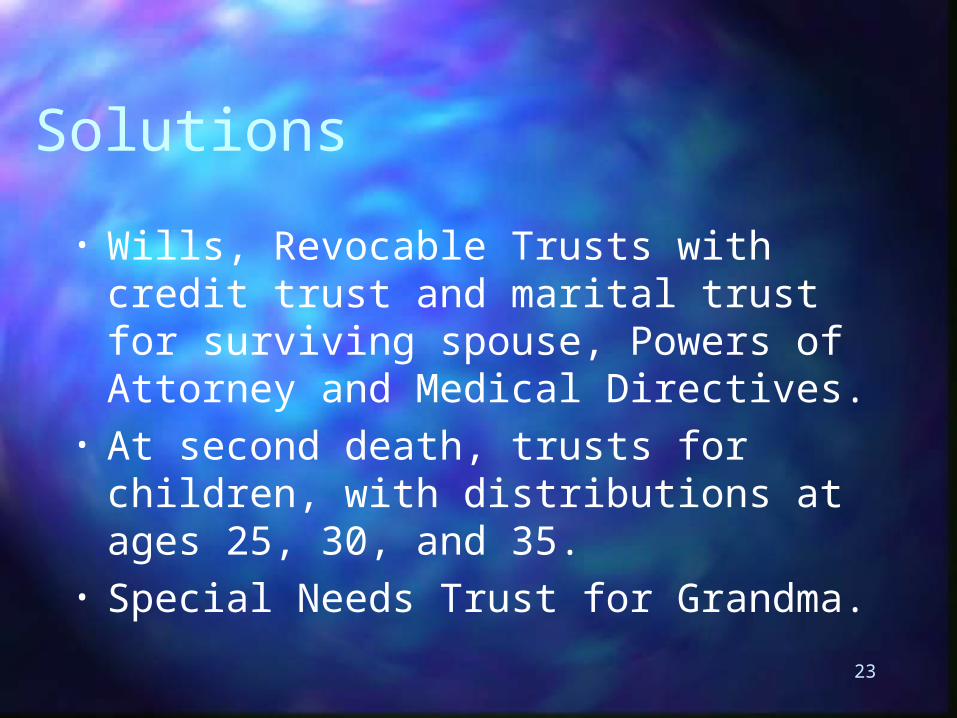

Solutions

• Wills, Revocable Trusts with credit trust and marital trust for surviving spouse, Powers of Attorney and Medical Directives.

• At second death, trusts for children, with distributions at ages 25, 30, and 35.

• Special Needs Trust for Grandma.

24

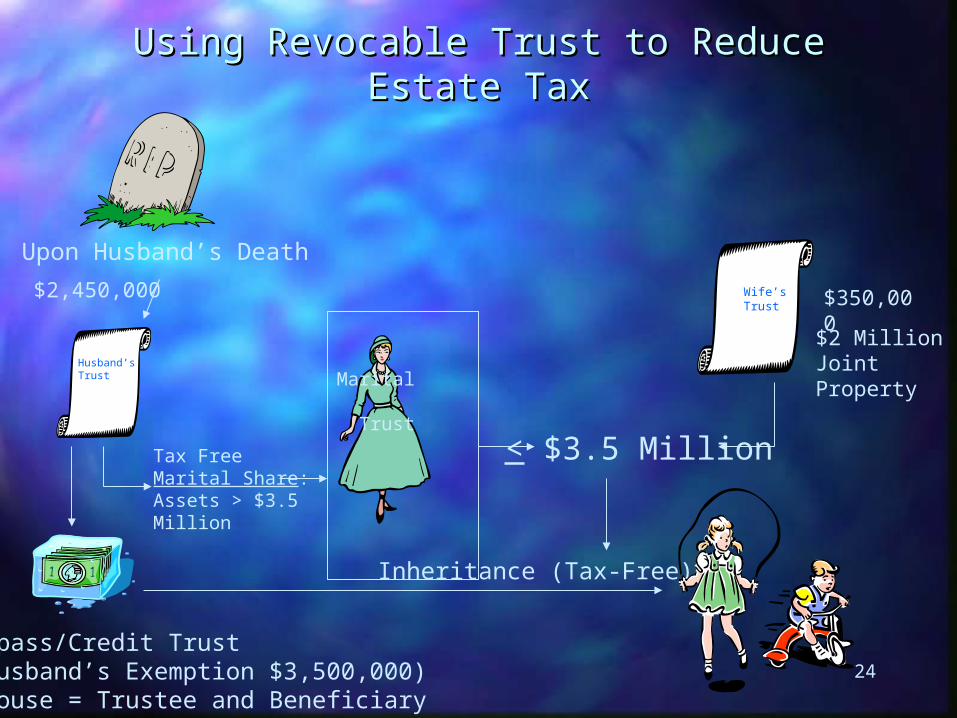

Using Revocable Trust to Reduce Estate Using Revocable Trust to Reduce Estate TaxTax

Upon Husband’s Death

Husband’sTrust

Bypass/Credit Trust(Husband’s Exemption $3,500,000)Spouse = Trustee and Beneficiary

Tax FreeMarital Share:Assets > $3.5 Million

< $3.5 Million

Inheritance (Tax-Free)

Marital Trust

$2,450,000 $350,000

$2 Million Joint Property

Wife’sTrust

25

Potential Titling Problems

• Wife dies first, only $350,000• Jointly held property• $1 million exemption amount in

2011?

26

Second DeathSecond Death

$3.5 Million $3.5 Million $$$

25 (1/3)30 (1/2)35 BalanceNeed Executor, Trustee, Guardian

Special Needs Trust