1 The Resource Rent and Taxation Lone Semmingsen, Tax Policy Department Norwegian Ministry of...

15

1 The Resource Rent and Taxation Lone Semmingsen, Tax Policy Department Norwegian Ministry of Finance 9 April 2010

-

Upload

finn-lockhart -

Category

Documents

-

view

214 -

download

0

Transcript of 1 The Resource Rent and Taxation Lone Semmingsen, Tax Policy Department Norwegian Ministry of...

1

The Resource Rent and Taxation

Lone Semmingsen, Tax Policy DepartmentNorwegian Ministry of Finance9 April 2010

Ministry of Finance

2

Taxing Natural Resources - Key Aspects

Extraordinary profits Immobile resources A good tax base!

• Profit based tax rules• Stability Predictability Simplicity Efficient tax administration

Ministry of Finance

3

Design of the Norwegian System

Super-profit: Potential for increased tax take

Extra allowance for ordinary returns Should not distort investment incentives

Ordinary income: • 28% on net income as in other industries • Neutrality between industries• Tax on ordinary returns and super-profit

Ministry of Finance

4

Petroleum Taxation

• Production from 1971• Resource rent tax

introduced 1975• Tax rate 50 %, total

marginal tax rate 78 %• profit based• CO2 tax and NOX tax

(negative external effects)

• Royalty phased out from 2000

Ministry of Finance

5

Total Government Take from the Petroleum Sector

-50

0

50

100

150

200

250

300

350

400

450

1971 1976 1981 1986 1991 1996 2001 2006

Billio

n N

OK

2010

Val

ue

0

20

40

60

80

100

120

USD

201

0 Va

lue

Taxes Environmental taxes SDFI Royalty and area fee StatoilHydro dividend Oil Price

Ministry of Finance

6

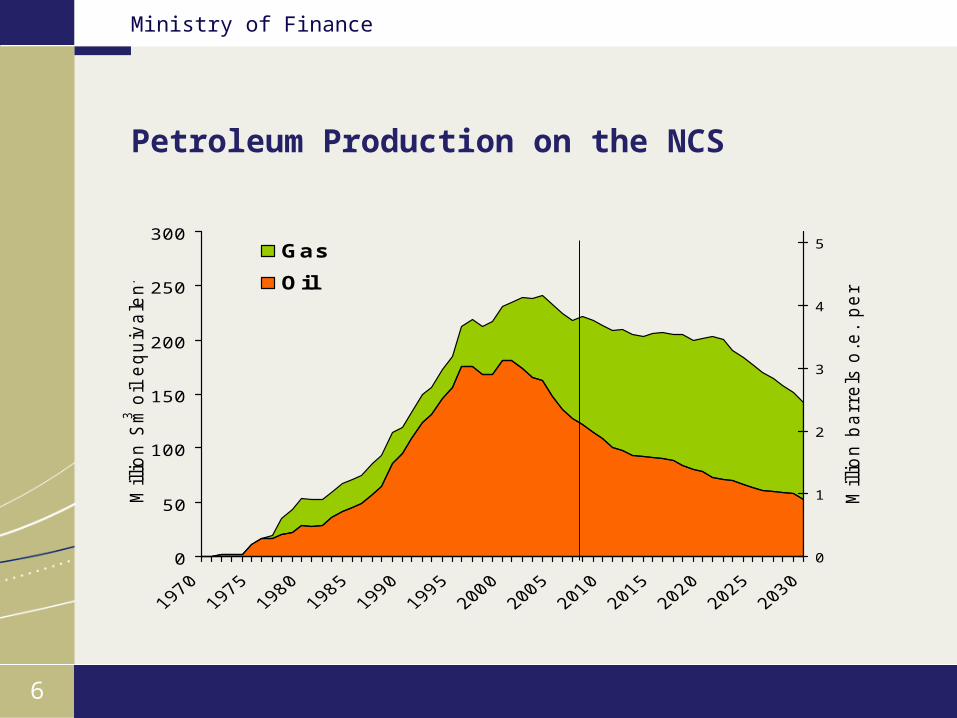

Petroleum Production on the NCS

0

50

100

150

200

250

300

Million S

m3 o

il e

quiv

ale

nts

0

1

2

3

4

5

Million b

arr

els

o.e

. per

dayGas

Oil

Ministry of Finance

7

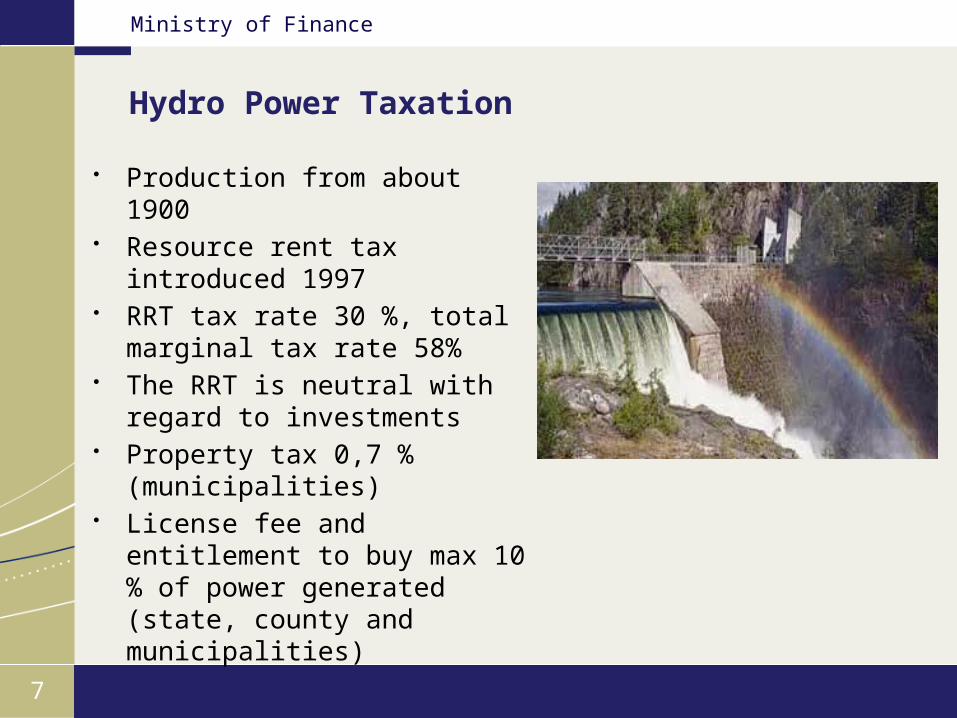

Hydro Power Taxation

• Production from about 1900• Resource rent tax introduced

1997• RRT tax rate 30 %, total

marginal tax rate 58%• The RRT is neutral with

regard to investments• Property tax 0,7 %

(municipalities)• License fee and entitlement

to buy max 10 % of power generated (state, county and municipalities)

Ministry of Finance

8

Hydro Power - Resource Rent Tax 1997-2008

0

1000

2000

3000

4000

5000

6000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

Mil

l. N

OK

Ministry of Finance

99

Norwegian Economic Structure 2009

Share of investments

Petroleum (27%)

Other

Share of exports

Petroleum (46%)

Other

Share of GDP

Petroleum (22%)

Other

Share of state revenues

Petroleum (28%)

Other

Ministry of Finance

10

State Direct Financial Interest (SDFI)• The SDFI is an arrangement where the state keeps an

interest in a number of oil and gas fields.• Each interest is decided when licenses are awarded, and

the size of state interest varies between fields.• The state pays its share of investments and costs and

receives a corresponding share of the gross income from the license.

• When Statoil was listed and partially privatised in 2001, the administration of the SDFI portfolio was transferred to a new state-owned trust company, Petoro.

• Petoro is funded over the state budget and does not receive any of the income from the SDFI.

Ministry of Finance

11

The Government Pension Fund – Global

0

500

1000

1500

2000

2500

300019

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

09

Bill

ion N

OK

0 %

25 %

50 %

75 %

100 %

125 %

150 %

175 %

Per

cen

t of

GD

P M

ain

land

Capital 31. of dec. (left scale)

Per cent of mainland GDP (right scale)

Ministry of Finance

12

Tax basis - Petroleum on company basis – ring fenced against mainland

Companies without taxable income Carry forward with interest - (risk free + 0,5%)*(1-0,28) Tax refund (pay out) of exploration costs Final losses can be sold or tax reimbursed from the state

Sales income (norm prices)- Operating costs- Capital depreciation (16,7 pct. over 6 years)- Financial costs- (Deficits from previous years)= Ordinary tax base liable to 28 pct. tax- Uplift (investment based extra depreciation, 7,5 pct. 4 years) - (Excess uplift from previous years)= Tax base liable to 50 pct. tax

Ministry of Finance

13

Tax basis – Hydropower

Negative resource rent will be entitled to a tax refund (pay out)

Sales income (market prices)- Operating costs- Concession fees- Property tax- Depreciation (linear: installations 1,5% equipment 2,5%)- Uplift (tax values * risk free rate)= Tax base liable to 30 pct. tax

Ministry of Finance

14

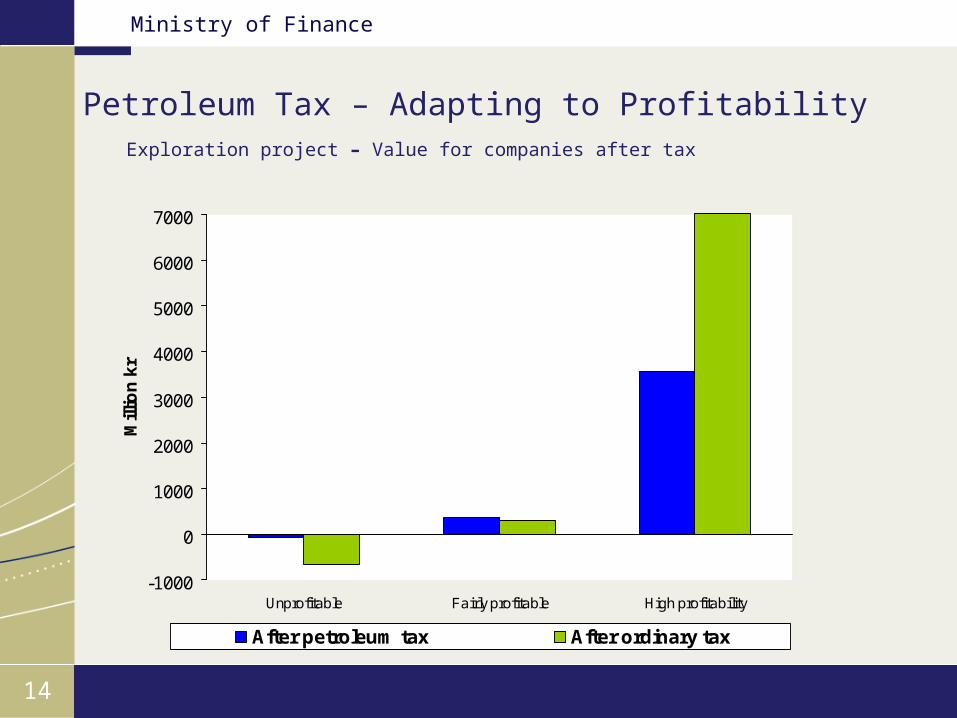

Petroleum Tax – Adapting to Profitability

-1000

0

1000

2000

3000

4000

5000

6000

7000

Unprofitable Fairly profitable High profitability

Mill

ion

kr

After petroleum tax After ordinary tax

Exploration project – Value for companies after tax

Ministry of Finance

15

Hydropower production

Revenues to local/regional government (2006)• Concessionary duties (2006) 640 mill. NOK• Concession power (2006) 2 600 mill. NOK• Property tax 0,7% (2006) 1 900 mill. NOK• Natural resource tax 1 600 mill. NOK• Local/regional ownership 45% of productionSource: Revidert nasjonalbudsjett 2008

State revenues (2008)• Ordinary tax 28% 5 000 mill. NOK• Resource rent tax 30% 5 623 mill. NOK• Tax deductions -2 809 mill. NOK• State ownership – Statkraft >40% of productionSource: SSB